NPC Sidney Lust Leader Theater, Washington, DC 1920

“It would be a slow-death scenario and in a way we are in this scenario. Something needs to change in order to avoid an accident..”

• Greece In ‘Slow-Death Scenario’ Amid Defaults Fears (CNBC)

Greece faces a “slow-death scenario”—including a default and messy exit from the euro zone—one analyst warned Thursday, as the country’s economic crisis took another turn for the worse following a credit rating downgrade. BofA’s Thanos Vamvakidis warned Thursday that if Greece fails to reach a deal with its European partners, a Grexit—or Greek exit from the euro zone becomes inevitable. His comments come after Greece’s unresolved negotiations with its international creditors prompted ratings agency Standard & Poor’s to cut its credit rating to “CCC+” from “B-” with a negative outlook.

“Without an agreement (with creditors over reforms), without official funding, there is a very high probability that Greece will default sometime in May and this could lead to a very negative scenario,” Vamvakidis told CNBC Thursday. He said that although nobody wants that, “the more they delay the higher the risks.” “(A Grexit) is not going to be overnight. It would be a slow-death scenario and in a way we are in this scenario. Something needs to change in order to avoid an accident,” he added. Reform discussions between Greece and the bodies overseeing its bailout program—the EC, ECB and IMF—have been unsuccessful over recent weeks. The country’s creditors agreed to extend its bailout program by four months in February in order to give Greece’s new leftwing government more time to enact reforms.

Lack of progress on reforms means Greece’s last tranche of aid—needed in order to make loan repayments to the IMF and ECB in the coming weeks and months—has not been released. [..] Despite growing fears of a euro zone exit, some euro zone officials have refused to countenance such a scenario, which could bring with it significant upheaval and potentially disastrous consequences for the euro zone. Not only could a default and Grexit prompt capital controls to prevent bank runs, international financial isolation and the introduction of a new currency in Greece, it could threaten the future of the 19-country single currency bloc.

Knowing that any such talk could spark international panic over Greece and the intergrity of the euro zone and its currency, the European Central Bank’s President Mario Draghi dismissed fears of a Greek default Wednesday, saying he was not ready to even “contemplate” such a scenario. Officials in the U.S. have openly warned over the risks posed by Greece, however. Greek Finance Minister, Yanis Varoufakis, is due to meet U.S. President Barack Obama on Thursday, and U.S. Treasury Secretary Jacob Lew on Friday (along with the ECB’s Draghi and IMF officials).

Time for some US pressure?

• IMF Knocks Greek Debt Rescheduling Hopes (FT)

Greek officials have made an informal approach to the IMF to delay repayments of loans to the international lender, highlighting the parlous state of Greek finances, but were told that no rescheduling was possible. According to officials briefed on the talks by both sides, Athens was persuaded not to make a specific request for a delay to the Fund, which is owed almost a €1bn in two separate payments due in May. Although Athens was rebuffed, the discussions, which occurred in private earlier this month, are a sign that the Greek government is finding it increasingly difficult to scrape together enough money to continue to pay wages and pensions while meeting its debt payments to external lenders.

Officials representing Greece’s creditors are unsure whether Athens will be able to make the payments in May. Even if they do, they are certain that the matter will come to a head by June, before much larger payments on bonds held by the ECB start coming due.

IMF officials have repeatedly said that a rescheduling of repayments can only come as part of a completely renegotiated new bailout programme. Were it to miss a payment, Greece would become the first developed economy to go into arrears at the Fund, something only counties like Zaire and Zimbabwe have done in the past.Greece informally raised the precedent of delaying IMF payments by at least one other developing country a generation ago in the 1980s. But IMF officials stuck to their guns saying that none of the underlying problems had been solved by payment delays. One source briefed on the approach said the proposal was to “reshuffle the repayment schedule for the IMF loan over the coming months,” allowing the new Greek government led by Alexis Tsipras to have the money to pay bills for pensions and public sector salaries while negotiating with European creditors over payment of the next tranche of bailout loans.

“..the Greek Finance Minister “will on Friday meet with infamous sovereign debt lawyer Lee Buchheit, who has helped numerous countries restructure their debt.”

• The Endgame For Greece Has Arrived (Zero Hedge)

To think it was just recently in September of last year when the S&P, seemingly unaware of the tragic reality facing Greece in just a few months (by reality we meen democratic elections which overthrew the previous regime which was merely a group of Troika picked technocrats), upgraded Greece to B and said “The upgrade reflects our view that risks to fiscal consolidation in Greece have abated.” Well, the risks have unabated, and two months after S&P flip-flopped and downgraded Greece back to B- on February 6, moments ago it downgraded it again, this time to triple hooks, aka the dreaded CCC+. S&P said that without deep economic reform or further relief, S&P expects Greece’s debt, other financial commitments to be unsustainable. S&P views that Greece increasingly depends on favorable business, financial, and economic conditions to meet its financial commitments.

