Marjory Collins 3rd shift defense workers, midnight, Baltimore April 1943

Greek bond yields have slid back into danger territory. They were at 9% last night, far higher than the 7% ‘barrier’ generally assumed to separate acceptable from unsustainable. Someone better do something quick. Left wing Syriza party chief Tsipras is waiting to take over.

• Greek Bond Rout Drags Down Markets From Ireland to France (Bloomberg)

Greece’s government debt is back in the spotlight and investors are looking for the exit. As the four-day rout in Greek bonds sent yields to the highest since January, the selloff started to infect nations from Ireland to Portugal and even larger countries such as France. In Spain, a debt auction fell short of the government’s maximum target, and European stocks extended their longest losing streak since 2003. German 10-year bunds fell for the first time in three days, pushing the yield on the euro region’s benchmark securities up from a record low. “We are in a typical flight-to-quality environment with substantial losses in stock markets and wider spreads,” said Patrick Jacq, a fixed-income strategist at BNP Paribas SA in Paris. “The Spanish auction suffered from the environment, not from domestic reasons. It’s the market environment which is not favorable.”

[..] It’s five years since a change in government in Greece set in motion the debt crisis by unveiling a budget deficit that was larger than previously reported by its predecessor. The country was eventually granted a €240 billion lifeline that has kept it afloat since 2010. Markets slid this week after euro-area finance ministers clashed with the nation’s leaders over their plan to leave their safety net, sparking concern that Greece won’t be able to finance itself at sustainable rates without the support of its regional partners. The lack of supervision may lead to the country backtracking on reforms agreed with the EU and the IMF. “Whether that’s a bellwether for more problems to come or not, I’m doubtful of, but we certainly saw the periphery sell off,” Andrew Wilson at Goldman Sachs said in an interview with Bloomberg TV, referring to the slump in Greek bonds yesterday. “It was a flight to quality, it was a bit of a scary story for a while there and I think that’s all it’s reflecting.” Greek bonds have lost 17% in the past month, cutting their return this year through yesterday to 9.9%.

“The yields are not just discounting a protracted slump, they are also starting to price default risk yet again, or even EMU break-up risk.”

• World Braces As Deflation Tremors Hit Eurozone Bond Markets (AEP)

Eurozone fears have returned with a vengeance as deepening deflation across Southern Europe and fresh turmoil in Greece set off wild moves on the European bond markets. Yields on 10-year German Bund plummeted to an all-time low on 0.72pc on flight to safety, touching levels never seen before in any major European country in recorded history. “This is not going to stop until the European Central Bank steps up to the plate. If it does not act in the next few days, this could snowball,” said Andrew Roberts, credit chief at RBS. Austria’s ECB governor, Ewald Nowotny, played down prospects for quantitative easing, warning that the markets had “exaggerated ideas about purchase volumes” and that no asset-backed securities (ABS) would be bought before December. Calls for action came as James Bullard, the once hawkish head of St Louis Federal Reserve, said the Fed may have to back-track on bond tapering in the US, hinting at yet further QE to fight deflationary pressures and shore up defences against a eurozone relapse.

“The forces of monetary deflation are gathering,” said CrossBorderCapital. “Global liquidity is declining and central banks are not doing enough, either in the West or the East to offset the decline. This may not be a repeat of 2007/2008, but it is starting to look more and more like another 1997/1998 episode.” This is a reference to the East Asia crisis and Russian default triggered by withdrawal of dollar liquidity. Ominously, French, Italian, Spanish, Irish, and Portuguese yields diverged sharply from German yields in early trading today, spiking suddenly in a sign that investors are again questioning the solidity of monetary union. The risk spread between Bunds and Italian 10-year yields briefly jumped 38 basis points. This was the biggest one-day move since the last spasm of the debt crisis in 2012. This sort of price action suggests that the markets fear deflation is becoming serious enough to threaten the debt dynamics of weaker EMU states. The yields are not just discounting a protracted slump, they are also starting to price default risk yet again, or even EMU break-up risk.

” … well beyond the 7%-threshold which many analysts believe is unsustainable”.

• Greek Drama: Bond Yields Near 9% Threshold (CNBC)

Greek government bond yields spiked beyond 8% on Thursday, in a sign of growing concern about the country’s economic stability given the possibility of snap elections and plans to exit its bailout early. The 10-year note yielded 8.9% on Thursday at Europe market close, well beyond the 7%-threshold which many analysts believe is unsustainable. It is the first time yields have passed this point since January. On Wednesday evening, the sovereign note yielded 7.863%. The volatility comes amid growing concerns about Athens’ plans to exit its bailout ahead of schedule. On Saturday, Prime Minister Antonis Samaras won a confidence vote in parliament, forcing lawmakers to back his plans to exit its international aid program early – a prospect that is looking increasingly unlikely. Samaras’ government has also been plagued by the prospect of snap elections early next year if the prime minister fails to gain the support of opposition lawmakers for his candidate for president. A promise to exit the painful program early was key in securing that backing.

