Edward S. Curtis Zuni Girl with Jar c. 1903

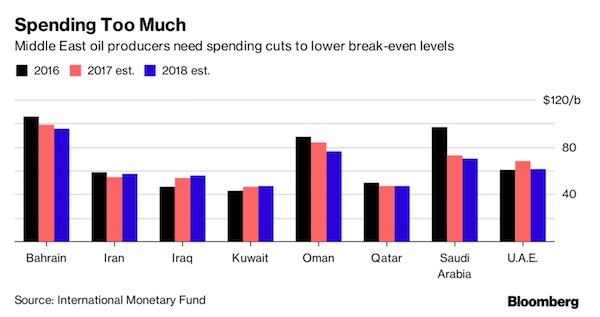

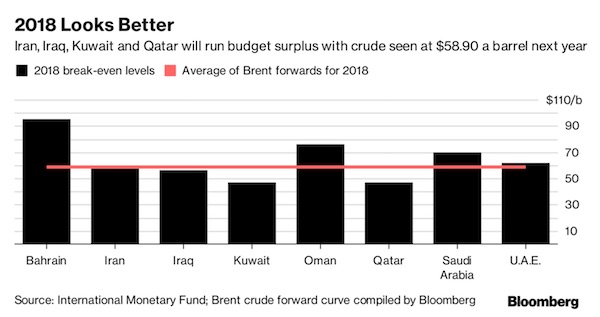

Reading a lot on Saudi. This is good by Ryan Grim. ” And make no mistake, MBS is a project of the UAE — an odd turn of events given the relative sizes of the two countries.”

• Saudi Arabia’s Government Purge — And How Washington Corruption Enabled It (IC)

Whatever the official explanation, it is being read around the world as a power grab by the kingdom’s rising crown prince. “The sweeping campaign of arrests appears to be the latest move to consolidate the power of Crown Prince Mohammed bin Salman, the favorite son and top adviser of King Salman,” as the New York Times put it. “The king had decreed the creation of a powerful new anti-corruption committee, headed by the crown prince, only hours before the committee ordered the arrests. The men are being held in the Ritz-Carlton Riyadh. “There is no jail for royals,” a Saudi source noted. The move marks a moment of reckoning for Washington’s foreign policy establishment, which struck a bargain of sorts with Mohammed bin Salman, known as MBS, and Yousef Al Otaiba, the United Arab Emirates ambassador to the U.S. who has been MBS’s leading advocate in Washington.

The unspoken arrangement was clear: The UAE and Saudi Arabia would pump millions into Washington’s political ecosystem while mouthing a belief in “reform,” and Washington would pretend to believe that they meant it. MBS has won praise for some policies, like an openness to reconsidering Saudi Arabia’s ban on women drivers. Meanwhile, however, the 32-year-old MBS has been pursuing a dangerously impulsive and aggressive regional policy, which has included a heightening of tensions with Iran, a catastrophic war on Yemen, and a blockade of ostensible ally Qatar. Those regional policies have been disasters for the millions who have suffered the consequences, including the starving people of Yemen, as well as for Saudi Arabia, but MBS has dug in harder and harder. And his supporters in Washington have not blinked.

The platitudes about reform were also challenged by recent mass arrests of religious figures and repression of anything that has remotely approached less than full support of MBS. The latest purge comes just days after White House adviser Jared Kushner, a close ally of Otaiba, visited Riyadh, and just hours after a bizarre-even-for-Trump tweet. Whatever legitimate debate there was about MBS ended Saturday — his drive to consolidate power is now too obvious to ignore. And that puts denizens of Washington’s think tank world in a difficult spot, as they have come to rely heavily on the Saudi and UAE end of the bargain. As The Intercept reported earlier, one think tank alone, the Middle East Institute, got a massive $20 million commitment from the UAE. And make no mistake, MBS is a project of the UAE — an odd turn of events given the relative sizes of the two countries.

