Lewis Wickes Hine Workers stringing beans in J.S. Farrand Packing Co, Baltimore 1920

“..Unfortunately, as Brazilian writer Paulo Coelho once observed, “Every time we repeat the same mistake, the price goes up.”

• A Lost Decade? We Should Be So Lucky (Das)

A growing number of economists seem convinced that the U.S., European Union and China are all headed for a prolonged period of sluggish growth — secular stagnation, in the words of former Treasury Secretary Larry Summers. A close parallel would seem to be 1990s Japan. There, too, the bursting of debt-funded asset price bubbles gave way to multiple rounds of fiscal stimulus, massive monetary easing and rock-bottom interest rates. Rescue efforts stabilized conditions but couldn’t spark a sustainable recovery, leaving the economy mired in low growth, low inflation and high debt. In some ways, this outcome might not seem so terrible. (One visiting English politician dazzled by Tokyo’s Ginza noted that if this was a recession, he wanted one too.)

When Japan entered its downturn, however, the country had several advantages both internally and externally that nations today don’t. For many, a Japan-style slump may be the best-case scenario. First and foremost, at the onset of its crisis, Japan enjoyed modest levels of government debt – around 20% of GDP – as well as strong domestic savings and an abnormally high home bias in investment. Even now, around 90% of government bonds are held by Japanese buyers. This has allowed successive Japanese governments to run large budget deficits and finance their spending domestically, assisted by an accommodative central bank that’s kept the cost of servicing debt low. By contrast, many problem economies today suffer from high levels of government debt – around 80% to 100% of GDP – as well as total debt. China’s official government debt is lower, around 55% of GDP.

But that number doesn’t take into account borrowing by large banks and other state-owned enterprises, which is backed up to varying degrees by the government. Some countries also have low domestic savings and are reliant on foreign capital, limiting their ability to finance budget deficits.

The gall: “Despite weak equity markets, the fund’s diversified portfolio and our investment team delivered a positive return..”

• NY Pension Fund Posts 0.19% Return In Fiscal Year (WGRZ)

New York’s $178 billion pension fund posted a mere 0.19% return on investments for the fiscal year that ended March 31, the lowest return since 2009, Comptroller Thomas DiNapoli announced Monday. New York’s Common Retirement Fund includes 1 million active members and retirees, and the performance of the fund impacts how much local governments have to pay into the system each year – which influences property taxes. Pension costs soared after the recession in 2009 when the fund plummeted nearly 25%. But the fund has improved in recent years, leading to back-to-back years of a decline in contribution rates for municipalities. DiNapoli said the fund’s performance was the result of a weak year on Wall Street.

“Despite weak equity markets, the fund’s diversified portfolio and our investment team delivered a positive return,” DiNapoli said in a statement. “We continue to have confidence in our asset allocation for the long term. Our investment team is focused on ensuring we remain one of the best funded and top performing plans in the country.” The fund is the third-largest public pension fund in the nation, giving it pull with investors and companies. The pension plan has often been cited as one of the best-funded plans in the nation, avoiding pension shortfalls found in other states. But DiNapoli has repeatedly lowered the fund’s expected rate of return – from 8% to 7.5% in 2010 and then again last year to 7% to limit the fund’s volatility.

In August or September, DiNapoli will announce the contribution rates for local governments for the coming year. Currently, the average contribution rate for state and local governments to fund the pension fund is 18% of payroll. For police and fire officers, the governments contribute about 25%. In the early 2000s, local governments contributed nearly zero to the fund.

Just wait till the recovery sets in. Everything will be just peachy.

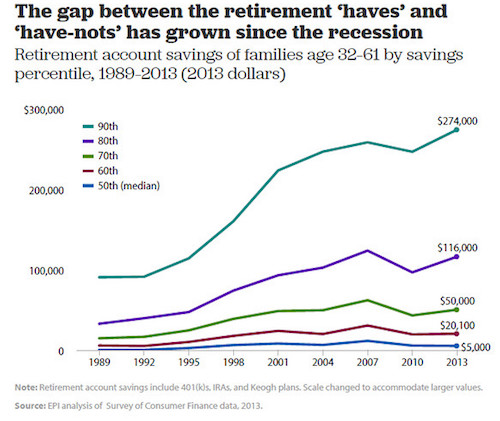

• The Typical American Couple Has Only $5,000 Saved For Retirement (MW)

