Vincent van Gogh Seine with Pont de Clichy 1887

Take their power away or else.

• Monetary Stimulus: How Much Is Too Much? (Lebowitz)

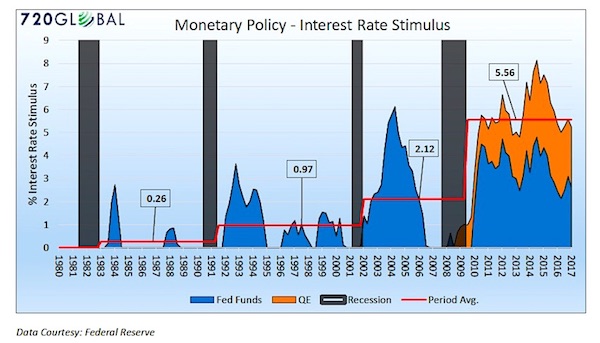

The amount of monetary stimulus increasingly imposed on the financial system creates false signals about the economy’s true growth rate, causing a vast misallocation of capital, impaired productivity and weakened economic activity. To help quantify the amount of stimulus, please consider the graph. Federal Reserve (Fed) monetary stimulus comes in two forms. First in the form of targeting the Fed Funds interest rate at a rate below the nominal rate of economic growth (blue). Second, it stems from the large scale asset purchases QE) by the Fed (orange). When these two metrics are quantified, it yields an estimate of the average amount of monetary stimulus (red) applied during each post-recession period since 1980. It has been almost ten years since the 2008 financial crisis and the Fed is applying the equivalent of 5.25% of interest rate stimulus to the economy, dwarfing that of prior periods.

The graph highlights that the Fed has been increasingly aggressive in both the amount of stimulus employed as well as the amount of time that such monetary stimulus remains outstanding. Amazingly few investors seem to comprehend that despite the massive level of monetary stimulus, economic growth is trending well below recoveries of years past. Additionally, as witnessed by historically high valuations, the rise in the prices of many financial assets is not based on improving economic fundamentals but simply the stimulative effect that QE and low interest rates have on investor confidence and financial leverage. Now consider the ramifications of a Fed that continues to increase the Fed Funds rate and moves forward with plans to slowly remove QE.

America: the House that Debt Built.

• Yes, You Should Be Concerned With Consumer Debt (Roberts)

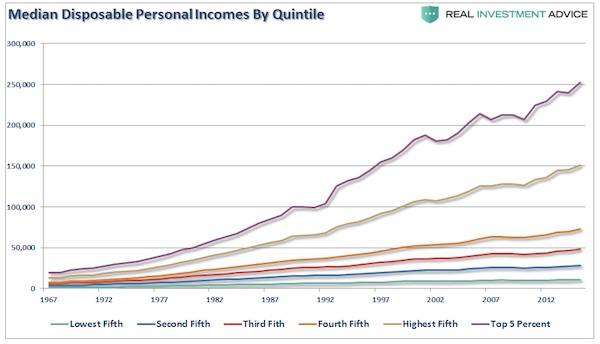

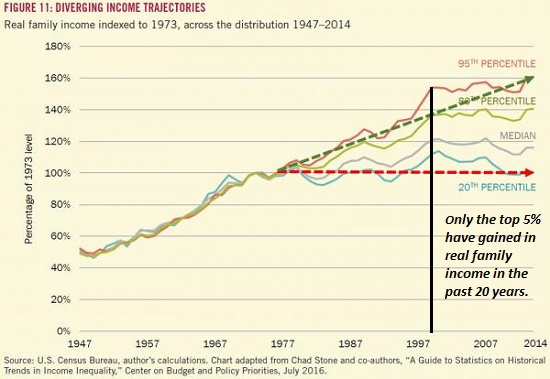

First, the calculation of disposable personal income, income less taxes, is largely a guess and very inaccurate due to the variability of income taxes paid by households. Secondly, but most importantly, the measure is heavily skewed by the top 20% of income earners, needless to say, the top 5%. As shown in the chart below, those in the top 20% have seen substantially larger median wage growth versus the bottom 80%.

