Gertrude Käsebier Young negro woman, Newport, Rhode Island 1902

And it never will be.

• Wall Street Isn’t Ready For A 1,100-Point Tumble In The Dow Industrials (MW)

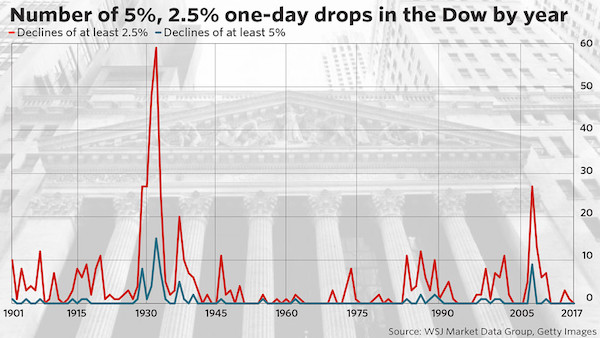

The U.S. stock market has been on such a parabolic march higher that Wall Street investors may have forgotten what a typical, sharp downturn feels like. Indeed, much has been made about the lack of volatility. The CBOE Volatility Index otherwise known as the “fear gauge,” had been flirting with its lowest close on record, implying that market expectations for a sharp, sudden fall are near rock bottom, as the Dow Jones Industrial Average, S&P 500 and the Nasdaq Composite Index scale new heights. (The Dow notched a fresh record on Friday to end the week 1.2% higher.) The recent level of complacency permeating the market has pundits talking about the lack of 5% falls in the market—an occurrence that isn’t unusual in a normal market environment. However, a 5% tumble, while normal, isn’t that common either. It has occurred at least 75 times over the course of the blue-chip index’s, according to WSJ Market Data Group, using data going back to 1901.

The Dow, however, hasn’t experienced a 5% decline since 2011, and before that a 5% drop hadn’t happened since 2008, when there were 9 such drops: At this point, with the Dow just 200 points shy of 22,000, a 5% selloff would equate to a 1,100-point, one-day slide in the gauge. Is the market ready for that sort of sudden jolt lower, given the optics of a quadruple-digit downturn and how it might rattle investment psyche? Art Hogan, chief market strategist at Wunderlich Securities, doesn’t think so. “I would say no because we’re out of practice. Your usual standard garden-variety volatility just hasn’t been around, and we haven’t seen it for 12 months,” Hogan told MarketWatch. “Quiet markets have been the norm and not the exception and I think a major pullback is going to feel a whole lot larger for lack of experience and the numbers are larger,” he said.

Even a 2.5% drop in the Dow, adding up a 550-point decline, could be unsettling, market participants said. Those sorts of tumbles are far more frequent, with 564 such moves of that magnitude occurring in the Dow since 1901. The most recent slump of at least 2.5% was on June 24, 2016, when the Dow tumbled about 610 points, or 3.4%, a day after U.K. citizens voted to end the country’s membership in the EU. There were 3 falls for the Dow of at least 2.5% in 2015. Hogan said it is even hard to imagine what the landscape of the market would like in the face of a plunge of the same magnitude of the 1987 crash, when the Dow lost 22.6% of its value, or 508 points, in a single session. “That’s why it is hard for investors to think about it intuitively. We have no muscle memory for it. It’s hard to harken back to 30 years ago. We have been lulled to sleep,” he said.

What always happpens when everyone is on the same side of the boat.

• Dangerous Game: Shorting the VIX (Barron’s)

As stocks keep dancing around record highs, and the CBOE Volatility Index remains historically low, some investors are preparing for a violent end to one of the world’s most popular trades: shorting volatility. A one-day Standard & Poor’s 500 correction of 3% to 4% could force some funds that short futures on the index, such as the ProShares Short VIX Short-term Future s exchange-traded fund (ticker: SVXY) and the VelocityShares Daily Inverse VIX ST ETN (XIV), to cover their positions. That could make the VIX skyrocket. If the weighted-average of 30-day VIX futures sharply jumped—say by 80% in one day—it would, in turn, trigger an “acceleration event” that would force more funds to buy back short VIX futures contracts. Some VIX funds could face margin calls.

