DPC Launch of battleship Georgia, Bath, Maine, Oct 1904

No conscience. No humanity. No God.

• At Least 10 More Children And 6 Adult Refugees Drown Off Greek Islands (Kath.)

As EU leaders seek to boost cooperation in tackling a major refugee crisis, there has been more tragedy in the Aegean with at least 16 migrants drowning in their attempt to get to Greece from Turkey. In one incident late on Friday, the bodies of four children – three girls, aged 5, 9 and 16, and a 2-year-old boy – were discovered by the Greek coast guard off Kalymnos. According to the accounts of 11 adult survivors, another boy was missing. On Saturday, the Turkish coast guard recovered the bodies of another 12 migrants whose boat sank off Turkey’s coast. According to sources, they were heading to the Greek island of Lesvos. Lesvos has borne the brunt of an influx of migrants. Last week alone, at least 10 people, including six children, drowned in an attempt to get the island. On a visit to Lesvos on Friday, European Migration Commissioner Dimitris Avramopoulos inaugurated Greece’s first refugee screening center, or “hotspot.”

“The German states have reported some 409,000 new arrivals between Sept. 5 and Oct. 15..”

• Germany Shows Signs of Strain from Mass of Refugees (Spiegel)

The road to the reception camp in Hesepe has become something of a refugees’ avenue. Small groups of young men wander along the sidewalk. A family from Syria schleps a clutch of shopping bags towards the gate. A Sudanese man snakes along the road on his bicycle. Most people don’t speak a word of German, just a little fragmentary English, but when they see locals, they offer a friendly wave and call out, “Hello!” The main road “is like a pedestrian shopping zone,” says one resident, “except without the stores.” Red-brick houses with pretty gardens line both sides of the street, and Kathrin and Ralf Meyer are standing outside theirs. “It’s gotten a bit too much for us,” says the 31-year-old mother of three. “Too much noise, too many refugees, too much garbage.” Now the Meyers are planning to move out in November.

They’re sick of seeing asylum-seekers sit on their garden wall or rummage through their garbage cans for anything they can use. Though “you do feel sorry for them,” says Ralf, who’s handed out some clothes that his children have grown out of. “But there are just too many of them here now.” Hesepe, a village of 2,500 that comprises one district of the small town of Bramsche in the state of Lower Saxony, is now hosting some 4,000 asylum-seekers, making it a symbol of Germany’s refugee crisis. Locals are still showing a great willingness to help, but the sheer number of refugees is testing them. The German states have reported some 409,000 new arrivals between Sept. 5 and Oct. 15 – more than ever before in a comparable time period – though it remains unclear how many of those include people who have been registered twice.

Six weeks after Chancellor Angela Merkel’s historic decision to open Germany’s borders, there is a shortage of basic supplies in many places in this prosperous nation. Cots, portable housing containers and chemical toilets are largely sold out. There is a shortage of German teachers, social workers and administrative judges. Authorities in many towns are worried about the approaching winter, because thousands of asylum-seekers are still sleeping in tents. But what Germany lacks more than anything is a plan to make Merkel’s two most-pronounced statements on the crisis – “We can do it” and “We cannot close our borders” – fit together. In the second month of what has been dubbed the country’s brand new “Welcoming Culture,” it has become clear to many that Germany will only be able to cope if the number of refugees drops.

But that is unlikely to happen anytime soon. Tens of thousands of people are making their way to Germany along the so-called Balkan route; at the same time, Merkel’s efforts to reduce the influx through diplomacy and tougher regulations remain just that.

Impressive take-down of the many failures of Brussels.

• Why The Euro Divides Europe (Wolfgang Streeck)

The ‘European idea’—or better: ideology—notwithstanding, the euro has split Europe in two. As the engine of an ever-closer union the currency’s balance sheet has been disastrous. Norway and Switzerland will not be joining the EU any time soon; Britain is actively considering leaving it altogether. Sweden and Denmark were supposed to adopt the euro at some point; that is now off the table. The Eurozone itself is split between surplus and deficit countries, North and South, Germany and the rest. At no point since the end of World War Two have its nation-states confronted each other with so much hostility; the historic achievements of European unification have never been so threatened.