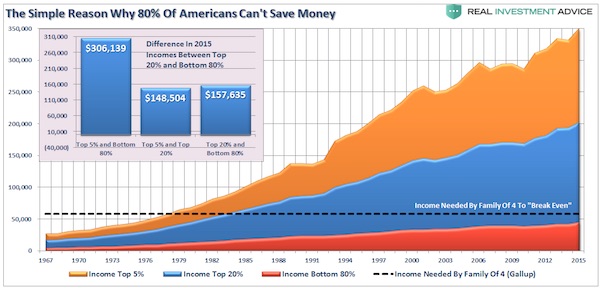

Lastly, disposable incomes and discretionary incomes are two very different animals. Discretionary income is what is left of disposable incomes after you pay for all of the mandatory spending like rent, food, utilities, health care premiums, insurance, etc. According to a Gallup survey, it requires about $53,000 a year to maintain a family of four in the United States. For 80% of Americans, this is a problem even on a GROSS income basis.

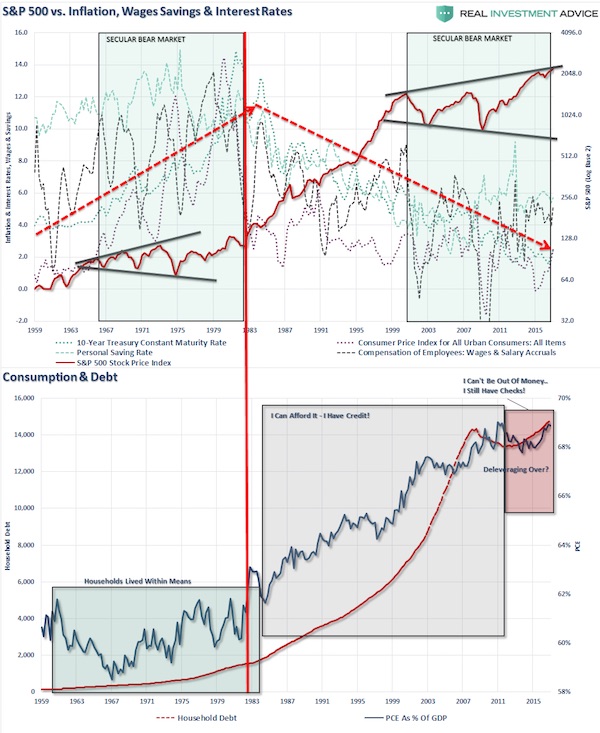

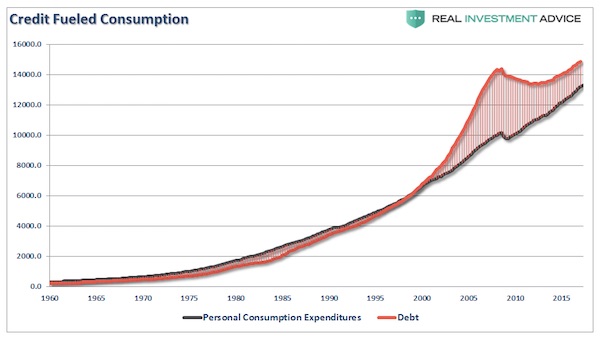

This is why record levels of consumer debt is a problem. There is simply a limit to how much “debt” each household can carry even at historically low interest rates. It is also the primary reason why we can not have a replay of the 1980-90’s. “Beginning 1983, the secular bull market of the 80-90’s began. Driven by falling rates of inflation, interest rates, and the deregulation of the banking industry, the debt-induced ramp up of the 90’s gained traction as consumers levered their way into a higher standard of living.”

“While the Internet boom did cause an increase in productivity, it also had a very deleterious effect on the economy. As shown in the chart above, the rise in personal debt was used to offset the declines in personal income and savings rates. This plunge into indebtedness supported the ‘consumption function’ of the economy. The ‘borrowing and spending like mad’ provided a false sense of economic prosperity. During the boom market of the 1980’s and 90’s consumption, as a%age of the economy, grew from roughly 61% to 68% currently. The increase in consumption was largely built upon a falling interest rate environment, lower borrowing costs, and relaxation of lending standards. (Think mortgage, auto, student and sub-prime loans.) In 1980, household credit market debt stood at $1.3 Trillion. To move consumption, as a% of the economy, from 61% to 67% by the year 2000 it required an increase of $5.6 Trillion in debt. Since 2000, consumption as a% of the economy has risen by just 2% over the last 17 years, however, that increase required more than a $6 Trillion in debt.

Doomed growth projections.

