Andrew Korybko approached me a few days ago asking if we could share some of his work. I don’t view the Automatic Earth as a publishing platform, and given all the censorship of the past 2-3 years (it’s expensive!), I will be very cautious about letting anyone in. But I like Andrew’s writing, so I said: let’s give it a go.

Then I had to transfer his Word file to the simple text editor I have been using for many years, but that only took half an hour … I don’t like Word. Or Bill Gates. Here’s Andrew:

Andrew Korybko: The “official narrative” surrounding the UkrainianConflict has flipped in recent weeks from prematurely celebrating Kiev’s supposedly “inevitable” victory to nowadays seriously warning about its likely loss. It was therefore expected in hindsight that other dimensions of the information warfare campaign waged by the US-led West’s GoldenBillion against Russia would also change. As proof of precisely that, the New York Times (NYT) just admitted that the West’s anti-Russian sanctions are a failure.

In Ana Swanson’s article about how “Russia Sidesteps Western Punishments, With Help From Friends”, she cites Western experts who concluded that “Russia’s imports may have already recovered to prewar levels, or will soon do so, depending on their models.” Even more compelling, she references the IMF’s latest assessment from Monday, which “now expected the Russian economy to grow 0.3 percent this year, a sharp improvement from its previous estimate of a 2.3 percent contraction.”

Neither the NYT, the Western experts that Swanson cites, nor the IMF can credibly be accused of being “Russian-friendly”, let alone so-called “Russian propagandists” or even “Russian agents”, which thus confirms the observation that this dimension of the Golden Billion’s infowar has also decisively shifted. The fact of the matter is that the West’s anti-Russian sanctions failed to catalyze the collapse of that targeted multipolar Great Power’s economy, which continues to remain impressively resilient.

The timing at which this narrative changed is also important because it extends credence to the more widely known new narrative that’s nowadays seriously warning about Kiev’s likely loss in NATO’s proxy war on Russia. After all, if the sanctions achieved the goal that they were supposed to and which the US-led West’s Mainstream Media (MSM) hitherto lied that they supposedly had, then it naturally follows that Kiev would “inevitably” win exactly as they claimed would happen up until mid-January.

With this in mind, the most effective way to “reprogram” the average Westerner after brainwashing them over the past 11 months into expecting Kiev’s supposedly “inevitable” victory is to also decisively change the supplementary narratives that artificially manufactured that aforesaid false conclusion. To that end, the order was given to begin raising the public’s awareness about the failure of the Golden Billion’s anti-Russian sanctions, ergo the NYT’s latest piece and the specific timing thereof.

What’s left unsaid in that article is the “politically incorrect” but nevertheless heavily implied observation that the jointly BRICS– & SCO-led GlobalSouth of which Russia is a part has defied the Golden Billion’s demands to “isolate” that multipolar Great Power. No MSM outlet will ever admit it, at least not yet, but their de facto New Cold War bloc has limited sway outside the US’ recently restored “sphere of influence” in Europe, whose countries are the only ones suffering from these sanctions.

The NYT’s latest piece might inadvertently make many members of their public conscious of that, however, and they might therefore increasingly object to their governments scalingup their commitment to NATO’s proxy war on Russia under American pressure. Croatian President Zoran Milanovic recently joined Hungarian Prime Minister Viktor Orban in condemning this campaign and raising wider awareness of just how counterproductive it’s been for Europe’s objective interests.

As Europeans come to realize that they’re the only ones suffering from the anti-Russian sanctions that their American overlord coerced them into imposing and that their sacrifices haven’t adversely affected that targeted multipolar Great Power’s special operation, massive unrest might follow. It’s unlikely to influence their US-controlled leaders into reversing course, remembering that the German Foreign Minister vowed late last year never to do so, but could instead catalyze a violent police crackdown.

The reason behind this pessimistic prediction is that a reversal or at the very least lessening of the presently rigid anti-Russian sanctions regime would represent an unprecedentedly independent move by whichever European state(s) does/do so. Seeing as how that didn’t even happen in the eight years prior to the US’ successful reassertion of its unipolar hegemony all across 2022, the likelihood of that happening nowadays under those much more difficult conditions is practically nil.

The US’ “Lead From Behind” subordinate for “managing” European affairs as part of its new so-called “burden-sharing” strategy, Germany, has more than enough levers of economic, institutional, and political influence to several punish any of those lower-tier American vassals who get out of place. It’s therefore unrealistic to expect any single EU member to unilaterally defy the bloc’s anti-Russian sanctions that their own government previously agreed to.

Considering this reality, those leaders who want to remain in power or at least not risk the US’ German-driven HybridWar wrath against their economies are loath restore a semblance of their largely lost sovereignty in such a dramatic manner. Instead, their most pragmatic course of action is to not participate in the military aspect of this proxy war by refusing to dispatch arms to Kiev exactly as the emerging Central European pragmatic bloc of Austria, Croatia, and Hungary have done.

The population of those countries are thus unlikely to protest against the sanctions even after being made aware of the facts contained in the NYT’s latest piece and naturally coming to the conclusion that the anti-Russian sanctions have only harmed their own economies and not that targeted Great Power’s. Folks in France, Germany, and Italy, however, could very well react differently, especially considering their tradition of organizing massive protests.

In such a scenario, their governments are expected to order a violent police crackdown under whatever pretext they concoct, whether it’s falsely accusing the protesters of employing violence first or accusing them all of being so-called “Russian agents”. Regardless of how it happens, the outcome will be the same whereby Western European countries will slide deeper into liberal-totalitarian dictatorship, which will in turn contribute to further radicalizing their population towards uncertain ends.

Returning back to the NYT’s piece, it represents a remarkable reversal of the “official narrative” by frankly admitting that the West’s anti-Russian sanctions are a failure. This coincides with the decisive shift of the larger narrative driven by American and Polish leaders over the past month whereby they’re nowadays seriously warning about Kiev’s likely loss in NATO’s proxy war on Russia. It remains to be seen what other narratives will change as well, but it’s predicted that more such ones will inevitably do so.

We try to run the Automatic Earth on donations. Since ad revenue has collapsed, you are now not just a reader, but an integral part of the process that builds this site. Thank you for your support.

Support the Automatic Earth in virustime. Click at the top of the sidebars to donate with Paypal and Patreon.

“There is no such thing as a heartbeat at six weeks. It is a manufactured sound designed to convince people that men have the right to take control of a woman’s body.”

.@MattWalshBlog talks to @TuckerCarlson about Vanderbilt's transgender clinic: "We know for a fact…that [at] Vanderbilt they perform double mastectomies on minor girls…They give [children] irreversible hormone drugs that change their bodies permanently." pic.twitter.com/rJ6usEHfB6

MIT climate scientist Dr. Richard Lindzen laughs at the sheer lunacy of declaring trace CO2 to be a pollutant: "What kind pollutant is it? You get rid of it and you die". pic.twitter.com/8meYfWPgeO

Navy Admiral Charles Richard, commander of US Strategic Command, declared on Wednesday that for the first time since the end of the Cold War, the US faces the possibility of nuclear war with a peer-level opponent. Speaking at an Air Force-organized conference in Maryland, Richard claimed that the US would have to prepare to escalate quickly against possible opponents, including to defend the United States itself. “All of us in this room are back in the business of contemplating…direct armed conflict with a nuclear-capable peer,” he said, according to a Pentagon summary of his comments. “We have not had to do that in over 30 years.”

“Russia and China can escalate to any level of violence that they choose in any domain with any instrument of power worldwide,” he continued. “We just haven’t faced competitors and opponents like that in a long time.” In the eyes of Moscow, the US is currently locked in a proxy conflict with Russia in Ukraine, and has steadily escalated its commitment of weapons, intelligence and financial assistance to Kiev since Russian troops entered Ukraine in February. Russia’s current nuclear doctrine allows for the use of nuclear weapons in the event of a first nuclear strike on its territory or infrastructure, or if the existence of the Russian state is threatened by either nuclear or conventional weapons. American doctrine allows for a nuclear first strike in “extreme circumstances to defend the vital interests of the United States or its allies and partners.”