When American companies began switching from traditional pensions to self-directed 401(k)-like plans in the 1980s and 1990s, it was supposed to lead to a golden age of retirement security. No longer would workers be at the mercy of the company’s generosity or of Social Security’s solvency; workers themselves would be responsible for saving enough for a comfortable retirement. Some 30 years later, the results are in: The median working-age couple has saved only $5,000 for their retirement, according to an analysis of the Federal Reserve’s 2013 Survey of Consumer Finances by economist Monique Morrissey of the Economic Policy Institute. The do-it-yourself pension system is a disaster.

Even as the traditional company-funded pension has nearly disappeared and even as Social Security benefits are being slowly eroded, most workers haven’t saved enough to offset those losses to their retirement income. Seventy percent of couples have less than $50,000 saved. Even those on the cusp of retirement — the median couple in their late 50s or early 60s — has saved only $17,000 in a retirement savings account, such as a defined-contribution 401(k), individual retirement account, Keogh or similar savings account. How long does $5,000, or even $50,000, last? Until the first big medical bill? Morrissey figures that about 43% of working-age families have no retirement savings at all. Among those who are five to 10 years away from retirement, 39% have no retirement savings of their own.

Not exactly news, is it?

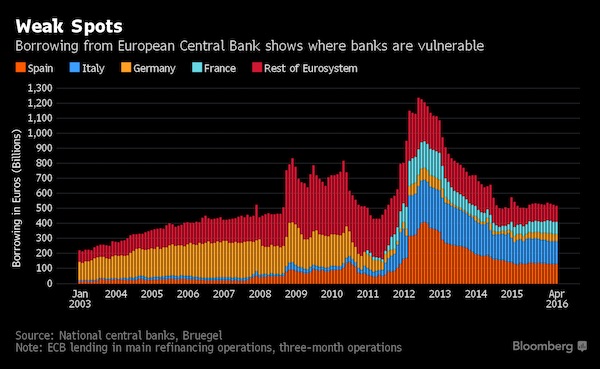

• Borrowing From ECB Shows Where Banks Are Most Vulnerable (BBG)

Spanish and Italian banks scoop up more than half of the money the European Central Bank provides in its regular refinancing operations, signaling that borrowing in financial markets remains difficult or unattractive for them eight years after the collapse of Lehman Brothers Holdings Inc. Banks’ balance sheets remain cluttered with non-performing loans and foreclosed assets just as revenue generation is damped by sluggish credit demand and low interest rates depressing margins. In addition to the weekly and three-months operations, the ECB will offer targeted longer-term loans next week that’ll mature in 2020.

To phrase it differently: how crazy are central bankers?

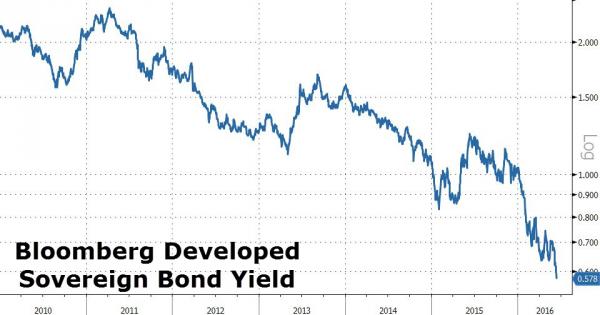

• How Low Can Bond Yields Go? Lower (ZH)

How low can bond yields go? Every day seems to provide fresh evidence that we really don’t know. But whatever your answer, between the gravitational pull of central bank debt purchases and a slowing global economy, the reality is: probably lower. Milestones include unprecedented 10-year yields in Germany, Japan and the U.K. British government debt has returned 8.1% this year and the spread between 10-year gilts and comparable Treasuries is at the widest since 2006 on concern the U.K. may vote to leave the EU. It may seem crazy that 11 sovereigns have negative-yielding five-year debt. Hard though it is to accept, bondholders aren’t playing the greater fool. Central banks are primed to push yields lower until they get results. “It’s a mad scramble for defensive positions,” said Jack McIntyre, a bond manager with Brandywine Global Investment Management. “We’re competing against the world’s central banks” for bonds”.