• Why We’re Doomed: Stagnant Wages (CHS)

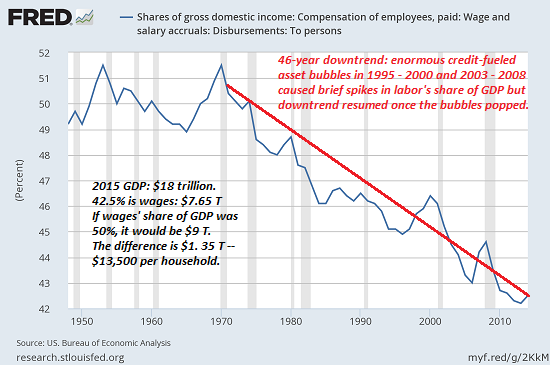

Despite all the happy talk about “recovery” and higher growth, wages have gone nowhere since 2000–and for the bottom 20% of workers, they’ve gone nowhere since the 1970s. GDP has risen smartly since 2000, but the share of GDP going to wages and salaries has plummeted: this is simply an extension of a 47-year downtrend. [..] .. our system requires ever-higher household incomes to function–not just in the top 5%, but in the top 80%. Our federal social programs–Social Security, Medicare and Medicaid–are pay-as-you-go: all the expenditures this year are paid by taxes collected this year. As I have detailed many times, the so-called “Trust Funds” are fictions; when Social Security runs a deficit, the difference between receipts and expenses are filled by selling Treasury bonds in the open market–the exact same mechanism ther government uses to fund any other deficit.

The demographics of the nation have changed in the past two generations. The Baby Boom is retiring en masse, expanding the number of beneficiaries of these programs, while the number of full-time workers to retirees is down from 10-to-1 in the good old days to 2-to-1: there are 60 million beneficiaries of Social Security and Medicare and about 120 million full-time workers in the U.S. Meanwhile, medical expenses per person are soaring. Profiteering by healthcare cartels, new and ever-more costly treatments, the rise of chronic lifestyle illnesses–there are many drivers of this trend. There is absolutely no evidence to support the fantasy that this trend will magically reverse.

Costs are skyrocketing and the number of retirees is ballooning, but wages are going nowhere. Do you see the problem? All pay-as-you-go programs are based on the assumption that the number of workers and the wages they earn will both rise at a rate that is above the underlying rate of inflation and equal to the rate of increase in pay-as-you-go programs. If 95% of the households are earning less money when adjusted for inflation, and their wealth has also declined or stagnated, then how can we pay for programs which expand by 6% or more every year? The short answer is you can’t.

Are we going to add this to the cost of Harvey?

• US Fuel Shortages From Harvey To Hamper Labor Day Travel (R.)

Travelers and fuel suppliers across the United States braced for higher prices and shortages ahead of the Labor Day holiday weekend as the country’s biggest fuel pipelines and refineries curb operations after Hurricane Harvey. Just six days after Harvey slammed into the heart of the U.S. energy industry in Texas, the effects are being felt not just in Houston, but also in Chicago and New York, and prices at the pump nationwide have hit a high for the year. Supply shortages have developed even though there are nearly a quarter of a billion barrels of gasoline stockpiled in the United States. But much of it is held in places where it cannot be accessed due to massive floods, or too far away from the places it is needed. Some of it is unfinished, meaning it needs to be blended before it can go to gas stations.

Harvey has highlighted another weakness in the system: pipeline terminals typically only have a five-day supply in storage to load into the lines. Some of the biggest pipelines in the United States, supplying the northeast market and the Chicago area, have already shut down or reduced operations because they have no fuel to pump. “Gasoline is very much a ‘just-in-time’ fuel, for as many million barrels as they think we have,” said Patrick DeHaan, petroleum analyst at GasBuddy. “Sure, they are somewhere, but they still have to be mixed and blended together.” At least two East Coast refiners, including Philadelphia Energy Solutions and Irving Oil, have already run out of gasoline for immediate delivery as they have rushed to send supplies to the U.S. Southeast, Caribbean, Mexico and South America to offset the lack of exports since Harvey.

Lock them up!

• Wells Fargo Says 3.5 Million Accounts Involved In Scandal (AP)

The scope of Wells Fargo’s fake accounts scandal grew significantly on Thursday, with the bank now saying that 3.5 million accounts were potentially opened without customers’ permission between 2009 and 2016. That’s up from 2.1 million accounts that the bank had cited in September 2016, when it acknowledged that employees under pressure to meet aggressive sales targets had opened accounts that customers might not have even been aware existed. People may have had different kinds of accounts in their names, so the number of customers affected may differ from the account total. Wells Fargo said Thursday that about half a million of the newly discovered accounts were missed during the original review, which covered the years 2011 to 2015.

