Ben Shahn Sideshow, county fair, central Ohio 1938

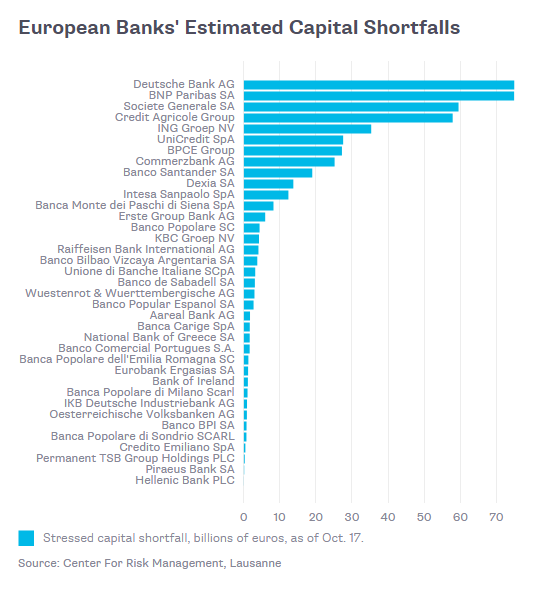

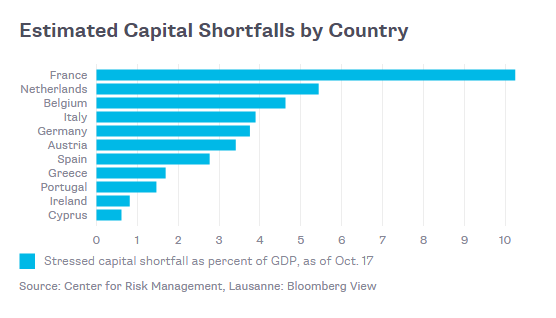

“That sum is not far away from the present market capitalisation of these banks, implying that they are massively overexposed.”

• UK’s Four Biggest Banks £155 Billion Short Of Safety (Ind.)

The UK’s four biggest banks would need to raise another £155bn in fresh capital to withstand a new financial crisis, despite the view of the Bank of England Governor that lenders have an adequate cushion to cope with further turmoil. Those are the results of research from three respected financial academics – and add to a growing feeling that the Bank of England is dangerously undercooking its capital requirements on UK lenders in the face of swelling instability in financial markets. UK banks had to be rescued in 2008 and 2009 at massive cost to British taxpayers. Capital represents the shareholder funds in banks available to absorb losses. When losses are greater than the capital cushion the bank is bust and may need to tap state support if deemed to be systemically important by politicians and regulators.

In a new paper Viral Acharya of New York University, Diane Pierret of the University of Lausanne and Sascha Steffen of the University of Mannheim calculate that HSBC, Barclays, Lloyds and the Royal Bank of Scotland would need to raise $185bn (£155bn) of new equity between them to retain a 5.5% capital cushion in a crisis, which is the benchmark of safety used in the past by the European Banking Authority. That sum is not far away from the present market capitalisation of these banks, implying that they are massively overexposed. The EBA’s stress test exercise last Friday showed the UK’s major lenders would see their capital diminished in another European economic crisis, but not below the 5.5% level of so-called “risk-weighted assets” that would have created pressure for more equity injections.

[..] Acharya, Pierret and Steffen argue that the broader European banking sector could be undercapitalised to the tune of around €890bn – a figure they calculated using stock market valuations of banks’ equity rather than the sums reported by lenders themselves. Bank share prices have continued to fall since last Friday’s EBA stress test, implying investors are far from reassured by the fact that most lenders received a clean bill of health from the regulators.

Would it even help anymore?

• Want To Avoid Recession? Then Shower UK Households With Cash (G.)

Just give people the money. Give them cash, dole it out, increase benefits, slash VAT, hand it to those most likely to spend it: the poor. Put £1,000 into every debit account. Whatever you do, don’t give it to banks. They will just hoard it or use it to boost house prices. Britain is suffering from a classic liquidity trap. There is insufficient demand. Yet all the Bank of England did on Thursday was wring its hands, blame Brexit and go on digging the same old holes. They are labelled lower interest rates, quantitative easing and more cash for banks. Those policies have been in place for some seven years. They have failed, failed, failed. Not one commentator yesterday thought cutting interest rates to 0.25% would make any difference to the threat of recession.

