Andre Kertesz Bumper cars at amusement park in Neuilly-sur-Seine, near Paris 1930

I read a lot, been doing it for years, about finance and affiliated topics (a wide horizon of them), which means I’ve inevitably seen a wholesale lot of nonsense fly by. But for some reason, and I think I know why, Q3 2016 has been gunning for a top -or bottom- seat in that regard, and Q4 is looking to do it one better/worse.

Apart from the fast increasingly brainless political ‘discussions’ that don’t deserve the name, in the US and UK and beyond, there are the transnational organizations, NATO, IMF, EU and all those things, all suffocating in their own hubris, things I’ve dealt with before in for instance Globalization Is Dead, But The Idea Is Not and Why There is Trump. But none of it still seems to have trickled through anywhere that I can see.

The end of growth exposes the stupidity and ignorance of all but (and even that’s a maybe) a precious few (of our) ‘leaders’. There is no other way this could have run, because an era of growth simply selects for different people to float to the top of the pond than a period of contraction does. Can we agree on that?

‘Growth leaders’ only have to seduce voters into believing that they can keep growth going, and create more of it (though in reality they have no control over it at all). Anyone can do that. So ‘anyone’ who’s sufficiently hooked on power games will apply.

‘Contraction leaders’ have a much harder time; they must convince voters that they can minimize the ‘suffering of the herd’. Which is invariably a herd that no-one wants to belong to. A tough sell.

Any end to growth will and must therefore inevitably change the structure of a democracy, any democracy, any society for that matter. It will lead to new leaders, and new parties, coming to the front. And it should not surprise anyone that some of these new leaders and parties will question the very structure of the democracy they are part of, if only because that structure is already undergoing change anyway.

The tight connection between an era of economic growth (and/or contraction) and the politicians that ‘rule’ during that era is reflected in Hazel Henderson’s“economics is nothing but politics in disguise”.

On the one hand you have the incumbent class seeking to hold on to their waning power, churning out false positive numbers and claiming that theirs is the only way to go (just more of it), and on the other hand you have a loose affiliation – to the extent there’s any affiliation at all- of left and right, individuals and parties, who smell change that they can use to their own benefit.

They just mostly don’t know how to use it yet. But they’ll find out, or some of them will. Blaming people and groups of people for what’s gone wrong will be a major way forward, because it’s just so easy. It’s another reason why the incumbents class, the traditional parties, will go the way of the dodo: they will be blamed, and rightly so in most cases, for the fall of the economic system.

That’ll be the number one criteria: if you’re -perceived as- part of the old guard, you’re out. Not at the flick of a switch, but nevertheless the rise of Trump and Farage and all those folks has been much faster than just about anyone would have thought possible until very recently.

They feed on discontent, but they can do so only because that discontent has been completely ignored by the ruling classes everywhere. Which has a lot to do with the rulers in all these instances we see pop up now still being well-off, while the lower rungs of societies definitely are not.

Moreover, if most people still had comfortable middle-class lives, the dislike of immigrants and refugees would have been so much less that Trump and Wilders and Le Pen and Alternative for Deutschland could never have ‘struck gold’. It’s the perception that the ‘new’ people are somehow to blame for one’s deteriorating living conditions that makes it fertile ground for whoever wants to use it.

And since the far left can’t go there, the right takes over by default. Bernie Sanders and Jeremy Corbyn have brave ideas on redistribution of wealth, but there is still too much resistance, at the moment, to that, from the incumbent class and their voters, to have much chance of getting anywhere.

Of course the traditional right wing smells the opportunity too, so Hillary (yeah, she’s right wing) and Theresa May and Sarkozy and Merkel are all orchestrating sharp turns to the right, away from their once comfortable seats in the center. They all sense that power will not be emanating from the center going forward, and it’s power, much more than principles, that they are after.

But enough about politicians and their parties, who can and will all be voted out of power. Much harder to get rid of will be the transnational organizations, like the EU and IMF (there are many more), though they represent the ‘doomed construction’ perhaps even more than mere local or national power-hungries. The leading principle is simple: What has all the centralization led to? To today’s contracting economies.

