Paul Gauguin Yellow haystacks (Golden harvest) 1889

Short is hip again.

• US Market Gurus Who Predicted Selloff Say Current Calm An Illusion (R.)

You ain’t seen nothing yet. Some veteran investors who were vindicated in calling for a pullback in shares and a spike in volatility could now be cheering. Actually, they’re looking at the risks that still lie ahead in the current relative calm. The last week’s wild market swings confirmed that the market was in correction territory – falling more than 10% from its high. The falls were triggered by higher bond yields and fears of inflation but came against a backdrop of a stretched market that had taken price/earnings levels to as high as 18.9. Adding to downwards pressure was the unwinding of bets that volatility would stay low. The fall had come after a growing number of strategists and investors said a pullback was in the offing – although the consensus opinion was that the market would then start rising again. The big question is: what comes now?

“Do you honestly believe today is the bottom?” said Jeffrey Gundlach, known as Wall Street’s Bond King, last week, who had been warning for more than a year that markets were too calm. Gundlach had been particularly vocal in his warnings about the VIX, Wall Street’s “fear gauge,” which tracks the volatility implied by options on the S&P 500. The sell-off in U.S. stocks derailed some popular short volatility exchange-traded products, which contributed to more downwards pressure on the market. Gundlach in May last year warned that the VIX was “insanely low.” Hedge fund manager Douglas Kass was short SPDR S&P 500 ETF and said he “took a lot of small losses” last year but says he still sees more stress ahead. He said he is now re-shorting that ETF. Investors who bet low volatility would continue will need time to unwind their strategies, Kass said.

[..] Veteran short-seller Bill Fleckenstein, who ran a short fund but closed it in 2009, said that “last week’s action was an early indication that the end of bull market is upon us.” Fleckenstein said there was a lot of money in the market with no conviction behind it, for example, buying index funds and ETFs just “to be part of the party” which was an element of “hot money.” “Last week was just the preview to the bigger event that we’ll see this year probably,” Fleckenstein said. Fleckenstein said he is not short at the moment – although he did make “a couple of bucks” last week shorting Nasdaq futures. He said he is looking for an opportunity to get short again. He said he has “flirted with the idea of restarting a short fund”.

The US is betting big. But don’t let that blind you to the fact that so is everyone else.

