NPC Hendrick Motor Co., Carroll Avenue, Takoma Park, Maryland 1928

70% minimum (90%?!) of which is entirely virtual.

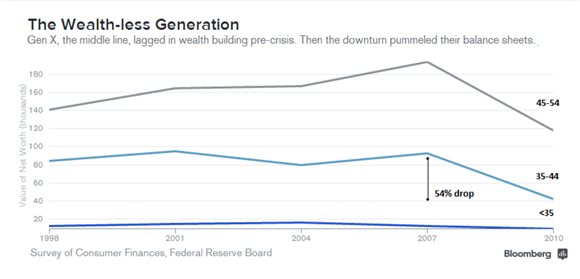

• Rising Stocks, Homes Boost US Household Wealth To Record $83 Trillion (AP)

Fueled by higher stock and home values, Americans’ net worth reached a record high in the final three months of 2014. Household wealth rose 1.9% during the October-December quarter to nearly $83 trillion, the Federal Reserve said Thursday. Stock and mutual fund portfolios gained $742 billion, while the value of Americans’ homes rose $356 billion. The typical household didn’t benefit much, though. Most of the wealth remains concentrated among richer families. The wealthiest 10% of U.S. households own about 80% of stocks. Still, greater wealth could help lift spending and economic growth. Higher stock and home values can make people feel more financially secure and more willing to spend, and consumer spending fuels about 70% of the economy.

The Fed’s figures aren’t adjusted for population growth or inflation. Household wealth, or net worth, reflects the value of homes, stocks and other assets minus mortgages, credit cards and other debts U.S. corporations are also seeing sharp improvements in their finances, the Fed report showed. Businesses amassed $2 trillion in cash by the end of last year— a record high — up from less than $1.9 trillion three months earlier. Cash-rich corporations could spend more on investments in machinery, computers and other equipment. That would make workers more productive and accelerate economic growth. They could also use some of their cash to raise pay at a time when many employees have been stuck with stagnant wages.

Some economists have criticized publicly traded companies for spending heavily on repurchasing their own shares, which boosts profits and serves shareholders rather than employees. Businesses are also taking advantage of low interest rates by taking on more debt, which typically signals confidence in the economy and future growth. Business debt rose 7.2% in the fourth quarter, the sharpest quarterly increase in more than six years. During the Great Recession, which officially ended in June 2009, Americans’ net worth plummeted as stock and home values sank. Household wealth tumbled to $55 trillion in the first quarter of 2009 from a pre-recession peak of $67.9 trillion. Wealth didn’t surpass that peak until the third quarter of 2012.

Once you get to 124, may be some will wake up.

• Rate Cuts: 24 Countries So Far And There’s More To Come (CNBC)

An interest rate cut from South Korea Thursday takes the number of central banks that have stepped up their monetary easing this year to 24 and that number is likely to rise, analysts say. South Korea’s decision to cut its key rate by 25 basis points to a record low of 1.75% follows a rate cut by Thailand’s central bank on Wednesday and easing by central banks in China, India and Poland since March began. Russia and Malaysia are among the countries that economists say could join the growing list of central banks that have slashed borrowing costs since the start of the year. The main reason for such a flurry of action, they add, is a backdrop of falling or low inflation which is highlighting the need to boost lackluster economic growth.

“I find it interesting that people say that these [rate cuts] are surprises and we heard that when it happened in Australia, when it happened in India, Indonesia and today in Korea,” Joshua Crabb, head of Asian Equities at Old Mutual Global Investors, told CNBC Asia’s “Squawk Box.” “But if we look at inflation, it is coming down dramatically, real rates are high and the economy is weak so it makes a lot of sense that we see these cuts and we will see that continue to happen,” he said. Thanks in part to the sharp fall in oil prices since last June, many economies are facing falling or low inflation rates.