The concerns have led to a turbulent few days for Greek markets, with the Athens’ benchmark index tanking up to 9% on Wednesday. On Thursday, the ASE closed down around 2.2% lower and is now down around 25% this year. It also proved to be the spark that turned markets south on Thursday morning after equities bounced back slightly at the session open. “This smacks of the ‘risk off’ move of old,” Richard McGuire, a senior rate strategist at Rabobank told CNBC via email. “The peripherals are under pressure across the board which is potentially an alarming sign that fundamental risk is returning.” In a bid to free up some more money for the country’s banks, the European Central Bank cut the haircut it applies on bonds submitted by Greece’s banks as collateral to raise money. The new discount meant an extra 12 billion euros of liquidity could be tapped by Greek banks, the country’s central bank governor Yannis Stournaras told reporters.

There we go again.

• Eurozone Crisis, 5 Years On: No Happy Ending For Greek Odyssey (Guardian)

Greece loves its epic tales and the greatest of them is the story of Odysseus, the hero who took 10 years to find his way back to Ithaca at the end of the Trojan War. A modern version of the Odyssey began in Greece five years ago this weekend when the government in Athens admitted that it had cooked the books to make its budget deficit look much smaller than it actually was. Few thought then that the scandal would have serious ramifications or that the journey through the stormy seas of crisis would have taken so long. Back in October 2009, the mood in the eurozone was one of cautious optimism.

The year had started with Europe caught up in the global economic crash that followed the collapse of Lehman Brothers, but co-ordinated action by the G20 during the winter of 2008-09 had created the conditions for a recovery in growth that appeared to be gaining strength as the year wore on. The admission by George Papandreou’s new socialist government of a black hole in Greece’s public finances was unwelcome but not viewed as something to be unduly worried about. But the policy makers in Brussels and Frankfurt were wrong. Greece did matter. What has become clear subsequently is that the eurozone crisis is similar to Scylla, the monster that devoured many of Odysseus’s men: a many-headed beast.

The first sign of the crisis to come was the deterioration in government finances, not just in Greece but in other eurozone countries. In truth, though, rising deficits were symptoms of three bigger problems. The first was that many countries in the eurozone had a competitiveness problem. Monetary union had given all the members of the single currency a common interest rate and no freedom to adjust their exchange rates. This meant that if a country had a higher inflation rate than its neighbour, its goods for export would gradually become more expensive. This is what had happened regularly to Italy during the post-war period, when its inflation rate was invariably higher than that in Germany. This time, however, Italy could not devalue.

Samaras’ game is up.

• European Bonds: It’s Every Country For Itself Now (CNBC)

The honeymoon for European bond rates appears to be over for the Continent’s most-troubled economies. After more than a year of interest rates across the Continent moving lower in lockstep—regardless of the country—the last 24 hours show a breakdown in the relationship. Investors are still pouring into German bunds, much as they are still moving into U.S. Treasurys. But they are selling Italian, Spanish, Portuguese and especially Greek debt. Doug Rediker, CEO of International Capital Strategies, told CNBC that the differentiation represents “a more rational recognition of both credit risks and economic performance within the euro zone.” Investors are once again differentiating between countries based on the ability of their economies to grow—and for their governments to eventually pay back their debts.

Peter Boockvar, chief market analyst at The Lindsey Group, said that the end of easy money from quantitative easing and the “impotence” of the European Central Bank have alerted investors to a region that is not growing and where “debt-to-GDP ratios continue to rise.” Regarding Europe’s biggest economy, Rediker noted that “the German economy is underperforming, but overall its domestic economic performance is considered strong. Countries like Italy and France have far less to shout about in terms of economic performance and reform efforts.” The rise in Greek bond yields is particularly sharp. The country’s 10-year yield stood at nearly 9% on Thursday, after being below 6% just last month. The current Greek government, led by Antonis Samaras, is trying to make an early exit from a bailout program it got from the European Union and International Monetary Fund, but investors are nervous about the country’s ability to live without a financial backstop that would provide them cheap money in the event of a shortfall.

“They’ll be hoping this turmoil will pass on its own.”

• Euro Economy’s Managers Aren’t Blinking in Market Rout (Bloomberg)

German Chancellor Angela Merkel and European Central Bank President Mario Draghi aren’t blinking yet. The longest losing streak in European stocks in 11 years and the weakest inflation since 2009 has intensified pressure on the managers of the euro area’s already ailing economy to deliver fresh stimulus programs. Battle-hardened by the debt crisis that almost broke the euro two years ago, policy makers are refusing to panic as they argue enough help is in the pipeline. The lesson of that last turmoil is nevertheless that investors may ultimately force action with taboo-busting quantitative easing from the ECB likely drawing closer as deflation fears intensify. “The main story really is that the recovery is very weak, very fragile, and something has to happen,” said Martin Van Vliet, an economist at ING Groep NV in Amsterdam. “Markets are increasingly expecting they’ll have to do sovereign QE.”

