Pable Picasso Le Pengouin 1907

Our economies cannot function without constant new money creation by banks on the back of mortgages and other loans.

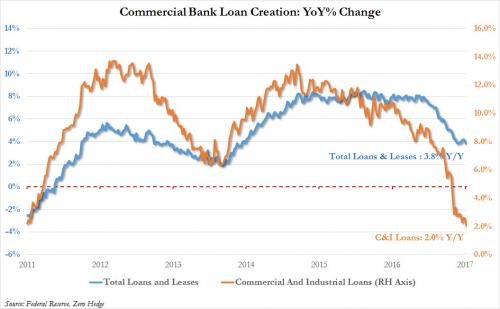

• US Loan Creation Crashes To Six-Year Low (ZH)

According to the latest Fed data, the all-important C&I loan growth contraction has not only continued, but over the past two months, another 50% has been chopped off, and what in early March was a 4.0% annual growth is now barely positive, down to just 2.0%, and set to turn negative in just a few weeks. This was the lowest growth rate since May 2011, right around the time the Fed was about to launch QE2. At the same time, total loan growth has likewise continued to decline, and as of the second week of May was down to 3.8%, the weakest overall loan creation in three years.

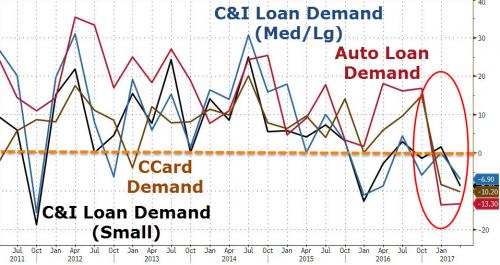

Another loan category that has seen a dramatic slowdown since last September, when Ford’s CEO aptly predicted that “sales have reached a plateau.” Since then auto loan growth has been slashed by more than 50% and at this runrate, is set to turn negative some time in late 2017. Needless to say, that would wreak even further havoc on the US car market. For a while, despite numerous attempts at explanation, there was no definitive theory why this dramatic slowdown was taking place. It even prompted the WSJ to inquire “who hit the brakes?” Well, after the latest Fed Senior Loan Officer Survey, we may have the answer.

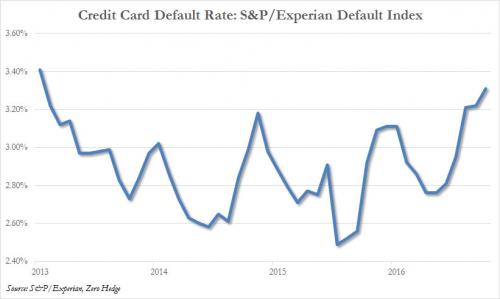

First, recall that in late April we showed another very troubling trend: consumer credit card default rate as tracked by S&P/Experian Bankcard had surged to the highest level since June 2013, suggesting that contrary to reports otherwise, the US consumer is increasingly unwell. A quick look at the latest Fed Senior Loan officer survey revealed even more disturbing trends. According to the report, “banks reported tightening most credit policies on Commercial Real Estate loans over the past year…. On balance, banks reported weaker demand for CRE loans in the first quarter.” Even more troubling was the continued drop in demand for C&I loans among small, medium and large corporations, with “inquiries for C&I lines of credit remained basically unchanged” staying at a modestly depressed rate.

This stark admission that in addition to declining bank supply due to tighter standard (i.e., worries about further losses), there was less demand by businesses and consumers for loans, has explained once and for all the ongoing collapse in commercial bank loan creation, both total, C&I and auto. Of the two, the declining demand for loans businesses, is by far the most concerning aspect of an economy that is supposedly growing, and where companies should be willing to take out new credit to fund expansion (instead of merely issuing bonds to buyback their stock).

Position very similar to US. And many others, obviously.

• UK Has All The Ingredients For A New Credit Crunch (G.)

A credit crunch is brewing and when it happens, the UK is going to get hurt. That is the message emerging from senior executives in the financial services industry, who do not think Britain has changed that much since the 2008 credit disaster and the devastating crash that followed. Three developments lie at the heart of this disturbing analysis: spectacular growth in the sale of second mortgages, car loans and credit cards. Second mortgages are widely seen as a signal of consumers taking on risky levels of debt that leave them vulnerable to a downturn in the economy. It was the same before the last banking crash. Tens of thousands of households, many of them struggling to pay monthly mortgage payments, used second mortgages to bypass borrowing limits set by their mortgage lender.