“Our relationship with them is based on strategic depth, shared interests, and most importantly the hope that we could influence them. Not the other way around,” Otaiba has said privately. For the past two years, Otaiba has introduced MBS around Washington and offered assurances of his commitment to modernizing and reforming Saudi Arabia, according to people who’ve spoken with him, confirmed by emails leaked by the group, Global Leaks. When confronted with damning headlines, Otaiba tends to acknowledge the reform project is a work in progress, but insists that it is progress nonetheless, and in MBS resides the best chance of the region.

Read more …

“The region cannot support more turmoil..”

• Saudi Arabia Accuses Lebanon Of ‘Declaring War,’ Egypt Calls For Calm (CNBC)

Egyptian President Abdel Fattah al-Sisi called on Middle Eastern nations to maintain stability just as tensions were suddenly spiking between Lebanon and Saudi Arabia. “The stability of the region is very important and we all have to protect it … I am talking to all the parties in the region to preserve it,” Al-Sisi said in an interview with CNBC over the weekend that aired Tuesday morning. On Saturday, Lebanese Prime Minister Saad al-Hariri shocked the political establishment in Beirut by announcing his resignation. The leader said he was stepping down amid concerns of a potential assassination plot against him. Speaking from Riyadh, Hariri criticized Iran, and its Lebanese ally Hezbollah, for igniting conflict in the region.

Following the CNBC interview, Reuters reported that Saudi Arabia sharply escalated rhetoric in the region by declaring that Lebanon had — figuratively at least — declared “war” against it because of aggression from Hezbollah. Saudi Gulf Affairs Minister Thamer al-Sabhan said the government of Lebanon “would be dealt with as a government declaring war on Saudi Arabia,” Reuters reported. When asked whether the time had come for Egypt to consider its own measures against Hezbollah, Al-Sisi replied, “The subject is not about taking on or not taking on, the subject is about the status of the fragile stability in the region in light of the unrest facing the region.” “The region cannot support more turmoil,” he said.

Read more …

What OPEC couldn’t do.

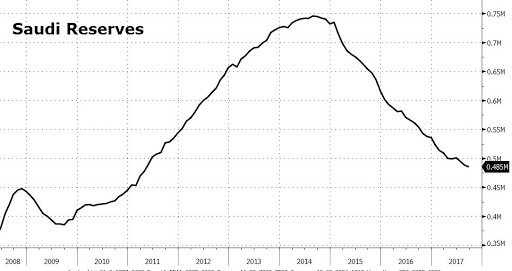

• Oil Prices Surge On Saudi Purge (CNBC)

Oil prices surged to their highest levels since the summer of 2015 on Monday as a major political shakeup in Saudi Arabia underpinned a rally fueled by geopolitical risk, analysts said. Crude futures hit the new highs overnight after the powerful Saudi Crown Prince Mohammad bin Salman coordinated the arrest of several princes and ministers, ostensibly as part of crackdown on corruption. Prices pulled back in morning trade as the market digested a wealth of analysis on the Saudi purge, but futures suddenly shot higher at midday. International benchmark Brent crude oil topped $64 a barrel for the first time since June 2015. Meanwhile U.S. West Texas Intermediate crude broke above $57, a level the market has not seen since July 2015.

