NPC Wilkins-Rogers Milling Co., Washington, DC 1926

“Hegel is arguing that the reality is merely an a priori adjunct of non-naturalistic ethics..”

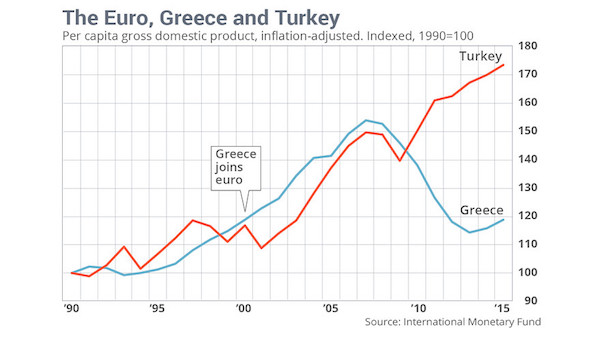

• Germany vs Greece: “Marx Is Claiming It Was Offside” (WaPo)

Many top English-speaking economists are either alarmed or aghast over Europe’s handling of the crisis in Greece. Several Nobel Prize winners say it has been exacerbated, time and again, by an unnecessarily rigid approach by Germany, Europe’s economic powerhouse and decision-maker. Greece simply cannot repay its debts, economists argue, no matter how much the country slashes public services or raises taxes. So by insisting it keep on trying, the thinking goes, Germany seems to be intent on punishing Greece. The Germans see it differently, saying what they are doing may be painful, but necessary, to get the country on a sustainable footing for the long term. To understand the massive gap in opinion, it might help to watch a Monty Python sketch from 1974 about a soccer match between Germany and Greece.

In the match, the two countries are represented by their foremost philosophers. For much of the game, the two sides do nothing but talk. Then, in the final minute, there is movement. Socrates scores past German goalie Gottfried Wilhelm Leibniz, who lived from 1646 to 1716, to win. The German philosophers G.W.F. Hegel, Immanuel Kant and Karl Marx then dispute the goal with the referee, Confucius. “Hegel is arguing that the reality is merely an a priori adjunct of non-naturalistic ethics. Kant via the categorical imperative is holding that ontologically it exists only in the imagination,” the announcer says. “Marx is claiming it was offside.”

Exactly my argument for why Troika negotiators should all be fired: “The IMF’s report is important because it reveals that the creditors negotiated with Greece in bad faith.”

On July 2, the IMF released its analysis of whether Greek debt was sustainable or not. The report said that Greek debt was not sustainable and deep debt relief along with substantial new financing were needed to stabilize Greece. In reaching this new assessment, the IMF stated it had learned many lessons. Among them: Greeks would not take adequate structural reforms to spur growth, they would not sell enough of their assets to repay their debt, and they were unable to undertake sufficient fiscal austerity. That left no choice but to grant Greece greater debt relief and to provide new financing to tide Greece over till it could stand on its own feet. The relief, the IMF, says must be provided by European creditors while the IMF is repaid in whole.

The IMF’s report is important because it reveals that the creditors negotiated with Greece in bad faith. For months, a haze was allowed to settle over the question of Greek debt sustainability. The timing of the report’s release—on the eve of a historic Greek referendum, well after the technical negotiations have broken down—suggests that there was no intention to allow a sober analysis of the Greek debt burden. Paul Taylor of Reuters tells us that the European authorities worked hard to suppress it and Landon Thomas of the New York Times reports that, until a few days ago, the IMF had played along. As a result, the entire burden of adjustment was to fall on the Greeks before any debt reduction could even be contemplated. This conclusion was based on indefensible economic logic and the absence of the IMF’s debt sustainability analysis intentionally biased the negotiations.

