NPC Ford Motor Co., McReynolds & Sons garage, L Street, Washington DC 1926

The US will keep doing what it can to prop up this bubble.

• US Existing Home Sales Tumble 7.1% In Warning For Housing Market (Reuters)

U.S. home resales fell sharply in February in a potentially troubling sign for America’s economy which has otherwise looked resilient to the global economic slowdown. The National Association of Realtors said on Monday existing home sales dropped 7.1% to an annual rate of 5.08 million units, the lowest level since November. Sales have been volatile and prone to big swings up and down in recent months following the introduction in October of new mortgage regulations, which are intended to help homebuyers understand their loan options and shop around for loans best suited to their financial circumstances. February’s decline weighed on investor sentiment, with the S&P 500 stock index falling after the data was released. Sales fell across the country, including a 17.1% plunge in the U.S. Northeast.

Economists had forecast home resales decreasing 2.8% to a pace of 5.32 million units last month. Sales were up 2.2% from a year ago. The median price for a previously owned home increased 4.4% from a year ago to $210,800. The housing report runs counter to data showing strong job growth and a stabilization of factory output, which had taken a hit from weaker demand overseas and a strong U.S. dollar. Housing continues to be supported by a tightening labor market, which is starting to push up wage growth, boosting household formation. But a relative dearth of properties available for sale remains a challenge. “Finding the right property at an affordable price is burdening many potential buyers,” said NAR economist Lawrence Yun.

Beware when accountants become society’s most creative people.

• Companies Haven’t Fudged Their Numbers This Much Since 2009 (Yahoo)

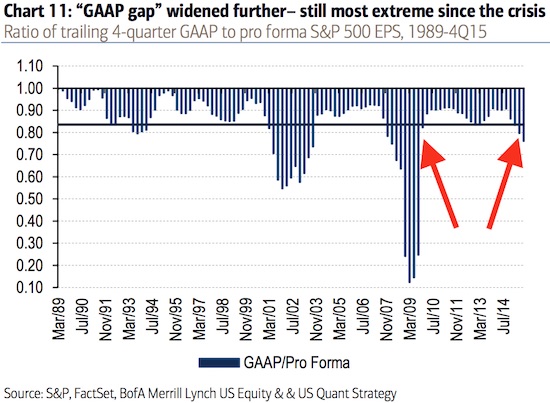

Almost all of the companies in the S&P 500 have announced their quarterly earnings, and now Wall Street’s number crunchers are finalizing their conclusions as to what actually happened during the last three months of 2015. Unfortunately, it’s become an increasingly challenging task to understand the true financial performance of the big publicly traded companies because of the widening of something called the “GAAP gap.” Don’t worry: this topic isn’t as scary a concept as it sounds. In a nutshell, there’s a standard known as generally accepted accounting principles, or GAAP, which encourages some uniformity in how companies will report financial results. Unfortunately, the strict standards of GAAP often force companies to report big one-time, non-recurring items that will distort quarterly earnings, in turn making them a poor reflection of underlying operations.

And so, many companies will make adjustments for these items and separately report adjusted or non-GAAP financial results. All of that’s well and good. But there’s an unsettling trend we’ve been witnessing: the gap between GAAP and non-GAAP numbers is widening. Specifically, this “GAAP gap” is widening in such a way that more and more costs and expenses are being removed to make underlying profits look higher. “The gap between GAAP (reported) and pro forma (adjusted) EPS continued to widen in 4Q, with the GAAP/Pro forma ratio of 0.74 still at its most extreme levels since 2009,” Bank of America Merrill Lynch’s Savita Subramanian said on Monday. “Trailing four-quarter (2015) GAAP EPS came in at $87 vs. $118 for pro forma EPS.”

It’s jarring to hear that any metric has returned to levels last seen during the financial crisis. Unfortunately, it’s hard to conclude what the implications are here because the issues are tied to just a few industries that are facing their own unique issues. “As was the case last quarter, the chief contributor to “GAAP gap” has been Energy asset impairments/write-downs, followed by M&A costs within Health Care,” Subramanian continued. “The Energy sector alone contributed to nearly half of the “GAAP gap” this quarter.” While this is certainly a top worth keeping an eye on, it would probably be a mistake to jump to any sweeping conclusions about the market and the economy. “We found that while a widening GAAP gap is not a leading indicator of a market downturn, companies with increasing deviations tend to systematically underperform the market,” Subramanian said.

One day we’ll understand just how crazy this is.

• Beware of Draghi Dropping Hints (FT)

It is a risky game, taking central bankers at their word. Investors should be wary of what central bankers appear to be saying or signalling. Like some politicians, economists and even journalists, they often change their mind. Mario Draghi, the president of the ECB, is a case in point. Don’t be fooled by Mr Draghi when he signals that interest rates have been cut as low as they can go, as he did at the ECB’s March policy meeting. After reducing the deposit rate to minus 0.4%, he could not have been clearer when he said: “We don’t anticipate that it will be necessary to reduce rates further.” Although he kept the option of further cuts open, he outlined his unease about negative rates and their impact on the region’s commercial banks. Consequently, some investors and commentators think interest rates have hit their floor in the euro zone.