The rater adds that “conditions have worsened due to the uncertainty stemming from the prolonged negotiations between the Greek govt and its official creditors” and that economic prospects could deteriorate further unless talks between Greece and its creditors conclude soon.” In short: Greece is about to default and/or exit the Eurozone so this time at least S&P is prepared. Ironically this comes a day before Varoufakis is set to meet with Obama. It will be followed by meetings with European Central Bank head Mario Draghi on Friday, Secretary of the Treasury Jack Lew, Italy’s finance minister Pier Carlo Padoan and IMF officials. But, as City AM reports, the biggest news is that the Greek Finance Minister “will on Friday meet with infamous sovereign debt lawyer Lee Buchheit, who has helped numerous countries restructure their debt. Buchheit is a partner at top US law firm Cleary Gottlieb.”

It comes just a week before a vital meeting of Eurozone finance ministers on 24 April which could be the last chance Greece has of gaining extra funds before hefty repayments are due to its creditors in May.

As a reminder, “Lee Buchheit, a leading sovereign-debt attorney and the man who managed the eventual Greek debt restructuring in 2012, was harshly critical of the authorities’ failure to face up to reality. As he put it, “I find it hard to imagine they will now man up to the proposition that they delayed – at appalling cost to Greece, its creditors, and its official-sector sponsors – an essential debt restructuring.” The endgame for Greece has arrived.

One kind of logic.

• Why The Grexit Is Inevitable – How About May 9th? (Raas Consulting)

One thing in common for almost all of my Pinewood International Schools (TiHi to some) class of ’78 is that we left. Many still live in Greece and in Thessaloniki or have returned, and they are closest to the pain. The real pain of the past decade, that has destroyed wealth and hope. Unemployment is running at levels not see in Europe since after the war, and at levels that encouraged the socialist – fascist civil wars of the 1930s. Those did not end well.

But that does not explain why the Grexit is inevitable, and why it will happen very soon.

1) This is what the Greek people voted for. No, they did not vote to stay in the Euro, they voted for the party that said it would reduce the debt and meet pension obligations. The Greek people and voters are not stupid. They knew this could only happen by either the rest of Europe bailing out Greece again, or by leaving the Euro.

2) The Greek people know perfectly well that Europe is not going to bail them out, because to do so will only set everyone up for the next bailout.

3) The Greek people, and the rest of Europe, know full well that the debt will never be repaid, and that the Troika are now acting as nothing better than the enforcers of loan sharks.

4) Syriza knows that it had six months before the voters would throw them out, and once out, Syriza would never come back.

5) The Greeks needed to show “good faith” in actually attempting to negotiate a resolution with the Troika. This has now been done, and is failing.

6) The demand for reparations from Germany is designed not to actually extract the reparations, but to anger the Germans to the point that they will block any compromise that Syriza would have been required to accept.The Greek government, elected by a battered and exploited Greek people, has been establishing the conditions that will give them the moral high ground (in the eyes of their voters) needed to actually leave the Euro. Having set the conditions, when will it happen? I’m still guessing May 9th. Why? Greece will leave the Euro, and they will do it sooner than later. They’ve made the April payment, but simply do not have the money for the May or June payments, and they cannot pass the legislation required by Europe and the Germans and stay in power. That gives us a late May or June date. So why earlier?

Capital flight. Imposing currency controls will be a fundamental element of any Grexit. Accounts will be frozen, and any money in accounts will be re-denominated in New Drachmas. Once the bank accounts are unfrozen, the residual, former Euros will now be worth whatever the New Drachma has dropped to, and the drop will be significant, over–correcting to the downside. Once it is accepted that the Grexit is coming and there will be no last minute deal, and with memories of Cyprus too fresh in every Greek’s mind, the money will flow out of the country. Not just corporate money (most of which is probably off-share already) but any remaining personal money in bank accounts. So Greece has to move before the coming Grexit is perceived as inevitable, and the money starts to flow out.

Weekend event. When the Grexit happens, it will be on a weekend. The banks will be closed, parliament will be called into emergency session, and a packet of laws will be passed. As this needs to be on a Saturday to avoid wholesale capital flight the moment that parliament is called into session, were it a weekday. This leaves only a few possible dates. And where there are few possible dates, I’m punting on the earlier date, so earlier in May. And looking at the calendar, that leaves us with May 2nd, 9th or 16th. My own guess is that the 2nd is too soon, and the 16th is too late. That leaves me guessing May 9th.

It is pretty silly that anyone would doubt this. Or believe reassurances to the contrary.

• UBS Says Europe Risks Bank Runs On Grexit (Zero Hedge)

UBS: When examining the risk of contagion from any possible Greek exit from the Euro we come back again and again to the fact that in every monetary union collapse of the last century, the trigger for breakup was not the bond markets, current account positions, or political will, but banks. If ordinary bank depositors lose faith in the integrity of a monetary union they will hasten its demise by shifting their money out of their banks – either into physical cash, or into banks domiciled in areas of the monetary union that are perceived as “stronger”. Both of these traits were evident in the US monetary union breakup, and have been in evidence in more recent events this century.