The euro area is again at the epicenter of a global rout in financial markets as investors increasingly fret its toxic mix of weak growth and sliding inflation may become the norm elsewhere as central banks run out of ways to provide support. With Europe straining amid tit-for-tat sanctions on Russia, Germany this week showing fresh signs that it is no longer immune to the slowdown in its neighbors. Confirmation yesterday that inflation slowed to just 0.3% in September helped drive down the Stoxx Europe 600 Index for an eighth day. Germany’s 10-year bond yield hit a record low. For the moment, policy makers are holding to their view that the region needs time rather than new stimulus even with prices already shrinking in Italy, Spain, Greece, Slovakia and Slovenia. “I think they’re surprised by the market correction,” Michael Schubert, an economist at Commerzbank AG in Frankfurt, said in a telephone interview. “They’ll be hoping this turmoil will pass on its own.”

Risk off.

• Volckerized Wall Street Dumping Bonds With Rest of Herd (Bloomberg)

Corporate bond values are swinging the most in more than a year and here’s one reason why: Wall Street’s biggest banks are following the crowd and selling, too. Take junk bonds, which have lost 2% in the past month. Dealers, which traditionally used their own money to take bonds off clients desperate to sell during sinking markets, sold about $2 billion of the securities during the period, according to data compiled by Trace, the bond-price reporting system of the Financial Industry Regulatory Authority. Banks have cut debt holdings in the face of higher capital requirements and curbs of proprietary trading under the U.S. Dodd-Frank Act’s Volcker Rule. Their lack of desire to take risks has had the unintended consequence of exacerbating price swings amid the rout now, said Jon Breuer, a credit trader at Peridiem Global Investors LLC in Los Angeles, California.

“There just isn’t the appetite and ability to warehouse the risk anymore,” he wrote in an e-mail. “Everyone is afraid to catch the falling knife.” High-yield bonds have lost 1.1% this month, following a 2.1% decline in September. That was the worst monthly performance since June 2013 for the $1.3 trillion market that’s ballooned 82% since 2007, according to the Bank of America Merrill Lynch U.S. high-yield index. Debt of speculative-grade energy companies has been particularly hard hit along with oil prices, tumbling 3.4% this month with relatively few buyers willing to step in to mitigate the drop. For example, notes of oil and gas producer Samson Investment Co. have lost 25% since the end of August. The market’s indigestion was brought on by many reasons: signs of a global economic slowdown, Ebola spreading and concern that U.S. energy companies will struggle to meet their debt obligations after financing their expansion by issuing bonds.

But obviously there’s money to be made in a rout like this.

• Pimco To Blackstone Preparing To Feast On Junk Bonds (Bloomberg)

In a junk-bond market that has been anything but high-yield for almost two years, the world’s biggest debt-fund managers have been stockpiling cash for a selloff. After the worst one in three years, they’re getting ready to pounce. Firms from Pacific Investment Management Co. to Blackstone Group LP say they are poised to scoop up speculative-grade corporate bonds after yields rose to the highest levels in more than a year. They’re looking for bargains after building up the highest levels of cash in almost three years. “Credit is a buy here, specifically high yield” bonds and loans, Mark Kiesel, one of three managers who oversee Pimco’s $202 billion Total Return Fund, said yesterday in a Bloomberg Television interview. At Blackstone, Chief Executive Officer Stephen Schwarzman told investors yesterday that the firm’s $70.2 billion credit unit is ready to “feast” on lower-rated, long-term debt, particularly in Europe, after “waiting patiently for something bad to happen.”

Taxable corporate-bond mutual funds tracked by the Investment Company Institute increased the proportion of cash and cash-like instruments they set aside to 8.5% of their $1.96 trillion of assets in August. That’s up from a three-year low of 4.9% in April 2013 and the most since November 2011, ICI data show. By amassing cash or parking money in easy-to-sell debt such as Treasuries, fund managers have been maintaining flexibility to swoop in and buy securities at discounts. Average yields on speculative-grade bonds sold by companies from the U.S. to Japan climbed to 6.67% yesterday, jumping more than 1 percentage point from a record-low 5.64% in June, according to Bank of America Merrill Lynch index data. The debt is now paying 5.3 percentage points more than government bonds, the widest spread since July 2013 and up from 3.6percentage points in June. The market hasn’t moved that much since the European debt crisis in 2011, the index data show.

