Max Ernst Untitled 1913

With a 12-hour delay, Vladimir Putin has declared a partial mobilization in Russia (300,000 reservists?!), citing the need to protect a 1,000 km frontline with Ukraine. Details will be forthcoming. Lots of rumors swirling around, the most interesting of which is perhaps that Central Bank Governor Elvira Nabiullina allegedly submitted her resignation. A condition for her staying on was no mobilization. How she feels about this partial one we will find out.

One thing that is obvious is that it is no longer Russia vs Ukraine. That 1,000 km frontline requires a lot of non-Ukrainian forces and weapons. Obviously, the upcoming elections in four Ukraine regions, perhaps as soon as this weekend, carry the potential of Russia needing to protect these regions vs attacks. They have largely Russian populations, and Putin is sworn to protect these people.

Excess death

https://twitter.com/i/status/1572032165478801408

Szamuely

.@vonderleyen's bizarre "State of the Union" address to the European Parliament. pic.twitter.com/7VbrksgD5T

— George Szamuely (@GeorgeSzamuely) September 20, 2022

This is from yesterday, well before Putin’s speech at 8 am Moscow time:

• Russian Lawmaker Reveals Mobilization Plans (RT)

Amending the criminal code with provisions for mobilization, martial law and wartime doesn’t necessarily mean Moscow is about to declare a draft – or war, Russian lawmaker Andrey Kartapolov clarified on Tuesday. Kartapolov, who chairs the Defense Committee of the State Duma, was the co-author of the amendments the lower house of the Russian parliament approved on Tuesday. Among other things, they establish criminal penalties for crimes committed during “wartime,” “martial law,” or a “mobilization period.” Fears that this means a mobilization are “absolutely unjustified,” Kartapolov told the Parliamentary Gazette.

“There will be no general mobilization. The president has spoken about this more than once and is directly speaking through his press secretary Dmitry Peskov and many other politicians at the federal level.” Having a law is not the same thing as mobilization, Kartapolov argued, adding that the amendments were “not specifically linked to the special military operation” in Ukraine, but were designed to function “for a long time, at least until they are no longer needed.” The adopted amendments include harsher punishments for looting or going AWOL during wartime, or committing any crime during a period of military mobilization. They also criminalize the sabotage of defense contracts.

Kartapolov also confirmed that the militias of the Donbass republics would be integrated into the Russian military, in case Donetsk and Lugansk vote to join Russia later this week. This would “significantly change the situation in a number of ways,” he said. Donetsk and Lugansk declared independence in 2014, after a US-backed coup in Kiev. Moscow recognized them in February, shortly before launching the military operation in Ukraine. Territories of Zaporozhye and Kherson under the control of the Russian and Donbass troops also announced on Tuesday that they would vote to join Russia later this week.

Will Schryver thinks it’s all a done deal.

It is a foregone conclusion that Lugansk, Donetsk, Zaporozhye, and Kherson regions of the former Novorossiya will be re-assimilated into the Russian motherland. Odessa will follow at some point in the not-so-distant future. And the empire’s refusal to acknowledge the legitimacy of these developments will prove utterly irrelevant. Western media and puppet politicians can scream “Russian aggression” and “sham election” all they want, but the unadorned fact is that these regions are overwhelmingly ethnic Russians whose collective desire is to be reunited with what they view as a powerful and ascendant Russia.

In conjunction with this shrewd political act, Vladimir Putin will almost certainly announce later today a major escalation of Russian military action in Ukraine – very likely at least a partial mobilization of Russia’s as yet untapped military might. This will result in a rapid acceleration in the ongoing process of annihilation of the Ukrainian military, its mountains of NATO weaponry, and its numerous “foreign volunteers”. This, of course, presents the empire with an existential dilemma. The defeat of NATO’s proxy army, weapons, and leadership in Ukraine at the hands of the Russians will be viewed all around the world as an unprecedented defeat of American hegemony; a watershed moment that will carry with it profound geopolitical consequences.

