Harris&Ewing Less taxes, more jobs, US Chamber of Commerce campaign 1939

“..no matter how hard the Fed works to prop and boost the market, nearly half of Americans no longer have any faith left in what has become clear to most is just a tool to push some crooked, crony-capitalist policy, but mostly to make the richest even richer.”

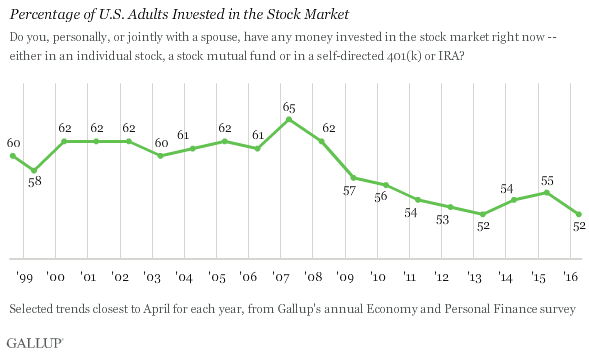

• US Middle Class Flees The Stock Market (ZH)

Three recurring laments heard in the corridors of the Marriner Eccles building are why, with stocks at record highs after levitating in more or less a straight line for the past 7 years, i) has the economic recovery not been stronger, ii) has inflation not been higher, and iii) have consumer spending and sentiment never really recovered. A just released Gallup survey may have the answer. According to a poll of over 1,000 American adults, even with the Dow Jones industrial average near its record high, only slightly more than half of Americans (52%) say they currently have money in the stock market, matching the lowest ownership rate in Gallup’s 19-year trend.

The current figure is down slightly from 2014 and 2015, and continues a secular decline that started in 2007. But most troubling is that the generation which is expected to take over the stock ownership reins when the Baby Boomers start selling their equity holders, middle-class adults, especially those younger than 35, are the least likely to invest. As Gallup notes, “although Americans in all income groups are less likely to have stock investments now than before the Great Recession, middle-class Americans have been the most likely to flee the market” Gallup’s conclusion: “Fewer Americans – particularly those in middle-income families – are benefiting from the recent gains in stock values than would have been the case a decade ago.”

Which is the worst possible news for Janet Yellen, because no matter how hard the Fed works to prop and boost the market, nearly half of Americans no longer have any faith left in what has become clear to most is just a tool to push some crooked, crony-capitalist policy, but mostly to make the richest even richer.

Read more …

Wobbly.

• China Markets Send Ominous Signals as Global Stocks Rally (BBG)

As equities climb around the world, Chinese traders aren’t celebrating. The Shanghai Composite Index has fallen 4.6% this week, the worst performance among 93 global benchmark gauges tracked by Bloomberg and the steepest decline since January. It’s not just the stock market. The yuan is trading around its lowest level against a basket of currencies since November 2014, while yields on corporate debt have risen for 10 of the past 12 days. Concern is mounting over rising credit defaults, while traders are also paring bets for more stimulus amid signs of stabilizing growth, according to Dai Ming at Hengsheng in Shanghai. A sudden 4.5% plunge by the benchmark equity gauge on Wednesday revived memories of January’s stomach-churning turmoil, when shares sank 23% over the course of the month. “People are still very skeptical, and with good reason,” said Hao Hong at Bocom International in Hong Kong.

International concern about the health of China’s economy has been fading from view as data showed an improving picture and volatility in its stock and currency markets waned. Wednesday’s equity tumble in Shanghai caused barely a ripple among global shares as international traders focused on surging commodity prices – spurred partly by expectations of higher Chinese demand. Questions are being asked about how long the Communist Party can keep pumping money into the economy to prop up growth. New credit topped $1 trillion in the first quarter, helping GDP to expand 6.7% – still the slowest pace in seven years. Much of that money flowed into the property market, spurring concerns of a bubble. “There’s still a lot of doubt over the sustainability of the turnaround in the Chinese macro numbers,” said Adrian Zuercher UBS’s wealth management unit. “It’s a very stimulus-driven rebound that we now see.”

Read more …

“..the highest share any country has enjoyed since the United States in 1968.”

