DPC Main Street, Buffalo, NY 1900

And Spain and Italy are watching its every move.

• ECB Turns The Screws On Greek Banks (Kathimerini)

The bank holiday has been extended by at least two days (until Wednesday night), but local lenders are now just a step away from serious solvency problems after the ECB decided on Monday to increase the haircut on the collateral they use to draw liquidity. Frankfurt’s decision sent shock waves through Greece’s banking sector as hardly anyone had expected it would use a haircut on collateral to send its own message before the political decisions expected on Tuesday in Brussels. In doing so, the ECB is further increasing the pressure on the Greek government to agree to a deal at Tuesday’s eurozone summit, otherwise the country’s banks may face a sustainability problem on top of their liquidity woes.

The haircut increase reduces the last cash banks can draw from the emergency liquidity assistance (ELA) by two-thirds, running the risk of finding themselves unable to complete any transactions and thus be deemed insolvent. The European Stability Mechanism (ESM) warned late last week that Greece’s failure to pay a €1.6 billion tranche to the IMF on June 30 constitutes a payment default and allows the ESM to immediately demand all the funds it has lent to Greece and confiscate all bank shares controlled by the Hellenic Financial Stability Fund (HFSF). Banks estimate that after Monday’s decision the ceiling on the cash available for them to withdraw has dropped from €18 billion before the haircut increase to just €5 billion.

A similar increase at Wednesday’s ECB meeting would mean that Greek banks would be unable to cover the liquidity they have already drawn with new collateral. The ECB also kept the limit on the ELA available to Greek lenders unchanged and will review the situation at Wednesday’s meeting, i.e. after the completion of Tuesday’s eurozone summit. Bank officials are clearly saying that the country has reached the point of no return and is at risk of bankruptcy unless there is an immediate agreement between the SYRIZA-led government and Greece’s creditors.

“..the bulk of transactions today are electronic, meaning we are dealing with an accounting issue more than anything. The euro existed electronically BEFORE it became printed money; Greece should do the same right now.”

• Greece Should Immediately Begin To Print Drachma (Martin Armstrong)

Brussels has been dead wrong. The stupid idea that the euro will bring stability and peace, as it was sold from the outset, has migrated to European domination as if this were “Game of Thrones”. Those in power have misread history, almost at every possible level. The assumption that the D-marks’ strength was a good thing that would transfer to the euro has failed because they failed to comprehend the backdrop to the D-mark. Germany moved opposite of the USA toward extreme austerity and conservative economics because of its experience with hyperinflation. The USA moved toward stimulation because of the austerity policies that created the Great Depression, which led to a shortage of money, and many cities had to issue their own currency just to function.

The federal government thought, like Brussels today, that they had to up the confidence in the bond market and that called for raising taxes and cutting spending at the expense of the people. The same thinking process has played out numerous times throughout history. Our problem is that no one ever asks – Hey, did someone try this before? Did it work? This is why history repeats – we do ZERO research when it comes to economics. It is all hype and self-interest. Greece should immediately begin to print drachma. By no means has the introduction of a new currency been a walk in the park. There is always a learning curve, as in the case of East Germany’s adoption of the Deutsche mark, the Czech-Slovak divorce of 1993, and the creation of the euro itself .

However, the bulk of transactions today are electronic, meaning we are dealing with an accounting issue more than anything. The euro existed electronically BEFORE it became printed money; Greece should do the same right now. The difference concerning East Germany and others was the fact that there was no history. This is more akin to the 1933 devaluation of the dollar by FDR whereby an executive order reneged on promises to pay prior debt in gold. This would be similar. The new drachma should be issued at two-per euro, only because the people will think the drachma should be worth less than a euro based on pride. If the new drachma is issued at par, the speculators will sell, assuming it will decline. Issue it at 50% and you will eventually see the opposite trend emerge once people see the contagion begin to spread.