But Mr Draghi has made similar assertions after cutting rates before. In June 2014, he reduced rates to minus 0.1% and said: “For all practical purposes we have reached the lower bound.” In September 2014, he dropped rates to minus 0.2% and said: “We are at the lower bound where technical adjustments are not going to be possible any longer.” There is an obvious pattern. Mr Draghi signals the floor has been reached, only to change his mind later. The likely reason for his “no lower” signals is that he does not want to scare markets. Bank stocks, bonds and credit default swaps, which are a kind of insurance against default, have all been rocked by worries about negative rates and their impact on the banking business. There are also concerns for banks in euro zone countries such as Austria, Portugal and Spain, where mortgage rates could go negative in the event of the ECB cutting further, as these mortgages are linked to euro zone money market rates.

In other words, banks in Austria, Portugal and Spain may end up paying customers for lending to them, which would be bad news for their balance sheets. The Bank for International Settlements warned in a report this month that there was great uncertainty over the potential for deeper cuts into negative territory. However, “Life Below Zero”, a research paper by HSBC, the bank, suggests that the ECB could cut rates much further. It says that the Swiss National Bank currently operates the most negative rate of all the world’s leading central banks (minus 0.75%). If the costs incurred by Swiss banks were applied to the euro zone banking system, then the ECB’s deposit rate would be much more negative, at minus 1.8%. The ECB could also tier rates. At the moment, the ECB charges about 90% of its bank reserves at negative rates.

“It’s capitalism with Chinese characteristics.”

• Central Banks Creep Toward Uncomfortable Role as Central Planners (WSJ)

Are central banks heading back to an era of rationing money? The question may sound daft when policy makers are pumping gushers of cash into several of the world’s major economies. But as the central banks become more desperate to boost inflation and growth, they are starting to break one of the modern tenets of the profession by funneling that cash directly to what they regard as “good” uses. The past two weeks brought interventions by the Bank of Japan and ECB, which would have been unthinkable just a few years ago. The Bank of Japan’s conditions for companies to qualify for exchange-traded funds it would like to buy sound like they come from a well-meaning government minister, not a monetary authority concerned about overall growth and inflation.

Companies could qualify by offering an “improving working environment, providing child-care support, or expanding employee-training programs.” The central bank wants financiers to create a new breed of ETFs it would like to buy. The ETFs would hold only shares of companies that are increasing capital spending, expanding spending on research and development or boosting what the Bank of Japan calls “human capital.” The latter means pay raises for staff, taking on more people or improving human resources. All these are eminently reasonable things to demand of companies, especially Japanese firms. All would probably be good for the economy, too. However, they have nothing to do with monetary policy. The basic aim of central banks is to adjust the overall economy while leaving the market and government to decide the best use of capital, decisions that are inherently political.

The problem, as Neal Soss, vice chairman of research at Credit Suisse, puts it, is “these are very, very challenging times for the economic orthodoxy,” and if governments won’t step up with an expansionary fiscal policy, central banks have little choice but to fill the gap. To be fair, Bank of Japan Gov. Haruhiko Kuroda is hardly drawing up a Soviet-style five-year plan. Only ¥300 billion ($2.7 billion) a year will be spent “with the aim of supporting firms that are proactively investing in physical and human capital.” The worry is that the Bank of Japan has only just begun. “It’s a massive politicization of credit: Here are the legitimate things for lending, and here are the illegitimate things,” said Russell Napier, an independent strategist and author of “Anatomy of the Bear,” a study of 70,000 Wall Street Journal articles during major bear markets. “It’s capitalism with Chinese characteristics.”

It’s awfully similar indeed. So why do we allow it to happen?

• The ECB and The Mississippi Company Bubble (Macleod)

Last week, the ECB extended its monetary madness, pushing deposit rates further into negative figures. It is extending quantitative easing from sovereign debt into non-financial investment grade bonds, while increasing the pace of acquisition to €80bn per month. The ECB also promised to pay the banks to take credit from it in “targeted longer-term refinancing operations”. Any Frenchman with a knowledge of his country’s history should hear alarm bells ringing. The ECB is running the Eurozone’s money and assets in a similar fashion to that of John Law’s Banque Generale Privée (renamed Banque Royale in 1719), which ran those of France in 1716-20. The scheme at its heart was simple: use the money-issuing monopoly granted to the bank by the state to drive up the value of the Mississippi Company’s shares using paper money created for the purpose.

The Duc d’Orleans, regent of France for the young Louis XV, agreed to the scheme because it would provide the Bourbons with much-needed funds. This is pretty much what the ECB is doing today, except on a far larger Eurozone-wide basis. The need for government funds is of primary importance today, as it was then. In Law’s day, France did not have a central bank, such as the Bank of England, managing the issue of government debt, let alone a functioning government bond market. The profligate spending of Louis XIV had left the state three billion livres in debt, which was the equivalent of 1,840 tonnes of gold. This was about 85% of the world’s estimated gold stock at that time, at the livre’s conversion rate into Louis d’Or. John Law would almost double that by June 1720, with unbacked livre notes issued by his bank.

