Rembrandt van Rijn The flight into Egypt – a night piece 1651

It’s your borrowing that will do you in.

• The Household Debt Ticking Time Bomb (IRD)

I fully expect the Government’s Census Bureau to post a mind-blowing headline retail sales number for December. Hyperbolic headline economic statistics derived from mysterious “seasonal adjustments” based on questionable sampling methodology is part of the official propaganda policy mandated by the Executive Branch of Government. But I also believe that retail sales were likely more robust than saner minds were expecting because it appears that households have become accustomed to the easy credit provided by the banking system to make ends meet. Borrow money to “spend and pretend.” The Fed reported that consumer credit hit an all-time record in November. The primary driver was credit card debt, which hit a new all-time high (previous record was in 2008). Credit debt also increased a record monthly amount in November.

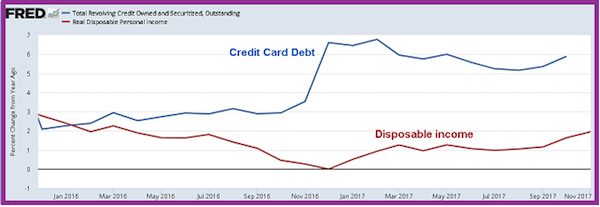

“Speaking of signposts, households have grown increasingly comfortable with leverage to maintain their living standards, which of course economists cheer. That’s worked for 24 straight months as credit card spending growth has outrun that of income growth” – Danielle DiMartino Booth, who was an advisor for nine years to former Dallas Fed President, Richard Fisher. The graph above shows the year over year monthly percentage change in revolving credit – which is primarily credit card debt – and real disposable personal income. Real disposable personal income is after-tax income adjusted for CPI inflation. As you can see, the growth in the use of credit card debt has indeed outstripped the growth in after-tax household income. The credit metric above would not include home equity lines of credit.

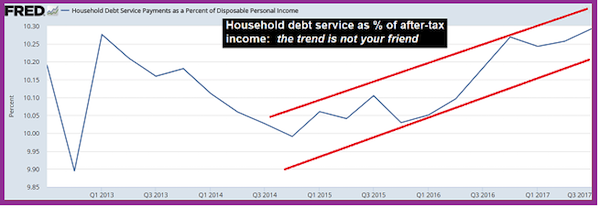

At some point, assuming the relationship between the two variables above continues along the same trend, and we have no reason to believe that it won’t, credit card debt will collide with reality and there will be a horrifying number of credit card defaults. Worse than 2008-2010. [The next] chart shows household debt service payments as a percentage of after-tax income: “Debt service” is interest + principal payments. With auto loan and credit card debt, most of the debt service payment is interest. This metric climbed to a 5-year high during a period of time when interest rates hit all-time record lows. Currently the average household is unable to make more than the minimum principle payment per the information conveyed by the first graphic. What happens to the debt service:income ratio metric as households continue to pile on debt to make ends meet while interest rates rise?

Household debt service includes mortgage debt service payments. Household mortgage debt outstanding is not quite at the all-time high recorded in Q2 2008. The current number from the Fed is through Q3 2017. At the current quarterly rate of increase, an new all-time high in mortgage debt outstanding should occur during Q2 2018. However, it should be noted that the number of homes sold per quarter during this current housing bubble is below the number of units sold per quarter at the peak of the previous housing bubble. This means that the average size of mortgage per home sold is higher now than during the earlier housing bubble. This is a fact that overlooked by every housing and credit market analyst, either intentionally or from ignorance (I’ll let you decide).

Until it does.

• The Stock Market Never Goes Down Anymore (BBG)

The New Year’s rally has pushed the S&P 500 Index to its best start since the administration of George W. Bush. Now it’s bumping against speed barriers that marked the upper limits of bull markets for decades. Up eight times in the first nine days of 2018, the S&P 500 has broken away from a trend line, its 200-day moving average, with a velocity unseen since 2013, the best year for equities in a generation. The benchmark now sits more than 11% above the level, putting it in the 92nd percentile of momentum, data going back 20 years show. Something has changed in equities. If 2017 was a slow but steady slog, 2018 has been off to the races, with shares rising at four times last year’s daily rate on the back of Donald Trump’s tax package and gathering signs of economic strength.

