Ivan Aivazovsky Creation of the World 1864

https://twitter.com/BoLoudon/status/2051012329362317518?s=20

https://twitter.com/Tironianae/status/2050939495596347494?s=20 https://twitter.com/elonmusk/status/2050822211947356494?s=20 https://twitter.com/ToscaAusten/status/2051013132970017132?s=20Tesla https://t.co/eIIksloKQY

— Elon Musk (@elonmusk) May 4, 2026

“Trump threatened that any interference with the U.S. operation would “have to be dealt with forcefully.”

Two things are not up for negotiation:

1) No nukes for Iran.

2) Free passage in Street of Hormuz.

So far, Iran refuses to acknowledge this.

The guys who play the leadership now may not be the leaders.

• Trump’s Strait of Hormuz Move Blends Power and Mercy (David Manney)

President Donald Trump announced Sunday that the United States will begin helping ships from “neutral and innocent” countries leave the Strait of Hormuz starting Monday morning. He called the effort Project Freedom and framed it as a humanitarian move for ships trapped by the Iran war. Plenty of politicians mention compassion when cameras are rolling, but Trump continues to demonstrate how removed he is from “regular” politicians, tying the decision to action, sea power, and safe passage through one of the most dangerous waterways on Earth.Read more …

The Strait of Hormuz carries enormous weight in global commerce, and energy markets still watch it like a man watches smoke near a dry field. Hundreds of ships and roughly 20,000 seafarers have been stranded as the conflict involving Iran disrupts traffic through the region. Iran has been blocking nearly all shipping from the Gulf apart from its own for more than two months. Last month, the U.S. imposed its own blockade of ships from Iranian ports. It was not immediately clear which countries the U.S. operation would aid or how the operation would work. The White House did not immediately respond to a request for comment on the matter and the Pentagon declined to comment.Trump threatened that any interference with the U.S. operation would “have to be dealt with forcefully.” Iran said on Sunday it had received a U.S. response to its latest offer for peace talks a day after Trump said he would probably reject the Iranian proposal because “they have not paid a big enough price.” Many crew members come from South and Southeast Asia; they had nothing to do with the war. They didn’t start it, write Iran’s threats, or choose to become bargaining chips in a dangerous waterway. Ships and seafarers, many on oil and gas tankers and cargo ships, have been stuck in the Persian Gulf since the war began.

Crew members have described to The Associated Press watching intercepted drones and missiles explode over the waters, and running low on drinking water, food and other supplies. Many sailors come from India and other countries in south and southeast Asia. Those people were doing ordinary work when an extraordinary crisis fell on them like an ex-Iranian cleric cannonballing in a pool. Trump’s statement cut through the usual fog, saying the United States had told those countries that America would guide their ships safely out of restricted waterways so they could “freely and ably get on with their business.”

The wording set the mission’s tone: America isn’t rescuing hostile actors; it’s notifying neutral nations that lawful commerce and helpless crews won’t be abandoned because Iran turned a vital shipping corridor into a danger zone. The market noticed. Oil prices fell after Trump’s announcement. Brent crude dropped $1.83 to $106.34 per barrel — it’s not much, but better than a stick in the eye — while the U.S. West Texas Intermediate fell $1.72 to $100.22. Markets don’t reward speeches because the words sound cool; they move when a president signals that chaos won’t be allowed to spread.

Nobody should pretend Project Freedom will be simple; public details remain limited, and follow-up from the White House and Pentagon hadn’t filled in every operational blank by Sunday afternoon. I’m not a CNN reporter; I’m smart enough to avoid asking the president his military plans. Trump’s posture is clear; he’s telling Iran, shipowners, seafarers, and energy markets that the United States sees what’s going on and intends to move. In a region where hesitation often gets read as weakness—or, as in the case of U.S. mainstream media, thinking Trump is overmatched—the announcement gives America’s allies and neutral partners something firmer than diplomatic shrugging.

The compassion angle deserves notice because strength doesn’t only count when it punishes. American power protects supply lines, calms markets, and helps stranded crews get home or get moving again. The same Navy that deters enemies also clears a path for working sailors who just want to leave a dangerous place alive. People on the left will find reasons to complain because some people find a scandal when the rest of us call it Monday. They’ll argue over timing, tone, risk, wording, tie color, head angle, and whatever else can be fed into the outrage machine before breakfast. Mike seems to get hangry before breakfast.

Meanwhile, the ships still need passage, crews still need safety, and oil prices still affect American families filling their tanks and paying their bills. Trump is acting in the space where leadership has to live, between danger and delay. Or between the space of $4.25 gas and the Biden-era genius of calling paralysis a policy. Project Freedom gives the country a clean view of Trump’s governing style in a crisis; he didn’t offer sympathy cards to the gay, comatose Iranian leader; he’s offering safe passage to neutral nations trapped near Iran. Trump’s not treating energy markets as abstract numbers on a screen: he understands that every barrel eventually touches a household budget somewhere. Strength and mercy don’t have to be enemies; sometimes they work best when they sail together.

Was Obama right about laughing off Bibi’s threats? We’ll never know. Trump thinks even if it is an empty threat, Iran still has terrorized the Middle East for 50 years.