Trends in consumer prices haven’t acted as a brake. Inflation in advanced economies fell to 0.3% last year, the least since 2009 and down from 1.4% in 2014, according to IMF data. The U.K. vote has broader consequences. Recent polls have favored the Brexit camp, and should voters seek separation, others in the EU may try to follow. Should that happen, German 10-year yields could go more negative than -0.03%. Gilts have rallied without BOE purchases. A decision to depart may force its hand in lowering rates or resuming bond acquisitions, boosting gains in the process. McIntyre prefers Treasuries to gilts in either voting outcome. They’ll hold their value better should the U.K. remain, while Brexit may tarnish its standing as a top-tier issuer by introducing credit risk.

Bunch of manipulators.

• China Devalues Yuan To Weakest Since Jan 2011 (ZH)

Just in case The Fed had any ideas of surprising markets with a “confidence-inspiring” rate-hike tomorrow, The PBOC just sent a message loud and clear to Janet as they devalued the Yuan fix by over 2 handles, above 6.60 for the first time since January 2011. This is the 3rd major devaluation step in the last 10 months (remember when China said August was a “one off”?)

Bear in mind this kind of currency turmoil has not ended well for US equities in the past…

Which may help explain why funding market stress is starting to appear in Libor/OIS and basis-swaps (demand for USDollars), and why US and European banks are tumbling…

“..investors clearly indicated that they would like to see further improvements in the accessibility..”

• China Stocks Denied MSCI Entry In Blow To Xi’s Ambitions (BBG)

China’s domestic equities were denied entry into MSCI Inc.’s benchmark indexes for a third time, a setback for President Xi Jinping’s efforts to raise the profile of mainland markets and turn the yuan into an international currency. Policy makers need to make additional improvements to the accessibility of the A share market, according to a statement from the index compiler on Tuesday. MSCI, whose emerging-market index is tracked by investors with $1.5 trillion in assets, said it will reconsider inclusion in its 2017 review, while not ruling out an earlier announcement.

China was rejected despite a flurry of measures this year to address MSCI’s concerns, including curbs on arbitrary trading halts and looser restrictions on cross-border capital flows. The decision suggests international investors are still uncomfortable putting their money in the $6 trillion market after a botched government campaign to prop up share prices roiled global equities last year. While Chinese authorities have demonstrated a commitment to opening the market, “investors clearly indicated that they would like to see further improvements in the accessibility,” Remy Briand, MSCI’s global head of research, said in the statement.

“..it could also force discussion of whether to raise the inflation target in order to try to push the entire rate structure higher.”

• Fed Faces Battle To Escape World’s Low Interest Rate Grip (R.)

Evidence that the U.S. neutral rate of interest remains stalled near zero may slow Federal Reserve rate hikes even more than expected, tying the hands of policymakers until a rebound in global demand or other forces raise that key measure of the economy’s underlying strength. Though difficult to estimate precisely, the neutral rate is the point at which monetary policy neither encourages nor discourages spending and investment, and is thus a key measure of whether a given federal funds rate is stimulating or restricting the economy. With the Fed still trying to encourage spending, investment and hiring, a low neutral rate means the Fed has less room to move before that stimulus is gone.

Fed estimates published online show little consistent movement in the neutral rate in recent years even as the labor market tightened and growth continued above trend, confounding expectations that it would move higher in an economy expanding beyond potential. Officials cite a variety of possible explanations, but the result is the same: until policymakers are satisfied that the neutral rate is moving higher, they face an effective cap of 2% or even less on the federal funds rate. Coupled with a 2% inflation rate, the Fed’s target, that would put the “real” federal funds rate at zero. If inflation remains below target, the ceiling on the Fed would be that much lower as well.

That is a far cry from the 3.5 to 4% that the Fed’s policy rate has averaged since the 1990s, and means the central bank will treat each move with particular caution, current and former Fed officials say. It also means the central bank would be stuck near zero, and more likely to have to return to unconventional policy in a downturn; it could also force discussion of whether to raise the inflation target in order to try to push the entire rate structure higher.

“They’ve turned into the ‘Zombie Fed.'”

• Jeff Gundlach Says ‘Central Banks Are Losing Control’ (R.)