Brussels already cut off the banks in Greece. All accounts in Greece should be electronically switched to drachmas. Begin to issue printed drachma for small change. The umbilical cord to Brussels must be cut immediately for Greece to stand on its own. You cannot negotiate with people who will not change their view of the world, for their own self-interest will cloud their perspective. All EXTERNAL debt should be suspended. Any future resolution of debt should be reduced by 50% to account for the overvaluation of prior debt, thanks to the euro, and any interest previously paid should be deducted from the total loan.

She’s got it upside down.

• Giving In To Greece Could ‘Blow Apart’ The Euro, Warns Merkel (DM)

Germany warned last night that the euro could ‘blow apart’ if the single currency’s members give in to demands from Greece to water down austerity measures. Angela Merkel and Francois Hollande were locked in a bitter stand-off ahead of yet another bid by eurozone leaders to prevent the debt-ridden state crashing out of the single currency. Athens yesterday extended its ‘bank holiday’ until at least Thursday after the European Central Bank deferred a decision on whether to continue propping up the country’s financial institutions. But one American hedge fund, Balyasny, yesterday warned investors that Greek banks were on the verge of running dry, leaving the country 48 hours from civil unrest.

In a further signal that Greece’s financial woes could spark a wider geo-political crisis for the West, Greek Prime Minister Alexis Tsipras yesterday held talks by phone with Russian President Vladimir Putin. Moscow said the call had been arranged ‘at the request’ of Mr Tsipras, with the two men discussing the outcome of the referendum. Some observers believe Moscow could agree to bail out Greece in return for Athens blocking further EU sanctions against Russia. France was last night pushing for an EU brokered deal, with Mr Hollande saying it was vital to Europe to show ‘solidarity’ with Greece. The French President said ‘the door is open’ to further discussions with Mr Tsipras, who is expected to table fresh proposals in Brussels today.

But Germany gave no sign it is willing to back down in the face of the Greek referendum on Sunday, when voters overwhelmingly rejected the austerity measures demanded as a condition of future bailout funds. Mrs Merkel said the conditions for a deal ‘are not there yet’. She added: ‘We have already shown a great deal of solidarity to Greece and the latest proposal put forward to them was extremely generous.’ Sigmar Gabriel, the German vice-chancellor and economy minister, said there could be no question of writing off Greek debt because other countries that have had loans such as Ireland, Portugal and Spain would demand equal treatment.

Empty rethoric.

• Merkel Warns Greece Time Is Running Out to Save Place in Euro (Bloomberg)

Greek Prime Minister Alexis Tsipras was given hours to come up with a plan to keep his country in the euro as citizens endure a second week of capital controls. German Chancellor Angela Merkel said “time is running out” as she and French President Francois Hollande, leaders of the two biggest countries in the euro bloc, responded to Sunday’s referendum. The European Central Bank piled on the pressure by making it tougher for Greek banks to access emergency loans. Finance ministers and leaders from the 19-member region gather Tuesday.

After promising Greek voters a “no” outcome against austerity would strengthen his negotiating hand, the onus is on Tsipras to prove he can get a deal with creditors insistent on tax hikes and spending cuts as the price for a new bailout of Europe’s most indebted nation. “The last offer that we made was a very generous one,” Merkel said Monday at the Elysee Palace in Paris. “On the other hand, Europe can only stand together, if each nation takes on its own responsibility.” Heading into the Brussels talks – 1 p.m. for the finance chiefs, and 6 p.m. for the leaders – Greece made a pre-emptive concession to its trio of creditors with the resignation of outspoken Finance Minister Yanis Varoufakis who clashed with his counterparts from other countries, especially Germany’s Wolfgang Schaeuble.

U.S. President Barack Obama spoke by phone with Hollande and the two agreed on the need for a way forward that’ll allow Greece to resume reforms and return to growth within the euro area, according to a White House statement. Treasury Secretary Jack Lew spoke with Tsipras and new finance chief Euclid Tsakalotos and urged a constructive outcome. With bank closures extended through Wednesday to stem deposit withdrawals, Greek lenders are being kept on the equivalent of a drip feed by the ECB.

She won’t Philippe. She’s dug in deeply.