The latest industry figures show the number of people opting to saddle themselves with a second mortgage leapt 22% in March to its highest level since 2008. Car loans are already on the regulator’s radar. Like second mortgages, they are considered secured credit on the basis that lenders have a claim against an asset when borrowers can no longer pay monthly instalments. But cars depreciate from the moment they are bought, so they rank low down the scale of secure credit. And loans have turned in recent years into leases that have customers renewing contracts every three years, keeping them in effect permanently hooked. The main consumer regulator for the financial services industry, the Financial Conduct Authority, is reviewing the market for car leasing, which now accounts for more than 90% of car sales, to check for mis-selling to poorer households who will be vulnerable to default.

The Bank of England is also on the case. More importantly, it is also looking at the big picture and what happens if unemployment suddenly rises and a large number of households default on payments. Officials at the Bank have a growing list of concerns. Not only is there the second mortgage problem and the number of car loans: figures show consumer spending on unsecured credit has also rocketed in the last year. In March alone, the amount UK consumers owed on loans and cards grew by £1.9bn, the highest figure in 11 years. Households are known to have increased their reliance on short-term unsecured loans to buy cars and furniture, and to kit out new kitchens. Some use them to maintain their lifestyle in the face of a decade of flat wages.

Unfortunately, another group use credit to pay the monthly rent. Shelter, the homelessness charity, says one in three renters – around half a million people – on low incomes are having to borrow money to pay the rent. It said the borrowing is often from family and friends, but also on credit cards and through loans.

Why US mainstream media are on their last legs.

• Media To Trump: Only Cozy Up To The Right Dictators (FAIR)

After a series of friendly gestures by President Donald Trump toward Filipino President Rodrigo Duterte and Egypt’s Abdel Fattah el-Sisi over the past few months, US media have recoiled with disgust at the open embrace of governments that ostensibly had heretofore been beyond the pale. “Enabling Egypt’s President Sisi, an Enemy of Human Rights,” was the New York Times‘ editorial position (4/4/17)—followed by “Donald Trump Embraces Another Despot” (5/1/17). A week later, Sen. John McCain (R.-Ariz.) lectured Secretary of State Rex Tillerson on the Times op-ed page (5/8/17) on “Why We Must Support Human Rights.” “How Trump Makes Dictators Stronger” was Washington Post columnist Anne Applebaum’s lament (5/1/17). “Trump keeps praising international strongmen, alarming human rights advocates,” reported an upset Philip Rucker (Washington Post, 5/2/17).

Post contributor Tom Toles (5/2/17) added, “Trump invites ruthless dictators to the White House.” Trump had gone too far, was the media message, crossing a line with his enthusiastic outreach to brutal tyrants. So the Trump administration’s announcement of a plan for not just a friendly visit to Saudi Arabia—scheduled for May 20–21—but also the sale of up to $300 billion in weapons to the oppressive regime, must have provoked the same outcry from these critics, right? Actually, no. Thus far, the LA Times, CNN, NBC, MSNBC, CNN, ABC and CBS haven’t reported on Trump’s massive arms deal with Saudi Arabia, much less had a pundit or editorial board condemn it. Saudi Arabia’s war on Yemen has killed at least 10,000 civilians, resulted in near-famine conditions for 7 million people and led to a deadly cholera epidemic—all made possible with US weapons and logistical support.

John McCain, whose New York Times op-ed was unironically shared by dozens of high-status pundits, aggressively backs Saudi Arabia’s brutal bombing of Yemen, and has called for increased military support to the absolute monarchy. The New York Times hasn’t written an editorial about Saudi Arabia since October of last year (10/1/16), when, for the second time in the span of a week, the paper defended the regime against potential lawsuits over its role in the 9/11 attacks. When the Times does speak out on the topic of Saudi Arabia, it does so to run interference for its possible connection to international terrorism.

