Piet Mondriaan Still Life with Gingerpot I 1911/12

https://twitter.com/Real_RobN/status/2044957624215724224?s=20

"So it all starts to tie together and show this, this real distinct bias they had against President Trump and how they tried to undermine his entire first term" @Jim_Jordan explains how newly revealed impeachment memos show the clear bias of 2019 Ukraine accuser pic.twitter.com/4xCcevLMGZ

— Just the News (@JustTheNews) April 16, 2026

BOMBSHELL EXPOSÉ: Twenty CIA and FBI agents confirmed that Barack Obama and a former CIA director fabricated the Russia Hoax, which was then 'locked away in a CIA vault for almost a decade,' to brainwash voters and discredit Trump's election by manipulating intelligence. pic.twitter.com/F6gPpVgQ9U

— FAN TRUMP ARMY (@TRUMP_ARMY_) April 16, 2026

John Solomon Just Blew My Mind with His Prediction About Deep State Accountability

— Benny Johnson (@bennyjohnson) April 16, 2026

Solomon says President Trump is about to begin declassifying documents at lightning speed in an operation he is calling “Hypersonic Clarity."

He believes this massive document dump could pave… pic.twitter.com/oABYOmDTPR

John Solomon Reveals New John Brennan and James Comey Indictments Could Be Coming VERY Soon

— Benny Johnson (@bennyjohnson) April 16, 2026

Brennan is accused of lying to Congress in 2023 testimony about the CIA's use of the discredited Steele dossier in intelligence assessments of Russian interference in the 2016 election.… pic.twitter.com/x0iMyKz91Y

https://twitter.com/VigilantFox/status/2044812878192992698?s=20Hillary Clinton is cooked if the emails and videos from the Weiner laptop are fully released. This will burn the entire corrupt system down and everyone in it. Those emails contained:

— The SCIF (@TheSCIF) April 17, 2026

– Child trafficking and abuse

– Money laundering

– Epstein ties

– Weiner's "Insurance policy"… pic.twitter.com/9X2u1kSbcu

The notion of Iranian strength persists. Why? The US will never accept the mullahs with nukes, and US/Israel want Iran to stop stoking up Hezbollah etc. They won’t give up until they have what they want.

• Trump Is Turning Iran Into An Anti-Globalist Superpower (Rachel Marsden)

If Team Trump has dragged itself to the negotiating table with Iran, it’s not because the U.S. is winning this war. One side of these talks features top Iranian brass. The other, two real estate agents (Steve Witkoff and Jared “Gaza Riviera” Kushner), Vice President JD Vance who’s fresh off complaining about meddling in Hungarian elections while over there doing some himself, and a top Pentagon official sufficiently problematic to have escaped recent firings by a war secretary who keeps evoking Holy War.Read more …

To even get to the table, Iran demanded a release of billions of U.S.-held funds under sanctions, and for Israel to stop bombing Lebanon under its usual pretext of striking terrorists, who routinely just always happen to be hanging out on land that it’s long wanted to expand into. We’re a long way from Trump’s longstanding whining about how Obama “gave” Iran $6 billion of its own money back that had, in fact, been held under U.S. sanctions in American banks.“Obama gave them $1.7 billion in cash – green, green cash, took it out of banks from Virginia, DC and Maryland, all the cash they had, flew it by airplanes in an attempt to buy their respect and loyalty but it didn’t work. They laughed at our president,” Trump said in a primetime address earlier this month. Guess they’re laughing even harder now. Not only have any longstanding U.S.-Israeli objectives for Iran been frustrated, but they’ve virtually evaporated. First, there’s everything that Iran has maintained. It still has its enriched uranium, despite what Iran qualified as a failed Pentagon operation to take it while pretending to stage a personnel rescue.

But now it enjoys the added bonus of not being under any official obligation to abide by inspections either, since Trump unilaterally ripped that treaty up.] It’s also under no compulsion to open the Strait of Hormuz and let through oil tankers that fuel the world. A problem that didn’t actually exist until Trump unilaterally created it. But since the opportunity presented for Iran to close it under the pretext that missiles were flying around overhead, why wouldn’t they seize that leverage?

Now, the strait sits at the center of negotiations between the two sides. Not only has the U.S. lacked any leverage to compel Iran to open Hormuz, but they’ll also have to find some additional consideration to get Iran to give up the tolls that it recently imposed on ships passing through. And good luck trying to settle this one quickly, since Iran has also said that, “Oh yeah, by the way, we can’t find some of those land mines that we scattered underwater to prevent trespassing ships.” Guess that’ll conveniently take awhile to resolve, all while they collect tolls at the purported rate of $2 million per ship.

Tehran seems to have no end of weapons to adequately defend its territory from attacks, all while Britain’s Royal United Services Institute think tank reports “a strategically ruinous cost-exchange ratio that the West’s industrial capacity is not prepared to sustain” despite the astronomical cost billed routinely to Western taxpayers in order to avoid such things. So toss the myth of western military omnipotence onto the mounting pile of ripoff schemes that have aged badly. Who knew that an attempt to ruin Iran’s navy and army would result in the demilitarization of the West? Not the brainiacs in charge, apparently.

Iranian governance continuity doesn’t seem to have missed a beat, either, despite Trump’s avowed regime- change attempts. And when Trump issued his Churchillian ultimatum last week for Iran to “Open the F–kin’ Strait, you crazy bastards, or you’ll be living in Hell,” and threatened that “Tuesday will be Power Plant Day, and Bridge Day, all wrapped up in one,” the same Iranians whom Trump had previously promised to liberate before bombing them, flooded Iranian cities to protect their own infrastructure from their self-styled savior.

