Ted Russell James Baldwin and Bob Dylan 1963

Very true of course, but what’s this worth coming from a polarized view?

• America Is Racing Toward Peak Polarization (NYMag)

There is a venerable, centrist point of view that partisan polarization is a function of Washington’s warring politicians, who inflate artificial differences into causes for political war. Out there in the country, it is thought, Americans simply want politicians to come together and work out sensible, centrist policies. Whatever this gospel’s general applicability, it is increasingly clear that in the era of Donald Trump it’s The People who are even more polarized than their representatives in Washington. A new poll from Morning Consult for Politico has this jarring news: after the president’s first overseas trip, his job approval ratings rose. But so, too, did the percentage of Americans who want impeachment proceedings against him to begin post-haste.

Indeed, we are rapidly approaching the point where Americans are basically divided between those who think the president’s doing a good job (45% at present), and those who think he should be removed from office before his first term ends (43% at present). Unsurprisingly, these sentiments closely match partisan preferences. According to this same poll, 82% of self-identified Republicans approve of Trump’s job performance, 46% of them strongly. 79% of self-identified Democrats disapprove of Trump’s job performance, 65% of them strongly. These grassroots Americans are really, really at odds. That becomes even more obvious when the possibility of impeachment is introduced. Seventy-one% of Democrats want Congress to initiate impeachment proceedings.

Over half of these impeachment supporters say he’s unfit to serve, whether or not he has committed an impeachable offense. 76% of Republicans oppose the idea. For all the talk about anti-Trump Republicans and moderate Democrats, the truth is there is not a lot of support out there for anything other than the highly partisan approach Trump and the congressional GOP have taken this year, and for what some Democrats have called “the resistance.”

Empty bags can get heavy.

• US Middle Class Is Now The Company Store Class (Michael Hudson)

Students usually don’t think of themselves as a class. They seem “pre-class,” because they have not yet entered the labor force. They can only hope to become part of the middle class after they graduate. And that means becoming a wage earner – what impolitely is called the working class. But as soon as they take out a student debt, they become part of the economy. They are in this sense a debtor class. But to be a debtor, one needs a means to pay – and the student’s means to pay is out of the wages and salaries they may earn after they graduate. And after all, the reason most students get an education is so that they can qualify for a middle-class job. The middle class in America consists of the widening sector of the working class that qualifies for bank loans – not merely usurious short-term payday loans, but a lifetime of debt.

So the middle class today is a debtor class. Shedding crocodile tears for the slow growth of U.S. employment in the post-2008 doldrums (the “permanent Obama economy” in which only the banks were bailed out, not the economy), the financial class views the role industry and the economy at large as being to pay its employees enough so that they can take on an exponentially rising volume of debt. Interest and fees (late fees and penalties now yield credit card companies more than they receive in interest charges) are soaring, leaving the economy of goods and services languishing. Although money and banking textbooks say that all interest (and fees) are a compensation for risk, any banker who actually takes a risk is quickly fired. Banks don’t take risks. That’s what the governments are for. (Socializing the risk, privatizing the profits.)

Anticipating that the U.S. economy may be unable to recover under the weight of the junk mortgages and other bad debts that the Obama administration left on the books in 2008, banks insisted that the government guarantee all student debt. They also insisted that the government guarantees the financial gold-mine buried in such indebtedness: the late fees that accumulate. So whether students actually succeed in becoming wage-earners or not, the banks will receive payments in today’s emerging fictitious “as if” economy. The government will pay the banks “as if” there is actually a recovery. And if there were to be a recovery, then it would mean that the banks were taking a risk – a big enough risk to justify the high interest rates charge on student loans.

This is simply a replay of what banks have negotiated for real estate mortgage lending. Students who do succeed in getting a job hope to start a family, or at least joining the middle class. The most typical criterion of middle-class life in today’s world (apart from having a college education) is to own a home. But almost nobody can buy a home without getting a mortgage. And the price of such a mortgage is to pay up to 43% of one’s income for thirty years, that is, one’s prospective working life (in today’s as-if world that assumes full employment, not just a gig economy).