“The SEC caught Athena ‘placing a large number of aggressive, rapid-fire trades in the final two seconds of almost every trading day during a six-month period to manipulate the closing prices of thousands of Nasdaq-listed stocks.’ ”

• High-Speed Traders Put a Bit Too Much Gravy on Their Meat (Bloomberg)

One good general rule is that it’s harder than you think it is to figure out what’s market manipulation and what isn’t. Trading a lot, cancelling a lot of orders, putting in orders or doing trades on both sides of the market, trading a lot right before a close or fixing — all of those things could be signs of nefarious manipulation, or just normal risk management. No single event or pattern proves manipulation. You often need to look for subtle clues to figure out whether a trade is actually manipulative One subtle clue is, if you name your algorithms “Meat” and “Gravy,” there is probably something wrong with you! And your trading, I mean. But also your aesthetic sensibilities. Here is a Securities and Exchange case against Athena Capital Research, which the SEC touts as “the first high frequency trading manipulation case.”

The SEC caught Athena “placing a large number of aggressive, rapid-fire trades in the final two seconds of almost every trading day during a six-month period to manipulate the closing prices of thousands of Nasdaq-listed stocks.” That period was in late 2009, by the way. Athena settled for $1 million, and while it did so “without admitting or denying the findings,” the SEC’s order has the usual litany of dumb, so you can tell that Athena was fairly caught. In fact, the SEC is kind enough to put the dumb quotes in boldface, so they’re easy to find,1 though somehow this didn’t make it into bold: Athena referred to its accumulation immediately after the first Imbalance Message as “Meat,” and to its last second trading strategies as “Gravy.

Heehee that’s dumb. What is going on here? It starts with the fact that Nasdaq basically does two sorts of trading in the late afternoon. One is just its regular continuous order book trading, the kind it does all day. There are bids, there are offers, and there are lots of little trades that are constantly updating the price of every stock. Someone trades 100 shares at $20.01, 100 shares at $20.02, 200 shares at $20.03, 100 more at $20.02 again, etc., all within a fraction of a second. There is also the closing auction, which is more or less a separate institution. This is an auction that occurs at a single point in time, just after the 4:00 p.m. close. People put in buy orders and sell orders throughout the day, and then they all trade with each other simultaneously just after 4 p.m. at the clearing price of the auction.

This ain’t over by a long shot. Wait till prices start dropping.

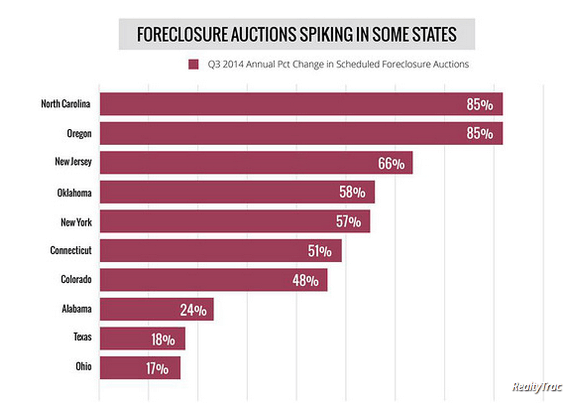

• 10 States Where Foreclosures Are Soaring (MarketWatch)

The property market is improving and foreclosures are falling — except in these 10 markets. Some 317,171 U.S. properties had foreclosure filings in the third quarter, down 16% on the same period last year, according to real-estate website RealtyTrac. However, default notices in the third quarter increased from a year ago in certain states, including Indiana (up 59%), Oklahoma (up 49%), Massachusetts (up 38%), New Jersey (up 19%), Iowa (up 12%) and New York (up 2%). States with the five highest foreclosure rates in the third quarter were among those hit hardest by the 2008 property crash: Florida, Maryland, New Jersey, Nevada, and Illinois. Some 58,589 Florida properties had a foreclosure filing in the third quarter of 2014.

That was down 4% from the previous quarter and down 17% from a year ago, but it still meant that in every 153 housing units had a foreclosure filing. Orlando, Fla., Atlantic City, N.J., and Macon, Ga., had the top metro foreclosure rates in the third quarter. With one in every 117 housing units with a foreclosure filing, Orlando had the highest foreclosure rate among metropolitan areas with a population of 200,000 or more. A total of 8,052 Orlando-area properties had a foreclosure filing, down 1% on the quarter but up 16% from a year ago.

While the Ohio property markets have seen a decline in the number of available foreclosures on the market over the last year, “We have equally noticed an increase in activity of lender servicers acquiring properties at sheriff sales and deed-in-lieu workouts,” says Michael Mahon, who covers the Cincinnati, Columbus and Dayton markets as executive vice president at HER Realtors. One explanation: Many Americans are choosing foreclosure over short sales. A couple of years ago, 18 out of 20 clients underwater who couldn’t afford to keep their home chose a short sale, says Frank Duran, a broker in Denver, but now only 2 out of 20 opt for a short sale. One explanation: In a short sale, canceled debt — or the difference between the value and sale price of the house — is often treated as taxable income.