As an international organization responsible for global financial stability, it is the IMF’s role to explain clearly and honestly the economic parameters of a bailout negotiation. The Greeks, many said, benefited from low interest rates and repayments stretched out over many years. Therefore, no debt relief was needed. But, of course, as the IMF now makes clear, if a country has to repay about 4 percent of its income each year over the next 40 years and that country has poor growth prospects precisely because repaying that debt will lower growth, then debt is not sustainable. If this report had been made public earlier, the tone of the public debate and the media’s boorish stereotyping of Greeks and its government would have been balanced by greater clarity on the Greek position.

Ambromance.

• EU Warns Of Armageddon If Greek Voters Reject Terms (AEP)

Greece risks a collapse of the medical system, power black-outs, and an import blockade, if the Greek people reject creditor demands in a make-or-break referendum tomorrow, the EU’s highest elected official has warned. Martin Schulz, the president of the European Parliament, said the EU authorities may have to prepare emergency loans to keep basic public services functioning and to prevent the debt-stricken country spinning out of control next week. “Without new money, salaries won’t be paid, the health system will stop functioning, the power network and public transport will break down, and they won’t be able to import vital goods because nobody can pay,” he said. Mr Schulz earlier called for the elected Syriza government to be replaced by “technocrat” rule until stability is restored.

The alarmist warnings are part of an escalating pressure campaign by European leaders as Greeks decide their destiny in what has become – despite attempts by Syriza to present it otherwise – an in-out vote on euro membership after five years of economic depression and mass unemployment. Yanis Varoufakis, the Greek finance minister, said his country is on “war-footing” and accused the eurozone of trying to terrify Greek voters into submission. “What they’re doing with Greece has a name: terrorism. Why have they forced us to close the banks? To frighten people. It’s about spreading terror,” he told El Mundo. The complete break-down in trust between Syriza and the EU-IMF inspectors comes as polls show the “No” side neck and neck, each driven by powerful emotions in the bitterly divided country.

An estimated 40,000 people gathered for a rally for “No” side on Friday in front of the Greek parliament, drawn by a star-casting of Greek singers and defiant appearance by premier Alexis Tsipras. Some 18,000 thronged a nearby stadium for the “Yes” campaign, blowing whistles and waving Greek and EU flags, many afraid that Greece would be blown out of the EU altogether after 34 years, and cast into oblivion. The crisis has reached a point where the Greece’s manufacturing system is grinding to a halt. Crucial imports and raw materials have been stuck in ports since imposition of capital controls and the shut-down of the banking system a week ago. Industrialists cannot pay suppliers outside the country unless they are deemed a top priority by an emergency payments committee at the Greek treasury.

“..why would you dig around under the sofa and behind the fridge to find the last few pennies so you could ship them off to Brussels?”

• Why I’d Vote ‘No’ On Greece’s Referendum (Brett Arends)

While America celebrates its Declaration of Independence this weekend, the people of Greece are preparing for their own awesome display of democracy. Sunday’s referendum in Greece is about much more than economics, financial reform and the terms of debt repayments.It is about Greek independence — or its continued submission to the dictatorship of the so-called troika.The Greeks will make their own decisions. But if I were among them, I would certainly vote “no” to the troika. It isn’t even difficult. Here’s why.

1. Six years of a Great Depression is enough. Greek output has fallen 25% since the crisis began. Imports have plunged by 40%. A million people have lost their jobs. The official unemployment rate is now 25%, and it is north of 60% among young people. This is a social catastrophe. It is destroying jobs and lives. It is serving no purpose. Enough is enough.

2. If austerity were going to work, it would have done so by now. The Greek government has already tightened its belt even more than demanded, as the IMF has admitted. The country has turned big government deficits into government surpluses (before interest payments). When they struck their deal with the troika in 2010, the Greeks were expected to cut their gross national debts by this year to $350 billion. Instead, they’ve cut them down to $316 billion, 10% lower. They’ve tightened so far that by last summer the price of Greek government bonds had rallied 400% from their crisis lows. Belt tightened. House in order. Confidence restored. Right? Yet the economy has just kept going down and down and down.