To that end, let’s just tear into a recent random Bloomberg piece on this week’s IMF meeting, and the ‘expert opinions’ on it:

Existential Threat To World Order Confronts Elite At IMF Meeting

Policy-making elites converge on Washington this week for meetings that epitomize a faith in globalization that’s at odds with the growing backlash against the inequities it creates. From Britain’s vote to leave the EU to Donald Trump’s championing of “America First,” pressures are mounting to roll back the economic integration that has been a hallmark of gatherings of the IMF and World Bank for more than 70 years. Fed by stagnant wages and diminishing job security, the populist uprising threatens to depress a world economy that IMF Managing Director Christine Lagarde says is already “weak and fragile.”

The calls for less integration and more trade barriers also pose risks for elevated financial markets that remain susceptible to sudden swings in investor sentiment , as underscored by recent jitters over Deutsche Bank’s financial health. “The backlash against globalization is manifesting itself in increased nationalistic sentiment, against the outside world and in favor of increasing isolation,” said Louis Kuijs at Oxford Economics in Hong Kong, a former IMF official. “If we lose consensus on what kind of a world we want to have, the world will probably be worse off.”

Oh, but we do have consensus, Louis: Ever more people don’t want what they have now. That too is consensus. And since you said that what it takes is consensus, we should be fine then, right?!

Also, I find the term ‘elevated markets’ interesting, even if I don’t know what it’s supposed to mean. I can only guess.

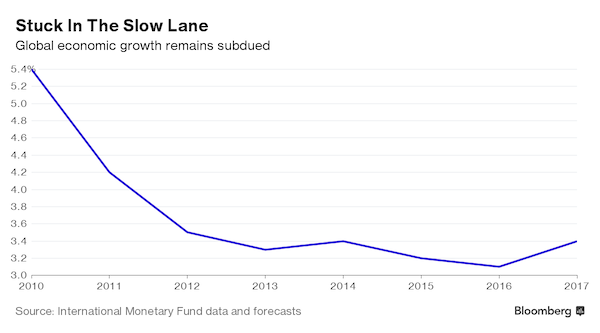

In its latest World Economic Outlook released Tuesday, the fund highlighted the threats from the anti-trade movement to an already subdued global expansion. After growth of 3.2% in 2015, the world economy’s expansion will slow to 3.1% this year before rebounding to 3.4% in 2017, according to the report, keeping those estimates unchanged from July projections. The forecasts for U.S. growth were cut to 1.6% this year and 2.2% in 2017.

“We’d like to see an end to the creeping protectionism in the world and more progress on moving ahead with free-trade agreements and other trade-creating measures,” Maurice Obstfeld, director of the IMF’s research department, said in a Bloomberg Television interview with Tom Keene. Lagarde said last week that policy makers attending the Oct. 7-9 annual meeting of the IMF and World Bank have two tasks. First, do no harm, which above all means resisting the temptation to throw up protectionist barriers to trade. And second, take action to boost lackluster global growth and make it more inclusive.

I can see how a vote against the likes of Hollande, Hillary or Cameron constitutes a “the backlash against globalization”. What I don’t see is how that has now become the same as the anti-trade movement. When did Trump express any feelings against trade? Against international trade deals as they exist and are further prepared, yes.

But those deals don’t define ‘trade’ to the exclusion of all other definitions. As for ‘protectionism’, that’s just a term designed to make something perfectly fine and normal look bad. Every single society on the planet should protect its basic necessities from being controlled by foreigners, either for money or for power.

Nothing good can come of relinquishing that control for any society, ever. There‘s not a thing wrong with protecting your control of your own water and food and shelter, and these are indeed things that should never be traded or negotiated in global markets.

So claiming that ‘do no harm’ equals NOT protecting your basics is nothing but a self-serving and dangerous kind of baloney coming your way courtesy of those people whose sociopathic plush seats and plusher bank accounts depend on your ongoing personal loss of control over what you need to survive.