The contagion risk after a possible Greek exit arises if bank depositors elsewhere in the Euro area believe that a physical euro note held “under the mattress” at home today is worth more than a euro in a bank – because a euro in a bank might be forcibly converted into a national currency tomorrow. In a breakup scenario it is more likely that retail bank deposits withdrawn will end up as physical cash, owing to the difficulties of opening and using a bank account in a different country. This is not a question of banking system solvency. Highly solvent banks will be subject to deposit flight if it is the value of the currency in that country that is uncertain…

The contagion story is serious. Even if a depositor thinks that there is only a 1% chance their country will exit the Euro, why take a 1% chance that your life savings are forcibly converted into a perceived worthless currency if by acting quickly (and withdrawing deposits) one can have 100% certainty that your life savings remain in Euros? If Greece were to walk away from the Euro, then the policy makers of the Euro area would have to convince bank depositors across the Euro area that a Euro in their local banking system was worth the same as a Euro in another country’s banking system, and that the possibility of any other country exiting the Euro was nil. If that double guarantee was not utterly credible, then the risk of other countries joining Greece in exiting the Euro would be high.

This suggests that financial markets are treating the risks around Greek exit with too little regard for the probable dangers.

Like before the recovery gets out of hand.

• Fed’s Bullard Says Rate Hikes Are Needed For Coming ‘Boom’ (MarketWatch)

A leading hawk on the Federal Reserve on Wednesday made a case for raising interest rates soon, arguing the level needs to be appropriate for the coming “boom” for the U.S. economy. St. Louis Fed President James Bullard, speaking at the annual Hyman Minsky conference here, acknowledged a boom by current standards might not be the same as the growth in the late 1990s. He pointed out that even if gross domestic product expanded just 1.5% in the first quarter, the four-quarter growth rate would be about 3.3%.With the current potential growth around 2%, growth in the low 3% range “represents growth well above trend,” he said. The first reading on first-quarter GDP is due April 29. Unlike his colleagues, Bullard expects the unemployment rate to fall below 5% from a current level of 5.5%. Bullard said jobless rates in the 4% range are consistent with a boom.

In his remarks, he notably did not specify a month to lift interest rates, and asked by reporters afterwards, he said, “I’m being deliberately vague.” The June meeting is considered the first in which the Federal Open Market Committee will give serious consideration to lifting interest rates. His biggest fear from keeping low rates — they have been near zero for 6.5 years — is that they could lead to financial-stability problems later. He said asset valuations currently look fairly valued, with the notable exception of bonds which Fed policy influences. “So it’s hard to know what that really means.” But he pointed out that Fed policy typically impacts the economy with a lag. “Boom times ahead, plus us already charting out low interest rates, sounds like risky from a bubble perspective,” he said.

She’s not the only one. But perhaps she should have said this a year ago.

• Warren Says Auto Lending Reminds Her Of Pre-Crisis Housing Days (MarketWatch)

Senator Elizabeth Warren on Wednesday used a major address on financial regulation to chide automobile lending practices as she continued her criticism of the country’s largest banks. Warren was speaking on the topic of the unfinished business of financial reform, and looking at the financial sector five years after the passage of the Dodd-Frank reform law. Warren, the leading contender to block a Hillary Clinton presidential nomination on the Democratic side if she were to step into the race, took particular aim at the fast-growing automobile lending category. “Right now, the auto loan market looks increasingly like the pre-crisis housing market, with good actors and bad actors mixed together,” the Massachusetts Democrat said.

“The market is now thick with loose underwriting standards, predatory and discriminatory lending practices, and increasing repossessions.” Warren pointed out that car dealers got a specific exemption from the Consumer Financial Protection Bureau, the agency which Warren all but singlehandedly brought to life. “It is no coincidence that auto loans are now the most troubled consumer financial product. Congress should give the CFPB the authority it needs to supervise car loans – and keep that $26 billion a year in the pockets of consumers where it belongs,” she said, referring to an estimate of dealer markups.

The CFPB has taken some steps in the area of automobile loans and has proposed a rule that would bring larger auto lenders that are not already banks under its jurisdiction. Warren was on more familiar ground with her call to break up the nation’s banks. She pointed out that last summer the Federal Reserve and the Federal Deposit Insurance Corp. said 11 banks were risky enough to bring down the U.S. economy if they were to fail. She also blasted the Justice Department, the Federal Reserve and the Securities and Exchange Commission for timidity in going after major banks. “The DOJ and SEC sit by while the same giant financial institutions keep breaking the law — and, time after time, the government just says, ‘Please don’t do it again.’ ”

How much further must this go before something is done?

• 27% Of US Students Are Over A Month Behind On Their Loan Payments (Zero Hedge)

As we’ve documented exhaustively in the past, the country is laboring under around $1.3 trillion in non-dischargeable loans to students which isn’t a good thing, especially in a country where the jobs driving the economic “recovery” have, until last month, been created in the food service industry and where wage growth is a concept reserved for only 20% of the workforce. It would seem that this could make it increasingly difficult for students to repay their debt, especially considering how quickly tuition costs have risen. In other words, tuition is going up, wages aren’t, and the latter point there is only relevant in the event you find a job that pays you a wage in the first place (i.e. where your compensation isn’t determined by the generosity of the “supervisory” Americans who can still afford to eat out).

The severity of the problem has been partially masked at times by the tendency to inflate the denominator when one goes to calculate delinquency rates. That is, if you include all student debt outstanding, even that in deferment or forbearance in the denominator, then clearly the delinquency rate will be biased to the downside because the numerator will by necessity only include those students who are currently in repayment. That’s really convenient if you want to make things look less bleak than they actually are.