• Be Bold, Frau Merkel (Philippe Legrain)

The Greek people have spoken, delivering a defiant oxi (no) to their creditors’ terms. Blackmailed with the threat of being forced out of the eurozone and under siege in an economy starved of cash by the political European Central Bank, Greeks resoundingly rejected — by 61.3% to 38.7% — the prospect of being a permanently depressed colony bled dry by their incompetent creditors. Now what? Most spreadsheet shifters and politicians on the creditor side want to persist with the logic of confrontation. To quote Oscar Wilde, they know “the price of everything and the value of nothing.” But even in narrow accounting terms, their strategy is flawed: Contrary to their expectations, Greeks have not surrendered, and pushing them out of the eurozone would be more costly to the creditors than clinching a deal.

Besides, the stakes are much bigger than that. Does the eurozone really want to be an empire that tramples on democracy and crushes dissent? Is fear enough to hold it together, or might disintegration have a domino effect? What about the cost of neglecting all the other big issues that Europe’s leaders ought to be addressing? For everyone’s sake, it is time to break free of the narrow, destructive logic of creditor nationalism and draw a line under the Greek crisis.For everyone’s sake, it is time to break free of the narrow, destructive logic of creditor nationalism and draw a line under the Greek crisis. The creditors pretend their small-mindedness is a point of principle: Everyone has to obey eurozone rules, and these stipulate that governments must pay their debts. Except they don’t stipulate that.

Nowhere in the Maastricht Treaty that created the euro does it state that governments have to pay their debts in full. How could it? Sometimes they can’t. But instead of creating a mechanism for restructuring the debts of an insolvent sovereign, the treaty drafters left a blank in the hope that such a situation would never arise. They did stipulate, though, that governments should not bail out their peers. When Greece became insolvent in 2010, its debts ought to have been restructured, as independent analysts and IMF experts advised. Instead, eurozone governments made a catastrophic policy choice. Insisting that debts were sacrosanct and the stability of the entire eurozone was at stake, they decided to breach the no-bailout rule and lend European taxpayers’ money to Greece. As Karl Otto Pöhl, the former president of the Bundesbank, put it: “It was about protecting German banks, but especially the French banks, from debt write-offs.… Now we have this mess.”

Critics contend that this is ancient history, but it isn’t. That tragic decision and subsequent mistakes have transformed the political economy of the eurozone. Initially a voluntary union of equal member states, it has become a hierarchical relationship in which eurozone institutions have become instruments for creditors to impose their will on debtors. The bailout of Greece’s private creditors has also set Europeans against each other: Germans, Spaniards, Slovaks, and others now have an interest in resisting the debt relief that Greece needs to recover. To find an amicable solution to the Greek crisis, the eurozone needs to escape from this destructive logic.

“The debt providers and caretakers of debt basically accuse the Syriza government of not feeling enough guilt – they are accused of feeling innocent.”

• Europe: The Paradox Of The Superego (New Statesman)

In western Europe we like to look on Greece as if we are detached observers who follow with compassion and sympathy the plight of the impoverished nation. Such a comfortable standpoint relies on a fateful illusion – what has been happening in Greece these last weeks concerns all of us; it is the future of Europe that is at stake. So when we read about Greece, we should always bear in mind that, as the old saying goes, de te fabula narrator (the name changed, the story applies to you). An ideal is gradually emerging from the European establishment’s reaction to the Greek referendum, the ideal best rendered by the headline of a recent Gideon Rachman column in the Financial Times: “Eurozone’s weakest link is the voters.”

In this ideal world, Europe gets rid of this “weakest link” and experts gain the power to directly impose necessary economic measures – if elections take place at all, their function is just to confirm the consensus of experts. The problem is that this policy of experts is based on a fiction, the fiction of “extend and pretend” (extending the payback period, but pretending that all debts will eventually be paid). Why is the fiction so stubborn? It is not only that this fiction makes debt extension more acceptable to German voters; it is also not only that the write-off of the Greek debt may trigger similar demands from Portugal, Ireland, Spain. It is that those in power do not really want the debt fully repaid. The debt providers and caretakers of debt accuse the indebted countries of not feeling enough guilt – they are accused of feeling innocent.