Jeffrey Gundlach, the chief executive of DoubleLine Capital, said on Tuesday investors are dropping risky assets and turning to safer securities including Treasuries and gold because they are losing faith in central banks. The man known on Wall Street as the ‘Bond King’ is one of the first heavyweight investors to publicly raise red flags about the credibility of major central banks, including the U.S. Federal Reserve, as countries struggle to manage economic growth. Last year, Gundlach correctly predicted that oil prices would plunge, junk bonds would live up to their name and China’s slowing economy would pressure emerging markets. In 2014, he forecast U.S. Treasury yields would fall, not rise as many others had expected.

“Central banks are losing control and they don’t know what to do … just like the Republican establishment and Donald Trump,” Gundlach told Reuters in a telephone interview, referring to the Republic Party’s unpredictable presumptive nominee for U.S. President. Safe-haven German Bund yields fell below zero on Tuesday for the first time and global equity markets slid for a fourth day in a row on intensifying worries about a potential British exit from the EU next week. [..] “The Fed is confused and their confusion spills into investor psychology,” said Gundlach. [..] “The Fed changes its tone so frequently, it seems every other week the message is different. They’ve turned into the ‘Zombie Fed.’ They say the meeting this week is ‘live,’ but investors all know it isn’t at all.”

[..] Gundlach also noted the dramatic “drawdowns” from the highs in several stock markets. Germany is down 22%, Japan is down 23%, China is down 45%, the United Kingdom market is down 15% and France is down 20%. “Negative rates do not prop up stock markets,” Gundlach said on the webcast.

How to kill a city.

• London House Prices Up 14% In A Year (Ind.)

House prices across the UK continued to grow in April, with London prices leaping by more than 14% over the past year, according to official figures published on Tuesday. The average house price in the UK increased 8.2% year on year to £209,054, up 16,000 from the same time in 2015. In London, which continued to be far more expensive than anywhere else in the country, the average house price is now more than £470,000, up by nearly £60,000 on April last year. [..]

The average house price for England was £225,000, an increase of 9.1% on last year compared, with £139,000 in Wales, £138,000 in Scotland and £118,000 in Northern Ireland. The increase came despite clear evidence that housing market activity has slowed markedly following April’s Stamp Duty increase for buy-to-let investors and second home buyers. The possibility of the UK leaving the European Union following the referendum on 23 June has not dampened demand, the ONS said. “Despite the short term uncertainty of next week’s EU referendum, regional property markets are receiving a pre-summer swell, giving homebuyers more choices.

You guys should have thought of that before creating your biggest ever housing bubble.

• Let’s Not Sleepwalk Into Economic And Geopolitical Catastrophe (T.)

If Europe’s political leaders awake on Friday June 24 to find that Britain has voted to leave the EU – which judging by the polls is looking ever more likely – they will know who to blame most: themselves. For many citizens, there are much greater issues of principle and interest at stake in this referendum than the economy. But for me, economic and political stability are the prime consideration, which is why, as regular readers of my columns will already have guessed, I will be voting to remain. Yet I do so with a deep sense of foreboding, for despite the benefits Britain has enjoyed in its 43 years of membership, the EU has become a dysfunctional Byzantium of paralysing political and economic complexity. It has not been possible for a long time now to be an enthusiastic European.

Much of what was good about the EU as a force for peace through trade and economic advancement has long since ceased to be true. Over the last eight years, the EU has faced two distinct but related, existential crises – the eurozone debt meltdown and the challenge of mass, cross border migration. On both counts it has failed miserably. Though very different in their characteristics, these crises essentially have the same genesis. Both result from the attempt to crunch together economies of widely different income, wealth and welfare support. Give Greece, Spain, Portugal and Italy the ability to borrow at a German interest rate, and they were always bound to be enveloped by an unsustainable credit boom.

Denied both the natural market adjustment mechanism of free floating exchange rates, and the policy flexibility to mount a nationally-determined response, these debt crises have been left festering and unresolved, with devastating consequences for growth and jobs. Similarly, if the inhabitants of a low income, developing country are given the right to live and work in a much richer one with far superior public services and social welfare, then nobody should be surprised by both the reality of mass migration and the now all too evident backlash against it. In this regard too, the single European market, with its founding “four freedoms”, has proved incapable of responding.

