Arthur Rothstein Going to church to pray for rain., Grassy Butte, North Dakota Jul 1936

Panic.

• ‘Panic Situation’ As Asia Stocks Tumble Amid Fears Of New Global Recession (G.)

Japan’s Nikkei index plummeted more than 950 points on Tuesday, its biggest intraday loss since May 2013, and the yen briefly soared to a 14-month high against the US dollar, as continued fears over the health of the global economy saw a continuation of the previous day’s selloff in Europe and the US. The Nikkei dived 5.1% to 16,132.25 in morning trading and extended losses into the afternoon, while Australia’s S&P/ASX 200 fell 2.6% to 4,946.70. Markets were also down in the Philippines, Indonesia, Thailand and New Zealand. The MSCI’s index of Asia-Pacific shares outside Japan fell 1% and might have fallen further had several Asian markets not been closed.

Markets in China, Hong Kong, Taiwan and South Korea were closed for Lunar New Year holidays. Most markets in the region will re-open from Wednesday, with Chinese markets returning next week. The volatility affecting global markets last month appears set to continue amid concern about Chinese economic growth, falling oil prices and speculation that the US federal reserve could change course with interest rates. “The combination of concerns that the United States could be heading toward a recession and the global stock sell-off is curbing risk appetite and is sending investors to the safe-haven yen,” Takuya Takahashi at Daiwa Securities told Kyodo News.

After hovering around the 117-yen line on Monday, the Japanese currency briefly rose to the upper 114 zone to its strongest level against the dollar since November 2014. Investors regard the yen as a “save haven” currency when global markets are hit by the kind of turmoil witnessed in recent weeks. The yen is expected to make further gains – a trend that eats into the repatriated profits of Japanese auto and other exporters. Three-month dollar/yen implied volatility – which indicates how much currency movement is expected in the months ahead – reached 12.137% its highest since September 2013. Responding to the yen’s rise, Japan’s finance minister, Taro Aso, told reporters: “It is clear that recent moves in the market have been rough. We will continue to carefully monitor developments in the currency market.”

And more panic.

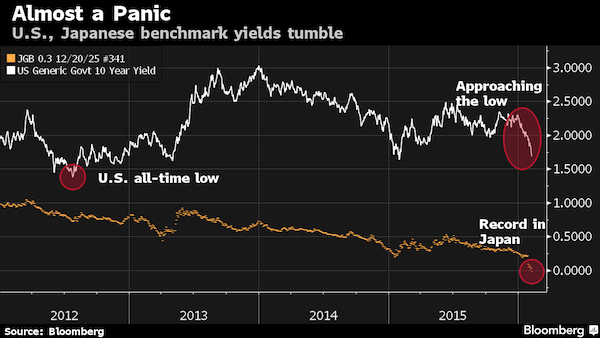

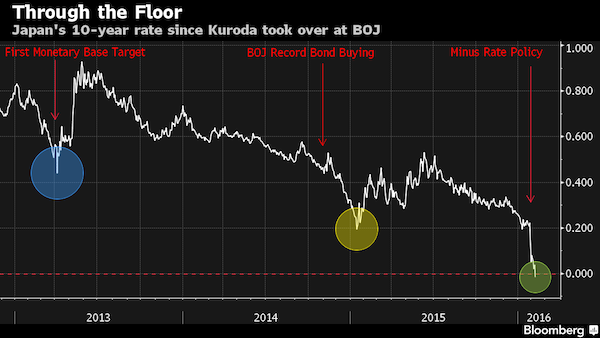

• Global Bond Rally Near ‘Panic’ Level With Japan Yield Below Zero (BBG)

Sovereign bonds surged, sending the Japanese benchmark 10-year yield below zero for the first time, as investors seeking the safest assets gorged on government debt. Treasury yields dropped to a one-year low in the rush to refuge from a worldwide stock rout. Traders pared the odds the Federal Reserve will raise interest rates this year to 30%, before Chair Janet Yellen begins her two-day testimony to Congress on Wednesday. The yield on the Bank of America Merrill Lynch World Sovereign Bond Index tumbled to 1.29%, the least in data that go back to 2005. “It’s almost like a panic,” said Hideo Shimomura, the chief fund investor in Tokyo at Mitsubishi UFJ Kokusai Asset Management. “The flight to quality is exaggerated.”