Nice words to the wrong dictators unleash a torrent of outrage from our pundit class. Nice words to the right dictators—along with billions in military hardware, which unlike nice words will be used to continue to slaughter residents of a neighboring country and suppress domestic dissent–result in uniform silence. Not a word from Anne Applebaum, no condemnation from Philip Rucker, no moral preening from Sen. John McCain, no sense that any line had been crossed from the New York Times editorial board. The US’s warm embrace and arming of the Saudis is factored in, it’s bipartisan, and thus not worthy of outrage.

NassimNicholasTaleb on Twitter:

“What @realDonaldTrump is doing: sucking in the last $100 billion before the bankruptcy of SaudiBarbaria. If anything, cruel to the Saudis.”

• America’s Cash Cow: ‘Trump Does Not Value The Saudis, Only Their Money’ (RT)

RT: Trump signed a $110-billion dollar arms deal with Saudi Arabia. How do you think this is going to be received in the US and in the wider international community?

Sharmine Narwani: Not very well. We’ve seen what the Saudis have done with arms in the last six years or so. To understand why this administration is upping arms sales to the Saudis, we have to go back a little bit. In 2010, 2011 at the start of the Arab Spring, the Saudis signed contracts for over $65 billion at that time, the largest ever. And then here we are a number of years later. And the numbers are 110, possibly up to $300 billion. And the reason behind this is basically after the failures of the US intervention in Iraq and invasion of Afghanistan, the Americans were no longer willing to sacrifice blood and treasure, and moving forward they were going to use local proxies to fight their wars. And Saudi Arabia is willing and able to fight wars in Syria, in Iraq, in Yemen on behalf of the American administration. But unfortunately, to no avail; these are not winnable wars. And at this point, I think Trump is looking at them as a cash cow.

RT: Trump says he wants to help bring peace to the Middle East. But does striking such a huge arms deal right off the bat send the right signal?

SN: Peace is a relative term. What do the Americans and what does the Trump administration mean by peace, for starters? Peace means the status quo, it means the Americans continue to exercise hegemony over the region, and that is not possible with an empire in decline. So, I think right now what we are seeing with the Trump administration headed by Jared Kushner, his son-in-law, spearheading an effort to create what they are calling the Arab NATO, which is a peace deal struck over the Israel-Palestine conflict in which the Saudis and the Gulf States and other Sunni states will agree to some kind of a solution there in order to cooperate with Israel to target Iran. So, in fact, we are going to see an escalation, not peace.

“We have today so many people sitting in the New York Times Washington office, in an air conditioned office, who can dictate foreign policy with zero risk.”

• Nassim Taleb Tells Ron Paul: “We’ll Destroy What Needs To Be Destroyed” (ZH)

Just how homogenous is the U.S. foreign policy elite? Remember that through the end of Hillary Clinton’s tenure as Secretary of State in 2013, either a Bush or a Clinton held one of the three highest offices in the U.S. – the presidency, vice presidency or secretary of state – for eight straight terms. Another reason why interventionist foreign policy often fails is because federal-government bureaucrats and other outsiders don’t have “skin in the game” – an entrenched interest, financial or of another sort, in the conflict – and therefore, are incapable of achieving a comprehensive understanding of the situation. That goes for both elected leaders, beauracrats, and the media. “We have today so many people sitting in the New York Times Washington office, in an air conditioned office, who can dictate foreign policy with zero risk.”

Dr. Paul seized the opportunity to criticize the “Chickenhawks” who advocate interventionism, but avoided serving in the military during Vietnam. “I don’t fault them for trying to avoid the war, but I fault them for advocating war,” Paul said. Many still haven’t internalized the lesson of the 2007-2008 economic crash and how the monetary policy missteps made by former Fed Chairman Alan Greenspan helped cause the crash. As a result, throughout human history, “we’ve never had so many people transferring risk to others,” Taleb asserts. One reason these actors have been allowed to remain in power is that it’s difficult to assign blame to individuals when you’re dealing with “macro” conflicts like the Syrian conflict that involve many different state actors.