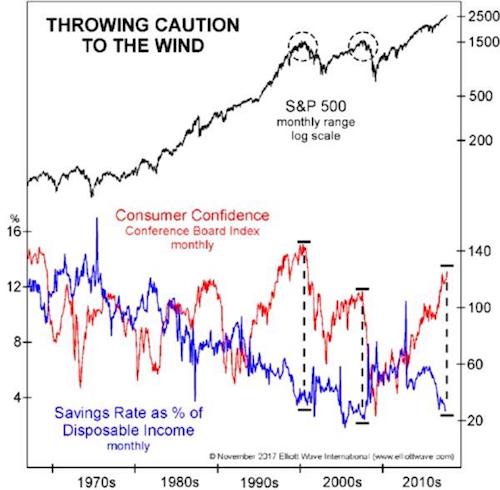

WTI finished Monday’s session $1.71 or 3.1 percent, higher at $57.35. Brent was trading up $2.04, or 3.3 percent, at $64.11 by 2:27 p.m. ET. Analysts cautioned against pinning the surge on any one headline, or even the Saudi arrests alone. Instead, they said a growing cloud of geopolitical uncertainty was unleashing animal spirits in an already bullish market. “You can grab all sorts of different headlines when you have a runaway market, and this is a runaway market right now,” said Tom Kloza, global head of energy analysis at Oil Price Information Service. In this kind of environment, “people throw caution to the wind, and this is like the grand finale of fireworks,” he said.

Read more …

More debt, fast.

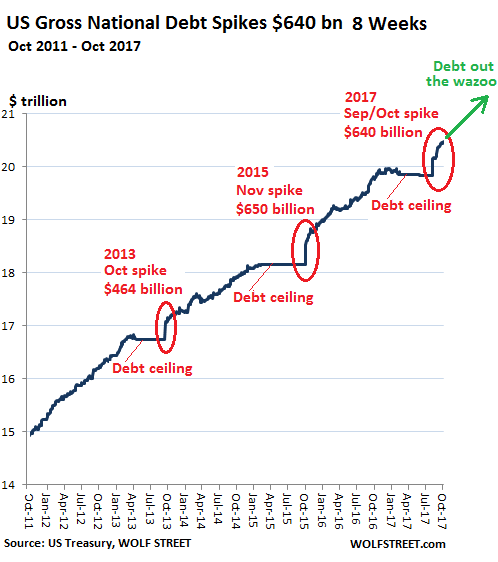

• The Black Swan In Plain Sight – Debt Out The Wazoo (Stockman)

The black swan in plain sight does emit the Donald’s orangish glow, but at the end of the day its true color is actually red. That is, monumental towers of rapidly rising debt loom everywhere on the planet. For the moment, the artificial cash flow from this unsustainable borrowing spree is keeping a simulacrum of growth and prosperity alive. Yet this whole outbreak of debt madness – represented by $225 trillion outstanding on a global basis – is careening toward a financial and economic dead end that will soon crush today’s fiscally profligate politicians and heedless financial punters, alike, in a devastating reset of bond yields. For our first case in point, the always excellent Wolf Richter published a great chart over the weekend on the exploding US public debt.

To say the least, it constitutes a clanging wake-up call amidst the absolute fantasy world that prevails on both ends of the Acela Corridor. That’s because during the mere 8 weeks since the public debt ceiling was suspended by the Donald’s end-run with Nancy and Chuckles in September, the national debt has spiked by $640 billion. That’s about $16 billion per Federal business day, and they are not done yet. The US Treasury will continue to borrow heavily until the current debt ceiling “suspension” expires on December 8 – at which time it will repair to the old game of divesting trusting funds and employing other gimmicks which circumvent the ceiling, while waiting for Congress to blink and raise the ceiling or authorize a new “temporary” suspension.

As Wolf pointed out, this pattern played out during the debt showdowns of 2013 and 2015, as well, when the resulting “temporary” suspension resulted in borrowing spikes of $464 billion and $650 billion, respectively. Accordingly, Washington has suspended it way into a $5.7 trillion increase in the public debt in just six years since October 2011. That is, during a period which supposedly constitutes the third longest business expansion in US history.

Read more …

“The “narrative” is firmest before its falseness is proved by the turn of events, and there are an awful lot of events out there waiting to present, like debutantes dressing for a winter ball.”

• What Could Go Wrong? (Jim Kunstler)

The economy isn’t growing and can’t grow. The economy is a revenant of something that used to exist, an industrial economy that has rolled over and died and come back as a moldy ghoul feeding on the ghostly memories of itself. Stocks go up because the unprecedented low interest rates established by the Fed allow company CEOs to “lever-up” issuing bonds (i.e. borrow “money” from, cough cough, “investors”) and then use the borrowed “money” to buy back their own stock to raise the share value, so they can justify their companies’ boards-of-directors jacking up their salaries and bonuses — based on the ghost of the idea that higher stock prices represent the creation of more actual things of value (front-end-loaders, pepperoni sticks, oil drilling rigs).