Data on Thursday for instance, showed Spain’s consumer price index rose to 0.2% in February from -1.6% the month before. In Indonesia, annual inflation stood at 6.29% last month, down from 6.96 in January. “Fundamentally, the easing around the world is driven by inflation turning out lower across the board,” Anatoli Annenkov, senior European economist at Societe General, told CNBC. “There is a debate about currency wars, monetary easing to push currencies lower, but fundamentally this is a story about growth and inflation,” he added.

More rate cuts.

• Watch Out: China Could Join The Currency War

Central banks may be spreading deflation by easing monetary policy and weakening their currencies, but the biggest threat is that China will wade into the battlefield, analysts say. “The three trillion dollar question is whether the People’s Bank of China (PBoC) will allow the yuan to depreciate and export their own disinflation to the rest of the world, setting off a series of competitive devaluations in the region,” Nicholas Ferres, investment director at Eastspring Investment said in a note on Friday. Twenty-four central banks have eased monetary policy this year amid slowing economic growth and deflationary pressure as oil prices hover near six-year lows. In February, the PBoC cut the one-year deposit rate by 25 basis points to 5.35%.

For now Chinese authorities continue to keep the yuan in a tight daily trading band against the U.S. dollar; the yuan has lost just 0.9% against the dollar year to date. By contrast, the dollar is up 3.3% again the Korean won and 4.2% against the Singapore dollar. But the euro’s around 12% decline against the greenback so far this year “will likely put more pressure on China to devalue the yuan… [which would] signal that China is joining the currency war,” Bank of America Merrill Lynch and Rates strategist David Woo said in a note published on Monday. “[This is] the biggest tail risk of 2015,” he said.

“Morse and his team of analysts at Citigroup have predicted that sometime this spring, as tanks reach their limits, oil prices will again nosedive, potentially all the way to $20 a barrel.”

• The U.S. Has Too Much Oil and Nowhere to Put It (Bloomberg)

Seven months ago the giant tanks in Cushing, Okla., the largest crude oil storage hub in North America, were three-quarters empty. After spending the last few years brimming with light, sweet crude unlocked by the shale drilling revolution, the tanks held just less than 18 million barrels by late July, down from a high of 52 million in early 2013. New pipelines to refineries along the Gulf Coast had drained Cushing of more than 30 million barrels in less than a year. As quickly as it emptied out, Cushing has filled back up again. Since October, the amount of oil stored there has almost tripled, to more than 51 million barrels. As oil prices have crashed, from more than $100 a barrel last summer to below $50 now, big trading companies are storing their crude in hopes of selling it for higher prices down the road.

With U.S. production continuing to expand, that’s led to the fastest increase in U.S. oil inventories on record. For most of this year, the U.S. has added almost 1 million barrels a day to its stash of crude supplies. As of March 11, nationwide stocks were at 449 million barrels, by far the most ever. Not only are the tanks at Cushing filling up, so are those across much of the U.S. Facilities in the Midwest are about 70% full, while the East Coast is at about 85% capacity. This has some analysts beginning to wonder if the U.S. has enough room to store all its oil. Ed Morse, the global head of commodities research at Citigroup, raised that concern on Feb. 23 at an oil symposium hosted by the Council on Foreign Relations in New York. “The fact of the matter is, we’re running out of storage capacity in the U.S.,” he said.

If oil supplies do overwhelm the ability to store them, the U.S. will likely cut back on imports and finally slow down the pace of its own production, since there won’t be anywhere to put excess supply. Prices could also fall, perhaps by a lot. Morse and his team of analysts at Citigroup have predicted that sometime this spring, as tanks reach their limits, oil prices will again nosedive, potentially all the way to $20 a barrel. With no place to store crude, producers and trading companies would likely have to sell their oil to refineries at discounted prices, which could finally persuade producers to stop pumping. If oil supplies do overwhelm the ability to store them, the U.S. will likely cut back on imports and finally slow down the pace of its own production, since there won’t be anywhere to put excess supply. Prices could also fall, perhaps by a lot. Morse and his team of analysts at Citigroup have predicted that sometime this spring, as tanks reach their limits, oil prices will again nosedive, potentially all the way to $20 a barrel.