The benchmark 10-year Treasury yield tumbled six basis points to 1.69% as of 2:31 p.m. in Tokyo, according to Bloomberg Bond Trader data. The price of the 2.25% security due in November 2025 rose 17/32, or $5.31 per $1,000 face amount, to 105. Japan’s 10-year yield fell to minus 0.01%, an unprecedented low for such a maturity in a Group-of-Seven economy. Australia’s dropped to 2.38%, a level not seen since April. Investors rushed to bonds as the MSCI Asia Pacific Index of stocks slid 2.8% and Japan’s Topix Index plunged 5.7%. “It’s hard to find a reason to short Treasuries,” said Tomohisa Fujiki at BNP Paribas in Tokyo, referring to bets that a security will fall. Turmoil “is now affecting equity markets in developed countries as well — and commodities and emerging markets have not stabilized yet.” BNP is one of the 22 primary dealers that underwrite the U.S. debt.

BoJ buys them all anyway.

• Japan’s 10-Year Yield Falls Below Zero for the First Time (BBG)

The yield on Japan’s benchmark 10-year government bonds fell below zero for the first time, an unprecedented level for a Group-of-Seven economy, as global financial turmoil and the Bank of Japan’s adoption of negative interest rates drive demand for the notes. The 10-year yield has tumbled from 0.22% before the BOJ surprised markets with the decision on Jan. 29 to introduce a minus 0.1% rate on some of the reserves financial institutions park at the central bank. It fell 7 1/2 basis points to a record minus 0.035% as of 3:05 p.m. in Tokyo. Japanese bonds are also climbing as sovereign securities rally worldwide. Global stocks have dropped 10% this year on concern growth is slowing in China, and as slumping oil prices undermine policy makers efforts to revive inflation.

About 29% of the outstanding debt in the Bloomberg Global Sovereign Bond index was yielding less than zero as of 5 p.m. in New York on Monday. Swiss 3% notes due in 2018 were offering the lowest yield in the index, according to data compiled by Bloomberg. “It was just a matter of time before 10-year yields went negative, so it wasn’t a surprise,” said Yusuke Ikawa at UBS. Five-year yields dropped seven basis points to minus 0.25%, while two-year yields slid five basis points to minus 0.245%. Both were record lows. A basis point is 0.01 percentage point. The expected price volatility for Japanese debt over a 60-day period soared to 3.13% on Monday, the highest level since June, according to data compiled by Bloomberg.

Banks across the globe are under fire.

• US Bank Stocks And Bonds Clobbered By Recession Worry (Reuters)

U.S. bank stocks and bonds took a pounding on Monday as recession fears compounded concern about their exposure to the energy sector and expectations that global interest rates are unlikely to rise quickly. The S&P 500 financial index, already the worst performing sector this year, fell 2.6% and now stands more than 20% from its July 2015 high, confirming the sector is in the grip of a bear market. Shares of Morgan Stanley slid 6.9% in their largest one-day drop since November 2012, while rival Goldman Sachs fell 4.6%. Both stocks closed at their lowest since the spring of 2013. Meanwhile, bonds issued by U.S. banks extended their decline, with the yield premium demanded by investors to hold these securities, rather than safer U.S. Treasury debt, climbing to the highest in three-and-a-half years, according to BofA Fixed Income Index data.

“Investors’ attitudes seem to be worsening relative to the likelihood of a global recession. I think that’s what financials are reflecting – that their net interest margins are going to be further compressed under collapsing (sovereign) bond yields,” said Mark Luschini, chief investment strategist at Janney Montgomery Scott in Philadelphia. Yields on sovereign bonds from so-called safe-haven issuers such as the United States, Germany and Japan have tumbled recently as investors increasingly doubt central banks in these countries will be able to raise interest rates any time soon. The U.S. Federal Reserve late last year pulled off its first rate increase in nearly a decade, but interest rate futures markets now assign just a 1-in-4 chance of another one this year. And the Bank of Japan last month cut rates into negative territory for some bank reserves.

Monday’s drop in U.S. bank stocks follows concern over stress in the financial sector in Europe, where the cost of insuring the European financial sector’s senior debt against default climbed to its highest level since late 2013. Credit default swaps on several U.S. banks have followed suit. The cost for a five-year CDS contract on Morgan Stanley debt, for instance, has rocketed by more than 27% since last Thursday and now stands at its highest since October 2013, data from Markit shows. Citigroup’s CDS, likewise, is at the highest since June 2013.