And a chain reaction would likely explode across the volatility spectrum and ultimately the stock market, pushing down share prices and boosting volatility further. So many institutional investors use strategies that increase portfolio leverage as equity volatility declines that Marko Kolanovic, JPMorgan’s top quantitative strategist, fears the markets are nearing a turning point. “While these strategies include concepts like ‘risk control’, ‘crisis alpha’, etc. in various degrees they rely on selling into market weakness to cut losses. This creates a ‘stop-loss order’ that gets larger in size and closer to the current market price as volatility gets lower,” Kolanovic wrote last week. The S&P 500’s realized volatility–the level that’s materialized already—is the lowest since 1966. That influences expectations for future, or implied, volatility.

In fact, CBOE Volatility Index levels are so meager that relatively small point moves can create big percentage changes, creating a major problem for VIX funds. “The one-day percentage change is a big deal in the VIX complex because the levered and inverse VIX ETFs and ETNs rebalance daily, based on the percentage change, and some of the thresholds for forced [unwinding of positions] are based on the percentage change. This is why lower volatility creates higher risk,” Christopher Metli, a Morgan Stanley quantitative derivatives strategist, recently warned clients.

But Draghi gets praised for saving the EU economy. Well, you can’t have it both ways. Decide.

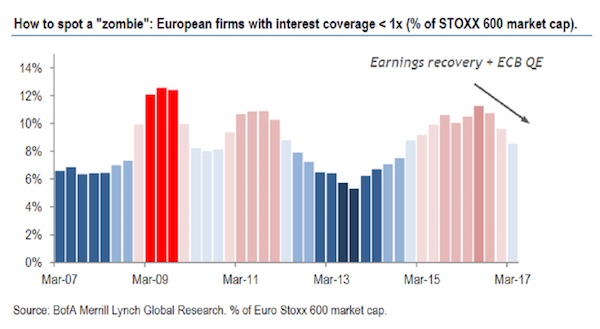

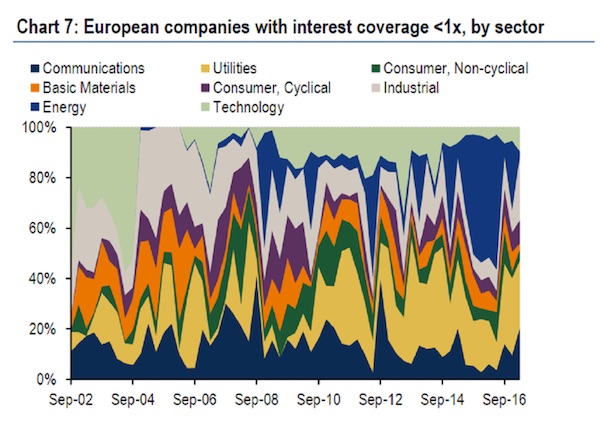

• Zombie Companies Littering Europe May Tie the ECB’s Hands for Years (BBG)

Watch out for the zombies. The plethora of companies propped up by the ECB will limit policy makers’ ability to withdraw monetary stimulus that’s been supporting the continent’s bond market since the financial crisis, according to strategists at Bank of America. About 9% of Europe’s biggest companies could be classified as the walking dead, companies that risk collapse if the support dries up, according to the analysts. After the crash of Lehman Brothers sent global markets into a tailspin, a decade of easy-money policies gave breathing room for nations to get their balance sheets in check and allowed for a spirited revival in corporate profits. But as central bankers look to pull back stimulus for fear of overheating, the potentially grim outlook for vulnerable companies may give them pause, according to Bank of America.

“Monetary support in Europe over the last five years has allowed companies with weak profitability to continue to refinance their debt and stave off defaults,” analysts led by Barnaby Martin wrote in a note Monday. “This supports the point that our economists have been making: that the ECB will likely be very slow and patient in removing their extraordinary stimulus over the next year and a half.” The strategists classify zombies as non-financial companies in the Euro Stoxx 600 with interest-coverage ratios – earnings relative to interest expenses – at 1 or less. The thinking goes that companies in this category are particularly vulnerable to rising interest rates. About 6% of European companies had a coverage ratio of less than 1 on the eve of Lehman’s downfall, a %age that fell to as low as 5% in 2013 when the euro-area sovereign debt crisis cooled.