The economy is actually contracting because we can’t afford the energy it takes to run the things we do — mostly just driving around — and unemployment is not historically low, it’s simply mis-represented by not including the tens of millions of people who have dropped out of the work force. And an epic wickedness combined with cowardice drives the old legacy news business to look the other way and concoct its good times “narrative.” If any of the reporters at The New York Times and The Wall Street Journal really understand the legerdemain at work in these “mysteries” of finance, they’re afraid to say. The companies they work for are dying, like so many other enterprises in the non-financial realm of the used-to-be economy, and they don’t want to be out of paycheck until the lights finally go out.

The “narrative” is firmest before its falseness is proved by the turn of events, and there are an awful lot of events out there waiting to present, like debutantes dressing for a winter ball. The debt ceiling… North Korea… Mueller… Hillarygate….the state pension funds….That so many agree the USA has entered a permanent plateau of exquisite prosperity is a sure sign of its imminent implosion. What could go wrong?

Read more …

All bubbles disrupt.

• Growing Homeless Camps Contrast With West Coast Tech Wealth (AP)

SEATTLE — Housing prices are soaring here thanks to the tech industry, but the boom comes with a consequence: A surge in homelessness marked by 400 unauthorized tent camps in parks, under bridges, on freeway medians and along busy sidewalks. The liberal city is trying to figure out what to do. “I’ve got economically zero unemployment in my city, and I’ve got thousands of homeless people that actually are working and just can’t afford housing,” said Seattle City Councilman Mike O’Brien. “There’s nowhere for these folks to move to.” That struggle is not Seattle’s alone. A homeless crisis is rocking the entire West Coast, pushing abject poverty into the open like never before. Public health is at risk, several cities have declared states of emergency, and cities and counties are spending millions – in some cases billions – in a search for solutions.

San Diego now scrubs its sidewalks with bleach to counter a deadly hepatitis A outbreak. In Anaheim, 400 people sleep along a bike path in the shadow of Angel Stadium. Organizers in Portland lit incense at an outdoor food festival to cover up the stench of urine in a parking lot where vendors set up shop. Homelessness is not new on the West Coast. But interviews with local officials and those who serve the homeless in California, Oregon and Washington — coupled with an Associated Press review of preliminary homeless data — confirm it’s getting worse. People who were once able to get by, even if they suffered a setback, are now pushed to the streets because housing has become so expensive. All it takes is a prolonged illness, a lost job, a broken limb, a family crisis. What was once a blip in fortunes now seems a life sentence.

Read more …

“There is no European Union standing ready to bail out Puerto Rico.”

• Profiting from Puerto Rico’s Pain (New Yorker)

In 2012, Cate Long was working at the news service Reuters, where she wrote a daily column on the municipal-bond market. Municipal bonds are typically a sleepy corner of investing. They are forms of debt issued by states, counties, or cities, usually to fund infrastructure projects, such as airports and highways, and they are generally considered a safe investment, paying relatively low levels of interest. Finding a compelling story about the municipal-bond market is not an easy task, so when Long came across a document related to an $800 million bond sale that Puerto Rico would be undertaking that spring, she decided to look at the numbers more closely. What she found was startling. “I sat down and read it for a couple of hours, and I said, ‘These people are going to default,’ ” she told me recently. “It was pretty obvious.”

