Walter Langley Never morning wore to evening but some heart did break 1894

If there’s one myth -and there are many- that we should invalidate in the cross-over world of politics and economics, it‘s that central banks have saved us from a financial crisis. It’s a carefully construed myth, but it’s as false as can be. Our central banks have caused our financial crises, not saved us from them.

It really should -but doesn’t- make us cringe uncontrollably to see Bank of England governor-for-hire Mark Carney announce -straightfaced- that:

“A decade after the start of the global financial crisis, G20 reforms are building a safer, simpler and fairer financial system. “We have fixed the issues that caused the last crisis. They were fundamental and deep-seated, which is why it was such a major job.”

Or, for that matter, to see Fed chief Janet Yellen declare that there won’t be another financial crisis in her lifetime, while she’s busy-bee busy building that next crisis as we speak. These people are now saying increasingly crazy things, and that should make us pause.

Central banks don’t serve people, or even societies, as that same myth claims. They serve banks. Even if central bankers themselves believe that this is one and the same thing, that doesn’t make it true. And if they don’t understand this, they should never be let anywhere near the positions they hold.

You can pin the moment central banks went awry at any point in time you like. The Bank of England’s foundation in 1694, the Federal Reserve’s in 1913, the ECB much more recently. What’s crucial in the timing is where and when the best interests of the banks split off from those of their societies. Because that is when central banks will stop serving those societies. We are at such a -turning?!- point right now. And it’s been coming for some time, ‘slowly’ working its way towards an inevitable abyss.

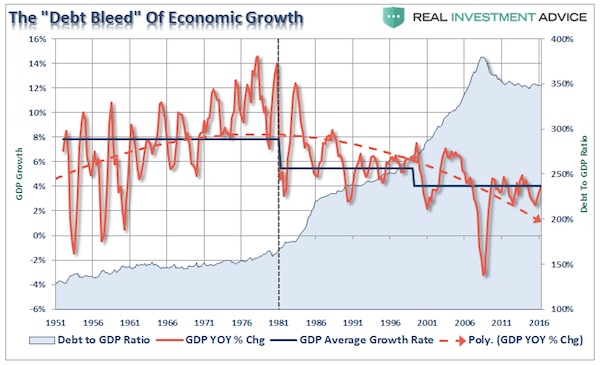

Over the past few years the Automatic Earth has argues repeatedly, along several different avenues, that American society was at its richest between the late 1960s and early 1980s. Yet another illustration of this came only yesterday in a Lance Roberts graph:

Anyone see a recovery in there? Lance uses 1981 as a ‘cut-off’ date, but the GDP growth rate as represented by the dotted line doesn’t really begin to go ‘bad’ until 1986 or so. At the tail end of the late 1960s to early 1980s period, as the American economy was inexorably getting poorer, Alan Greenspan took over as Federal Reserve governor in 1987. A narrative was carefully crafted by and for the media with Greenspan as an ‘oracle’ or even a ‘rock star’, but in reality he has been instrumental in saddling the economy with what will turn out to be insurmountable problems.

Greenspan was a major driving force behind the repeal of Glass-Steagall, which was finally established through the Gramm-Leach-Bliley act of 1999. This was an open political act by the Federal Reserve governor, something that everyone should have then protested, and still should now, but didn’t and doesn’t. Central bankers should be kept far removed from politics, anywhere and everywhere, because they represent a small segment of society, banks, not society as a whole.

Because of the ‘oracle’ narrative, Greenspan was instead praised for saving the world. But all that Greenspan and his accomplices, Robert Rubin and Larry Summers, actually did in getting rid of the 1933 Glass-Steagall act separation between investment- and consumer banking was to open the floodgates of debt, and even more importantly, leveraged debt. All part of the ‘financial innovations’ Greenspan famously lauded for saving and growing economies. It was all just more debt on top of more debt.

Greenspan et al ‘simply’ did what central bankers do: they represent the best interests of banks. And the world’s central bankers have never looked back. That most people still find it hard to believe that America -and the west- has been getting poorer for the past 30-40 years, goes to show how effective the narratives have been. The world looks richer instead of poorer, after all. That this is exclusively because of rising debt numbers wherever you look is not part of the narratives. Indeed, ruling economic models and theories ignore the role played by both banks and credit in an economy, almost entirely.