“.. the largest producer in North Dakota’s Bakken shale basin put itself up for sale..”

• Get Ready for Oil Deals: Shale Is Going on Sale (Bloomberg)

A decision by Whiting Petroleum, the largest producer in North Dakota’s Bakken shale basin, to put itself up for sale looks to be the first tremor in a potential wave of consolidation as $50-a-barrel prices undercut companies with heavy debt and high costs. For the first time since wildcatters such as Harold Hamm of Continental began extracting significant amounts of oil from shale formations, acquisition prospects from Texas to the Great Plains are looking less expensive. Buyers are ultimately after reserves, the amount of oil a company has in the ground based on its drilling acreage. The value of about 75 shale-focused U.S. producers based on their reserves fell by a median of 25% by the end of 2014 compared to 2013, according to data compiled by Bloomberg.

That’s opening up new opportunities for bigger companies with a better handle on their debt, said William Arnold, a former executive at Shell. “In this market, there are whales and there are fishes, and the whales are well armed,” said Arnold, who also worked as an energy-industry banker and now teaches at Rice University in Houston. “There are some very vulnerable little fishes out there trying to survive any way they can.” Smaller producers with significant debt that depend on higher prices to make money are the most likely early targets for buyers such as Exxon Mobil or Chevron, companies that have bided their time for years as the value of some shale fields soared to $38,000 an acre from $450 just a few years earlier.

The market crash is creating “a consolidation game,” Concho CEO Timothy Leach said on a Feb. 26 call with investors. “It’s harder to be a small company today than it has been in the past.” In the pre-plunge days, acquisitions were dominated by foreign buyers overpaying to get a seat at the shale boom table. That buying frenzy was followed by an explosion in asset sales as companies pieced together their ideal drilling portfolios. Joint ventures were a popular way of funding what seemed like an unstoppable drilling machine.

Europe now exists to protect us from democracy…

• Daniel Hannan Explains How Democracy Died In Europe (Zero Hedge)

With Greece on the edge of being kicked out of the Eurozone , either voluntarily or otherwise, with an anti-austerity party on the verge of taking over the reins of power in Spain, with Beppe Grillo waiting in the corridors for his chance to pounce in Italy and with Marine le Pen and her nationalist party on the verge of becoming the biggest shocker of Europe over the coming years, here, according to Daniel Hannan, is what killed democracy in Europe. Europe itself. Here are the punchlines, which are all based documented fact:

We were told the Euro would be an antidote to extremism, that it would make countries get on better, and make moderate politics more mainstream. Well, how’s that working out for you. Look at the elections in Greece – a Trotskyist party came first, a Nazi party came third. And as for the national animosities read the way the German newspaper now refer to the Greeks and vice versa. Would you say this is soothing or stoking national rivalries in Europe?

But worst of all is the impact on democratic accountability. After the Greek election results came in, the German finance minister said “elections change nothing.” He was talking specifically about Greece but this could be a watchword describing the entire Brussels racket. As Jean Claude Juncker put it the next day, “there can be no democratic choice against the European treaties.” This is the same European Commission that in late 2011 in Italy and Greece engaged in practice in civilian coups, toppling elected prime ministers and replacing them with former technocrats.

As the former president of the European Commission Barroso puts it, “democratic governments are often wrong. If you trust them too much they make bad decisions.” And so we have this syste,min Europe where power is deliberately vested in the hands of people who are invulnerable to public opinion. Being against that shouldn’t make you anti-Europe, it doesn’t make you Euroskeptic, it makes you pro-democracy. What a tragedy that in the country where democracy was born, in the part of the world that evolved this sublime idea, that our rulers should be accountable to the rest of us, in that same country that wonderful idea that laws should not be passed nor taxes raised except by our own representatives, has been abandoned.” Tragedy indeed, and while nobody else is willing to admit it, only a violent overthrow of this unelected group of self-serving oligarchs is the only probably outcome.

Ha!