Today, the assets being overvalued for the governments’ benefit are government bonds themselves, but the principal is the same. There is no need to use a separate, Mississippi-style vehicle, because there is a fully functioning government bond market. Banque Generale created the bank credit for France’s upper and middle classes to buy Mississippi Company shares, driving up the price and making yet higher prices a certainty. Law had set up a money-making machine for those with a modicum of wealth, but the ten% down-payment required to subscribe for Mississippi shares made speculation available to the servant classes as well. The result was virtually everyone in Paris was caught up in the speculative fever, and Mississippi shares increased from the 15 livres deposit to 18,000 livres fully paid at the peak in June 1720. The term “millionaire” dated from that time.

Simplistic. if Germany goes, so must Holland. And Austria. And then Belgium. France.

• Germany Must Leave Eurozone To Save It: Mervyn King (CNBC)

Germany has grown too powerful and should leave the euro zone in order to save the union, former Bank of England Governor Mervyn King said Monday. “That would be the best way forward, and I would hope that many of my American friends would stop pushing the Europeans to throw money at the problem and say we must make the euro successful,” he told CNBC’s “Squawk Box.” The tragedy of the euro zone, said King, is that Germany entered the project in a bid to bind itself into Europe so that no European country would ever again fear the country’s power. But now Germany is more powerful economically and politically than it was when the euro was adopted, he said. Germany also sacrificed the Deutsche mark in the process, “the one really successful symbol of post-war German reconstruction,” he said.

While the United States, the U.K., and some European countries need to export and invest more while consuming less, Germany and China need to spend more and export less, King said. “Unless we’re prepared to tackle that problem head-on, which will involve some restructuring of the economy, then we shall just continue down this path of ever-lower rates and no growth,” he said. Last week, European Central Bank President Mario Draghi warned European leaders that monetary policy alone would not be enough to jump-start the economy and that governments needed to do their job by pushing through structural reforms. “I made clear that even though monetary policy has been really the only policy driving the recovery in the last few years, it cannot address some basic structural weaknesses of the euro zone economy,” Draghi told reporters.

It’s just a matter of what comes first: run out of credit or run out of growth. Since ever more credit is needed to produce one ‘unit’ of growth, diminishing returns rule the day.

• Government Debt Could Bring China’s Credit Party To A Halt (MW)

China’s economy may have run out of growth before it ran out of credit, but no one told its companies. One of the biggest China puzzles today is the seemingly never-ending ability of its corporates to access new supplies of credit, without running into trouble or someone saying no. Some analysts warn that we are looking in the wrong place for distress; it could be building in the government bond market. This year, China’s easy money policy has been most graphically on display through an unprecedented overseas buying spree by its companies. The latest Chinese company throwing its checkbook around is insurer Anbang with a $13.1 billion cash offer for Starwood Hotels and Resorts. Earlier ChemChina broke China’s record for outbound merger and acquisition activity with an offer to buy Syngenta in cash for $44.1 billion.

In fact, in the first three months of this year, China outbound M&A activity has rocketed to $102.7 billion, almost equal to the record total of $107.5 billion for the whole of 2015, according to data from Dealogic. Heavily geared balance sheets appear no hindrance to connected mainland companies being able to access funding. On Monday, Shanghai shares rallied after more, cheaper money was promised to China’s brokers for margin financing. Yet it was possible to detect a hint of caution from the central bank governor at the weekend after the chorus of upbeat commentaries on the economy from China’s leaders in recent weeks. Zhou Xiaochuan said that “lending as a share of [gross domestic product], especially corporate lending as a share of GDP, is too high” and also that a high leverage ratio is more prone to macroeconomic risk.

Corporate gearing in China is now widely estimated at some 160% of GDP. It is these kinds of concerns that have led Moody’s to downgrade the outlook on China’s sovereign rating at the beginning of March. Other analysts are also turning their attention to central government debt — which has long been viewed as manageable — as these funding needs could emerge as a new fault line of distress. Societe Generale said in a new report the government bond market faces an unprecedented supply glut due to combined local and central government bond issuance. As the market has yet to factor in this exponential growth in government paper, it could lead to disruption, which could potentially spill over into the corporate bond market, they warn.

The upswing in issuance is due to an expanded local government debt swap program (where bad loans from special funding vehicles were swapped for debt) and central and local government fiscal deficits. In total, SG calculates this year could see a total net issuance of 7.58 trillion yuan, up by 2.66 trillion yuan from 2015. And this paper will keep coming. The latest audit report put the amount of local government debt eligible for being swapped into bonds at a massive 15.4 trillion yuan.

Until it no longer can.

• China’s Debt Burden Is Only Going To Get Bigger (BV)

China’s debt burden is only going to get bigger. Total borrowing has grown rapidly to reach about 250% of GDP last year, raising concerns about runaway credit. But pressure to meet unrealistic economic growth targets will delay any sustained effort to bring debt back down. The government’s latest five-year plan highlights the dilemma. Prime Minister Li Keqiang pledged that the world’s second-largest economy will expand by at least 6.5% a year, in real terms, until 2020. Meanwhile, planners expect total “social financing” – a broad measure of private sector credit – to grow by 13% in 2016 alone. So even if inflation reaches the optimistic target of 3%, debt will outstrip nominal GDP.