Why anyone would trust even one word from the Fed anymore is beyond me.

• ‘Stunning’ Fed Move Put Bottom Under Stocks (CNBC)

After a swift and serious selloff, stocks have managed to rise on Thursday’s session with help from the soothing words of St. Louis Federal Reserve President James Bullard. And after dropping just shy of 10% from high to low, the S&P 500 looks to have finally bottomed out, some traders say. “Whether the complete correction is over I’m not positive yet, but there looks to be some relative calm,” said Jim Iuorio of TJM Institutional Services. “I think the next leg is going to be higher.” Iuorio is focusing on the comments Bullard made Thursday morning on Bloomberg TV, where he discussed the quantitative easing program, which the Fed is currently winding down.

He said, “We have to make sure that inflation expectations remain near our target. And for that reason, I think a reasonable response by the Fed in this situation would be to … pause on the taper at this juncture, and wait until we see how the data shakes out in December.” Bullard’s comments come two days after those of San Francisco Fed President John Williams (who, like Bullard, is a non-voting member of the Fed Open Market Committee). Williams told Reuters “If we get a sustained, disinflationary forecast… then I think moving back to additional asset purchases in a situation like that should be something we seriously consider.”

The proper theater for these matters. Courts require proof.

• Russia Takes EU To Court Over Ukraine Sanctions (FT)

Russia is taking the EU to court over sanctions imposed on some of its biggest companies. The move is a sign of the pain that the companies’ exclusion from global capital markets is inflicting on the Russian economy. Rosneft, the state oil company, and Arkady Rotenberg, a long-time friend and former judo sparring partner of President Vladimir Putin, have both launched legal challenges to the sanctions, imposed over Russia’s actions in Ukraine. The EU bans, with similar measures adopted by the U.S., have all but frozen Russian companies and banks out of western capital markets, at a time when they have to refinance more than $130 billion of foreign debt due for redemption by the end of 2015. Rosneft filed a case against the EU’s European Council in the general court under the European Court of Justice on October 9, requesting an annulment of the council’s July 31 decision that largely barred it and other Russian energy companies and state banks from raising funds on European capital markets.

Mr Rotenberg, who was hit with an EU visa ban and asset freeze in July, filed a legal case in the same court on October 10 challenging the move. The challenges follow verdicts that have gone against the council in relation to similar measures imposed on Iran and Syria. In particular, the court has ruled that in implementing sanctions, European states have been too reliant on confidential sources, which impair the targets’ ability to mount an effective defense. A Russian lawyer who advises one company on legal strategies over sanctions said the challenges by Rosneft and Mr Rotenberg might help sway some EU member states when the bloc begins to discuss whether to renew its sanctions against Russia next spring.

Oh, yeah, big-screen TVs for everyone!

• The Big Perk Of Oil’s Wild Slide (CNBC)

Crude oil is plummeting – down some $25 bucks a barrel from the yearly high set just a few months ago. And those lower prices mean lower gasoline prices for people like you and me, which should result in a few extra dollars in your pocket. This is big news, guys, because the biggest and most celebrated holiday of the year is coming up for many of you — Black Friday! (Oh, you thought I was going to say something like Thanksgiving or Christmas. Please! Those holidays are just a goofy excuse to miss work.) I digress. But if the current trend remains intact, we’re going to hear about record breaking sales on Black Friday, which is awesome for retailers and the economy. I say spend, spend, spend those pennies you’re saving while gassing up the F-150. And, according to Moody’s, you should have a lot of dough to play with.

A 10-cent decrease in gas prices translates to an extra $93.25 in gasoline and diesel expenditures per year for the average American household, which equates to $11 billion in consumer spending. Over the past month, gasoline prices have declined 6%, or 20 cents per gallon. That, Mr. math wizard, is $22 billion in available cash. And, knowing many Americans prefer to spend than save, I would be thinking about opening a big-screen TV store if I were you. If you prefer happy endings and would rather stay away from reality, I would suggest stop reading; because this is where I tell you lower gas prices will likely have a dramatic and terrifying impact on violence around the globe.

These guys sure don’t understand the Saudis. or shale, for that matter.

• Gloves Off Over Oil: Saudi Arabia Versus Shale (CNBC)

Oil prices might have halted their earlier slide below $80 a barrel this week but analysts believe the dog fight between major oil producers over reducing the supply of oil could lead to lower prices yet. Oil markets have seen prices fall sharply over the last four months, as faltering global growth in major economies has cut demand at a time of over-supply. On Thursday, WTI crude fell below $80 a barrel for the first time since June 2012 before recovering to 82.88 on Friday. The global oil benchmark Brent crude climbed by almost a dollar to near $86 a barrel on Friday morning – up from a near four-year low at below $83 on Thursday – after more positive economic data from the U.S. Prices have fallen over 20% since June, however, when turmoil in Iraq lifted prices to $116 a barrel.