Boy, is she doing a bad job. Calling an election and not showing up. And yeah, we get it: if she would show up, numbers would be even worse. On Twitter: “A Ladbrokes customer in Chelsea has just had £2,000 at 100/1 for Boris Johnson to be PM on July 1st. #GE2017”

• Theresa May’s Lead Slashed To Record Low Of Three Points In New Poll (Ind.)

Labour is closing the gap with Tories and now stands just three points from Theresa May’s party, a new YouGov poll shows. The poll, commissioned by The Times, found the Conservative lead has slipped dramatically in recent weeks and is now within the margin of error. The figures show the Conservatives on 42 points but Labour are close behind on 39. Meanwhile, the Liberal Democrats are struggling to maintain the momentum of their “fightback” as they slip to just 7% vote share. The poll points to a remarkable change in fortunes for the Tories, which had a 24-point lead over Labour when the snap general election was called in April. Ms May has struggled in recent weeks after she was forced into an embarrassing U-turn over plans to reform social care in the party’s manifesto.

The party said elderly people who needed care will be able to put off playing for it until after their deaths so they could potentially stay in their own home for as long as possible. But critics said this would unfairly penalise people who suffer a slow decline from illnesses like dementia, over people who die suddenly and can then leave their estate to their children. Ms May has faced criticism for refusing to to engage with voters, especially after she declined to take part in televised debates. During the debate, Green party leader Caroline Lucas said: “You don’t call a general election and say it is the most important election in her lifetime and then not even be bothered to debate the issues at hand.” She added: “I think the first rule of leadership is to show up.”

Fitting comment on Twitter to the original title “Three minutes of nothing”: “Does this pass the Turing test?”

• Does Theresa May Pass The Turing Test? (PH)

Before 8.30am today, I had never interviewed a Prime Minister. Heading back to the office to transcribe my encounter with Theresa May at Plymouth’s fish market, I couldn’t be certain that had changed. To start with, it was quite an exciting experience. We got the call late on Tuesday night, and the visit was kept totally secret until her arrival. We waited in the drizzle as she chatted with fishermen and nodded earnestly at nets and buckets, leopard print heels click-clacking on the harbour floor. ired-looking campaign managers hurried back and forth, mulling over our request for a filmed interview which had been denied on her previous visit. Then suddenly we were on. I had a list of four questions, all on local issues, carefully prepared with the help of my newsroom colleagues.

Two visits in six weeks to one of the country’s most marginal constituencies – is she getting worried?

May: “I’m very clear that this is a crucial election for this country.”

Plymouth is feeling the effects of military cuts. Will she guarantee to protect the city from further pain?

May: “I’m very clear that Plymouth has a proud record of connection with the armed forces.”

How will your Brexit plan make Plymouth better off?

May: “I think there is a better future ahead for Plymouth and for the whole of the UK.”

Will you promise to sort out our transport links?

May: “I’m very clear that connectivity is hugely important for Plymouth and the South West generally.”

I was pleased to have secured the interview and happy to have squeezed all my points in. But no sooner had the ministerial car pulled away from Sutton Harbour than I began to feel a bit deflated. If the ultimate job of a journalist is to get answers, I had failed. Should I have stopped her and demanded she be more specific? Could I have gone full angry Paxman, or brought the interview to an abrupt close in protest? Back at the office, we scratched our heads and wondered what the top line was. She had and given me absolutely nothing. It was like a postmodern version of Radio 4’s Just A Minute. I pictured Nicholas Parsons in the chair: “The next topic is how Plymouth will be affected by Brexit, military cuts and transport meltdown. Theresa, you have three minutes to talk without clarity, candour or transparency. Your time starts now.”

No, Theresa May in reality is not so funny or innocent.