Meanwhile, under pressure from their own citizens, blowback from U.S. allies is intensifying against Trump and his sidekick, Israeli Prime Minister Netanyahu. European countries have denied military access to their airspace for the purpose of any attacks. Several European nations, and the European Commission itself, are now talking about suspending the bloc’s economic association agreement with Israel. “Israeli strikes killed hundreds last night, making it hard to argue that such heavy-handed actions fall within self-defence,” said the EU’s chief diplomat, Kaja Kallas, of Tel Aviv’s attacks on Lebanon.

It’s all rapidly shaping up to be a prelude to anti-Israeli sanctions, all while Iran heads in the other direction with negotiation and rapprochement with European nations in exchange for passage through Hormuz. And for Team Trump’s deal with Iran to achieve a peaceful outcome and unscrew the global economy, they’ll have the added bonus of being stuck permanently babysitting loose-cannon Israel. Which is a markedly different relationship from the previous arrangement of backing Israel as a proxy against Iran while shrugging and promoting Tel Aviv’s sovereign right to self-defense.

Back home in the U.S., calls for cracking down on the kind of Israeli foreign interference in American politics that led Trump into this useless but totally counterproductive war are emerging. Hardly surprising when the average American citizen is being fiscally mugged by the consequences of double standards that have long been at play, with Israeli entities not only exempt from registering as foreign agents, but exceptionally blessed to freely interfere in American political life.

At this point, Iran is looking less like a rival to the average Westerner, and more like an ally of the America First anti-globalist movement, successfully dismantling the illusion that exorbitant and self-indulgent Western foreign policy serves anything more than outdated narratives.

Rachel Marsden

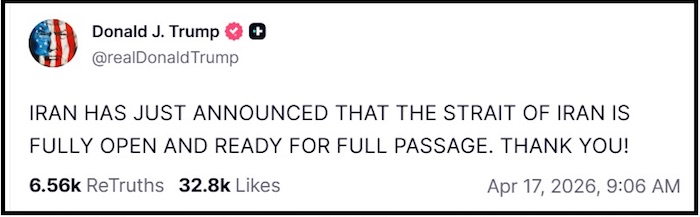

“It appears the blockade was successful in finally convincing Iran they had very few options.”

• Blockade Successful – Deal Reached – Strait Open – Oil Prices Plummet (CTH)

In a series of posts on Truth Social, President Trump has announced that a deconfliction deal with Iran has been agreed.Read more …

It appears the blockade was successful in finally convincing Iran they had very few options. Additionally, as we all well understand here, the blockade was halting oil shipments to China. It is very likely that Beijing was also putting pressure on Iran to reach a deal.

“THE STRAIT OF HORMUZ IS COMPLETELY OPEN AND READY FOR BUSINESS AND FULL PASSAGE, BUT THE NAVAL BLOCKADE WILL REMAIN IN FULL FORCE AND EFFECT AS IT PERTAINS TO IRAN, ONLY, UNTIL SUCH TIME AS OUR TRANSACTION WITH IRAN IS 100% COMPLETE. THIS PROCESS SHOULD GO VERY QUICKLY IN THAT MOST OF THE POINTS ARE ALREADY NEGOTIATED. THANK YOU FOR YOUR ATTENTION TO THIS MATTER!” ~ PRESIDENT DONALD J.TRUMP“The U.S.A. will get all Nuclear “Dust,” created by our great B2 Bombers – No money will exchange hands in any way, shape, or form. This deal is in no way subject to Lebanon, either, but the USA will, separately, work with Lebanon, and deal with the Hezboolah situation in an appropriate manner. Israel will not be bombing Lebanon any longer. They are PROHIBITED from doing so by the U.S.A. Enough is enough!!! Thank you!” ~ President DJT

“Now that the Hormuz Strait situation is over, I received a call from NATO asking if we would need some help. I TOLD THEM TO STAY AWAY, UNLESS THEY JUST WANT TO LOAD UP THEIR SHIPS WITH OIL. They were useless when needed, a Paper Tiger!” ~ President DJT

“Thank you to Saudi Arabia, UAE, and Qatar for your great bravery and help!” President DONALD J. TRUMP

“Iran, with the help of the U.S.A., has removed, or is removing, all sea mines! Thank you!” President DJT “

Again! This deal is not tied, in any way, to Lebanon, but we will, MAKE LEBANON GREAT AGAIN!”

“Thank you to Pakistan and its Great Prime Minister and Field Marshall, two fantastic people!!!” President DONALD J. TRUMP

“A GREAT AND BRILLIANT DAY FOR THE WORLD!” DJT

“Iran has agreed to never close the Strait of Hormuz again. It will no longer be used as a weapon against the World!” ~President DONALD J. TRUMP

With the fighting ending and the conflict over, suddenly the U.K and France come running to assist.

War makes the world go ’round.

• Re-enter Death Spiral When Iran War Stops – John Rubino (USAW)

Analyst and financial writer John Rubino is still warning of a currency crisis. He thinks the big run up in gold and silver in the past year are sending a message about the quality of fiat currency that governments print at will. Lots of money will be printed to prosecute the Iran war, and there will be a financial price to pay. Rubino says, “War is incredibly expensive. If the US has to add another $1 trillion to the deficit to finish this thing off, that’s another trillion we have to borrow. . .. So, we are eroding the trust that people have in our big systems. . .. The wars that we have seen lately are making the financial crisis coming our way . . much worse and making it come that much sooner.Read more …

The more money we borrow right now, the bigger of a deal it is for inflation and currency exchange rate and, ultimately, for gold and silver. Nobody should hope things like this happen, but if you are strictly looking at your own finances and you are a gold bug . . . we are screwing up the financial system that is bad for the fiat currencies and great for real money (gold and silver) and other commodities. . .. There are a lot of reasons to think commodities benefit from this war. I am kind of hesitant to look on the bright side of war . . . but I do think a war time economy is inherently inflationary, and that is inherently good for commodities.”If the war drags on, Rubino says, “It will make the coming financial crisis worse sooner.” If war finishes soon, can we all breathe a sigh of relief and be out of the woods? Rubino says, “Here’s hoping because that would be awesome. Let’s say it ends tomorrow. Then we go back to what we were doing before, which is bailing out everybody in sight, creating huge amounts of currency and lobbying the Fed to cut interest rates. In other words, we re-enter the death spiral of the world’s fiat currencies.”