Alan Greenspan left as Fed head in 2006, after having wreaked his havoc on America for almost two decades, right before the financial crisis that took off in 2007-2008 became apparent to the world at large. The crisis was largely his doing, but he has escaped just about all the blame for it. Good PR.

With Ben Bernanke, an alleged academic genius on the Great Depression, as Greenspan’s replacement, the Fed just kept going and turned it up a notch. It was no longer possible in the financial world to pretend that banks and people had the same interests, so the former were bailed out at the expense of the latter. The illusionary narrative for the public, however, remained intact. What do people know about finance, anyway? Just make sure the S&P goes up. Easy as pie.

The narrative has switched to Bernanke, and Yellen after him, as well as Mario Draghi at the ECB and Haruhiko Kuroda at the Bank of Japan, saving the world from doom. But once again, they are the ones who are creating the crisis, not the ones saving us from it. They are saving the banks, and saddling the people with the costs.

In the past decade, these central bankers have purchased $20-$50 trillion in bonds, securities and stocks. The only intention, and indeed the only result, is to keep banks from falling over, increase their profits, and maintain the illusion that economies are recovering and growing.

They can only achieve this by creating bubbles wherever they can. Apart from the QE programs under which they bought all those ‘assets’, they used -and still do- another tool: lowering interest rates to the point where borrowing money becomes so cheap everyone can do it, and then do it some more. It has worked miracles in blowing stock market valuations out of all realistic proportions, and in doing the same for housing markets in locations all over the globe.

The role of China’s central bank in this is interesting too, but it is such an open and obvious political tool that it really deserves its own discussion and narrative. Basically, Beijing did what it saw Washington do and thought: why hold back?

Fast forward to today and we see that we’ve landed in a whole new, and next, phase of the story. The world’s central banks are all stuck in their own – self-created – bubbles and narratives. They all talk about how they solved all the issues, and how they will now return to normal, but the sad truth is they can’t and they know it.

The Fed stopped purchasing assets through its QE program a while back, but it could only do that because Frankfurt and Japan took over. And now they, too, talk about quitting QE. Slowly, yada yada, because of control, yada yada, but they know they must. They also know they can’t. Because the entire recovery narrative is a mirage, a fata morgana, a sleight of hand.

And that means we have arrived at a point that is new and very dangerous for the entire global economy and all of its people.

That is, the world’s central bankers now have an incentive to create the next crisis. This is because they know this crisis is inevitable, and they know their masters and protégés, the banks, risk suffering immensely or even going under. ‘Tapering’, or whatever you might call the -slow- end to QE and the -slow- hiking of interest rates, will prick and blow up bubbles one by one, and often in violent fashion.

When housing bubbles burst, economies lose the primary ingredient for maintaining -let alone increasing- their money supply: banks creating money out of thin hot air. Since the money supply is one of the key components of inflation, along with velocity of money, there will be fantastic outbursts of debt deflation. You’ve never seen -let alone imagined- anything like it.

The worst part of it is not government debt, though that, when financed with bond sales, is not not an instrument to infinity and beyond either. But the big hit to economies will be private debt. Where in many bubble areas, and they’re too numerous too mention, eager potential buyers today fret over affordable housing supply, it’ll all turn on a dime and owners won’t be able to sell without being suffocated by crippling losses.

Pension funds, which have already suffered perhaps more than any other parties because of low interest ZIRP and NIRP policies, have switched en masse to riskier assets like stocks. Well, another whammy, and a bigger one, is waiting just outside the door. Pensions will be so last century.

That another crisis is waiting to happen, and that politics and media have made sure that just about no-one at all is aware of it, is one thing. We already knew this, a few of us. That the world’s main central bankers have an active incentive to bring about the crisis, if only by sitting on their hands long enough, is new. But they do.

Yellen, Draghi and Kuroda may opt to leave before pulling the trigger, or be fired soon enough. But whoever is in the governor seats will realize that unleashing a crisis sooner rather than later is the only option left not to be blamed for it. Let the house of dominoes crumble now, and they can say “nobody could have seen this coming”, while at the same time saving what they can for the banks and bankers they serve. That option will not be on the table for much longer.

We should have never given them, let alone their member/master banks, the power to conjure up trillions out of nothing, and use that power as a political tool. But it is too late now.

Home › Forums › Central Banks ARE The Crisis