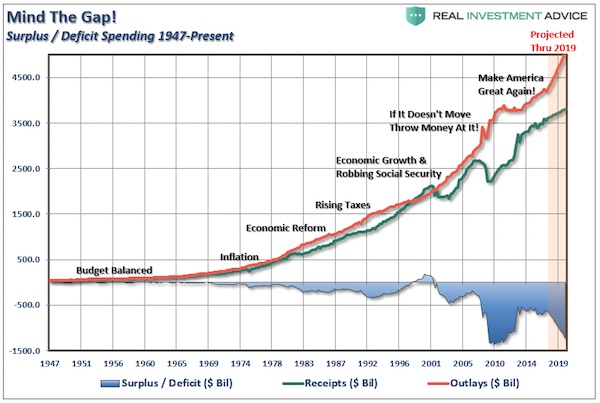

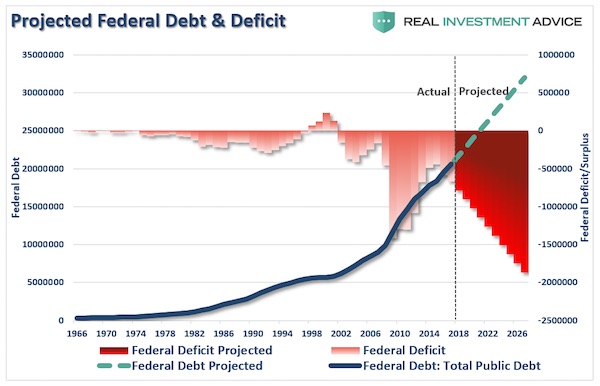

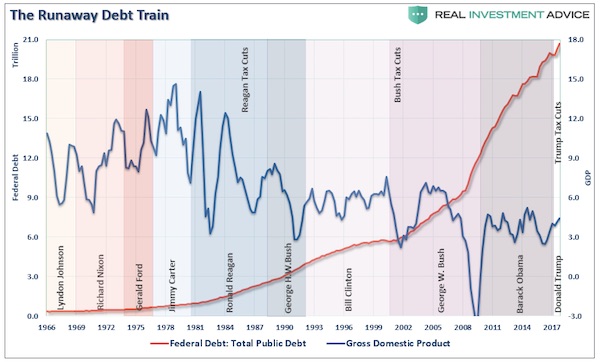

• There Will Be No Economic Boom (Roberts)

Last week, Congress passed a 2-year “continuing resolution, or C.R.,” to keep the Government funded through the 2018 elections. While “fiscal conservatism” was just placed on the sacrificial alter to satisfy the “Re-election” Gods,” the bigger issue is the impact to the economy and, ultimately, the financial markets. The passage of the $400 billion C.R. has an impact that few people understand. When a C.R. is passed it keeps Government spending at the same previous baseline PLUS an 8% increase. The recent C.R. just added $200 billion per year to that baseline. This means over the next decade, the C.R. will add $2 Trillion in spending to the Federal budget. Then add to that any other spending approved such as the proposed $200 billion for an infrastructure spending bill, money for DACA/Immigration reform, or a whole host of other social welfare programs that will require additional funding.

But that is only half the problem. The recent passage of tax reform will trim roughly $2 Trillion from revenues over the next decade as well. This is easy math. Cut $2 trillion in revenue, add $2 trillion in spending, and you create a $4 trillion dollar gap in the budget. Of course, that is $4 Trillion in addition to the current run rate in spending which continues the current acceleration of the “debt problem.”

But it gets worse. As Oxford Economics reported via Zerohedge: “The tax cuts passed late last year, combined with the spending bill Congress passed last week, will push deficits sharply higher. Furthermore, Trump’s own budget anticipates that US debt will hit $30 trillion by 2028: an increase of $10 trillion.” Oxford is right. In order to “pay for” all of the proposed spending, at a time when the government will receive less revenue in the form of tax collections, the difference will be funded through debt issuance.

Simon Black recently penned an interesting note on this: “Less than two weeks ago, the United States Department of Treasury very quietly released its own internal projections for the federal government’s budget deficits over the next several years. And the numbers are pretty gruesome. In order to plug the gaps from its soaring deficits, the Treasury Department expects to borrow nearly $1 trillion this fiscal year. Then nearly $1.1 trillion next fiscal year. And up to $1.3 trillion the year after that. This means that the national debt will exceed $25 trillion by September 30, 2020.”

Of course, “fiscal responsibility” left Washington a long time ago, so, what’s another $10 Trillion at this point? While this issue is not lost on a vast majority of Americans that “choose” to pay attention, it has been quickly dismissed by much of the mainstream media, and Congressman running for re-election, by suggesting tax reform will significantly boost economic growth over the next decade. The general statement has been: “By passing much-needed tax reform, we will finally unleash the economic growth engine which will more than pay for these tax cuts in the future.”

Nobody expects the bond vigilantes?!

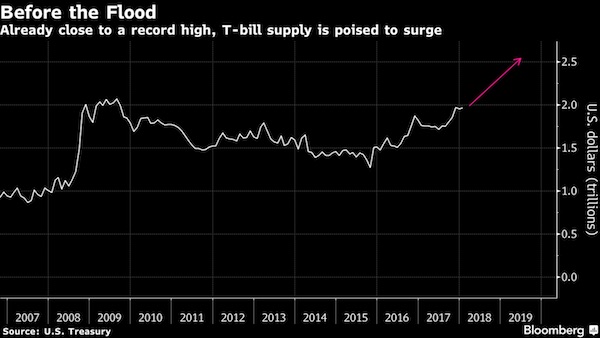

• T-Bills Flood Set to Put Upward Pressure on Short-Term Funding Costs (BBG)