• Obama’s Iran Tale Trips Over Its Own Halo (David Manney)

And now for something completely different. Picture an old Shakespearean theater (or, as the snobs would say, thee-aa-taaa-hh), right when the fidgety crowd grows silent because the holy curtain, resplendent with images of the miraculous Obama, slowly rises. Barack Obama, former president of these here United States, appears on the stage of world events wearing the invisible crown of moral superiority. Entering stage right is Israeli Prime Minister Benjamin Netanyahu, who carries ill tidings about Iran, nuclear danger, and the small matter of a regime that’s spent decades threatening Israel and chanting “DEATH TO AMERICA!”Read more …

Obama looks up, with a face appearing to be pulled out at the chin, leaving a pair of substantial ears to anchor him in place. He raises one hand, pausing for applause only he can hear (it’s the ears, you know), and announces that he alone resisted the madness. “Drag me into war? Never,” he seems to say from his very tall stool of virtue. Out of nowhere, a fake medieval trumpet wheezes, dust blowing out the bell, a giant foot drops from the sky, covering the stage, and the sketch abruptly ends. Okay, it’s not the best Monty Python parody to use for satire, but hopefully some symbolism pulled through.In a recently published interview, Obama claimed that Netanyahu used the same arguments with him that the Israeli leader later used with President Donald Trump. Obama cast himself as the steady man who refused military action and, instead, opted for diplomacy. He also said he still believes his approach was right. In Barack Obama’s final days in office, he found himself in the painful position of trying to console his staff, the Democratic Party, and millions of supporters. He attempted to convince them—even if he could not entirely convince himself—that the looming Presidency of Donald Trump was not a national calamity. In the past, he would say, the country had endured slavery, the Civil War, the Great Depression, Jim Crow, assassinations.

And, though Trump was alarming in many ways, America was blessed by the strength of its institutions and the resilience of its people. The word “guardrails” was uttered constantly. In Obama’s estimation, Trump would not erase all his achievements. As he put it, “Maybe fifteen per cent of that gets rolled back.” This kind of calm was pure Obama. His appeal had as much to do with character and temperament as it did with his center-left ideology. Although Obama believed that Trump’s ugliest slurs against him, particularly his deployment of the birther theory, were a racist outrage that heightened the threats against him and his family, he now took pains to set aside his contempt. Insuring that there was another orderly transition of power—that, too, was part of his rhetoric of consolation.

Such poise was not easy to sustain. When Obama met Trump for a ritual pre-Inauguration visit to the Oval Office, he was struck by how unschooled and incurious the President-elect was. Trump, Obama told people, seemed indifferent to hearing about potential national-security perils—North Korea, Russia—preferring to brag about the size of the crowds at his campaign rallies. Obama pitched Trump on preserving several of his signature achievements, including the Affordable Care Act and the Iran nuclear deal. Trump responded that he would consider the request, and Obama thought it was not impossible that he meant it. Naturally, the tale arrives with Obama placed at the center of wisdom, restraint, and good lighting—lighting tips learned at the knees of Beyoncé and Jay-Z.

The timing isn’t subtle: Trump authorized Operation Epic Fury against Iran after months of pressure, intelligence sharing, and escalating danger involving Israel and Iran. Obama’s story lets him suggest that Netanyahu used the same pitch for years and that Trump finally went where Obama refused to go. In an interview with The New Yorker, Obama said Netanyahu had tried to convince him to pursue war with Iran, adding that the Israeli leader “got what he wanted” in more recent developments. However, Obama questioned whether such an outcome ultimately benefits either Israel or the United States.

Beyond the immediate issue of Iran, Obama warned that current geopolitical shifts could have long-term consequences for global stability. He pointed to strains in traditional alliances and cautioned that the international system built after World War II, anchored by institutions like NATO, is under pressure. Obama also discussed the broader challenges facing US global leadership, arguing that rebuilding trust with allies may be more difficult than addressing domestic issues. If you think about it, it’s really a neat little performance: Netanyahu becomes the pushy salesman, Trump becomes the buyer, and Obama becomes the only adult in the room who read the fine print.

Netanyahu has long warned that Iran’s nuclear program poses an existential danger to Israel. Obama knows that history, and he also knows many Americans remember his Iran posture as weak, naive, and too eager to treat Tehran like a difficult negotiating partner instead of a hostile regime with innocent blood on its hands. Instead of pursuing joint strikes with Israel, Obama said he prioritized diplomacy with Iran. Those efforts led to the 2015 nuclear agreement, formally known as the Joint Comprehensive Plan of Action, which imposed limits on Iran’s nuclear activities in exchange for sanctions relief. Netanyahu strongly opposed the agreement, warning it would fail to prevent Iran from obtaining nuclear weapons and would strengthen the country economically and militarily.

Trump later withdrew the United States from the deal in 2018, reimposing sanctions on Iran and aligning more closely with Netanyahu’s position. Barry’s new version tries sanding down all of that to leave one shiny statue standing: Obama, the restrained, austere scholar, nobly blinking while everybody else reaches for a sword. The real purpose looks obvious: Obama wants to reopen an old argument and drive a wedge between Trump supporters who disagree over foreign policy. Barry is implying that Trump got handled by Netanyahu while Obama stayed too wise to be moved. It’s less foreign policy analysis than reputation repair with better upholstery.

There’s something missing that I just can’t place my finger on. Please help me remember something about a plane, pallets, tons of cash … ah! Yes, even after paying a several billion dollar bribe to the mullahs, Obama removes the part where Iran didn’t become less dangerous because of his preference for green diplomacy. Tehran, with help from brand-new U.S. dollars, kept funding terror, threatening Israel, and expanding its reach while Western leaders congratulated themselves for managing the problem. Obama’s defenders call his approach patient, while plenty of Americans would call it wishful thinking — at best — in a tailored suit.