3. The troika is crazy.They keep doing the same thing over and over again and expecting different results. In 2010, they said a policy of austerity would produce a “V-shaped” recovery. Ha ha! In 2013, they took another look at the situation and basically concluded: • The Greeks have done everything we asked of them and more. • It hasn’t worked. • Huh. How ’bout that? Their prescription: more austerity. And here we are again in 2015. The economy’s even worse. The solution? Er … even more austerity. Would you really take the advice of a crazy doctor?

4. Austerity doesn’t make sense anyway.It’s based on single-entry book-keeping — or the logical “fallacy of composition,” the belief that the whole is just a bigger version of each individual part. Yes, any person can make himself richer by raising his income and cutting his spending. But a society overall can’t do that, because my spending is your income and your spending is my income. Simple math. It’s like thinking that everyone at the poker table can win by playing well. So even if the Greek government keeps balancing its budget, that alone won’t make Greece overall somehow richer. It will simply transfer money from the private sector to the state (and thence to Brussels).

For that matter, while any person can run out of money, a country can’t. It doesn’t make any sense. Money is an accounting system — a form of IOU. How can everyone be forced to sit at home twiddling their thumbs because “there isn’t any money to go around”? And why, if that were the case, would you dig around under the sofa and behind the fridge to find the last few pennies so you could ship them off to Brussels?

It’s getting scary out there.

• How a Greek Default Could Hammer Bonds (Carl B. Weinberg)

Greece is on the verge of defaulting on €490 billion in loans, bond obligations, central-bank liquidity assistance, and interbank balances. Who will bear those losses? Greece’s creditors, which are all public entities across the euro zone, and that are on the hook for some €335 billion in loan guarantees. How will those losses be covered? Bonds will have to be sold that will roughly equal the increase in annual debt purchases by the European Central Bank announced last January. This is a hit to the European financial system nearly as big as Lehman Brothers’ balance sheet was in 2008. There are precious few alternatives left for Greece or Prime Minister Alexis Tsipras. His government has walked out of talks with its creditors, and he has called a national referendum for July 5.

Its choices are to accept “help” in the form of new loans to replace old loans (and accept austerity conditions), negotiate a debt restructuring with creditors, or default. The government has said it doesn’t want new loans—it wants debt relief. An IMF report on Thursday said that without at least $36 billion in new money over the next three years, Greece can’t meet its obligations without debt reduction. The government appears ready to renege on its debt obligations. So Greece’s creditors are going to lose money—a lot of money. Since these creditors are public entities, the losses will be borne, initially, by the public. You can’t find public-sector exposure in the national accounts of lending governments because they are off-balance-sheet contingent liabilities that don’t exist until they are needed.

But they add up to hundreds of billions of euros in guarantees for everything from the European Stability Mechanism, or ESM, to the ECB, to the interbank clearing system. Bonds will have to be sold to cover those markers. Issuance on this scale promises to be a blow for a market already vulnerable to a price correction. Talks between the Greek government and its creditors have nothing to do with saving Greece or bailing it out. This crisis is about managing the resolution of bad Greek assets in a way that inconveniences creditor governments the least, forcing the least net new public borrowing, and minimizing financial system risks. The best way to do that is to avert a hard default, even if it means kicking the can down the road.

Consider the ESM, Greece’s biggest creditor. Under its previous name, the European Financial Stability Facility, it loaned Greece €145 billion. If Greece defaults, the ESM, a Luxembourg corporation owned by the 19 European Monetary Union governments, will have to declare loans to Greece as nonperforming within 120 days. Accounting rules and regulators insist that financial institutions write off nonperforming assets in full, charging losses against reserves and hitting capital. Here’s the rub: The ESM has no loan-loss contingency reserves. Its only assets—other than loans to Greece—are loans to Ireland and Portugal. Its liabilities are triple A-rated bonds sold to the public.