Zombies shot up to as high as 11% in June 2016 before easing in recent months. Energy companies, thanks to weak oil prices, and those based in southern Europe –particularly smaller firms faced with weak profit generation amid feeble growth – make up a disproportionate share of the zombie world, according to Bank of America. To be sure, different metrics tell different stories about the health of corporate leverage, with some investors citing growth projections and yardsticks like net debt to earnings as reasons bond buyers can be more sanguine. But the coverage ratio is particularly useful in projecting how companies can cover debt costs from their earnings as interest costs rise.

Leverage kills.

• Markets Relax Merrily on a Powerful Time Bomb (WS)

Stock and bond market leverage is everywhere. Some of it is transparent, such as NYSE margin debt which was $539 billion as of the June report. But the hottest form of stock and bond market leverage is opaque, offered by financial firms that usually don’t disclose the totals: securities-based loans (SBLs) — or “shadow margin” because no one knows how much of it there is. But it’s a lot. And it’s booming. These loans can be used for anything – pay for tuition, fix up that kitchen, or fund a vacation. The money is spent, the loan remains. When security prices fall, the problems begin. Finra, the regulator for brokerages, doesn’t track this shadow margin, nor does the SEC. Both, however, have been warning about the risks. No one knows the overall amount of this shadow margin, but some details have been reported:

Morgan Stanley had $36 billion of these loans on its balance sheet as of the end of 2016, up 26% from 2016, and more than twice the amount in 2013. • Bank of America Merrill Lynch had $40 billion in SBLs on the balance sheet at the end of 2016, up 140% from 2010; • UBS and Wells Fargo “also have made billions in such loans, people familiar with those banks” told the Wall Street Journal. Raymond James, Stifel Nicolaus… they’re all doing it. • Fidelity used to fund its own SBLs for its clients, but three years ago partnered with US Bancorp. • Even the little ones are trying to get their slice of the pie: In April, robo-advisory startup Wealthfront, with less than $6 billion, announced that it would offer SBLs to its clients.

And now Goldman Sachs, which has been offering SBLs to its 12,000 super-wealthy clients through its Private Banking unit — accounting “for more than half of the unit’s $29 billion in loans outstanding,” according to the Wall Street Journal — announced on Thursday that this wasn’t enough and that it is partnering with Fidelity Investments to spread these loans far and wide.

No. It’s an outright lie. Pure make believe.

• US Economic Resilience Is An Exaggeration (DDMB)

Are US Federal Reserve stress tests leading economic indicators? That certainly seems to be the case. Just ask Capital One. As of the first quarter, credit card loss provisions at Capital One were above 5%, a six-year high. The company recorded some improvement for the second quarter, yet Fed stress tests of the bank’s overall loan portfolio in a deep downturn show losses topping 12%. That explains Capital One’s “conditional” passing score, a black eye that prompted a reduced share buy-back plan and no increase in its dividend. Most economists today applaud the resilience of the current recovery, which has stretched into its eighth year, the third-longest in postwar history. Resilience and rising household defaults, though, don’t tend to go hand in hand.

Pressures have been building in the background for some time. When adjusted for inflation, credit card usage has grown faster than incomes for 18 months. According to Fed data, that time frame coincides with the upturn in revolving credit, a proxy for credit card debt. In November 2015, outstanding revolving credit crossed above the $900-billion threshold for the first time since December 2009. By May of this year, annual growth was clocking 8.7%. Meanwhile, credit card balances hit $1.02 trillion, the highest level in almost eight years. Whether by choice or force, the aftermath of the financial crisis prompted households to ratchet back their usage of credit cards. As the recovery got underway, frugality prevailed, punctuated by an increase in debit card purchases.

It is thus notable that Bank of America data find debit card usage has weakened in recent years as households grew more comfortable rebuilding their credit card balances. “Confidence” is the term most associated with the rising credit card debt. But it’s fair to ask why confident households would choose to pay so dearly for the privilege. At 15.83%, the average rate on credit card balances is at a record high. It is more likely that households are increasingly tapping their credit cards to cover the cost of necessities, that they are less confident and more anxious about their future finances.

This should be presented as a major mea culpa by WaPo, but no, it’s not them, it’s “the media” who screwed up. NYT runs similar piece. WIll they all fit through the exit door at the same time?