No ruler today would dare to call a referendum in France, the Netherlands or Denmark on even the smallest steps towards further integration. Thanks to the single currency, hopes for a European Germany—for integration as a solution to the problems of both German identity and European hegemony—have been superseded by fears of a German Europe, not least in the FRG itself. In consequence, election campaigns in Southern Europe are being fought and won against Germany and its Chancellor; pictures of Merkel and Schäuble wearing swastikas have begun appearing, not just in Greece and Italy but even in France. That Germany finds itself increasingly faced by demands for reparations—not only from Greece but also Italy—shows how far its post-war policy of Europeanizing itself has foundered since its transition to the single currency.

Anyone wishing to understand how an institution such as the single currency can wreak such havoc needs a concept of money that goes beyond that of the liberal economic tradition and the sociological theory informed by it. The conflicts in the Eurozone can only be decoded with the aid of an economic theory that can conceive of money not merely as a system of signs that symbolize claims and contractual obligations, but also, in tune with Weber’s view, as the product of a ruling organization, and hence as a contentious and contested institution with distributive consequences full of potential for conflict.

3% growth?! Or worse? “..His work finds that growth collapsed to a mere 0.2pc during the Asian Financial Crisis, rather than the official figure of 7.8pc.”

• The Truth Behind China’s Manipulated Economic Numbers (Telegraph)

\Beijing’s massaged growth statistics have long over-estimated growth. So what do we really know about what’s going on in the world’s second largest economy? The true state of China’s economic fortunes remain a mystery to the world. Monday will see the latest round of official quarterly GDP statistics from Beijing’s National Statistics Bureau. Economists expect they will reveal another moderate slowdown in growth to around 6.8pc – the lowest rate of expansion since the depths of the financial crisis six years ago. Yet the government’s estimates have long been dismissed as an accurate barometer of what’s really going on in the Chinese economy. [..] Questions over China’s “actual” rate of growth have been thrown into sharp relief after a summer of turmoil in financial markets. Sudden anxiety over a Chinese “hard-landing” left investors dumbstruck.

Billions were wiped off global stock indices and authorities were forced to suspend trading to prop up equity prices. China data-watching has now become the main driver for global economic sentiment. In July, Chinese market ructions were sparked by weak industrial profits numbers. By August, a six-year slump in monthly manufacturing triggered the ugliest day of global trading since the depths of the financial crisis eight years ago. “China’s new export this year is fear” says Paul Gruenwald, chief Asia economist at Standard & Poor’s rating agency. “The joke with Asian analysts on China is that we don’t need to forecast the actual rate of Chinese growth, we have to forecast what the Chinese authorities will say the rate will be.” But China’s GDP figure remains totemic. This stems in large part from the Politburo’s own fixation on annualised growth.

Authorities now say they are targeting yearly expansion of “around 7pc”. Harry Wu, an economics professor at Hitotsubashi University in Tokyo, has calculated the states’ GDP numbers have long played down the effects of external shocks to the economy. His work finds that growth collapsed to a mere 0.2pc during the Asian Financial Crisis, rather than the official figure of 7.8pc. For the period from 2008-14, his readings show an average expansion of 6.1pc, rather than 8.7pc. “Would I bet the actual growth rate is 7pc? No”, says Gruenwald. “Do we have enough indicators to work out what’s going on in the economy? Yes.” “The statistics are still catching up – that’s part of the fun of being an Asia [analyst]…we get to put on our detective hats and do a little investigative economics.” This investigative turn has led to a proliferation in “proxy” indicators for Chinese growth.

The calculations range from anything from 3pc-7pc real GDP growth in 2015. This diversity means there is plenty to support the case for China bulls and China bears. One gauge that has grown in popularity in recent years is the “Li Keqiang index”, named after China’s current premier, and revealed as his preferred measure of economic activity while serving as a senior Communist party secretary in the province of Liaoning a decade ago. GDP numbers were merely a “man-made” and “unreliable” construct, Mr Li was quoted as saying in diplomatic cables published by Wikileaks in 2010. Instead, he chose to focus on a trio of real economic indicators – bank lending, rail freight volumes and electricity production. Taking their cue from the premier, economics consultancy Fathom compile the Li Index as the “true” reflection of what the Communist party’s senior officials are most worried about. It suggests the economy has come to a standstill. Growth will reach just 3pc this year, according to Fathom.

Look: “A Reuters poll of 50 economists put expected growth at 6.8% year on year..” vs “Industrial profits fell 8.8% year on year in August..” That means that A) Reuters polls idiot economists because B) that 6.8% growth is utter nonsense.