Their pressure fits perfectly what psychoanalysis calls “superego”: the paradox of the superego is that, as Freud saw it, the more we obey its demands, the more we feel guilty. Imagine a vicious teacher who gives to his pupils impossible tasks, and then sadistically jeers when he sees their anxiety and panic. The true goal of lending money to the debtor is not to get the debt reimbursed with a profit, but the indefinite continuation of the debt that keeps the debtor in permanent dependency and subordination. For most of the debtors, for there are debtors and debtors. Not only Greece but also the US will not be able even theoretically to repay its debt, as it is now publicly recognised. So there are debtors who can blackmail their creditors because they cannot be allowed to fail (big banks), debtors who can control the conditions of their repayment (US government), and, finally, debtors who can be pushed around and humiliated (Greece).

The debt providers and caretakers of debt basically accuse the Syriza government of not feeling enough guilt – they are accused of feeling innocent. That’s what is so disturbing for the EU establishment about the Syriza government: that it admits debt, but without guilt. They got rid of the superego pressure. Varoufakis personified this stance in his dealings with Brussels: he fully acknowledged the weight of the debt, and he argued quite rationally that, since the EU policy obviously didn’t work, another option should be found.

And who shouldn’t have to.

• Yanis Varoufakis: The Economist Who Wouldn’t Play Politics (Paul Mason)

Why did Varoufakis go? The official reason, on his blog, was pressure from creditors. But there are a whole host of other reasons that made it easier for him to decide to yield to it. First, though he came from the centre-left towards Syriza, Varoufakis ended up consistently taking a harder line than many others in the Greek cabinet over the shape of the deal to be done, and the kind of resistance they might have to unleash if the Germans refused a deal. Second, because Varoufakis is an economist, not a politician. His entire career, and his academic qualifications are built on the conviction that a) austerity does not work; b) the Eurozone will collapse unless it becomes a union for recycling tax from rich countries to poor countries; c) Greece is insolvent and its debts need to be cancelled.

By those measures, any deal Greece can do this week will falls short of what he thinks will work. On top of that, politicians are built for compromise. Tsipras has to work the party machine, the government machine, the machine of parliament. Varoufakis’ machine is his own brain. If he wound up the creditors it was for a reason: they’d convinced themselves that Tsipras was a Greek Tony Blair and would simply betray his promises and compromise on taking office. The lenders detested Varoufakis because he looked and sounded like one of them. He spoke the language of the IMF and ECB, and turned their own logic against them. But he achieved his objective: he convinced the lenders Greece was serious.

Varoufakis critics in Greek politics accused him of flamboyant gestures and adopting a stance he could not deliver on. His critics in Syriza believed from the outset he was “a neo-liberal”. Among the lenders it was always the north European politicians who could not live with Varoufakis. Though he was at odds with the IMF’s Christine Lagarde and at odds with the IMF over all matters of substance they at least spoke the same language. His policy was total honesty, and when it could not be honesty in public it was honesty in private. He exploded the world of Brussels journalism, which had become back-channel stenography, by publishing the key documents, usually sometime after midnight.

Trojan horse.

• Tsipras Taps Longtime Ally to Soothe Debt Confrontation (Bloomberg)

Greek Prime Minister Alexis Tsipras is counting on a change of style, if not necessarily substance, by turning to a longtime ally to seek a deal with creditors to keep his nation in the euro. Euclid Tsakalotos was named finance minister to replace Yanis Varoufakis, who resigned Monday after more than five months of fruitless back-and-forth. An Oxford-educated economist who was previously deputy foreign minister, Tsakalotos had already begun to take a leading role in debt talks before Tsipras’s surprise referendum call brought them to a halt on June 27. Tsipras is betting that a new, less confrontational face will help him bring German Chancellor Angela Merkel and other European leaders back to the table after Greeks voted to reject further austerity in Sunday’s vote.