In the column she wrote about her analysis, titled “Puerto Rico Is America’s Greece,” Long expressed concern about the island’s economic health, calling it “America’s own Third World country.” At the time, Puerto Rico’s per-capita income was just $15,203 (less than half that of Mississippi, the poorest of the fifty states), and 45% of its residents were living below the poverty line. Puerto Rico also had a “massive” amount of debt, and was issuing even more bonds, which mutual funds and individuals were eagerly buying up, in spite of the warning signs. In her article, Long seemed to charge almost everyone involved, borrowers and creditors alike, with disingenuousness, incompetence, or both. “As happened with Greece, bond investors continue to buy the debt assuming at some point the government will be bailed out by somebody, somewhere,” she wrote.

“Caution, bond investors: There is no European Union standing ready to bail out Puerto Rico.” The article sent shock waves through the investment community. Moody’s Investors Service, which provides credit ratings, asked Long to come to its offices and defend her findings. (Her defense was, essentially, “I’m looking at the numbers.”) Nevertheless, the island continued its unsustainable borrowing for years—and Wall Street investors kept lending it money. By 2017, five years after Long’s warning, Puerto Rico’s bond debt had soared to $74 billion, almost a third of which was held by hedge funds. Meanwhile, the government was struggling to provide basic services to residents.

Read more …

Guess: he won’t be back in Catalonia in time for the Dec 21 elections.

• Sacked Catalan President Condemns ‘Brutal Judicial Offensive’ (G.)

The deposed Catalan president, Carles Puigdemont, has accused the Spanish authorities of conducting a “brutal judicial offensive” against members of his ousted government and said he was afraid they would not receive an unbiased hearing in Spanish courts. Writing in the Guardian, Puigdemont said it was a “colossal outrage” that he and 13 colleagues were being investigated over possible charges including sedition and rebellion in relation to their roles in last month’s declaration of independence. “Today, the leaders of this democratic project stand accused of rebellion and face the severest punishment possible under the Spanish penal code; the same as for cases of terrorism and murder: 30 years in prison,” he said.

Puigdemont said he doubted that he and his colleagues would get a “fair and independent hearing” and called for “scrutiny from abroad” to help bring the Catalan crisis to a political, rather than judicial, conclusion. He added: “The Spanish state must honour what was said so many times in the years of terrorism: end violence and we can talk about everything. We, the supporters of Catalan independence, have never opted for violence, on the contrary. But now we find it was all a lie that everything is up for discussion.” The former Catalan leader fled to Brussels with a handful of cabinet colleagues last week, hours before Spain’s attorney general announced he would be seeking to bring charges of rebellion, sedition and misuse of public funds against them.

On Thursday, a national court judge ordered the jailing of the eight Catalan politicians and, a day later, issued a European arrest warrant for Puigdemont and four of his allies. Late on Sunday, a Belgian judge granted the five conditional release. They will make their first appearance in court on 17 November when a judge will decide on whether to execute the arrest warrant. The conditions of release include a ban on them leaving Belgium until their appearance in the court of first instance in Brussels later this month. With the extradition process likely to take months rather than weeks, there is growing scope for Puigdemont’s presence in Belgium to cause the country’s coalition government serious difficulties.

Read more …

No kidding.

• Bernie Sanders Warns Of ‘International Oligarchy’ – Paradise Papers (G.)

Bernie Sanders has warned that the world is rapidly becoming an “international oligarchy” controlled by a tiny number of billionaires, highlighted by the revelations in the Paradise Papers. In a statement to the Guardian in the wake of the massive leak of documents exposing the secrets of offshore investors, Sanders said that the enrichment of wealthy individuals and companies in tax havens was “the major issue of our time”. He said the Paradise Papers opened the door on a “major problem not just for the US but for governments throughout the world”. “The major issue of our time is the rapid movement toward international oligarchy in which a handful of billionaires own and control a significant part of the global economy. The Paradise Papers shows how these billionaires and multinational corporations get richer by hiding their wealth and profits and avoid paying their fair share of taxes,” the US senator from Vermont said.