Get ready for the deluge of Treasury bills, and the increase in short-term funding costs that’s likely to accompany it. Investors are bracing for an onslaught of T-bill supply following last week’s U.S. debt ceiling suspension. That’s already prompting them to demand higher rates from borrowers across money markets. And that’s just a result of the government replenishing its cash hoard to normal levels. The ballooning budget deficit means there’s even more to come later, and that deluge of supply could further buoy funding costs down the line, making life more expensive both for the government and companies that borrow in the short-term market. Concerns about the U.S. borrowing cap had forced the Treasury to trim the total amount of bills it had outstanding, but that’s no longer a problem and the government is now busy ramping up issuance.

Financing estimates from January show that the Treasury expects to issue $441 billion in net marketable debt in the current quarter and the bulk of that is likely to be in the short-term market. “Supply will come in waves and we’re in a very heavy wave right now,” said Mark Cabana at Bank of America. “If you take Treasury at their word that they want to issue $300 billion in bills, that’s a lot of net supply that needs to come to market.” Next week’s three- and six-month bill auctions will be the largest on record at $51 billion and $45 billion respectively, Treasury said Thursday. The four-week auction will be boosted to $55 billion next week, having already been lifted to $50 billion for the Feb. 13 sale. Auction volume at the tenor had earlier been shrunk to just $15 billion.

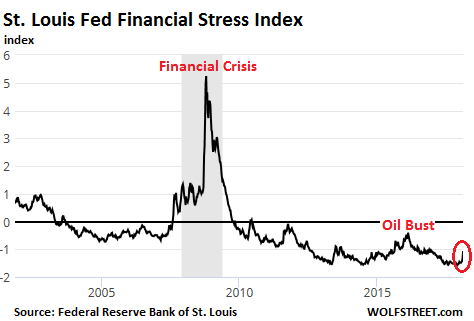

Spikes but is still negative. Wait till that changes.

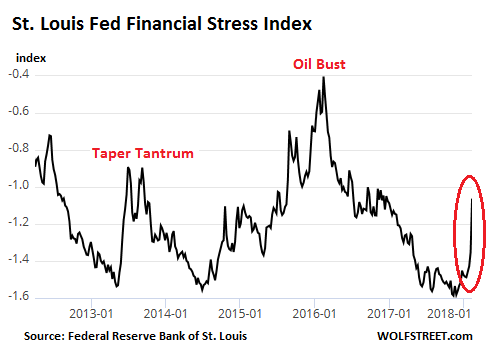

• “Financial Stress” Spikes – Just As The Fed Intends (WS)

The weekly St. Louis Fed Financial Stress index, released today, just spiked beautifully. It had been at historic lows back in November, an expression of ultra-loose financial conditions in the US economy, dominated by risk-blind investors chasing any kind of yield with a passion, which resulted in minuscule risk premiums for investors and ultra-low borrowing costs even for even junk-rated borrows. The index ticked since then, but in the latest week, ended February 9, something happened. The index, which is made up of 18 components (seven interest rate measures, six yield spreads, and five other indices) had hit a historic low of -1.6 on November 3, 2017, even as the Fed had been raising its target range for the federal funds rate and had started the QE Unwind. It began ticking up late last year, hit -1.35 a week ago, and now spiked to -1.06.

The chart above shows the spike of the latest week in relationship to the two-year Oil Bust that saw credit freeze up for junk-rated energy companies, with the average yield of CCC-or-below-rated junk bonds soaring to over 20%. Given the size of oil-and-gas sector debt, energy credits had a large impact on the overall average. The chart also compares today’s spike to the “Taper Tantrum” in the bond market in 2014 after the Fed suggested that it might actually taper “QE Infinity,” as it had come to be called, out of existence. This caused yields and risk premiums to spike, as shown by the Financial Stress index. This time, it’s the other way around: The Fed has been raising rates like clockwork, and its QE Unwind is accelerating, but for months markets blithely ignored it. Until suddenly they didn’t.