Rubino is especially bullish on silver. A year ago, silver was selling in the low $30 per ounce range. Today, even after the big sell-off, it is selling in the low $80 per ounce range. Rubino says you ain’t seen nothing yet. Rubino says, “The silver story is great. More and more industries need it, and fewer and fewer mines are producing it. We have this decision point coming soon where the price is going to have to jump up to reflect the panic buying coming from the shortages.”

Rubino thinks you will be seeing $15,000 per ounce gold and $300 per ounce silver, but he can’t say exactly when. He just knows it will happen because with fiat currencies, history always repeats. Rubino says, “This sounds crazy now, but they are probably going to happen. That is just how currency collapses play out. We have seen hundreds of currencies in human history that have died. Just Google hyperinflation, and you will see a list of name brand countries that destroyed their currency. They rode them down to virtually zero. It’s hyperinflation, and something like that is coming. . .. We should not even think about it in terms of dollars, just buy it (physical gold and silver) to have real money.”

“:.. akin to a Monty Python skit that’s missing the part where a guy comes out and slaps them in the face with a big fish.”

• With Strait Open, Kier Starmer Makes Effort to Remain Relevant (CTH)

British Prime Minister Kier Starmer, French President Emmanuel Macron, Italian Prime Minister Giorgia Meloni and German Chancellor Friedrich Merz issue a joint statement on their plan to open the Strait of Hormuz, after President Trump secured and opened the Strait of Hormuz.Read more …

Essentially, after holding an international teleconference, leaders from the U.K, France, Italy and Germany gather to express their importance on an issue that has been entirely resolved without them. The result is akin to a Monty Python skit that’s missing the part where a guy comes out and slaps them in the face with a big fish.

They play hard to get: juat move them around. Whack a mole. “… It is completely healthy and normal to change members of legal teams.”

• Miami Prosecutor Moved from Brennan Conspiracy Investigation (CTH)

According to multiple media reports Maria Medetis Long has moved away from the investigative case surrounding John Brennan.CNN was the first to report the move, and the anonymous sourcing indicates the information likely comes from notification sent by the prosecuting attorney to the witnesses and targets of the Florida-based grand jury.

Via CNN-The Justice Department has removed the career Miami federal prosecutor leading the investigation into John Brennan, after she resisted pressure to quickly bring charges against the former CIA director and prominent critic of President Donald Trump, according to people briefed on the matter. Maria Medetis Long on Friday notified attorneys representing people involved in the case that she was no longer handling the investigation, the people familiar with the matter said. She has led the politically sensitive probe for months amid demands from Trump to prosecute Brennan and other critics. The investigation into Brennan is focused on one of the president’s longest standing political grievances t�h�e� �2�0�1�7� �i�n�t�e�l�l�i�g�e�n�c�e� �a�s�s�e�s�s�m�e�n�t� �t�h�a�t� �f�o�u�n�d� � R�u�s�s�i�a� �i�n�t�e�r�f�e�r�e�d� �i�n� �t�h�e� �2�0�1�6� �p�r�e�s�i�d�e�n�t�i�a�l� �e�l�e�c�t�i�o�n� �t�o� �h�e�l�p� �h�i�m�.� �(�r�e�a�d� �m�o�r�e�)� � �T�h�e� �f�r�a�u�d�u�l�e�n�t� �a�n�d� �p�o�l�i�t�i�c�a�l�l�y� �m�a�n�i�p�u�l�a�t�e�d� �I�n�t�e�l�l�i�g�e�n�c�e� �C�o�m�m�u�n�i�t�y� �A�s�s�e�s�s�m�e�n�t� �t�o�u�c�h�e�s� �o�n� �t�h�e� �C�i�a�r�a�m�e�l�l�a� �i�n�f�o�r�m�a�t�i�o�n� �r�e�c�e�n�t�l�y� �r�e�l�e�a�s�e�d�.� � �C�i�a�r�a�m�e�l�l�a� �p�a�r�t�i�c�i�p�a�t�e�d� �i�n� �b�o�t�h� �t�h�e� �c�o�n�s�t�r�u�c�t� �o�f� �t�h�e� �I�C�A� �i�n� �e�a�r�l�y� �2�0�1�7� �a�n�d� �t�h�e�n� �b�e�c�a�m�e� �t�h�e� �a�n�o�n�y�m�o�u�s� �C�I�A� �w�h�i�s�t�l�e�b�l�o�w�e�r� �i�n� �2�0�1�9�.� T�h�e�r�e� �i�s� �n�o� �i�n�d�i�c�a�t�i�o�n� �t�h�e� �m�o�v�e� �o�f� �M�a�r�i�a� �M�e�d�e�t�i�s� �L�o�n�g� �i�s� �r�e�l�a�t�e�d� �t�o� �t�h�e� �r�e�c�e�n�t� �d�i�s�c�o�v�e�r�i�e�s�;� �h�o�w�e�v�e�r�,� �t�h�e�r�e� �i�s� �a� �c�e�r�t�a�i�n� �c�o�n�t�i�n�u�i�t�y� �o�f� �c�o�n�s�p�i�r�a�c�y� �n�o�t�e�d� �i�n� �t�h�e� �t�i�m�e�l�i�n�e� �t�h�a�t� �c�o�n�n�e�c�t�s� �C�I�A� �D�i�r�e�c�t�o�r� �J�o�h�n� �B�r�e�n�n�a�n� �a�n�d� �C�I�A� �A�n�a�l�y�s�t� �E�r�i�c� �C�i�a�r�a�m�e�l�l�a�.� We shall wait to see what else surfaces.