This is one reason the policy elite at the State Department – whom Taleb compared to doctors from ancient times, who inflicted more harm than healing on their patients – have managed to stay in power, while a modern-day doctor who was causing an unusual number of patient deaths would quickly be barred from practicing. Turning the conversation toward the asset bubbles that have continued growing since the last crisis, Taleb explained how Greenspan’s discovery that he could stabilize markets by slashing interest rates has led to our current struggle with unprecedented debt creation and a belief in “perpetual wealth and perpetual growth.” “Lowering rates in such a manner leads to distortions. If we didn’t have a Fed, we’d be better off because the price of money would be negotiated between people.”

[..] Whatever happens to the Federal Reserve -if it’s allowed to continue monetizing debt or not – it may not matter. Because digital currencies like bitcoin, which are quickly growing in popularity and value, could one day supplant the use of fiat currencies altogether, Taleb said. During the last U.S. election, people showed that they aren’t “victims of the New York Times.” Moreover, Twitter has helped upend the media power structure in favor of the people and independent thought. “Trump was elected in spite of 264 top newspapers wanting him to lose,” Taleb noted, adding that he believes the future will be “a libertarian dream.” “We will destroy what needs to be destroyed, and build what needs to be built,” he said.

Taibbi is crawling back a little.

• How Did Russiagate Start? (Matt Taibbi)

[..] there was no way to listen to the March 5th interview and not come away feeling like Clapper believed he would have known of the existence of a FISA warrant, or of any indications of collusion between the Trump campaign and Russia, had they existed up until the time he left office on January 20th of this year. Todd went out of his way to hammer at the question of whether or not he knew of any evidence of collusion. Clapper again said, “Not to my knowledge.” Here Todd appropriately pressed him: If it did exist, would you know? To this, Clapper merely answered, “This could have unfolded or become available in the time since I left the government.” That’s not an unequivocal “yes,” but it’s close. There’s no way to compare Clapper’s statements on March 5th to his interviews last week and not feel that something significant changed between then and now.

Clapper’s statements seem even stranger in light of James Comey’s own testimony in the House on March 20th. In that appearance, Comey – who by then had dropped his bombshell about the existence of an investigation into Trump campaign figures – was asked by New York Republican Elise Stefanik when he notified the DNI about his inquiry. “Good question,” Comey said. “Obviously, the Department of Justice has been aware of it all along. The DNI, I don’t know what the DNI’s knowledge of it was, because we didn’t have a DNI – until Mr. Coats took office and I briefed him his first morning.” Comey was saying that he hadn’t briefed the DNI because between January 20th, when Clapper left office, and March 16th, when former Indiana senator and now Trump appointee Dan Coats took office, the DNI position was unfilled.

But Comey had said the counterintelligence investigation dated back to July, when he was FBI director under a Democratic president. So what happened between July and January? If Comey felt the existence of his investigation was so important that he he had to disclose it to DNI Coats on Coats’ first day in office, why didn’t he feel the same need to disclose the existence of an investigation to Clapper at any time between July and January? Furthermore, how could the FBI participate in a joint assessment about Russian efforts to meddle in American elections and not tell Clapper and the other intelligence chiefs about what would seemingly be a highly germane counterintelligence investigation in that direction?

If Corbyn doesn‘t beat May, it’ll be due to his own party members. Corbyn equals Sanders in many ways. Left wing parties, to avoid oblivion, must be drastically changed and rebuilt. But vested interests make that very hard in both the UK and US.

• Jeremy Corbyn Defies His Critics To Become Labour’s Best Hope Of Survival (G.)

In 2009 the Greek Socialist party, Pasok, entered government with 44% of the vote; by 2015 it was down to seventh, with just 5%. The party’s demise coincided with, and was arguably precipitated by, the rise of the more leftwing Syrza, which went from 5% and fifth place to 36% and government within the same period. This dual trajectory gave rise to the term Pasokification: the dramatic decline of a centre-left party that is eclipsed by a more leftwing alternative. A word was needed for it because there’s a lot of it about. Earlier this month the French Socialist party came fifth in the first round of the presidential election with just 6% of the vote, while the hard left won 20%; back in 2012 the Socialists came first with 28% and went on to win the presidency. In Holland the PvdA, the mainstream social democratic party, won 6% in March and came 7th while the GreenLeft coalition won 9%; back in 2012 the PvdA came second, with 25%.