Sanders, who came in a close second to Hillary Clinton in the race for the Democratic presidential nomination last year, pointed the finger of blame for the flourishing of offshore holdings on both Congress and the Trump administration. He told the Guardian that Republicans in Congress were responsible for providing “even more tax breaks to profitable corporations like Apple and Nike”. The same tax breaks, he said, were being seized upon by super-wealthy members of Trump’s cabinet “who avoid billions in US taxes by shifting American jobs and profits to offshore tax havens. We need to close these loopholes and demand a fair and progressive tax system.”

Read more …

“We must accept that Big Finance and runaway inequality are incompatible with either a functioning democracy or a sustainable economy.”

• End These Offshore Games Or Our Democracy Will Die (G.)

Tax avoidance is now so systemic that the Queen’s own wealth managers apparently see nothing wrong with her receiving £82m a year from taxpayers while shunting £10m into the Caymans and elsewhere. Shuttling between tax havens is so commonplace that economist Gabriel Zucman describes it as an “elite sport” – a sport in which the loser each time is the rest of society, which sees its taxbase shrink. These papers are aptly named: they outline a model that is paradise for the super-rich and purgatory for the rest of us. The second myth of British politics is that austerity was the only correct response to the high-living of the New Labour boom. That was always opposed by some of us – now it is exploded with each new tax investigation.

Drawing in part on data from last year’s Panama Papers and the HSBC files leaked in 2015, Zucman recently co-published a study that found wealthy Britons have stashed about £300bn – equivalent to 15% of our GDP – in offshore tax havens. Three hundred billion quid would more than cover our entire education budget for the rest of this decade and into the 2020s. Or, if you prefer, it is the equivalent of £350m being paid into the NHS every week for the next 16 years. Instead, it is funnelled offshore and used to buy yachts and mansions and other baubles – tax efficiently, of course. The economics of David Cameron and George Osborne can be summed up simply: punish the poor, but reward the rich for fear they will flee offshore. To that end, they scrapped the 50p tax rate for millionaires, they drove down corporation tax to a record low, and cut sweetheart deals with companies such as Google who couldn’t be bothered to pay even that much.

The result is that London has more super-rich residents than any other city – yet however soft the kid gloves with which they are treated, our wealthiest 0.01% stick 30-40% of their wealth offshore. In high-tax Sweden, by contrast, the rich do not use havens half as much. The logic that has underpinned our tax system over this entire decade is rubbish. [..] Add the City of London to Britain’s crown dependencies such as Jersey and the Isle of Man, and overseas territories such as the Caymans, and Britain’s tax havens account for nearly a quarter of the entire offshore financial industry. According to Deutsche Bank, London itself receives about £1bn a month in what it calls “hidden capital flows”, much of it Russian. It ends up in Stucco-fronted houses and fine art.

Much of this could be changed, and quickly. Britain has previously ordered the Caymans and other overseas territories to decriminalise homosexuality and abolish the death penalty. It could do the same with tax transparency, in an Order of Council that, a Mayfair tax lawyer recently told me, need be no longer than two sides of A4. We could change the rules on Lords and Commons’ members’ interests so that all offshore holdings would have to be registered. These are the fixes, but a real solution is ultimately political. We must accept that Big Finance and runaway inequality are incompatible with either a functioning democracy or a sustainable economy. Britain either shrinks the City of London, or the City of London will swallow Britain.

Read more …

Lots of talk about this, with widely differing views.

• Four False Viral Claims Spread by Journalists on Twitter in One Week (GG)

There is ample talk, particularly of late, about the threats posed by social media to democracy and political discourse. Yet one of the primary ways that democracy is degraded by platforms such as Facebook and Twitter is, for obvious reasons, typically ignored in such discussions: the way they are used by American journalists to endorse factually false claims that quickly spread and become viral, entrenched into narratives, and thus can never be adequately corrected. The design of Twitter, where many political journalists spend their time, is in large part responsible for this damage. Its space constraints mean that tweeted headlines or tiny summaries of reporting are often assumed to be true with no critical analysis of their accuracy, and are easily spread.