Of course you can’t be delinquent when you aren’t yet required to make payments, so the more accurate way to calculate the figure would be to include only those students in repayment in the denominator. This apples-to-apples comparison is likely to paint much more accurate picture and sure enough, a new St. Louis Fed (who recently documented the shrinking American Middle Class) study finds that the delinquency rate for students in repayment is 27.3%, well above the 17% figure for all student borrowers. Here’s more:

[..] if we adjust the delinquency rate to consider that only a fraction of the borrowers have payments due, this level of delinquency is very concerning: A delinquency rate of 15% for all student loan borrowers implies a delinquency rate of 27.3% for borrowers with loans in repayment. This level of delinquency is much higher than for any other type of debt (credit cards, auto loans, mortgages, and so on).

That feels more like it. Over 70% of capital invested in housing, which fell 6%…

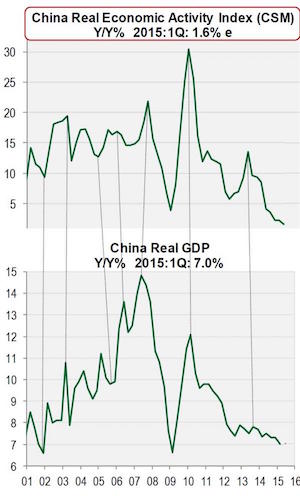

• China’s True Economic Growth Rate: 1.6% (Zero Hedge)

Cornerstone Macro reports, “Our China Real Economic Activity Index Slowed To Just 1.6% YY In 1Q.” The indicator in question looks at many of the components shown above, such as retail sales, car sales, rail freight, industrial production, and several others, to determine an accurate indicator of the true state of China’s economy. It finds that not only is China’s economic growth rate not rising at a 7.0% Y/Y rate, but is in fact the lowest it has been in modern history! And a 1.6% growth rate by what was formerly the world’s most rapidly growing (and largest according to the IMF) economy explains perfectly what happened with the US economy over the past 6 months. Hint: it has nothing to do with the winter, and everything to do with China hard landing into a brick wall.

“China is currently enjoying the somewhat dubious fruits of one of the all-time great stock manias.”

• The South (China) Sea Bubble (Corrigan)

The first hard data release of the month for China was hardly guaranteed to reassure. Two-way trade in USD terms dropped 6.3% in the first quarter from its level of a year ago, the second most severe setback since the Crash and only the third such instance in the whole era of ‘Opening Up’. From a strictly local perspective, the bad news was mitigated by the fact that exports managed to eke out a modest YOY gain of 4.7% (though that still means they were effectively unchanged from 2013 levels) and so the trade surplus was left at a record seasonal high. For the rest of us, however, anxious as we are to sell more of our wares to China, there was no such comfort. Imports plunged by more than a sixth to a four-year low, registering a drop which, if nowhere near as large in percentage terms, was, when measured in numbers of dollars, equal to that suffered in the global freeze which ensued in the aftermath of the Lehman collapse.

Though it always does to await the full data release for the first quarter – given the inordinate impact on comparisons of that highly moveable feast, the Lunar New Year – these numbers are fully consonant with the evidence presented during the first two months which showed flat non-residential electricity use and rail freight volumes down to seven year seasonal lows. It is undoubtedly the case that the bulk of the pain being felt is concentrated where it should be – up in the dirty, surplus capacity-plagued end of heavy industry and extraction – but, nevertheless, Chinese data show that 12-month running profits have dwindled to zero (if we strip out companies’ non-core – qua speculative – activities) and that for the last three months for which we have numbers they had actually declined in a manner not seen since the world stood still in late 2008/early 2009.

Revenue growth was also sickly, while balance sheets continue to swell with debt and receivables. Granted, private joint-stock companies continue to outperform their state-owned peers – or so the NBS would have us believe – but, even here, core profit growth over the whole of 2014 was a mere 4.2% with turnover up 9.2% (suggesting that margins simultaneously contracted). In such an environment, you might think that investor spirits would be dampened but, as anyone who has opened a paper in recent days will be aware, that is very much far from being the case.

Indeed, China is currently enjoying the somewhat dubious fruits of one of the all-time great stock manias. The CSI300 composite of Shanghai and Shenzhen equities has double since last July, with the seven-eighths of those gains coming in the last six months and almost a third of them in the past six weeks. With first Y1 trillion then Y1.5 trillion trading days being recorded and with 1.6 million [sic] new trading accounts being opened in the latest week for which we have the numbers, it is easy to see that this has rapidly degenerated into an indiscriminate free-for-all.

“..a Keynesian-on-steroids stimulus that occurs at the municipal level by building all sorts of public infrastructure that requires stealing land from farmers..”

• Don’t Invest In ‘Unsustainable’ China: Professor (CNBC)

China bear Peter Navarro is telling investors not to put their money in the country because its economic model is unsustainable. “What you got is a mercantilist export-driven model for China coupled with a Keynesian-on-steroids stimulus that occurs at the municipal level by building all sorts of public infrastructure that requires stealing land from farmers,” the University of California, Irvine economics professor told CNBC’s “Power Lunch” on Wednesday. Navarro, who co-wrote “Death By China,” attributes China’s slowing growth to less demand coming from the U.S. and Europe for Chinese exports.