Less pronounced versions of the same dynamic have occurred across the continent. When parties created to represent the interests of working people in parliament decide instead to make working people pay for the crisis in capital they get punished, and ultimately may be discarded. Anyone who believes that Labour is immune from this contagion just needs to take a look at Scotland, where the party went from 41 seats in 2010 to just one in 2015, before Corbyn was elected leader. To understand the Labour party’s fortunes in this election outside of this trend would be like looking at each national uprising during the Arab spring in 2011, or the collapse of Eastern bloc dictatorships in 1989, as being somehow wholly discrete from each other.

Bold move. But there’s only two weeks left.

• UK Labour Pledges To Abolish Tuition Fees As Early As Autumn 2017 (G.)

New university students will be freed from paying £9,000 in tuition fees as early as this autumn if Labour wins the election, Jeremy Corbyn will say on Monday. The Labour leader and Angela Rayner, his shadow education secretary, will say tuition fees will be completely abolished through legislation from 2018 onwards. But students starting courses in September will have fees for their first year written off retrospectively so as not to encourage them to defer their studies for a year. Labour said it would seek to provide free tuition for EU students and push for reciprocal arrangements at EU universities as part of the Brexit negotiations. Students who are partway through their courses would no longer have to pay tuition fees from 2018, meaning those starting their final year of study in September would be the last cohort liable for the £27,000 of debts to be paid back when graduates pass an earnings threshold.

Labour said those students would be protected from above-inflation interest rate rises on their debts and the party would look for ways to reduce the burden for them in future. “The Conservatives have held students back for too long, saddling them with debt that blights the start of their working lives. Labour will lift this cloud of debt and make education free for all as part of our plan for a richer Britain for the many not the few,” Corbyn will say. “We will scrap tuition fees and ensure universities have the resources they need to continue to provide a world-class education. Students will benefit from having more money in their pockets, and we will all benefit from the engineers, doctors, teachers and scientists that our universities produce.”

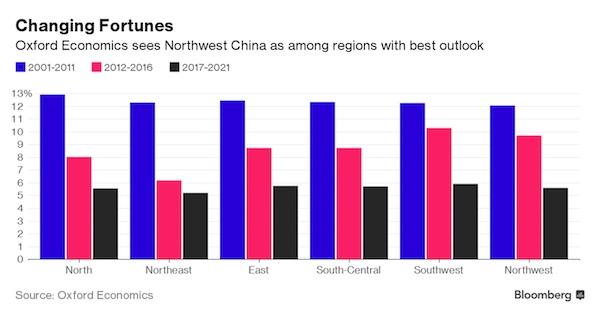

And then they run out of ‘cheaper’ areas. But at least there’s new space to build ghost cities in.

• China’s Tide Of Internal Migration Is Shifting (BBG)

Growth in China’s economy has long centered on the coast, where Shanghai and the Pearl River Delta form some of the world’s most productive regions on their own. But now that tide of internal migration that drew hundreds of millions of workers from the farm to factory is shifting, and lifting the economic prospects of the country’s interior.As big-city living costs rise and job openings become less abundant, more migrants are now leaving China’s urban centers than new ones arriving, according to Oxford Economics. “Labor costs on the East Coast are now too high for industries further down the value chain to remain competitive internationally,” London-based economist Alessandro Theiss wrote in a report, citing an 8 million decline in the migrant population from 2014 to 2016.

The shift should benefit inland provinces, especially in southwest regions like Sichuan, as companies move production to take advantage of lower costs while remaining connected to coastal export hubs and industrial clusters, he said. Southern and northwestern provinces are are likely to keep expanding relatively fast as they benefit from catch-up growth, fiscal support and geographic location, while the northeast is likely to remain the slowest-growing region as population declines and coal mining consolidates more in inland provinces, according to Theiss. While the east coast was hit by slower global trade in recent years, conditions are now improving. Specialized manufacturing clusters and export hubs are innovating and moving up the value chain, and research activity is boosting the region.

That’s good news for some of China’s biggest drivers: Coastal Guangdong, Jiangsu and Shandong provinces each account for around 10% of national output and all had output last year that exceeded Mexico’s, Theiss said. The future looks favorable for east coast provinces with more mature economies, as well as those in central China.

If “Everybody Knows Everything”, the markets must be rigged if anyone wants to make any money.