Let’s return to our stage. Obama takes his final bow, still certain of his intestinal fortitude to resist the warmongering fever. Netanyahu remains Israel’s prime minister, dealing with Iran as a legitimate threat, not a TED Talk topic. President Trump remains president of the United States, making decisions in a world Obama (and, with Susan Rice’s work, Biden) helped create. The curtain falls. The giant foot lands again, but in a way that a set of ears sits on either side of the heel, looking like a giant Temu version of Mercury’s foot, about to send a message from the Roman gods.

The audience is asked to admire the former president’s restraint, but the joke lingers because Obama is speaking without a script, so the man keeps talking and talking and talking. Barry never sees what happened; he didn’t stop the danger out of Iran. He just wrote himself inside a narrative where he never belonged, where he never succeeded, and into a reset of a history that never happened. In short, Obama has long since become a president losing hold of his carefully crafted narrative, one polished for years until reality started showing through the shine.

WaPo-ABC poll.

At the same time, CNN came with a poll that said 100% of 2024 MAGA voters still would vote MAGA.

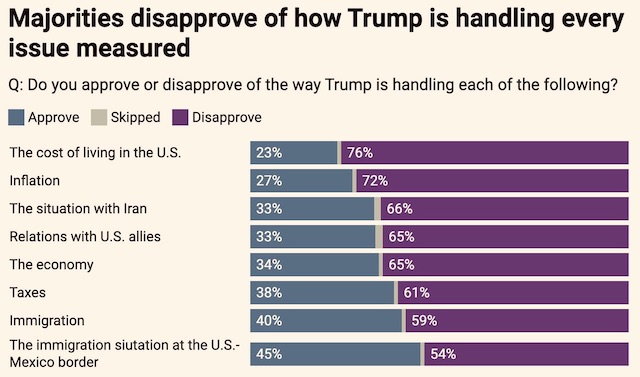

• Trump Disapproval Rate Hits Career-High – War And Rising Costs Take Toll (ZH)

Though tempered by the prospect of additional GOP gerrymandering of House districts in the wake of a pivotal Supreme Court decision, Democrats’ hopes for a rout of Republicans in the approaching midterm elections are rising after a Washington Post-ABC News-Ipsos poll found that President Trump’s disapproval rating is now the highest of either of his two terms in office. Trump’s decision to launch a war on Iran is taking a toll — voters are not only dismayed by his handling of Iran, but also dissatisfied with his work on the economy, which is itself being harmed by the war.Read more …

In a survey of US adults taken in the last week of April, 62% said they disapprove of his general performance in the Oval Office. A whopping 76% disapprove of his handling of the cost of living and 66% disapprove of what he’s done with Iran. A majority of Americans surveyed expressed disapproval of his handling of every issue covered by the survey.

While 85% of Republicans approve of his performance, the share who strongly approve fell to 45% — that’s down 8% since September and is a new Trump low. Perhaps more importantly, his approval among Republican-leaning independents is also at a new low of 56%. Overall, just 25% of independents approve of his performance. Trump also scored terribly on some personal attributes. For example, 71% said the descriptors “honest and trustworthy” are not applicable to Trump, while 67% said Trump does not “carefully consider important decisions.” Meanwhile, 59% said he lacks the “mental sharpness” required of his position.The poll provides a little insight into the upcoming midterm races. Today, Republicans have a slim, 3-seat margin of control of the House of Representatives. Asked if they would vote for a Democrat or Republican candidate if the House election were held today, 49% said they would for a Democrat, compared to 44% who would choose a Republican. At the same point in the 2022 midterms, that question yielded a 42-42 tie, with the GOP proceeding to win the House when votes were cast six months later, securing a 222 – 213 margin in seats (a 9-seat pickup for the Republicans). As for intended turnout, 79% of registered Democrats say they are “absolutely certain” they’ll vote, compared to 72% of Republicans — a 7-point improvement on the GOP turnout expectation recorded in a February survey.

Vance had higher approval and disapproval ratings than Rubio — as more survey participants shrugged at the Rubio performance question. Looking at the big picture, 67% of Americans said the country is moving in the wrong direction. Here, there’s a vast difference among parties: 94% of Democrats felt that way, compared to 25% of Republicans. As a general caveat, we’ll note that — since more and more Americans identify as independent — party results are growing less meaningful. A hefty 78% of independents say the country is heading south.

Finally, the poll had some incidental insights for those looking ahead to the 2028 presidential race. While participants weren’t asked about that contest, they were asked to rate the job performance of various Trump administration officials, including two potential GOP contenders: Vice President JD Vance and Secretary of State Marco Rubio. They came out with similar approval ratings — 35% for Vance and 33% for Rubio — but Vance had a 48% disapproval rating, compared to 40% for Rubio. The remainder of respondents had no opinion.

No longer “little” Marco.