• The Quest To Prove Collusion Is Crumbling (WaPo)

While everyone is fixated on President Trump’s unbecoming and inexplicable assault on Attorney General Jeff Sessions, the media has been trying to sneak away from the “Russian collusion” story. That’s right. For all the breathless hype, the on-air furrowed brows and the not-so-veiled hopes that this could be Watergate, Jared Kushner’s statement and testimony before Congress have made Democrats and many in the media come to the realization that the collusion they were counting on just isn’t there. As the date of the Kushner testimony approached, the media thought it was going to advance and refresh the story. But Kushner’s clear, precise and convincing account of what really occurred during the campaign and after the election has left many of President Trump’s loudest enemies trying to quietly back out of the room unnoticed.

Cable news airtime and in-print word count dedicated to the nonexistent collusion story appear to be dwindling. Democrats and their allies in the media seem less eager to talk about it, and when they do, they say something to the effect of “but, but, but … Kushner didn’t answer every question … He wasn’t under oath … There are still more witnesses … What about this or that new gadfly?” They are stammering. And it hasn’t taken long for news producers and editors to realize that the story is fading. At last, the story that never was is not happening. There are a few showstoppers from Kushner’s testimony that make it obvious to any fair-minded, thinking person that there was no collusion with Russia. In his own words, Kushner makes it clear that his actions were innocent but, at times, misguided and ill-conceived.

He plainly states he had “hardly any” contacts with Russians during the campaign and found his June 2016 meeting with Donald Trump Jr. and the infamous Russian lawyer to be an absolute “waste of time.” Democrats and their allies in the media have exhausted themselves building a scandalous narrative surrounding the Russian lawyer meeting, but according to Kushner, the meeting was so useless that he “actually emailed an assistant from the meeting after [he] had been there for ten or so minutes and wrote ‘Can u pls call me on my cell? Need excuse to get out of meeting.”’ Maybe the collusion didn’t take very long, or maybe he realized what the lawyer had to say was a useless farce and he wanted to get on with his day.

Much to the dismay of Trump’s haters, Kushner’s account of events even further proves just how far the media has stretched the collusion story. When the campaign received an official note of congratulations from Russian President Vladimir Putin the day after the election, Kushner had to send Dimitri Simes of the Center for the National Interest an email asking for the name of the Russian ambassador so that he could reach out and confirm the message’s authenticity. So, that’s that. If you can’t remember your handler’s name, you can’t be guilty of nefariously colluding with that person. How much collusion could Kushner have possibly done with someone whom he had so little communication with that he could not remember his name and did not know how to contact him?

From interview with David Sirota. Party has no future. Get out or go down with it.

• What’s The Matter With Democrats – Thomas Frank (IBT)

Basically, I think the Democratic party is in deep trouble. The evidence of that is now plain, I think, to everyone — that they’re in a state of historic wipe-out across the country and in both of Houses of Congress, and of course, they lost the presidency, too… The leadership of the party have persuaded themselves that they don’t really have a problem, that all they have to do is wait for [Donald] Trump to screw up and they’ll waltz right back in, and so they don’t have to do anything different. I think Trump represents the culmination of a long-term shift of working people, working-class people away from the Democratic Party.

[..] The way I look at it is that this is a long-term problem. This is a culmination of a very long-term problem with the Democrats very gradually, but definitely, abandoning the interests of working-class voters, identifying themselves instead with a more affluent group, with the affluent white-collar professionals. It starts in the 1970s with the Democrats removing organized labor from its structural position in the Democratic party, and then it goes up through Bill Clinton getting NAFTA done, the free trade deals that the Democrats have … By the way, in my opinion, free trade or the trade agreements, I should say, was probably the issue that if there was one issue that really did Hillary in, I think that’s what it was: the trade deals under the Clinton administration, Obama sort of dropping the ball on labor’s various issues, doing these incredible favors for Wall Street while he blew off the concerns of union.