• Commodity Traders Are Stuck in a World Where Everybody Knows Everything (BBG)

For commodity traders operating in the Information Age, just good old trading doesn’t cut it anymore. Unlike the stock market in which transactions are typically based on information that’s public, firms that buy and sell raw materials thrived for decades in an opaque world where their metier relied on knowledge privy only to a few. Now, technological development, expanding sources of data, more sophisticated producers and consumers as well as transparency surrounding deals are eroding their advantage. “Everything is transparent, everybody knows everything and has access to information,” Daniel Jaeggi, the president of Mercuria Energy Group, said on Thursday at the Global Trader Summit organized by IE Singapore, a government agency that promotes international trade.

Sitting next to him at a panel discussing ‘What’s Next for Commodity Trading: Drivers, Disruptors and Opportunities’, Sunny Verghese, the chief executive officer of food trader Olam International Ltd., lamented declining margins. “The consumers and producers are trying to eat our lunch. So we got to be smart about differentiating ourselves,” he said. As market participants’ access to information increases, the traders highlighted the need to more than simply buy and sell commodities as profits from arbitrage – or gains made from a differential in prices – shrinks. That means getting involved in the supply chain by potentially buying into infrastructure that’s key to the production and distribution of raw materials, and also providing financing for the development of such assets.

Interest only loans are deadly weapons. Lots of them in various EU countries too.

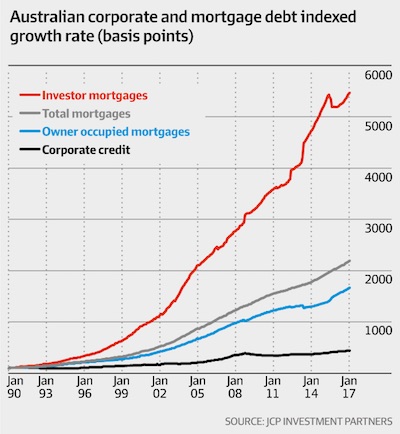

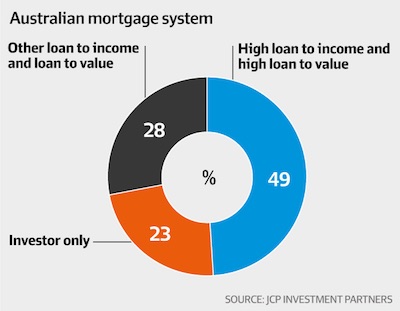

• Interest-Only Loans Could Be ‘Australia’s Subprime’ (AFR)

High-risk mortgage loans to young families, professionals and other over-extended borrowers amounting to more than six times household incomes could wipe out 20% of the major banks’ equity base, institutional investment fund JCP Investment Partners has warned. The fund manager’s study warns that official estimates of average household indebtedness are depressed by the sizeable number of mortgages that are effectively full paid off. In a proprietary study of the nation’s record high-and-growing household debt mountain, the Melbourne-based fund said Irish-style housing losses for the bigger-than-recognised pool of riskier borrowers could wipe out half of the banks’ equity capital.

It also follows a review by Australian Prudential Regulation Authority chairman Wayne Byres of bank capital requirements for housing exposures, given the “notable concentration in housing”, announced at The Australian Financial Review Banking and Wealth Summit last month. Among the biggest concerns is what may happen when households feel they can no longer service their loans, for instance, as borrowing costs are reset higher or those with interest only mortgages are forced to repay the principal as well. That creates a negative feedback loop – experienced by Ireland after the financial crisis – in which stressed borrowers slash their spending, in turn crunching the economy, driving up unemployment and adding to downward pressure on house prices.

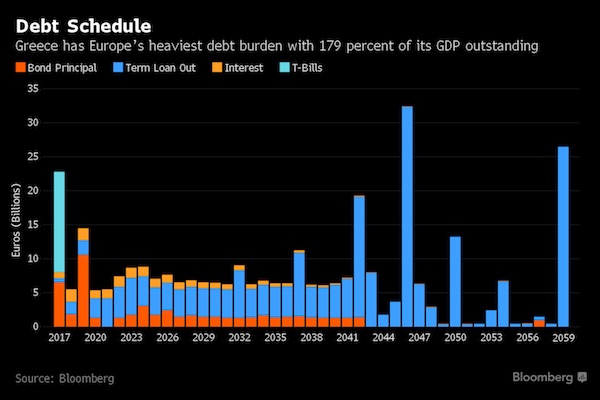

They seek to break Greece, not the impasse.