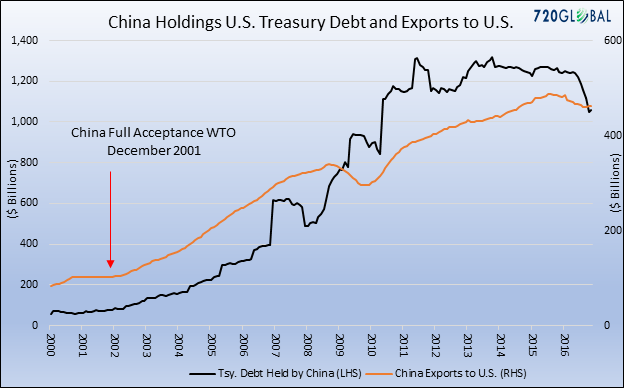

• China Seizes Biggest Share Of Global Exports In Almost 50 Years (R.)

Chinese exporters have found a silver lining in weak global demand by seizing market share from their competitors – good news for China but an expansion that is aggravating trade tensions. China’s proportion of global exports rose to 13.8% last year from 12.3% in 2014, data from the United Nations Conference on Trade and Employment shows, the highest share any country has enjoyed since the United States in 1968. The success belies widespread predictions rising costs for Chinese labor and a currency that has increased nearly 20% against the dollar in the last decade would cause China to lose market share to cheaper competitors. Instead, China’s manufacturing infrastructure built during the country’s industrial rise of recent decades is keeping exports humming and providing the basis for firms to produce higher-value products.

“China cannot be replaced,” said Fredrik Guitman, formerly China general manager for a Danish maker of silver products, adding that reliable delivery times were more important than price. “If they say 45 days, it will be 45 days.” Still, even as Chinese firms compete in more sophisticated product lines, they are unloading overstocked inventory from entrenched industrial overcapacity in sectors like steel, an irritant in global trading relationships. The United States and seven other countries this week called for urgent action to address a steel supply glut that many blame on China. At the same time, China’s imports from other countries fell sharply – down over 14% in 2015 – leading some economists to suggest China was deploying an “import substitution” strategy that is pushing foreign brands out of its domestic markets.

On Wednesday, Beijing rolled out fresh measures to support machinery exports, including tax rebates, and encouraged banks to lend more to exporters. Machinery and mechanical appliances make up the biggest portion of China’s exports. Such policies may not be welcomed in the United States, where Republican presidential hopeful Donald Trump has called for 45% tariffs on Chinese imports – a message that appears to resonate with American voters. The risk is that the Chinese firms successfully moving up the value chain will see their overseas profits destroyed by a trade war if Trump’s ideas find place in policy.

Read more …

Risk it? War is on.

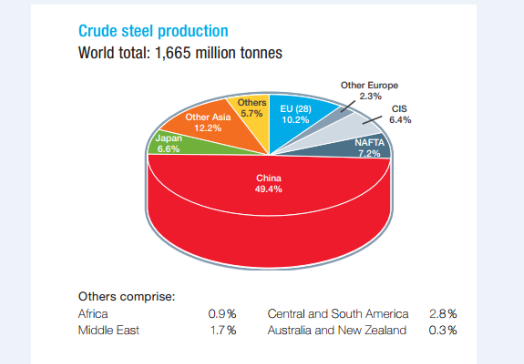

• China Risks Global ‘Steel War’ As Tempers Flare (AEP)

China is on a collision course with the world’s leading powers over excess steel output after it refused to sign up to an emergency global plan to cut capacity and eliminate subsidies. The clash comes as fresh data confirms fears that China is still cranking up production and even reopening shuttered plants supposedly due for closure, despite the massive glut on the world market. Chinese mills produced a record 70.65m tonnes in March, 51pc of global output and five times as much as the whole EU. “Just words from China are no longer good enough. It is now clear to everybody that the Chinese have no intention at all of changing the structure of their steel industry,” said Axel Eggert, head of the European steel federation Eurofer. “They refused even to accept basic principles. They don’t recognise the problem, and they are not looking for a compromise,” he said.

The world’s steel-making powers, led by the US, Japan and the EU, agreed to joint steps to tackle the crisis at special OECD summit in Brussels on Monday, but China’s name was conspicuously absent when the final document was released later. This renders the plan meaningless since China’s excesses capacity alone is 400m tonnes, greater than the entire production of Europe and North America. Officials were shocked by the tone of the encounter with the Chinese delegation. “It was eye-opening,” said one source. “The scale of the emergency in the sector means it is now life or death for many companies,” said Cecilia Malmstrom, the EU trade commissioner. Brussels has been slow to roll out anti-dumping sanctions, partly due to pressure from Britain and other states courting China for their own political reasons.