• Draghi Makes Greenspan Look Like A Rank Amateur (Albert Edwards via ZH)

We have long fulminated against strategists who are unwilling to predict sharp market moves. The violent downmove in the euro over the last few weeks is a case in point. Mario Draghi and the ECB’s manipulation of asset prices makes Greenspan’s Fed look like a rank amateur. More shocking though than the plunge in the euro, and more shocking even that 25% of sovereign eurozone bonds now trade in negative territory, is what has happened to eurozone equity valuations. For, as we approach the sixth anniversary of the US cyclical bull market (a post-war record), the PE expansion of eurozone equities is simply off the scale. History suggests this will end very badly indeed. Ask Alan!

I promise to keep insulting you…

• Tsipras Promises Greece Will Keep Its Word Amid German Spat (Reuters)

Prime Minister Alexis Tsipras tried to reassure euro zone partners on Thursday that Greece would stick to an extended bailout agreement with its international creditors even as a war of words rumbled on between Athens and Berlin. Tsipras used a visit to the Paris-based Organization for Economic Cooperation and Development, an inter-governmental think-tank, to make his case for a long-term restructuring of Greece’s debt while promising to implement agreed reforms. “There is no reason for concern… even if there is no timely disbursement of a (loan) tranche, Greece will meet its obligations,” he told reporters.

“We are here in order for the OECD to put its stamp on the reforms that the Greek government wants to push on with and I believe that this stamp in our passport will be very significant to build mutual trust with our lenders.” His soothing words contrasted to the tone of recrimination between Greece and Germany over austerity, relations between their finance ministers and demands for reparations over the World War Two Nazi occupation of Greece. Greece submitted a formal protest to the German Foreign Ministry, accusing Finance Minister Wolfgang Schaeuble of having insulted his Greek counterpart, Yanis Varoufakis, further eroding a relationship that has been strained by Berlin’s tough stance on the Greek debt crisis.

Schaeuble denied having called Varoufakis “foolishly naive”, as reported by some Greek media, telling Reuters it was “nonsense” to say he had insulted the Greek minister. Greek Foreign Ministry spokesman Constantinos Koutras told Reuters the complaint was about the general tone of Schaeuble’s remarks, questioning data presented by Greece and doubting its willingness to meet its commitments. Recounting a private meeting with Varoufakis this week, Schaeuble told reporters on Tuesday in Brussels: “He said to me ‘The media are dreadful’. So I said: ‘Yes but the first impression you made on us was that you were stronger at communication that on substance. That may have been a mistake’.”

One for the bleachers.

• Greece Complains About Schaeuble in Deepening Conflict (Bloomberg)

Greece’s war of words with Germany deepened as Greece renewed demands for war reparations and formally complained about Finance Minister Wolfgang Schaeuble. Germany and Greece confirmed Thursday that the Greek ambassador in Berlin made an official protest late Tuesday to the German Foreign Ministry over comments made by Schaeuble. Schaeuble and his Greek counterpart Yanis Varoufakis have traded barbs in recent weeks, with Schaeuble suggesting on Tuesday that Varoufakis needed to look more closely at an agreement Greece signed in February and commenting on his fellow minister’s communication strategy. Schaeuble said Thursday that any suggestion he had insulted Varoufakis was “absurd.”

Tensions have risen between Greece and Germany since the election of Prime Minister Alexis Tsipras on Jan. 25 on a platform on ending the austerity his Syriza party blames Chancellor Angela Merkel for pushing. Germany is the biggest country contributor to Greece’s €240 billion twin bailouts and the chief proponent of budget cuts and reforms measures in return. The latest spat centers on Tuesday’s press conference in Brussels, when Schaeuble referred to a Feb. 20 declaration that Varoufakis had signed, saying that “he just has to read it. I’m willing to lend him my copy if need be.” He also said he talked with Varoufakis about the latter’s treatment at the hands of the media, saying that he had told his Greek counterpart: “In terms of communication, you made a stronger impression on us than in substance. But that may well have been a false impression. That he should suddenly be naive in terms of communication, I told him, that is quite new to me. But you live and learn.”