Varoufakis had vowed to “cut off my arm” rather than sign a bad deal, and was involved in a long series of spats with negotiating partners in his six months on the job. “It’s an important symbolic and necessary move,” Famke Krumbmuller, an analyst at political consultancy Eurasia Group, said by e-mail. Creditors “now really need to see the trust restored by a serious and credible commitment from the Greek side to implement reforms,” she said. Time is running short: Greek banks are almost out of cash and commerce is grinding to a halt in the absence of a new bailout deal and lifeline from the ECB. Tsipras’s government has extended bank closures and capital controls through Wednesday to stem withdrawals. [..]

Tsakalotos became more prominent in Greece’s debt negotiations in June as relations between Varoufakis and creditors worsened. Varoufakis today said he was resigning because “there was a certain preference” among some European governments that he be “absent” from the next round of talks, if and when they begin. Though Tsakalotos’s button-downed style may help endear him to creditors, he’s still a staunch supporter of Syriza’s more radical policies and a harsh critic of European austerity, putting him on the opposite side of the ideological spectrum from key politicians including Germany’s Wolfgang Schaeuble.

That’s all the flavors we have.

• The Euro: Austerity vs Democracy (Aditya Chakrabortty)

The challenge facing Europe today goes far wider and deeper than how to handle a small bankrupt country holding only 2% of the EU’s population. No, the bigger question is this: can Europe handle democracy, however awkward and messy and downright truculent it may be? The answer to that will probably decide whether the euro lives on as the currency of 19 nations. Say what you like about the referendum held in Greece this Sunday, it was democracy at its most raw. Yes, the ballot question was impenetrable, and Alexis Tsipras, the Greek prime minister, came close to urging voters to say oxi (no) to a deal he’d pretty much said nai (yes) to just a couple of days earlier.

Yet in the face of the country’s political and media establishment warning Greeks to vote yes – echoing every major European leader (and quite a few faceless ones) – and the shock-and-awe tactics of the ECB in pulling the plug on Greek banks, the country still delivered a loud no to austerity, troika-style. Intelligent pragmatists might look at that landslide and argue that it is time for the troika – made up of the EU, ECB and IMF – to react by altering both policy and tone. My colleague Jonathan Freedland neatly expressed that attitude on these pages a couple of days ago, petitioning the European commission, the ECB and the IMF “to demonstrate that the euro and austerity are not synonymous terms”.

I sympathise with Freedland’s view – but am far more pessimistic about the ability of the euro’s leading powers to change course. Austerity is not some policy mistake the eurozone’s leaders have absent-mindedly made – like a weekend motorist blindly following the satnav into a cul-de-sac. On the contrary, the bone-headed and self-defeating policy of forcing Greece to make severe spending cuts amid an economic depression is a direct product of the eurozone’s lack of democracy. Just how closely fused austerity and the eurozone’s unrepresentative politics are can be seen from the insistence of European leaders in the run-up to the referendum that any vote against austerity was tantamount to a vote for leaving the euro.

That attitude reached its apex in the insistence last week of Martin Schulz, the European parliament president, that the troika could only deal with Greece if it were represented by an unelected “technocratic government”. This is the former leader of the European parliament’s Progressive Alliance of Socialists & Democrats calling for regime change against an elected government.

Still the main story on Greece.

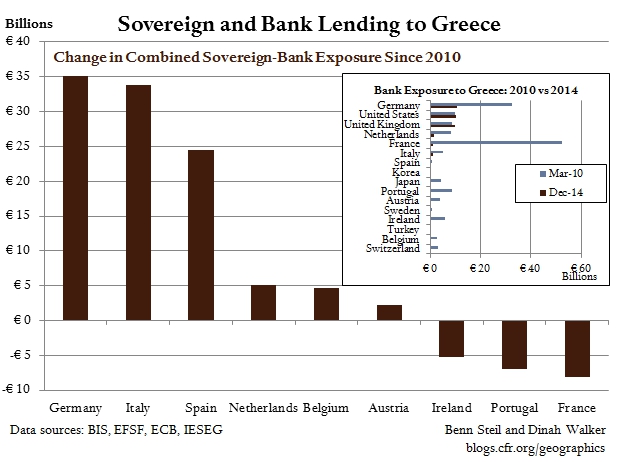

• Italy and Spain Have Funded a Massive Backdoor Bailout of French Banks (CFR)