Claims from journalists that people want to believe are shared like wildfire, while less popular, subsequent corrections or nuanced debunking are easily ignored. Whatever one’s views are on the actual impact of Twitter Russian bots, surely the propensity of journalistic falsehoods to spread far and wide is at least as significant. Just in the last week alone, there have been four major factually false claims that have gone viral because journalists on Twitter endorsed and spread them: three about the controversy involving Donna Brazile and the DNC, and one about documents and emails published by WikiLeaks during the 2016 campaign. It’s well worth examining them, both to document what the actual truth is as well as to understand how often and easily this online journalistic misleading occurs:

Viral Falsehood #1: The Clinton/DNC agreement cited by Brazile only applied to the General Election, not the primary.

Viral Falsehood #2: Sanders signed the same agreement with the DNC that Clinton did.

Viral Falsehood #3: Brazile stupidly thought she could unilaterally remove Clinton as the nominee.

Viral Falsehood #4: Evidence has emerged proving that the content of WikiLeaks documents and emails was doctored.

Read more …

Deep deep deeper and down.

• Growing Number of Greeks Unable To Pay Taxes (K.)

Almost half a million taxpayers were added to the long list of debtors to the state in the month of September, according to the latest data from the Independent Authority for Public Revenue. The authority’s figures are a reflection of citizens’ increasing inability to pay their taxes, with 410,000 not paying their second income tax installment and the ENFIA property tax in September. More specifically, 4,267,408 taxpayers owed money to the Greek state in September, up from 3,857,086 in August. Moreover, by the end of September, the amount of unpaid taxes since the beginning of the year came to 9.25 billion euros. What concerns the government is whether the 410,000 that couldn’t pay their taxes in September will join the Finance Ministry’s 12-month installment program, as the hole in tax revenues will only grow if they don’t.

Read more …

What good will kicking people out do?

• Greek Notaries Refuse To Carry Out Foreclosures (K.)

The outlook for property foreclosures in Greece is unclear after notaries announced a boycott on auctions until the end of the year, citing abuse by protesters, though foreign creditors expect the first online auctions to take place this month. According to sources, Greece’s lenders have suggested that the responsibility for foreclosures be shifted from notaries to Greek courts or possibly to Justice Ministry officials. The latter model, which has been tried and tested in Germany and Spain, was first mooted last month during a visit to Athens by bailout monitors. The auditors made it clear that the resumption of foreclosures on the homes of overindebted Greeks, which have dragged during the crisis years due to strikes by lawyers and notaries and more recently due to anti-austerity protesters, is a prerequisite for the successful conclusion of Greece’s current bailout review.

In comments at Monday’s summit of eurozone finance ministers in Brussels, ECB President Mario Draghi indicated that the resumption of property auctions would help banks by reducing the large proportion of bad loans that they hold. Commenting, Greek Finance Ministry sources said Athens was committed to “not taking our foot off the gas in the implementation of reforms for the review.” One of the many conditions of the latest review is that Greece launch electronic foreclosures. The first is supposed to take place on November 29. However, it is unclear how that procedure will be carried out in view of the protracted walkout by Greek notaries.

In a joint statement on Monday, the associations representing notaries in Athens, Piraeus and the islands of the Aegean and the Dodecanese said they will not be conducting any property auctions through December 31. The decision was reached during a meeting on Saturday with a vote of 134 in favor and 132 against. The associations said the decision was aimed at initiating talks with the Justice Ministry in order to provide protection to notaries who have come under attack – often violent – by anti-establishment groups and protesters opposed to foreclosures. Notaries also want the Justice Ministry to be made responsible for electronic auctions, as well as to address any disputes that may arise from them.

Read more …

I don’t share his optimism.