According to Deutsche Presse-Agentur, Schaeuble was cited in some Greek media as calling Varoufakis “foolishly naive” in his handling of the press. Greek Foreign Ministry spokesman Konstantinos Koutras rejected suggestions that the government’s complaint had been based on a “wrong translation” of Schaeuble’s remarks. “On the contrary, the reason for this complaint to the government of a friend, counterpart and ally country was based on the essence of what Mr. Schaeuble said,” Koutras said in an e-mail.

Hand out.

• ECB Increases Greek ELA Ceiling by €600 Million (Bloomberg)

The European Central Bank increased the maximum Emergency Liquidity Assistance that Greek banks can get from their national central bank by €600 million, according to two people familiar with the decision. The amount matches the request by the Greek central bank, said the people, who asked not to be named because the talks are private. The ECB’s Governing Council held a phone conference on Thursday to set the limit, which policy makers had increased by €500 million to €68.8 billion on March 5. The council is scheduled to review the level again on March 18.

“The ECB is saying you better reach an agreement and you better do as you’re told, or else,” said Gabriel Sterne, head of global macro research at Oxford Economics. “This is an extraordinarily small extension. It seems to say: we’re just going to drip feed you liquidity, no more, no less, just exactly what you need and no breathing space.” Greek banks didn’t absorb all ELA funds available under the previous ceiling and have about €3.5 billion in liquidity left, said a Bank of Greece official, who asked not to be named because the matter is private.

The ECB is reviewing ELA weekly, reflecting concern that banks will use it to finance the Greek government and so violate European Union law. The newly elected administration in Athens is struggling to gain access to aid payments as a cash crunch looms before the end of the month. “Where the government is unable to tap the market and where banks are unable to tap the market, in my view there are concerns about monetary financing if ELA is used to purchase treasury bills or to roll over treasury bills,” Bundesbank President Jens Weidmann said in a Bloomberg Television interview in Frankfurt after the decision.

Funny.

• Central Bank Stimulus Is Ancient Recipe for Trouble (Bloomberg)

Central bankers would do well to learn lessons about monetary stimulus from history – ancient history. The practice of governments boosting the amount of money in circulation to spur economic growth isn’t as unconventional as one might think, according to Kabir Sehgal’s new book, “Coined: The Rich Life of Money and How Its History Has Shaped Us.” In it, the 32-year-old former equities salesman at JPMorgan looks at the economics, history and psychology of currencies and the role they play in life. “You need paper money to engender short-term riches to get us out of a crisis, but what ends up happening is it’s hard to keep that in check,” Sehgal said in an interview.

“Currencies devalue, there’s inflation. Then there’s a monetary crisis which leads to an economic crisis.” After carrying out unprecedented stimulus in the wake of the financial crisis, the U.S. Federal Reserve now stands out among major central banks in accepting a higher exchange rate as a sign of economic strength. Peers from Tokyo to Frankfurt, Zurich and Sydney are cutting rates and buying government bonds to stimulate growth and, in the process, sometimes weakening their currencies Rulers have used the supply of hard and paper money to pursue economic and political goals as early as the Roman Empire and in Kublai Khan’s 13th-century Mongol Empire, according to Sehgal.

In the U.S., Benjamin Franklin and Abraham Lincoln advocated printing more paper currency to spur trade and commerce. “The lesson that keeps coming up is really a Faustian bargain,” he said. “It seems great, but eventually it leads to economic trouble.” Sehgal, also a Grammy-award winning jazz producer, left his position as a vice president for emerging-market equities at JPMorgan this week.

“Now is the time to give a message of hope to the Greek people, not only implement, implement, implement and obligations, obligations, obligations..”