• China’s Premier Li Says Achieving Growth Of Around 7% ‘Not Easy’ (Reuters)

China’s Premier Li Keqiang said that with the global economic recovery losing steam, achieving domestic growth of around 7% is “not easy”, according to a transcript of his remarks posted on the website of the State Council, China’s cabinet. Nonetheless in his comments, made at a recent meeting with senior provincial officials, the premier said that continued strength in the labour market and services were reasons for optimism, despite the headwinds facing the manufacturing sector. “As long as employment remains adequate, the people’s income grows, and the environment continuously improves, GDP a little higher or lower than 7% is acceptable,” the premier said in the comments posted on Saturday. China is due to release its third-quarter GDP growth figures on Monday.

A Reuters poll of 50 economists put expected growth at 6.8% year on year, which would be the slowest since the financial crisis in 2009. China’s growth in the first half of 2015, at 7%, was already the slowest since that time. Policymakers had previously forecast growth of “around 7%” for 2015. Most official and private estimates show that the Chinese labour market as a whole is outperforming the steep slowdown in industry, largely due to continuing strength in the service sector. But some analysts have expressed concern that the sharp drop in industrial profits over the past year indicates deeper weakness in income growth and wages next year, which could weaken overall growth further.

Industrial profits fell 8.8% year on year in August, the steepest drop since China’s statistics agency began publishing such data in 2011. The premier cited the emergence of new industries including the Internet sector, the continued need for high infrastructure investment in western regions, and ongoing urbanization as additional reasons for optimism on China’s future growth trajectory. Nonetheless, Li also highlighted the need for further market-oriented reforms and a reduced government role in the economy in order to fully grasp new economic opportunities and maintain growth.

And unofficially much more.

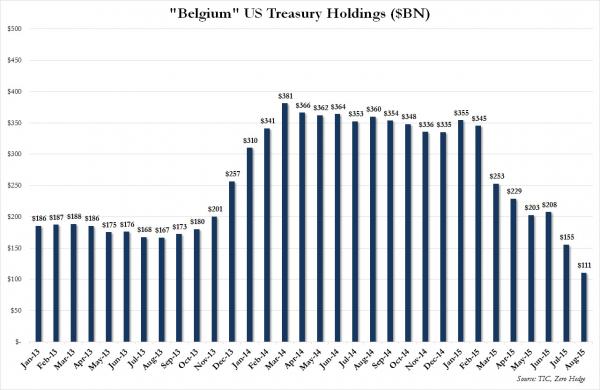

• China Officially Sold A Quarter Trillion Treasurys In The Past Year (ZH)

Back in May, this website was the first to explain the “mystery” behind Belgium’s ravenous Treasury buying which in early 2015 had turned into sudden selling, and which we demonstrated was merely China transacting using offshore Euroclear-based accounts to preserve anonymity. Since then theme of Belgium as a Chinese proxy has become so popular, even CNBC gets it. Consequently, we were also the first to correctly warn that China had begun liquidating its Treasury holdings (a finding which left none other than Goldman “speechless”), which also helped us predict that China is about to announce its currency devaluation three days before it happened as the conversion of Chinese reserves from inert paper to active dollars hinted at a massive effort to stabilize the currency, and thus unprecedented capital outflows.

As a result, the only data point which mattered in yesterday’s Treasury International Capital data release was not China’s holdings, which actually “rose” $1.7 billion in the month when China actively devalued its currency and then spent hundreds of billions to prevent the devaluation from becoming an all out FX rout, but the ongoing decline in Belgium holdings. As the chart below shows, Belgium, pardon Euroclear – which is a clearing house not only for China but many other EM nations who park their reserves in Belgium – sold another $45 billion in Treasurys last month, bringing the total to a dangerously low $111 billion, down from $355 billion at the start of the year.

Lumping Belgium and China holdings into one, as we have done since May, shows that as expected, Chinese selling continued in August, and the result was another drop of $43 billion in TSY holdings in the month of August, which incidentally mirrors perfectly the previously announced decline in September Chinese FX reserves, which according to official data declined from $3.557 trillion to $3.514 trillion.

According to the chart above, while to many Quantitative Tightening is a novel concept, the reality is that China (+ Euroclear) have been dumping Treasurys and liquidating reserves since January when total holdings peaked at $1.6 trillion last summer, and have since declined to $1.38 trillion. It means that China has sold a quarter trillion dollars worth of Treasurys in the past year, in the process offsetting what would have been about 25% of the Fed’s QE3. However, the real number is likely far greater.