(ABC) – Asked about the move, a Justice Department spokesperson said, “as a matter of routine practice, attorneys are moved around on cases so offices can most effectively allocate resources. It is completely healthy and normal to change members of legal teams.” (more)

Again: never happened before. But it seems more likely by the day now.

Congress can do it (too)?

• Judiciary Chair Confirms House Moving To Expunge Trump Impeachment (JTN)

Rep. Jim Jordan, R-Ohio, Chairman of the House Committee on the Judiciary, has disclosed to Just The News that the House of Representatives, where President Donald Trump was impeached during his first term over a phone call with Ukrainian President Volodymyr Zelensky, is moving to expunge that impeachment from the congressional record. “You need a majority vote, we need a bill, and it’s actually something we’re looking at,” Jordan told Just The News.Read more …

On Monday, Just The News was first to report on declassified secret memos from the 2019 Ukraine whistle-blower scandal, which revealed that the CIA analyst accuser (identified in media as Eric Ciaramella) admitted having no direct knowledge of Trump’s private comments or communications with Zelenskyy, basing the complaint entirely on hearsay and second- or third-hand accounts. The latest disclosures also document Ciaramella’s potential political bias, including his status as a registered Democrat who worked closely with Vice President Joe Biden on Ukraine policy, including traveling with him and discussing the dismissal of Ukrainian Prosecutor General Yuriy Lutsenko, who was probing Burisma, the corporation that paid Biden’s son Hunter millions of dollars.Hiding facts from Congress, and the public

The memos also reveal Ciaramella’s dislike for Republicans like former Representative Devin Nunes and Kash Patel, and his prior procedural contact with Rep. Adam Schiff’s, D-Calif., staff, which he initially omitted from the official disclosure form before apologizing. A supporting “Witness 2,” an NSC/NSA official and co-author of the controversial 2016 Intelligence Community Assessment (ICA) on Russian election interference, linked to Peter Strzok backed the complaint.This, despite admitting he lacked granular insight, would not have acted on it himself, and was motivated by a “moral and patriotic duty” to help Ciaramella “sleep at night.” The concealed evidence of bias and hearsay was kept classified during Trump’s House impeachment in December 2019 and the subsequent Senate trial. On Monday, Harvard Law Professor Emeritus Alan Dershowitz reacted to the idea of expungement and said, “I don’t see any reason why it couldn’t be done. Impeachment is a quasi-judicial procedure, whether you have to go back to Congress and ask them to expunge it or go to the courts.”

Dershowitz: “They violated the Constitution”

The constitutional law expert continued: “But I have to tell you one thing, history will expunge it already because what you’ve done is you’ve created so much doubt about the credibility of the main accuser that it’s hard for anybody to sit back now and say that was a just impeachment. They violated the Constitution.”Several members of the U.S. House of Representatives have introduced simple resolutions to expunge Trump’s two impeachments from the congressional record. In June 2023, during the 118th Congress, former GOP Rep. Marjorie Taylor Greene introduced a resolution for the 2019 impeachment, while New York Rep. Elise Stefanik introduced one for the 2021 impeachment. Former Speaker of the House, Kevin McCarthy, also publicly supported those resolutions.

“Everything that’s wrong is staring us right in the face, and half this country simply will not join us in fighting and fixing it. It’s infuriating and depressing and maddening.” —James Woods on X

• Showdown (James Howard Kunstler)

The closer this Iran war comes to a favorable resolution, the more garishly negative the puling Lefty-left gets, wishing fervently for the enemy to prevail. Why? Because the Lefty-left is also an enemy of our country. They want the operation to fail so they can reclaim power and resume wrecking and looting the USA. By the way, what exactly would a favorable outcome of this war look like? An Iran that doesn’t threaten nuclear jihad and doesn’t sponsor endless terror operations here, there, and everywhere. It looks like we are going to get to that. Iran’s choice is how deep do they want to take their own economic collapse before capitulating? If they’ll just stop now, they’ll still keep the lights on. They can be a normal, modern, developed nation without a death wish.Read more …

Anyway, the paradigm Iran was operating in as a rogue state is dead, especially the malign influence of Britain’s banking and MI6 intel matrix. Britain, proven by its actions to be not a friend of America. . . Britain, a wretched little has-been island empire with bad teeth, overrun by wrathful Islamists, and, alas, soon to be a caliphate. President Donald Trump has rearranged the geopolitical landscape with startling speed and efficacy. Much of Europe, it turns out, are not our friends, either. They would not let us use the NATO bases we pay for to conduct air operations over Iran. Hence, NATO is four dead letters. They can go dangle while they figure out how to live without oil, possibly go back to their centuries-long condition as a nonstop slaughterhouse, besetting each other with stupid, age-old feuds. Not our problem anymore.China? Their Belt-and-Road isn’t what it was just six months ago. Mr. Trump has kicked them out of South America. Their oil supply is suddenly sketchy. Notice, they didn’t lend a hand helping to clear the Strait of Hormuz. Turned out that the radars and air defenses they gifted Iran didn’t work too well. Uncle Xi Pooh Bear will have to re-think situation.

Mr. Trump says he might travel to Pakistan this weekend if there are papers to sign with Iran. Israel and Lebanon announced a ten-day truce to sort out where things stand. Both of them want Hezbollah expelled for good. Anyway, Hezbollah can no longer enjoy financial support from Iran, meaning no more munitions or salaries for Hezbollah warriors, meaning Hezbollah is out of business — a major regional irritant neutralized. Can you dare to imagine a peaceable Middle East?

So, things have changed-up greatly in this long-volatile corner the world, and that will leave Mr. Trump freer to attend to the discord and animus at home, namely the psychopathic Democratic Party’s non-stop demolition of political norms, with assistance from the bureaucratic Deep State and the NGO underworld. Just at hand this week, we have Director of National Intelligence Tulsi Gabbard sending criminal referrals to the DOJ on two key players (both liars) in Trump Impeachment No. 1: former Intel Inspector General Michael Atkinson and CIA agent “whistleblower” Eric Ciaramella — whose name the news media still fears to speak.