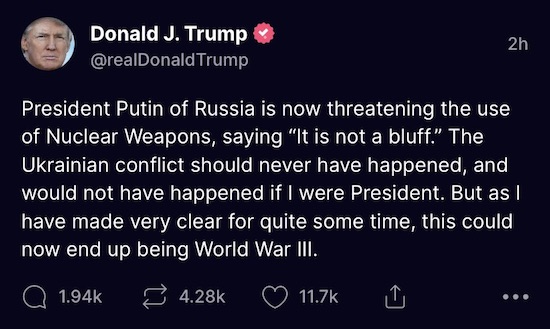

Russian President Vladimir Putin reiterated this position on Wednesday, declaring that the Kremlin would “without a doubt use all available means to protect Russia and our people,” should Russian territory be threatened. Russian Foreign Minister Sergey Lavrov also warned that the US was “teetering on the brink” of becoming a direct party in the Ukraine conflict, with Washington risking “a direct collision between nuclear powers.” Similar warnings have come from within the US too, most notably from former President Donald Trump, who declared on Wednesday that the conflict, which he said “should have never happened,” could “end up being World War III.”

The US could destroy Russia’s Crimea-based Black Sea Fleet or its bases on the peninsula if Moscow resorts to using nuclear weapons in Ukraine, the former commander of the US Army in Europe, Ben Hodges, has said. In an interview with the Daily Mail on Wednesday, Hodges described the possibility of Russian President Vladimir Putin ordering the deployment of nukes as “very unlikely.” Putin will not do so because “he knows the US will have to respond if Russia uses a nuclear weapon,” he claimed. “The US response may not be nuclear… but could very well be a devastating strike that could, for example, destroy the Black Sea Fleet or destroy Russian bases in Crimea,” Hodges, who was in charge of the US forces in Europe between 2014 and 2018, said.

“So, I think President Putin and those around him will be reluctant to draw the US into the conflict directly.” The comments were made in response to Putin’s address earlier that day, in which he said Russia is fighting “the entire Western military machine” in Ukraine, citing the lavish assistance in lethal aid and intelligence provided to Kiev by the US, UK, EU and others. “If the territorial integrity of our nation is threatened, we will certainly use all the means that we have to defend Russia and our people,”he warned. White House National Security Council spokesman John Kirby said the Biden administration took Putin’s words “seriously,”but insisted that it was “irresponsible rhetoric for a nuclear power to talk that way.”

The President of Serbia has warned that the planet is entering into a “great world conflict” that could take place within the next two months. Aleksandar Vucic made the alarming comments during the first day of the UN General Assembly session in New York. “You see a crisis in every part of the world,” Vucic told the Serbian state broadcaster RTS. “I think realistic predictions ought to be even darker,” he added. “Our position is even worse, since the UN has been weakened and the great powers have taken over and practically destroyed the UN order over the past several decades.” The Serbian leader cautioned that the war between Russia and Ukraine had moved on to a far deadlier phase.

“I assume that we’re leaving the phase of the special military operation and approaching a major armed conflict, and now the question becomes where is the line, and whether after a certain time – maybe a month or two, even – we will enter a great world conflict not seen since the Second World War,” he said. Vucic’s remarks were made on the same day that Russian President Vladimir Putin ordered an immediate “partial mobilization” of troops amounting to 300,000 soldiers. In a public address to the nation, Putin warned that he wasn’t bluffing and that he was prepared to use “all the means at our disposal” to protect Moscow’s territorial integrity. “Now they (the West) are talking about nuclear blackmail,” said Putin. “The Zaporizhzhia nuclear power plant was shelled and also some high positions – representatives of NATO states – who are saying there might be possibility and permissibility to use nuclear weapons against Russia,” he added.

Putin ominously asserted that western powers should “be reminded that our country also has various weapons of destruction, and with regard to certain components they’re even more modern than NATO ones.” As we highlighted last month, a study conducted by Rutgers University found that nuclear war between the United States and Russia would cause two-thirds of the planet to starve to death within two years. 5 billion people would perish, primarily as a result of nuclear detonations causing huge infernos that inject soot into the atmosphere which blocks out the sun and devastates crops. One wonders how a generation that thinks words are “violence” and misgendering someone is stochastic terrorism will react to an intercontinental nuclear war. The mind truly boggles.

Moscow may use nuclear weapons to defend its territory, including the Donbass republics and Zaporozhye and Kherson Regions, should they decide to join Russia, former president, Dmitry Medvedev said on Thursday. He also warned that “retired idiots” in the Western military should not contemplate strikes on Moscow’s naval bases in the Black Sea. Writing on Telegram on Thursday, Medvedev stressed that the referendums, planned for between September 23 and 27, would definitely take place, and “the Donbass republics and other territories would be admitted to Russia.” The former president went on to say that the Russian military would “significantly reinforce” the defenses of all incorporated territories.

He added that to defend its territories, Russia may use “not only its mobilization capabilities, but also any Russian weapons, including strategic nuclear weapons.” Without naming names, Medvedev cautioned that “retired idiots with generals’ stripes” should not attempt to intimidate Moscow by claiming that NATO could attack Crimea, a peninsula that overwhelmingly voted to unite with Russia in 2014 following a coup in Kiev. “Hypersonic [missiles] are sure to hit targets in Europe and the US much faster,” he warned, adding that “the Western establishment and NATO citizens need to understand that Russia has chosen its own path” and there is “no way back.”

On Wednesday, Ben Hodges, the former commander of the US Army in Europe, said that Washington could destroy Russia’s Black Sea Fleet, that’s based in Crimea, or its bases on the peninsula if Moscow resorts to using nuclear weapons in Ukraine. He noted that it’s “very unlikely” that Russian President Vladimir Putin would order to deploy nukes. Last week, Medvedev accused Western “half-wits” from “stupid think tanks” of leading their countries down the road of nuclear Armageddon with their hybrid war against Moscow. He also warned that the “unrestrained pumping of the Kiev regime with the most dangerous types of weapons,” could prompt Russia to move its military campaign to the next level.

European Commission chief Ursula von der Leyen has, as could be expected, called for new sanctions against Russia in connection with the forthcomingreferendums in Donbass and two regions of Ukraine. These concern the Donetsk and Lugansk People’s Republics – which have been de-facto self-governing since 2014 – and the Kherson and Zaporozhye regions. In her opinion, the penalties already imposed on Russia are having an impact.”The sanctions have been very successful. If you look at the Russian economy, its industry is in tatters,” the politician asserted. Let’s allow ourselves to argue a little with Ms. von der Leyen. The key measure of the effectiveness of sanctions is whether they change the political course of the target country.

This criterion has been well researched in both academic and applied literature and few people have any doubts about its veracity. However, Russia has not changed its political course in Ukraine under the influence of the large-scale sanctions of the EU, US and other initiators. Moreover, its position is hardening, as evidenced by this week’s announcements of both a partial mobilization and the referendums. Thus, we can say that the measures are actually having a negative effect in terms of what they are supposed to be doing. Apparently, Ms. von der Leyen links effectiveness to the amount of pain inflicted. In other words, she believes that the greater it is, the better. There are problems here, too. The damage is indeed large. But we are not just sitting still and feeling sorry for ourselves. We are adapting very energetically.

Now, you can criticize Russia’s domestic financial policy and question import substitution as much as you like. And they will not, of course, make ‘everything as it was.’ But it is clear that the economy is shrinking much less than expected, that inflation has, at least so far, been brought under control, and that adaptations in sourcing, helped by domestic production, are mitigating the effects of the sanctions. The economy is simply becoming different. It is changing in terms of focus and quality. In a number of sectors it will “run slower” or limp along. But Russiawill continue to live. Of course, we have already heard the words “the Russian economy is in tatters,” from US President Barack Obama. That was in 2015. Seven years ago.

The EU has agreed to slap new sanctions on Russia “as soon as possible” over plans to hold referendums in the Donbass republics and Russian-controlled regions in Ukraine on whether to unite with Russia, the bloc’s foreign policy chief said on Wednesday. Speaking after an emergency meeting of EU foreign ministers, Josep Borrell said that the bloc had made a “political” decision to impose new sectoral and individual sanctions on Russia. “These restrictive measures would be brought forward as soon as possible against Russia in coordination with partners,” he said. While he did not clarify the details of the new sanctions, he hinted that they would hit the Russian economy, especially the technology sector, while the EU would also blacklist a number of individuals.