• Trump Sends Rubio to Calm Tensions with Italy and the Pope (Anderson)

Relations between the United States and Italy and between Donald Trump and Pope Leo XIV have been delicate lately to say the least. So, the Trump administration is sending in the one man to the Vatican who can possibly help them recalibrate them this week: Marco Rubio. The State Department announced on Monday that the secretary of State will travel to Rome on Wednesday “to advance bilateral relations with Italy and the Vatican.” “Secretary Rubio will meet with Holy See leadership to discuss the situation in the Middle East and mutual interests in the Western Hemisphere,” the statement continued. “Meetings with Italian counterparts will be focused on shared security interests and strategic alignment.”Read more …

Several MSM outlets are saying that he will meet with the pope and Cardinal Pietro Parolin, the Vatican’s foreign minister, on Thursday. He’ll most likely also meet with Italian Foreign Minister Antonio Tajani and Defense Minister Guido Crosetto, and possibly even Italian Prime Minister Giorgia Meloni herself, but the State Department didn’t specify that information. We all know the background. The pope has repeatedly criticized the United States and Israel’s conflict in Iran, calling for more dialogue and peace talks — you know, the sort of thing that hasn’t worked for decades. “Faced with the possibility of a tragedy of enormous proportions,” he said in March, shortly after the conflict began. “I address to the parties involved a heartfelt appeal to assume the moral responsibility to stop the spiral of violence before it becomes an irreparable abyss!”While this is standard Vatican peace talk, he’s also criticized Trump’s rhetoric regarding Iran, particularly calling the infamous “a whole civilization will die tonight” line “truly unacceptable.” Trump didn’t take too kindly to that and has responded via social media and interviews with various outlets, calling the pope “weak on crime,” “very liberal,” and “terrible for foreign policy.” On Truth Social on April 12, the president wrote: “I don’t want a Pope who thinks it’s OK for Iran to have a Nuclear Weapon…I don’t want a Pope who thinks U.S. action against Venezuela was wrong.” (I can’t speak for the Iranians, but I can tell you that the Venezuelans are firmly in favor of the U.S. action against Venezuela.)

The president added, “And I don’t want a Pope who criticizes the President of the United States because I’m doing exactly what I was elected, IN A LANDSLIDE, to do…” He concluded that the pontiff needed to “get his act together as Pope, use Common Sense, stop catering to the Radical Left, and focus on being a Great Pope, not a Politician. It’s hurting him very badly and, more importantly, it’s hurting the Catholic Church!” When talking to reporters later, the president said, “I’m not a big fan of Pope Leo. He’s a very liberal person, and he’s a man that doesn’t believe in stopping crime. He’s a man that doesn’t think that we should be toying with a country that wants a nuclear weapon so they can blow up the world. I’m not a fan of Pope Leo.”

Eventually, Italian Prime Minister Giorgia Meloni — someone who is typically a pretty staunch Trump ally — got into the spat and criticized Trump’s words against the pope, calling them “unacceptable.” She said it was normal for the head of the Catholic Church to condemn “every form for war.” Trump didn’t take too kindly to this either and said that “she’s the one who’s unacceptable” and claims she’s “no longer the same person.” The two have been distancing themselves from each other ever since.

Meloni has also been critical of military action in Iran herself, and “sided with France, Spain, the U.K., and Germany in declining to participate in mine sweeping and other military operations to reopen the Strait of Hormuz during Iran’s initial blockade of the strategic waterway.”So, can DJ Rubio Secretary Rubio save the day? He is our country’s top diplomat after all, but more importantly, Trump knows that Rubio’s got the personality to handle these types of situations when the president himself… well, let’s just say he’s a bit more blunt. And he admits it too. Earlier this year, he confessed that Rubio, who has become one of this most trusted advisors, was teaching him.

“I became a diplomat for the first time. Well, you know, taught me that? Marco Rubio. He said, ‘Let me teach you about diplomacy,’” the president said at the World Economic Forum in Davos in January. The president has also admitted on several occasions that Rubio is “a bit more diplomatic” than Vice President JD Vance, who has Trump’s knack for telling it like it is. But that doesn’t mean Rubio is soft. We all saw the speech he gave at the Munich Security Conference earlier this year, telling European leaders that “we in America have no interest in being polite and orderly caretakers of the West’s managed decline.” Let’s just hope he carries that energy into his trip this week. And maybe a little of this energy too. I mean, who can resist it?:

“CENTCOM confirms Iran has NOT successfully struck ANY Navy ships this morning, despite claiming they’ve done so.” —Eric Daugherty on X

• All’s Not So Quiet on Any Front (James Howard Kunstler)

Project Freedom. Cute move! Notice that it’s not Operation Freedom. That would frame it as a military move. The President is tactically framing this as a humanitarian action. Mr. Trump has advised Congress as of May 1 that hostilities with Iran (Operation Epic Fury) are terminated, at the 60-day limit of the War Powers Resolution. Commercial ships from countries not involved in the Iran / US dispute will now get escorted safely through the Strait of Hormuz by US naval vessels.Read more …

Any attack on these ships by Iran would prompt a forceful response and trigger a re-wind of the clock on the War Powers Resolution (WPR), meaning, another sixty days to conduct military operations, such as the destruction of key bridges and electric power plants promised earlier. Iran’s leadership — whoever that is — thought it could juke Mr. Trump on the 60-day deadline by stalling negotiations while it reorganized its remaining missile launchers. Tactical fail. Incidentally, the Supreme Court has never directly ruled on the WPR’s constitutionality or enforced the 60-day limit.Also, by the way, the “neutral and innocent bystanders” designation means that oil tankers from Kuwait, the Emirate states, Qatar, and Saudi Arabia will be given safe escorts out of the Persian Gulf. That will have two effects: 1) avert the “shutting-in” of their productive oil wells (and the prospective geological damage to the oil fields); and 2) alleviate the price pressure on oil generally with new supply reentering the global oil market.