It’s what any ‘body’ does that has reached the limits of its growth: it starts feeding on its host. Be it a cancerous tumor, the Roman Empire or our present perennial-growth driven economic models, they’re all the same same thing because they are fueled by the same -thoughtless- principle.

Ilargi: See that upward line at the end? Well, it’s an IMF growth ‘forecast’. Which are always so wrong, and always revised downward, that you must wonder if the term ‘forecast’ is even appropriate

Achieving even those modest objectives may prove elusive. Free trade has become polling poison in the U.S. presidential campaign, with Democratic nominee Hillary Clinton now criticizing a trade deal with Pacific nations, which isn’t yet ratified in the U.S., that she had praised when it was being negotiated. Republican challenger Trump has lashed out at Mexico and China, threatening to slap big tariffs on imports from both nations. Rattled by the U.K.’s June vote to leave the EU, European leaders know it may just be the start of a political earthquake that’s threatening the continent’s old certainties.

In case you didn’t catch it, “..the continent’s old certainties” is a goal-seeked term. Old in this case means not older than, say, 1950, if that. Look back 100 years and “the continent’s old certainties” dress in a whole other meaning.

Next year sees elections in Germany and France, the euro area’s two largest economies, and in the Netherlands. In all three countries anti-establishment forces are gaining ground. With growing resentment of the EU from Budapest to Madrid, policy makers have described the current surge in populism as the greatest threat to the bloc since its creation out of the ashes of World War II. There are also growing signs that the union and Britain are heading for a so-called “hard exit” that would sharply reduce the bloc’s trade and financial ties with the island nation. U.K. Prime Minister Theresa May said on Oct. 2 that she’ll begin her country’s withdrawal from the EU in the first quarter of next year.

I have addressed the misleading use of the term ‘populism’ before. In its core, it simple means something like: for, and by, the people. How that can be presented as somehow being a threat to democracy is a mystery to me. They should have picked another term, but settled on this one.

And in the western media consensus, it comprises anything from Trump to Beppe Grillo, via Hungary’s Orban and Nigel Farage, Spain’s Podemos, Greece’s Syriza and Germany’s AfD. All these completely different movements have one thing only in common: they protest the failed and fast deteriorating status quo, and receive a lot of support from their people for doing that.

Because it’s the people that bear the brunt of the failure, not the leadership; even Greece’s politicians still pay themselves a comparatively lush salary.

As for Britain, it’s the textbook example of utter blindness. Those who were/are well provided for, be they politically left or right, missed out on what was happening around them so much they had no idea Brexit was a real option. And in the 15 weeks since the Brexit vote, all anyone has done in the UK is seeking to blame someone, anyone but themselves for what they all failed to see coming.

Perhaps the biggest beneficiary of free trade over the past generation, China, still restricts access to many of its key industries, with economists worried about increasingly mercantilist policies. It’s also seeking a larger role in the existing global framework, with entry of the yuan into the IMF’s basket of reserve currencies on Oct. 1 the most recent example. An all-out trade war would be a disaster for China’s economy, with Trump’s threatened tariff potentially wiping off almost 5% of its GDP, according to a calculation by Daiwa Capital Markets.

John Williamson, whose Washington Consensus of open trade and deregulation was effectively the governing ethos for the IMF and World Bank for decades, said the 2008-09 financial meltdown had undercut support for economic integration. “There was agreement on globalization before the crisis and that’s one thing that’s been lost since the financial crisis,” said Williamson, a former senior fellow at Peterson Institute for International Economics who is now retired.

The growing opposition to economic integration has been fueled by a sub-par global recovery. “Perhaps the most striking macroeconomic fact about advanced economies today is how anemic demand remains in the face of zero interest rates,” former IMF chief economist Olivier Blanchard wrote last week in a policy brief for the Peterson Institute.