China’s killing the world steel industry by dumping its surplus stock. Britain knows all about it.

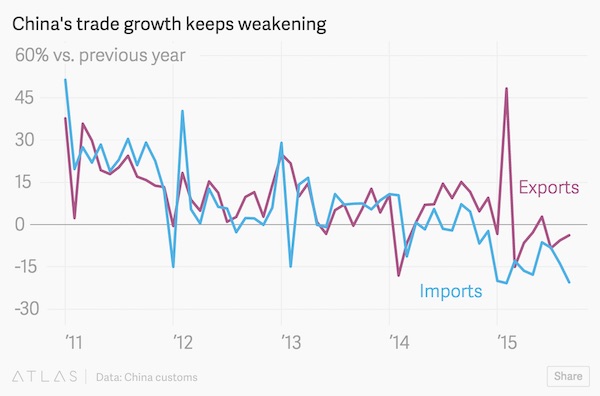

• The Only Thing In China’s Trade Data That’s Growing -But Shouldn’t Be (Quartz)

China’s trade data have been a reliable monthly horror show over the last year, and September was no exception. Exports fell nearly 4% from year-earlier levels, while imports dove an astonishing 20%. One thing, however, is growing quite quickly. The trade gap shown here—illustrating the value of goods China exports minus the value of goods that it imports—leapt more than 90% versus September 2014. In fact, if you discount distortions during Chinese New Year, China’s trade gap was the highest it’s ever been. Some of that gap might be due to slumping commodity prices weighing more heavily on China’s import values. Still, the boom in extra exports reflects the fact that China continues to benefit from the global economy much more than the global economy benefits from China.

This is because the People’s Republic hogs more than its due share of global demand. To get why, let’s first look at how China has engineered its yawning trade surplus. As economist Michael Pettis explained in his book The Great Rebalancing, when one country rigs its economy to produce more than it consumes, it amasses extra savings that it then foists onto its trade partners. For more than a decade, this is exactly what the Chinese government has done. By keeping interest rates and the yuan artificially cheap, it suppressed its people’s purchasing power and moved money out of the hands of Chinese consumers, shifting it instead to Chinese manufacturers at artificially low rates. Thanks to these subsidies, Chinese manufacturers cut export prices, driving global competitors out of business.

That’s not the only risk it stokes.

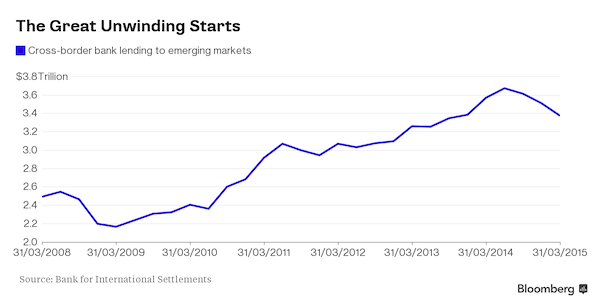

• Emerging Nations Trimming $5 Trillion Debt Stokes Currency Risk (Bloomberg)

Borrowers in emerging markets have started to address a $5 trillion mountain of dollar-denominated bonds and loans, reducing their obligations for the first time in seven years in a move that threatens to cut short a budding rally in currencies from Brazil to Malaysia. Companies in developing nations paid back $38 billion of dollar debt last quarter, $3 billion more than they borrowed in the period and marking the first reduction in net issuance since 2008, according to data compiled by Bloomberg. Demand for greenbacks among borrowers needing the currency to repay debt is contributing to the largest capital outflows in almost three decades.

The borrowing binge, which took off in the wake of the global financial crisis as interest rates tumbled, may now be reversing as economic growth slows, commodity prices fall and lenders demand higher yields. While developing-nation currencies are rebounding from their record lows, analysts surveyed by Bloomberg expect the depreciation trend to resume as dollar debt repayments accelerate. “This is a massive event,” said Stephen Jen, the co-founder of London-based hedge fund SLJ Macro Partners LLP and a former economist at the IMF whose bearish call on emerging markets since 2012 has proven prescient. “They want to pay down their dollar loans. We are early in the game, there’s pretty intense pressure on emerging markets.”