While the US has imposed penalties of 266pc on Chinese cold-rolled steel, the EU has acted more slowly and stopped at 13pc. But the mood is shifting. Mrs Malmstrom said there is no doubt that the surge in Chinese exports is the reason why steel prices have crashed by 40pc this year, insisting that it is imperative to “act quickly” before the crisis asphyxiates European industry. “The situation is putting hundreds of thousands of jobs in the EU at risk. It’s also undermining a strategic sector with importance for the wider economy,” she said. Emmanuel Macron, the French economy minister, said Europe can no longer tolerate the flood of Chinese supply. “You do not respect the rules of world trade. Your steel output is subsidised, and the excess capacity is dumped below cost. It is destroying our productive capacity, and it is unacceptable,” he said.

Anger is also rising on Capitol Hill, with mounting calls from the US Congress for a much tougher stand, a theme echoed daily on the presidential campaign trail. “The American steel industry faces the greatest import crisis in modern history,” said Tim Murphy, head of the Congressional steel caucus. “We’re at the tipping point, with US mills averaging only 70pc of capacity utilisation, a level that is simply not sustainable. We are in real danger of losing this industry and becoming dependent on foreign countries. We can’t let that happen.”

Read more …

There’s no reason other than speculation and manipulation for the yen to be where it is.

• Yen Falls By Most In 7 Weeks As BOJ Considers Negative-Rate Loans (BBG)

The yen dropped the most in seven weeks after people familiar with the matter said that the Bank of Japan may consider helping financial institutions to lend by offering a negative rate on some loans. Japan’s currency slid against all except one of its 16 major counterparts after the people said a discussion on this may happen in conjunction with any decision to make a deeper cut to the current negative rate on reserves. The people asked not to be named as the matter is private. The BOJ meets April 27-28 to decide on its next policy move. “We thought they would be doing more quantitative easing but it looks like they may be doing more on the negative interest-rate front,” said Joseph Capurso at Commonwealth Bank of Australia.

That’s driving the move lower in the Japanese currency and “if delivered, you’ll get a temporary but significant spike up in dollar-yen. The yen dropped 0.8% to 110.30 per dollar as of 7:06 a.m. in London, the biggest decline since March 1. Japan’s currency weakened 0.9% to 124.68 per euro. Twenty three of 41 analysts surveyed by Bloomberg predict the BOJ will expand stimulus next week. Nineteen forecast the central bank will increase purchases of exchange-traded funds, eight expect a boost in bond buying and eight project the BOJ will lower its negative rate, the survey conducted April 15-21 shows.

Commonwealth Bank recommended buying the dollar against the yen through two-week options to take advantage of the diverging monetary policies of the Fed and the BOJ. National Australia Bank Ltd. said in a report it favors purchasing dollars at current levels before the BOJ meeting, targeting an appreciation to 113 yen. The Federal Open Market Committee meeting April 26-27 will also be closely watched for guidance on how soon U.S. policy makers will raise the benchmark rate after an increase at the end of last year. Traders have increased the odds of a Fed move by December to 63% from about 50% at the end of last week, according to data compiled by Bloomberg based on fed fund futures.

Read more …

Isn’t it time to get serious yet?

• Draghi Defies German Disfavor With Claim ECB Stimulus Works (BBG)

Mario Draghi has two stubborn adversaries – low inflation everywhere, and low regard in Germany. He’s now extending his offensive on both fronts. A recovery in credit, and output proving resilient to global shocks, are buttressing the European Central Bank’s argument that the range of stimulus measures it bolstered only last month is working. On Thursday, the ECB president used that evidence to make ground against German critics who say he’s on the wrong track. After more than four years at the helm of the central bank, Draghi is still fielding persistent attacks from the ECB’s host country, where a public perception of him as a profligate Italian whose low interest rates are killing retirement savings has become part of the political furniture.

At a press conference in Frankfurt, he fumed that the more critics undermine his stimulus, the more of it he’ll have to do. “Impatience in the markets and in politics can come up like a geyser sometimes, but the ECB has to continue to be as steady as a rock,” said Torsten Slok at Deutsche Bank in New York. “The more it shows up in the data, the easier it is for them to say that their policies are working. The ECB is defending itself and making sure the arguments are solid.” The backdrop to Thursday’s policy meeting, where the Governing Council kept its interest rates on hold after cutting them to record lows in March, was colored by a row stepped up by Germany’s Wolfgang Schaeuble.