Tune in next week and/or tomorrow for Hell Freezes Over.

• George Osborne: Vote For Brexit And Face £30 Billion Of Taxes And Cuts (G.)

George Osborne will warn that he would have to fill the £30bn blackhole in public finances triggered by a vote to leave the European Union by hiking income tax, alcohol and petrol duties and making massive cuts to the NHS, schools and defence. In a sign of the panic gripping the remain campaign, the chancellor plans to say that the hit to the economy will be so large that he will have little choice but to tear apart Conservative manifesto promises in an emergency budget delivered within weeks of an out vote. “Far from freeing up money to spend on public services as the leave campaign would like you to believe, quitting the EU would mean less money,” Osborne will say. “Billions less. It’s a lose-lose situation for British families and we shouldn’t risk it.”

The chancellor will spell out his concerns at an event where he will be joined by his predecessor, Alistair Darling. The Labour politician will say he is more worried now than he was during the 2008 financial crisis, arguing that a Brexit vote will result in not just one emergency budget but “one after another”. The pair will publish an “illustrative budget scorecard” comprising a long list of the sort of measures they say may have to be implemented.

Or so they say.

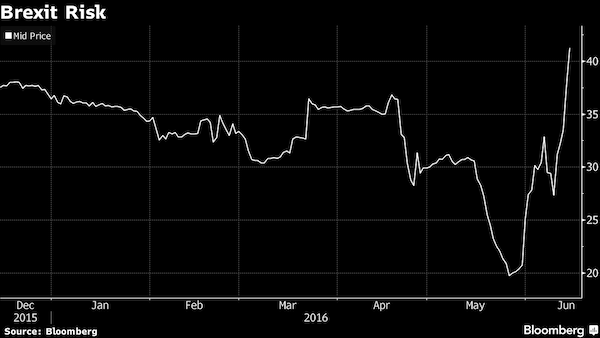

• Bookies Are Still Pretty Sure Brexit Isn’t Going to Happen (BBG)

While polls show the U.K.’s Brexit vote poised on a knife’s edge, bookies remain fairly confident the nation will stay in the European Union. Most of the biggest betting firms and exchanges in the U.K., Ireland and beyond place a 60% or better chance on David Cameron averting a so-called Brexit. That’s even after five polls published this week showed the “Leave” side ahead, with the latest survey giving it as much as a 7 percentage-point lead over “Remain.” “Pollsters ask people what they feel on a particular day; we are predicting what they will actually do on June 23,” said Jamie McKittrick, head of sports trading at Ladbrokes Plc. “Historically, we have seen a late swing to the status quo, especially among the undecideds.”

Analysts at firms like Danske Bank A/S and Investec Plc now routinely include gambling odds in client notes, with betting markets viewed as offering clues to the direction of political events. In March, for example, Paddy Power Betfair Plc, Ireland’s largest bookmaker, paid out 120,000 euros ($135,000) on Donald Trump winning the U.S. Republican presidential nomination, months before he won enough delegates to become the presumptive nominee. [..] As recently as last month, oddsmakers were placing a 20% chance on the possibility of the U.K. leaving the EU. While bookmakers like Ladbrokes this week slashed the odds on a Brexit, for now, they still make the U.K. staying in the EU the most likely outcome. That’s a pattern apparent across most betting firms and exchanges.

“The EU referendum market has exploded into life in the past week with an average of 1 million pounds traded every day, ” said Naomi Totten of Betfair, which also places a 60% probability on the U.K. opting to stay inside the EU. “Brexit has been backed heavily in the past 24 hours, although Remain is still clinging to favoritism.”

Excellent Dmitry on Dunbar’s rule of 150.

• The Law of Attraction (Dmitry Orlov)

One unintended consequence of our current mode of living is that it has warped and perverted our interpersonal interactions. In order to be able to afford to simply inhabit the planet and satisfy our basic needs, we are required to play all sorts of contrived roles. Specifically, we are forced deal with each other according to arbitrary rules that are forced upon us. As employees we are expected to readily lie to customers to protect our employers’ profits. As salespeople we are expected to sell things we know better than to ever want to buy. Then there is a whole category of people who work as enforcers, and are specifically paid to disregard all humane considerations and to dole out punishments without any allowance for dire personal circumstances.