Extend those trends, and borrowing will hit about 290% of annual output by 2020. Central bank Governor Zhou Xiaochuan has expressed concerns about rising corporate debt levels but there’s little sign that China is reining in credit. Banks extended new loans worth 3.5 trillion yuan ($540 billion) in the first two months of 2016, a third more than in the same period of last year. Meanwhile, Chinese companies are using domestic debt to help finance an overseas M&A binge which totals nearly $100 billion this year, according to ThomsonOne. Though a healthier stock market would allow corporations to deleverage by issuing more equity, the collapse of last year’s bubble has made investors understandably skittish.

The government could perhaps take on a greater burden: official borrowing was about 44% of GDP last year, according to Breakingviews calculations based on data from the Bank for International Settlements. That’s well below the level in developed countries. However, this excludes borrowing by state-owned entities and local governments. Moody’s puts these contingent liabilities at between 50 and 70% of GDP. That leaves consumers, whose borrowings are just 39% of GDP. So households have plenty of scope to load up on mortgages and credit cards. A consumer credit boom might help deliver growth targets while also shifting the economy towards greater consumption. Whoever does the borrowing, however, debt levels will keep rising. As in the rest of the world, deleveraging will have to wait.

More or less correct.

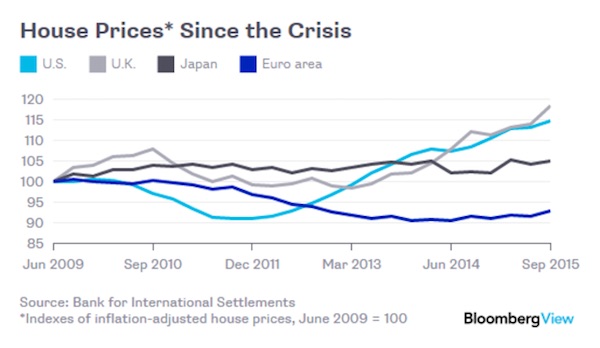

• Home Is Where the Inflation Is (BBG)

The U.S. Federal Reserve has had a tough time getting inflation back up to desired levels. There’s one area, though, where it may be having a bigger effect than some of its major foreign counterparts: house prices. Comparing house prices across borders can be a fraught enterprise, given the idiosyncratic nature of housing markets and statistics. That said, after the U.S. housing bust tanked the global economy, the Bank for International Settlements started collecting and publishing data for a large number of countries. Though still imperfect, the data allow for some rough comparisons. The latest numbers, updated Friday, show the U.S. on a run: Over the year through September 2015, house prices exceeded consumer-price inflation by 5.9% – more than in the euro area, Japan or the U.K.

That put them up almost 15% in inflation-adjusted terms since the economy hit bottom in mid-2016, just short of the U.K. Although many factors can affect house prices, much of the difference is probably attributable to central-bank policy – pushing up house prices, after all, is one of the goals of monetary stimulus. The Fed and the Bank of England moved quickly and decisively to push down short-term and long-term interest rates in 2009 and beyond, while the ECB was relatively slow to respond to economic malaise and the Bank of Japan had already used much of its ammunition (though Japan’s demographics play a role, too).

The question, then, is whether higher house prices will do any good. In the short term, they increase inequality, because the benefit accrues to relatively wealthy property owners and raises the bar for poorer folks who want to own. The expectation is that this wealth effect will translate into greater spending and investment that will benefit everyone. There are some signs that may be happening – the U.S. economy is certainly doing better than the euro area’s. Still, real median household income – though rising – only slightly exceeds its pre-recession level. Price gains are undoubtedly a relief for millions of U.S. homeowners who came out of the crisis owing more on their mortgages than their houses were worth. Now the rest of the economy just has to catch up.

I’m sure Steve will come back to the BIS source data, this time for other countries.

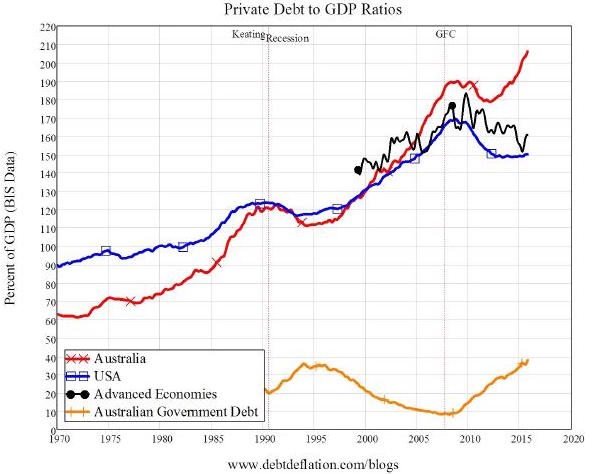

• Get Ready For An Australian Recession By 2017 (Steve Keen)

For the last 25 years, Australian politicians of both Liberal and Labor hue have been able to brag that, under their stewardship, Australia has avoided a recession. Those bragging rights are about to come to an end. During the life of the next Parliament -and probably by 2017- Australia will fall into a prolonged recession. Whichever party is in opposition at the time will blame the incumbent, but in reality this recession has been set up by the sidestep both parties have used to avoid downturns for the past quarter century: whenever a crisis has loomed, they’ve avoided recession by encouraging the private sector to borrow and spend.