Draghi deployed a volley of arguments against the finance minister’s charge that ECB policies are contributing to the rise of anti-euro populism, and the broader assumption that savers are being penalized, adding that Schaeuble either “didn’t mean what he said or didn’t say what he meant.” “In fact real rates today are higher than they were about 20-30 years ago,” Draghi said. “But I’m aware that to explain real interest rates to savers may be difficult.” Draghi has been dogged by sniping in Germany since taking office, with the popular press often using his nationality as shorthand for a tendency to allow high inflation. In fact, he’s had the opposite problem, with price gains too far below the 2% goal for more than three years.

Read more …

ZIRP and NIRP kill pensions sytems around the planet. And Draghi claims ‘ECB Stimulus Works’.

• Pension Cuts Loom For Millions of Dutch As Big Funds Struggle (DN)

The assets of the Netherlands’ four biggest pension funds have fallen again, making it more likely that millions of people will face pension cuts next year. By law, a pension fund must have a coverage ratio of 105%, meaning its assets outweigh its obligations by 5%. However, that of the massive civil service fund ABP has now gone down to 90.4%, a drop of seven%age points since the end of 2015. Health service fund Zorg & Welzijn and the two engineering funds also have a coverage ratio of around 90%. ‘Our financial position remains worrying,’ said ABP chairwoman Corien Wortmann-Kool. ‘We are heading to the danger zone and that means there is a real risk of a pension cut in 2017.’ ABP is one of the biggest pension funds in the world. The heads of the other three funds have made similar statements. If the pension funds have a coverage ratio of below 90% at the end of the year, they will have to cut pensions.

Read more …

“..a joint currency that enabled its strongest member to execute a beggar-thy-neighbor mercantilist trade policy that penalized countries without the size or drive of Germany..”

• Eurozone Mess Can’t Be Fixed; It Can Only Be ‘Muddled Through’ (MW)

If you’re waiting for international policy makers to pull a rabbit out of the hat and solve the euro problem, stop holding your breath. After a generally a desultory meeting of the IMF in Washington last week, the prevailing pessimism about the future of the euro came grimly to the fore in one of the many meetings held on the sidelines of the semiannual IMF gathering. Two dozen policy makers convened by the Official Monetary and Financial Institutions Forum (OMFIF), a private London-based group, met this week to discuss the future of the European Union’s joint currency. The off-the-record discussion involved an international array of current and former government officials, central bankers, and private-sector financiers.

The verdicts ranged from “deeply pessimistic” to “not ready to give up” – perhaps the most optimistic assessment at the meeting – and the group in its assembled wisdom concluded that there are no realistic solutions and the only course of action they could see is “muddling through.” They rehearsed all the usual analysis of what went wrong – an attempted common currency without the underpinning of joint fiscal policy, a banking union, and most importantly, a political union with an institutional infrastructure for making decisions. Without this follow-through on the original plan for “an ever closer union,” the EU has stumbled along a path of “incompetence,” with individual countries acting only in their own interests.

Even the ECB, the only EU-wide institution that has shown itself capable of taking action in this environment, came in for criticism because its successive moves to ease the stress in the system left the political leaders off the hook in coming to terms with the underlying issues. And yet, participants noted, the European public seems reluctant to give up the euro. Not even Greece, which has suffered terribly in the straitjacket of a common currency with Germany, is willing to give it up. So the answer is muddling through. And muddling through is one thing Europeans excel at, even though it has brought mixed results. Europe, after all, muddled through the arms buildup in the early 20th century to World War I. It muddled through to the banking collapse of 1931 (which contributed more to the Great Depression in the U.S. than the 1929 stock market crash).

Then it muddled through into fascism and World War II. Rebuilding from the rubble of that conflict led to a relatively brief period of constructive behavior as the continent, shielded by the U.S. defense umbrella, built new democracies and an ever-widening free trade zone. As U.S. influence — and interest — waned, Europe began again to resort to muddling through as a way of coping with stress. It muddled through the crisis in Bosnia and genocidal conflict at its very doorstep, until the U.S. intervened and sorted things out. It muddled through into a joint currency that enabled its strongest member to execute a beggar-thy-neighbor mercantilist trade policy that penalized countries without the size or drive of Germany, slashing their standard of living and reducing whole swaths of the populations to penury. Then it muddled through into a refugee crisis that threatens the very fabric and identity of individual nations, giving rise to a xenophobic backlash that harkens back to the days of Depression and fascism less than a century ago.

Read more …

Oh boy, are we getting tough or what?!