In March 2010, two months before the announcement of the first Greek bailout, European banks had €134 billion worth of claims on Greece. French banks, as shown in the right-hand figure above, had by far the largest exposure: €52 billion – this was 1.6 times that of Germany, eleven times that of Italy, and sixty-two times that of Spain. The €110 billion of loans provided to Greece by the IMF and Eurozone in May 2010 enabled Greece to avoid default on its obligations to these banks. In the absence of such loans, France would have been forced into a massive bailout of its banking system. Instead, French banks were able virtually to eliminate their exposure to Greece by selling bonds, allowing bonds to mature, and taking partial write-offs in 2012. The bailout effectively mutualized much of their exposure within the Eurozone.

The impact of this backdoor bailout of French banks is being felt now, with Greece on the precipice of an historic default. Whereas in March 2010 about 40% of total European lending to Greece was via French banks, today only 0.6% is. Governments have filled the breach, but not in proportion to their banks’ exposure in 2010. Rather, it is in proportion to their paid-up capital at the ECB – which in France’s case is only 20%. In consequence, France has actually managed to reduce its total Greek exposure – sovereign and bank – by €8 billion, as seen in the main figure above. In contrast, Italy, which had virtually no exposure to Greece in 2010 now has a massive one: €39 billion. Total German exposure is up by a similar amount – €35 billion. Spain has also seen its exposure rocket from nearly nothing in 2009 to €25 billion today.

In short, France has managed to use the Greek bailout to offload €8 billion in junk debt onto its neighbors and burden them with tens of billions more in debt they could have avoided had Greece simply been allowed to default in 2010. The upshot is that Italy and Spain are much closer to financial crisis today than they should be.

They will and should.

• Greece May Apply For BRICS bank, But Not Discussed Officially – Putin Aide (RT)

Although there are speculations in the media about Greece applying to join the BRICS bank, the issue hasn’t been discussed at an official level, one of President Putin’s top aides told RT, VGTRK and Ria in an interview. Rumors about Greece possibly joining the bank emerged ahead of the leaders of Russia, China, Brazil, India and South Africa preparing to launch their own development bank at a the seventh summit of the organization in Russia’s Ufa later this week. “There has been speculation in the media that Greece may apply for accession to the New Development Bank. We know of these assumptions, but so far no one has officially discussed such an option with us,” Yury Ushakov, President Putin’s aide, said.

The top official revealed that the upcoming discussions are going to “touch on the parameters of the practical operation of the BRICS’ New Development Bank (NDB) and currency reserve pool.” “They don’t constitute an attempt to oppose the International Monetary Fund or the World Bank,” Ushakov stressed. These institutions are rather new instruments for “addressing our shared objectives,” he said. The NDB is just launching its operations, Ushakov noted, and it still has to “set out its priorities and start to function.” “And it certainly won’t start its operations with Greece,” Ushakov added, pointing out that the NBD has “its own tasks and challenges to deal with.”

The issue of Greece is going to be discussed anyway, but not in the context of its accession to the NDB “even in the long term,” the presidential aid said. The BRICS’ New Development Bank has an initial capital of $US 50 blillion and is believed to have triggered a major reshape of the Western-dominated financial system. The NDB is expected to be up and running by the end of the year. The BRICS countries are also busy creating an alternative to the US-dominated western SWIFT payment system.

Revealing.

• Mario Draghi, Goldman Sachs and Greece (Zero Hedge)

Back in June 2012, the ECB, whose head was the recently crowned Mario Draghi who had less than a decade ago worked at none other than Goldman Sachs, was sued by Bloomberg’s legendary Mark Pittman under Freedom of Information rules demanding access to two internal papers drafted for the central bank’s six-member Executive Board. They show how Greece used swaps to hide its borrowings, according to a March 3, 2010, note attached to the papers and obtained by Bloomberg News. The first document is entitled “The impact on government deficit and debt from off-market swaps: the Greek case.” The second reviews Titlos Plc, a securitization that allowed National Bank of Greece SA, the country’s biggest lender, to exchange swaps on Greek government debt for funding from the ECB, the Executive Board said in the cover note. From Bloomberg:

In the largest derivative transaction disclosed so far, Greece borrowed €2.8 billion from Goldman Sachs in 2001 through a derivative that swapped dollar- and yen-denominated debt issued by the nation for euros using a historical exchange rate, a move that generated an implied reduction in total borrowings.