“Japanese Finance Minister Taro Aso felt moved enough to warn the yen’s rise was “rough”..”

• Investors Dump Stocks, Seek Safe Havens As Bank Fears Flare (Reuters)

Asian share markets were scorched on Tuesday as stability concerns put a torch to European bank stocks and sent investors stampeding to only the safest of safe-haven assets. As fear overwhelmed greed, yields on longer-term Japanese bonds fell below zero for the first time, the yen surged to a 15-month peak and gold reached its most precious since June. Japanese Finance Minister Taro Aso felt moved enough to warn the yen’s rise was “rough”, something of an understatement as the Nikkei nosedived 5.4%. MSCI’s broadest index of Asia-Pacific shares outside Japan fell 1.2%, with Australian shares hitting 2-1/2-year closing low, and would have been lower if not for holidays in many centres.

Spread-betters see another weak session in European shares, where German DAX is seen falling 0.7% and Britain’s FTSE 0.5%. S&P 500 e-mini futures fell more than 1% at one point. “Sentiment towards risk assets remained extremely bearish and price action reflected a market that may be capitulating,” said Jo Masters, a senior economist at ANZ. All of which magnified the stakes for U.S. Federal Reserve Chair Janet Yellen’s testimony this week. “She needs to come across as optimistic without being too hawkish and cautious without being negative,” said Masters. “Hawkishness or dovishness could easily exacerbate the current sell-off, tightening financial conditions further.”

Wall Street pared losses but still ended deep in the red. The Dow lost 1.1%, while the S&P 500 fell 1.42% and the Nasdaq 1.82%. The rout began in Europe on Monday, when the FTSEurofirst 300 index shed 3.4% to its lowest since late 2013, led by a near 6% dive in the banking sector. Deutsche Bank alone sank 9.5% as concerns mounted about its ability to maintain bond payments. Late Monday, the German bank said it has “sufficient” reserves to make due payments this year on AT1 securities. The cost of insuring bank debt against default also climbed to its highest since late 2013. Borrowing costs in Spain, Portugal and Italy jumped as investors demanded a fatter risk premium over safer German paper, where two-year yields hit record lows at minus 52 basis points.

“..additional Tier 1 bonds..” Sounds solid?!

• Banks Bonds Are “The Epicenter Of Growth Concerns Globally” (BBG)

Last year’s sure thing in credit markets is quickly becoming this year’s nightmare for bond investors. The riskiest European bank debt generated returns of about 8% last year, according to BofAML index data, beating every type of credit investment globally. In less than six weeks this year, those gains have been all but wiped out, even after interest payments. Investors are increasingly concerned that weak earnings and a global market rout will make it harder for banks to pay the interest on at least some of these securities, or to buy them back as soon as investors had hoped. The bonds allow banks to skip interest payments without defaulting, and they turn into equity in times of stress. Deutsche Bank may struggle to pay the interest on these securities next year, a report from independent research firm CreditSights earlier on Monday said. The bank took the unusual step of saying that it has enough capacity to pay coupons for the next two years.

“The worries about these bonds represent real fears that the European banking system may be weaker and more vulnerable to slowing growth than a lot of people originally thought,” said Gary Herbert at Brandywine Global Investment Management. “It’s the epicenter of growth concerns globally. And it doesn’t look pretty,” he added. Money managers’ concerns are spreading even to safer bank bonds, underscoring how investors are running away from risk across a broad range of assets now, from stocks to commodities to corporate bonds. The cost of protecting against defaults on safer U.S. and European financial debt known as senior unsecured notes has jumped to the highest level since 2013. European banks are looking less solid since their last earnings reports.

Deutsche Bank for example last month posted its first full-year loss since 2008, and its shares have plunged. Credit Suisse’s shares plunged to their lowest level since 1991 after the Swiss bank posted its biggest quarterly loss since the crisis. Banks have issued about €91 billion of the riskiest notes, called additional Tier 1 bonds, since April 2013. The problem is the securities are untested and if a troubled bank fails to redeem them at the first opportunity or halts coupon payments investors may jump ship, sparking a wider selloff in corporate credit markets. “It’s the first thing that gets cut from portfolios,” said David Butler, a portfolio manager at Rogge Global Partners, which oversees about $35 billion of assets. “When the wider credit market turns, it leaves investors exposed.”