[..] In the $1.4 trillion corporate debt market, new bond sales dropped to a four-year low of $35 billion last quarter, from a peak of $121 billion in June 2014, data compiled by Bloomberg show. “When growth deteriorates, investment opportunities are naturally lower, therefore money leaves, either to repay debt or buy alternative investments elsewhere,” said Koon Chow, a strategist at Union Bancaire Privee in London and former head of emerging-market strategy at Barclays Capital. “There’s a good chance that the deleveraging does continue because on the commodity side, the reduction in capex is going to be long term.”

The Institute of International Finance forecast on Oct. 1 that about $540 billion will leave emerging markets this year, the first net capital outflow since 1988. The unwinding of dollar borrowings is more than a fleeting phenomenon, which will contribute to the weakening of emerging-market currencies against the U.S. currency, according to Pierre Lapointe at Pavilion Global Markets. The Fed’s broad measure of the dollar against major U.S. trading partners has rallied 16% since the middle of 2014 and reached a 12-year high last month. “We expect the theme of EM external deleveraging to remain with us for a long time,” Lapointe said in a note on Oct. 9. “Historically, this process tends to last many years. In this context, we are probably halfway throughout the current structural dollar uptrend.”

It’s the loss of Fed credibility more than anything.

• Federal Reserve Inaction Could Start Currency War (The Street)

Sometimes doing nothing is the same as doing something – at least, that’s how it is when it comes to the Federal Reserve not raising interest rates. The stock market stays high because the Fed is not going to raise short-term interest rates. The Fed is not going to raise short-term interest rates because the U.S. inflation rate remains low. The inflation rate remains low because the value of the U.S. dollar is high. The dollar is strong because world commodity prices have fallen and have “driven up the dollar and held down U.S. import prices.” According to the Financial Times, the last three items mentioned are interrelated. Furthermore, it now seems as if momentum is picking up within the Federal Reserve to postpone any increases in it policy rate for an extended period of time. That inaction may not be the best decision in terms of the relative strength of currencies.

At least the doves – those reluctant to raise interest rates – are making their voices heard on the issues. Yesterday, Daniel Tarullo, one of the Fed’s Governors, joined another Fed Governor, Lael Brainard, who argued on Monday that the Fed should not raise its target short-term interest rate any time soon. The value of the dollar fell. By early afternoon Wednesday, it cost around $1.145 to buy a Euro, the same rate as on Sept. 17, the day the Federal Open Market Committee decided that the Fed would keep its target short-term interest rate unchanged. The Governors believe that inflation is not going to return that quickly and that without data supporting the return of inflation toward a level closer to the Fed’s target rate of 2%, there should be no upward movement in the policy rate.

Certainly, the predictions of Fed officials don’t indicate any quick return of the economy to the Fed’s target. In these forecasts the expectation is for the inflation rate to pick up in 2016 and 2017, but a 2% inflation rate is not expected until 2018. That’s a long time. According to the Financial Times article, if the Fed doesn’t move interest rates for a long time, the value of the dollar will continue to fall. This should connect to a faster rise in inflation than is forecast by the Fed. With interest rates constant, the stock market should continue to rise. But if inflation begins to rise, the Fed will have a justification for raising short-term interest rates, which will cause the value of the dollar to increase. This will result in slowing down the inflation rate once again. According to this argument, the stock market should begin to fall because the Fed is raising interest rates.

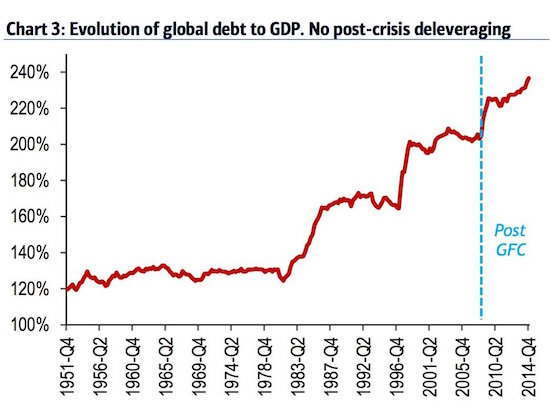

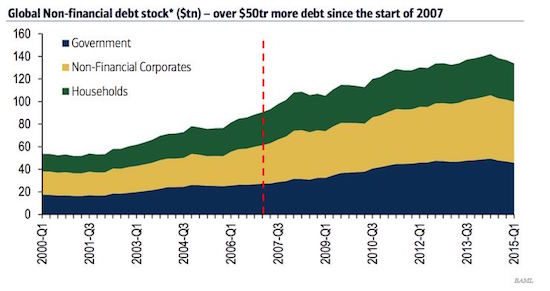

Since 2007/8: “The total stock of global debt, even excluding debts held by the financial sector, is up by more than $50 trillion. That’s an increase of more than 50%.”