As I have argued for months now, it will mean the end of NATO as a credible military alliance. It will mean the end of the European Union as presently constituted. In other words, a decisive defeat of the empire’s aspirations in Ukraine will be viewed in Washington, London, and Brussels as an existential threat – which it is. And, as such, it is difficult for me to envision them submissively acquiescing to the outcome.

Where better to turn for background info than the tried and tested Guardian?

• Four Occupied Ukraine Regions Plan Imminent ‘Votes’ On Joining Russia (G.)

Four Russian-occupied regions in Ukraine have said they are planning to hold “referendums” on joining the Russian Federation in a series of coordinated announcements that could indicate the Kremlin has made a decision to formally annex the territories. Moscow may be betting that a formal annexation would help halt Russian territorial losses, after a successful Ukrainian counteroffensive that has reclaimed large portions of territory in the Kharkiv region. The occupied Donetsk and Luhansk regions have said they are ready to hold “polls”, which will be universally viewed as rigged, as soon as this week, with announcements also made in Kherson and Zaporizhzhia. Some Russian media have reported that Vladimir Putin may deliver a speech on Tuesday evening on a potential annexation.

As Ukrainian troops begin making advances in the Luhansk region, Russia may be worried that it can’t win on the battlefield and threaten a potential escalation, including a formal declaration of war or even a nuclear attack, by claiming to defend its own territory. “Everything that’s happening today is an absolutely unequivocal ultimatum to Ukraine and the West,” wrote Tatiana Stanovaya, an expert on Kremlin politics and founder of R.Politik. “Either Ukraine retreats or there will be nuclear war.” “To guarantee ‘victory’, Putin is ready to hold referendums immediately in order to obtain the right (in his understanding) to use nuclear weapons to defend Russian territory.” Also on Tuesday, the Russian state Duma passed new amendments to the legal code that directly refer to “mobilisation” and “martial law” and introduce criminal liability for desertion or wilful surrender during that period.

The Kremlin has so far resisted a full mobilisation, likely due to fear of a political backlash. Now, however, it seems that the Kremlin may be willing to go further than before, including using nuclear blackmail in order to freeze the war and solidify its territorial gains in Ukraine. The decision has not been publicly adopted by the Kremlin or Vladimir Putin. However, senior Russian officials, including the former president Dmitry Medvedev, have supported calls for the referendums. In a post on his Telegram page, Medvedev, the deputy head of Russia’s security council, said that the referendums would “completely change the vector of Russia’s development for decades”. They would also prevent a future Russian leader from reversing Russian support for the Ukrainian regions, he wrote. “That is why these referendums are so feared in Kyiv and in the west,” he wrote. “That is why they need to be carried out.”

Remember that Russia declined to recognize the 2014 votes in Luhansk and Donetsk until February 2022.

• Russia Will Support Donbass Referendums – Duma Speaker (RT)

Should the Donbass republics vote to join the Russian Federation after holding public referendums, Moscow will respect that decision, Vyacheslav Volodin, chairman of the lower house of parliament, said on Tuesday. During a plenary session of the State Duma, Volodin stated: “if in the course of a direct declaration of will they say they want to be part of Russia, we will support them.” He added that the people of Donbass “must understand today that we expect them to freely express their will.” Volodin’s comments came as the leaders of the Donetsk and Lugansk People’s Republics announced that they will be holding referendums on joining Russia, with the votes set to take place between 23 and 27 September.

The Russian-controlled Kherson and Zaporozhye regions of Ukraine have also confirmed they will be holding similar referendums on the same dates. The Deputy leader of the Kherson military-civilian administration, Kirill Stremousov, stated that residents want to join the Russian Federation as soon as possible because they fear being left behind, and want “guarantees” that Moscow will protect them from Kiev’s forces.

Perhaps the main reason for the partial mobilization.