• US Regulators Line Up to Consider New Executive Compensation Proposal (WSJ)

Federal regulators are lining up to consider a new rule to rein in Wall Street’s executive compensation nearly a decade after the financial crisis. The National Credit Union Administration plans to meet Thursday, giving Wall Street banks, investors and others the first glimpse of the regulators’ latest effort to overhaul Wall Street pay rules for top executives. Next week, two other regulators are scheduled to consider the revised plan, according to a government notice posted Wednesday. The rule would require banks to retain much of an executive’s bonus beyond the three years already adopted by many firms, people familiar with the matter said. The board of the Federal Deposit Insurance Corp., led by Chairman Martin Gruenberg, will meet Tuesday to vet the compensation proposal.

The FDIC board also includes Comptroller of the Currency Thomas Curry. The Office of the Comptroller of the Currency will likely consider the proposal separately later the same day, according to a person familiar with the matter. On Thursday, the NCUA will release documents, including a roughly 250-page preamble to the joint rule, when the board meets at 10 a.m. EDT. It will also unveil rules specifically drafted for a handful of federally insured credit unions with $1 billion or more in assets, including the Navy Federal Credit Union and State Employees Credit Union. Six agencies have joint responsibility for rewriting the original government plan on Wall Street pay: the FDIC, the OCC, the NCUA, the Federal Reserve Board, the Securities and Exchange Commission and the Federal Housing Finance Agency.

All six are required to sign off on the draft measure before it can be released to the industry and the public for comment. Representatives from the Fed and SEC declined to comment on the timing of their meetings to consider the proposal. The FHFA plans to consider the proposal soon, according to a person familiar with the matter. The effort to complete the rule, which has been under way for five years, got a nudge from President Barack Obama last month at a White House meeting of top financial regulators. The president urged regulators to wrap up the executive compensation rule before he leaves office early next year. It is unclear whether the agencies will be able to coordinate their efforts and get the rule completed by then.

Read more …

Little bit wishful thinking, perhaps, Gillian?!

• How Goldman Sachs’ Vampire Squid Became A Flattened Slug (Tett)

A decade ago, Goldman Sachs reported that its return on common shareholder equity had hit a dazzling 39.8%. It symbolised a gilded age: back in 2006, as markets boomed, the power — and profits — of big banks seemed unstoppable. How times change. This week, American banks unveiled downbeat results, with revenues for the biggest five tumbling 16% year-on-year. But Goldman was even weaker: net income was 56% lower, while return on equity, a key measure of profitability, was 6.4%, below even the sector average in 2015 of 10.3%. A bank which was once so adept at sucking out profits that it was called a “vampire squid” (by Rolling Stone magazine) is thus producing returns more commonly associated with a utility. The phrase “flattened slug” might seem appropriate.

Is this just a temporary downturn? Financiers certainly hope so. After all, they point out, this week’s results did feature some upbeat (ish) points. None of America’s banks actually blew up in the first quarter of the year, even though markets gyrated in dramatic ways; the post-crisis reforms have improved risk controls and reserves. Meanwhile, banking in America looks healthier than in Europe, where the reform process has been slower. Overall credit quality at American banks, outside the energy sector, does not seem alarming. Net interest margins are now increasing a touch, after several years of decline, because the Federal Reserve has raised rates. The last quarter’s results might have been depressed by temporary geopolitical woes, such as business uncertainty about Brexit, the American elections, oil prices and the Chinese economy.

Once this angst fades away later this year, returns may rebound; analysts expect the Goldman ROE, for example, to move towards 10% later this year. “The market feels a little fragile,” says Harvey Schwartz, its chief financial officer. “[But] it feels like that is behind us.” Perhaps. But even if this “optimism” is justified, nobody should ignore the cognitive shift. After all, a decade ago, an ROE of 10% was considered a disaster, not a relief, at Goldman Sachs. So perhaps the most important lesson from this week is this: if American regulators had hoped to make the banks look truly dull — not dazzling — in this post-crisis era, they are now succeeding better than anyone might have thought.

Read more …

“If there is a haircut on bank deposits it will be the end and, so far, that is the only measure they haven’t taken. If Greece defaults it will be impossible to find oil, impossible to find medicines. And this time round everything seems possible.”

• Greek Talks With Lenders Fraught As Fears Grow Of Default (G.)