“The problem is simply that Europe and the U.S., which provided the 10% growth year after year for three decades, are now too weak to sustain that,” he said. In addition, China is facing rising wages, labor issues, water shortages and a stock market and real estate bubble, Navarro said. On Wednesday, China’s statistics bureau announced that GDP grew an annual 7% in the first quarter, slowing from 7.3% in the previous quarter. That was the country’s slowest pace of growth in six years, suggesting the world’s second-largest economy was still losing momentum.

“..every investment-led growth miracle in the last 100 years has broken down.”

• The Major Paradox at the Heart of the Chinese Economy (Bloomberg)

“The latest GDP report underscores offsets coming from China’s services-led transformation — a key underpinning of consumer demand,” said Stephen Roach… “I suspect the economy is close to bottoming and could well begin to pick up over the balance of this year.” Chinese officialdom has little choice but to tap on the brakes of the old-line economy. Years of politically driven investment with diminishing returns led to too much debt and industrial overcapacity, as well as ghost towns with unfinished hotels and unoccupied residential towers. Bad debt piled up at a faster pace at China’s big state banks in the fourth quarter. Meanwhile, the country’s total debt — government, corporate and household — rose to about $28 trillion by mid-2014, according to an estimate by McKinsey, or about 282% of GDP.

Xi and Premier Li Keqiang are trying to defuse that debt bomb, rein in banks and local governments and promote the nation’s stock markets as a primary way for innovative and smaller companies to raise capital. Both leaders say they’ve mapped out more than 300 reforms that over time will reduce state intervention in the economy. Among the initiatives is scaling back energy-price controls that favor manufacturers. The changes are also designed to improve the social safety net and encourage market-driven deposit rates to get Chinese families saving less and spending more.

Few countries with the scale of China’s credit boom have escaped unscathed without experiencing some sort of banking crisis. Research by Michael Pettis, a finance professor at Peking University, shows that “every investment-led growth miracle in the last 100 years has broken down.” Avoiding that fate requires a high-wire balancing act for the government. It needs to wind down the torrent of investment – 49% of China’s GDP from 2010 to 2014 – without cratering the economy and worsening the situation for indebted local governments or the bad-debt burden of Chinese banks.

Anything goes by now?!

• China Seen Expanding Mortgage Bonds to Revive Housing (Bloomberg)

China is poised to expand mortgage bonds to lift its slumping real estate market that accounts for a third of the economy. Officials will likely allow banks to sell commercial mortgage-backed notes for the first time by the end of the year after reviving securities tied to home loans in 2014, according to China Merchants Securities Co. and China Chengxin International Credit Rating Co. The offerings, which help banks boost mortgage lending by freeing space on balance sheets, will grow “substantially” this year, China Credit Rating Co. said. The government of Premier Li Keqiang eased home-purchase rules after new housing prices slid in many cities across China in February.

Authorities, who halted securitization in 2009 after subprime mortgage bonds triggered the global financial crisis, are returning to such offerings to spur an economy growing at the slowest pace since 1990. “The launch of commercial mortgage-backed securities may send a strong policy signal because it will give banks more space to lend money directly to property developers,” said Zuo Fei, a Shenzhen-based director of structured finance at China Merchants Securities, underwriter of the first RMBS deal this year. “The regulators are trying to improve property purchases in a gradual and an appropriate way.”

The People’s Bank of China on March 30 cut the required down payment for some second homes to 40% from 60% and has reduced benchmark interest rates twice since November. The central bank and the China Banking Regulatory Commission said on Sept. 30 that they will encourage lenders to issue mortgage-backed securities. The government is trying balance efforts to provide new financing with steps to rein in unprecedented borrowing. Real estate companies sold a record $44.4 billion-equivalent of bonds in 2014, data compiled by Bloomberg show. In the latest sign of industry stress, Kaisa Group Holdings Ltd., based in the southern city of Shenzhen, is seeking a restructuring that would impose noteholder losses, fueling speculation that builder defaults may spread.

Is Ambrose seeking to offset the bleak views he posted lately?

• Bonds Beware As Money Catches Fire In The US And Europe (AEP)

Be thankful for small mercies. The world economy is no longer in a liquidity trap. The slide into deflation has, for now, run its course. The broad M3 money supply in the US has been soaring at an annual rate of 8.2pc over the past six months, harbinger of a reflationary boomlet by year’s end. Europe is catching up fast. A dynamic measure of eurozone M3 known as Divisia – tracked by the Bruegel Institute in Brussels – is back to growth levels last seen in 2007. History may judge that the ECB launched quantitative easing when the cycle was already turning, but Italy’s debt trajectory needs all the help it can get. The full force of monetary expansion – not to be confused with liquidity, which can move in the opposite direction – will kick in just as the one-off effects of cheap oil are washed out of the price data.

“Forecasters ignore broad money at their peril,” says Gabriel Stein, at Oxford Economics. Inflation will soon be flirting with 2pc across the Atlantic world. Within a year, the global economic landscape will look entirely different, with an emphasis on the word “look”. In my view this will prove to be mini-cyclical in a world of “secular stagnation” and deficient demand, but mini-cycles can be powerful. Mr Stein said total loans in the US are now growing at a faster rate (six-month annualised) than during the five-year build-up to the Lehman crisis. “The risk is that the Fed will have to raise rates much more quickly than the markets expect. This is what happened in 1994,” he said. That episode set off a bond rout. Yields on 10-year US Treasuries rose 260 basis points over 15 months, resetting the global price of money. It detonated Mexico’s Tequila crisis.