He also noted that the bloc would provide Ukraine with security assistance for “as long as it takes.” “Today it’s clear that we will continue to increase our military support and continue to provide arms to Ukraine,” he added. Borrell also commented on recent developments in the Ukraine conflict, accusing Russian President Vladimir Putin of “trying to destroy Ukraine” and organizing partial mobilization to support what he called “illegal referenda.” On Wednesday, Vladimir Putin announced a partial mobilization which calls on 300,000 reservists to take part in the conflict with Ukraine. The move comes a day after the two Donbass republics and Russian-controlled Zaporozhye and Kherson Regions decided to hold referendums from September 23 to 27, on whether to unite with Russia.

The EU leadership caused a continent-wide crisis by imposing sanctions on Russian energy, Hungarian Prime Minister Viktor Orban has said. The Eurosceptic politician criticized Brussels on his Facebook page on Wednesday evening as he announced a meeting with members of the ruling coalition in the parliament. According to local media, during the closed-door gathering, he blamed EU bureaucrats for the hardships that member states, including Hungary, currently face. Orban told MPs from his Fidesz party and the allied Christian Democrats (KDNP) that if the EU’s sanctions on Russia were dropped, gas prices would go down by one-half, and as a result, inflation would also decline, Magyar Nemzet daily reported.

The Hungarian PM said the EU leadership promised in early summer that the sanctions would hurt Russia’s economy, not people in the EU, but the opposite has occurred, according to the report. Orban predicted that dropping the sanctions would allow the EU to avoid a recession. In November, there will be a meaningful opportunity for the EU to reconsider the restrictions on trading with Russia, Orban reportedly said, and the ruling Hungarian coalition should work hard to have them lifted by the end of the year. The prime minister also lashed out at the Hungarian opposition, accusing them of backing Brussels’ policies without giving a second thought to the damage they are causing to the country, Magyar Nemzet said.

He also outlined a number of measures, such as energy subsidies, which the Fidesz–KDNP government is taking to alleviate the effects of the skyrocketing prices, the newspaper reported. Orban, who was re-elected in a landslide victory in April, is an outspoken critic of the EU leadership. He has called the bloc the main loser in the Russia-Ukraine conflict, in which it sided with Kiev. The sanctions were imposed by Brussels in retaliation for Russia’s decision to send troops into Ukraine in late February.

Vienna will say an emphatic ‘no’ to proposals of a ban on Russian natural gas imports, Austrian Foreign Minister Alexander Schallenberg said on Thursday, noting that the already adopted EU sanctions packages are comprehensive and may require clarification. “I have said in the past that we should discuss this [possible tightening of sanctions] in an appropriate way, namely behind closed doors, but yes – we have already adopted six large-scale sanctions packages, and now we can think about closing the loopholes,” the FM told ORF while answering a question on whether Vienna’s position has changed regarding the possible strengthening of sanctions against Russia. Schallenberg added that “in case of further steps, primarily in the energy sector, with regard to gas, there will be a clear ‘no’ from Austria.”

Austria, which is heavily dependent on Russian energy and sources around 80% of natural gas from Russia, has been opposing the EU’s plan to restrict imports from Moscow. The Federation of Austrian Industries earlier warned that the suspension of Russian gas supplies would be “a serious blow” to the welfare of the Austrian people as it threatens some 300,000 jobs. According to the president of the federation, Georg Knill, almost the entire food industry depends on the supply of the “blue fuel.” He stated in May that he saw danger not so much in the fact that Russia could “turn off the taps,”but in the decision of the European Union to stop importing Russian gas. In March, the EU rolled out a plan to reduce dependence on Russian gas by two thirds before the end of the year. The proposal is part of a wider plan to become independent from all Russian fossil fuels “well before 2030.”

Starting last month Ukrainian lawmakers began seeking to implement severe consequences for those participating in Russia-sponsored referendums in occupied territories of Ukraine. For example, a law is being pushed through parliament which criminalizes obtaining a Russian passport in temporarily occupied territories, Ukrainian sources reported last week, according to Yahoo News. Proposed possible punishments have included losing Ukrainian citizenship, or even lengthy jail sentences. But other officials have argued for a more compromising approach given the necessity of survival in occupied areas. But now the Ukrainian government has reiterated its willingness to impose steep penalties for even participating in any Kremlin-sponsored vote to join the Russian Federation.

Russian President Putin’s Wednesday morning address announcing partial mobilization also affirmed plans to move forward with referendums in the LPR, DPR, Kherson and Zaporozhye regions. Ukraine has responded by warning its citizens that any official who promotes or organizes the voting faces a “prison term of five to ten years” – as well as possible asset seizure by the state, and being barred from employment in select positions for up to 15 years. Ukrainian Deputy Prime Minister Irina Vereshchuk announced this week that a five year prison term is currently being considered for anyone caught participating in “sham referenda” by government authorities:

“Some lawyers believe that those actions fall under Article 110 part 1 of the Criminal Code of Ukraine, ‘Infringement on Ukraine’s territorial integrity,’ punishable with a prison term of up to five years,” she told the Strana portal on Tuesday. She further called on citizens currently in occupied to territories to “leave, if possible.” Vereshchuk was cited further as follows according to a Russian media translation of her words: “This [may] mean imprisonment for up to five years. So, once again I strongly advise residents of the temporarily occupied territories: do not take a [Russian] passport, do not go to referendums, do not cooperate with the occupiers and leave, if it’s possible,” the official stated.

US defense companies should send their new weapons to Ukraine so they can be tested in actual combat against Russian forces, Kiev’s deputy defense minister, Vladimir Gavrilov, has said. Gavrilov made the suggestion during a speech before hundreds of American defense industry representatives and military acquisitions personnel at the Future Force Capabilities Conference and Exhibition in Austin, Texas on Wednesday. “If you have some ideas, or some pilot projects to be tested before mass manufacturing, you can send it to us and we will explain how to do it. And in the end you will get the stamp, proved by the war in Ukraine. You will sell it easy,” he said, as cited by the Military Times.

According to the deputy defense minister, startup companies, including those involved in anti-drone and anti-jamming equipment, have already brought new technologies to the Ukrainian battlefield. “And they come back with a product that is competitive in the market now because it was tested in a combat zone,” Gavrilov said, without revealing the companies that have worked with Ukraine in this capacity. His comments were made on the day Russian President Vladimir Putin announced a partial mobilization, which he said is necessary because Russia has been fighting “the entire Western military machine” in Ukraine. Defense Minister Sergey Shoigu later stated that around 300,000 reservists are planned to be called up.

In view of this shift in Russia’s tactics, Kiev will require more counter-drone and electronic warfare technologies, armored vehicles, and long-range anti-tank and precision fire weapons, Gavrilov said. Ukraine is now almost entirely dependent on weapons supplied by the US, UK, EU, and other nations, according to Shoigu, as most of the Soviet-made hardware it had before the fighting began in late February has been destroyed by Russian forces.

The current crisis in Ukraine was brought about by the West systematically covering up the crimes of the Kiev government since the 2014 coup, Russian Foreign Minister Sergey Lavrov told the UN Security Council on Thursday. Lavrov noted that “impunity” is a good term for what has been happening in Ukraine, not since February but since 2014, when US-backed nationalists and neo-Nazis seized power by force. No one has ever been held responsible for the murders on the Maidan, the burning of peaceful protesters in Odessa, or the assassinations of dissidents, he pointed out. Civilians of Donbass have been bombed mercilessly for years and dubbed terrorists and even subhuman, simply for refusing to accept the results of the coup and insisting on their basic human right to speak Russian, Lavrov said.

The Russian foreign minister presented a long list of human rights violations by Kiev that went ignored by various European and global human rights groups, from “burning books, just like in Nazi Germany” to using banned ‘petal’ land mines against civilians this summer. “Such outrages became possible and remain unpunished due to the fact that the US and its allies, with the connivance of international human rights institutions, have been systematically covering up the crimes of the Kiev regime for eight years, basing their policy towards [Ukrainian President Vladimir] Zelensky based on the well-known American principle: he may be a son of a b*tch, but he is our son of a b*tch,” said Lavrov.

This was a reference to an apocryphal quote attributed to President Franklin Delano Roosevelt, and thought to apply either to Anastasio Somoza of Nicaragua or Rafael Trujillo of the Dominican Republic – both US-backed dictators. Lavrov also accused the Ukrainian armed forces of using civilians as human shields and said that Russia and the Donbass republics are fighting against the “Western military machine” in Ukraine, with the US and its allies perilously close to being overt participants in the conflict. Moscow has shared evidence demonstrating that the West has sought to turn Ukraine into a forward outpost that could threaten Russia’s security, Lavrov told the UN. “I can assure you, we will not let that happen.”