How do you get a triple-A rating on a bond backed entirely by loans to junk-rated sovereign borrowers? Well, the governments guarantee the bonds, and because they are unfunded off-balance-sheet liabilities, they aren’t counted in their debt burdens—unless borrowers default. If Greece defaults hard, governments will be on the hook for €145 billion in guarantees on those loans to the ESM. We expect credit-rating agencies to insist that these unfunded guarantees be funded. After all, unfunded guarantees are worthless guarantees.

Forgot one: Marine Le Pen. A much bigger crisis than Britain could ever be.

• Quartet Of Crises Threatens Europe’s Core (Reuters)

Four great crises around Europe’s fringes threaten to engulf the European Union, potentially setting the ambitious post-war unification project back by decades. The EU’s unity, solidarity and international standing are at risk from Greece’s debt, Russia’s role in Ukraine, Britain’s pursuit of opt-outs and Mediterranean migration. Failure to cope adequately with any one of these would worsen the others, amplifying the perils confronting “Project Europe”. Greece’s default and the risk, dubbed ‘Grexit’, that it may crash out of the shared euro currency is the most immediate challenge to the long-standing notion of an “ever closer union” of European states and peoples.

“The longer-term consequences of Grexit would affect the European project as a whole. It would set a precedent and it would further undermine the raison d’être of the EU,” Fabian Zuleeg and Janis Emmanouilidis wrote in an analysis for the European Policy Center think-tank. Though Greece accounts for barely 2% of the euro zone’s economic output and of the EU’s population, its state bankruptcy after two bailouts in which euro zone partners lent it nearly €200 billion is a massive blow to EU prestige. Even before the outcome of Sunday’s Greek referendum was known, the atmosphere in Brussels was thick with recrimination – Greeks blaming Germans, most others blaming Greeks, Keynesian economists blaming a blinkered obsession with austerity, EU officials emphasizing the success of bailouts elsewhere in the bloc.

While its fate is still uncertain, Athens has already shown that the euro’s founders were deluded when they declared that membership of Europe’s single currency was unbreakable. Now its partners may try to slam the stable door behind Greece and take rapid steps to bind the remaining members closer together, perhaps repairing some of the initial design flaws of monetary union, though German opposition is likely to prevent any move toward joint government bond issuance. The next time recession or a spike in sovereign bond yields shakes the euro zone, markets will remember the Greek precedent.

€1 trillion.

• Europe Can’t Afford To Let Athens Go Under, Says Varoufakis (Reuters)

Europe will lose a trillion euros if it allows Greece to go under, the country’s finance minister said on Saturday, accusing creditors of ‘terrorizing’ Greeks into accepting austerity in a referendum on bailout terms. After a week in which Greece defaulted, closed its banks and began rationing cash, Greeks vote on Sunday on whether to accept or reject tough conditions sought by international creditors to extend a lending lifeline keeping the country afloat. Their decision could determine Greece’s future as a member of the single currency. Addressing a crowd of over 50,000 in central Athens, left-wing Prime Minister Alexis Tsipras urged them to spurn the deal, rejecting warnings from Greece’s European partners that this may bring an exit from the euro and even greater hardship.

A slew of opinion polls on Friday gave the “Yes” camp, which favors accepting the bailout terms, a slender lead but all were within the margin of error and pollsters said the vote was too close to call. Only one had the “No” vote advocated by the government winning. Tsipras’ finance minister, Yanis Varoufakis, said there was too much at stake for Europe to cast Greece adrift. “As much for Greece as for Europe, I’m sure,” Varoufakis told the Spanish newspaper El Mundo. “If Greece crashes, a trillion euros (the equivalent of Spain’s GDP) will be lost. It’s too much money and I don’t believe Europe could allow it.” “What they’re doing with Greece has a name: terrorism,” said Varoufakis. “Why have they forced us to close the banks? To frighten people. And when it’s about spreading terror, that is known as terrorism.”