You can conclude that this “project” will bring new pressure on the “whoevers” running Iran to stop shucking and jiving about how this thing ends — which is them surrendering the 1000-pounds of 60-percent enriched uranium stashed somewhere on their premises. Of course, coming to terms on the nuclear bomb-making issue would allow Iran the possibility of becoming, once more, a normal advanced industrial modern nation, should it also decide to eschew the rule of the mullahs and their psychotic minions in the Revolutionary Guard (IRGC). But that remains to be seen.

The other major project underway is on the domestic US scene: the much-needed severe beat-down of the so-called Democratic Party that has become captive to seditionists, overt communists, racketeers, and jihadis. DOJ prosecutions of color revolutionaries accelerate under Acting Attorney General Todd Blanche. James Comey finally has to account for his “86 / 47” seashell prank in a Carolina federal court while a long-dormant case was revived in the Eastern District of Virginia of Comey having used Columbia prof Daniel Richman as a cut-out to leak classified information to the press at the inception of RussiaGate, 2017.

Nobody knows exactly what’s going down in the Southern District of Florida these days (no leaks) where a grand Jury was convened in January to hear evidence in the RussiaGate matter including the years’ long train of organized seditions aimed at bum-rushing Mr. Trump out of the Oval Office in his first term, plus the mounting of various other operations (2020 election-rigging, the J-6 “Fedsurrection,” and maliciously fake serial prosecutions) aimed at stuffing him in prison at the end of that term.

All this is being treated as a “grand conspiracy” involving scores of agency officials and lawfare ninjas operating in the penumbra at the edge of government. Do not be surprised when rafts of indictments come out of the Fort Pierce, Florida, grand jury, probably in bunches, each bunch dedicated to a particular phase or operation.

Characters such as former President Barack Obama, FBI Director Christopher Wray, Senator Adam Schiff (D-CS), CIA-agent Eric Ciaramella, legal tacticians Norm Eisen, Marc Elias, and Mary McCord, Andrew Weissmann, crooked member of the Senate Intel Committee Sen. Mark Warner (D-VA), and former CIA Directors Brennan with former DNI James Clapper, were involved in multiple seditions and possible treasons. Supporting actors such as the tag-team of Peter Strzok and Lisa Page, former Deputy AG Rod Rosenstein, former AG Merrick Garland, former Deputy AG Lisa Monaco, former Sec’y of State Hillary Clinton, “Joe Biden” autopen operators Jake Sullivan, Mike Donlon, Steve Richetti, Anita Dunn, Neera Tanden, former Sec’y of State Antony Blinken, and Domestic Policy Advisor Susan Rice, are probably in the mix somewhere, too.

“The greatest threat the bloc currently faces emanates not from “external enemies,” but rather its “ongoing disintegration..”

• NATO Holds Secret Meetings With Movie, TV Makers – Guardian (RT)

Creatives reportedly fear that the US-led military bloc is moving to influence TV and film industry professionals. NATO is holding closed-door consultations with TV and film industry professionals across Europe and the US, The Guardian reported on Sunday. The move has prompted accusations that the bloc is working to leverage the arts for “fear mongering” and “propaganda,” it added. The military bloc has held three private meetings with directors, producers and screenwriters in Los Angeles, Brussels and Paris, and is planning to convene with members of the Writers’ Guild of Great Britain (WGGB) in London next month, the newspaper wrote.Read more …

The upcoming meeting will be overseen by the British think tank Chatham House and will discuss the “evolving security situation in Europe and beyond,” according to the report. NATO cyber and innovation technology deputy head James Appathurai is expected to attend, among other officials, the newspaper added. So far, the conversations have partly “inspired” at least “three separate projects,” The Guardian wrote, citing an internal WGGB e-mail.The military bloc’s move has reportedly sparked concern in the film and TV industry. The planned meeting is “clearly propaganda,” Irish film writer Alan O’Gorman said, as cited by The Guardian. “I think there’s fearmongering throughout Europe at the moment that our defenses are down,” he reportedly said, adding that he has seen a media and government push in Ireland “to present NATO in a positive light and align ourselves with them.” Other screenwriters were “pretty offended that art would be used in a way that was supporting war” and believed they were being asked to “contribute towards propaganda for NATO,” he said, according to the newspaper.

The Washington-led military bloc has been undergoing a growing internal rift, with US President Donald Trump again describing NATO as a “paper tiger” after multiple member states refused to join his war on Iran in recent months. Tensions between European NATO countries and the US had already been heightened by Trump’s threats in preceding months to annex Denmark’s autonomous territory of Greenland. The greatest threat the bloc currently faces emanates not from “external enemies,” but rather its “ongoing disintegration,” Polish Prime Minister Donald Tusk said on Saturday.

It’s not the people who had a happy childhood who do these things, decide for you what you can see.

• EU to Begin Censoring Emojis on Social Media — For ‘Safety’ (Bartee)

The European Commission apparently finds itself no longer satiated with controlling what combinations of letters it permits the serfs on its techno-planation to spell out on social media and has now expanded the scope of its Orwellian censorship regime to emojis.Read more …

Via European Commission: \”European regulators, the European Commission and the Board of the Digital Services Coordinators, enforcing the Digital Service Act published a world-wide first report on the landscape of prominent and recurrent risks on very large online platforms and search engines in the European Union. The report (pdf) identifies systemic risks such as, among others, the spread of illegal content or threats to fundamental rights, occurring on very large online platforms. It also gives a first overview of the mitigation measures taken by platforms, based on the transparency requirements under the DSA.Key findings cover risks to mental health and to the protection of minors online*; the impact of emerging technologies, such as generative AI, on online platforms; and challenges to intellectual property protection on online marketplaces. Among the notable mitigation measures highlighted are, for example, the use of automated systems to detect emojis used as code for illegal activities online, such as the sale of illegal drugs.