JPMorgan Chase CEO Jamie Dimon said slamming the brakes on new oil and gas production “would be the road to hell for America” after Rep. Rashida Tlaib asked him to divest in oil. Dimon’s comments came during a House hearing where the far-left Michigan Democrat asked him and other top bank execs if they would commit to no longer investing funds into oil and gas companies to slow down climate change. “Please answer with a simple yes or no, does your bank have a policy against funding new oil and gas products,” Tlaib asked, with Dimon up first. “Absolutely not and that would be the road to hell for America,” Dimon shot back.

Tlaib then slammed JPMorgan-Chase and circled back to criticism Dimon leveled against President Joe Biden’s plan to forgive up to $20,000 in student debt during the hearing. She encouraged people to cancel their accounts with the major bank. “Sir, you know what, everybody that got relief from student loans — has a bank account with your bank — should probably take out their account and close their account,” an irritated Tlaib said. “The fact that you’re not even there to help relieve many of the folks that are in debt, extreme debt, because of student loan debt and you’re out there criticizing it,” Tlaib said before moving on to the next bank executive on the panel, Citi CEO Jane Fraser, who offered a more diplomatic response.

The sequence of events leading to the exposure of Greece’s Watergate scandal began in July 2019, immediately after Mr Mitsotakis won the last general election on behalf of New Democracy, our conservative party. One of the very first decrees he issued, as incoming Prime Minister, was one that gave his office direct control over and responsibility for EYP. “Why on earth is the PM taking over the supervision of EYP?”, I remember a parliamentary colleague asking me that very day. It was, indeed, a curious move. Our trepidation only grew following two personnel choices. First, Mitsotakis appointed a nephew of his, Grigoris Dimitriadis, to oversee EYP on his behalf. Secondly, he chose as EYP’s new head Panagiotis Kontoleon, the CEO of the Greek franchise of the private security firm G4 — a man with no record of public service, and whose appointment Mitsotakis could only complete after amending the relevant law to remove the prerequisite that the EYP chief holds a postgraduate degree.

Given his concerted and very public efforts to take complete control of the state intelligence agency, something no other PM had ever done, it became impossible to shift blame to some other minister once the faeces hit the proverbial fan. Of the more than 17,000 wiretaps that EYP admits it has placed during the last year alone, two cases are at the heart of the current scandal. The first is that of Thanasis Koukakis, an investigative journalist who dared look into Greek shipowners’ loans that had been illegally written off by the Bank of Piraeus (one of the banks that Greek taxpayers have had to repeatedly bailout). It turns out that Koukakis was one of EYP’s “subjects of interest”, an outrage that would have probably gone unnoticed without the second, higher profile, case.

It was this case that broke the camel’s back: an investigation begun by the European Parliament’s IT department accidentally revealed that Nikos Androulakis, an MEP belonging to PASOK (the formerly dominant party in Greek politics), was being phone-tapped by EYP. It was explosive news because, at the time his phone was tapped, Androulakis was contesting the leadership of PASOK — a contest that he, eventually, won. The significance of that contest cannot be understated, since its outcome mattered a great deal to Mitsotakis and his governing New Democracy party. Since the middle of the pandemic, opinion polls have persistently suggested that the next election, which must take place by July 2023, will result in a hung parliament. While Mitsotakis’ New Democracy seemed likely to remain the largest party, it was not even close to an absolute majority. PASOK, in third place, was therefore positioned as kingmaker: whoever the party chose to side with would end up in government.

The stakes of PASOK’s leadership race suddenly seemed very high. Of the three main candidates, the one that would almost certainly choose to back New Democracy and Mitsotakis to form a government was Andreas Loverdos — an MP and former minister who had served gladly in New Democracy-PASOK coalition governments between 2011 and 2015. Every newspaper, radio and television station supporting Mitsotakis was rooting for Loverdos to beat Androulakis in the PASOK leadership primary. Is it any wonder that the revelation of EYP’s surveillance of Androulakis was big news? In a period during which the ruling party was rooting for Androulakis’s opponent, the nation’s spy agency — which ruling party’s leader and his nephew controlled and supervised to the full — was tapping Androulakis’ phone!

Letitia James ran on “get Trump” and then spent her entire tenure as NY AG trying to “get Trump”, already the most investigated and prosecuted person in the history of the US. She will fail just like the others.

Meanwhile: why did James make this a civil, not a criminal case?

And: if Trump defrauded banks and pension funds, why did none of them ever file a case?

Donald Trump’s legal perils have become insurmountable and could snuff out the former US president’s hopes of an election-winning comeback, according to political analysts and legal experts. On Wednesday, Trump and three of his adult children were accused of lying to tax collectors, lenders and insurers in a “staggering” fraud scheme that routinely misstated the value of his properties to enrich themselves. The civil lawsuit, filed by New York’s attorney general, came as the FBI investigates Trump’s holding of sensitive government documents at his Mar-a-Lago estate in Florida and a special grand jury in Georgia considers whether he and others attempted to influence state election officials after his defeat there by Joe Biden.

The former US president has repeatedly hinted that he intends to run for the White House again in 2024. But the cascade of criminal, civil and congressional investigations could yet derail that bid. “He’s done,” said Allan Lichtman, a history professor at American University, in Washington, who has accurately predicted every presidential election since 1984. “He’s got too many burdens, too much baggage to be able to run again even presuming he escapes jail, he escapes bankruptcy. I’m not sure he’s going to escape jail.” After a three-year investigation, Letitia James, the New York attorney general, alleged that Trump provided fraudulent statements of his net worth and false asset valuations to obtain and satisfy loans, get insurance benefits and pay lower taxes. Offspring Don Jr, Ivanka and Eric were also named as defendants.

At a press conference, James riffed on the title of Trump’s 1987 memoir and business how-to book, The Art of the Deal. “This investigation revealed that Donald Trump engaged in years of illegal conduct to inflate his net worth, to deceive banks and the people of the great state of New York. Claiming you have money that you do not have does not amount to ‘the art of the deal’. It’s the art of the steal,” she said. Her office requested that the former president pay at least $250m in penalties and that his family be banned from running businesses in the state. James cannot bring criminal charges against Trump in this civil investigation but she said she was referring allegations of criminal fraud to federal prosecutors in Manhattan as well as the Internal Revenue Service.

Austria’s chancellor is set to meet Vladimir Putin on Monday, the Russian president’s first face-to-face meeting with an EU leader since ordering the invasion of Ukraine, amid warnings of a fresh offensive and shelling in the east. Karl Nehammer said the meeting would take place in Moscow and that Austria had a “clear position on the Russian war of aggression”, calling for humanitarian corridors, a ceasefire and full investigation of war crimes. On the ground, Russian forces pounded targets in eastern Ukraine with missiles and artillery on Sunday, and Ramzan Kadyrov, the powerful head of Russia’s republic of Chechnya, said there would be an offensive not only on the besieged southern port of Mariupol but also on Kyiv and other Ukrainian cities.

“Luhansk and Donetsk – we will fully liberate in the first place … and then take Kyiv and all other cities,” Kadyrov said in a video posted on his Telegram channel. The US has warned that the appointment of a new general in command of Russia’s military campaign is likely to usher in a fresh round of “crimes and brutality” against civilians. Alexander Dvornikov, 60, came to prominence at the head of Russian troops in Syria in 2015-16, when there was particularly brutal bombardment of rebel-held areas, including civilian populations, in Aleppo. Jake Sullivan, the national security adviser in Washington, said: “This particular general has a résumé that includes brutality against civilians in other theatres – in Syria – and we can expect more of the same” in Ukraine.

Nehammer met Ukrainian president Volodymyr Zelenskiy in Kyiv on Saturday – the same day as the British prime minister, Boris Johnson, who promised to give Ukraine 120 armoured vehicles and anti-ship missile systems. Washington has also pledged to give Ukraine “the weapons it needs” to defend itself against a new Russian offensive. Russia has failed to take any major cities, but Ukraine says it has been gathering its forces in the east for a major assault and has urged people to flee. Russian forces fired rockets into Ukraine’s Luhansk and Dnipropetrovsk regions on Sunday, officials said. Missiles completely destroyed the airport in the city of Dnipro, said Valentyn Reznichenko, governor of the central Dnipropetrovsk region. Russia’s defence ministry said high-precision missiles had destroyed the headquarters of Ukraine’s Dnipro battalion in the town of Zvonetsky.