• Tsipras Says Greece Doing Its Part In Eurozone Deal (Reuters)

Greece’s problems are euro zone’s problems and the single currency area should send Greece a message of solidarity as Athens stands ready to deliver on promises to reform in exchange for more loans, Greek Prime Minister Alexis Tsipras said. “Greece has already started fulfilling its commitments mentioned in the Eurogroup decision of 20 Feb so we are doing our part and we expect our partners to do their own,” Tsipras told reporters after meeting the speaker of the European Parliament Martin Schulz. “And I’m very optimistic … that we will find a solution because I strongly believe that this is our common interest. I believe that there is no Greek problem, there is a European problem,” he said. Eurozone finance ministers agreed on Feb 20 to extend Greece’s financial rescue by four months, averting a potential cash crunch in March that could have forced the country out of the currency area.

But the extension was granted to give Athens time to negotiate a list of reforms by the end of April that would unblock further aid to the country, whose leftist-led government pledged to reverse austerity. Tsipras, who was also meeting European Commission President Jean-Claude Juncker on Friday, called for a change in the message the euro zone was sending Greece. “Now is the time to give a message of hope to the Greek people, not only implement, implement, implement and obligations, obligations, obligations,” he said. “The message that the European institutions will give help and solidarity with particular rates, in order to over come this very bad situation at the social level,” he said referring to the unemployment rate at 26%.

Primary dealers, you can tickle them but….

• Why The Fed Failed Two Of Europe’s Biggest Banks (CNBC)

The U.S. operations of Germany’s and Spain’s largest banks had their knuckles rapped by the U.S. Federal Reserve late Wednesday. The Fed failed Deutsche Bank and Santander in key tests of their ability to withstand a future financial crisis. But what exactly have they done wrong? After all, they are two of Europe’s most prestigious and largest banks which passed the European Central Bank’s October stress tests comfortably. To start with, the Fed is anxious about having to support the U.S. operations of non-U.S. banks in the event of a future economic crisis, so it is subjecting them to tough scrutiny. While both banks were judged to have enough capital to pass the Fed’s minimum capital requirements, “widespread and substantial weaknesses across their capital planning processes” were identified by the central bank.

Essentially, the banks have not failed in terms of their capital position, but in the quality of their analysis of risk. Some investors argue that this is not much to worry about. This is the second year in a row Santander has failed the tests, while Deutsche’s U.S. unit failed them the first year it took them. However, It was the first time all of the U.S. domestic banks passed the stress tests since they began in 2009. “The European banks have only failed at the margins,” Dennis Gartman, the influential investor and author of the “Gartman Letter”, who dismissed the tests as “borderline silly”, told CNBC Thursday. “I’m not that concerned, nor do I think anyone else should be.

In the case of the stress tests, we know when they will be administered and what questions they have to answer – the fact that anyone will have failed is beyond belief.” Until the U.S. divisions of Deutsche Bank and Santander come up with new capital plans, the Fed has barred them from raising dividends or making stock buybacks. This is not likely to derail any plans for shareholder rewards this year – Deutsche Bank said it didn’t request any dividend payments anyway, and Santander has permission to keep a dividend payout announced earlier this year.

Not a great Whitney fan necessarily, but he’s got this one quote right.

• How Putin Blocked the US Pivot to Asia (Whitney)

On February 10, 2007, Vladimir Putin delivered a speech at the 43rd Munich Security Conference that created a rift between Washington and Moscow that has only deepened over time. The Russian President’s blistering hour-long critique of US foreign policy provided a rational, point-by-point indictment of US interventions around the world and their devastating effect on global security. Putin probably didn’t realize the impact his candid observations would have on the assembly in Munich or the reaction of powerbrokers in the US who saw the presentation as a turning point in US-Russian relations. But, the fact is, Washington’s hostility towards Russia can be traced back to this particular incident, a speech in which Putin publicly committed himself to a multipolar global system, thus, repudiating the NWO pretensions of US elites. Here’s what he said:

“I am convinced that we have reached that decisive moment when we must seriously think about the architecture of global security. And we must proceed by searching for a reasonable balance between the interests of all participants in the international dialogue.”