• How Global Debt Has Changed Since The Financial Crisis (WEF)

Debt levels have been a subject of constant news in the years since the financial crisis — from the sub-prime housing crisis in the United States, to the eurozone sovereign debt crisis, to the dramatic increases in debt evident in emerging markets now. Graphs produced by analysts at Bank of America Merrill Lynch show an astonishing acceleration in global debt levels, and demonstrate just how little de-leveraging there’s been since the 2008 financial crisis (none). They say its evidence that “the world is still in love with debt.” After 30 years of relative stability from the early 1950s to the early 1980s, something changed, and debt started ramping up:

Debt then took a rapid step up in the mid-1980s, and another in the late 1990s. Over the last 30 years or so, global debt has risen by around 100% of GDP — so it hasn’t just grown in total terms, but has massively outstripped the economic expansion over that period. In some developed economies, like the United States, the United Kingdom and Ireland, there’s been some deleveraging since the financial crisis, particularly by households. But that’s been more than offset by increases in emerging markets. The total stock of global debt, even excluding debts held by the financial sector, is up by more than $50 trillion. That’s an increase of more than 50%.

Household debt has ticked up a little, and government debt has expanded as states attempted to stimulate their economies in the aftermath of the financial crisis. But the main increase has been down to non-financial corporate debt, which has risen by 63% over the period, largely in emerging markets.

One of many.

• Volkswagen Faces €40 Billion Lawsuit From Investors (Telegraph)

Volkswagen is set to be pushed deeper into crisis after it emerged that the carmaker is facing a record-breaking €40bn (£30bn) legal attack spearheaded by one of the world’s top law firms. Quinn Emanuel, which has won almost $50bn (£32bn) for clients and represented Google, Sony and Fifa, has been retained by claim funding group Bentham to prepare a case for VW shareholders over the diesel emissions scandal, The Sunday Telegraph can reveal. Bentham has recently backed an action by Tesco shareholders over the retailer’s overstating of profits. The pair are attempting to assemble a huge class action following what they call “fundamental dishonesty” at the German auto giant, which plunged the carmaker into crisis after it admitted using “defeat devices” to cheat pollution tests.

The admission has been hugely costly for shareholders after it wiped more than €25bn off VW’s stock market value. Recalls and fines worth tens of billions of euros more are also expected. Now Quinn Emanuel and Bentham are contacting VW’s biggest investors – which include sovereign wealth funds of Qatar and Norway – to ask them to join the claim. VW has admitted that it fitted “defeat devices” to 11m cars that allowed them to fraudulently pass pollution controls, though the company’s senior management has insisted it was unaware of the practices. Richard East, co-managing partner of Quinn Emanuel in London, said: “We estimate shareholders’ losses could be €40bn as a result of VW’s failure to provide relevant disclosure [about defeat devices] to the market and gives rise to questions about fundamental dishonesty.”

Legal action would be pursued in Germany under its Securities Trading Act, according to Quinn Emanuel, which hopes to file the first wave of actions by February. The law firm will argue that VW’s failure to reveal its use of defeat devices to shareholders constituted gross negligence by management. Mr East added that damages could be calculated from 2009 – when VW started fitting the devices to its engines – and that if investors had known about them they would not have held or traded in VW shares. “We don’t think it will be very hard to find shareholders who have suffered because of it,” he said.

Deeply embedded. There needs to be an independent investigation.

• VW Made Several Defeat Devices To Cheat Emissions Tests (Reuters)

Volkswagen made several versions of its “defeat device” software to rig diesel emissions tests, three people familiar with the matter told Reuters, potentially suggesting a complex deception by the German carmaker. During seven years of self-confessed cheating, Volkswagen altered its illegal software for four engine types, said the sources, who include a VW manager with knowledge of the matter and a U.S. official close to an investigation into the company. Spokespersons for VW in Europe and the United States declined to comment on whether it developed multiple defeat devices, citing ongoing investigations by the company and authorities in both regions. Asked about the number of people who might have known about the cheating, a spokesman at company headquarters in Wolfsburg, Germany, said: “We are working intensely to investigate who knew what and when, but it’s far too early to tell.”