“The bearishness in the global oil market is all being driven by the U.S. shale revolution,” Seth Kleinman, head of Global Energy Strategy at Citi, told CNBC. “It’s being driven by this massive infrastructure build out that we’ve seen over the last few years and it’s taken the market a lot more time to catch up and act more rationally.” The U.S. shale gas industry has boomed over the last decade with shale gas and oil producers proliferating and production surging in the country, becoming a competitor for major oil-exporting countries such as Saudi Arabia.

The drop in oil prices has led to expectations that OPEC could cut output in an attempt to shore up prices, but OPEC members Saudi Arabia and Kuwait played down such a move at the start of the week. That could pile pressure on the U.S. shale industry and its producers to cut supply themselves if and when prices decline further. “Everyone was assuming that the Saudis were going to pull back and defend prices,” Kleinman told CNBC Europe’s “Squawk Box” on Friday. “They probably could have defended $100 but they sent the message loudly, clearly and by every venue possible of ‘we’re not going to defend prices here.’ In fact, they started slashing prices to Asia.”

Stay with the dollar.

• The New Defensives: High Yield And The Dollar (CNBC)

As world markets tumble and the euro zone crisis seemingly reared its head once more, investors have scrambled to find somewhere safe to house their cash. Equities on both sides of the Atlantic have been hammered as volatility has peaked to 2011 levels amid worries over global growth and the spread Ebola. A flight to traditional safe haven U.S. Treasurys pushed yields down around 1.8% on Thursday, levels not seen since 2013 – making it an expensive option for investors as prices move inverse to yields. “Sometimes, when markets fall, you get to a ‘no-brainer’ moment, when you can afford to ignore short-term concerns and take advantage of sudden decline in prices. This is not such a moment for equities,” chief investment officer at Cazenove Capital Management, Richard Jeffrey said. “Markets are not cheap, and could fall further. Indeed, although we might expect it to remain so, the U.S. market looks quite expensive,” he said.

Cash levels jumped and bearish sentiment reached levels not seen for two years according to Bank of America’s monthly fund manager survey, but managers have also taken another look at high yield bonds as stocks have been hit. “The current environment presents the opportunity to take another look at asset classes that had sold off and now look more attractive,” BlackRock’s global chief investment strategist Russ Koesterich said. One such asset class is high yield bonds as the yield difference between high yield bonds and higher-quality, lower-yielding U.S. Treasurys has widened out to the highest level in a year, he said. “This indicates high yield bonds offer better value. Given that corporate America remains strong and default rates low, high yield now looks likely to provide a reasonable level of income relative to the rest of the fixed income market,” he said.

Australia will get badly hurt by China’s rising tariffs and falling economic reality.

• Is The ‘Lucky Country’ Headed For Gloomy Times? (CNBC)

Sentiment in the so-called ‘lucky country’ has deteriorated sharply, analysts told CNBC. Australia’s stock market has fallen 8% since the start of September, weighed by concerns over global economic growth, steep declines in commodity prices and the state of Australia’s property market. “Investor sentiment has certainly collapsed across a range of measures,” Shane Oliver, head of investment strategy at AMP Capital, told CNBC. Investors are much more concerned about the prospect of a market downturn and the state of Australia’s housing market than they were in the second quarter of this year, a survey of fixed income investors by Fitch Ratings showed on Wednesday. 79% of respondents flagged a downturn as a high or moderate risk, up from 43% in Fitch’s second quarter survey.

The frothy housing market was high on respondents’ worry list; 53% expect house prices to rise by 2 to 10% in 2015. “The concerns demonstrated in the Fitch Ratings survey are very clearly the case,” said Evan Lucas, market strategist at IG. “Housing is a major part of Australia confidence, [so] any issues around housing and wages are going to see sentiment fall.” Australian dwelling values rose 9.3% over the 12 months to September, spurred by a record 15-month run of historically low interest rates. Values in Sydney and Melbourne rose 14.3% and 8.1%, respectively, over that period, RP Data figures show. And in recent months, the Reserve Bank of Australia warned of regulatory steps to rein in loans to investors.

Indeed. Not going to happen.

• Don’t Hold Your Breath Waiting For QE4 (CNBC)

Suggestions quantitative easing (QE) might go on a reunion tour in the U.S. helped to staunch market losses Thursday, but don’t hold your breath waiting for the Federal Reserve to whip out the checkbook, analysts said. “It’s part of a strategy to calm markets down, to remind them that ‘we still have your back and we’re on top of this’ from a central bank point of view,” Mikio Kumada, global strategist at LGT Capital Partners, told CNBC. “Whether they will actually do it, I’m not so sure. At least as far as the U.S. is concerned, the economic conditions are decent enough.”