Worse, by cutting annuity yields it would impoverish many old people who would otherwise spend. The Bank’s cumbersome monetary bureaucracy was set up to keep inflation under control by curbing bank lending. That failed during the credit crunch. Now it is failing in the opposite direction. Channelling policy through the banks has proved useless in protecting the economy from deflation and recession. The Bank is trapped intellectually in the world in which it lives, that of the City and the banking system. Like chateau generals at the Somme, it never ventures to the economy’s frontline, where buyers meet sellers and generate growth. It thinks of bonds, investments and the only glamour spending it recognises, on infrastructure. It believes that an economy can be regenerated through middle-class home ownership and state mega-projects.

But there is no shortage of funds to invest. Companies, like banks, are awash in cash. The problem is that savers are not spending; if they spend on anything it is on property, and that, too, may now slide. It is irresponsible to await the chancellor’s autumn statement and a political fiddle with tax rates. The engine of the economy must crash into forward gear. Money must be got into bank accounts, cash cards, shops tills and revenues. The plea from 35 economists published in the Guardian this week for “unconventional measures” made only one mistake. It suggested more spending on state infrastructure, which is just spending delayed. Where the economists were right was in suggesting “an immediate increase in household disposable incomes”.

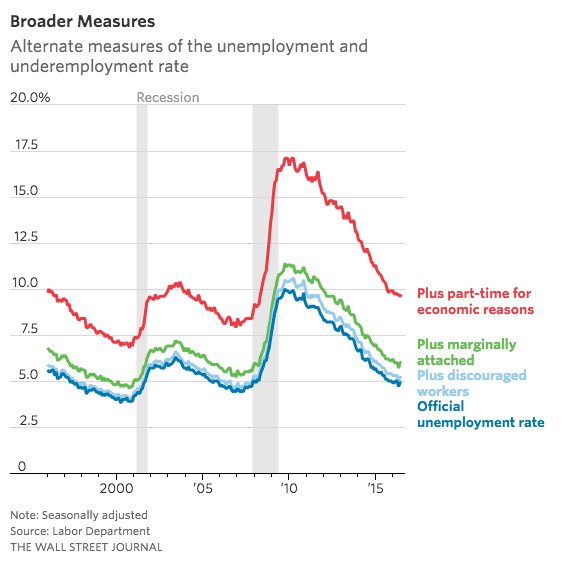

“..the U-6 unemployment number is 10.7% of the nation’s workforce..”

• A Realistic Look at July’s Nonfarm Payrolls (M2)

The Bureau of Labor Statistics (BLS) released its nonfarm payroll data this morning, showing that 255,000 jobs were created in July. The unemployment rate remained at 4.9%. May data was revised up from the eyebrow-raising low number of 11,000 jobs to 24,000 jobs while June was also revised upward from 287,000 jobs to 292,000. That brought the monthly average to 190,000 jobs over the past three months. Unfortunately, drilling down into the more granular details, a far less rosy picture emerges; a picture which is far more consistent with an economy feeling the continued weight of unprecedented wealth and income inequality; a picture that is far more correlated to an economy where “58% of all new income since the Wall Street crash has gone to the top 1%,” to quote Senator Bernie Sanders.

The data for July shows that the U-6 unemployment number is 10.7% of the nation’s workforce, more than double the official number of 4.9%. The U-6 unemployment rate includes the number of people unemployed; plus individuals just marginally attached to the labor force; plus those employed part-time for economic reasons. (The Bureau of Labor Statistics provides the following definition of marginally attached: “Persons marginally attached to the labor force are those who currently are neither working nor looking for work but indicate that they want and are available for a job and have looked for work sometime in the past 12 months. Discouraged workers, a subset of the marginally attached, have given a job-market related reason for not currently looking for work.)

But a far bigger problem with the BLS data is what constitutes an “employed” worker to our Federal government’s numbers crunchers. According to the Bureau of Labor Statistics, you could be an out of work MBA graduate but if you help your brother in his deli for 15 hours in a week while living in his home, you’re counted as employed. (The BLS says that a worker who makes no money at all donating his or her services to a family business for 15 hours or more per week is considered employed.)