Some industry experts and analysts said several versions of the defeat device raised the possibility that a range of employees were involved. Software technicians would have needed regular funding and knowledge of engine programs, they said. The number of people involved is a key issue for investors because it could affect the size of potential fines and the extent of management change at the company, said Arndt Ellinghorst, an analyst at banking advisory firm Evercore ISI. Brandon Garrett, a corporate crime expert at the University of Virginia School of Law, said federal prosecution guidelines would call for the U.S. Justice Department to seek tougher penalties if numerous senior executives were found to have been involved in the cheating. “The more higher-ups that are involved, the more the company is considered blameworthy and deserving of more serious punishment,” said Garrett.

Paper fake wealth.

• ETFs’ Rapid Growth Sparks Concern at SEC (WSJ)

The proliferation of exchange-traded funds is causing concern at the U.S. Securities and Exchange Commission, the latest sign of increased scrutiny of the popular products. Investors have piled into the funds over the past decade, attracted to the products’ low fees and issuers’ pitch that they provide exposure to a variety of asset classes while offering the chance to get in and out of positions easily. But they have been drawing scrutiny from the SEC, even before wild trading on Aug. 24 exposed problems with how the funds are set up to trade. “It seems fairly certain that the explosive growth of ETFs in recent years poses a challenge that isn’t going away—and may well become even more acute as new ETFs enter the market,” said SEC Commissioner Luis Aguilar.

The number of exchange-traded products in the U.S. has swelled by more than 60% over the past five years to 1,787 as of the end of September, according to ETFGI, a London consulting firm. And a record number of new providers launched products this year, the firm has said. Competition to list new products is ramping up. Last month, BATS Global Markets Inc. said it would start a new plan to pay ETF providers as much as $400,000 a year to list on its exchange. On Aug. 24, some funds, including ones run by the largest ETF providers, priced at steep discounts to their underlying holdings during that session. Circuit breakers halted trading more than 1,000 times of stocks and ETFs, interfering with pricing of some the funds.

“Why ETFs proved so fragile that morning raises many questions, and suggests that it may be time to re-examine the entire ETF ecosystem,” Mr. Aguilar said in his remarks. Some large ETF providers have said the tumultuous trading on Aug. 24 was partly because of market-structure issues, not the products themselves. “The events of Aug. 24 were a result of the convergence of various market structure issues, including market volatility, price uncertainty, and the use of market and stop orders,” said Vanguard Group in a statement on Friday. (Market orders are instructions to buy or sell a stock at the market price, as opposed to a specific price.) “These issues exacerbated trading difficulties with respect to some ETFs.”

“..if 10% of the loan balances of the top 100 borrowers were lowered from non-risk to risky categories, annual bank earnings would fall between 11% and 25%.”

• JPMorgan Says Bad Corporate Loans Pose Main Risk For Brazil Banks (Reuters)

A deterioration in the quality of corporate loan books poses the most obvious risk to Brazil’s largest listed banks, which are wrestling with the nation’s steepest recession in a quarter century, JPMorgan Securities said on Friday. In a report, analysts led by Saúl Martínez said the nation’s top banks are working actively with debt-laden borrowers to ease terms of their credit in order to improve loan affordability, while simultaneously asking for more guarantees. Their assessment was based on talks with industry players. Such a move comes as banks seek to mitigate the earnings impact of worsening corporate balance sheets, with the country sinking into a recession, a corruption probe at state firms and plunging confidence magnifying the current crisis. At this point, Martínez said, “a small number of loans can have a big impact” on loan-related losses at banks.

“Unexpected losses can be greater for corporate loans given that average exposures to specific borrowers are much larger,” the report said. “This is relevant as signs of financial strain in the Brazilian corporate sector are appearing.” His remarks underscore the uncertain outlook facing Brazilian banks. Brazil’s economy shrank in recent quarters and is slated to contract this year and next, the first back-to-back annual declines since the 1930s. Industrial output, retail sales and capital spending indicators have all tumbled over the past two years, with no sign of relief in the near term. According to the analysts’ estimates, if 10% of the loan balances of the top 100 borrowers were lowered from non-risk to risky categories, annual bank earnings would fall between 11% and 25%.