Russia will take legal action if the West tries to force it to default on its sovereign debt, Finance Minister Anton Siluanov told the pro-Kremlin Izvestia newspaper on Monday, sharpening Moscow’s tone in its financial wrestle with the West. “Of course we will sue, because we have taken all the necessary steps to ensure that investors receive their payments,” Siluanov told the newspaper in an interview. “We will present in court our bills confirming our efforts to pay both in foreign currency and in roubles. It will not be an easy process. We will have to very actively prove our case, despite all the difficulties.” Siluanov did not elaborate on Russia’s legal options.

Russia faces its first sovereign external default in more than a century after it made arrangements to make an international bond repayment in roubles earlier this week, even though the payment was due in U.S. dollars. Last week, Siluanov said Russia will do everything possible to make sure its creditors are paid. “Russia tried in good faith to pay off external creditors,” Siluanov said on Monday. “Nevertheless, the deliberate policy of Western countries is to artificially create a man-made default by all means.” Siluanov said Russia’s external liabilities amount to about 20% of the total public debt, which stood at about 21 trillion roubles ($261.7 billion). Of that, about 4.5-4.7 trillion roubles were external liabilities.

Russia has not defaulted on its external debt since the aftermath of its 1917 revolution, but its bonds have now emerged as a flashpoint in its economic tussle with Western countries. A default was unimaginable until recently, with Russia rated as investment grade in the run up to its Feb. 24 invasion of Ukraine, which Moscow calls a “special military operation” and which on Sunday intensified in eastern Ukraine. “If an economic and financial war is waged against our country, we are forced to react, while still fulfilling all our obligations,” Siluanov said. “If we are not allowed to do it in foreign currency, we do it in roubles.”

The Finnish government is poised to formally apply for NATO membership “before midsummer” and potentially as early as May. Finnish Prime Minister Sanna Marin stated Friday that the country would vote “before midsummer” on sending an application to join NATO. Former Prime Minister Alexander Stubb says the vote will likely happen as early as May, according to Agence France-Presse. “We will have very careful discussions but not taking any more time than we have to,” Marin said during a press conference. “I think we will end the discussion before midsummer.” Stubb, however, was more specific in his prediction, telling the AFP on Saturday the government would likely vote on the issue before the end of May, just in time for NATO’s June summit in Madrid.

“The Finns think that if Putin can slaughter his sisters, brothers and cousins in Ukraine, as he is doing now, then there is nothing stopping him from doing it in Finland. We simply don’t want to be left alone again,” Stubb told AFP. While the Finnish public has traditionally been opposed to joining NATO, polls showed a seismic shift on the issue following Russia’s invasion of Ukraine in late February. Finland shares an 830-mile border with Russia, and support for joining NATO jumped from 26% to 60% following the invasion. Finland has remained wary of its eastern neighbor since the Winter War of 1939, when Soviet forces attempted to invade at the start of World War II. Finish forces famously delivered a resounding defeat to the Soviets. Finland lost 26,000 soldiers compared at least 126,000 dead or missing for the USSR. NATO General Secretary Jens Stoltenberg has stated that Finland would certainly be approved should it apply to join the alliance.

Some Russian lawmakers are already offering hostile language regarding a potential NATO-allied Finland. Russian lawmaker Vladimir Dzhabarov stated that joining the alliance would be a “strategic mistake” for Finland, adding that the country would “become a target.” “I think it [would be] a terrible tragedy for the entire Finnish people,” Dzhabarov said, adding that with such an action, “the Finns themselves will sign a card for the destruction of their country.”

The North Atlantic Treaty Organisation (NATO) has announced that it will begin engaging in the Asia-Pacific region both practically and politically in light of Beijing’s growing influence and coercion and its unwillingness to condemn Russia’s invasion of Ukraine. Speaking following the meetings of NATO Ministers of Foreign Affairs on April 7, NATO Secretary-General Jens Stoltenberg said the global implications of the Ukrainian conflict had propelled the organisation to step up its engagement with Asia-Pacific partners for the first time. “We have seen that China is unwilling to condemn Russia’s aggression. And Beijing has joined Moscow in questioning the right of nations to choose their own path,” Stoltenberg said. “This is a serious challenge to us all. And it makes it even more important that we stand together to protect our values.”

NATO and its Asia-Pacific partners—Australia, Japan, New Zealand, and the Republic of Korea—met in Brussels to discuss international support for Ukraine. Stoltenberg said the gathered foreign ministers agreed that NATO’s next Strategic Concept briefing, expected to be finalised for the Madrid Summit in June, must deliver a response on how they relate to Russia in the future and how, for the first time, they take into account that their security is affected by China’s growing influence and coercive policies. “NATO and our Asia-Pacific partners have now agreed to step up our practical and political cooperation in several areas, including cyber, new technology, and countering disinformation,” he said. “We will also work more closely together in other areas such as maritime security, climate change, and resilience. Because global challenges demand global solutions.”

‘Nice country of 1.5 billion hungry people you got there Modi. With all this talk of global famine going around, it’d be a shame if you couldn’t feed them.’

Against the backdrop of increased Russia-India trade {link}, and the BRICS discussions about new trade payment mechanisms to avoid being shackled to the dollar {link}, it would appear the people behind the White House operation to create/maintain conflict with Russia are scheduling a stern conversation with India’s Prime Minister Narendra Modi. WHITE HOUSE – ” President Joseph R. Biden, Jr. will meet virtually with Prime Minister Narendra Modi of India on Monday, April 11 to further deepen ties between our governments, economies, and our people. President Biden and Prime Minister Modi will discuss cooperation on a range of issues.” … “President Biden will continue our close consultations on the consequences of Russia’s brutal war against Ukraine and mitigating its destabilizing impact on global food supply and commodity markets.”

The message from the White House will likely be akin to: ‘Nice country of 1.5 billion hungry people you got there Modi. With all this talk of global famine going around, it’d be a shame if you couldn’t feed them.’ Oh, and by the way, did you happen to catch what just rolled out in Pakistan? Imagine that – what with common borders and such… For those unfamiliar, it appears the DoS/CIA were up to their old tricks again, because Pakistan was favorable to the position of China and Russia in the Ukraine conflict and would not take sides with NATO and western allied leaders. Pakistani Prime Minister Imran Khan was ousted through a majority parliamentary no-confidence vote early Sunday, that smells identical to the way Obama/Biden DoS/CIA ousted Egyptian President Hosni Mubarak.

(VOA) – […] Khan is the first prime minister to be ousted by a no-confidence vote in Pakistan, but no democratically elected prime minister has served a full five-year term since the founding of the country in 1947. The repeatedly delayed no-confidence vote against Khan was held after the country’s Supreme Court ruled last week he had acted unconstitutionally when he previously blocked the no-confidence vote, and subsequently dissolved parliament. The embattled Pakistani leader had defended his blocking of the vote, alleging that the no-confidence motion was the result of the United States meddling in his country’s politics. Washington rejected the charges, saying there was “no truth” to them.

[..] (VIA ABC) – […] Khan has claimed the U.S. worked behind the scenes to bring him down, purportedly because of Washington’s displeasure over his independent foreign policy choices, which often favor China and Russia. He has occasionally defied America and stridently criticized America’s post 9/11 war on terror. Khan said America was deeply disturbed by his visit to Russia and his meeting with Russian President Vladimir Putin on Feb. 24, the start of the devastating war in Ukraine. The U.S. State Department has denied his allegations.

According to bioweapons expert Francis Boyle, Russia’s accusation that Ukraine is conducting U.S.-funded bioweapons research appears to be accurate If true, everyone involved is subject to life in prison under the Biological Weapons Anti-Terrorism Act of 1989. According to Boyle, the U.S. government and Pentagon have had a “comprehensive policy” to “surround Russia with biological warfare laboratories” and “preposition biological weapons” there for use against them The problem with trying to make a distinction between “biodefense” and “biowarfare” is that, basically, there is none. No biodefense research is purely defensive, because to do biodefense work, you’re automatically engaged in the creation of biological weapons, and all dual use research can be used for military purposes. SARS-CoV-2 may be the result of such dual use research

Boyle believes we can hold the culprits behind the SARS-CoV-2 bioweapon accountable by asking local prosecutors to convene a grand jury to seek the indictment of those responsible for the pandemic for murder and conspiracy to commit murder In the video above, “InfoWars” host Owen Shroyer interviews Francis Boyle, Ph.D., a Harvard educated lawyer and bioweapons expert with a Ph.D. in political science, about the biolabs in Ukraine, which Russia claims are engaged in U.S.-funded bioweapons research. For decades, Boyle has advocated against the development and use of bioweapons. In fact, he was the one who called for biowarfare legislation at the Biological Weapons Convention of 1972. He then went on to draft the Biological Weapons Anti-Terrorism Act, which was passed unanimously by both houses of Congress and signed into law by then-president George Bush Sr. in May 1989.