The US keeps addding more people than jobs.

• The Politically Incorrect Jobs Numbers Everyone is Hushing Up (WS)

On its population clock, the Census Bureau estimates that the US population on August 5, 2016, at 4:49 p.m. ET (yup, down to the minute) was 324.17 million. That’s up from 308.76 million in April 2010. Since the darkest days of the Great Recession, the US population has grown by 15.4 million. The Census Bureau also estimates that there are currently 8.6 births per minute, minus 4.6 deaths per minute, plus 2 arriving immigrants (“net”) per minute, for a gain of nearly 6 folks per minute. Everyone ages, so the young ones move into the labor force, but the baby boomers are fit and healthy and don’t feel like retiring, and so they hang on to their jobs for as long as they can, despite the rampant age discrimination they face in many sectors, particularly in tech, though obviously not in politics.

In 2010, 24% of the people were under 18. That was 74 million people. Millions of them have since moved into the labor force, elbowing each other while scrambling for jobs, as have those millions who were then between 18 and their twenties and in college or grad school. These millennials have arrived on the job market in very large numbers. In April 2010, there were 130.1 million nonfarm payrolls. In today’s July report, there were 144.4 million. Hence, 14.3 million jobs have been added to the economy over the time span, even as the total population has grown by 15.4 million. So that’s not working out very well. On average, 205,300 jobs need to be created every month just to keep up with population growth and not allow the unemployment situation to get worse.

Maybe they should be forced to pay back all their clients and close?

• Hacked Bitcoin Firm Plans To Spread Losses Across All Users (CNBC)

The bitcoin exchange Bitfinex has said it is considering sharing losses among all its users after around $70 million worth of bitcoin was stolen earlier in the week. “We are still working out the details so nothing is set in stone, however we are leaning towards a socialized loss scenario among bitcoin balances and active loans to (bitcoin/dollar) positions,” the Hong-Kong based company said on its website on Friday. Bitfinex revealed it had been hacked on Tuesday and suspended trading, causing prices of the digital currency to fall significantly. A total of 119,756 bitcoins, worth $68 million at current prices, were reportedly stolen as a result of a security breach.

The company added in its latest statement that nothing had yet been decided and it was still settling positions and account balances. Bitfinex’s “socialized loss scenario” most likely means it will distribute its losses among all of the platform’s users, according to Charles Hayter, chief executive and founder of digital currency comparison website CryptoCompare. This would mean users whose bitcoins were never originally stolen would be affected. “In essence, (this is) a haircut for all users on their deposits. To what degree depends on the devil in the details and what the total capital held by BitFinex is,” Hayter told CNBC via email.

A heavily indebted company gets permission to open a bank, to rival another bank that has 25% of its loans off-balance-sheet and non-performing. What could go wrong?

• In China, When in Debt, Dig Deeper (WSJ)

When the going gets tough in China, just get a bank. With profits headed south, heavily indebted Chinese heavy-machinery giant Sany Heavy Industries said this week it won approval to set up a bank in the Hunan province city of Changsha. With 3 billion yuan ($450 million) of registered capital, it will be a relatively large institution as Chinese city-based banks go. Sanyplans to join forces with a pharmaceutical company and an aluminum company.

In recent months several city commercial banks in China have been taken over by the likes of tobacco and travel companies, recapitalized and renamed. Banking licenses are scarce in China, and rarely are new banks set up from scratch. Sany’s Sanxiang Bank will be up and running in six months. It will go up against crosstown rival Bank of Changsha, which at the end of last year had substantial 90 billion yuan book of off-balance-sheet loans, more than a quarter of them nonperforming. Sany had better ramp up quickly.

Comment on the WSJ piece above.

• Only In China: Companies Become Banks To ‘Solve’ Financial Difficulties

China is desperate to solve several problems it has due to its debt to GDP ratio being north of 300%. It may have found a pretty unconventional one by letting companies become banks, according to a report by the Wall Street Journal. “With profits headed south, heavily indebted Chinese heavy-machinery giant Sany Heavy Industries said this week it won approval to set up a bank in the Hunan Province city of Changsha. With 3 billion yuan ($450 million) of registered capital, it will be a relatively large institution as Chinese city-based banks go. Sany plans to join forces with a pharmaceutical company and an aluminum company. Sany already operates an insurance and finance division with the goal of internal financing and insurance services for clients.”