The end product of that is starkly evident in a new database on private and government debt published by the Bank of International Settlements. Australia’s most famous recession sidestep was during the GFC, when it was one of only two countries in the OECD to avoid experiencing two consecutive quarters of negative GDP growth (the other country was South Korea). Since then, the private sectors of the advanced countries have collectively de-levered, reducing their debt levels from about 170 to 160% of GDP. Australia, in stark contrast, has levered up. Our private debt to GDP ratio is now more than 20% higher than when the GFC began, and more than 50% higher than in the USA (see Figure 1).

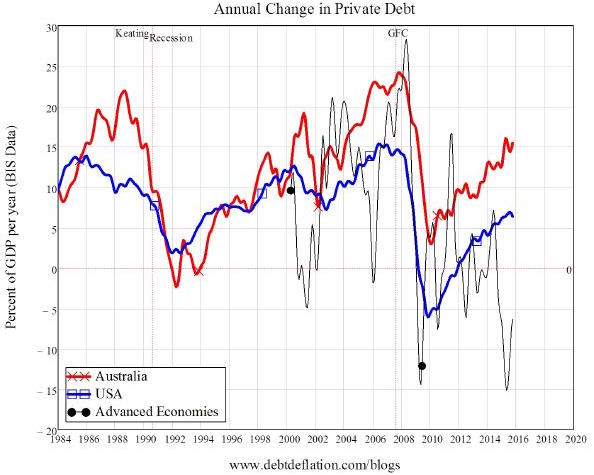

This credit sidestep has worked because the extra debt-financed expenditure lifted aggregate demand and income well above what it would have been in the absence of a debt binge (see Figure 2).

Unfortunately for Australia’s next Prime Minister, there are two catches to this trick. The obvious catch is that getting that much extra demand out of credit necessarily increases debt much faster than it increases income — hence the runaway ratio of debt to GDP shown in Figure 1 —and this can’t go on forever. The less obvious one is that when debt is at stratospheric levels that apply in Australia today, total demand falls even if the debt ratio merely stabilises. The logic is pretty simple: your spending in a year is the total of what you earn plus what you borrow, and the same maths applies to the economy as a whole. If nominal GDP grows this year at the 2.8% rate it has averaged for the last five years, then GDP in 2016 will be roughly $1,634 billion. If private debt continues to grow at its average rate of 6.9% per year, it will reach $3,414 billion —an increase of $220 billion over the year.

Total private sector demand (which is spent on both goods and services and asset purchases) will be $1,855 billion. What about 2017, if private debt grows at the same rate as GDP itself, so that the debt ratio stabilises? Then GDP will be $1,680bn, and private debt will rise from $3,414bn to $3,509bn — an increase of just $96bn over the year (compared to $220bn the year before). The sum of the two will be $1,775bn — 4.3% less than the year before. This is the inevitable debt crunch coming Australia’s way, but conventional economists are oblivious to this danger because they’ve brainwashed themselves to ignore private debt as just a “pure redistribution”, to quote Ben Bernanke. This deluded textbook thinking is why Bernanke didn’t see the GFC coming.

But American banks’ exposure is much higher.

• Regulator Warns Canadian Banks on Oil and Gas Reserves (WSJ)

Canada’s banking regulator is urging the country’s major banks to review their accounting practices to ensure they have sufficient reserves as the commodity-price collapse takes a toll on the economy. The Office of the Superintendent of Financial Institutions wants lenders to scrutinize their collective allowances, reserve funds that act as cushions to absorb potential future loan losses, the regulator’s chief said in an interview. “We want them to take a good look at their accounting practices,” said Superintendent of Financial Institutions Jeremy Rudin. “They should support loss-absorbing capacity and the ability to manage through difficult times in general,” he added.

The regulator is giving the country’s six biggest banks this guidance on their accounting as they face mounting criticism from some analysts that they haven’t amassed enough reserves to cover soured loans to the energy sector. That criticism was a recurring theme during calls following their fiscal first-quarter results, in which many banks warned of rising provisions for credit losses but assured investors their rainy-day cushions were adequate. Canadian bank shares have tumbled over the past year as the price of oil has collapsed, but the S&P/TSX Composite Bank Index is now up about 16.77% from its low in February, reflecting a rebound in oil. Still, oil prices remain an overhang for banks, underscoring the size of the energy industry in the Canadian economy and concerns that lenders will eventually be stung by higher loan losses.

Energy loans totaled 49.7 billion Canadian dollars ($38.2 billion) for the country’s six biggest banks during the November-to-January quarter, according to a report by TD Securities. Bank of Nova Scotia, Canada’s third-largest bank by assets, has the biggest direct oil and gas exposure at 3.6% of total loans. Some analysts are skeptical about the lenders’ reserving practices in part because U.S. banks, including J.P. Morgan and Wells Fargo, have set aside millions more for their reserves as they brace for bigger energy-related losses.