Feel better now? “For those “brave enough to defy Mr Market’s gloomy prognosis”, this may be an ideal time to jump back into the stock market, said Mr Hatzius.”

• Goldman Sachs Sees Near-Zero Risk Of UK Recession Despite Market Tantrum (AEP)

Britain is extremely unlikely to face an economic recession over the next two years and is on safer ground than any other major country in the developed world, according to a new crisis-study by Goldman Sachs. The US investment bank said the global stock market rout and the credit tremors this year are sending off false signals, insisting that underlying indicators of economic health show little sign of a sudden rupture in Europe, the US or across the OECD bloc of rich states. An array of “alarm” indicators – based on the experience of 20 countries since 1970 – suggest that the current business cycle is still in full swing and far from exhaustion, even if risks have been ratcheting up over recent months. Credit ratios are high but they have not been spiking higher in most OECD states, and there is still plenty of slack left in the economy.

This allows central banks to take their time before having to slam on the brakes – the time-honoured cause of recessions. Jan Hatzius, Goldman’s chief US economist, cited a string of episodes where markets were gripped by fear and emotion yet the storm passed without doing much damage. These included the 1987 stock market crash, the 1994 bond rout, Mexico’s Tequila crisis, the failure of the giant hedge fund Long-Term Capital Management and the Asian crisis in 1998, the corporate credit squeeze from 2002-2003 at the onset of the Iraq War and the eurozone sovereign debt crisis. “In each case, at least some financial markets were priced for significant recession risk, if not an outright slump,” he said. Yet Goldman cautioned that it would be a “grave error” to ignore the latest market tantrum altogether.

The US Federal Reserve was able to slash interest rates and flush the international financial system with liquidity to weather the 1987 and 1998 storms, something that would be much harder to pull off today. Mounting worry over China – and its linkages through the commodity nexus – has put everybody’s nerves on edge this time. “Financial markets now signal a high probability of another recession. High-yield spreads are at levels almost never seen outside of recessions,” said Mr Hatzius. “The message from the equity market is less clear-cut, but there are only a few non-recessionary instances over the past three decades in which the S&P 500 (index of US equities) performed as poorly as it did over the past year,” he said. That said, Britain appears rock-solid under the Goldman Sachs model with a mere 3pc risk of losing its footing over the next eight quarters, followed by Sweden, Denmark and South Korea.

“Basically they’re maxxing out their credit cards before the banks can cut them off.”

• Chesapeake Energy Plunges On Bankruptcy Fears (Forbes)

Shares in Chesapeake Energy were halted in mid-morning trading after selling off more than 50% to new lows on a report from Debtwire that the company had hired restructuring specialists Kirkland & Ellis . Seeking to stem the panic, Chesapeake issued a statement saying it “has no plans to pursue bankruptcy” and that Kirkland & Ellis had been one the company’s law firms since 2010. Chesapeake also reportedly hired restructuring specialists Evercore Partners back in December. After trading resumed, shares recovered some of their ground, jumping from $1.50 to $2.25, though still off 27% on the day so far. At these levels, all of Chesapeake’s equity could be had for $1.4 billion. Shares traded above $30 in 2014, and north of $60 in 2008, when natural gas prices hit record highs.

Naturally, holders of Chesapeake debt are shooting first and asking questions later. Its nearest-term bond matures March 15; it traded as high as 95 cents on the dollar late last week, but plunged this morning to 73.75 cents. After the announcement the bonds recovered above 80 cents, according to FINRA data. Investors are concerned that Chesapeake will be unwilling or unable to roll the debt. According to a report this morning from Troubled Company Reporter, some of Chesapeake’s longer dated issues are trading below 30 cents. Chesapeake has been looking for options to improve liquidity. Late last year amended its $4 billion bank revolver, changing it from an unsecured line to secured. It also did a distressed-debt-exchange offer, taking in $3.8 billion in notes in exchange for $2.4 billion in second-lien debt. It recently canceled dividend payments on its preferred stock.