After Wells Fargo acknowledged the fake accounts last year, evidence quickly appeared that the sales practices problems dated back even further. So Wells Fargo hired an outside consulting firm to analyze 165 million retail bank accounts opened between 2009 and 2016. Wells said the firm found that, along with the 2.1 million accounts originally disclosed, 981,000 more accounts were found in the expanded timeline. And roughly 450,000 accounts were found in the original window. The scandal was the biggest in Wells Fargo’s history. It cost then-CEO John Stumpf his job, and the bank’s once-sterling industry reputation was in tatters. The company ended up paying $185 million to regulators and settled a class-action suit for $142 million. New managers have been trying to amends with customers, politicians and the public.

But it’s been tough, as new revelations keep coming. Wells Fargo said last month that roughly 570,000 customers were signed up for and billed for car insurance that they didn’t need or necessarily know about. Many couldn’t afford the extra costs and fell behind in their payments, and in about 20,000 cases, cars were repossessed. Other customers have filed lawsuits against Wells Fargo saying they were victims of unfair overdraft practices. Wells Fargo is also still under several investigations for its sales practices problems, including a congressional inquiry and one by the Justice Department. Wells Fargo said Thursday that of the 3.5 million accounts potentially opened without permission, 190,000 of those incurred fees and charges. That’s up from 130,000 that the bank originally said. Wells Fargo will refund $2.8 million to customers, in addition to the $3.3 million it already agreed to pay.

Wise.

• World’s Biggest Wealth Fund Reveals Bleak View on Global Trade (BBG)

Yngve Slyngstad, chief executive officer of Norges Bank Investment Management, as the fund is known, says the heyday of cross-border trade is probably behind us. “The question investors are asking themselves is if the easy wins already have been made,” Slyngstad said in an Aug. 29 interview from his office on the top floor of Norway’s central bank in Oslo. “The global supply chains have in a way had a one-time gain primarily through outsourcing of multinationals to China.” Norway’s wealth fund owns 1.3% of globally listed stocks, spread out over almost 80 countries. And with interest rates at record lows, the investor has cut its long-term return expectations to about 3% from 4%, even after winning approval from parliament to raise its share of equities to 70% from 60%.

Slyngstad, who became CEO in 2008 just as the global economy was sinking into the worst crisis since the Great Depression, noted that back then the fund rode out the turmoil by dumping bonds and buying stocks. “I don’t expect that we will act differently in any similar crisis in the future,” he said. During a recent conference on globalization, the fund’s chief strategist, Bjorn Erik Orskaug, suggested the world might be at an “inflection point” in trade, with shallower value chains and less cross-border production. And then there’s the protectionist agenda some governments are pursuing. “Is there also a political situation that could make it more challenging?” Slyngstad said. “Time will tell, but there’s of course a risk on the horizon.” He says the wealth fund’s extremely long-term investment timeline allows it to look past the noise coming from governments that come and go.

The fund will probably stay over-weighted in Europe, where it’s more of an active investor. But the only two economies that really matter are the U.S. and China, Slyngstad said. [..] As the fund approaches $1 trillion in value, its stated goal is to safeguard today’s oil wealth for future generations of Norwegians. It has surged in size since its inception two decades ago, generating an annual nominal return of 5.89%. Norway’s government last year started taking cash out of the fund for the first time, to make up for lower oil revenue. Withdrawals are set to hit about 72 billion kroner ($9.3 billion) in 2017, and remain at that level in coming years amid stricter fiscal rules.

Once the creative accounting is removed, there won’t be much left.

• New Math Deals Minnesota’s Pensions the Biggest Hit in the US (BBG)

Minnesota’s debt to its workers’ retirement system has soared by $33.4 billion, or $6,000 for every resident, courtesy of accounting rules. The jump caused the finances of Minnesota’s pensions to erode more than any other state’s last year as accounting standards seek to prevent governments from using overly optimistic assumptions to minimize what they owe public employees decades from now. Because of changes in actuarial math, Minnesota in 2016 reported having just 53% of what it needed to cover promised benefits, down from 80% a year earlier, transforming it from one of the best funded state systems to the seventh worst, according to data compiled by Bloomberg. “It’s a crisis,” said Susan Lenczewski, executive director of the state’s Legislative Commission on Pensions and Retirement.