• Kiev Vows To Use Force Against Breakaway Regions (RT)

Senior officials in Kiev have dismissed as irrelevant plans for a number of current and former Ukrainian regions to hold referendums on whether to join Russia. Andrey Yermak, President Vladimir Zelensky’s chief of staff, described the proposed votes as “blackmail” by Moscow. “This is what fear of defeat looks like. The enemy is afraid and uses primitive manipulations,” he said in a post on social media on Tuesday. Yermak added that “Ukraine will solve the Russian question,” insisting this could be done “only by force.” Foreign Minister Dmitry Kuleba also downplayed news of the upcoming referendums, dismissing the move as a “sham.”

“Ukraine has every right to liberate its territories and will keep liberating them whatever Russia has to say,” he tweeted. The condemnations and threats came in response to bids by the Donetsk and Lugansk People’s Republics, as well as Ukraine’s Kherson and Zaporozhye regions, to hold referendums on the question of joining the Russian Federation. The votes could take place as early as this week. Kiev previously threatened any person who takes part in such a plebiscite with criminal prosecution. Ukrainian Deputy Prime Minister Irina Vereshchuk said participants could be sent to prison for up to 12 years.

Crystal clear.

• Peaceful Solution To Ukraine Crisis Currently Not Possible – Russia (RT)

The armed conflict in Ukraine cannot be resolved through negotiations under current circumstances, Kremlin spokesman Dmitry Peskov said on Monday, as cited by Interfax. Asked if there was a path towards a diplomatic settlement, Peskov said that “at the moment, such a prospect cannot be observed,” the news agency reported. Moscow blamed Kiev for the suspension of peace talks. In late March, the two parties discussed a draft peace agreement, which would make Ukraine a neutral state in exchange for security guarantees given by major world powers. However the Ukrainian government ended talks in April, after accusing Russian troops of having committed war crimes, an allegation that Moscow said was based on falsified evidence.

Ukrainian President Vladimir Zelensky has since declared that his country will only be satisfied by defeating Russia on the battlefield and pushing its forces from the entire territory claimed by Kiev. That includes Crimea, the former Ukrainian region that rejoined Russia after an armed coup in Kiev in 2014. Moscow considers Crimea to be under its sovereignty and its status not subject to discussions. Russian President Vladimir Putin commented on Kiev’s position last week stating: “Zelensky said publicly … that he is not ready to talk to Russia. Well, if he is not, fine by us.” Earlier this month, Ukraine launched a major military counter-offensive in the north east, forcing Russian troops to pull back from some areas. Another of Kiev’s attempts to make gains in the south was far less successful and reportedly resulted in serious casualties and loss of military equipment.

A friend pointed out that RT’s articles pop up at other places, a sort of workaround of the ban. For most articles that is not necessary, since they’re short and I can just copy them. For longer ones, I’ll try to use for instance this site, azerbaycan24.com.

• The West Is Waging A War To Destroy Russia (Kornilov)

And here comes Bucha 2.0: Another provocation where Ukraine has allegedly discovered “mass graves of victims” shortly after Russian troops have withdrawn. This time in Izium. What it amounts to is clear evidence that along with the development of the military conflict in Ukraine, the informational “special” operation against Russia is intensifying. It’s not even about Kiev’s reaction – officials there concoct primitive fakes against our state and the army non-stop, around the clock. The indicator here is the way in which this provocation was immediately picked up by Western politicians, who are already urgently calling for an “international tribunal” to punish Russia. Meanwhile, the West’s media, in a united push, is putting unfounded statements about “mass executions and torture in Izium” on its front pages.

[..] Now the masks are being thrown off and the cadre of Russophobes can openly articulate their long-held dreams. The Daily Telegraph recently featured the former NATO commander in Europe, General Ben Hodges, in a high-profile article about preparing for Russia’s disintegration. Hodges, who is employed by CEPA – a lobby group bankrolled by US arms contractors and NATO – is arguably one of the most active ‘talking heads’ about the Ukrainian crisis on Western television right now. The general hopes the collapse of our state will be fueled by our ethnic diversity and he hopes that Western economic sanctions will create a situation in which it will be impossible to feed 144 million people. The American has clearly not thought how these arguments could also be applied to his home country, which has been torn apart by racial divisions in recent years.