A big problem for Chesapeake and many other exploration and production companies: their oil and gas hedges are rolling off, meaning that the little protection they used to have against low commodity prices is evaporating. As billionaire natural gas trader John Arnold tweeted this morning: “The wave of E&P bankruptcies starts now. CHK alone has nearly $1 billion less in hedging gains in ’16 than ’15 at today’s prices.” I talked to a well-placed banker over the weekend who says restructuring advisors at shops like Lazard and Kirkland & Ellis had been advising his clients to begin drawing down any cash remaining on their bank revolvers in order to maximize liquidity to get them through the next few months. Basically they’re maxxing out their credit cards before the banks can cut them off. That’s exactly what Linn Energy said last week that it had done; with more than $4 billion in credit facilities maxxed. Shares in LINE fell 50% on Friday and are off another 24% today. Linn’s debt is trading below 20 cents.

“We need to close that gap. And the way that that will happen is the rest of those bankruptcies will go forward.”

• 150 Oil And Gas Companies “At Risk Of Bankruptcy” As Prices Fall (BBG)

About 150 oil and gas companies tracked by energy consultant IHS Inc. may go bust as a supply glut pressures prices and punishes revenues. The number of companies at risk is more than twice the 60 producers that have already filed for bankruptcy, Bob Fryklund, chief upstream analyst at IHS, said in an interview. A further shake out would help stimulate deals that have been on hold because buyers and sellers have disagreed on asset values, he said. Oil has collapsed about 70% over the past two years as U.S. shale producers boosted output and OPEC flooded the market with crude to drive out higher-cost suppliers. More bankruptcies would be one signal that energy prices have reached a bottom and would help kick off deals for the $230 billion worth of oil and gas assets currently up for sale, according to Fryklund.

“Nobody is buying because there is a mismatch between expectations,” Fryklund said in an interview in Tokyo. “We need to close that gap. And the way that that will happen is the rest of those bankruptcies will go forward.” Companies that plan to make investments are likely to wait for prices to gain for six months because they want to be confident in a recovery, according to Fryklund. “It usually happens as we begin to come back up on price,” he said. “There is always a little lag on timing.” The global oil surplus that fueled crude’s decline to a 12-year low will shift to a deficit as output falls and a new bull market begins before the year is out, Goldman Sachs said in January.

U.S. production will drop by 620,000 barrels a day, or about 7%, from the first quarter to the fourth, according to the Energy Information Administration. Low prices are also spurring greater efficiency, according to IHS. Operating costs on a per barrel basis declined about 35% last year in North America and have dropped about 20% globally, according to the consultant. Crude output from North Dakota rose through most of last year and some producers in the Permian Basin in western Texas can break-even drilling oil at $35 a barrel, he said.

88% full is about as full as it can get. Tanks at Cushing are used for blending too. Can’t do that if they get even fuller.

• US Oil Industry Woes Grow As Storage Levels Hit ‘Critical Level’ (MW)

The storage tanks at Cushing, Okla., the delivery point for the New York Mercantile Exchange crude contract, are edging closer to their limits, raising a new set of problems for an industry that has already suffered from a 70% drop in prices in the past year and a half. Cushing, which represents about 13% of the nation’s oil storage, has a working capacity of about 73.014 million barrels of crude oil, according to data from Sept. 2015, the latest available from the EIA. As of the week ended Jan. 29, there was 64.174 million barrels of oil in storage at Cushing, so it is at about 88% full. “Where inventories count the most—at the Nymex terminal complex in Cushing, Oklahoma—storage is already at a critical level,” said Stephen Schork, in The Schork Report published Monday.

“Approximately 6 out of 7 barrels available storage capacity at the Nymex hub are now full.” The report highlighted an article from Reuters that discussed delays in crude deliveries from storage tanks at Cushing because there wasn’t enough room to drain existing tanks to blend oil to meet West Texas Intermediate crude specifications. Cushing serves as a blending station, where crude oil from the midcontinent is mixed to the specific grades required by different refineries, according to StateImpact Oklahoma. “We soon might be in a situation that we have so much oil, that we don’t have enough of the right kind of oil,” Schork said.