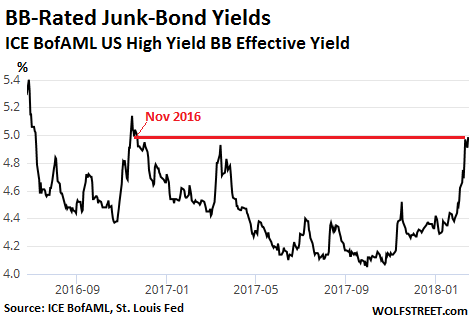

This reaction is visible in the 10-year Treasury yield, which had been declining for much of last year, despite the Fed’s rate hikes, only to surge late in the year and so far this year. It’s also visible in the stock market, which suddenly experienced a dramatic bout of volatility and a breathless drop from record highs. And it is now visible in other measures, including junk-bond yields that suddenly began surging from historic low levels. The chart of the ICE BofAML US High Yield BB Effective Yield Index, via the St. Louis Fed, shows how the average yield of BB-rated junk bonds surged from around 4.05% last September to 4.98% now, the highest since November 20, 2016:

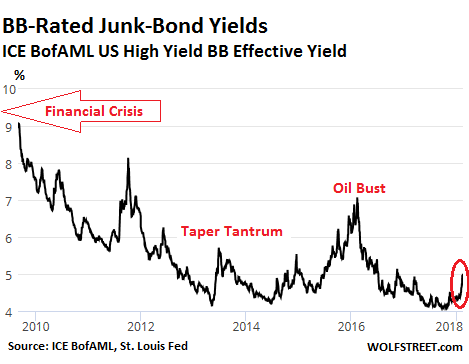

But a longer-term chart shows just how low the BB-yield still is compared to where it had been in the years after the Financial Crisis, and how much more of a trajectory it might have ahead:

The Financial Stress Index is designed to show a level of zero for “normal” financial conditions. When these conditions are easy and when there is less financial stress than normal, the index is negative. The index turns positive when financial conditions are tighter than normal. But at -1.06, it remains below zero. In other words, financial conditions remain extraordinarily easy. This is clear in a long-term chart of the index that barely shows the recent spike, given the magnitude of prior moves. This is precisely what the Fed wants to accomplish.

Feels a bit like Soros vs Britain in 1992.

• Hedge Fund King Dalio Bets Big Against Europe (BBG)

Ray Dalio, billionaire philosopher-king of the world’s biggest hedge fund, has a checklist to identify the best time to sell stocks: a strong economy, close to full employment and rising interest rates. That may explain why the firm he created, Bridgewater Associates, has caused a to-do the past two weeks by quickly amassing an $21.65 billion bet against Europe’s biggest companies. The firm’s total asset pool is $150 billion, according to its website. Economic conditions in Europe appear to fit Dalio’s requirements. Last year, the continent’s economy grew at the fastest pace in a decade, and ECB President Mario Draghi has indicated he’s on a slow path toward boosting rates as economic slack narrows. Factories around the world are finding it increasingly hard to keep up with demand, potentially forcing them to raise prices.

But Dalio is leading his firm down a path that few other funds care to tread. Renaissance Technologies, most recently famous for its association with Breitbart donor Robert Mercer, is only $42 million short in Europe. Two Sigma Investments is betting even less than that. Kenneth Griffin’s Citadel has less than $2 billion in European company shorts. So Dalio will rise or fall virtually on his own. “It is not unusual to see strong economies accompanied by falling stock and other asset prices, which is curious to people who wonder why stocks go down when the economy is strong and don’t understand how this dynamic works,” Dalio wrote in a LinkedIn post this week. Bridgewater’s shorting spree started last fall in Italy. With the country’s big banks accumulating billions in bad debt, Bridgewater mounted a $770 million wager against Italian financial stocks.