That impeachment, over the so-called “Ukraine phone call,” was from start to finish a complete fake, a criminal conspiracy. It involves a much larger cast-of-characters including then House Intel Committee Chair (now senator) Adam Schiff, then Secretary of State Mike Pompeo, CIA Director Gina Haspel, Chief Justice John Roberts, and virtually the whole Kiev US embassy staff at the time. Everybody involved was lying about one thing or another. The case is on Acting AG Todd Blanche’s desk now. Do you suppose it can just sit there?

The Brussels-backed intelligence operation will happen again, Vladimir Palko has warned.

• EU Spied On Orban For Years – Former Slovak Minister (RT)

The EU spy campaign that helped bring down Hungarian Prime Minister Viktor Orban is a lesson to anyone who defies Brussels, former Slovak Interior Minister Vladimir Palko has warned. “What they did to Orban yesterday, they can do to you tomorrow,” he told the outlet ‘Marker’ on Monday. Orban’s Fidesz party suffered a landslide defeat to Peter Magyar’s Tisza on Sunday, with Tisza outperforming even the most one-sided polls to win a 54% to 38% over Fidesz. Magyar’s party now holds 137 of 199 seats in parliament, giving the incoming PM power to rewrite the country’s constitution as he – and his allies in Brussels – see fit.Read more …

That the EU wanted this result was obvious. Orban had been a thorn in Brussels’ side for 16 years and was an insurmountable obstacle to the bloc’s plans to approve a €90 billion loan package for Ukraine. Throughout the election, evidence of interference by the EU, Ukraine, and opposition-friendly Hungarian media trickled out of Budapest. With the election over, the full extent of the EU’s intelligence campaign against Orban – and its implications for populists across Europe – is slowly becoming apparent. “The defeat of Viktor Orban after 16 years of rule is not surprising at all,” Palko told Marker. “However, the tragedy is what happened in the election campaign.”The EU spied on Orban for years

“Orban and his foreign minister were wiretapped by European intelligence for six years,” he continued. “Not Russian, not American. The secret service provided the content of phone calls to some journalists from several EU member states, and the members of the EU establishment used the content against Orban. This was an intervention into Hungarian elections.” Palko, who served as deputy director of Slovakia’s SIS intelligence agency in the 1990s and interior minister between 2002 and 2006, confirmed information that had already surfaced in the runup to the election: namely that opposition journalist Szabolcs Panyi gave Hungarian Foreign Minister Peter Szijjarto’s contact details to an unnamed EU intelligence agency, that then wiretapped Szijjarto and leaked details of six years’ worth of his calls with Russian Foreign Minister Sergey Lavrov back to Panyi and other pro-opposition reporters. Panyi’s outlet, Direkt36, derives 80% of its project costs from the EU.spies also fed the Hungarian and international media stories of Russian “election fixers” attempting to swing the election for Orban, and of plots by Russian military intelligence agents to stage an assassination attempt on Orban for publicity. The claims were unfounded, but were seized upon by Magyar, who worked chants of “Russians, go home!” into his campaign rallies. The EU in turn used these reports to justify the activation of its ‘Rapid Response System’ (RRS): a suite of online censorship tools that allowed Brussels’ “fact checkers” to remove supposed “disinformation” from social media platforms in the runup to the vote. In every election in which it has been activated, the RRS “almost exclusively targeted” right-wing and populist candidates like Orban, the US House Judiciary Committee found in an investigation last year.

“Only one thing is shown from the recorded phone calls: The Hungarians were friendly towards the Russians,” Palko noted. “But this already is a mortal sin for the EU establishment. This is the new European Union that is coming.” The EU’s pre-election attempts to influence the campaign offered a glimpse into a campaign that Orban alleges has been underway ever since he took a stance against Brussels on migration policy and support for Ukraine. However, Europe’s few populist leaders have largely stayed silent on the issue.

The Hungarian election ultimately came down to kitchen-table economic issues. Roads, healthcare, public safety, and public transport were the leading issues among voters in all 19 of Hungary’s counties, and the electorate chose Magyar’s promises of cash injections for underfunded public services over Orban’s geopolitics-heavy platform. Magyar will depend on the EU to fund his economic plan to the tune of €20 billion, and as such will be easily leveraged by Brussels, giving further incentive for the bloc to back his campaign.

Yet the role of EU intelligence in the result has been ignored, even by Orban’s ideological allies on the continent. This, Palko reckons, is a mistake. “All those who were not bothered by it should be warned,” he said. “What they did to Orban yesterday, they can do to you tomorrow.”As RT reported, the EU has rolled out its same censorship playbook in Bulgaria, where elections this weekend pit a veteran center-rightist against a populist, Euroskeptic challenger on the left. Robert Fico in Slovakia, a left-wing populist and vocal opponent of the EU’s Ukraine project, will likely face the same treatment when he seeks another term in office next year.