[..] Bailouts. The Wall Street bailout was the worst. This was, of course, George W. Bush … No, take a step back further. The deregulation under Clinton. Do you remember, bank deregulation was something that we now think of it as one of the central elements of neoliberalism, but Reagan couldn’t get it done. Reagan tried. They put some dents in Glass Steagall when Reagan was president, but it took a Democrat to really get it done, Bill Clinton, and it wasn’t just blowing up Glass-Steagall. There was this whole series of bank deregulatory measures when he was president. By the end of his term in office, basically, Wall Street was more or less openly identified with the Democratic Party. This is an enormous historical shift…

The Democratic party [used to be] this sworn enemy of Wall Street. Franklin Roosevelt broke up all of these banks, the Glass Steagall Act, put all these banks out of business, and set up the Securities and Exchange Commission to regulate these guys, all of these regulatory measures. That’s the Democratic heritage. That’s the legacy of the New Deal. Up until the days of Clinton, that’s really who the Democratic Party was. They had a very populist tone, and they would never identify themselves with Wall Street. Barack Obama comes in, and I was one of these people who thought that he represented a turn back in the other direction and that he would be, very shortly would be, getting tough with Wall Street. He had all the bailouts were underway. He had total authority over these guys, and he didn’t do it. Instead, he appointed all these various Clinton people to come in and manage the bailout situation.

Like that line.

• Decades From Now, They’ll Say He Had “The Tweets” (Jim Kunstler)

I know I’m not the first to point out how Anthony Scaramucci, President Trump’s brand new Communications Director, is suddenly and eerily carrying on like his namesake, the arch-rascal / buffoon of the Old World Commedia dell’Arte in lashing out at his fellow scamps and bozos in the clown school that the White House has become. Of course, these antics only reflect the astounding violent vulgarity of current US culture in general, especially as it recursively re-amplifies itself in the distorting echo chamber of TV. It’s how we roll nowadays – right up the collective butt-hole of history until some fateful event provokes a last frightful purging of our own bullshit. Still, it was rather shocking to hear Scaramucci refer to White House Chief of Staff Rance Priebus as “a fucking paranoid schizophrenic” and Trump ultra-insider Steve Bannon as someone who “enjoys sucking his own cock.”

It’s kind of like Paulie Walnuts of “The Sopranos” wandered into the West Wing of “Veep.” Somebody’s gonna get whacked, and it’ll be a laugh-riot when it happens. We need a little comic relief in these midsummer horse latitudes of the mind as the ill-starred Trump Show appears to enter its ceremonial death dance. There’s also something satisfyingly Napoleonesque about Scaramucci. Here’s a guy who cuts through the odious blubber of US politics right to the bone of things with a flensing blade of profane righteousness. Personally, I’d like to see him take some whacks at a few more deserving targets, and I can even imagine a somewhat farfetched scenario where the little guy shoves Trump out during a concocted national emergency and manages to declare himself First Citizen, or some such innovative title allowing him to run things for a while – say, until the generals toss him out a window.

Or maybe he’ll last less than a week in his current position. I would not be surprised, either, if Mr. Bannon beats little Mooch to death with an Oval Office fireplace poker right in front of the Golden Golem of Greatness himself. The mills of the gods grind slowly, but they grind exceedingly fine – in this case, inexorably toward the restorative medicine of the 25th amendment. There is, after all, that hoary old artifact called the national interest lurking somewhere offstage aside of all this colorful mummery, especially as the Russian Meddling gambit appears to be dribbling away to nothing. It’s more than self-evident that poor Trump is in so far over his head that he’s come down with something like the bends, a debilitating systemic disorder rendering him unfit to execute the powers of office. Decades from now, they’ll say he had “the tweets.”

You do know you live in a feudal society, right?

• Leasehold Tycoon Whose Firms Control 40,000 UK Homes (G.)

He does not appear on any rich list but he has built a property empire that rivals that of the Duke of Westminster. Companies controlled by James Tuttiett, aged 53, have quietly snapped up the freeholds of tens of thousands of houses and flats in almost every city in Britain, which are now at the centre of controversy over spiralling ground rents. The scale of Tuttiett’s property empire has never been previously disclosed. Documents at Companies House reveal that he is frequently the sole director of companies that own the freehold of large-scale developments in Newcastle, Birmingham, Leeds, Coventry and London. Leaseholders are obliged to pay ground rents to his company, E&J Estates, that in some cases will soar to £10,000 a year per home.

The government this week proposed a ban on new-build leaseholds, and said ground rents on new apartments should fall towards zero. At the launch of an eight-week consultation, the communities secretary, Sajid Javid, said: “It’s clear that far too many new houses are being built and sold as leaseholds, exploiting homebuyers with unfair agreements and spiralling ground rents.” “Enough is enough. These practices are unjust, unnecessary and need to stop,” said Javid, adding on BBC Radio 4’s Today programme that ground rent had been used “as an unjustifiable way to print money”. [..] Research by Guardian Money found an extraordinary web of 85 ground rent companies controlled by Tuttiett, where the freeholds include not just homes but also schools, health clubs and petrol stations.