Athens’ 18 partners in the euro zone say they can easily absorb the fallout from losing Greece, which accounts for barely 2% of the bloc’s economic output. But it would represent a massive blow to the prestige of Europe’s grand project to bind its nations into a union they said was unbreakable. “For Europe, this would be easy to manage economically,” Austrian Finance Minister Hans Joerg Schelling said in an interview with online newspaper Die Presse. For Greece, however, “it would indeed be considerably more dramatic.” Schelling said Greece would need humanitarian aid in case of a Grexit but described fears of widespread poverty as exaggerated and part of “a propaganda war”.

“The consequence, as Greece heads in to a momentous referendum Sunday, is a country broken both socially and economically.”

• Mirage of Economic Turnaround Masked New Greek Crisis in the Making (WSJ)

Last year, Greece looked as if it were on the way up. The economy was growing—at one point, faster than Germany’s. International investors jostled to buy the government’s bonds. Banks were rebuilding. Politicians talked about a “clean exit” from Greece’s yearslong bailout: no more loans, no more money, no more humiliating reviews by bureaucrats from Brussels. But many Greeks were still on the way down. Katerina Papalevizopoulou was out of work. Her husband had lost his job driving a truck and was driving a cab. In 2014, he made around €7,000 ($8,000), down from €9,000 the year before and half of what he had earned in 2008. They owe €70,000 on a mortgage on their apartment here. They sold their wedding rings. They sent their car to the scrap yard, for €250. They sent their boy, now 10, to live with his grandparents outside the city.

“I don’t want my son to be around this,” Ms. Papalevizopoulou says in their small and cluttered apartment. “If you want to look at my fridge, my pantry, it is empty,” she says. She apologizes that she has nothing to offer visitors. “The priest brings me food,” she says. For many Greeks, any economic improvement has been a mirage, even before the financial chaos of recent weeks. Debt burdens have become harder to bear. Wages have tumbled, pushed down by policies intended to make Greek workers more competitive internationally. Social services have been cut to help close the budget gap. As a result, Greek households have cut their own spending—and they have fallen behind on their debts. The consequence, as Greece heads in to a momentous referendum Sunday, is a country broken both socially and economically.

The rupture has helped elevate Alexis Tspiras, leader of the radical-left party Syriza, to prime minister. It has also been a force behind him as he has urged Greece to vote “no” to a deal with its European creditors. And no matter what outcome—a break with Europe or a rapprochement—the economic devastation means Greece will need a lot of fixing. Its banking system may be first in line, and a look at the country’s mortgage market shows why. When it entered the euro in 2001, Greece had a relatively small amount of consumer borrowing: Its banks had extended €24 billion in loans to domestic households at the end of that year. By the end of 2009, just before the debt crisis exploded, the figure had quadrupled to €99 billion.

Greece has high rates of homeownership, which Greek banks have financed with mortgages. Those are now in trouble. The crumbling economy has pushed many in the middle class to the lower middle class and many in the working class into poverty. Delinquencies on loans have soared. The four big Greek banks reported in the first quarter that between 32% and 39% of their Greek loans were nonperforming. And the pace of souring loans appears to have increased sharply this year: National Bank of Greece, the country’s largest lender, reported that €154 million in Greek mortgages became overdue, by 90 days or more, in the fourth quarter of last year. For the first quarter of this year, the figure jumped to more than €280 million.

Germans are sold a story that sells well. But fair or realistic it is not.

• Our Heretic (And Not-So-Simple) Views On The Greek Referendum (ZH)

Conventional wisdom has it as follows: Tsipras is a hardline communist, who overplayed his hand with the troika (or “the three institutions”, as he calls them). The referendum was a last-ditch play to retain power by stoking a nationalistic response to the standoff with creditors. We believe the current stand-off with Greece’s creditors is just part of the ongoing tug-of-war between Germany and the IMF on a possible haircut on Greek debt. The background of this conflict is as follows: the US (which exerts substantial influence on the IMF) is “pro Keynesian” while Germany is “pro austerity”.