Bonds are even more vulnerable to a reflation shock today. You need a very strong nerve to buy German 10-year Bunds at the current yield of 0.16pc, or French bonds at 0.43pc, at time when EMU money data no longer look remotely “Japanese”. Granted, there may be tactical reasons for buying Bunds, even at negative yields out to eight years maturity. Supply is drying up. Berlin is pursuing a budget surplus with religious zeal, paying down €18bn of debt over the past year. It has left the Bundesbank little to buy as it launches its share of QE. Yet this is collecting pfennigs on the rails of a high-speed train. The German property market is on the cusp of a boom. David Roberts, of Kames Capital, warns of a “poisonous cocktail” of resurgent inflation and rising wages. “If you look at Bunds in anything other than the shortest possible timescale, the risk becomes very clear.”

Dick Tator. Mr. Dick Tator.

• ECB’s Mario Draghi Says Stimulus Is Working (WSJ)

European Central Bank President Mario Draghi said the bank’s stimulus efforts are beginning to take hold in the European economy and batted away concerns in financial markets that the bank may have to end its more than €1 trillion ($1.1 trillion) asset purchase program early. Mr. Draghi’s Wednesday news conference, held after the ECB decided to keep interest rates and other policies unchanged, was briefly interrupted by a confetti-throwing protester who jumped on the table where Mr. Draghi was seated and shouted “end the ECB dictatorship” as he began his opening remarks.

Mr. Draghi, who appeared unfazed by the ruckus after being whisked away by his bodyguards to a side room for a few minutes, said the bank’s stimulus drive is “finally finding its root” in the economy through easier credit conditions and lower inflation-adjusted interest rates. “The euro area economy has gained further momentum since the end of 2014,” said Mr. Draghi. “We expect the economic recovery to broaden and strengthen gradually.” Still, Mr. Draghi said the region’s recovery depends on full implementation of the ECB’s policies. Those include a record-low lending rate that the ECB kept unchanged Wednesday; cheap four-year loans to banks; and a €60 billion-a-month program to buy mostly government bonds that the ECB launched last month and intends to continue through September 2016.

On Tuesday, the IMF raised its forecast for eurozone growth this year to 1.5% from 1.2%. Though well below the levels of growth the U.S. has achieved during its recovery, it was a welcome development for a region that last year narrowly escaped its third recession in six years. Mr. Draghi cited a long list of reasons why this recovery should continue whereas previous ones have faltered. Lower oil prices, which cut costs for businesses and households, are joining the ECB’s stimulus in boosting the economy, Mr. Draghi said, noting that business and consumer confidence is up and that there should be fewer headwinds from fiscal policy.

[..] Mr. Draghi also played down concerns that the superlow interest rates brought on by the ECB’s policies could fuel bubbles in financial markets. “So far we have not seen evidence of any bubble,” he said, adding that regulatory policies, known as macroprudential tools, would be “the first line of defense” if imbalances started to form. He sidestepped questions about how the ECB would react in the event Greece isn’t able to reach agreement with its international creditors to unlock bailout funds, saying developments are “entirely in the hands of the Greek government.”

Schaeuble needs to stop telling Greece what to do.

• Schaeuble Says Greece Must Ditch False Hopes, Commit to Reform (Bloomberg)

German Finance Minister Wolfgang Schaeuble ruled out further concessions to Greece, saying it’s up to the Greek government to commit to the reforms needed to release aid rather than give false hopes to its people. Schaeuble, speaking in a Bloomberg Television interview in New York on Wednesday, said that another debt restructuring wasn’t up for discussion now, and that Greek demands for war reparations from Germany were “completely unrealistic.” “It’s entirely down to Greece,” said Schaeuble, 72. While some kind of restructuring might be on the agenda in 10 years, “today the issue for Greece is reforming its economy in such a way that it becomes competitive at some point.”

Greece’s plight is deepening with no end in sight to the standoff with creditors over releasing the final installment of bailout aid that has been stalled since the January election of Prime Minister Alexis Tsipras’s anti-austerity government. Greek 10-year bond yields surged and bank stocks plunged to their lowest level in at least 20 years on Wednesday after a report in Die Zeit newspaper the German government was working on a plan to keep Greece in the euro area if the country defaulted, triggering a halt to European Central Bank funding. “We don’t have such plans, and if we were working on them – because ministry staff are taking just about everything into consideration – then we would definitely not talk about it,” said Schaeuble. “It makes no sense to speculate about it.”

With a monthly bill of about €1.5 billion for pensions and salaries and repayments to its international creditors looming, Greece is targeting next week’s meeting of euro-area finance ministers in Riga, Latvia, as a deadline for unlocking the funds. While Schaeuble said earlier Wednesday that “no one” in the euro region expects a resolution of the standoff by the Riga meeting on April 24, he softened his tone in the interview, saying that the end of the program on June 30 was the only deadline that mattered. “If Greece wants support, we will give this support as in recent years, but of course within the framework of what we agreed,” he said. While the decisions ultimately lie with Greece, “whatever happens: we know that Greece is part of the European Union and that we also have a responsibility for Greece and we will never disregard this solidarity.”