Saddled with non-performing loans and under constant regulatory scrutiny, they made for a juicy target. Throughout the fall and into winter the bet against Italy represented the majority of Bridgewater’s publicly disclosed short positions. The initial bet was eventually raised to encompass 18 firms and nearly $3 billion. Bridgewater had flipped its portfolio in January to turn bearish on Western Europe stocks and also started shorting Japanese equities, according to a person with knowledge of the matter. The hedge fund significantly raised its long U.S. equities exposure last month, the person added.

“This market is nuts.”

• Everybody’s Already Invested, So Who’s The Buyer? (ZH)

With stocks erasing their early-day losses and the VIX tumbling once again, CNBC – the go-to resource for retirees and other retail investors – was back to reassuring investors that this month’s explosion of volatility was just another dip deserving to be bought. But Embark Capital CIO Peter Toogood offered an important counterpoint during an appearance this morning where he warned his audience against exactly this kind of credulousness by ignoring the fundamental growth global growth story that seemingly every other portfolio manager has been relying on and instead pointing to one simple fact: “Everybody is already invested”.

But even with positioning stretched to such an exaggerated degree, that doesn’t necessarily mean a crash is right around the corner. Instead, Toogood foresees a “step bear market” that will continue until the PPT, newly reconstituted under the leadership of Jerome Powell, realizes that they must once again intervene…because with so much systemic debt and myriad other risks – like the dangerously underfunded pensions that we’ve highlighted again and again – a sustained selloff would be far too risky to countenance. “I noticed Dudley the other day say ‘this is small potatoes’ and warning investors not to worry about it. And I would accept that’s all true, if everybody wasn’t already invested. And I want to know who the marginal buyer of this story is. Everyone is in. Look at consumer sentiment surveys, loo at professional money managers, everyone is in. So who’s the buyer? It’s very 2007-2008.”

He added that hedge fund managers are now “sitting around scratching their heads” because even European high yield bonds – the debt of some of the worst companies on Earth – are yielding a staggeringly low 2%. Toogood also pointed out that stocks are breaking through important technical levels… “You’re breaking some very major levels in most markets outside of the US still, and that is very, very significant. That is the test of where you’d think a bear market is coming; I still do, just on valuation alone. I think this market is nuts,” Toogood said. Which is leaving asset managers in a bind… “It’s one of those extremely unpleasant moments when people need income but income is expensive and that’s the other problem we see … We are forced into high yield (bonds) and we don’t want to be there,” Toogood said.’

“..our currency, but your problem..”

• Donald Trump’s Dangerous Currency Game (Spiegel)

“There is no longer any doubt that the U.S. government is not only waging a currency war, but is also in the process of winning it,” Joachim Fels, chief economist at Pimco, says. Trump’s policies represent a threat to Europe’s recovery, a situation that has displeased the ECB. But there isn’t much the ECB can do about it. By pursuing economic policies that ignore the needs of America’s trading partners – an approach economists refer to as “beggar-thy-neighbor” – Trump has revisited an old American tradition. In the early 1970s, it was Treasury Secretary John Connally who raised the prospect of a budget deficit of $40 billion – a massive sum at the time – and justified it as “fiscal stimulus.” In response to concerns voiced by his European counterparts, worried as they were about the weak dollar, he responded with his legendary line that the dollar “is our currency, but your problem.”

Lloyd Bentsen, treasury secretary under Bill Clinton, informed the Japanese in 1993 that he urgently desired a stronger yen in order to stem the Asian trading partner’s high export surpluses. With “America First,” Trump has now elevated “beggar thy neighbor” to the status of administration doctrine. The first part of Trump’s economic policy agenda envisions stimulating the economy through tax cuts and public infrastructure investments. That would help American companies, and the rest of the world could also profit initially if the U.S. economy were to grow more rapidly and companies in Europe or Asia were to receive more orders. But it’s the second part of the Trump program that reveals the real strategic thrust.