The slowdown in the European economy is obviously affecting the US economy as well; hence the US interest is clearly justified. The USA has been nudging Europe to engage in some good-old Keynesian deficit-spending. Obviously, the deficit spending does not need to happen in Germany, whose economy is doing very well, thank you. It needs to happen in places like Greece, but then the question arises, how could this deficit be financed? Well, the markets are certainly not willing to finance Greece, so that leaves few people in the room able to do this. Rich Germany obviously comes to mind, but then this is a major no-no for German voters and politicians.

(West) Germany engaged in the mother of all expansionary policies (and fiscal transfers) at the time of reunification with East Germany, when it set a 1:1 conversion rate of the East German mark into the DEM, while the exchange rate applicable for East German exports had been at 1 to 4.3. Rightly or wrongly, it is widely accepted in Germany that the dismal performance of Germany during the rest of nineties is due to those very policies— justifiable perhaps at the time by a duty of solidarity. Quite understandably, the German public doesn’t feel such a strong duty of solidarity vis-à-vis Greece. Any German politician suggesting a large-scale fiscal transfer to Greece would be skewered. Any haircut on Greek official-sector debt would be seen as (and be) just that: a fiscal transfer to Greece.

One last background note: the German public seems convinced that Germany has already paid its dues when it comes to Greece. This is only partially true: the restructuring of Greek debt was at its heart an effort to convert private unsustainable debt into official unsustainable debt –saving major European banks in the process (including Deutsche Bank, which managed to stay afloat by engineering achieving a risk-weight asset density of 14% in 2008).

It was St. Augustine who said: Charity Is No Substitute For Justice Withheld.

• Euro Area Said to Weigh Push for Aid Deal Even If Greeks Vote No (Bloomberg)

Euro-area finance ministers may be ready to start work on a third bailout agreement for Greece after Sunday’s referendum, even if voters reject the bloc’s last aid proposal, according to two officials familiar with negotiations. A broad majority of finance chiefs have agreed to examine an official request from Greek Prime Minister Alexis Tsipras for aid from the European Stability Mechanism, the people said, asking not to be identified because the talks are confidential. That process could begin as soon as next week, one of them said. Officials on both sides of the negotiations are preparing to accelerate efforts to release aid for Greece irrespective of whether voters reject creditors’ aid terms in the referendum or inflict a defeat on the Tsipras government by delivering a “yes” vote.

With the banking system on lock down to shield it from deposit outflows ahead of the ballot, polls suggest the result is too close to call. The Eurogroup is waiting for the outcome of the referendum, a spokesman for Jeroen Dijsselbloem, the Dutch finance chief who leads meetings of euro-area ministers, said in a text message. While European leaders have framed the referendum as a vote on Greece’s future in the euro, the cost of a Greek exit may ultimately be greater than the bill for keeping the country in the currency. Finance ministers are no longer contemplating a Greek exit, said one of the officials. “We’re waiting for the referendum result,” German Finance Ministry spokesman Martin Jaeger told reporters in Berlin. “An ESM program would depend on a request from the Greek government.” Activating the ESM “is not a straightforward process,” he said.

The quickest way to release aid for Greece may be to hand over €3.3 billion in profit that the ECB made buying Greek debt during an earlier phase of the crisis. Finance ministers and some national parliaments would need to approve such a payment, which would likely be part of a broader third bailout deal. Greek Finance Minister Yanis Varoufakis said Friday he expects a deal to be done even if voters reject the euro area’s latest offer. Finance ministers discussed the request for a third bailout during a conference call on July 1. One of the officials said that Dijsselbloem intends to ask Greece’s creditors to make a swift assessment of any new proposals to speed up a disbursement. “We will come back to your request for financial stability support from the ESM only after and on the basis of the outcome of the referendum,” Dijsselbloem wrote in a July 1 letter to Tsipras.