“The Greek authorities had never informed Eurostat about this complex issue, and no opinion on the accounting treatment had been requested,” Eurostat, the Luxembourg-based statistics agency, said in a statement. The watchdog had only “general” discussions with financial institutions over its debt and deficit guidelines when the swap was executed in 2001. “It is possible that Goldman Sachs asked us for general clarifications,” Eurostat said, declining to elaborate further.

The ECB’s response: “the European Central Bank said it can’t release files showing how Greece may have used derivatives to hide its borrowings because disclosure could still inflame the crisis threatening the future of the single currency.”

Considering the crisis of the (not so) single currency is very much “inflamed” right now as it is about to be proven it was never “irreversible”, perhaps it is time for at least one aspiring, true journalist, unafraid of disturbing the status quo of wealthy oligarchs and central planners, to at least bring some closure to the Greek people as they are swept out of the Eurozone which has so greatly benefited the very same Goldman Sachs whose former lackey is currently deciding the immediate fate of over €100 billion in Greek savings.

Because something tells us the reason why Mario Draghi personally blocked Bloomberg’s FOIA into the circumstances surrounding Goldman’s structuring, and hiding, of Greek debt that allowed not only Goldman to receive a substantial fee on the transaction, but permitted Greece to enter the Eurozone when it should never have been allowed there in the first place, is that the person who oversaw and personally endorsed the perpetuation of the Greek lie is none other than Goldman’s Vice Chairman and Managing Director at Goldman Sachs International from 2002 to 2005. The man who is also now in charge of the ECB. Mario Draghi.

Big bust in the making.

• As China Intervenes to Prop Up Stocks, Foreigners Head for Exits (Bloomberg)

Foreign investors are selling Shanghai shares at a record pace as China steps up government intervention to combat a stock-market rout that many analysts say was inevitable. Sales of mainland shares through the Shanghai-Hong Kong exchange link swelled to an all-time high on Monday, while dual-listed shares in Hong Kong fell by the most since at least 2006 versus mainland counterparts. Options traders in the U.S. are paying near-record prices for insurance against further losses after Chinese stocks on American bourses posted their biggest one-day plunge since 2011. The latest attempts to stem the country’s $3.2 trillion equity rout, including stock purchases by state-run financial firms and a halt to initial public offerings, have undermined government pledges to move to a more market-based economy, according to Aberdeen Asset Management.

They also risk eroding confidence in policy makers’ ability to manage the financial system if the rout in stocks continues, said BMI Research, a unit of Fitch. “It’s coming to a point where you’re covering one bad policy with another,” said Tai Hui at JPMorgan Asset Management. “A lot of investors are still concerned about another correction.” Strategists at BlackRock. Credit Suisse, Bank of America and Morgan Stanley last month warned the nation’s equities were in a bubble. When the Shanghai Composite reached its high on June 12, shares were almost twice as expensive as they were when the gauge peaked in October 2007 and more than three times pricier than any of the world’s top 10 markets, on a median estimated earnings basis.

A 29% plunge by the gauge through Friday, the steepest three-week rout since 1992, prompted a flurry of measures to stabilize the market. A group of 21 brokerages pledged Saturday to invest at least 120 billion yuan ($19.3 billion) in a stock-market fund, executives from 25 mutual funds vowed to buy shares and hold them for at least a year, while Central Huijin Investment Ltd., a unit of China’s sovereign wealth fund, said it was buying exchange-traded funds.

“..collective punishment of one country to have it serve as a warning to others is beyond the pale.”