Brazil is a game of dominoes.

• Petrobras Posts Record $10 Billion Loss (Reuters)

Brazil’s state-controlled oil company Petrobras posted its biggest-ever quarterly loss on Monday after booking a large writedown for oil fields and other assets as oil prices slumped and refinery projects faltered. Petróleo Brasileiro as the company at the epicenter of Brazil’s massive corruption scandal is commonly known, had a consolidated net loss of 36.9 billion reais ($10.2 billion) in the fourth quarter, according to a securities filing. The bigger-than-expected shortfall was 48% larger than the 26.6 billion-real loss a year earlier, the previous record. It also turned the company’s full-year 2015 result, which was positive through September, into a full-year loss. For a second year in a row, CEO Almir Bendine said, Petrobras will not pay dividends to either its government or non-government investors and it plans to make no bonus payments to employees.

The result caught analysts and investors by surprise. The largest fourth-quarter loss expected in a Reuters survey of analysts was 9.7 billion reais. Petrobras common shares fell 5.5% in after-hours electronic trading in New York, after the results were released. The red ink at Petrobras was driven by a 46% decline in the price of benchmark Brent crude oil, a drop that has driven up losses and caused writedowns throughout the global oil industry. Of the 46.4 billion reais written off in the quarter, 83% was for oil fields. A year earlier, writedowns were also the cause of Petrobras losses, although they were largely related to the giant price-fixing, bribery and political kickback scandal that has roiled the company and help fuel calls for the impeachment of Brazilian President Dilma Rousseff.

Who needs enemies with friends like…

• Erdogan To Include Journalists, Politicians in ‘Terrorist’ Definition (Ind.)

Turkey’s President Tayyip Erdogan has claimed the definition of a terrorist should be changed to include their “supporters” – such as MPs, civil activists and journalists. It comes after three academics were arrested on charges of terrorist propaganda after publicly reading out a declaration that reiterated a call to end security operations in the south-east of Turkey, a predominantly Kurdish area. Mr Erdogan has said the academics will pay a price for their “treachery”. A British national was also detained on Tuesday despite having ordered the arrests, after he was found with pamphlets printed by the Kurdish linked People’s Democratic Party (HDP). “It is not only the person who pulls the trigger, but those who made that possible who should also be defined as terrorists, regardless of their title,” President Erdogan said on Monday, adding that this could be a journalist, an MP or a civil activist.

His comments came the day after a suicide bomb attack in the country’s capital of Ankara killed at least 34 people and wounded 125 others when a car bomb was detonated near a main square in the Kizilay neighbourhood. Violent action between the government and the PKK – which is being blamed by authorities for the Ankara bombing – has reached its worst level for 20 years since fighting restarted last July. Hundreds of civilians, militants and security forces have been killed since the summer. President Erdogan has already threatened the future of Turkey’s highest court after it ruled that holding two journalists in pre-trial detention was a violation of their rights to freedom of expression. The journalists, Cumhuriyet newspaper editor Can Dundar and Ankara bureau chief Erdem Gul, were arrested on charges of revealing state secrets and attempting to overthrow the government. They reportedly face calls for multiple life sentences from prosecutors and will stand trial later in March.

“It would be an awesome and wondrous event if the nation landed on November 8 with both parties in complete disarray..”

• The Uses of Disorder (Jim Kunstler)

Many thoughtful and patriotic citizens entering the Kubler-Ross free-fire zone of desperate bargaining with reality are at work attempting to chart an orderly course around the Godzilla-like figure of Trump looming outside the desecrated once-shining city of American democracy. I doubt there is such an orderly way through this political bad weather. When storms hit, things break up. It can be argued endlessly whether times produce the man or vice versa, but except in the most schematic and wishful sense, is there any question that Donald Trump is unfit for the office he’s seeking? Personally, I am tortured by the question: why him? Why this vulgarian who can’t string together two sequentially coherent thoughts? Are there in this land of 320 million-plus people no other men or women with comfortable fortunes and better minds bold enough to take on the matrix of mafias running our affairs into the ground? Apparently not.

Then there is the question — only nascently theoretical at this point — of where such an orderly course of decision and action might lead this country. For Trump, it seems to be a restoration of the 1950s, when armies of “breadwinner” factory workers churned out cornucopias of Maytag washers and Zenith black-and-white televisions, and the less numerous Wogs of the outside world busied themselves with basket-weaving, and Atoms For Peace would make electric power “too cheap to meter,” and popular entertainment came in the chaste form of Dinah Shore urging the upward-aspiring masses to “see the USA in your Chevrolet!” That was, of course, the time of Trump’s childhood (and my own), and if there is anything more certain than night following day, it is that America is not going back to that sunny moment.