During the same weak that the treasury secretary could be heard preaching the virtues of a weak dollar, the U.S. government imposed steep import tariffs on washing machines and solar cells. The combination of a weak dollar and protectionist measures are aimed at creating a competitive advantage for American companies versus their competitors from around the world. “The government clearly wants a weak dollar right now because inflation is moderate and a weaker dollar will make it easier for the manufacturing sector to grow,” says Barry Eichengreen, a professor for economics at the University of California at Berkeley.

Europe will have to act. Simple as that.

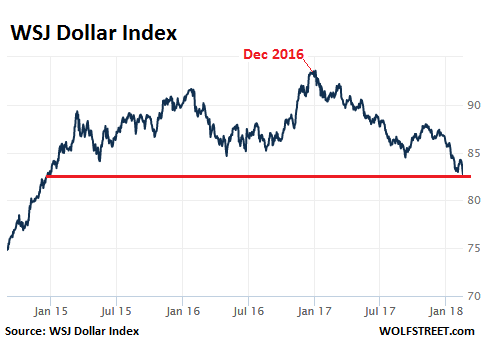

• US Dollar Spirals Down, Hits Lowest Point Since 2014 (WS)

The US dollar has dropped 2.0% in the past five days, 2.4% over the past month, 4.1% year-to-date, 5.3% over the past three months, and 9.4 % over the past 12 months, according to the WSJ Dollar Index. At 82.47, the index is at the lowest level since December 25, 2014: The index weighs the US dollar against a basket of 16 other currencies that account for about 80% of the global currency trading volume: Euro, Japanese Yen, Chinese Yuan, British Pound, Canadian Dollar, Mexican Peso, Australian Dollar, New Zealand Dollar, Hong Kong Dollar, South Korean Won, Swiss Franc, Swedish Krona, Singapore Dollar, Indian Rupee, Turkish Lira, and Russian Ruble. The currencies are weighted based on their foreign exchange trading volume.

Whatever the reasons may be for the decline of the dollar against this basket of currencies — everyone has their own theory, ranging from the much prophesied death of the dollar to Treasury Secretary Steve Mnuchin’s actively dissing the dollar at every opportunity he gets — one thing we know: The decline started in late December 2016, after the index had peaked at 93.50. And it has not abated since. With the index currently at 82.47, it has fallen nearly 12% over those 14 months. The dominant factor in the decline of the dollar index is the strength of the euro, the second largest currency. Over those 14 months, the euro, which had been given up for dead not too long ago, has surged 20% against the dollar. The decline of the dollar is another indication that markets have blown off the Fed, similar to the 10-year Treasury yield falling for much of last year, even as the Fed was raising its target range for the federal funds rate.

The Fed keeps an eye on the dollar. A weak dollar makes imports more expensive and, given the huge trade deficit of the US, adds to inflationary pressures in the US. Over the past few years, the Fed has practically been begging for more inflation. So for the Fed, which is chomping at the bit to raise rates further, the weak dollar is a welcome sight. Conversely, a surging dollar would worry the Fed. At some point it would get nervous and chime in with the chorus emanating from the Treasury Department and the White House trying to talk down the dollar. If the dollar were to surge past certain levels, and jawboning isn’t enough to knock it down, the Fed might alter its monetary policies and might back off its rate-hike strategies or it might slow down the QE Unwind.

“For 25- to 34-year-olds earning between £22,200 and £30,600 per year, home ownership fell to just 27% in 2016 from 65% two decades ago” Good luck trying to find buyers.

• Home Ownership Among Britain’s Young Adults Has ‘Collapsed’ (G.)