• Financial Nonsense Overload (Dmitry Orlov)

“Those whom the gods wish to destroy they first make mad” goes a quote wrongly attributed to Euripides. It seems to describe the current state of affairs with regard to the unfolding Greek imbroglio. It is a Greek tragedy all right: we have the various Eurocrats—elected, unelected, and soon-to-be-unelected—stumbling about the stage spewing forth fanciful nonsense, and we have the choir of the Greek electorate loudly announcing to the world what fanciful nonsense this is by means of a referendum. As most of you probably know, Greece is saddled with more debt than it can possibly hope to ever repay. Documents recently released by the IMF conceded this point. A lot of this bad debt was incurred in order to pay back German and French banks for previous bad debt.

The debt was bad to begin with, because it was made based on very faulty projections of Greece’s potential for economic growth. The lenders behaved irresponsibly in offering the loans in the first place, and they deserve to lose their money. However, Greece’s creditors refuse to consider declaring all of this bad debt null and void—not because of anything having to do with Greece, which is small enough to be forgiven much of its bad debt without causing major damage, but because of Spain, Italy and others, which, if similarly forgiven, would blow up the finances of the entire European Union. Thus, it is rather obvious that Greece is being punished to keep other countries in line. Collective punishment of a country—in the form of extracting payments for onerous debt incurred under false pretenses—is bad enough; but collective punishment of one country to have it serve as a warning to others is beyond the pale.

Add to this a double-helping of double standards. The IMF won’t lend to Greece because it requires some assurance of repayment; but it will continue to lend to the Ukraine, which is in default and collapsing rapidly, without any such assurances because, you see, the decision is a political one. The ECB no longer accepts Greek bonds as collateral because, you see, it considers them to be junk; but it will continue to suck in all sorts of other financial garbage and use it to spew forth Euros without comment, keeping other European countries on financial life support simply because they aren’t Greece. The German government insists on Greek repayment, considering this stance to be highly moral, ignoring the fact that Germany is the defaultiest country in all of Europe. If Germany were not repeatedly forgiven its debt it would be much poorer, and in much worse shape, than Greece.

Jim’s dead on. De-centralization, de-complexity. That’s our future.

• Welcome to Blackswansville (Jim Kunstler)

While the folks clogging the US tattoo parlors may not have noticed, things are beginning to look a little World War one-ish out there. Except the current blossoming world conflict is being fought not with massed troops and tanks but with interest rates and repayment schedules. Germany now dawdles in reply to the gauntlet slammed down Sunday in the Greek referendum (hell) “no” vote. Germany’s immediate strategy, it appears, is to apply some good old fashioned Teutonic todesfurcht — let the Greeks simmer in their own juices for a few days while depositors suck the dwindling cash reserves from the banks and the grocery store shelves empty out. Then what? Nobody knows. And anything can happen. One thing we ought to know: both sides in the current skirmish are fighting reality.

The Germans foolishly insist that the Greek’s meet their debt obligations. The German’s are just pissing into the wind on that one, a hazardous business for a nation of beer drinkers. The Greeks insist on living the 20th century deluxe industrial age lifestyle, complete with 24/7 electricity, cheap groceries, cushy office jobs, early retirement, and plenty of walking-around money. They’ll be lucky if they land back in the 1800s, comfort-wise. The Greeks may not recognize this, but they are in the vanguard of a movement that is wrenching the techno-industrial nations back to much older, more local, and simpler living arrangements. The Euro, by contrast, represents the trend that is over: centralization and bigness. The big questions are whether the latter still has enough mojo left to drag out the transition process, and for how long, and how painfully.

World affairs suffer from the disease of terminal excessive complexity. To make matters worse, much of the late-phase complexity operates in the service of accounting fraud of one kind or another. The world’s banking system is mired in the unreality of so many unmeetable obligations, cooked books, three-card-monte swap gimmicks, interest rate euchres, secret arbitrages, market manipulation monkeyshines, and countless other cons, swindles, and hornswoggles that all the auditors ever born could not produce a coherent record of what has been wreaked in the life of this universe (or several parallel universes). Remember Long Term Capital Management? That’s what the world has become. What happens in the case of untenable complexity is that it tends to unravel fast and furiously..

Home › Forums › Debt Rattle July 7 2015