Below Hodges, the idea has been cheerfully picked up by less well-known figures operating on the ideological field of Russophobia. The Polish magazine New Eastern Europe published an article about deconstructing Russia and reconstructing the “post-Russian space,” calling it a risky but inevitable scenario. The authors called on the West to lead the process of our state’s disintegration right away. This is echoed by the Canadian-British professor Taras Kuzio on the pages of the Atlantic Council, a NATO-aligned pressure group and the main mouthpiece of Western Russophobes. He, too, cheerfully declares that the process of “the collapse of Putin’s Russian empire” has begun.

Hodges’ theses are repeated almost word for word by Estonia’s top Kremlinologist Vladimir Yushkin on the pages of the website of the International Centre for Defence and Security. However, he adds nonsense about the allegedly developing “colonization of Siberia by the Chinese” –which tells us he doesn’t know how to use statistics.

Anti-aircraft defenses on the ground. But a one-sided claim.

• US General Claims Huge Ukrainian Successes In Air (RT)

Ukrainian forces have prevented Russia from gaining air superiority over the frontline in their country, while causing serious damage to Russian air power, a four-star US general reportedly claimed. Soviet-built anti-aircraft defenses fielded by Ukraine have managed to shoot down at least 55 Russian aircraft, Gen. James Hecker told the annual Air Force Association conference on Monday, as reported by Politico. The general, who commands the US Air Forces in Europe – Air Forces Africa (USAFE-AFAFRICA), spoke during a panel discussion about the conflict in Ukraine. Hecker said Ukraine’s use of anti-aircraft weapons has denied Russian ground forces the air support they needed. He said the situation has surprised Western military analysts. Ukraine is seeking to beef up its air defenses, and the general suggested that eastern European nations, who have old stockpiles of Soviet weapons, should transfer them to Kiev.

The top US official also claimed that Ukraine’s air force has mostly remained intact since the start of the conflict, retaining about 80% of its fleet, contrary to reports from Russia. The Russian military claims to have inflicted heavy losses on the Ukrainian air force throughout the conflict. As of Monday, it said it had destroyed 294 Ukrainian warplanes and 155 Ukrainian military helicopters. Part of the panel discussion focused on US efforts to arm Ukrainian warplanes with AGM-88 High Speed Radiation Missiles (HARM) anti-radiation missiles, which were recently included in US arms shipments to Kiev. Hecker said fitting the US-made weapons to Soviet-made aircraft “was quite an effort” for US military contractors and acknowledged that shooting them from F-16s was a better option, according to Breaking Defense outlet.

“.. it could take two to three years before Kiev could actually get them..”

• Ukraine Unlikely To Get US F-16s Soon – Politico (RT)

If the US decides to provide Ukraine with F-16 fighter jets, it could take two to three years before Kiev could actually get them. That’s according to a Politico report, citing US Air Force General James Hecker. Hecker, who heads US Air Forces in Europe – Air Forces Africa (USAFE-AFAFRICA) is said to have made the prediction during a speech on Monday at an annual Air Force Association conference. According to Politico, Hecker put the delay down to logistical and training issues, but said he believed that Ukraine could get the US-made warplanes sometime in the future, because “folks are starting to think more long term.” The outlet reported last week that the US government was considering sending F-16s and Patriot long-range anti-aircraft missiles to Ukraine, expecting that the conflict with Russia would last for years.

Washington has stepped up its arms shipments throughout the conflict, eventually agreeing to provide multi-launch rocket systems, such as HIMARS, as well as long-range artillery platforms. The US has been sending increasingly heavier weapons to Kiev, stating that it would provide military aid for as long as it takes to push Russian forces from every part of the territory that Ukraine claims under its sovereignty. However, the Pentagon has so far refrained from sending some of its more sophisticated weapons, such as heavy armor or fighter jets, instead agreeing to facilitate transfers of Soviet-era equipment from third countries such as Poland and the Czech Republic.

“..how dumb is the idea that we can punish Putin by pushing millions of German families into poverty and destroy our economy..”

• Germany’s Die Linke On Verge Of Split Over Sanctions On Russia (G.)