“Oh, and if France gets downgraded, Germany’s pro rata share of funding the EFSF jumps to a mindboggling €1.385 trillion, or 56% of German GDP!”

• The Greek Bluff In All Its Glory: Presenting The Grexit “Falling Dominoes” (ZH)

Earlier today, Yanis Varoufakis reiterated his core thesis driving the entire Greek approach from day 1 of its negotiations with the Eurogroup: “Europe [stands] to lose as much as Athens if the country is forced from the euro after a referendum on Sunday on bailout terms.” This is merely a recap of what we said 4 years ago when in July of 2011 we explained “How Euro Bailout #2 Could Cost Up To 56% Of German GDP”, recall:

… the bottom line is that for an enlarged EFSF (which is what its blank check expansion today provided) to be effective, it will need to cover Italy and Belgium. As AB says, “its firepower would have to rise to €1.45trn backed by a total of €1.7trn guarantees.” And here is where the whole premise breaks down, if not from a financial standpoint, then certainly from a political one: “As the guarantees of the periphery including Italy are worthless, the Guarantee Germany would have to provide rises to €790bn or 32% of GDP.” That’s right: by not monetizing European debt on its books, the ECB has effectively left Germany holding the bag to the entire European bailout via the blank check SPV.

The cost if things go wrong: a third of the country economic output, and the worst case scenario: a depression the likes of which Germany has not seen since the 1920-30s. Oh, and if France gets downgraded, Germany’s pro rata share of funding the EFSF jumps to a mindboggling €1.385 trillion, or 56% of German GDP!

Several years later, in anticipation of precisely the predicament Europe finds itself today, the ECB did begin to monetize European debt, which has since become the biggest European risk-shock absorber of all, and the one which the ECB is literally betting the bank on: just count the number of times the ECB has sworn it has the tools and can offset any Greek risk contagion simply by buying bonds. Unfortunately, it is not that simple.

The reason is precisely in the contagion threat inherent in Europe’s alphabet soup of bailout mechanism as we explained four years ago in the post above, and as Carl Weinberg of High-Frequency Economics did hours ago in today’s edition of Barrons. Here is how the Greek contagion would spread, laid out in all its simplicity, should there be a Grexit, an outcome which the ECB could catalyze as soon as Monday in case of a “No” vote by raising ELA collateral haircuts:

The [Greek] government appears ready to renege on its debt obligations. So Greece’s creditors are going to lose money—a lot of money. Since these creditors are public entities, the losses will be borne, initially, by the public.

This crisis is about managing the resolution of bad Greek assets in a way that inconveniences creditor governments the least, forcing the least net new public borrowing, and minimizing financial system risks. The best way to do that is to avert a hard default, even if it means kicking the can down the road.

That, once again, is the Varoufakis all-in gamble, a gamble which assumes the ECB will be rational enough (in a game theory context) to appreciate the fallout of a Grexit on Europe’s creditors.

Oh, that young Farrell guy again…

• 4th of July Fireworks: World War III With China Dead Ahead (Paul B. Farrell)

World War III? OK, so you’re distracted by Trump vs. Christie? By Wall Street hyping a bull-market recovery? So we forget war, they’re “over there,” nightly news clips of faraway killer bombs. Wrong, WWIII really is getting closer. At the launch of the Iraq War, the Bush team warned us of the “mother of all national security issues … by 2020 there is little doubt that something drastic is happening … warfare defining human life.” Pentagon generals are planning ahead for that 2020. But most Americans are more interested in their next gadget. Wake up. USA Today headline: “CIA veteran Morell: ISIS’ next test could be a 9/11-style attack.” That warning’s from an insider with George W. Bush in 2001 when hijacked airliners hit the World Trade Center. Twice acting CIA director, says USA Today’s Susan Page.