With that one formulation, Putin rejected the United States assumed role as the world’s only superpower and steward of global security, a privileged position which Washington feels it earned by prevailing in the Cold War and which entitles the US to unilaterally intervene whenever it sees fit. Putin’s announcement ended years of bickering and deliberation among think tank analysts as to whether Russia could be integrated into the US-led system or not. Now they knew that Putin would never dance to Washington’s tune. In the early years of his presidency, it was believed that Putin would learn to comply with western demands and accept a subordinate role in the Washington-centric system. But it hasn’t worked out that way. The speech in Munich merely underscored what many US hawks and Cold Warriors had been saying from the beginning, that Putin would not relinquish Russian sovereignty without a fight.

The declaration challenging US aspirations to rule the world, left no doubt that Putin was going to be a problem that had to be dealt with by any means necessary including harsh economic sanctions, a State Department-led coup in neighboring Ukraine, a conspiracy to crash oil prices, a speculative attack of the ruble, a proxy war in the Donbass using neo-Nazis as the empire’s shock troops, and myriad false flag operations used to discredit Putin personally while driving a wedge between Moscow and its primary business partners in Europe. Now the Pentagon is planning to send 600 paratroopers to Ukraine ostensibly to “train the Ukrainian National Guard”, a serious escalation that violates the spirit of Minsk 2 and which calls for a proportionate response from the Kremlin. Bottom line: The US is using all the weapons in its arsenal to prosecute its war on Putin.

By all means, let’s keep talking, but please not on the basis of baseless accusations..

• ‘Claims SU-25 Shot Down MH17 Unsupportable’ (RT)

Electronic countermeasure pods are no longer reliable source of information, so anyone who says the radar has identified a SU-25 aircraft in the MH17 tragedy is trying to mislead people, Gordon Duff, senior editor of Veterans Today newspaper, told RT.

RT: Though the preliminary results of the investigation into the crash of Malaysian Airlines flight MH17 over Ukraine won’t be known until July new theories of what happened appear every day. One claim is that the Boeing was brought down by an SU-25 fighter jet. But its chief designer has now told German media that’s impossible, because it can’t fly high enough. What do you make of that?

Gordon Duff: The claim that it was an SU-25 is unsupportable. Since 2010, NATO has begun using electronic countermeasure pods. They are designed by Raytheon and BAE Systems. When attached to an aircraft, an SU-27, an SU-29 maybe even an F-15, these allow the backscattering – that is when you use radar, and this is what was said the radar identified as two SU-25 aircraft. Well these pods that attach to any plane can make a plane look like an SU-25 when it’s not an SU-25 or a flock of birds or anything else. It’s a new version of poor man’s stealth…It’s called radar spoofing, so with radar spoofing anyone who says they have identified an aircraft by radar is trying to mislead people because that’s no longer a reliable way of dealing with things.

If I could go on with the SU-25, the claimed service ceiling is based on the oxygen’s supply in the aircraft. Now there is a claim that this plane will only work to 22,000 feet. At the end of the WWII a German ME-262 would fly at 40,000 feet. A P-51 Mustang propeller plane flew at 44,000 feet. The SU-25 was developed as an analogue of the A-10 Thunderbolt, an American attack plane. The planes have almost identical performance except that the SU-25 is faster and more powerful. The A-10 Thunderbolt has a service ceiling of 45,000 feet. The US estimates the absolute ceiling, which is a different term, of the SU-25. And we don’t know whether the SU-25 was involved at all, we are only taking people’s word and people we don’t trust. But the absolute ceiling for the plane is 52,000 feet.

RT: Do you agree with the statement that “many more factors indicate that the Boeing 777 was hit by a ground-to-air missile that was launched from a Buk missile system”? How much technical expertise would it take to fire a Buk launcher?

GD: We’ve looked at this. I had an investigating team, examiners, which included aircraft investigation experts from the US including from the FAA, the FBI and from the Air Line Pilots Association. I also had one of our air traffic and air operational officers…with the Central Intelligence Agency look at this. And one of the things we settled is that in the middle of the day if this were a Buk missile the contrail would have been seen for 50 miles. The contrail itself would have been photographed by thousands of people; it would have been on Instagram, Twitter, all over YouTube. And no one saw it.