Germany’s Die Linke could split into two parties over the Ukraine war, as the ailing leftwing party’s indecisive stance over economic sanctions against Russia triggered a series of high-profile resignations this week. The German Left party’s future has hung in a precarious balance since it snuck into the national parliament last autumn under a special provision for parties that win three or more constituency seats. Should three of its 39 delegates resign from the party, Die Linke would lose its status as a parliamentary group and attached privileges over speaking times and committee memberships. Party insiders say such resignations are a matter of when, not if, after a week of vicious public in-fighting over a speech in which the former co-leader Sahra Wagenknecht accused the German government of “launching an unprecedented economic war against our most important energy supplier”.

Supporters of Wagenknecht, a controversial but prominent figurehead, are already hatching plans for a breakaway party to compete in the 2024 European elections, the German newspaper Taz reported this week. Such a split would be likely to spell the end of Die Linke, 15 years after it was founded in a merger between the successor to East Germany’s Socialist Unity party and former Social Democrats disillusioned by their party’s direction under Gerhard Schröder, and just under a decade after it formed the largest opposition force in the Bundestag’s 2013-17 term.

In her speech last Thursday, Wagenknecht had called chancellor Olaf Scholz’s left-leaning governing coalition “the stupidest government in Europe” because it imposed sanctions on Russia, which supplied over half of Germany’s gas needs before the start of the war in the spring. “Yes, of course the war in Ukraine is a crime”, Wagenknecht said. “But how dumb is the idea that we can punish Putin by pushing millions of German families into poverty and destroy our economy while Gazprom makes record profits?” The speech was greeted with applause not only by the Linke leadership but also by delegates of the far-right Alternative für Deutschland (AfD).

“European products are becoming uncompetitive on the world market: their price is much higher because of the cost of electricity and gas.”

• Europe’s Economy And Living Standards Are Plummeting (OR)

The ill-considered sanctions against Russia have exposed the most acute problems of Europe which is rapidly losing its economic power. A tremendous amount of businesses are on the verge of bankruptcy. A flood of migrants from Africa, the Middle East and Ukraine requires more and more budget spending. Funds are also being used to support the Kiev regime. As a result, Europe’s economies are deteriorating and living standards are plummeting. In Britain 60% of enterprises are on the verge of closing due to higher electricity prices. This is reported by the analytical group Make UK, representing the interests of British industry. 13% of British factories have reduced working hours and 7% are temporarily closing down. Electricity bills have risen by more than 100% compared to last year.

In Germany, according to the Leibniz Institute for Economic Research, the number of firms and individuals went bankrupt in August alone rose 26% compared to the same period last year. The figure was significantly higher than German analysts had forecast. According to experts, during the autumn the number of bankruptcies will only increase. This is connected with the increase of the cost of production processes, in particular with the rise in prices for energy. German Chancellor Olaf Scholz acknowledged that many Germans have faced with rising prices for fuel and food. Most countries in Europe were in a similar situation. But the authorities are sacrificing the quality of people’s lives in order to continue to exert pressure on Russia. At the same time, many experts believe the stopping of Nord Stream will cause Europe’s worst energy crisis in decades.

This circumstance has already caused a sharp rise of prices of energy resources on the European market. As a result, energy bills of European households have increased. According to Goldman Sachs’ analysts, its cumulative cost will peak in early 2023, increasing by 2 trillion euros. It has also led to a record depreciation of the European currency over the past 20 years. The increased cost of gas, heat and electricity has an adverse effect on the living standard of the people. But an even more dangerous problem is the falling liquidity of European products produced at the new cost of energy. European products are becoming uncompetitive on the world market: their price is much higher because of the cost of electricity and gas.

Attempts by EU leaders to introduce a price cap on energy from Russia have completely failed. European countries are themselves to blame for the problems they face this coming winter because of reduced gas supplies from Russia, Turkish President Recep Tayyip Erdogan said. According to him, “Europe reaps what it sows”, while Turkey “has no problems with gas supplies”.

As long as you don’t recognize Taiwan as an independent state, you’re meddling in the internal affairs of China.