With Obama in the situation room when word came “Navy Seal Team Six had killed Osama bin Laden.” Morell’s new book, “The Great War of Our Time: The CIA’s Fight Against Terrorism From Al Qa’ida to ISIS,” makes clear America is already fighting World War III today. Worse, WWIII will go on for decades, “for as far as I can see,” says the CIA insider. Yes, WWIII is hot news with the Pentagon brass. The Wall Street Journal just reviewed “The Ghost Fleet” by Peter Singer and August Cole. Singer’s “one of Washington’s pre-eminent futurists.” He’s now “walking the Pentagon halls with an ominous warning for America’s military leaders: World War III with China is coming.”

In fact, even America’s advanced new F-35 fighter jets may be “blown from the sky by their Chinese-made microchips and Chinese hackers easily could worm their way into the military’s secretive intelligence service … and the Chinese Army may one day occupy Hawaii.” Speculation? No, the Journal’s Dion Nissenbaum reminded us Chinese hackers have already got into “White House computers, defense industry plans and millions of secret U.S. government files.” Singer’s “written authoritative books on America’s reliance on private military contractors, cybersecurity and the Defense Department’s growing dependence on robots, drones and technology,” and why that puts national security at high risk.

“How surreal do the signs and warnings have to become before we stop in our tracks? Are whales required to fall from the sky?”

• It’s Too Late To Save Our World, So Enjoy The Spectacle Of Doom (Guardian)

In the middle of a week of record temperatures, as if unaware of the irony, the business community celebrated the consolidation of its attempts to force the government’s hand to agree to a third filth-generating runway at Heathrow, tipping all species on Earth towards extinction. Everything will die soon, except for cockroaches, and Glastonbury favourite the Fall, who will survive even a nuclear holocaust, though they will still refuse to play their 80s chart hits. In Norfolk on Thursday, the tarmac melted, and ducklings became trapped in sticky blackness. When a lioness whelped in an ancient Roman street, Caesar thought something was up. Here, solid matter transmuted to hot liquid and swallowed baby birds whole. How surreal do the signs and warnings have to become before we stop in our tracks?

Are whales required to fall from the sky? Does Tim Henman have to give birth to a two-headed cat on Centre Court? CBI director John Cridland says: “The government must commit to the decision now, and get diggers in the ground at Heathrow swiftly by 2020.” Head of the Institute of Directors Simon Walker says: “There can now be no further delay from politicians.” And Segro chief executive David Sleath merely bellows: “Get on with it!”, like some selfish Top Gear presenter demanding his steak dinner after dawdling, the planet itself the powerless BBC employee he punches in the face. The business community has thrown its executive toys out of the pram, and now there are chrome ball bearings on strings everywhere, tripping up unpaid interns and making life difficult for immigrant cleaners scrabbling under desks on less than minimum wage.

David Cameron, an electoral promise to oppose the third runway sticking in his throat like an undigested salmon bone, can only duck his cowardly head and hope some terrible atrocity or a Wimbledon win wafts our attention away. When I was a child, my grandmother always referred to our pet dog’s excrement as “business”, so to this day, when I envisage “the business community”, I imagine a vast pile of sentient faeces issuing its demands while smoking a Cuban cigar, an image that seems increasing accurate as the decades pass. The destruction of all life on Earth is inevitable if fossil fuel use continues unabated. (Legal. Please advise. Are we allowed to say this now without being shouted down by Nigel Lawson?)

The business community’s genius move in the third runway debate has been to change the dialogue from an argument which should have been between building a runway and not building a runway at all, and trying to restructure our society to avoid the need for a third runway, into an argument about where exactly it was best to position this massive portent of our world’s forthcoming doom. It’s like offering an innocent man who doesn’t want to be hanged the chance to be poisoned instead.

Home › Forums › Debt Rattle July 5 2015