The latest reckoning won’t force Minnesota to pump more taxpayer money into its pensions, nor does it put retirees’ pension checks in any jeopardy. But it underscores the long-term financial pressure facing governments such as Minnesota, New Jersey and Illinois that have been left with massive shortfalls after years of failing to make adequate contributions to their retirement systems. The Governmental Accounting Standards Board’s rules, ushered in after the last recession, were intended to address concern that state and city pensions were understating the scale of their obligations by counting on steady investment gains even after they run out of cash – and no longer have money to invest. Pensions use the expected rate of return on their investments to calculate in today’s dollars, or discount, the value of pension checks that won’t be paid out for decades.

Everybody wants their share of the pie.

• Six Big Banks To Create A Blockchain-Based Cash System (R.)

Six new banks have joined a UBS-led effort to create a digital cash system that would allow financial markets to make payments and settle transactions quickly via blockchain technology. The group aims to launch the system late next year. Barclays, Credit Suisse, Canadian Imperial Bank of Commerce, HSBC, MUFG and State Street have joined the group developing the “utility settlement coin” (USC), a digital cash equivalent of each of the major currencies backed by central banks, UBS said on Thursday. The group is in discussions with central banks and regulators and is aiming for a “limited ’go live’” in the latter part of 2018, UBS’s head of strategic investment and fintech innovation told the Financial Times.

The Swiss bank first launched the concept in September 2015 with London-based blockchain company Clearmatics, and was later joined on the project by BNY Mellon, Deutsche Bank, Santander and brokerage ICAP. The USC would be convertible at parity with a bank deposit in the corresponding currency, making it fully backed by cash assets at a central bank. Spending a USC would be the same as spending the real currency it is paired with. Blockchain works as a tamper-proof shared ledger that can automatically process and settle transactions using computer algorithms, with no need for third-party verification. Because it does not require manual processing, nor authentication through intermediaries, the technology can make payments faster, more reliable and easier to audit.

Better talk with him.

• Putin Warns Of ‘Major Conflict’ Over North Korea, Urges Talks (AFP)

Russian President Vladimir Putin warned Friday of a “major conflict” looming on the Korean Peninsula, calling for talks to alleviate the crisis after Pyongyang fired a missile over Japan this week. “The problems in the region will only be solved via direct dialogue between all concerned parties, without preconditions,” Putin said. “Threats, pressure and insulting and militant rhetoric are a dead end,” a statement from his office said, adding that heaping additional pressure on North Korea in a bid to curb its nuclear programme was “wrong and futile.” Tensions on the Korean Peninsula are at their highest point in years after a series of missile tests by Pyongyang.

Early on Tuesday, the reclusive state fired an intermediate-range Hwasong-12 over Japan, prompting US President Donald Trump to insist that “all options” were on the table in an implied threat of pre-emptive military action. The UN Security Council denounced North Korea’s latest missile test, unanimously demanding that Pyongyang halt the programme. US heavy bombers and stealth jet fighters took part in a joint live fire drill in South Korea on Thursday, intended as a show of force against the North, Seoul said. Putin said he feared the peninsula was “on the verge of a major conflict” and called for all sides to sign up to a mediation programme drawn up by Moscow and Beijing. He echoed comments by Foreign Minister Sergei Lavrov who in a Wednesday telephone call with US counterpart Rex Tillerson “underscored… the need to refrain from any military steps that could have unpredictable consequences.”

Prime candidate for worst report ever. The Independent tweeetd: “12 Nobel Prize winners just warned Trump is one of the gravest threats to humanity “. But that’s not what the article by the Press Association says. It says two.

• Trump, Nuclear War And Climate Change Among Gravest Threats To Humanity (PA)

Nobel Prize winners consider nuclear war and US President Donald Trump as among the gravest threats to humanity, a survey has found. More than a third (34%) said environmental issues including over-population and climate change posed the greatest risk to mankind, according to the poll by Times Higher Education and Lindau Nobel Laureate Meetings. But amid rising tensions between the US and North Korea, almost a quarter (23%) said nuclear war was the most serious threat. Of the 50 living Nobel Prize winners canvassed, 6% said the ignorance of political leaders was their greatest concern – with two naming Mr Trump as a particular problem. Peter Agre, who won the Nobel Prize for chemistry in 2003, described the US President as “extraordinarily uninformed and bad-natured”. He told Times Higher Education: “Trump could play a villain in a Batman movie – everything he does is wicked or selfish.”