Human right? Who needs them?

• Revealed: How UK Targets Saudis For Top Contracts (Observer)

Government departments are intensifying efforts to win lucrative public contracts in Saudi Arabia, despite a growing human rights row that led the ministry of justice to pull out of a £6m prison contract in the kingdom last week. Documents seen by the Observer show the government identifying Saudi Arabia as a “priority market” and encouraging UK businesses to bid for contracts in health, security, defence and justice. “It’s becoming increasingly clear that ministers are bent on ever-closer ties with the world’s most notorious human rights abusers,” said Maya Foa, director of Reprieve’s death penalty team. “Ministers must urgently come clean about the true extent of our agreements with Saudi Arabia and other repressive regimes.”

The UK’s increasingly close relationship with Saudi Arabia – which observes sharia law, under which capital and corporal punishment are common – is under scrutiny because of the imminent beheading of two young Saudis. Ali al-Nimr and Dawoud al-Marhoon were both 17 when they were arrested at protests in 2012 and tortured into confessions, their lawyers say. France, Germany, the US and the UK have raised concerns about the sentences but this has not stopped Whitehall officials from quietly promoting UK interests in the kingdom – while refusing to make public the human rights concerns they have to consider before approving more controversial business deals there.

Several of the most important Saudi contracts were concluded under the obscurely named Overseas Security and Justice Assistance (OSJA) policy, which is meant to ensure that the UK’s security and justice activities are “consistent with a foreign policy based on British values, including human rights”. Foreign Office lawyers have gone to court to prevent the policy being made public. The Labour leader, Jeremy Corbyn, has written to David Cameron asking him to commit to an independent review of the use of the OSJA process. “By operating under a veil of secrecy, we risk making the OSJA process appear to be little more than a rubber-stamping exercise, enabling the UK to be complicit in gross human rights abuses,” Corbyn writes.

The UK has licensed £4bn of arms sales to the Saudis since the Conservatives came to power in 2010, according to research by Campaign Against Arms Trade. Around 240 ministry of defence civil servants and military personnel work in the UK and Saudi Arabia to support the contracts, which will next year include delivery of 22 Hawk jets in a deal worth £1.6bn. And research by the Stockholm International Peace Research Institute shows that the UK is now the kingdom’s largest arms supplier, responsible for 36% of all Saudi arms imports.

“They will be looking for horses and people in funny hats and meeting the Queen..”

• Britain Has Made ‘Visionary’ Choice To Become China’s Best Friend, Says Xi (Guardian)

Chinese president Xi Jinping praised Britain’s “visionary and strategic choice” to become Beijing’s best friend in the west as he prepared to jet off on his first state visit to the UK, taking with him billions of pounds of planned investment. The trip, Xi’s first to Britain in more than two decades, has been hailed by British and Chinese officials as the start of a “golden era” of relations which the Treasury hopes will make China Britain’s second biggest trade partner within 10 years. “The UK has stated that it will be the western country that is most open to China,” Xi told Reuters in a rare written interview published on the eve of his departure. “This is a visionary and strategic choice that fully meets Britain’s own long-term interest.”

During the four-day trip, which officially begins on Tuesday, Xi will be feted by sports and film stars, Nobel-winning scientists, members of the royal family and politicians. David Cameron and George Osborne will both accompany Xi, who Beijing describes as a football fan, to Manchester where he will visit Manchester City football club and dine at Town Hall. The Communist party leader will also address parliament. Chinese state media has predicted Britain will afford an “ultra-royal welcome” to Xi, who last set foot in the UK in 1994 when he was an official in the south-eastern city of Fuzhou. A frontpage story in the China Daily boasted that Xi’s arrival would be celebrated with a 103-gun salute – 41 in Green Park and 62 at the Tower of London.

Fraser Howie, the co-author of Red Capitalism, said Beijing would revel in the pomp and circumstance. “They will be looking for horses and people in funny hats and meeting the Queen. That plays fantastically well back in China and they make big use of that to show how important the Chinese leadership is,” he said. “It also plays to the pitch that China is now being recognised on the world stage as a great power. This is especially true in Britain’s case because it was those nasty Brits who beat them in the opium war. Now the table has turned and it is China in the ascendancy and it is Britain who is pandering to the Chinese.”

Home › Forums › Debt Rattle October 18 2015