Sergey Shoigu has cautioned Finland and the Baltic states against allowing Kiev to use their airspace for attacks on Russia

• Russian Security Chief Issues Warning To Four NATO States (RT)

Russia would have the right to retaliate if Finland and the Baltic states are deliberately allowing Ukrainian drones to pass through their airspace, Security Council Secretary Sergey Shoigu said on Thursday. “Recently, there has been an increase in Ukrainian drone strikes against Russia via Finland, Lithuania, Latvia, and Estonia,” Shoigu told journalists. “As a result, civilians are suffering and significant damage is being caused to civilian infrastructure.” Either Western air defenses are proving ineffective, or these four countries “deliberately provide their airspace, thereby becoming open accomplices in aggression against Russia,” he added.Read more …

In the latter case, Moscow has the right to self-defense in response to an “armed attack” under Article 51 of the UN Charter, the security chief stressed. In recent weeks, Kiev has intensified drone strikes on Russia in what Moscow has characterized as “terrorist attacks,” with the Russian military regularly reporting hundreds of UAVs downed in a single night. Late last month, Kiev attacked Russia’s Baltic Sea ports of Ust-Luga and Primorsk with swarms of UAVs. The raids resulted in fires in both cities, which house extensive petrochemical infrastructure.Kremlin aide Nikolay Patrushev said he believed that Finland and the Baltic states were “complicit in these crimes.” The provision of national airspace for Ukrainian drone strikes would “signify direct NATO participation” in attacks on Russia, he said Monday. Multiple Ukrainian drones have also struck the territories of Finland and the three Baltic states since early March. Despite this, all four nations have avoided condemning Kiev outright for violating their airspace.

Moscow has formally warned Lithuania, Latvia and Estonia against allowing Ukraine to send drones via their territory, Russian Foreign Ministry spokeswoman Maria Zakharova said last week. “If the regimes in these countries are smart enough, they will listen. If not, then they will have to deal with the consequences,” she said.

For SCOTUS, Trump is super-prepared.

• Does Trump Know Something We Don’t About Potential SCOTUS Vacancies? (Margolis)

The midterm elections are coming up in November, and Democrats are generally favored to win the House, while the Senate is kind of a coin flip. While it would suck for Democrats to win the House because they’ll almost certainly find some bogus pretext to impeach President Donald Trump, there’s potentially more at stake regarding control of the Senate, including implications for confirming judges and potentially filling any potential Supreme Court vacancies. No retirements have been announced, but speculation is mounting, and I’m starting to wonder if Trump knows vacancies are coming.Read more …

In a recent interview with Fox Business’ Maria Bartiromo, Trump confirmed he has a shortlist of potential nominees ready to go — and he’s prepared to fill as many as three seats if the opportunity arises. “In theory, it’s two — you just read the statistics — it could be two, could be three, could be one,” Trump said. “I don’t know. I’m prepared to do it. But when you mention Alito, he is a great justice.”He added, “He does what’s right for the country. It’s the law, and he goes by it as much as anybody, but he gets to the point.” High praise from a president who has been, let’s say, less enthusiastic about some of his own past nominees. According to Fox News Digital, “Trump’s remarks sharpen the stakes around any potential vacancy, as the president has signaled he is ready to seize the opportunity to deepen the court’s conservative majority. With retirement speculation around Alito and Republicans eyeing the window before the 2026 midterms, the prospect of an opening is already putting fresh focus on succession politics.”

Rumors about Alito, 76, potentially retiring have grown because of his age, his two-decade tenure on the bench and speculation that he may want to make sure a conservative successor is confirmed by the current Republican-led Senate, especially before the upcoming midterm elections in which Republicans are at risk of losing or seeing a diminished majority. The rumors were further fueled when it was revealed Alito was treated last month for dehydration after becoming ill at a Federalist Society dinner. A Supreme Court spokesperson clarified at the time that the justice was “thoroughly checked” and returned to the bench the following Monday.

A source close to Alito insists he is not stepping down this term and is in the process of hiring the rest of his clerks for the next term. So at least for now, it sounds like he’s not going anywhere. Yet, Trump is ready with a shortlist of replacements? Is that a tell that he knows something we don’t? It could be. Or it’s just being prepared. After watching some of his own nominees drift from his expectations on high-profile rulings, you can be certain he’ll be far more deliberate this time around. Whatever seats open up, expect Trump to treat the selection process with a level of scrutiny he may not have applied before.

The bigger picture here is worth appreciating. No president since Ronald Reagan has reshaped the Supreme Court the way Trump has. His first three appointments — Neil Gorsuch, Brett Kavanaugh, and Amy Coney Barrett — built the current 6-3 conservative majority. Trump may have an opportunity to secure a conservative majority for decades to come.= The question is, does he know that he will?

I haven’t been following Tucker’s split from Trump etc. closely.

• Tucker Carlson’s ‘Did He Really Say That?’ Era Is in Full Swing Now (Spencer)

Tucker Carlson, theologian, is at it again, giving rise to a new round of questions about what has happened to the man. The former Fox host and patriotic stalwart is now a full-time agitator against Israel and public relations agent for the religion of Islam, and if any religion ever needed a PR makeover, it’s Islam. In his newsletter on Wednesday, Carlson includes an entry with the curious title “Islam Is the Enemy? Are We Sure About That?” It’s an odd title because there isn’t anyone in either the Trump administration or the Israeli government who is saying, “Islam is the enemy.”Read more …

Certainly, there are people who point out Islam’s 1,400-year war against any and all non-Muslim entities, and its doctrines calling for warfare against and subjugation of unbelievers, which make it unique among what are called “the world’s great religions.” But such people aren’t in the Trump administration, or in the government of Israel, either. Also, up until now, Tucker has focused his ire upon the Netanyahu government, which is supposedly exercising Svengalian control over the Trump administration. Now, despite the fact that the Israeli government has not been critical of Islam, he is defending the religion of suicide bombings, stonings, amputations, and the rest.Referring to the fact that his previous assertion that Muslims love Jesus “set off a firestorm,” Carlson claimed that this was “largely because most Americans do not realize the overlap between Christianity and the Muslim faith.” He insinuates darkly that this is because of some sinister conspiracy: “That is no accident.” Carlson continues by making the preposterous assertion that “the forces supporting the Iran War do not want the public to realize that the Quran hails the Christian savior as a prophet and messenger of the Lord.” The idea that there are forces in America today that are deliberately concealing information that might make Americans think better of Islam than they do now is beyond ridiculous.