In 2016 one of these 85 companies, SF Funding Ltd, recorded an £80m increase in the value of its ground rents from the year before, taking them to £267.4m. Tuttiett is the sole director of the company, which has no other employees. The financing of Tuttiett’s property empire is helped by low-interest loans totalling £336m made by an insurance company, Rothesay Life, spun out of Goldman Sachs, in which the US investment bank remains the largest shareholder. Among the Rothesay Life loans made to E&J is one at £128m with a stated interest rate of just 0.95% a year, although it is understood the real rate paid is likely to be higher. The existence of the Rothesay loans opens a back door into Tuttiett’s interests, as Companies House lists all the properties over which Rothesay has a charge.

Lenders are getting out. But not because they care about the earth.

• Companies Abandon Nearly One Million Hectares of Alberta Oilsands (CP)

In another sign the bloom is off the boom for the oilsands, the industry has returned almost one million hectares of northern Alberta exploration leases to the province over the past two years. The total area covered by oilsands leases remained constant at about nine million hectares between 2011 and 2014. But it fell to 8.5 million hectares in 2015 and 8.1 million in 2016, following the crash in world oil prices from over US$100 to under $60 per barrel in 2014. Most of the returned acreage either represents expired or surrendered leases, according to Alberta Energy. Observers were surprised by the size of the lease returns which they attributed to industry cost-cutting and disinterest in spending to develop new prospects when there’s no money to build projects already on the books.

“It costs money to maintain these lands,” said Brad Hayes, president of Petrel Robertson Consulting in Calgary. “You can’t convince shareholders to continue to put that money out if there’s no prospect for success.” Alberta’s oilsands have been getting little respect lately, thanks to the exit of large foreign companies, the province’s hard cap on oilsands emissions, increasing carbon taxes and the stumbling price of crude oil. Its troubles have been welcomed by environmentalists who point out the industry’s outsized impact on air, land and water pollution. “This is good news. It’s a sign that investment dollars are shifting out of carbon-intensive energy,” said Keith Stewart, senior energy strategist with Greenpeace Canada.

Feels like all they do is try to create an ever bigger mess. Throw in another €100 million and say: We tried!

• EU Accused Of ‘Wilfully Letting Refugees Drown’ In The Mediterranean (Ind.)

Aid workers have accused the EU of “wilfully letting people drown in the Mediterranean” as they face being forced to suspend rescue missions for refugees attempting the world’s deadliest sea crossing. Italy is attempting to impose a code of conduct on NGOs operating ships in the search and rescue zone off the coast of Libya, which is now the main launching point for migrants trying to reach Europe on smugglers’ boats. Humanitarian groups have argued the code will impede their work by banning the transfer of refugees to larger ships, which allows vessels to continue rescues, and forcing them to allow police officers on board. A revised code of conduct is expected to be presented by the Italian interior ministry on Monday, following meetings between officials and NGOs.

The 11-point plan, which has been approved by the European Commission and border agency Frontex, could see any groups refusing to sign up denied access to Italian ports or forbidden from carrying out rescues. They are currently deployed by officials at Rome’s Maritime Rescue and Coordination Centre (MRCC) and charities fear any move to restrict their operations, leaving just Italian coastguard and naval ships, will dramatically reduce rescue capacity during peak season. German charity Sea-Watch announced the deployment of a second rescue vessel in response to the plans, which it called a “desperate reaction” by a country abandoned on the frontline of the refuge crisis by its European allies. “The EU is wilfully letting people drown in the Mediterranean by refusing to create a legal means of safe passage and failing to even provide adequate resources for maritime rescue,” said CEO Axel Grafmanns.

“The NGOs are currently bearing the brunt of the humanitarian crisis and they are being left alone.” Médecins Sans Frontières (MSF), which has staff on two rescue ships, said it was engaging with Italian authorities in an “open and constructive way” over the proposed code but had serious concerns over several clauses. “MSF employees are humanitarian workers, not police officers, and that for reasons of independence they will do what is strictly requested by the law but nothing more so as to protect our independence and neutrality,” a spokesperson said.

Home › Forums › Debt Rattle July 30 2017