Vast social and financial hierarchies reward psychopathic behavior (which is regarded as professionalism) while punishing altruism and compassion (which is regarded as weakness or corruption). Co-workers arbitrarily thrown together by managerial whim often spend more time with each other than with their own families, trapped in a world of stunted, superficial relationships that gradually erode their humanity. Parents often have no choice but to pay strangers to raise their children for them. These strangers work for a wage rather than out of love for the children, and when their contract ends, so does the bond between the child and caregiver, undermining the child’s faith in humanity. When parents do get to see their children, they are often tired and distracted, conditioning the children to treat them no better than they treat the strangers who take care of them the rest of the time.

Growing up with a constant deficit of sensitivity, sincerity, security and warmth, once they reach adulthood these children expect their relationships to be either manipulative and abusive, or regulated by contract. Their humanity becomes reduced to a set of selfish and materialistic drives. Their misshapen psyches are balanced on a knife’s edge between a morbid fear of exclusion, which drives them toward mimicry and conformism, and an unnatural, hypertrophied competitive drive that destroys their instinct for spontaneous cooperation. When you take a step back from it all and look at it, the impression is one of a society-wide mental disorder.

Good starting point, not great execution.

• Putting A Price On Nature Is Wrong (G.)

The paradox of environmental economics is that we feel compelled to price nature to make its loss visible on the balance sheet, but in doing so we legitimise its commodification and validate its critical overconsumption in an unbounded market system. No carbon market is yet designed to work within a precautionary limit on global emissions. That means that currently it would be possible to pay to emit the notional extra tonne of carbon that might push us over the edge into irreversible climatic upheaval. What price should that tonne of carbon carry? The more goods you pile onto a ship, the more likely it is to sink. You can price the relative risk of different levels of load, and insure it accordingly, and you can put a price on the economic cost of lost goods should the ship turn turtle.

But if your life depends on keeping the boat afloat, pricing ultimately becomes irrelevant. The point is to stay on the surface. That is why the Plimsoll safety line on the side of ships was introduced to prevent overloading (easy to spot, it looks exactly like the London Underground symbol). There are many economic and scientific problems in pricing nature and the environment, such as around offsetting, and there are philosophical ones too. In deciding whether or not to build a new road through a community woodland, how is the value of the woodland arrived at in any cost benefit analysis done by planners? Asking how much the community is prepared to pay to keep it would be constrained by ability to pay, but ask what amount would be needed to compensate for its intrinsic worth might, in theory, yield an infinite price.

Fiona Reynolds, former chief of the National Trust, is the latest to argue that we need whole other ways to assess the value of the natural world. When the economist Dieter Helm, chair of the Natural Capital Committee, wrote that: “the environment is part of the economy and needs to be properly integrated into it so that growth opportunities will not be missed,” he both gave the game away about pricing as a hostage to fortune, and made a category error. It is the economy that needs to be properly integrated into the environment so that its limits to growth can be understood.

“These stolen avocados can carry risks,” he said.

• Avocado Shortage Fuels Crime Wave In New Zealand (G.)

Surging local and international demand for avocados is fuelling a crime wave in New Zealand. Since January there have been close to 40 large-scale thefts from avocado orchards in the north island of New Zealand, with as many as 350 fruit stolen at a time. Avocados are selling for between NZ$4-6 each (£2-3) across the country, after a poor season last year and increasing local demand. According to New Zealand Avocado in 2015 an additional 96,000 New Zealand households began purchasing avocados, and local growers – largely geared towards the lucrative export market – have been unable to keep up with the surge in demand.

The recent thefts have taken place in the middle of the night, with the crop either “raked” from the tree and collected in blankets or sheets on the ground, or hand-picked and driven away to pop-up road-side stallsgrocery stores or small-scale sushi, fruit and sandwich shops in Auckland. Sergeant Aaron Fraser of Waihi said there had been “spates” of avocado thefts during his time in the police but nothing as sustained as the current activity. “These stolen avocados can carry risks,” he said. “They are unripe, some have been sprayed recently and they may still carry toxins on the skin. But with the prices so high at the moment, the potential for profit is a strong inducement for certain individuals.”

Home › Forums › Debt Rattle June 15 2016