• Greek Creditors Seek to Break Impasse on Stalled Bailout Review (BBG)

Euro-area finance ministers gather in Brussels on Monday to try to clinch a deal on easing Greece’s debt burden, which would resolve a stalled review of the country’s bailout and pave the way for a new set of rescue loans. While Greece and its bailout supervisors have agreed on economic overhauls, the completion of the country’s review has been held back by disagreements between key creditors over how much debt relief is needed. At the heart of the impasse lies the IMF’s reluctance to participate in a bailout unless the euro area takes further steps to ensure the country’s €315 billion ($353 billion) debt load becomes sustainable. Some nations like Germany, which is resisting changes to Greece’s debt profile, won’t release any new funds until the IMF joins the program. Athens needs its next aid installment of around €7 billion before it has to repay lenders in July.

A global agreement on Greek debt “is within reach and it’s vital,” EU Economic and Monetary Affairs Commissioner Pierre Moscovici said in an interview on France Inter radio on Sunday. Additional debt relief is also necessary for the ECB to include Greek bonds in its asset purchases program, which would ease the country’s access to bond markets. EU officials see chances for a deal on Monday at 50-50, and point to a meeting of euro-area finance ministry deputies ahead of the ministers’ gathering, which will determine the likelihood of an accord. A key issue of contention is the outlook for Greece’s economy after 2018, when the current bailout expires. The IMF has raised doubts about Greece’s ability to maintain such an optimistic budget performance for decades, while key creditors have been pushing for a more positive outlook. Less ambitious fiscal targets would increase the amount of debt relief needed.

Celebrate capitalism. While you’re alive.

• Syphilis Is On The Rise Because Penicillin Isn’t Profitable (Qz)

At least 18 countries, including South Africa, the US, Canada, Portugal, France, and Brazil, have faced shortages of benzathine penicillin G over the last three years, according to the World Health Organization (WHO). With only a few companies in the world still manufacturing the medicine, countries can’t find enough supply of the drug that changed modern medicine 76 years ago. Penicillin was discovered in 1928, but it really took off during World War II. In the early 1940s, a US government-led program brought together around 20 commercial firms, plus government and academic research laboratories, who collaborated to scale up penicillin production to supply the military. The goal, according to the book Sickness and Health in America, was to have enough penicillin for the troops landing in France in June 1944.

In March 1945, penicillin was, for the first time, made available for consumers across the US. It’s efficacy made it popular: by 1949, the US annual production of penicillin was 1.3 trillion units—compared to the relative pittance of 1.7 billion units in 1944.\ Penicillin was one of the great achievements of modern medicine. It was the first drug of its kind, considered a miracle, and ushered in the era of antibiotics. Before penicillin, any cut could kill if it got infected; surgeries of any kind could be fatal; and bacterial infections such as strep throat could kill. Gonorrhea, syphilis, and other sexually transmitted illnesses were basically a death sentence. But a single shot of benzathine penicillin G was enough to kill the first stages of syphilis, which had plagued humankind for over 500 years. It could also cure gonorrhea and other infectious disease. Today, benzathine penicillin G is still the most effective drug against deadly diseases such as rheumatic heart disease and syphilis.

[..] Today, just four companies in the world still produce the active ingredient for benzathine penicillin G. Three are in China: North China Pharmaceutical; CSPC Pharmaceuticals; Jiangxi Dongfeng Pharmaceutical. Austria-based Sandoz is the only producer of the active ingredient for benzathine penicillin G in the Western world. Together, these producers have the capacity to deliver up to 600 metric tons of benzathine penicillin G a year, but they produce less than 20% of that. “There is no money in penicillin,” says Amit Sengupta, the New Delhi-based global coordinator of the People’s Health Movement. A shot of benzathine penicillin G typically costs between $0.20 and $2.00, and usually all you need is one—strep throat and syphilis are both cured with a single injection of penicillin.

Home › Forums › Debt Rattle May 22 2017