The Hilton hotel in Athens makes the perfect backdrop for high-intensity talks. Its ambience is subdued, its corridors hushed, its meeting rooms an oasis of tranquility. When Greece, in one of its many stand-offs with the international creditors keeping it afloat, finally won the right to conduct negotiations outside the confines of government offices, it seemed only natural that they should be held at the hotel. However, in recent weeks the talks have assumed an increasingly nervous edge. An economic review that should have been completed months ago has been beset by wrangling as Alexis Tsipras’s leftist-led government has argued with lenders over the terms of a bailout agreed last summer.

The €86bn rescue programme agreed in July 2015 – the debt-stricken country’s third in six years – followed months of high-octane drama that saw Athens being pushed to the brink of bankruptcy and euro exit. Now, less than a year later – and with a crucial meeting of eurozone finance ministers lined up for Friday – a sense of crisis has returned to Greece. With politicians indulging in the angry rhetoric that put Athens on a collision course with lenders last year, investors have begun to worry. Yields on government bonds have risen, protesters have taken to the streets, and “Grexit” – the catch-all word that so conjured up Greece’s battle with economic meltdown – is being murmured again.

Against a backdrop of maturing debt – the country must repay €5bn to the ECB and IMF in June and July – commentators have begun to talk in terms of fatal miscalculation. “History is made of accidents which were not the result of some secret plan, but a string of errors, human weaknesses and obsessions,” wrote Alexis Papahelas in the conservative daily Kathimerini. “Lets hope we will avoid that.” On the street, the uncertainty has not only had a deadening effect on an economy already battered by years of withering austerity; it has also created mounting anxiety among a populace that has seen per capita GDP levels drop by 28%, unemployment nudge 30%, more than one in four businesses close and poverty afflict one in three.

After defying the doomsayers, there are fears Europe’s most indebted country could now be heading towards a disorderly default. “There is no one I know who isn’t worried,” says Yannis Tsandris, a private sector retiree whose pension has been cut by almost a third. “If there is a haircut on bank deposits it will be the end and, so far, that is the only measure they haven’t taken. If Greece defaults it will be impossible to find oil, impossible to find medicines. And this time round everything seems possible.”

Read more …

How peaceful do you think those Olympics are going to be?

• The Real Reason Dilma Rousseff’s Enemies Want Her Impeached (Miranda)

The story of Brazil’s political crisis, and the rapidly changing global perception of it, begins with its national media. The country’s dominant broadcast and print outlets are owned by a tiny handful of Brazil’s richest families, and are steadfastly conservative. For decades, those media outlets have been used to agitate for the Brazilian rich, ensuring that severe wealth inequality (and the political inequality that results) remains firmly in place. Indeed, most of today’s largest media outlets – that appear respectable to outsiders – supported the 1964 military coup that ushered in two decades of rightwing dictatorship and further enriched the nation’s oligarchs. This key historical event still casts a shadow over the country’s identity and politics.

Those corporations – led by the multiple media arms of the Globo organisation – heralded that coup as a noble blow against a corrupt, democratically elected liberal government. Sound familiar? For more than a year, those same media outlets have peddled a self-serving narrative: an angry citizenry, driven by fury over government corruption, rising against and demanding the overthrow of Brazil’s first female president, Dilma Rousseff, and her Workers’ party (PT). The world saw endless images of huge crowds of protesters in the streets, always an inspiring sight. But what most outside Brazil did not see was that the country’s plutocratic media had spent months inciting those protests (while pretending merely to “cover” them). The protesters were not remotely representative of Brazil’s population.

They were, instead, disproportionately white and wealthy: the very same people who have opposed the PT and its anti-poverty programmes for two decades. Slowly, the outside world has begun to see past the pleasing, two-dimensional caricature manufactured by its domestic press, and to recognise who will be empowered once Rousseff is removed. It has now become clear that corruption is not the cause of the effort to oust Brazil’s twice-elected president; rather, corruption is merely the pretext. Rousseff’s moderately leftwing party first gained the presidency in 2002, when her predecessor, Luiz Inácio Lula da Silva, won a resounding victory.

Due largely to his popularity and charisma, and bolstered by Brazil’s booming economic growth under his presidency, the PT has won four straight presidential elections – including Rousseff’s 2010 election victory and then, just 18 months ago, her re-election with 54 million votes. The country’s elite class and their media organs have failed, over and over, in their efforts to defeat the party at the ballot box. But plutocrats are not known for gently accepting defeat, nor for playing by the rules. What they have been unable to achieve democratically, they are now attempting to achieve anti-democratically: by having a bizarre mix of politicians – evangelical extremists, far-right supporters of a return to military rule, non-ideological backroom operatives – simply remove her from office.