Trump and I are way past done growing up as human organisms and America is done growing as a techno-industrial political economy. People decline and die and are replaced by new people, and political economies wither and morph into sets of new activities and relations. The forces of history want to take us to this new disposition of things, and just about everything on the American scene these days is a manifestation of resistance to that journey. The destination is a much re-scaled and down-scaled edition of daily life in a de-globalized economy, with far fewer luxuries and a greater demand for earnestness, purposeful work, generosity-of-spirit, and plain dealing. These are not qualities exhibited by Trump, who represents only the poorly-articulated and grandiose wish to “make America great again.”

The institutional collapse of the Republican Party is in full swing now thanks to Trump. By the way, it could easily be matched by an equally brutal collapse of the Democratic Party if the head of the FBI makes any criminal referrals in the matter of the Clinton Foundation’s entanglements in official State Department business via an email slime trail. It would be an awesome and wondrous event if the nation landed on November 8 with both parties in complete disarray and more than a couple of rump factions posting candidates with dubious legitimate credentials to stand for election. In over two hundred years we have not seen a national election postponed, or canceled.

Not since the dinosaurs died off. [..] “at the start of the PETM, no more than 1bn tonnes of carbon was being released into the atmosphere each year. In stark contrast, 10bn tonnes of carbon are released into the atmosphere every year by fossil fuel-burning and other human activity.”

• Carbon Emission Release Rate ‘Unprecedented’ In Past 66 Million Years (G.)

Humanity is pumping climate-warming carbon dioxide into the atmosphere 10 times faster than at any point in the past 66m years, according to new research. The revelation shows the world has entered “uncharted territory” and that the consequences for life on land and in the oceans may be more severe than at any time since the extinction of the dinosaurs. Scientists have already warned that unchecked global warming will inflict “severe, widespread, and irreversible impacts” on people and the natural world. But the new research shows how unprecedented the current rate of carbon emissions is, meaning geological records are unable to help predict the impacts of current climate change. Scientists have recently expressed alarm at the heat records shattered in the first months of 2016.

“Our carbon release rate is unprecedented over such a long time period in Earth’s history, [that] it means that we have effectively entered a ‘no-analogue’ state,” said Prof Richard Zeebe, at the University of Hawaii, who led the new work. “The present and future rate of climate change and ocean acidification is too fast for many species to adapt, which is likely to result in widespread future extinctions.” Many researchers think the human impacts on the planet has already pushed it into a new geological era, dubbed the Anthropocene. Wildlife is already being lost at rates similar to past mass extinctions, driven in part by the destruction of habitats. “The new results indicate that the current rate of carbon emissions is unprecedented … the most extreme global warming event of the past 66m years, by at least an order of magnitude,” said Peter Stassen, a geologist at the University of Leuven in Belgium, and who was not involved in the work.

The new research, published in the journal Nature Geoscience, examined an event 56m years ago believed to be the biggest release of carbon into the atmosphere since the dinosaur extinction 66m years ago. The so-called Palaeocene–Eocene Thermal Maximum (PETM) saw temperatures rise by 5C over a few thousand years. But until now, it had been impossible to determine how rapidly the carbon had been released at the start of the event because dating using radiometry and geological strata lacks sufficient resolution. Zeebe and colleagues developed a new method to determine the rate of temperature and carbon changes, using the stable isotopes of oxygen and carbon. It revealed that at the start of the PETM, no more than 1bn tonnes of carbon was being released into the atmosphere each year. In stark contrast, 10bn tonnes of carbon are released into the atmosphere every year by fossil fuel-burning and other human activity.

“Franck Düvell is an associate professor and senior researcher at The University of Oxford’s Centre on Migration, Policy and Society.”

• The EU’s Deal With Turkey Is a No-Win Situation (Fortune)

As of this year, 2.7 to 3.5 million Syrians, Iraqis, Afghans, and others have escaped to Turkey from the various evils and conflicts in the region, while 1 million moved on to the European Union. Policy failed to prevent this, and the EU is now entrenched in a moral panic over what is equivalent to a mere 0.2% of the population. Its recent deal with Turkey to send back irregular migrants in exchange for visa-free travel and billions in aid is not only a human rights violation, but could turn out to be a total PR stunt. The primary root of the refugee crisis stems back to the conflicts in Syria, Iraq, and Afghanistan. But a secondary root lies in the lack of access to protection in the countries outside of the EU. Notably in Turkey, non-Syrians have to wait eight years for asylum interviews, Syrians only get temporary protection, and access to regular employment and social services is restricted for both groups.

They endure severe poverty and years in limbo. Meanwhile, the continuation of the flow is partly driven by women and children following their husbands who made the journey last year. Until the summer of 2015, the EU failed to agree on preventive policies, and Turkey bemoaned that it was left alone with the refugee crisis while failing to stop the outflow. Meanwhile, the EU kept relatively quiet, embracing an almost laissez faire attitude. But then numbers exploded and borders were practically overrun, eventually collapsing under the sheer weight of the number of people. In some incidences, refugees protested, occasionally hurling stones, replicating the actions during the Arab Spring and once more demonstrating for human dignity. Their suffering added a Ghandi-esc dimension to their claims. Human agency supported by a myriad of facilitators proved stronger than state policy.