You can’t fire a missile and on a flat area in a middle of the day leaving a smoke trail into the air and having everyone not see it. There is no reliable information supporting that it was a Buk missile fired by anyone. And then additionally we have a limited amount of information that NATO and the Dutch investigators have released, forensic information, and that is contradicted by other experts that have looked at things. We don’t have reliable information to deal with but the least possible thing, the one thing we can write off immediately – it wasn’t a ground-to-air missile because you simply can’t fire a missile in the middle of the day without thousands and thousands of people seeing it and filming it with camera phones.

“Poor Fellow-Soldiers of Christ and of the Temple of Solomon”.

• Knights Templar Win Heresy Reprieve After 700 Years (Reuters)

The Knights Templar, the medieval Christian military order accused of heresy and sexual misconduct, will soon be partly rehabilitated when the Vatican publishes trial documents it had closely guarded for 700 years. A reproduction of the minutes of trials against the Templars, “‘Processus Contra Templarios — Papal Inquiry into the Trial of the Templars'” is a massive work and much more than a book – with a €5,900 euros price tag. “This is a milestone because it is the first time that these documents are being released by the Vatican, which gives a stamp of authority to the entire project,” said Professor Barbara Frale, a medievalist at the Vatican’s Secret Archives. “Nothing before this offered scholars original documents of the trials of the Templars,” she told Reuters in a telephone interview ahead of the official presentation of the work on October 25.

The epic comes in a soft leather case that includes a large-format book including scholarly commentary, reproductions of original parchments in Latin, and — to tantalize Templar buffs — replicas of the wax seals used by 14th-century inquisitors. Reuters was given an advance preview of the work, of which only 799 numbered copies have been made. One parchment measuring about half a meter wide by some two meters long is so detailed that it includes reproductions of stains and imperfections seen on the originals. Pope Benedict will be given the first set of the work, published by the Vatican Secret Archives in collaboration with Italy’s Scrinium cultural foundation, which acted as curator and will have exclusive world distribution rights. The Templars, whose full name was “Poor Fellow-Soldiers of Christ and of the Temple of Solomon”, were founded in 1119 by knights sworn to protecting Christian pilgrims visiting the Holy Land after the Crusaders captured Jerusalem in 1099.

Human kindness overflowing.

• Arctic Melt Brings More Persistent Heat Waves to US, Europe (Bloomberg)

The U.S., Europe and Russia face longer heat waves because summer winds that used to bring in cool ocean air have been weakened by climate change, German researchers said. Rapid Arctic warming disturbs air streams in ways that have “significantly” reduced summer storms, raising the likelihood of heat waves, the Potsdam Institute for Climate Impact Research said in a report Thursday in the journal Science. Hot weather in Russia in 2010 devastated crop harvests and caused wildfires. “Unabated climate change will probably further weaken summer circulation patterns which could thus aggravate the risk of heat waves,” co-author Jascha Lehmann said in a statement e-mailed by the institute.

“The warm temperature extremes we’ve experienced in recent years might be just a beginning.” With heat-trapping gases from burning oil, coal and natural gas at record levels, global temperatures are set to warm by 3.6 degrees Celsius (6.5 Fahrenheit) by the end of the century, according to the International Energy Agency. That’s the quickest climate shift in 10,000 years. Temperature gains can disrupt air flows that govern storm activity, the Potsdam report showed. “When the great air streams in the sky above us get disturbed by climate change, this can have severe effects on the ground,” lead author Dim Coumou said. The study used data on atmospheric circulation in the Northern Hemisphere from 1979 to 2013.

Warming in the Arctic, where temperatures rise faster than elsewhere as ice caps melt, is believed to narrow temperature differences and thus weaken the jet stream — air motion that’s important for shaping our weather, according to the scientists. “The reduced day-to-day variability that we observed makes weather more persistent, resulting in heat extremes on monthly timescales,” Coumou said. “The risk of high-impact heat waves is likely to increase.”