• Has Biden Passed The Point Of No Return In Provoking China? (Fomenko)

It’s not the first time Biden has made such direct comments regarding American involvement in a potential conflict. It’s actually the third time in a year. Yet each time, the White House has walked back on it stating the “policy has not changed” regarding the island. But at this point in time, it can hardly be described as a gaffe worth overlooking, and Beijing is no longer likely to see it that way. In their eyes, the US policy of “strategic ambiguity” is coming to an end, with America moving irreversibly toward the de-facto support of Taiwan independence to contain China. When the United States normalized relations with the People’s Republic of China in the 1970s and accepted the “One China Policy,”Congress quickly imposed the “Taiwan Relations Act” on the Presidency in order to legally entrench US commitment towards the island.

By stating that the US would support “peaceful reunification” but in the process was obligated to give the island a “means to defend itself”- the policy of strategic ambiguity was born, that is the lack of clarity as to whether the US would directly intervene in the event of a contingency. The US has made periodic weapons sales to the island which has enraged Beijing, yet things otherwise remained stable for decades bar one crisis in the 1990s. But now, we live in a completely different world. The US is increasingly abrogating its commitment to the “One China Policy” and “strategic ambiguity,” increasingly giving unconditional support to Taiwan with a view to obstructing reunification altogether. Whilst the US continues to speak of maintaining the “status quo” it is quite obvious that its actions have sought to completely undermine the equilibrium between the two by backing Beijing into a corner.

Nancy Pelosi’s highly provocative visit, and the scores of hawkish US congressmen who have flowed in after, talk of the US pre-emptively placing sanctions on China over Taiwan irrespective of whether it invades or not, and the advancing of the Taiwan Policy Act which aims to give Taipei billions in military aid. China’s stern response to these provocations, which involved considerable military exercises, did not deter the US or make it think twice at all. Rather, events in Ukraine – where Washington supports Kiev against Russia – have only emboldened the US to push forward with the Taiwan issue even more, precisely because it sits on the side lines and allows other countries to be destroyed whilst selling its arms and using mass media coverage to market it. Now, for example, Taiwan wants to buy HIMARS launchers from the US in 2023.

“Nobody is talking about peace . . . and don’t you dare talk about peace. . . . We are being driven to war by mentally ill people . . . All they want is control.”

• The Worst Socioeconomic & Geopolitical Crisis in History – Celente (USAW)

“We are facing the worst socioeconomic and geopolitical crisis in modern history. The Covid war, this happened and that happened because of the pandemic. There was no pandemic. This happened because of politicians, little pieces of scum crap . . . one after another said close down your business, don’t go outside, don’t go to the beach, close down the swings and don’t let kids go and play. You have a socioeconomic crisis, the likes of which are unprecedented, and the damage caused by the Covid war is incalculable. (The CV19 Vax is part of Covid War.) Office occupancy rates are at about 45% tops. So, all the businesses that depended on commuters are gone. 30% of dry cleaners are out of business.

No more happy hours. In New York City, there are about 1,300 less people that clean office buildings now. This is real. People forget that in 2019, Germany was going into a recession. There were protests and demonstrations going on all over the world. . . . People were taking to the streets and protesting a lack of basic living standards, government corruption, crime and violence. It was one of our top trends. This is before the Covid war. They artificially propped up the governments. It was the Federal Reserve and the central banksters. They artificially pumped up the economies. There is almost $8 trillion pumped into the U.S. economy by the government to artificially prop it up. . . .

When you look at the Covid war, the draconian, demonic mandates and lockdowns that they imposed on businesses, when you look at the Ukraine war, the sanctions and the stupid things they are doing, they are creating the worst socioeconomic and geopolitical crisis in modern history.” Celente points out, “Nobody is talking about peace . . . and don’t you dare talk about peace. . . . We are being driven to war by mentally ill people . . . All they want is control.”