*Always “for the children” — the eternal excuse of the nanny state gynocrats to trample on fundamental civil liberties.

https://twitter.com/DigitalEU/status/2046872384649478568

Who is going to decide which emojis have to go?Probably some unelected bureaucrat behind a screen in some Brussels lair — or else AI; I’m not sure which is more dystopian. Via Hungarian Conservative: “Beyond mockery, critics have also raised concerns about the implications for free speech and digital governance. A frequently cited argument is that identifying ‘coded language’ requires platforms to interpret context and intent—moving beyond clearly illegal content into more subjective territory.

This concern ties into broader scepticism surrounding the DSA, which obliges large platforms to assess and mitigate so-called ‘systemic risks’, including illegal content and threats to public security. Critics argue that this framework increasingly incentivizes proactive and interpretive moderation, rather than responses limited to clearly unlawful material, and in doing so risks encroaching on online free speech. The debate also highlights the technical challenges involved. Emojis are inherently ambiguous and context-dependent, making accurate detection difficult and increasing the likelihood of false positives. Experts have long noted that content moderation already operates in ‘grey areas’,** where meaning is fluid and difficult to define, particularly as platforms rely more heavily on automated systems.”

“Of course, in such cases of “grey areas,” the censor will always and reflexively err on the side of maximum censorship, which is what’s surely going to happen here. Was any of this what the European states signed up for with the 1950 establishment of the European Coal and Steel Community (ECSC), the promise being a limited economic cooperative agreement between a handful of Western European states that has now somehow ballooned into a sprawling bureaucracy dictating what emojis some Pole is permitted to use on Facebook?

“The problem is, Cole Allen did believe the rhetoric to the point of allegedly attempting to murder Trump administration officials at the dinner on April 25.”

• Erika Kirk Brilliantly Dismantles White House Correspondents’ Hypocrisy (Salgado)

Erika Kirk slammed attendees at the White House correspondents’ dinner who inspired the shooter’s hate but had intended to enjoy a luxury dinner with Donald Trump undisturbed, calling it the “ultimate hypocrisy” to “manufacture the hate and then profit off the results.” The crazies were “willing to have dinner with ‘Hitler’” if it meant free champagne.Read more …

Leftists believe in hurling the most inflammatory and vile rhetoric at their opponents, ginning up as much violence and chaos as possible, but never personally experiencing the negative results of any of their own lies. The same journalists and media anchors who spent years calling Donald Trump the greatest threat to democracy were cheerfully attending a dinner with him as the featured speaker, illustrating they didn’t really believe their own extreme rhetoric, as Erika highlighted. The problem is, Cole Allen did believe the rhetoric to the point of allegedly attempting to murder Trump administration officials at the dinner on April 25.“We may have big problems with illegal immigration in this country,” Erika said. “I have to tell you, we have an even bigger problem when it comes to the systemic indoctrination and radicalization of our own citizens. This is what got my husband killed.” It’s what inspired Cole Allen.

Charlie Kirk wanted his wife Erika to take over as head of his organization, Turning Point USA, if anything ever happened to him. Since her husband’s tragic assassination, she has managed to deal simultaneously with her own grief and that of her young children while also zealously carrying on Charlie’s legacy — all while sickos vilify her. She was understandably very traumatized by the assassination attempt at the White House Correspondents’ Dinner, but that did not stop her from continuing to tell the truth afterward with courage.

She emphasized, “Many of the left-wing journalists that attended the WHCD have spent years consistently calling President Trump a ‘Nazi’, a ‘threat to democracy’, and ‘Hitler’,yet they still joyfully attended the evening’s event.” But if “they truly believed their own rhetoric, they’re either joyfully willing to have dinner with ‘Hitler’ or they’re lying to radicalize American citizens with narratives they know are grossly exaggerated.”

Sunday -weekend- interviews.

• Extensive Interview with Treasury Secretary Scott Bessent (CTH)

Treasury Secretary Scott Bessent appears on Fox News with Maria Bartiromo to discuss current geopolitical events and the ramifications for the U.S. economy. It is a rather lengthy interview and discussion that touches on numerous key points. Bessent notes the upcoming meeting between President Trump and Chairman Xi of China is still on schedule and U.S. Operation Financial Fury against Iran is yielding good results. I had no idea the U.S. government has made $30 to $40 billion from the Intel backstop.Read more …

“..when people argue that it’s not about the economics of the thing – remind them, it’s always about the economics of the thing.”

• Interesting Reversal in Position by German Chancellor Friedrich Merz (CTH)

Six days ago, in Marsberg, German Chancellor Friedrich Merz criticized the U.S. approach to Iran, saying Washington was being “humiliated by the Iranian leadership” and demanding the conflict end “as quickly as possible.” Three days ago, President Trump responded with an announcement that U.S. troops in Germany would be drawn down, and there would be a 25% tariff on all imported European autos. {GO DEEP} Suddenly, Friedrich Merz reverses his position:Read more …

The United States is and will remain Germany‘s most important partner in the North Atlantic Alliance. We share a common goal: Iran must not be allowed to acquire nuclear weapons.