Stocks bounced back Thursday after a rough opening, with the S&P 500 ending the day less than a point higher, after St. Louis Federal Reserve President James Bullard Thursday morning suggested to Bloomberg TV, that the Fed should consider pausing its taper of the quantitative easing program. “We have to make sure that inflation expectations remain near our target. And for that reason, I think a reasonable response by the Fed in this situation would be to… pause on the taper at this juncture, and wait until we see how the data shakes out in December,” Bullard said. The Federal Reserve had expected to complete the taper later this month. Those comments come two days after those of San Francisco Fed President John Williams (who, like Bullard, is a non-voting member of the Fed Open Market Committee).

Williams told Reuters: “If we get a sustained, disinflationary forecast… then I think moving back to additional asset purchases in a situation like that should be something we seriously consider.” Some are extremely skeptical of a QE encore performance. “The only thing that could justify QE4 is a high probability of a downturn in the real economy and/or falling core inflation,” said Eric Chaney, chief economist at AXA Group, in a note. “The probability of a U.S. recession is close to zero,” he said. “Overall, there is not one single indicator flashing red, as far as the risk of recession is concerned,” he added, citing indicators such as the consumer debt-to-income ratio back at end-2002 levels, high corporate profitability and even the declining federal deficit.

That’s what you get for telling fairy tales all teh time.

• Bank of England Chief Economist ‘Gloomier’ About UK Prospects (Guardian)

The chances of an early rise in UK interest rates have fallen, says the Bank of England’s chief economist, Andrew Haldane, who admits he is “gloomier” about the prospects for the economy than he was a few months ago. In a speech on Friday morning, which will reinforce market views that rates are unlikely to rise from their record low of 0.5% until the middle of next year, Haldane said: “That reflects the mark-down in global growth, heightened geo-political and financial risks and the weak pipeline of inflationary pressures from wages internally and commodity prices externally. “Taken together, this implies interest rates could remain lower for longer, certainly than I had expected three months ago, without endangering the inflation target,” said Haldane, a member of the Bank’s nine-member interest rate setting committee. The prospect that interest rates will stay lower for longer sent sterling tumbling on the foreign exchanges, with the pound losing half a cent against the dollar.

Haldane also warned that Britain was vulnerable to another explosion in the eurozone crisis. He told ITV News: “It’s a concern. It [the eurozone] is our biggest trading partner by far. We know we’ve seen recently that any event on the continent laps back to the UK very quickly through our trade links, but also through our financial links and, indeed, increasingly just because of confidence. If confidence is ebbing on the continent, it appears to leak across here pretty quickly.” In June, Haldane had put even weight on moving interest rates sooner and moving them later. He used the cricketing terms “being on the front foot” and being on the “back foot”. On Friday, he said: “While still a close-run thing, the statistics now appear to favour the back foot. Recent evidence, in the UK and globally, has shifted my probability distribution towards the lower tail. Put in rather plainer English, I am gloomier.”

No, but it will come anyway.

• Is Asia Ready for Another Wild Ride? (Bloomberg)

From Ebola to debt to deflation, fear once again stalks the global economy. With bewildering speed, concerns about of credit defaults, slowing demand and political instability have eclipsed exuberance over America’s falling jobless rate and Alibaba’s record-breaking IPO. The most-asked question isn’t where to make profits, but where to find a safe haven from the coming storm. Could it be Asia again? Sadly, unlike during the most recent global recession, even this region finds itself in an increasingly dangerous position this time around. That’s not to say Asia doesn’t have enviable fundamentals. Even given China’s worsening data, the stalling of “Abenomics” in Japan and structural headwinds that challenge officials almost everywhere, Asia may yet ride out renewed turbulence better than the West — just as it did in 2008. If one thinks of investment destinations as beauty contestants, Asia is still hands-down the least ugly candidate.

But the region’s growth over the last six years has been driven more by asset bubbles than genuinely sustainable economic demand. Already, we are seeing structural slowdowns from Seoul to Jakarta. These strains will become even more pronounced as Europe’s debt troubles re-emerge and the Federal Reserve’s record stimulus loses potency. Asian policymakers also have less latitude going forward to support growth. “A full recovery of demand in the West, sufficient to pull Asia out of its malaise, remains a distant prospect,” says Qu Hongbin, Hong Kong-based co-head of Asian economic research at HSBC Holdings. “Rather, reviving growth in Asia, whether in China, Japan, India or anywhere in between, requires deep structural reforms: pruning subsidies, spending more on quality infrastructure, boosting education, opening further to foreign direct investment, and, perhaps most important of all, introducing greater competition in local markets. These are politically tough choices to make. But they will grow only more difficult, the longer they are put off.”