Read more …

Why bother with cheat software?

• All Diesel Cars’ Emissions Far Higher On Road Than In Lab (G.)

Diesel cars are producing many times more health-damaging pollutants than claimed by laboratory tests, with some emitting up to 12 times the EU maximum when tested on the road, according to a government investigation undertaken following the Volkswagen scandal. A Department for Transport (DfT) study of cars made by manufacturers such as Ford, Renault and Vauxhall found there was a vast difference in nitrogen oxide emissions measured in the laboratory and under normal driving conditions. Not a single car among 37 models tested against the two most recent nitrogen oxide emissions standards met the EU lab limit in real-world testing, with the average emissions being more than five times as high. However, the DfT said it had found no vehicles outside the VW group with systems in place to deliberately rig emissions figures.

Robert Goodwill, the junior transport minister, said: “Unlike the Volkswagen situation, there have been no laws broken. This has been done within the rules.” The minister denied that the findings meant the current emissions testing regime was a farce. “But certainly I am disappointed that the cars that we are driving on our roads are not as clean as we thought they might be. It’s up to manufacturers now to rise to the real-world tests and the tough standards we’re introducing,” he said. The DfT exercise was ordered after it emerged that Volkswagen had allegedly used technology to cheat emissions tests. It measured Nox, or nitrogen oxide emissions. Nitrogen oxide helps to form ozone smog that can badly affect people with chest conditions such as asthma.

The tests were carried out by a team led by Ricardo Martinez-Botas, professor of mechanical engineering at Imperial College London. Among the vehicles tested were 19 models that meet the latest Euro 6 limit of 80mg/km NOx emissions in laboratory tests. Euro 6 was introduced for all new cars sold after September last year. When driven in a real-world simulation of urban, rural and motorway travel, the average was nearer to 500mg/km, with some cars getting close to 1,100mg/km. Among the new models tested that are meant to comply with the Euro 6 standard were the Ford Focus, which had a real-world emission about eight times above the EU limit, the Renault Megane, whose emissions were more than 10 times higher, and the Vauxhall Insignia, almost 10 times higher.

Read more …

Already “The scandal has wiped around 40% off Mitsubishi’s market value..”

• Mitsubishi Scandal Deepens After US Demands Test Data (G.)

The scandal engulfing Mitsubishi Motors has deepened, sending its shares to a new low after US authorities said they had requested information from the Japanese automotive group. Mitsubishi admitted this week that it manipulated test data to overstate the fuel efficiency of 625,000 cars and there are fears that more models may be involved. Government officials raided one of its offices on Thursday. The scandal has wiped around 40% off Mitsubishi’s market value, amounting to losses of $3.2bn over three days. The shares fell nearly 14% on Friday, following declines of 20% on Thursday, when they were suspended, and 15% on Wednesday. An official at the US National Highway Traffic Safety Administration told Reuters that the regulator had asked Mitsubishi for information on vehicles sold in the US.

Japanese government officials said Mitsubishi could be responsible for reimbursing consumers and the government if investigations conclude that the vehicles were not as fuel-efficient as claimed. Transport minister Keiichi Ishii told a news conference on Friday: “This is a serious problem that could lead to the loss of trust in our country’s auto industry.” He said he wanted Mitsubishi to examine the possibility of buying back affected cars. Internal affairs minister Sanae Takaichi said the government would also ask the carmaker to pay for any subsidies granted to consumers if its cars are found to fail fuel economy standards, Jiji news agency reported. Japanese media reported that Mitsubishi had submitted misleading mileage data on its i-MiEV electric car, which is also sold overseas. The previously disclosed models whose fuel economy readings Mitsubishi has admitted to manipulating are only sold in Japan – four of its mini-cars, two of which it manufactured for Nissan.

Read more …

Subsidies.

• Why UK Landed Gentry Are So Desperate To Stay In The EU (G.)

The estate agent Carter Jonas established its reputation running the estates of the Marquess of Lincolnshire. “Some of the biggest property owners in the country are our loyal clients,” boasts its website. And, in a recent poll of these landowning clients, 67% of them said that Britain should stay in the EU. So why all this Euro-enthusiasm in the Tory heartlands and among the landed gentry? “Should the UK vote to leave the EU, the CAP subsidies will likely be reduced,” Tim Jones, head of Carter Jonas’s rural division, explained. Thank you, Tim, for putting it so clearly. We understand. A massive 38% of the entire 2014-20 EU budget is allocated as subsidies for European farmers. It is far and away the biggest item of euro expenditure, about €50bn a year.