• Terror In Britain: What Did The Prime Minister Know? (John Pilger)

The unsayable in Britain’s general election campaign is this. The causes of the Manchester atrocity, in which 22 mostly young people were murdered by a jihadist, are being suppressed to protect the secrets of British foreign policy. Critical questions – such as why the security service MI5 maintained terrorist “assets” in Manchester and why the government did not warn the public of the threat in their midst – remain unanswered, deflected by the promise of an internal “review”. The alleged suicide bomber, Salman Abedi, was part of an extremist group, the Libyan Islamic Fighting Group, that thrived in Manchester and was cultivated and used by MI5 for more than 20 years. The LIFG is proscribed by Britain as a terrorist organisation which seeks a “hardline Islamic state” in Libya and “is part of the wider global Islamist extremist movement, as inspired by al-Qaida”.

The “smoking gun” is that when Theresa May was Home Secretary, LIFG jihadists were allowed to travel unhindered across Europe and encouraged to engage in “battle”: first to remove Mu’ammar Gadaffi in Libya, then to join al-Qaida affiliated groups in Syria. Last year, the FBI reportedly placed Abedi on a “terrorist watch list” and warned MI5 that his group was looking for a “political target” in Britain. Why wasn’t he apprehended and the network around him prevented from planning and executing the atrocity on 22 May? These questions arise because of an FBI leak that demolished the “lone wolf” spin in the wake of the 22 May attack – thus, the panicky, uncharacteristic outrage directed at Washington from London and Donald Trump’s apology.

The Manchester atrocity lifts the rock of British foreign policy to reveal its Faustian alliance with extreme Islam, especially the sect known as Wahhabism or Salafism, whose principal custodian and banker is the oil kingdom of Saudi Arabia, Britain’s biggest weapons customer. This imperial marriage reaches back to the Second World War and the early days of the Muslim Brotherhood in Egypt. The aim of British policy was to stop pan-Arabism: Arab states developing a modern secularism, asserting their independence from the imperial west and controlling their resources. The creation of a rapacious Israel was meant to expedite this. Pan-Arabism has since been crushed; the goal now is division and conquest.

“The BoE has busted a gut to keep the mortgage market afloat with one scheme after another to subsidise everything from deposits to the lenders themselves. It must have been upsetting to see a fall in approvals for house purchases in April for the third month in a row.”

• UK Policymakers Face A Dilemma Over Public’s Slowing Demand For Credit (G.)

As the election on 8 June nears, the debate has intensified over how much Britain’s frothy cappuccino-drinking economy can cope without endless dollops of interest-free credit. Financial regulators are worried about it. So are the debt charity workers who pick up the pieces when the debt merry-go-round grinds to a halt. And they should be worried. Many of the biggest, shiniest new cars zipping round UK streets would still be sitting on the garage forecourt without ultra cheap credit deals that rival mortgages for their rock-bottom rates. On the high street, shops have in recent years relied more heavily on consumers using their credit cards for big purchases. Back in 2014 these shoppers could avoid paying the 18.9% interest commonly applied to credit card balances and use the two, even three-year interest-free period many card operators allow.

As we know from recent experience, when debt bubbles burst, they hit everyone and drag the economy down into recession. The Bank of England’s most recent data for April shows that the mania for borrowing last year and the year before has paused somewhat since January. That should be seen as good news. Net mortgage lending is down at levels seen a year ago while unsecured borrowing on credit cards and loans has stabilised at a growth rate of of just over 10% a year. But not everybody at the Bank of England will be content to see consumers putting their credit cards in a drawer. The economists attached to the BoE’s interest rate-setting committee know the economy runs on debt. To adapt a well-known first world war poster, they know Britain needs borrowers. If a reminder of this basic economic rule was needed, it was made clear earlier this month when the latest UK GDP figures appeared.