These ‘experts’ seem to have an idea there’s something amiss, but they don’t have the answers. Which is impossible to come and say out loud if you’re an expert. Experts must pretend to know it all, or at least know why they don’t know. “There was agreement on globalization before the crisis”, and now it’s no longer there. That they see.

That they ain’t coming back, neither the agreement on it nor globalization itself, is a step too far for them. To publicly acknowledge, at least. That Blanchard expresses surprise about ‘anemic demand’ at the same time that interest rates are equally anemic is something else.

That both are two sides of the same coin, or at least may be, is something he should at least mention. That is to say, low rates induce deflation, though they are allegedly supposed to induce the opposite. Economists are mostly very misguided people.

The world economy is getting some lift after rising at an annual rate just shy of 3% in the first half of this year, according to David Hensley, director of global economics for JPMorgan. But much of the boost will come from a lessening of drags rather than from a big burst of fresh growth, said Peter Hooper at Deutsche Bank Securities, a former Federal Reserve official. Recessions in Brazil and Russia are set to come to an end, while in the U.S. cutbacks in inventories and in oil and gas drilling will wane.

Please allow me to chip in here. ‘Lessening of drags’ in a nonsense term. And so is the idea that “..recessions in Brazil and Russia are set to come to an end”. That’s all goal-seeked day-dreaming. Smoke or drink something nice with it and you’ll feel good for a few hours, but that doesn’t make it real.

“I’m characterizing the global economy as something akin to a driverless car that’s stuck in the slow lane,” said David Stockton, a former Fed official and now chief economist at consultants LH Meyer. “Everybody feels like they’re being taken for a ride but they’re pretty nervous because they can’t see anybody in control.”

I really like this one, because off the bat I thought Stockton had it all wrong. What I think is the appropriate metaphor, is not “a driverless car that’s stuck in the slow lane”, but one of those cars in a carousel at a carnival, a merry-go-round, where you can sit in it forever and you always end up in the same spot. And the only one who’s in control in the boss who hollers that you need to pay another quarter if you want to keep on riding.

Or, alternatively, and to stay at the carnival, it’s a bumper car, which allows you to hit other cars and get hit, but never to leave the rink. That’s the global economy. Not getting anywhere, and running out of quarters fast.

Still, for the first time in the past few years, Stockton said he sees a real upside risk to his forecast of continued global growth of around 3% next year. And that’s coming from the possibility of looser fiscal policy in the U.S. and Europe. In the U.S., both Clinton and Trump have pledged to boost infrastructure spending on roads, bridges and the like. In Europe, rising populism provides a powerful incentive for governments to abandon austerity ahead of the elections next year – and perhaps beyond. Whether such a shift will be enough to mollify those who have been on the losing side of globalization for decades is debatable, however.

“The consensus in policy-making circles was that more trade meant better economic growth,” said Standard Chartered head of Greater China economic research Ding Shuang, who worked at the IMF from 1997 to 2010. “But the benefits weren’t shared equitably, so now we see a round of anti-globalization, anti-free trade. “Globalization will stall for the moment, until we can find a way to share those benefits,” he added.

Globalization is done. And while we can discuss whether that’s of necessity or not, and I continue to contend that the end of growth equals the end of all centralization including globalization, fact is that globalization was never designed to share anything at all, other than perhaps wealth among elites, and low wages among everyone else.

The EU and IMF have not delivered on what they promised, in the same way that traditional parties have not, from the US to UK to basically all of Europe. They promised growth, and growth is gone. They may have delivered for their pay masters, but they lost the rest of the world.

Anything else is just hot air. But that doesn’t mean they will hesitate to use their control of the military and police to hold on to what they got. In fact, that’s guaranteed. But it would only be viable in a dictatorial society, and even then.

We are transcending into an entirely different stage of our lives, our economies, our societies. Growth is gone, it went out the window long ago only to be replaced with debt. And that’s going to take a lot of getting used to. But there’s nothing that says we couldn’t see it coming.

Home › Forums › The IMF and All The Other Losers