GPIF moving away from Japan sovereign bonds is Abe’s riskiest move yet. And it will end where all his policies lead: into misery.

• Japan No.1 Pension Fund Would Be ‘Stupid’ to Give Asset Goals First (Bloomberg)

Japan’s $1.2 trillion retirement fund would be “stupid” to announce its new investment strategy before adjusting asset allocations, said Takatoshi Ito, a top government adviser on overhauling public pensions. Publishing target weightings in advance would move markets, forcing the Government Pension Investment Fund to buy at highs and sell at lows, Ito said in an interview in Tokyo on Oct. 14. GPIF should shift holdings as much as possible now, he said, while noting that the fund doesn’t seem to be doing so. Deciding the new asset split is taking time partly due to a debate on whether to make it public before or after changing the portfolio, Ito said.

Investors are waiting for the bond-heavy fund to confirm it will cut Japanese debt to buy local stocks and overseas assets, after a government-picked panel led by Ito advised GPIF to sell bonds in a report last year. Yasuhiro Yonezawa, the chairman of GPIF’s investment committee, said in July that while it would be ideal to adjust the fund’s assets before the announcement, it must also avoid disrupting markets. “Saying ‘we’re going to purchase as much as whatever%’ before buying anything is a stupid idea,” Ito said. “It’s tantamount to not fulfilling their fiduciary responsibilities and not appropriately investing the money entrusted to them. It’s wrong, and I’m against it.”

“Something that is easy to control got completely out of hand …”

• ‘Ebola Epidemic May Not End Without Developing Vaccine’ (Guardian)

The Ebola epidemic, which is out of control in three countries and directly threatening 15 others, may not end until the world has a vaccine against the disease, according to one of the scientists who discovered the virus. Professor Peter Piot, director of the London School of Hygiene and Tropical Medicine, said it would not have been difficult to contain the outbreak if those on the ground and the UN had acted promptly earlier this year. “Something that is easy to control got completely out of hand,” said Piot, who was part of a team that identified the causes of the first outbreak of Ebola in Zaire, now the Democratic Republic of Congo, in 1976 and helped bring it to an end. The scale of the epidemic in Sierra Leone, Liberia and Guinea means that isolation, care and tracing and monitoring contacts, which have worked before, will not halt the spread. “It may be that we have to wait for a vaccine to stop the epidemic,” he said.

On Thursday night, a Downing Street spokesman said a meeting of the government’s emergency response committee, Cobra, was told the chief medical officer still believed the risk to the UK remained low. “There was a discussion over the need for the international community to do much more to support the fight against the disease in the region,” the spokesman said. “This included greater coordination of the international effort, an increase in the amount of spending and more support for international workers who were, or who were considering, working in the region. The prime minister set out that he wanted to make progress on these issues at the European council next week.” Dr Tom Frieden, director of the Centers for Disease Control (CDC), in evidence to Congress, said he was confident the outbreak would be checked in the US, but stressed the need to halt the raging west African epidemic. “There are no shortcuts in the control of Ebola and it is not easy to control it. To protect the United States we need to stop it at its source,” he said.

How we blunder our way into disaster. Time and again.

• WHO Response To Ebola Outbreak Foundered On Bureaucracy (Bloomberg)

Poor communication, a lack of leadership and underfunding plagued the World Health Organization’s initial response to the Ebola outbreak, allowing the disease to spiral out of control. The agency’s reaction was hobbled by a paucity of notes from experts in the field; $500,000 in support for the response that was delayed by bureaucratic hurdles; medics who weren’t deployed because they weren’t issued visas; and contact-tracers who refused to work on concern they wouldn’t get paid. Director-General Margaret Chan described by telephone how she was “very unhappy” when in late June, three months after the outbreak was detected, she saw the scope of the health crisis in a memo outlining her local team’s deficiencies. The account of the WHO’s missteps, based on interviews with five people familiar with the agency who asked not to be identified, lifts the veil on the workings of an agency designed as the world’s health warden yet burdened by politics and bureaucracy.

“It needs to be a wakeup call,” said Lawrence Gostin, a professor of global health law at Georgetown University in Washington. The WHO is suffering from “a culture of stagnation, failure to think boldly about problems, and looking at itself as a technical agency rather than a global leader.” Two days after receiving the memo about her team’s shortcomings, Chan took personal command of the agency’s Ebola plan. She moved to replace the heads of offices in Guinea, Liberia and Sierra Leone, and upgraded the emergency to the top of a three-tier level, said the five people, who declined to be identified because the information isn’t public. Chan agreed to respond to their accounts in an interview. “I was not fully informed of the evolution of the outbreak,” she said today. “We responded, but our response may not have matched the scale of the outbreak and the complexity of the outbreak.”

Home › Forums › Debt Rattle October 17 2014