The reality, in fact, is exactly the opposite. Ever since George W. Bush stood inside a Washington, D.C. mosque on Sept. 17, 2001, and proclaimed that “Islam is peace” and warned Americans not to harass innocent Muslims (which was not happening in the first place), the political and media establishment has done everything it could to ensure that people didn’t think ill of Islam. The media reflex of saying that a jihadi’s motive was “unclear” when nothing under the living sun could have been clearer has been a running joke for years.

Tucker Carlson, however, would have you believe that supporters of the war against the entity where they regularly scream “Death to America” and “Death to Israel” have deliberately obscured the fact that Jesus appears in the Qur’an as a prophet of Islam. I can adduce my own work to show that this isn’t true. In numerous books, including The Complete Infidel’s Guide to the Koran and The Critical Qur’an, both of which were bestsellers, I’ve discussed the Qur’anic and Islamic view of Jesus in tremendous detail.

It’s not quite as wonderful as Carlson suggests. The Jesus of the Qur’an is an Invasion-of-the-Body-Snatchers version of the Biblical figure: he bears the same name, but is an entirely different personality. Even Carlson grants that the Qur’an’s mentions of Jesus do “not mean that Christianity and Islam are aligned. They definitely are not.” But he insists that “an anti-Muslim propaganda campaign” has “consumed our country for decades. Neocons have brainwashed the U.S. public into thinking Middle Eastern terrorists lust for American blood because they are Muslim. But it is not true. They behave as they do because they are evil criminals.”

Well, all right, Tucker, but they’re evil criminals whose holy book tells them to “kill them wherever you find them” (Qur’an 2:191, 4:89, 4:91), and just to make clear who ought to be killed, adds “kill the polytheists wherever you find them (9:5). In the Qur’anic scheme, pretty much everyone who is not a Muslim is a polytheist. The Qur’an also directs Muslims to fight Jews and Christians until they submit to second-class status under the hegemony of Islamic law (9:29).

Muslims are to fight unbelievers until “religion is all for Allah” (8:39), which is an open-ended declaration of war against all non-Islamic religious expression. Evil criminals they are indeed, but even more evil is the fact that when they plunder, rape, and kill, they think they are offering service to God, as the Biblical Jesus said would happen (John 16:2). The fact that Palestinian terrorist murderers are not considered “evil criminals” in Gaza, but great heroes, should give Tucker Carlson pause. But it won’t.

“4 out of 5 citizens also say they are dissatisfied with Chancellor Friedrich Merz’s government, according to YouGov poll..”

• Germany: Anti-Immigration AfD Party Jumps To 27%, 4 Points Ahead of CDU (RMX)

In a new poll from YouGov, the Alternative for Germany (AfD) party jumped to 27 percent, now four points ahead of the rival Christian Democrats (CDU), in a sign that the AfD continues to distance itself as the most popular party in Germany. AfD co-leader Alice Weidel was quick to publish the poll results on X, writing: “4 percentage points ahead of the Union, 4 out of 5 citizens dissatisfied with Merz: We no longer have time for undemocratic firewalls. The political turnaround must happen now.”Read more …4 Prozentpunkte Abstand zur Union, 4 von 5 Bürgern unzufrieden mit Merz: Wir haben keine Zeit mehr für undemokratische Brandmauern. Die politische Wende muß jetzt erfolgen. pic.twitter.com/rWe3sm04RU

— Alice Weidel (@Alice_Weidel) April 15, 2026

The governing parties that make up the federal government are seeing their fortunes quickly fall. The CDU/CSU fell by three percentage points to 23 percent, which was the lowest figure measured by YouGov since December 2021. The SPD figure is at 13 percent, which fell one point from 14 percent. Meanwhile, the Greens and the Left each gained one point, jumping to 14 percent and 10 percent respectively. According to the poll, more and more Germans are dissatisfied, totaling 79 percent, with the work of the federal government led by Friedrich Merz. In comparison, in June 2025, this value was only at 55 percent.Most threatening for Merz, CDU voters are increasingly turning on his government, with only 34 percent saying they are satisfied, falling from 48 percent in March. Other polls have shown AfD at the top, but with a narrower margin, averaging between 25 and 26 percent of the vote. Despite the AfD leading, the CDU has vowed to never form a coalition with the party. If the AfD’s values hold into the next national election, it may become increasingly difficult to form a coalition without the party’s support.

Democrats think it’s a sure thing they’ll win all upcoming elections. “If the Democrats win the presidency and both houses of Congress ..”

• “F**k It…Just Do It”: Carville’s Plan to Add States and Pack the Court (Turley)

Various Democrats have been openly discussing their plans after retaking power to change the system so they never lose power again. Democratic strategist James Carville has been one of the most vocal and returned to the subject this week in laying out how they will make D.C. and Puerto Rico states and pack the Supreme Court with a liberal majority. On his podcast with Al Hunt, Carville explained, “If the Democrats win the presidency and both houses of Congress, I think on day one, they should make Puerto Rico [and] D.C. a state, and they should expand the Supreme Court to 13. F— it. Eat our dust.”Read more …

Notably, this week, New Jersey just elected a radical new member, Analilia Mejia, who ran on packing the Court and other radical agenda items. While some of us have written about the expansion of the Court, these politicians and pundits are pushing for the packing, not just gradual expanding, of the Court. However, Carville (curiously on a national podcast) seriously suggested that Democrats should keep the plan quiet: “Don’t run on it. Don’t talk about it. Just do it.” Call it the Nike School of Constitutional Law. The need of the left to pack the Supreme Court is obvious. Many of the proposals coming from the left are clearly unconstitutional.You will need a partisan majority to make the political changes that these figures hope will give the Democrats a lock on power for years to come. Years ago, Harvard professor Michael Klarman laid out a radical agenda to change the system to guarantee Republicans “will never win another election.” However, he warned that “the Supreme Court could strike down everything I just described.” Therefore, the court must be packed in advance to allow these changes to occur. Likewise, Carville previously explained how this process of how the pack-to-power plan would work:

“I’m going to tell you what’s going to happen. A Democrat is going to be elected in 2028. You know that. I know that. The Democratic president is going to announce a special transition advisory committee on the reform of the Supreme Court. They’re going to recommend that the number of Supreme Court justices go from nine to 13. That’s going to happen, people.” The push for court packing and war chests on the left remains unchanged despite conservatives on the Court ruling against the Administration on major cases. Carville and others cannot claim that the conservative justices are robotically voting with the Administration, but it does not matter. They want a Court that will consistently uphold the changes being planned by Democratic strategists.