The relative lack of borrowing in the first three months of the year coincided with a dive in GDP growth from 0.7% in the final quarter of 2016 to 0.2% in the first quarter of this year. The BoE has busted a gut to keep the mortgage market afloat with one scheme after another to subsidise everything from deposits to the lenders themselves. It must have been upsetting to see a fall in approvals for house purchases in April for the third month in a row. Now there are signs that the credit habit is returning as almost zero interest rates work their magic again, Easter’s spending is out of the way and wage rises are being outpaced by inflation. Analysts say GDP growth in Q2 will be higher for this very reason. Is that a return of consumer confidence with shoppers shrugging off the election, they ask? Or is it, as the debt charities suspect, cash-strapped consumers rolling over their debts and taking out a bit more credit just to get by?

Yes, if you can’t get people to go deeper into debt, your growth shrinks. That’s economics these days.

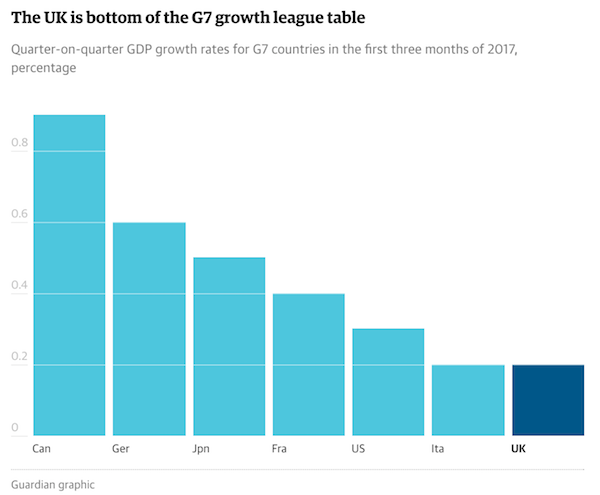

• UK Comes Bottom Of G7 Growth League, Canada Takes Lead (G.)

The UK has slumped to the bottom of the league table of advanced economies after Canada registered stellar growth in the first three months of the year. Canada was the final member of the G7 to report its growth figures, which confirmed the UK as officially the joint worst performing member so far this year. The announcement marked a significant decline for the UK economy, which a year ago was outshining Germany, the US and Japan. In February it was announced that Germany had pipped the UK as the fastest-growing G7 nation during 2016 by 10 basis points. However, the latest figures for Canada, which showed that growth accelerated to 0.9% in the first quarter, putting it top of the G7 performers, has left Britain languishing alongside Italy at the bottom of the table.

Germany is in second spot at 0.6%, followed by Japan with 0.5%, France 0.4% and the US at 0.3%. The UK and Italy are then level on growth of just 0.2%. The sluggish expansion in the first quarter provides the latest evidence that the early resilience to the EU referendum result last June is now wearing off as higher inflation puts consumers under pressure. Prices have been increasing since the Brexit vote because the referendum result sent the pound sharply lower and has raised the cost of imports to the UK. That higher inflation has hit household budgets and dented the main driver of UK growth, consumer spending. The Bank of England said earlier this month that it expected GDP growth would edge up marginally to 1.9% for 2017 from 1.8% in 2016. But it warned that living standards would fall this year because inflation would be higher than pay growth.

NATO needs enemies or it will disappear.

• Europe May Finally Rethink NATO Costs (McGovern)

President Donald Trump’s politically incorrect behavior at the gathering of NATO leaders in Brussels on Thursday could, in its own circuitous way, spotlight an existential threat to the alliance. Yes, that threat is Russia, but not in the customary sense in which Westerners have been taught to fear the Russian bear. It is a Russia too clever to rise to the bait – a Russia patient enough to wait for the Brussels bureaucrats and generals to fall of their own weight, pushed by financial exigencies in many NATO countries. At that point it will become possible to see through the West’s alarmist propaganda. It will also become more difficult to stoke artificial fears that Russia, for reasons known only to NATO war planners and neoconservative pundits, will attack NATO. As long as Russian hardliners do not push President Vladimir Putin aside, Moscow will continue to reject its assigned role as bête noire.