The chances of a young adult on a middle income owning a home have more than halved in the past two decades. New research from the Institute for Fiscal Studies shows how an explosion in house prices above income growth has increasingly robbed the younger generation of the ability to buy their own home. For 25- to 34-year-olds earning between £22,200 and £30,600 per year, home ownership fell to just 27% in 2016 from 65% two decades ago. Middle income young adults born in the late 1980s are now no more likely than those lower down the pay scale to own their own home. Those born in the 1970s were almost as likely as their peers on higher wages to have bought their own home during young adulthood.

Andrew Hood, a senior research economist at the IFS, said: “Home ownership among young adults has collapsed over the past 20 years, particularly for those on middle incomes.” The IFS said young adults from wealthy backgrounds are now significantly more likely than others to own their own home. Between 2014 and 2017 roughly 30% of 25- to 34-year-olds whose parents were in lower-skilled jobs such as delivery drivers or sales assistants owned their own home, versus 43% for the children of those in higher-skilled jobs such as lawyers and teachers. The study shows the growing disparities between rich and poor, as well as young and old, across the country. It also illustrates the drop in home ownership over the past decade. While those on middle incomes have seen the largest fall in ownership rates, those in the top income bracket have been least affected.

Who needs capitalism when you can worship the golden calf?

Long article in a new series at the Nation.

• Warren Buffett, Prime Example Of The Failure Of American Capitalism (Dayen)

Warren Buffett should not be celebrated as an avatar of American capitalism; he should be decried as a prime example of its failure, a false prophet leading the nation toward more monopoly and inequality. You probably didn’t realize that the same avuncular billionaire controls such diverse companies and products as See’s Candies, Duracell batteries, Justin Boots, Benjamin Moore Paints, and World Book encyclopedias. But Buffett has transformed Berkshire Hathaway, initially a relatively small textile manufacturer, into the world’s largest non-technology company by market value. Berkshire Hathaway owns over 60 different brands outright. And through Berkshire, Buffett also invests in scores of public corporations. The conglomerate closed 2016 with over $620 billion in assets.

The money mainly comes from Berkshire’s massive insurance business, composed of the auto insurer GEICO, the global underwriter General Reinsurance Corporation, and 10 other subsidiaries. Insurance premiums don’t get immediately paid out in claims; while the cash sits, Buffett can invest it. This is known as “float,” and Berkshire Hathaway’s float has ballooned from $39 million in 1970 to approximately $113 billion as of last September. It’s a huge advantage over rival investors—effectively the world’s largest interest-free loan, helping to finance Buffett’s pursuit of monopoly. “[W]e enjoy the use of free money—and, better yet, get paid for holding it,” Buffett said in his most recent investor letter. Indeed, as a 2017 Fortune article noted, with almost $100 billion in cash at the end of that year’s second fiscal quarter, Buffett’s Berkshire Hathaway literally has more money than it knows what to do with.

The dominant narrative around Buffett is that he invests in big, blue-chip companies whose products he enjoys, like Coca-Cola or Heinz ketchup. But Buffett’s taste for junk food cannot match his hunger for monopoly, and he scours the investment landscape to satisfy it.

Monopoly contradicts capitalism. Well, in theory, that is.

• Monopolies Game the System (Nation)

More than a century ago, Elizabeth Magie developed two sets of rules for a board game that would become known as Monopoly. There’s the one we know today: You play an aspiring real-estate tycoon, buying up properties to extract ever-larger sums from your opponents; you win when everyone else is destitute. But in Magie’s version, players could agree to switch midgame to a second rule book. Instead of paying rent to a landowner, they’d send funds to a common pot. The game would be over when the poorest player doubled their capital. Magie’s goal was to show the cruelty of monopoly power and the moral superiority of progressive taxation. Her board game was a rebuke to the slumlords and corporate giants of the Gilded Age.