While the U.S. has vehemently denied Russia’s accusations, Boyle says that based on what he’s discovered so far, the labs in Ukraine are all conducting biological warfare research — including ethnic-specific biological weapons — at the behest of the U.S. Pentagon, just as Russian authorities are claiming. “The Pentagon does not do missionary work,” he says. “They kill people, and that’s why they are there.” He also points out that everyone involved is subject to life in prison under the Biological Weapons Anti-Terrorism Act of 1989, which explains the mad scramble to project these labs as something other than what they are.

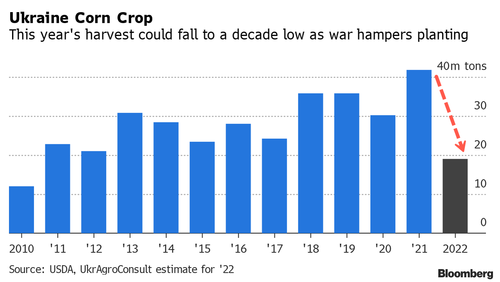

Ukraine is one of the world’s top exporters of corn, sunflower oil, and wheat. Disruptions stemming from Russia’s invasion of Ukraine have stoked fears the war-torn country could experience a 50% decline in crop output this year, according to Bloomberg. Forecast data from ag expert UkrAgroConsult show Ukraine’s corn output could be as low as 19 million tons, about half of last year’s 41 million tons. UkrAgroConsult’s pessimistic outlook follows huge production uncertainties as farmers experience shortages of diesel and fertilizer and bombed-out infrastructure.

The outlooks of two other ag firms aren’t as gloomy. Black Sea research firm SovEcon expects Ukraine’s 2022 corn harvest to be 27.7 million tons, and Barva Invest’s outlook is 29.5 million tons. Both a far below 2021 totals. Maxigrain analyst Elena Neroba warned if farmers don’t have diesel, they “can’t plant huge hectares.” “Some farmers still don’t have access to seeds and fertilizers. Even if they already paid for them, the delivery supply chain doesn’t work as well as it should,” Neroba said. Regardless of how much the conflict impacts output, global food prices have never risen so fast and have never been so high in anticipation of food shortages worldwide. In March, global food prices jumped a stunning 12.64% MoM – almost double the previous record monthly surge…

Seated around the dining table, the family of four stares blankly at pictures of food sketched on the tablecloth. “Tonight,” the father says, “we’re coloring for dinner.” The scene in a cartoon in a Moroccan newspaper speaks to the predicament facing the kingdom’s 37 million people and their peers across North Africa as the Muslim world marks Ramadan. Normally characterized by abstention broken by plentiful sunset feasts, the holy month for many this year is a confrontation with painful economic reality. Global foods costs are up more than 50% from mid 2020 to a record and households worldwide are trying to cope with the strains on their budgets. In North Africa, the challenge is more acute because of a legacy of economic mismanagement, drought and social unrest that’s forcing governments to walk a political tightrope at a precarious time.

The Middle East and North Africa region’s net food and energy importers are especially vulnerable to shocks to commodity markets and supply chains resulting from Russia’s war on Ukraine, according to the International Monetary Fund. That’s in countries where the rising cost of living helped trigger the Arab Spring uprisings a little over a decade ago. “Just how much more do we have to take?” asked Ahmed Moustafa, a 35-year-old driver and father of three in Cairo. He already had to sell some appliances to keep food on the table and cover other expenses, he said. “We keep being asked to cut and cut and cut, but there’s not much left to cut from.”

Home to large, mainly urban populations and lacking oil wealth, governments in Egypt, Morocco and Tunisia are struggling to maintain subsidies for food and fuel that have helped keep a lid on discontent. The World Food Programme has warned that people’s resilience is at “breaking point,” while the United Arab Emirates moved to help ally Egypt, the world’s largest buyer of wheat, to shore up its food security and ward off potential instability. Egypt is also seeking IMF help.

Amid warnings of an upcoming food crisis, Democrats on the House Agriculture Committee are prioritizing the installation of “Tesla charging stations” in rural America, Rep. Kat Cammack (R-Fla.) lamented this week. The United Nations’ World Food Programme (WFP) released a report Monday titled “Unprecedented Needs Threaten a Hunger Catastrophe.” “The world cannot afford another conflict as is happening today in Ukraine,” the report warned. “The war is a catastrophe, compounding what is already a year of destructive hunger.” “Ukraine and Russia account for a third of the global wheat supply, and over half of WFP’s supply of the grain,” the report explains. “The crisis in the breadbasket of Europe is driving up the price of wheat as well as maize, sunflower oil and crude oil — with dramatic fallouts for food security worldwide.”

If the Russian invasion continues beyond April, “an additional 47 million people” will experience acute hunger, up “from a prewar baseline of 276 million people,” WFP noted in another report, released on Wednesday. “Altogether, this means that up to 323 million people could become acutely food insecure in 2022,” the report added. On Friday, the U.N. Food and Agriculture Organization said the invasion of Ukraine is causing a 17.1% increase in prices for grain, which includes wheat, oats, barley and corn. On the John Solomon Reports podcast on Wednesday, Cammack warned of the approaching food crisis as Russia’s invasion of Ukraine continues, preventing the latter country from planting crops.

“Ukraine should be planting right now,” she said. “They are not planting. So while this would be a typical growing season and a planting season, tractors are being used for the war effort, fuel is being used for the war effort — that is going to be a major, major issue as we move into the fall and the winter, because they will have missed an entire season. There will be no harvest next year.” There will be a “700% increase in fertilizer costs,” Cammack predicted. “And when you compound that with fuel prices — it was $5.19 a gallon for diesel in my district just this past weekend. You factor in the regulatory environment that is squeezing our producers to death. This administration has thrown more red tape on them and the threat of new taxes and regulations on producers, and then you basically put a bow on it with a pretty scarce labor market, it’s looking pretty grim.”

THE SPIKE PROTEIN PATHOGENIC ALGORITHM – DUAL PATHS TO TERMINAL SYSTEMIC FIBROSIS: IMMEDIATE FOR THOSE WITH SIGNIFICANT COMORBIDITIES, INDUCED FOR THOSE WITHOUT. The Spike Protein is inducing terminal systemic fibrosis of all organs, including the blood, via two principal mechanisms. The first is a direct, immediate path via binding to RGD-binding integrins, which includes several TGF-β-activating integrins. This activates Myofibroblasts which induces Fibrosis. Indeed, in autopsies of COVID-19 patients with advanced disease, 38% collagen deposition was found in their lungs. This is a rapid and certainly fatal circumstance. But, this is not limited to the lungs. In a series of cardiac autopsies conducted in Washington state, the most common changes observed were fibrosis in 14 (100%) patients and myocyte hypertrophy in 13 (93%) patients.

Let that sink in. In 100%. In EVERY SINGLE CARDIAC AUTOPSY, FIBROSIS WAS OBSERVED. The other mechanism is via DNA Double Strand Breaks and Impaired DNA Repair Mechanisms. This induces fatal systemic fibrosis in those who do not succumb to the initial assault. In mice that have their DNA Repair Mechanisms genetically deleted (this kind of mouse was developed to study Alzheimer’s) they experience The same level of DNA Damage as normal type mice. However, they accumlate DNA lesions faster due to their impaired DNA repair response. What is the effect of this? THEIR AGING IS ACCELERATED 6-FOLD OVER NORMAL TYPE MICE. What happens to these mice? They develop conditions common in elderly humans such as osteoporosis, pulmonary fibrosis, chronic kidney disease, cardiovascular disease, muscle wasting, peripheral neuropathy, hepatic fibrosis, urinary incontinence, intervertebral disc degeneration, cognitive decline, and loss of hearing and vision.