• Hawking: AI Could Be ‘Worst Event In The History Of Our Civilization’ (CNBC)

The emergence of artificial intelligence (AI) could be the “worst event in the history of our civilization” unless society finds a way to control its development, high-profile physicist Stephen Hawking said Monday. He made the comments during a talk at the Web Summit technology conference in Lisbon, Portugal, in which he said, “computers can, in theory, emulate human intelligence, and exceed it.” Hawking talked up the potential of AI to help undo damage done to the natural world, or eradicate poverty and disease, with every aspect of society being “transformed.” But he admitted the future was uncertain. “Success in creating effective AI, could be the biggest event in the history of our civilization. Or the worst. We just don’t know. So we cannot know if we will be infinitely helped by AI, or ignored by it and side-lined, or conceivably destroyed by it,” Hawking said during the speech.

“Unless we learn how to prepare for, and avoid, the potential risks, AI could be the worst event in the history of our civilization. It brings dangers, like powerful autonomous weapons, or new ways for the few to oppress the many. It could bring great disruption to our economy.” Hawking explained that to avoid this potential reality, creators of AI need to “employ best practice and effective management.” The scientist highlighted some of the legislative work being carried out in Europe, particularly proposals put forward by lawmakers earlier this year to establish new rules around AI and robotics. Members of the European Parliament said European Union-wide rules were needed on the matter. Such developments are giving Hawking hope.

“I am an optimist and I believe that we can create AI for the good of the world. That it can work in harmony with us. We simply need to be aware of the dangers, identify them, employ the best possible practice and management, and prepare for its consequences well in advance,” Hawking said.

Read more …

We want one!

• The Charter of the Forest (Standing)

Eight hundred years ago this month, after the death of a detested king and the defeat of a French invasion in the Battle of Lincoln, one of the foundation stones of the British constitution was laid down. It was the Charter of the Forest, sealed in St Paul’s on November 6, 1217, alongside a shortened Charter of Liberties from 2 years earlier (which became the Magna Carta). The Charter of the Forest was the first environmental charter forced on any government. It was the first to assert the rights of the property-less, of the commoners, and of the commons. It also made a modest advance for feminism, as it coincided with recognition of the rights of widows to have access to means of subsistence and to refuse to be remarried. The Charter has the distinction of having been on the statute books for longer than any other piece of legislation.

It was repealed 754 years later, in 1971, by a Tory government. In 2015, while spending lavishly on celebrating the Magna Carta anniversary, the government was asked in a written question in the House of Lords whether it would be celebrating the Charter this year. A Minister of Justice, Lord Faulks, airily dismissed the idea, stating that it was unimportant, without international significance. Yet earlier this year the American Bar Association suggested the Charter of the Forest had been a foundation of the American Constitution and that it was more important now than ever before. They were right. It is scarcely surprising that the political Right want to ignore the Charter. It is about the economic rights of the property-less, limiting private property rights and rolling back the enclosure of land, returning vast expanses to the commons.

It was remarkably subversive Sadly, whereas every school child is taught about the Magna Carta, few hear of the Charter. Yet for hundreds of years the Charter led the Magna Carta. It had to be read out in every church in England four times a year. It inspired struggles against enclosure and the plunder of the commons by the monarchy, aristocracy and emerging capitalist class, famously influencing the Diggers and Levellers in the 17th century, and protests against enclosure in the 18th and 19th. At the heart of the Charter, which is hard to understand unless words that have faded from use are interpreted, is the concept of the commons and the need to protect them and to compensate commoners for their loss. It is scarcely surprising that a government that is privatising and commercialising the remaining commons should wish to ignore it.

In 1066, William the Conqueror not only distributed parts of the commons to his bandits but also turned large tracts of them into ‘royal forests’ – ie, his own hunting grounds. By the time of the Domesday Book in 1086, there were 25 such forests. William’s successors expanded and turned them into revenue-raising zones to help pay for their wars. By 1217, there were 143 royal forests. The Charter achieved a reversal, and forced the monarchy to recognise the right of free men and women to pursue their livelihoods in forests. The notion of forest was much broader than it is today, and included villages and areas with few trees, such as Dartmoor and Exmoor. The forest was where commoners lived and worked collaboratively.

Read more …