“..Tsipras’s government had “destroyed” progress made by previous administrations..” That’s the progress that led to hungry children?!

• Schaeuble Criticizes Greece for Backsliding as Time Runs Out (Bloomberg)

German Finance Minister Wolfgang Schaeuble criticized Greece for backsliding on reforms, saying that “no one” expects a resolution next week of the standoff with Alexis Tsipras’s government over untapped bailout funds. Schaeuble, in his first comments on the matter since before the Easter holidays, said Tsipras’s government had “destroyed” progress made by previous administrations in overhauling the Greek economy. “It’s a tragedy,” he said Wednesday at the Council on Foreign Relations in New York, adding that the country needed to become competitive to stop being a “bottomless pit.” The comments by the finance chief of the region’s biggest economy underscored the rising concern in European capitals that Greece is running out of time to unfreeze the aid needed to keep the country afloat.

Standard & Poor’s cut Greece’s rating Wednesday, citing the country’s deteriorating outlook. Schaeuble is among European officials who are skeptical that there’s enough time to work out a deal ahead of a meeting of euro-area finance ministers at the end of next week in Riga, Latvia, to assess whether Greece has made enough progress to warrant a disbursement from its €240 billion bailout fund. Leaders are pressuring Greece to submit specific reforms as the country runs out of cash and faces debt payments and monthly salary obligations in the coming weeks.

Germany said Wednesday that an aid payment from the bailout fund won’t happen this month, and that Greece’s negotiations with creditors have failed to move forward. “I said last time that there has been progress, but that really there is still a considerable need for negotiations,” Friederike von Tiesenhausen, a German Finance Ministry spokeswoman, said. “Things have not really changed.” Greece’s credit rating was lowered one level to CCC+, with a negative outlook, by S&P, which estimated that the country’s economy contracted close to 1% in the past six months. The downgrade leaves the nation’s rating seven steps into junk territory.

“..taxes might have to go up to cover a $25bn budget black hole caused by falling commodity prices..” “..BHP Billiton and Rio Tinto launched a huge expansion which saw mining investment as a percentage of the Australian economy peak at a whopping 7% in 2012. ”

• Australia’s Economy: Is The Lucky Country Running Out Of Luck? (Guardian)

After 24 years of uninterrupted economic growth, Australia is entering the kind of difficult waters experienced by every other major developed country in the past decade. Even if Thursday’s unemployment figures show more jobs were added last month, the Coalition is set to go into the next election with an unusually gloomy outlook. Australians are finding it harder to get a job than at any time in more than decade and those who are in work are seeing the weakest wage growth for two decades. There are even fears that taxes might have to go up to cover a $25bn budget black hole caused by falling commodity prices. As one leading economist put it, the lucky country is running out of luck. Growth is still on target for a healthy at 2.8% for this year, according to the IMF, the kind of number that would send European leaders scrambling for the tweet button.

But the question of whether Australia loses its remarkable record of continuous growth depends, as with almost everything else in the economy, on what happens in China. “Australia has gone 24 years without a recession thanks to good management and good luck,” said Saul Eslake at BoA in Sydney. “Up to the early 2000s it was managed well and then it wasn’t. But then the luck improved because of China’s huge stimulus after the global financial crisis. Now the luck is running out.” The slowdown in the world’s second biggest economy is now well and truly underway. Demand for Australia’s iron ore and coal has plummeted from a decade ago as Beijing seeks to scale back its huge building schemes and create a more consumer-led economy. The price of the steel-making commodity, Australia’s biggest export, has fallen from $130 at the start of 2014 to around $50. Coal has halved in price in the past four years.

Buoyed by the good times, resource companies led by BHP Billiton and Rio Tinto launched a huge expansion which saw mining investment as a percentage of the Australian economy peak at a whopping 7% in 2012. The new output from their giant mines in Western Australia is now hitting the market, making export figures look healthy but adding to the pressure on prices and leaving Australia with a potentially wretched hangover.

How does this not violate the Minsk agreement?

• US Military Lands in Ukraine (Ron Paul Inst.)

Paratroopers from the US Army’s 173rd Airborne Brigade have arrived in Ukraine to begin training that country’s national guard and provide it with new military equipment. The Ukrainian government took power in a US-backed coup in early 2014 and has waged war on eastern provinces that wish to breakaway from what they see as an illegitimate government. The US military action, dubbed “Operation Fearless Guardian,” will improve the Washington-backed faction’s ability to wage war against the breakaway regions, but at least in spirit will violate the “Minsk II” ceasefire agreement which mandates a “pullout of all foreign armed formations, military equipment.”