The EU-Turkey “deal” refers to stopping and returning “irregular migrants” and “migrants not in need of international protection” in exchange for refugees to be resettled from Turkey. But 85% of all arrivals are from countries with many refugees, so the numbers affected would be comparably small. But then it also lists Syrians, hence refugees, to be returned. So far, Turkey has already struggled to stop the outflow within the limits of the law, and now turns to violent and illegal measures. The deal is thus inconsistent—and in case refugees are returned—highly legally questionable. The deal is also practically questionable. Which border gates will be used? Are there ferries, planes, and busses available to ship tens of thousands of people back to Turkey? Where will the returned be kept? How will their human dignity be secured?

How will the people who are resettled in exchange from Turkey to Europe be selected? Does Turkey have the political will and capacity to prevent human rights violations like destitution, or to change its legislation and extent refugee status to non-Europeans? In order to make the deal work, Turkey would (a) need to grant a refugee status that complies with EU and international law, and (b) rapidly develop and, more importantly, implement an integration strategy that could justify containing and simultaneously convincing refugees to stay in Turkey. And in the EU, many political parties and several governments need to drop their objections to visa liberalization for Turkey. And Member states that have so far refused to resettle refugees would need to change their position. All of this seems rather unrealistic.

Insane that this was not done BEFORE the deal was signed.

• Greece Appeals For EU Logistics Aid For Migrant Deal To Work (Reuters)

Greece appealed to EU partners on Monday for logistical help to implement a deal with Turkey meant to stem an influx of migrants into Europe, as people – many unaware of the tough new rules – continued to come ashore on Greek islands. Economically battered Greece, for months at the epicenter of Europe’s biggest migrant crisis since World War Two, is struggling to mount the massive logistics operation needed to process asylum applications from the many hundreds of migrants still arriving daily along its shoreline. Turkish officials arrived on the Greek island of Lesvos on Monday to help realize the deal, which requires new arrivals from March 20 to be held until their asylum applications are processed and for those deemed ineligible to be sent back to Turkey from April 4 onwards.

“We must move very swiftly and in a coordinated manner over the next few days to get the best possible result,” Greek Prime Minister Alexis Tsipras said after meeting EU Migration Commissioner Dimitris Avramopoulos in Athens. “Assistance in human resources must come quickly.” Under the EU-Turkey roadmap agreed last Friday, a coordination structure must be created by March 25 and some 4,000 personnel – more than half from other European Union member states – deployed to the islands by next week. Avramopoulos said France, Germany and the Netherlands had already pledged logistics and personnel. “We are at a crucial turning point … The management of the refugee crisis for Europe as a whole hinges on the progress and success of this agreement,” he said.

However, on Monday, the day after the formal start of an agreement intended to close off the main route through which a million refugees and migrants arrived in Europe last year, authorities said 1,662 people had arrived on Greek islands by 7 a.m. (0500 GMT), twice the official count of the day before.

Too late.

• EU Rights Chief Demands More Protection For Refugees (AP)

The Council of Europe commissioner for human rights is calling for additional measures to protect the rights of migrants now that a deal has been reached by the EU and Turkey. Nils Muiznieks said the deal’s legal and procedural safeguards should apply to all people – not just Syrians – reaching Greece or any EU country. Such safeguards should likewise extend to anyone who is returned to Turkey. He also called on Greece and Turkey to limit the use of detention of migrants to “exceptional” cases and take steps to ensure there are no collective returns. Muiznieks described the deal, which officially came into effect on Sunday, as “just a patch to plug one of the holes in the highly dysfunctional approach of European states to migration.”

People come to you for help and you lock them up?!

• Greece Sets Up Detention Camps As Refugee Deal Hits Delays (AP)

Greece detained hundreds of refugees and migrants on its islands Monday, as officials in Athens and the European Union conceded a much-heralded agreement to send thousands of asylum-seekers back to Turkey is facing delays. Migrants who arrived after the deal took effect Sunday were being led to previously open refugee camps on the islands of Lesbos and Chios and held in detention, authorities on the islands said. EU countries are trying to avoid a repeat of the mass migration in 2015, when more than a million people entered the bloc. Most were fleeing civil war in Syria and other conflicts, traveling first to Turkey and then to the nearby Greek islands in dinghies and small boats. Efforts to limit migration have run into multiple legal and practical obstacles.

Under the deal, Greek authorities will detain and return newly arrived refugees to Turkey. The EU will settle more refugees directly from Turkey and speed up financial aid to Ankara. The two sides, however, are still working out how migrants will be sent back. “We are conscious of the difficulties,” EU Commission spokesman Margaritis Schinas said in Brussels. “And we are working 24-7 to make sure that everything that needs to be in place for this agreement to be implemented soon is happening.” Commission officials said support staff needed to implement the deal -including hundreds of translators and migration officers- would not start arriving until next week. Returns, they said, cannot start until Greece changes its law to recognize Turkey as a “safe country” for asylum applications.

The human rights group Amnesty International sharply criticized the plan. “Turkey does not offer adequate protection to anyone,” Iverna McGowan, the head of Amnesty’s EU office, told The Associated Press, accusing Turkey of routinely forcing Syrians back across the border.