But that’s not the only problem. Richard Hastings, macro strategist at Seaport Global Securities, said building more tanks would take time and there would be questions over how the cost of tanks would be shared across the supply chain. Meanwhile, the market is dealing with a “constant high volume” of crude oil coming from the floating storage at the Gulf Coast, the Canadian crudes coming by rail to the U.S. and domestic production, said Hastings. “If the volumes get too high, then the intermediate delivery steps—moving large volumes from tanks to pipelines—could be difficult if the local hub’s pipeline capacity is constrained,” he said.

“..no matter how much P.R. or whitewashing they use, the market knows this is over and we’re not going to play this game anymore.”

• Jim Rogers: “The Market Knows It’s Over” (SHTF)

Back in the 1970’s as recession gripped the world for a decade, stocks stagnated and commodities crashed, investor Jim Rogers made a fortune. His understanding of markets, capital flows and timing is legendary. As crisis struck in late 2008, he did it again, often recommending gold and silver to those looking for wealth preservation strategies – move that would have paid of multi-fold when precious metals hit all time highs in 2011. He warned that the crash would lead to massive job losses, dependence on government bailouts, and unprecedented central bank printing on a global scale. Now, Rogers says that investors around the world are realizing that the jig is up. Stocks are over bloated and central banks will have little choice but to take action again. But this time, says Rogers in his latest interview with CrushTheStreet.com, there will be no stopping it and people all over the world are going to feel the pain, including in China and the United States.

We’re all going to suffer… I can think of very few places that won’t suffer. But most people are going to suffer the next time around. Central banks will panic. They will do whatever they can to save the markets. It’s artificial… it won’t work… there comes a time when no matter how much money you have, the market has more money. [..] I don’t know if they’ll even call it QE (Quantitative Easing) in the future… who knows what they’ll call it to disguise it… they’re going to try whatever they can… printing more money or lowering interest rates or buying more assets… but unfortunately, no matter how much P.R. or whitewashing they use, the market knows this is over and we’re not going to play this game anymore.

The entire world is about to get hammered and the average person on the street is the one who will pay the price, as is usually the case. We can expect more losses in markets, more losses in jobs and more losses to freedom as governments and central banks point the finger at everyone but themselves.

If that’s your sole alternative…

• Can Hobbit Tourism Save New Zealand’s Troubled Dairy Farmers? (BBG)

New Zealand farmer Ian Diprose used to count on the dairy industry for most of his income. Today, he relies on tourism. As plunging milk prices push dairy farms into the red and hurt rural businesses, Diprose and wife Joy are making more money accommodating tourists than other farmers’ cows. That’s because their grazing property in Waikato, New Zealand’s dairying heartland, is about 16 kilometers (10 miles) from Hobbiton, a life-sized imitation of Bilbo Baggins’ Shire created for Peter Jackson’s Lord of the Rings and Hobbit movies. “A lot of the people who come through here are Hobbiton-crazy,” said Diprose, 73, whose De Preaux Lodge in Matamata offers bed, breakfast, a home-cooked meal and an authentic New Zealand farm experience for NZ$175 ($120) a night. “In our little town, we have something like 30 cafes or places to eat because of the tourists coming through.”

The Diproses started offering accommodation five years ago as a hobby to augment income from agisting cattle. Today, it’s their main business. Four out of five dairy farmers in New Zealand, the world’s biggest dairy exporter, will operate at a loss this season as the global slump in milk prices enters its third year, according to the central bank. That’s curbing farmers’ spending and damping economic growth, even as a tourism boom helps to soften the blow. “I’ve reduced my grazing prices to one of my customers quite drastically because she’s a young farmer and I know she’s struggling,” said Diprose, who has two sons dairying. “The impact it’s having on them is crippling. The financial situation of the dairy farmers, I weigh that up every day in my heart.” As farmers tighten their belts, demand for fertilizer to veterinary services has fallen, and retailers in rural towns are feeling the pinch.

At Giltrap AgriZone, which sells hay balers and tractors at three outlets around Waikato, sales are down 30% from a year ago, said Managing Director Andrew Giltrap. “We’re on a roller coaster and we just have to ride it out,” he said. New Zealand, once known as the country with 10 times more sheep than people, has stepped up investment in dairy farming in the past decade. The nation now boasts 5 million cows, more than its 4.5 million human population, while sheep numbers have declined 26% since 2006 to 29.5 million. The strategy made sense when milk prices surged to a record in 2007 and neared that peak again in 2013. Since then, a global oversupply and waning demand for milk powder from a slumping China have seen prices crash. With plunging oil prices now sapping milk purchases by Russia and other energy-producing nations, dairy prices are approaching the 12-year low they hit in August.