Today, a few corporations once again dominate sectors of our economy. In an interview with The Nation’s George Zornick, Senator Elizabeth Warren points out that two companies sell 70% of the beer in the country; four companies produce 85% of American beef; and four airlines account for 80% of domestic seats. With monopolies squeezing out the competition and underpaying workers, profits are funneled to a tiny elite. It’s no coincidence that the three richest Americans—Amazon’s Jeff Bezos, Microsoft’s Bill Gates, and Berkshire Hathaway’s Warren Buffett—are together worth slightly more than the bottom half of the entire US population.

Just as railroad monopolies once controlled the crucial infrastructure of 19th-century commerce, tech companies are trying to own the infrastructure of the 21st. As Stacy Mitchell explains in “The Empire of Everything,” Amazon is not only the leading retail platform, but it has developed a vast distribution network to handle package delivery. Amazon announced in February that it would begin testing its own delivery service, which could soon rival UPS and FedEx. It also runs more than a third of the world’s cloud-computing capacity, handling data for the likes of Netflix, Nordstrom, and The Nation. Unlike past monopolies, however, Amazon doesn’t want to dictate to the market; it seeks to replace the market entirely.

Under these conditions, small businesses and start-ups are struggling to compete. In 2017, there were approximately 7,000 store closings—more than triple the number in the prior year. And the percentage of companies in the United States that are new businesses has dropped by nearly half since 1978. In many industries, starting a new business is like playing Monopoly when all the squares have already been purchased: Everywhere you land, there’s a monopolist making demands, everything from fees to sell items on its website to the release of data with which to undercut you later.

EU and US better act. Greece will start shooting soon. They have a formidable army.

• Greece Warns Turkey Of Non-Peaceful Response Next Time (K.)

Athens toughened up its stance on Turkish action in the eastern Aegean, with the foreign minister and the government spokesman making it clear to Ankara that Greece’s response to another incident will not be peaceful. Foreign Minister Nikos Kotzias said in an interview on Alpha TV late on Thursday that the incident on Monday, when a Turkish vessel rammed a Greek one off Imia island, “touched on the red line and in some sense it overstepped it.” He went on to add that there will not be another such peaceful behavior by the Greek side should such an incident recur.

Kotzias also clarified that “Imia is Greek” and warned Ankara “you should not open a gray-zone issue, because if we do, based on international law, not only are you wrong but you will also incur losses.” Government spokesman Dimitris Tzanakopoulos echoed Kotzias on Friday morning, warning that aggression will be met with an equal response. “If there is another act of Turkish aggression on Greek territory, there will be a response and there is no other way for us,” he told Skai TV. Greece’s verbal toughening comes as the Turkish armed forces conducted an extensive war game near the Greek-Turkish land border by Evros river in Thrace, including the scenario of crossing a river to invade a neighboring country.

Words cannot express the sadness. Once we’ve eradicated the man of the woods, man is next.

• Borneo Has Lost Half Its Orangutans This Century (Ind.)

Borneo has lost more than 100,000 orangutans in the space of just 16 years as a result of hunting and habitat loss, according to a new report. Logging, mining, oil palm, paper, and linked deforestation have been blamed for the the diminishing numbers. However, researchers also found many orangutans have vanished from more intact, forested regions, suggesting that hunting and other direct conflict between orangutans and humans continues to be a chief threat to the species. The report published in the Current Biology Journal found more than 100,000 of the island’s orangutans vanished in the period of 1999 to 2015. “Orangutans are disappearing at an alarming rate,” said Emma Keller, agricultural commodities manager at the Worldwide Fund for Nature (WWF).

“Their forests homes have been lost and degraded, and hunting threatens the existence of this magnificent great ape. “Immediate action is needed to reform industries that have pushed orangutans to the brink of extinction. UK consumers can make a difference through only supporting brands and retailers that buy sustainable palm oil.” Around half of the orangutans living on the island of Borneo, the largest island in Asia, were lost as a result of changes in land cover. [..] The report comes after an orangutan was shot at least 130 times with an air gun before it died earlier in the month, according to police in Borneo.

Home › Forums › Debt Rattle February 16 2018