— Bundeskanzler Friedrich Merz (@bundeskanzler) May 3, 2026

Imagine that.But seriously folks, when people argue that it’s not about the economics of the thing – remind them, it’s always about the economics of the thing. Germany is facing a perfect storm of economic consequences following their decision to chase the climate change agenda (Build Back Better) and eliminate their coal and nuclear power plants. Combine the German/EU policy to stop purchasing cheap LNG and oil from Russia, in addition to skyrocketing energy costs from oil/gas flows from the Middle East, and the outcome is rising manufacturing costs leading to massive layoffs.

The German industrial economy is the heart of the EU economy, and President Trump is now hitting them both right where it hurts.Chancellor Friedrich Merz is already facing serious political issues within Germany as the economy continues to contract. The political opposition parties are on the rise and Merz is in a very precarious position. President Trump is exploiting this vulnerability by apply further economic pressure on Germany.

Just yesterday….

Via Bloomberg – “Germany’s automotive industry pleaded for an urgent de-escalation in the tariff dispute between the US and the European Union and called for immediate talks between the two sides after President Donald Trump said he would increase auto tariffs on the bloc next week.”

Let him cook.

President Donald Trump's plan to withdraw at least 5,000 US troops from Germany has raised concerns among residents living near Ramstein Air Base. pic.twitter.com/hllQNYiuYg

— DW News (@dwnews) May 3, 2026

“..there has been nothing going on, no hostilities, no exchange of fire since – in almost a month, in almost a month. And how do you end a conflict? How do you end this? You have a ceasefire. ”

• Acting AG Todd Blanche On Legal Aspects of Iran, James Comey and More (CTH)

Acting Attorney General Todd Blanche appears on NBC News to discuss the legal framework for the Iran conflict and push back against the media’s defense of James Comey.Read more …

[Transcript] – KRISTEN WELKER: And joining me now is acting Attorney General Todd Blanche. Mr. Blanche, welcome back to Meet the Press.ACTING ATTORNEY GENERAL TODD BLANCHE: Good morning.

KRISTEN WELKER: Good morning. Thank you for being here in person.

ACTING ATTORNEY GENERAL TODD BLANCHE: Of course.

KRISTEN WELKER: We really appreciate it. Let’s start right there with the war. As you know, the War Powers Act requires Congress to authorize military action beyond 60 days, which the U.S. passed on Friday. The president did send a letter to Congress, just to recap, saying that hostilities have been terminated, given the ceasefire that was put in place on April 7th. And yet, the U.S. is actively engaged in a naval blockade of Iranian ports as part of this conflict. Is the United States at war with Iran?

ACTING ATTORNEY GENERAL TODD BLANCHE: No. I mean, what President Trump said this weekend is absolutely true. My job as the acting attorney general is to make sure that the president, that we all are doing the right thing legally. And we absolutely are. As we said to Congress last week, there has been nothing going on, no hostilities, no exchange of fire since – in almost a month, in almost a month. And how do you end a conflict? How do you end this? You have a ceasefire. And that’s exactly what we have, and Congress knows that and the leadership knows that. And there’s a lot of drama. I’m sure that Senator Schiff will come on here and say something different. This has been done repeatedly for many, many years, with many, many presidents. And there’s nothing inconsistent about what we’re doing and what’s been done in the past.

-Orthodox- Greece was occupied by the -muslim- Ottoman empire for a very long time. That’s the background.

• Greece Rejects Ukraine’s Terms For Naval Drone Deal – Media (RT)

Negotiations between Ukraine and Greece over the joint production of naval drones have stalled because Kiev wants to retain control over how Athens can use the technology, local media have reported. According to Greek Reporter, the countries agreed last November that Ukraine would supply components for drones to be built at shipyards in Greece, while Greek companies would manufacture electronic and optical systems. The end result would have been an improved version of the Magura-type attack drones which Kiev uses against Russia.Read more …

The newspaper Kathimerini reported on Thursday, however, that Ukrainian officials had demanded that Kiev retain a say over how the Greek military would use the drones, a condition Athens rejected. Greece believes Ukraine set these terms to “maintain a balance” with its longtime rival Türkiye, the newspaper said.Greece and Türkiye have long accused each other of fueling tensions, with Athens reportedly opposing Ankara’s bid to join the EU’s Drone Wall program aimed at improving the bloc’s ability to detect and intercept hostile UAVs. Türkiye hosted Russian-Ukrainian peace talks in 2022 and 2025, presenting itself as a neutral mediator in the conflict. Ankara also condemned Ukrainian attacks on Russian-linked tankers near the Turkish coast last year.

“Edward Juul Rod-Larsen, 25, was found dead in Oslo days after French and Norwegian police reportedly launched a joint investigation into his parents,”

• Epstein Inheritor Kills Himself (RT)

The son of two senior Norwegian diplomats under investigation over ties to late sex offender Jeffrey Epstein has taken his own life, Norwegian newspaper VG reported earlier this week, citing lawyers for the family. Edward Juul Rod-Larsen, 25, was found dead in Oslo days after French and Norwegian police reportedly launched a joint investigation into his parents, Mona Juul and Terje Rod-Larsen. The probe is centered around allegations that the disgraced US financier had helped the couple purchase an apartment, and left $5 million to each of their two children in his will.Read more …

The probe is part of widening international fallout from the latest release of millions of Epstein documents, which have triggered criminal investigations, arrests, and resignations across politics, business, and even royalty. Epstein, who pleaded guilty in 2008 to soliciting sex from a minor and served 13 months of an 18-month sentence, was arrested again in 2019 on federal sex trafficking charges. He died by suicide in his jail cell ahead of his trial. The US Department of Justice has gradually released materials related to the case under the Epstein Files Transparency Act, signed into law by US President Donald Trump.The released documents mention numerous high-profile figures, linking some to Epstein’s network or questionable financial dealings. The disclosures have triggered resignations, probes, and reviews worldwide, with many acknowledging contact but denying wrongdoing, with some charges brought in a limited number of cases. Last month, Former Norwegian Prime Minister Thorbjorn Jagland was hospitalized after a reported suicide attempt, days after being charged with gross corruption over accepting Epstein’s hospitality. World Economic Forum CEO Borge Brende stepped down over dinners and communications with the disgraced financier.