But they’ll let him, want to bet? Europe’s rudderless. He has a demand or two in Syria as well.

• Turkey’s Erdogan Threatened To Flood Europe With Migrants (Reuters)

Turkish President Tayyip Erdogan threatened in November to flood Europe with migrants if EU leaders did not offer him a better deal to help manage the Middle East refugee crisis, a Greek news website said on Monday. Publishing what it said were minutes of a tense meeting last November, the euro2day.gr financial news website revealed deep mutual irritation and distrust in talks between Erdogan and the EU’s two top officials, Jean-Claude Juncker and Donald Tusk. The EU officials were trying to enlist Ankara’s help in stemming an influx of Syrian refugees and migrants into Europe. Over a million arrived last year, most crossing the narrow sea gap between Turkey and islands belonging to EU member Greece.

Tusk’s European Council and Juncker’s European Commission declined to confirm or deny the authenticity of the document, and Erdogan’s office in Ankara had no immediate comment. The account of the meeting, in English, was produced in facsimile on the website. It does not state when or where the meeting took place, but it appears to have been on Nov. 16 in Antalya, Turkey, where the three met after a G20 summit there. “We can open the doors to Greece and Bulgaria anytime and we can put the refugees on buses … So how will you deal with refugees if you don’t get a deal? Kill the refugees?” Erdogan was quoted in the text as telling the EU officials. It also quoted him as demanding €6 billion over two years. When Juncker made clear only half that amount was on offer, he said Turkey didn’t need the EU’s money anyway.

The EU eventually agreed a €3 billion fund to improve conditions for refugees in Turkey, revive Ankara’s long-stalled accession talks and accelerate visa-free travel for Turks in exchange for Ankara curbing the numbers of migrants pouring into neighboring Greece. In heated exchanges, Erdogan often interrupted Juncker and Tusk, the purported minutes show, accusing the EU of deceiving Turkey and Juncker personally of being disrespectful to him.The Turkish leader was also quoted as telling Juncker, a former prime minister of tiny Luxembourg, to show more respect to the 80-million-strong Turkey. “Luxembourg is just like a little town in Turkey,” he was quoted as saying.The tense dialogue highlighted the depth of mutual suspicion at a time when the EU is banking on Turkish help to alleviate its worst migration crisis since World War Two.

The EU says the flow of people from Turkey, which hosts more than 2.5 million Syrian refugees, has not decreased in any significant way since the bloc’s joint summit with Ankara in November, when they had agreed the fund for refugees there.The report prompted a member of the European Parliament from the Greek centrist party To Potami to ask the European Commission to confirm the purported talks.”If the relevant dialogues between the EU officials and the Turkish President are true, it seems that there are aspects of the deal between Ankara and the EU which were concealed on purpose,” Miltos Kyrkos said in the question he submitted to the Commission. “We want immediately an answer on whether these revelations are true and where the Commission’s legitimacy to negotiate, using Turkey’s accession course as a trump card, is coming from,” Kyrkos said.

Sweet Jesus.

• 35 Refugees Die Off Turkish Coast (Guardian)

At least 35 people have died after two boats carrying refugees sank off Turkey’s Aegean coast, according to reports. The Turkish coastguard said 24 drowned when a boat capsized in the Bay of Edremit, near the Greek island of Lesbos, while the Dogan news agency reported that the bodies of 11 people were found after a separate accident further south, near the Aegean resort of Dikili. The deaths came as Angela Merkel, the German chancellor, met the Turkish prime minister, Ahmet Davutoglu, for more talks on reducing the influx of refugees to Europe.

Turkey is central to Merkel s diplomatic efforts to reduce the flow. Germany saw an unprecedented 1.1 million asylum seekers arrive last year, many of them fleeing conflicts in Syria, Iraq and Afghanistan. In her weekly video message on Saturday, Merkel said European Union countries agree that the bloc needs to protect its external borders better, and that that is why she is seeking a solution with Turkey. She added that, if Europe wants to prevent smuggling, “we must be prepared to take in quotas of refugees legally and bear our part of the task”. “I don t think Europe can keep itself completely out of this”, Merkel said.