First a request: Let me ask those of you who believe Russia is planning to invade Europe to put down the New York Times for a minute or two. Take a deep cleansing breath, and try to be open to the possibility that heightened tensions in Europe are, rather, largely a result of the ineluctable expansion of NATO eastward over the quarter-century since the Berlin Wall fell in 1989. Actually, NATO has doubled in size, despite a U.S. quid-pro-quo promise in early 1990 to Russian leader Mikhail Gorbachev in early 1990 not to expand NATO “one inch” to the east of Germany. The quid required of Russia was acquiescence to a reunited Germany within NATO and withdrawal of the 300,000-plus Russian troops stationed in East Germany.

The US reneged on its quo side of the bargain as the NATO alliance added country after country east of Germany with eyes on even more – while Russia was not strong enough to stop NATO expansion until February 2014 when, as it turned out, NATO’s eyes finally proved too big for its stomach. A U.S.-led coup d’etat overthrew elected President Viktor Yanukovych and installed new, handpicked leaders in Kiev who favored NATO membership. That crossed Russia’s red line; it was determined – and at that point able – to react strongly, and it did.

No, Bloomberg, spending more is not an answer to any serious question.

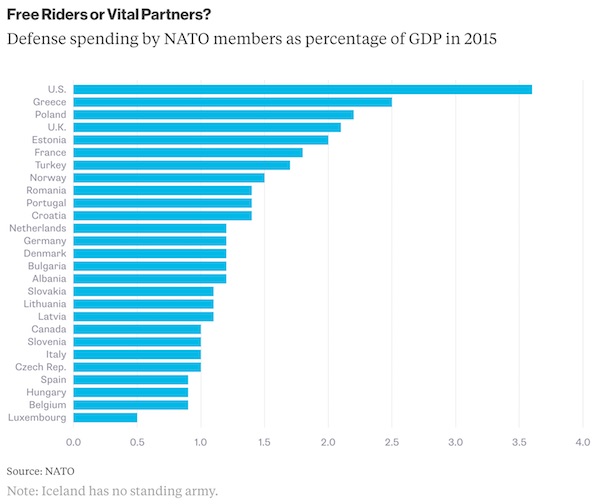

• NATO Allies Can Spend More Money, More Wisely (BBG)

If Donald Trump and Barack Obama agree on something, does that mean it’s true? In the case of Europe’s woeful support of its collective defense, yes: Member states need to contribute their “fair share” toward the North Atlantic Treaty Organization, a phrase both men used in speeches in European capitals. The question is what “fair share” means. Instead of measuring how much member nations spend on their defense, NATO should pay more attention to how they spend it. The current definition – members are expected to spend at least 2% of GDP on defense – is both misleading and unfair. Currently, only four European members meet the alliance’s target and things are going the wrong direction. Across Europe, including non-NATO members, military spending as a percentage of GDP has dropped by almost 9% in the last five years.

But some kinds of military spending are better than others. Money for major training exercises, or transport planes and helicopters for airlift operations, is far more valuable than lots of spending on ill-equipped troops in glorified jobs programs. Spending on national defense is always going to reflect national priorities. That said, better coordination among member nations can bolster both their security and the alliance’s. A wealthy nation may want some shiny new fighter jets, but the collective defense may be better served by more prosaic equipment such as refueling tankers. To their credit, not only have the alliance’s newer members such as the Baltic States been paying up, they’ve been helpful in buying what NATO most needs. Arriving at a consensus as to what constitutes useful spending among 28 separate militaries would be contentious and difficult, to put it mildly. It would still be a useful exercise.

Flip flop. Up down.

• Oil Prices Crushed As Traders Bet Against OPEC, Russia (CNBC)

The oil market has serious doubts that the production deal between OPEC and Russia is sufficient enough to bring the world oil market back into balance, against a potential wave of new supply. As a result, traders appeared to be adding to short positions, as crude fell sharply Wednesday morning, analysts said. The decline in oil prices was triggered by news that Libya had increased its production to a three-year high of 827,000 barrels a day. “The game of chicken between them and the market is back on again,” said John Kilduff, partner at Again Capital. West Texas Intermediate crude for July settled off 2.7%, at $48.32 per barrel after briefly breaking $48. Brent, the international benchmark, dipped temporarily below the psychological $50 for the first time in two weeks, and was down 3% at $50.66 in afternoon trading.