If these billions were being used to prop up a heavy industry – steel, for example – then the neoliberals would be up in arms, complaining like mad that if an industry can’t cope with a free market then it should be left to die. Creative destruction, they call it. But, for some reason, when it comes to agriculture, different rules apply. Farms are not called “uneconomic” in the same way that pits and factories are. So every British household coughs up about £250 a year and hands it over to the EU, which hands it over to people like the Duke of Westminster – already worth £7bn himself. In 2011, the duke received £748,716 in EU subsidies for his various estates. So, too, Saudi Prince Bandar (he of the dodgy al-Yamamah arms deal), who pocketed £273,905 of EU money for his estate in Oxfordshire.

The common agricultural policy is socialism for the rich. It’s a mechanism to buttress the aristocracy – who own a third of the land in this country – from the chill winds of economic liberalism. So why are we hearing so little about all of this in the current debate over Europe? Because the right doesn’t want to worry its landowning friends and the left has somehow persuaded itself that the EU is a progressive force – so it suits no one’s purpose to raise this issue. Yet it’s a huge deal. For the European Union has become a huge and largely invisible way of redistributing wealth from the poor to the rich, subsidising lord so-and so’s grouse moor, while redundancies are handed out to workers at Port Talbot (whose jobs the government can’t help subsidise because of EU rules).

But even more problematic is the way our massively subsidised agricultural sector negatively affects farmers in the developing world. “Trade not aid” has been David Cameron’s repeated mantra for dealing with poverty in the developing world. But not only does the CAP subsidy to European farmers make it impossible for the unsubsidised African farmer to compete fairly in European markets, but it also creates situations where food is overproduced in Europe – remember butter mountains, milk lakes etc.

Read more …

While this crazy barter goes on, the short stick is for the refugees.

• Angela Merkel Faces Balancing Act On Visit To Turkey (G.)

Angela Merkel is facing dual pressure to both raise freedom of speech issues and patch up fraying diplomatic relations with Turkey during a visit to Gaziantep province on Saturday. The issue of visa-free travel, one of the key elements of the month-old deal between the European Union and Turkey, is expected to be at the top of the agenda as the German chancellor visits the country alongside the European Council president, Donald Tusk, and European commission vice-president Frans Timmermans. On Tuesday, Turkey’s prime minister, Ahmet Davutoglu, threatened to pull out of the deal if no progress was made on the visa arrangement.

But in Germany, Merkel is under growing pressure to show more spine in her dealings with the Turkish government, after giving in to Recep Tayyip Erdogan’s request for the comedian Jan Böhmermann to be prosecuted for reading out a poem that insulted the president. In the run-up to Merkel’s Gaziantep trip, the secretary general of the Social Democrats, a junior party in the governing coalition, has called on Merkel to send out a “strong message on the issue of freedom of speech”. “Without this basic right, democracy does not work – the Turkish government too has to recognise that,” Katarina Barley told the newspaper Bild.

Coming on the anniversary of the foundation of Turkey’s parliament, and a day before many people commemorate the start of the Armenian genocide, secularists and minorities in Turkey too will hope for a signal against Turkey’s authoritarian turn from the German chancellor. The German government has so far refrained from providing details of the chancellor’s schedule during her trip. In recent days Merkel has been struggling to limit the damage caused by the Böhmermann affair. Even though the comedian is unlikely to face more than a financial penalty, the incident has taken its toll on the chancellor’s authority in the public eye, with her personal approval ratings dropping by over 10 percentage points in a recent poll.

In another poll, 66% of the German public said they disapproved of the chancellor’s decision to authorise criminal proceedings against the comedian. The justice minister Heiko Maas announced on Thursday that he would present a draft bill to abolish the law on “insulting a foreign head of state” that lies at the centre of the Böhmermann affair before the end of this week. Merkel had originally promised to abolish the law by January 2018. Were the relevant paragraph of the penal code scrapped before Böhmermann goes on trial, the chancellor would look even more exposed. Diplomatic ties between Germany and Turkey were further strained when the journalist Volker Schwenck of the public broadcaster ARD was detained at Istanbul airport on Tuesday morning and denied entry to the country. Schwenck had previously reported from rebel-held areas in northern Syria.

Read more …