Sounds like Long COVID, doesn’t it? How does this happen? SARS–CoV–2 full–length spike protein inhibits DNA damage repair by hindering DNA repair protein recruitment. Why should this happen in some faster than others? Let us look at Diabetics. Diabetes-induced, persistent DNA damage is associated with organ fibrosis. Non-diabetics are accumulating DNA damage lesions, which will result in terminal fibrosis, but Diabetics are accumulating them FASTER as they already experience HIGHER LEVELS OF DNA DAMAGE, WHICH IS ALSO NOT. BEING. REPAIRED.

Let us look at Obesity. Altered DNA repair; an early pathogenic pathway in Alzheimer’s disease and obesity. In an inverted mechanism to Diabetes, the Obese already have an impaired DNA Repair Response, so, their DNA Repair Response becomes DYSREGULATED INCREASINGLY FASTER than those without this common comorbidity. What is the ultimate point of the Spike Protein’s inhibition of DNA repair Loss of the DNA repair potential results in persistent DNA damage signaling, senescence, SASP, fibrosis, and organ failure.

White House Chief Medical Adviser Dr. Anthony Fauci admitted on Sunday that COVID-19 will not be eliminated and that people will have to calculate their own level of risk that they are willing to take with the virus. “This is not going to be eradicated and it’s not going to be eliminated,” Fauci told Jonathan Karl on ABC’s “This Week.” “What’s going to happen is that we’re going to see that each individual is going to have to make their calculation of the amount of risk that they want to take in going to indoor dinners and in going to functions, even within the realm of a green zone map of the country where you see everything looks green but it’s starting to tick up,” he said.

As of Sunday, the Centers for Disease Control and Prevention has placed most of the United States at green, or at a “low” level of community transmission, and the 7-day moving average for cases sits at less than 27,000. “We’re going to have to live with some degree of virus in the community,” Fauci said, adding, “The best way to mitigate that, Jon, is to get vaccinated.” Fauci urged Americans ages 50 and older as well as immunocompromised people to get the fourth COVID-19 vaccine. He also warned that Americans could be required to mask-up again if cases rise. “We may need to revert back to being more careful and having more utilizations of masks indoors. But right now we’re watching it very, very carefully. And there is concern that it’s going up,” he said. “But hopefully we’re not going to see increased severity.”

For over two weeks the financial capital of China, Shanghai, has been locked down tight. Some 26 million people languish in their apartments, staring at their now-empty refrigerators, unable to set foot outside to forage for food for fear of arrest and incarceration. Foreigners are in the same predicament, as one complained on Twitter: “Day 16 of our COVID lockdown in Shanghai today and food is the key thing on people’s minds. We aren’t allowed to leave home so delivery is the only way I was up at 6 am yesterday trying to get any kind of delivery but nothing was available all day. So far, same results today..” Yet the homebound are the lucky ones.

The unlucky ones are those who test positive for COVID each day, like the 17,077 Shanghainese who did on Wednesday. Symptomatic or not — and nine out of 10 show no signs of illness — they are hauled off to hastily erected quarantine camps. The Shanghai lockdown, the largest since the first Wuhan lockdown two years ago, is China’s latest attempt to achieve COVID Zero. An army of health care workers, some 38,000 in all, have been sent to Shanghai, with instructions to completely stamp out the coronavirus within the city. They are frantically testing and retesting everyone. Unable to protest their lock-up any other way, people have taken to venting their anger by yelling out of their apartment windows. Most of their complaints have to do with food. “We have no food to eat,” they scream. “We haven’t eaten in a very long time. We are starving to death.”

One starving lockdowner found a quieter way to protest his growling stomach. He rolled his refrigerator onto his balcony and opened its doors. The inside is completely empty. Other protests have taken more tragic forms. As they did in Wuhan two years ago, people are once again jumping off the balconies of high-rise apartment buildings. One video circulating in China shows a couple falling to their deaths. The husband was said to be distraught because the lockdown had cost him his business. Those desperate enough to venture outside in their search for food are hunted down by “Big Whites” — members of the security forces who owe their nickname to the white hazmat suits they wear. Patrolling the streets day and night, the “Big Whites” arrest and jail anyone caught breaking quarantine, who often get beaten in the process.

French President Emmanuel Macron will face off against hard-right leader Marine Le Pen later this month in a runoff election. With 97% of the votes in, the incumbent Macron won 27.35% of the vote while Le Pen came in second at 23.97%, according to the French Interior Ministry. Paris mayor Anne Hidalgo, the Socialist candidate, received less than 2% of the vote. Macron, of The Republic On the Move Party, has served as president since 2017. “Make no mistake, nothing is decided,” he told supporters on Sunday evening, according to the BBC. Le Pen celebrated Sunday’s results on Twitter. “I call on all French people, of all sensitivities, to join this great national and popular gathering that I am carrying!” she wrote.

Le Pen has surged in popularity following Russia’s invasion of Ukraine as the cost of living increased, the Financial Times reported. She has been accused of being far-right for her anti-Islam views. Le Pen has said that she would limit immigration and forbid the Muslim veil in public. “That’s not us,” Macron said. “Make no mistake. This contest is not finished, and the debate we’ll have in the next two weeks will be decisive for our country and for Europe … I want a France rooted in a strong Europe.” Le Pen has also been skeptical of the European Union and NATO. If she wins, the founder of the National Rally Party promised to restore France’s “prosperity and grandeur.” Left-wing Jean-Luc Melenchon, who came in third at less than 22%, urged his followers Sunday evening, “You must not give a single vote to Marine Le Pen,” according to the BBC. He did not, however, endorse the current president.

Doug Casey talks Great Reset, says we’re in for a tough time, that trends in motion tend to stay in motion, and fears the stage is being set for some authoritarian leader to rise to power. He feels the people who love liberty (e.g. libertarians) are an anomaly or rounding error compared to the rest of society. He gives his thoughts on being an international man in the brave new world where air travel has collapsed and authority has become more digital and centralized. We discuss Ukraine…he believes the Russians are on the right side of all this. The U.S. Government is a collapsing empire and has become the greatest danger in the world today. We could be looking at real chaos over the next decade or two. He gives us some tips on surviving the apocalypse.

“..the government’s debt to GDP ratio soaring to 125 percent. For perspective, that ratio was just 53 percent back in 1960, and only 58 percent as recently as 2000..”

The U.S. economy is already deteriorating due to the humongous fiscal and monetary cliffs. These cliffs are now being compounded by the war in Eastern Europe and near record-high inflation. And, the Fed’s “PUT” is much lower and smaller in size than Wall Street believes. The war in Ukraine will exacerbate the negative supply shocks that are already in place due to COVID-19. Worsening bottlenecks will combine with rising inflation to produce a contraction in global growth. Russia produces 12 percent of the world’s oil supply and exports 18 percent of the world’s wheat consumption. Ukraine accounts for 25 percent of global wheat production. Sanctions and war will serve to slow the economy further and send prices for these vital commodities even higher.

But the upcoming recession will be extraordinarily unique. Not only will it occur while inflation is at a multi-decade high, it will be the first U.S. economic contraction to take place while the Federal Reserve had its target interest rate at or near zero percent. For comparison, look at how much room the Fed had to reduce borrowing costs during previous economic contractions. The following historical data indicates the level of the Fed Funds Rate just prior to the outset of all 10 U.S. recessions since WWII: 1957 3.5 percent, 1960 4.0 percent, 1969 10.5 percent, 1973 13.0 percent, 1979 16.01 percent, 1981 20.61 percent, 1989 10.71 percent, 2000 6.86 percent, 2007 5.31 percent, and 2019 2.45 percent.

In addition, the swoon in GDP will occur after the Fed has just finished printing $4.5 trillion over the past two years and with the national debt vaulting over $30 trillion due to the massive increase in government deficits in the wake of the COVID-19 pandemic. Such borrowing helped send the government’s debt to GDP ratio soaring to 125 percent. For perspective, that ratio was just 53 percent back in 1960, and only 58 percent as recently as 2000. Inflation is destroying real wages, and rising borrowing costs are destroying consumers’ ability to consume. Consumption is 70 percent of GDP, and that means the rate of economic growth is set to plunge. This would normally spur the government into remediative action. But the fact remains that the ability of the Treasury and Federal Reserve to turn around a recession expeditiously by borrowing trillions of dollars and having that debt monetized by the Fed has become greatly fettered this time around.