The US military involvement on behalf of the US-backed government in Kiev comes at a key time in the shaky ceasefire. The Organization for Security and Cooperation in Europe (OSCE) has noted a serious increase in fighting in the breakaway eastern regions of Ukraine and OSCE monitors have pointed the finger at US-backed Kiev as the instigator of these new attacks. The relevant OSCE report finds:

…that the Ukrainian side (assessed to be the Right Sector volunteer battalion) earlier had made an offensive push through the line of contact towards Zhabunki (“DPR”-controlled, 14km west-north-west of Donetsk…

The US military’s “Operation Fearless Guardian” will ultimately involve some 300 US Army personnel “training three battalions of Ukrainian troops in a range of infantry tactics.” With Ukraine’s US-backed president promising to “retake” the breakaway regions in the east despite having signed the ceasefire, it is clear that US training constitutes the beginning of direct US military involvement in the Ukrainian conflict. As such it is undeniably an escalation.

Well, they sure have no money to buy entirely new systems.

• Greece In Talks With Russia To Buy Missiles For S-300 Systems (Reuters)

Greece is negotiating with Russia for the purchase of missiles for its S-300 anti-missile systems and for their maintenance, Russia’s RIA news agency quoted Greek Defense Minister Panos Kammenos as saying on Wednesday. The report followed a visit by Greek Prime Minister Alexis Tsipras last week to Moscow, where he won pledges of Russian moral support and long-term cooperation but no fresh funds to help avert bankruptcy for his heavily indebted nation. NATO member Greece has been in possession of the Russian-made S-300 air defense systems since the late 1990s.

“We are limiting ourselves to replacement of missiles (for the systems),” RIA quoted Kammenos, who is in Moscow for a security conference, as saying. “There are negotiations between Russia and Greece on the maintenance of the systems … as well as for the purchase of new missiles for the S-300 systems,” he said. The Greek defense ministry in Athens later issued a statement quoting Kammenos as saying: “The existing defense cooperation programs will continue. There will be maintenance for the existing programs.”

Paid for years ago.

• Putin to Netanyahu: Iran S-300 Air Defense System is .. Defensive (Juan Cole)

Russian President Vladimir Putin spoke by phone with Israeli Prime Minister Binyamin Netanyahu Tuesday with regard to the Russian Federation’s decision to go ahead with the sale to Iran of S-300 anti-aircraft batteries. Iran bought the batteries several years ago, but delivery was delayed by Moscow because of US and international pressure. The US has led the imposition of severe economic sanctions on Iran, perhaps the most severe ever applied to any country in modern history, including having Iran kicked off the SWIFT bank exchange. In deference to US wishes, Russia did not ship the system.

Two things have now changed. First, Russia and the US are not getting along nearly as well in the wake of the Russian annexation (or reclaiming, from Moscow’s point of view) of Crimea from Ukraine and its support for ethnically Russian fighters in Ukraine’s east. In fact, the US has begun imposing sanctions on Russia. In turn, Russia no longer has great regard for US wishes. Second, the five permanent members of the UN Security Council plus Germany have concluded a framework agreement permitting Iran’s civilian nuclear enrichment program, which is aimed at imposing inspections and equipment restrictions that would make it very difficult if not impossible for Iran to break out and create a nuclear weapon.

Russia and China have been the least supportive of severe sanctions on Iran, and Russia appears to have decided that since the negotiations have reached a serious phase, it is time to go ahead with this deal, concluded some time ago. The announcement alarmed Israeli Prime Minister Binyamin Netanyahu, whose government has often hinted around that it might bomb Iran. The Putin government issued a communique that “gave a detailed explanation of the logic behind Russia’s decision…emphasizing the fact that the tactical and technical specifications of the S-300 system make it a purely defensive weapon; therefore, it would not pose any threat to the security of Israel or other countries in the Middle East.”

“..safeguard Creation … Because if we destroy Creation, Creation will destroy us!”

• Vatican Announces Major Summit On Climate Change (ThinkProgress)

Catholic officials announced on Tuesday plans for a landmark climate change-themed conference to be hosted at Vatican later this month, the latest in Pope Francis’ faith-rooted campaign to raise awareness about global warming. The summit, which is scheduled for April 28 and entitled “Protect the Earth, Dignify Humanity. The Moral Dimensions of Climate Change and Sustainable Development,” will draw together a combination of scientists, global faith leaders, and influential conservation advocates. UN Secretary General Ban Ki-moon is slotted to offer the opening address, and organizers say the goal of the conference is to “build a consensus that the values of sustainable development cohere with values of the leading religious traditions, with a special focus on the most vulnerable.”

“[The conference hopes to] help build a global movement across all religions for sustainable development and climate change throughout 2015 and beyond,” read a statement posted on several Vatican-run websites. According to a preliminary schedule of events for the convening, attendees hope to offer a joint statement highlighting the “intrinsic connection” between caring for the earth and caring for fellow human beings, “especially the poor, the excluded, victims of human trafficking and modern slavery, children, and future generations.” The gathering will undoubtedly build momentum for the pope’s forthcoming encyclical on the environment, an influential papal document expected to be released in June or July.

The Catholic Church has a long history of championing conservation and green initiatives, but Francis has made the climate change a fixture of his papacy: he directly addressed the issue during his inaugural mass in 2013, and told a crowd in Rome last May that mistreating the environment is a sin, insisting that believers “safeguard Creation … Because if we destroy Creation, Creation will destroy us! Never forget this!” The Vatican also held a five-day summit on sustainability in 2014, calling together microbiologists, economists, legal scholars, and other experts to discuss ways to address climate change.

Home › Forums › Debt Rattle April 16 2015