The fact that these changes would come after the 250th anniversary of the most successful democratic system in history is a crushing irony. However, it is notable that the Democrats want Congress and the courts to push through these changes, not the public. The public remains opposed to court packing and making D.C. a state. That is why Carville wants candidates to keep quiet on the plan and run, like Virginia’s Abigail Spanberger, as faux moderates. Then, as in Virginia, they can move to fundamentally change districts and rules to guarantee their hold on power. It is a mentality summed up by NEA President Becky Pringle:

Hard times in the art markets. Dad is AWOL.

• “Mr. Biden Lives Abroad”: Hunter Leaves Country (Turley)

“Mr. Biden lives abroad.” Those four words in a filing from Barry Coburn confirmed what had long been rumored about his client: Hunter Biden has left the country as his former lawyers and creditors seek millions in unpaid debts. He added, “He cannot pay his current lawyers.” As I wrote about years ago, Biden’s art grift would dry up as soon as he could no longer deliver influence and access to power. Reportedly unable to move art, Hunter has moved out of the reach of many creditors. He is rumored to be in South Africa, where his wife, Melissa Cohen, was born and raised.Read more …

Hunter is the Blanche DuBois of American politics. He has always relied on the kindness (and greed) of strangers when he could allegedly offer influence or access to his father, Joe Biden. Hunter told a South African podcast in November that “We’re trying to be between Cape Town and the States, go back and forth.” He added, “I’ve fallen madly in love with Cape Town. You guys do not know how good you have it here. It’s the most beautiful city in the world.” It just also happens to be roughly 9000 miles away from creditors in Delaware.According to his former counsel at Winston & Strawn LLP, Hunter has not paid a “substantial portion” of the fees owed to his legal team. Hunter told the podcast that he is facing “$17 million in debt … as it relates to my legal fees.” His criminal defense did not ultimately protect him. He was found guilty of a variety of crimes, and his father then broke his repeated promise to the public and pardoned his own son in December 2024. I have been a long-time critic of the Bidens, going back to when Joe Biden was still a senator. The family was long accused of influence peddling and corruption. Hunter Biden was hardly subtle in marketing his access and influence. He is now without a law license and any known means of support despite an enabling media that pushed his past books and art.

For those of us who have written about the Bidens for decades, the relocation to South Africa is about as surprising as having his father pop into dinners at Cafe Milano with foreign clients. Hunter Biden is the Enfant terrible created by his father and released upon the world.

I recently wrote that the Swalwell scandal reveals an ironic analogy to Hunter’s signature lifestyle. Swalwell supported Hunter and was by his side as he defied a congressional subpoena. Like Hunter, he has controversial dealings, including using tens of thousands of campaign contributions for child care. He even had the campaign support of Hunter’s “sugar brother” Kevin Morris, who appears to have a proclivity for narcissistic, self-destructive personalities. Swalwell could also face the same financial crunch as Hunter, as his campaign and congressional money run out. If so, there is always South Africa.

Take this very seriously.

Elon Musk: “This is going to sound pretty crazy. I’d say the economy is ten times its current size in ten years

— Mars University (@MarsUniversityX) April 17, 2026

Greater than 10x in roughly ten years is actually a fairly comfortable prediction

Obviously, if there’s World War III or something, that could put a kink in those… pic.twitter.com/puG9NeIU2S

Universal HIGH INCOME via checks issued by the Federal government is the best way to deal with unemployment caused by AI.

— Elon Musk (@elonmusk) April 17, 2026

AI/robotics will produce goods & services far in excess of the increase in the money supply, so there will not be inflation.

Elon Musk just weaponized gravity.

— Dustin (@r0ck3t23) April 17, 2026

The entire trucking industry has a physics leak bleeding billions.

Musk just sealed it.

Most people look at the Tesla Semi and see a cleaner diesel. A truck that swapped a gas tank for a battery.

That is a complete misread of the physics.… pic.twitter.com/QAlAYz27ay

BREAKING: President Trump vows to look into the 10 scientists who have gone missing or turned up dead:

— Fox News (@FoxNews) April 16, 2026

"I hope it's random, but we're going to know in the next week and a half."

"I just left a meeting on that subject."

"Pretty serious stuff… Some of them were very important… pic.twitter.com/VMgeZyayXl

HUNGARIAN 5D CHESS THAT MAKES BRUSSELS CRY!

— Paul White Gold Eagle (@PaulGoldEagle) April 16, 2026

According to information provided by Serbian intelligence sources, the real objective of Orbán's "defeat" is to allow him to become the Trojan horse that Donald Trump wants to place at the heart of the European Union.

The American… pic.twitter.com/u2ZxwZrykT

A single bird has completed a journey covering nearly one-third of Earth’s circumference, without stopping to eat, drink, or rest.

— Science girl (@sciencegirl) April 16, 2026

A five-month-old Bar-tailed Godwit, set a new record for the longest nonstop flight ever documented in a bird. It traveled from Alaska to Tasmania,… pic.twitter.com/jera80hl6Q

Imagine being able to make marble look like water.

— James Lucas (@JamesLucasIT) April 16, 2026

In 1858, an Italian sculptor did exactly that.

And no one has done it since…

He was commissioned to carve a naiad — a water nymph — for the baths of a palazzo in Brescia, Italy. In Greek mythology, Naiads were the living… pic.twitter.com/T2rkREhtNd

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.