Deutsche Bank closed at $16.50 on the New York Stock Exchange on February 10 of this year. It closed at $10.23 yesterday – a decline of 38 percent in a month’s time. That’s a big problem because Deutsche Bank is heavily interconnected to Wall Street banks via derivatives. According to Deutsche Bank’s most recent annual report, as of December 31, 2020, it held $35.4 trillion in notional derivatives. (Notional means face amount.) Deutsche Bank, a large German bank, was among the global banks bailed out by the Fed during the financial crash of 2008 as well as during the (still unexplained) liquidity crash that saw the Fed pump trillions of dollars in cumulative loans into global banks from September 17, 2019 through July 2, 2020.

In June 2016, The International Monetary Fund (IMF) released a report with a finding that Deutsche Bank posed the greatest threat to global financial stability than any other bank because of its interconnections to Wall Street mega banks and large banks in Europe. The largest bank in the United States, JPMorgan Chase, was shown as one of the banks with the largest amount of exposure. Despite that finding by the IMF in 2016, Deutsche Bank has been allowed by regulators in Europe and the U.S. to continue engaging in high-risk Over-the-Counter derivatives. It also has an uncomfortable history of suicides and rogue behavior. See a sampling of its history since 2014 below. Yes, President Joe Biden’s administration has a lot on its plate. But if it doesn’t get serious about reforming Wall Street and its derivative weapons of mass destruction, it will have a lot more to deal with eventually.

And they’re back! It’s like one of those 1960s Hammer Film Productions horror-movie series with Peter Cushing and Christopher Lee … Return of the Putin-Nazis! Revenge of the Putin-Nazis! Return of the Revenge of the Bride of the Putin-Nazis! And this time they are not horsing around with stealing elections from Hillary Clinton with anti-masturbation Facebook ads. They are going straight for “Democracy’s” jugular! Yes, that’s right, folks, Vladimir Putin, leader of the Putin-Nazis and official “Evil Dictator of the Day,” has launched a Kamikazi attack on the United Forces of Goodness (and Freedom) to provoke us into losing our temper and waging a global thermonuclear war that will wipe out the entire human species and most other forms of life on earth!

I’m referring, of course, to Putin’s inexplicable and totally unprovoked invasion of Ukraine, a totally peaceful, Nazi-free country which was just sitting there minding its non-Nazi business, singing Kumbaya, and so on, and not in any way collaborating with or being cynically used by GloboCap to menace and eventually destabilize Russia so that the GloboCap boys can get back in there and resume the Caligulan orgy of “privatization” they enjoyed throughout the 1990’s. No, clearly, Putin has just lost his mind, and has no strategic objective whatsoever (other than the total extermination of humanity), and is just running around the Kremlin shouting “DROP THE BOMBS! EXTERMINATE THE BRUTES!” all crazy-eyed and with his face painted green like Colonel Kurtz in Apocalypse Now … because what other explanation is there?

Or … OK, sure, there are other explanations, but they’re all just “Russian disinformation” and “Putin-Nazi propaganda” disseminated by “Putin-apologizing, Trump-loving, discord-sowing racists,” “transphobic, anti-vax conspiracy theorists,” “Covid-denying domestic extremists,” and other traitorous blasphemers and heretics, who are being paid by Putin to infect us with doubt, historical knowledge, and critical thinking, because they hate us for our freedom … or whatever. Let’s take a quick look at some of that “Russian disinformation” and “propaganda,” purely to inoculate ourselves against it. We need to be familiar with it, so we can switch off our minds and shout thought-terminating clichés and official platitudes at it whenever we encounter it on the Internet. It might be a little uncomfortable to do this, but just think of it as a Russian-propaganda “vaccine,” like an ideological mRNA fact-check booster (guaranteed to be “safe and effective”)!

OK, the first thing we need to look at, and dismiss, and deny, and pretend we never learned about, is this nonsense about “Ukrainian Nazis.” Just because Ukraine is full of neo-Nazis, and recent members of its government were neo-Nazis, and its military has neo-Nazi units (e.g., the notorious Azov Battalion), and it has a national holiday celebrating a Nazi, and government officials hang his portrait in their offices, and the military and neo-Nazi militias have been terrorizing and murdering ethnic Russians since the USA and the Forces of Goodness supported and stage-managed a “revolution” (i.e., a coup) back in 2014 with the assistance of a lot of neo-Nazis … that doesn’t mean Ukraine has a “Nazi problem.” After all, its current president is Jewish!

Self-anointed “fact-checkers” in the U.S. corporate press have spent two weeks mocking as disinformation and a false conspiracy theory the claim that Ukraine has biological weapons labs, either alone or with U.S. support. They never presented any evidence for their ruling — how could they possibly know? and how could they prove the negative? — but nonetheless they invoked their characteristically authoritative, above-it-all tone of self-assurance and self-arrogated right to decree the truth and label such claims false. Claims that Ukraine currently maintains dangerous biological weapons labs came from Russia as well as China. The Chinese Foreign Ministry this month claimed: “The US has 336 labs in 30 countries under its control, including 26 in Ukraine alone.”

Nuland

"Ukraine has biological research facilities," says Under Secretary Victoria Nuland. She has "no doubt" that in the event of a biological or chemical attack, #Russia would be responsible. pic.twitter.com/dHQ2Iy3Xxz

The Russian Foreign Ministry asserted that “Russia obtained documents proving that Ukrainian biological laboratories located near Russian borders worked on development of components of biological weapons.” Such assertions deserve the same level of skepticism as U.S. denials: namely, none of it should be believed to be true or false absent evidence. Yet U.S. fact-checkers dutifully and reflexively sided with the U.S. Government to declare such claims “disinformation” and to mock them as QAnon conspiracy theories. Unfortunately for this propaganda racket masquerading as neutral and high-minded fact-checking, the neocon official long in charge of U.S. policy in Ukraine testified on Monday before the Senate Foreign Relations Committee and strongly suggested that such claims are, at least in part, true.

Yesterday afternoon, Under Secretary of State Victoria Nuland testified before the Senate Foreign Relations Committee. Sen. Marco Rubio (R-FL), hoping to debunk growing claims that there are chemical weapons labs in Ukraine, smugly asked Nuland: “Does Ukraine have chemical or biological weapons?” Rubio undoubtedly expected a flat denial by Nuland, thus providing further “proof” that such speculation is dastardly Fake News emanating from the Kremlin, the CCP and QAnon. Instead, Nuland did something completely uncharacteristic for her, for neocons, and for senior U.S. foreign policy officials: for some reason, she told a version of the truth. Her answer visibly stunned Rubio, who — as soon as he realized the damage she was doing to the U.S. messaging campaign by telling the truth — interrupted her and demanded that she instead affirm that if a biological attack were to occur, everyone should be “100% sure” that it was Russia who did it. Grateful for the life raft, Nuland told Rubio he was right.

On Wednesday, the White House claimed without evidence that Russia might use chemical or biological weapons to create a false flag operation in Ukraine. The White House also dismissed Moscow’s accusations that the US is involved in biological weapons research in Ukraine even though there are Pentagon-linked labs in the country. On Twitter, White House Press Secretary Jen Psaki said to be on the lookout “for Russia to possibly use chemical or biological weapons in Ukraine, or to create a false flag operation using them.” She said Russia’s claim of the US having biological weapons labs in Ukraine is “preposterous.” Psaki’s denial comes a day after Undersecretary of State Victoria Nuland said there are “biological research facilities” in Ukraine the US is concerned Russian forces might seize.

Nuland made the comments after being asked if there are bioweapons in Ukraine and said the US is working with the Ukrainians to keep “research materials” out of Russia’s hands. The Russian military has claimed that it uncovered 30 biological laboratories in Ukraine linked to the Pentagon’s Defense Threat Reduction Agency (DTRA). On Wednesday, Russian Foreign Ministry spokeswoman Maria Zakharova said Russia has documents that show Ukraine ordered the destruction of samples of plague, cholera, anthrax, and other pathogens before Russia launched its attack on February 24. According to a February 25 article from the Bulletin of Atomic Scientists, the US government has worked with 26 biological research facilities in Ukraine. The article quoted Robert Pope of the DTRA’s Cooperative Threat Reduction Program, who warned some of the labs could have Pathogens leftover from the Soviet Union’s bioweapons program.

Lavrov biological weapons

Russia FM Lavrov:"We have information that US built two biological warfare labs in Kiev & Odessa. pic.twitter.com/wgB1YXzjqZ