Last week, Saudi Arabia and other members of OPEC agreed with Russia and other producers to extend their agreement to cut back output by 1.8 million barrels a day for another nine months. But market expectations had been hinging on the idea that producers would take even more barrels off the market because of the overhang of supply. Oil plunged 5% last Thursday, after the announcement. “The meeting was much more of a failure than people realize because of what wasn’t achieved. There are no caps on production for Libya, or Nigeria, or Iran,” said Kilduff. Libya has shipped an average of 500,000 barrels per day of oil so far this year, up from 300,000 per day last year. Production reached 800,000 barrels per day earlier this month.

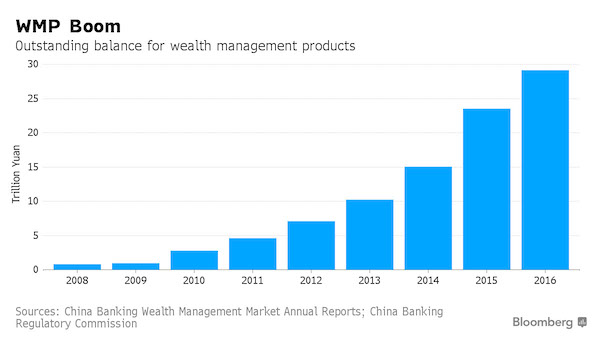

“Shadow bank run” is a good way to put it. I’ve been warning about Chinese shadown banking for years, and I haven’t been wrong. Baidu is a search engine, for pete’s sake… which “does not need to set aside large capital against potential defaults on its WMPs”… Beijing facilitates the shadows, and they in turn lend into the economy what Beijing’s state banks can’t do without raising bright red alarms.

• Fitch Warns Baidu Faces “Default Risk” Due To Growing Shadow Banking Business (ZH)

Less than a week after Moody’s downgraded China’s sovereign credit rating, prompting an unprecedented currency response by the PBOC which as noted earlier resumed its crusade against Yuan shorts by sending CNH overnight deposit rates as high as 65%, on Wednesday another rating agency, Fitch, took aim at what many consider the weakest link in China’s financial system: the nearly $9 trillion in shadow banking “assets”, of which roughly $4 billion are Wealth Management Products. Just as surprising was the target of Fitch’s wrath: none other than China’s tech giant Baidu, which Fitch put on “negative watch” warning that the company’s financial services division faced increased risk of default as a result of its growing reliance on shadow banking in general and Wealth Management Products (WMPs) in particlar.

As reported previously, China’s popular WMPs offer a higher yielding alternative to conventional financial instruments by bundling together investments into money market bonds, corporate loans and many other products, all of which are usually a mystery to the buyer. As of 2016, China had nearly 30 trillion yuan outstanding in WMPs. Baidu, China’s dominant search engine, has not been immune to the scramble for funding optionality provided by shadow banking alternatives, and has been getting into the WMP game by rapidly expanding its Financial Services Group, which Fitch says is increasing Baidu’s overall business risk. While Baidu is not under obligation to pay the returned target on these products, a failure could be potentially damaging to Baidu’s reputation, Fitch warned.

“As with Chinese banks, Baidu does not need to set aside large capital against potential defaults on its WMPs … WMPs have become an alternative form of financing for projects or investments that would not qualify for bank loans,” Fitch said. This could lead to an increased risk of default or “shadow bank run”, since many of the bundled assets are of poor quality and would not qualify for bank loans. The WMP warning from Fitch came less than two weeks after Moody’s also put Baidu’s corporate debt on watch for a potential downgrade. WMPs have been behind the staggering surge in total assets of Baidu’s Financial Services Group, which have more than doubled to CNY25 billion in the period ended April 2017.

Home › Forums › Debt Rattle June 1 2017