In the US, the release has placed renewed scrutiny on former President Bill Clinton and his wife, former Secretary of State Hillary Clinton. Both have been deposed about their associations with Epstein, but have denied knowledge of his trafficking operation.

Commenting on the disclosures, Russian Foreign Ministry spokeswoman Maria Zakharova described the scandal as exposing the “pure Satanism” at the heart of the collective West, accusing Western elites of inventing threats from Russia to distract from their own “monstrous crimes.”

“Now, replace [Germany] with [Canada]

• Volkswagen to Let Chinese Automaker Build in Shuttered Volkswagen Plants (CTH)

How do you sum up the economic forecast for Europe? This story highlights one of the craziest stories in a long time. This is so blindingly suicidal, it cannot be stupidity. This is intentional. BACKGROUND – You might remember last year due to climate/carbon emission regulations inside Europe EU automakers had to pay fines to the EU Commission if they did not meet electric vehicle targets. In order to avoid the penalties many EU automakers began purchasing ‘carbon credit’ offsets from Chinese EV automakers.

European car makers were paying China for carbon credits, and Chinese car companies began using the payments to lower prices. Europe was, essentially, paying China to undercut their own auto market. The result was European car makers, specifically those in Germany, losing market share to lower price EVs from China. German industry began shrinking. If that wasn’t crazy enough, what comes next is beyond laughable. As a result of lost sales and diminished volumes, Volkswagen had shut down auto plants. Now, Volkswagen is announcing that Chinese automakers, their China “partners,” will take over the underutilized facilities and start building Chinese cars in Germany.GERMANY – Volkswagen Group is facing increased pressure from its board to further cut costs despite already announcing radical measures, such as axing around 50,000 jobs in Germany by 2030 and reducing production capacity by up to 3 million units per year to 9 million, which would make it very difficult to avoid plant closures or sales. Overall, Europe’s largest automaker aims to reduce costs by 20% by the end of 2028. bIn an attempt to mitigate the effect of these measures, the automaker appears ready to do what not too long ago would have seemed unthinkable, namely selling China-developed cars in Europe and even sharing its underutilized plants in the region with its Chinese partners.

That’s what CEO Oliver Blume told investors and analysts on April 30 after presenting the company’s first-quarter 2026 results, which saw the automaker’s profit drop 14% to $2.92 billion amid higher U.S. tariffs and intense competition from Chinese carmakers. In order to deal with excess capacity in Europe and rising competition from Chinese brands in Europe in the coming years, Blume said VW Group is considering selling China-built cars in Europe. It’s the first time that Volkswagen has acknowledged it is contemplating such a move. (read more)

SUMMARY: Volkswagen went to China to sell cars. Volkswagen opened EV auto plants in China bringing in German industrial technology and equipment. China learned from Volkswagen and started their own EV auto companies to compete. Volkswagen EV sales in China started dropping dramatically, and the Chinese EV brands took over. Due to internal climate regulations in Europe, Volkswagen in the EU then begins giving money to China that subsidizes their competition. China exports their EVs to Europe. Volkswagen EV auto plants start closing. China now takes control of the Volkswagen EV auto plants to build Chinese EVs in Germany.

With operations now inside the house, the Chinese government extract European wealth and pump subsidies into their EV operations in Germany, flooding the European market with cheap EVs that will undercut the German auto manufacturing sector. You cannot make steel with windmills and solar panel energy. Germany has destroyed much of their coal and nuclear power plants. German energy prices have skyrocketed. German steel is expensive. German cars are expensive as a result. Where do you think the inexpensive steel for the ultra-cheap Chinese EVs will come from?

Now, replace [Germany] with [Canada].

We now have clear evidence that the COVID shots have crippled the reproductive capacity of humanity.

— Nicolas Hulscher, MPH (@NicHulscher) May 3, 2026

In animal models, they destroy over 60% of women’s non-renewable egg supply.

In human data (n=1.3 MILLION), vaccinated women have ~33% fewer successful pregnancies than… https://t.co/67w7BgvvFN pic.twitter.com/vkZvI505G4

https://twitter.com/MikeBales/status/2050884796725788721?s=20The Mysterious Deaths Surrounding the Clintons

— The SCIF (@TheSCIF) May 3, 2026

12 of their own bodyguards past away alone.

Nobody has 47+ people close to them who all mysteriously died or took their own life.

– James McDougal: Apparent "heart attack"

– Mary Mahoney: Murdered

– Vince Foster: Gunshot to head,… pic.twitter.com/D8OmwN4cB5

The Acropolis in Athens as never been seen before – Experience ancient Greece as it truly was pic.twitter.com/qlLmPlN8W3

— Ancient History Hub (@AncientHistorry) May 2, 2026

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.