One problem is that companies are defaulting on bond payments and there is no adequate resolution mechanism for bad debts, at least according to Goldman Sachs. “A clearer debt resolution process (for example, how debt restructuring on public bonds can be achieved, how valuation and recovery on defaulted bonds are arrived at, the timely disclosure of information and clarity on court-sanctioned processes) would help to pave the way for more defaults, which in our view are needed if policymakers are to deliver on structural reforms,” the investment bank writes in a note. By becoming or owning banks, the companies can just shift debt around different balance sheets to avoid a default, although this is probably not the resolution that Goldman Sachs had in mind when talking about structural reforms.

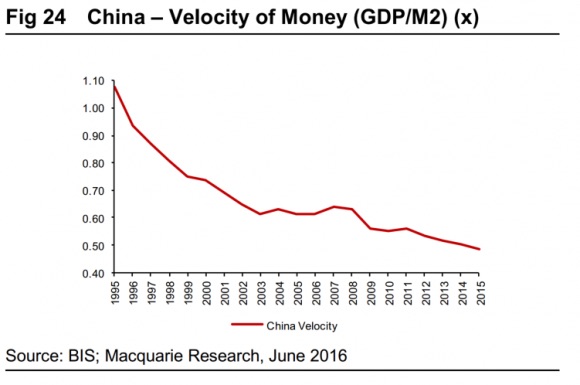

Another problem is that the regime has more and more difficulties pushing more debt into the economy to grease the wheels and keep GDP growth from collapsing entirely. China needs 11.9 units of new debt to create one unit of GDP growth. At the same time, the velocity of money or the measure of how often one unit of money changes hands during a year has fallen to below 0.5, another measure of how saturated the economy is with uneconomical credit. If the velocity of money goes down, the economy needs a higher stock of money to keep the same level of activity.

Kathimerini is going off the rails, as are a group of Greeks. Accusing Varoufakis and Galbraith of planning a military coup is so far beyond the pale, it’s reason to look at legal action.

• Galbraith Says Critics Have It All Wrong Over Greece ‘Plan X’ (Kath.)

University of Texas professor James Galbraith, a close associate of Yanis Varoufakis, has urged the 23 US-educated Greeks who recently criticized him for his part in last year’s negotiations with Greece’s creditors to read his book. Galbraith’s response came in the form of a letter to Kathimerini, which had published a story on July 29 on the letter from the 23 academics, addressed to the president of the University of Texas. In his own letter, Galbraith mentions the fact that his critics say they learned of his work as head of the team that worked on the so-called “Plan X” from interviews in the Greek press and excerpts of the Greek translation of his book, “Welcome to the Poisoned Chalice” (Yale University Press).

He asks why, given their knowledge of English, they did not read the original: “Had they done so, they would have found that the allegations they made are factually false.” Galbraith characterizes Plan X as “preliminary,” admitting that “the work of a small team cannot fully prepare for such a dramatic event.” He repeats that it would only have been activated if the Europeans had carried out their threat to cut off emergency liquidity via the ECB to Greek banks. “This would have triggered a forced exit of Greece from the euro, against the will of the government,” he notes. “The threat had been delivered by the president of the Eurogroup, Jeroen Dijsselbloem, in late January,” he adds, mentioning also the suggestion by German Finance Minister Wolfgang Schaeuble that Greece take a “holiday from the euro.”

Galbraith further rejects the claim made by the 23 that his plan constituted a “monetary-cum-military coup d’etat” and that it would involve “mobilizing the Greek armed forces to suppress possible civil disorder.” “We did not suggest using the military inappropriately or outside the Constitution. The only use of the word ‘mobilization’ in my book refers to the civil service.” He also denies that the plan included a plot to arrest the governor of the central bank. The memo on Plan X, as Galbraith repeats in his letter, “was prepared at the request of the prime minister” and “at no time was the working group engaged in advocating exit or any policy choice. The job was strictly to study the operational issues that would arise if Greece were forced to issue scrip or if it were forced out of the euro.”