Laureates for chemistry, physics, physiology, medicine and economics took part in the survey, with some highlighting more than one threat. Peace Prize and Literature Prize recipients were not canvassed. Infectious diseases and drug resistance were considered the gravest threats to humankind by 8% of respondents, while 8% cited selfishness and dishonesty and 6% cited terrorism and fundamentalism. Another 6% spoke of the dangers of “ignorance and the distortion of truth”. Despite high-profile figures Elon Musk and Professor Stephen Hawking expressing concern about the dangers associated with artificial intelligence, just two of those surveyed identified it as among the biggest threats facing humans.

John Gill, editor of Times Higher Education, said the survey offers “a unique insight into the issues that keep the world’s greatest scientific minds awake at night”. He said: “There is a consensus that heading off these dangers requires political will and action, the prioritisation of education on a global scale, and above all avoiding the risk of inaction through complacency.”

Stockholm Syndrome?

• Greece Doesn’t Want Any More Rescues – But It Does Need Something Else (CNBC)

Greece wants nothing more than to avoid another bailout — which means it needs debt relief. And so far, that’s the sticking point. “There is now light at the end of the tunnel,” Greek Finance Minister Euclid Tsakalotos said hopefully in June. After months of wrangling, the European Union and International Monetary Fund had just agreed to release more rescue funds to the perennially troubled nation, bringing the total from its third bailout alone to €40.2 billion ($47.75 billion). Euro zone finance ministers took very light steps toward debt relief at that time — they said they were willing to keep deferring interest on financial assistance Greece had already received — but those measures fell short of the relief Greek Prime Minister Alexis Tsipras was pressing for.

The current bailout program is set to end in September of next year. Greece has been wracked by perennial financial crises since 2010, and it even appeared at risk of leaving the euro zone altogether in 2015. Tsipras’s objective is to re-gain full market access to international bond markets and to leave institutional help behind, so the subject of long-term debt is one that will continue to dominate discussions as it draws closer to September 2018. In July, Greece dipped into bond markets after a 3-year hiatus, issuing 5-year debt at an average yield of 4.66%. Greece is expected to return to the market again in the next 12 months. But Greece’s debt isn’t manageable in the long-run without being either extended or forgiven, according to the IMF, which is pressing for easier budgetary targets for Greece while simultaneously undertaking reforms.

Its European creditors currently require it to achieve a primary surplus before debt service of 3.5% of gross domestic product. The ECB has also been emphatic that it will not include Greek government bonds in its own debt-buying mechanism, the Public Sector Purchase Program. In a June letter, ECB President Mario Draghi ruled out that possibility, saying the central bank’s staff wasn’t in a position to fully analyze Greece’s public debt. Analysts at Barclays have estimated that the inclusion of Greek debt into ECB’s bond-buying program would entail monthly purchases of around 115 million euros ($136.5 million).

Not looking good.

• Hurricane Irma Turning Into Monster (ZH)

Hurricane Irma continues to strengthen much faster than pretty much any computer model predicted as of yesterday or even this morning. Per the National Hurricane Center’s (NHC) latest update, Irma is currently a Cat-3 storm with sustained winds of 115 mph but is expected to strengthen to a devastating Cat-5 with winds that could top out at 180 mph or more. Longer term computer models still vary widely but suggest that Irma will make landfall in the U.S. either in the Gulf of Mexico or Florida. Meteorological Scientist Michael Ventrice of the Weather Channel is forecasting windspeeds of up to 180 mph, which he described as the “highest windspeed forecasts I’ve ever seen in my 10 yrs of Atlantic hurricane forecasting.”

In a separate tweet, Ventrice had the following troubling comment: “Wow, a number of ECMWF EPS members show a maximum-sustained windspeed of 180+mph for #Irma, rivaling Hurricane #Allen (1980) for record wind”. The Weather Channel meteorologist also calculated the odds for a landfall along the eastern seaboard at 30%. Meanwhile, the Weather Channel has the “most likely” path of Irma passing directly over Antigua, Puerto Rico and Domincan Republic toward the middle of next week.

Home › Forums › Debt Rattle September 1 2017