Let rates rise…

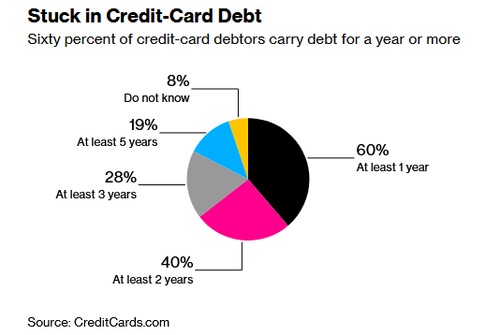

• Americans Drowning In Long-Term Credit Card Debt (ZH)

In June we reported that consumer credit – particular revolving credit – was through the roof, as tapped-out consumers relied on credit cards to make ends meet. This has only gotten worse.. Acccording to an Aug. 30 report from the Federal Reserve Bank of New York, credit card balances increased by $46 billion from last year, becoming the second-biggest source of overall debt last quarter. While both student and car loans hit all time new highs at the end of the 1st quarter. And so it comes as no surprise from Bloomberg that more US consumers are saddled with credit card debt for longer periods of time. According to a survey by CreditCards.com released on Monday, 60% of credit card debtors have been holding this type of debt for at least a year, up 50% from a year ago, while those holding debt for over two years is up 40%, from 32%, according to the online credit card marketplace.

And while total credit-card balances remain slightly lower than pre-pandemic levels, inflation and rising interest rates are taking a toll on the already-stretched finances of US households. “About a quarter of respondents said day-to-day expenses are the primary reason why they carry a balance. Almost half cite an emergency or unexpected expense, including medical bills and home or car repair. The Federal Reserve is likely to raise interest rates for the fifth time this year next week. Credit-card rates are typically directly tied to the Fed Funds rate, and their increase along with a softening economy may lead to higher delinquencies. Total consumer debt rose $23.8 billion in July to a record $4.64 trillion, according to data from the Federal Reserve.” -Bloomberg. The Fed’s figures include credit card and auto debt, as well as student loans, but does not factor in mortgage debt.

CIA.

• America’s Open Wound (Edward Snowden)

Our glittering nation of laws observes this year two birthdays: the 70th anniversary of the National Security Agency, on which my thoughts have been recorded, and the 75th anniversary of the Central Intelligence Agency. The CIA was founded in the wake of the 1947 National Security Act. The Act foresaw no need for the Courts and Congress to oversee a simple information-aggregation facility, and therefore subordinated it exclusively to the President, through the National Security Council he controls. Within a year, the young agency had already slipped the leash of its intended role of intelligence collection and analysis to establish a covert operations division.

Within a decade, the CIA was directing the coverage of American news organizations, overthrowing democratically elected governments (at times merely to benefit a favored corporation), establishing propaganda outfits to manipulate public sentiment, launching a long-running series of mind-control experiments on unwitting human subjects (purportedly contributing to the creation of the Unabomber), and—gasp—interfering with foreign elections. From there, it was a short hop to wiretapping journalists and compiling files on Americans who opposed its wars. In 1963, no less than former President Harry Truman confessed that the very agency he personally signed into law had transformed into something altogether different than he intended, writing: “For some time I have been disturbed by the way CIA has been diverted from its original assignment. It has become an operational and at times a policy-making arm of the Government. This has led to trouble…”

Many today comfort themselves by imagining that the Agency has been reformed, and that such abuses are relics of the distant past, but what few reforms our democracy has won have been watered-down or compromised. The limited “Intelligence Oversight” role that was eventually conceded to Congress in order to placate the public has never been taken seriously by either the committee’s majority—which prefers cheerleading over investigating—or by the Agency itself, which continues to conceal politically-sensitive operations from the very group most likely to defend them.

Dan Aykroyd SNL 1978

https://twitter.com/i/status/1572332575137402882

Human chain

“Courage Calls to Courage Everywhere”

#SurroundParliament on 8th Oct with the #HumanChain

#FreeAssangeNOW pic.twitter.com/3b36XWXfKw

— Siuan the Amyrlin (@SiuantheAmyrlin) September 20, 2022

Support the Automatic Earth in virustime with Paypal, Bitcoin and Patreon.