Finally, Galbraith responds to claims in the letter from the 23 that he regretted the non-activation of Plan X. “This claim also is false,” he writes, making reference to his interview with Kathimerini on July 6, 2016, in which he had stated that “we were preparing for a scenario that everyone hoped to avoid.”

“..even as an expert on economic and organized crime, I was amazed to see so much of what we talk about in theory was confirmed in practice..”

• Stiglitz Quits Panama Papers Probe, Cites Lack Of Transparency (R.)

The committee set up to investigate lack of transparency in Panama’s financial system itself lacks transparency, Nobel Prize-winning economist Joseph Stiglitz told Reuters on Friday after resigning from the “Panama Papers” commission. The leak in April of more than 11.5 million documents from the Panamanian law firm Mossack Fonseca, dubbed the “Panama Papers,” detailed financial information from offshore accounts and potential tax evasion by the rich and powerful. Stiglitz and Swiss anti-corruption expert Mark Pieth joined a seven-member commission tasked with probing Panama’s notoriously opaque financial system, but they say they found the government unwilling to back an open investigation.

Both quit the group on Friday after they say Panama refused to guarantee the committee’s report would be made public. “I thought the government was more committed, but obviously they’re not,” Stiglitz said. “It’s amazing how they tried to undermine us.” The Panamanian government defended the committee’s “autonomous” management in a statement issued later on Friday, and while it said it regretted the resignations of Stiglitz and Pieth, it chalked them up to unspecified “internal differences.”

[..] In addition to embarrassing leaders worldwide who had interests tied to secretive business concerns, the leak heaped pressure on Panama, well-known for its lax financial laws, to clean up its act. “I have had a close look at the so called Panama Papers, and I must admit that even as an expert on economic and organized crime, I was amazed to see so much of what we talk about in theory was confirmed in practice,” Pieth said in a telephone interview. In the papers he said he found evidence of crimes such as money laundering for child prostitution rings. “We’re being asked to do this as a courtesy for them and we’re paraded in front of the world media first, and then we’re told to shut up when they don’t like it,” Pieth, a criminal law professor at Basel University, said.

Long and strong summary by Kristi Culpepper. Damning.

• Is Hillary Clinton Corrupt? An Archive of Financial Improprieties (Medium)

[..] Under Clinton’s leadership, the State Department approved $165 billion worth of commercial arms sales to 20 nations whose governments have given money to the Clinton Foundation, according to an IBTimes analysis of State Department and foundation data. That figure – derived from the three full fiscal years of Clinton’s term as Secretary of State (from October 2010 to September 2012) – represented nearly double the value of American arms sales made to the those countries and approved by the State Department during the same period of President George W. Bush’s second term.

The Clinton-led State Department also authorized $151 billion of separate Pentagon-brokered deals for 16 of the countries that donated to the Clinton Foundation, resulting in a 143% increase in completed sales to those nations over the same time frame during the Bush administration. These extra sales were part of a broad increase in American military exports that accompanied Obama’s arrival in the White House. The 143% increase in U.S. arms sales to Clinton Foundation donors compares to an 80% increase in such sales to all countries over the same time period.

[..] It’s really not all that difficult to see why Clinton hasn’t given a press conference in 244 days and avoids the media at her campaign events, is it? Asking her to explain every ethically questionable deal she has been involved in would probably take longer than the State Department requires to vet her emails.

In just 20 years. Wow.

• Average American 15 Pounds Heavier Than 20 Years Ago (HDN)

There’s no doubt about it: Americans are getting heavier and heavier. But new U.S. estimates may still come as a shock – since the late 1980s and early 1990s, the average American has put on 15 or more additional pounds without getting any taller. Even 11-year-old kids aren’t immune from this weight plague, the study found. Girls are more than seven pounds heavier even though their height is the same. Boys gained an inch in height, but also packed on an additional 13.5 pounds compared to two decades ago. When looked at by race, blacks gained the most on average. Black women added 22 pounds despite staying the same average height. Black men grew about one-fifth of an inch, but added 18 pounds, the study found.

[..] According to the report, the average weight of men in the United States rose from 181 pounds to 196 pounds between 1988-1994 and 2011-2014. Their average height remained the same at about 5 feet, 9 inches. The average woman, meanwhile, expanded from 152 pounds to 169 pounds while her height remained steady at just under 5 feet, 4 inches.