Forty seven companies in the S&P 500 are already up at least 10% this year, compared with just two down as much. “Even if you were the bullest of the bulls, this crazy rally start to the year took you off guard,” said Michael Antonelli at Robert W. Baird & Co. “We’ve completely run out of ways to describe what’s happening. We get asked a lot, are you seeing anything different that could explain the rally? The answer is no.” Fear of missing out is rampant not just on Wall Street but worldwide. Globally, stock funds saw a $24 billion inflow in the five days through Thursday, the sixth largest weekly total ever. Concern the U.S. stocks have jumped too much too fast prompted Morgan Stanley’s Andrew Sheets to cut the U.S. stocks’s exposure in favor of European equities this week.

Sheets isn’t the only one having a hard time keeping up. The average of 23 strategists predictions is for the S&P 500 to reach 2,914 at year-end. If stocks were to maintain the same upward trajectory they’ve exhibited in the last nine days, it would take roughly two more weeks to reach the strategists’ target. At 3.4 times its book value, the S&P 500 trades at the most expensive level since 2002, while its 14-day relative strength index reached a level unseen since 1996. The S&P 500 rose 1.6% to 2,786 this week, pushing the spread between the gauge and its 200-day moving average to 11.5%, the widest in five years.

Because it can.

• Fed Pays Banks $30 Billion on “Excess Reserves” for 2017 (WS)

The Federal Reserve’s income from operations in 2017 dropped by $11.7 billion to $80.7 billion, the Fed announced today. Its $4.45-trillion of assets – including $2.45 trillion of US Treasury securities and $1.76 trillion of mortgage-backed securities that it acquired during years of QE – produce a lot of interest income. How much interest income? $113.6 billion. It also made $1.9 billion in foreign currency gains, resulting “from the daily revaluation of foreign currency denominated investments at current exchange rates.” For a total income of about $115.5 billion. Those are just “estimates,” the Fed said. Final “audited” results of the Federal Reserve Banks are due in March. This “audit” is of course the annual financial audit executed by KPMG that the Fed hires to do this.

It’s not the kind of audit that some members in Congress have been clamoring for – an audit that would try to find out what actually is going on at the Fed. No, this is just a financial audit. As the Fed points out in its 2016 audited “Combined Financial Statements,” the audit attempts to make sure that the accounting is in conformity with the accounting principles in the Financial Accounting Manual for Federal Reserve Banks. Given that the Fed prints its own money to invest or manipulate markets with – which makes for some crazy accounting issues – the Generally Accepted Accounting Principles (GAAP) that apply to US businesses to do not apply to the Fed. This annual audit by KPMG reveals nothing except that the Fed’s accounting is in conformity with the Fed’s own accounting manual.

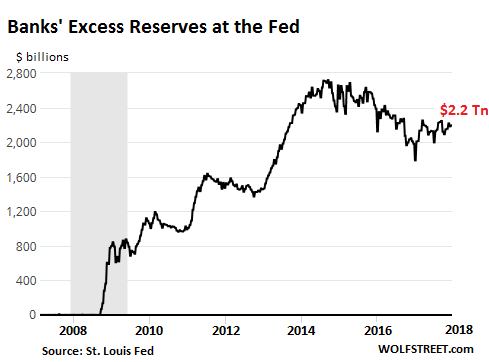

The Fed pays the banks interest on their “Required Reserves” and on their “Excess Reserves” at the Fed. Excess Reserves are the biggie: As a result of QE, they jumped from $1.7 billion in July 2008, to $2.7 trillion at the peak in September 2014. They’ve since dwindled, if that’s the right word, to $2.2 trillion:

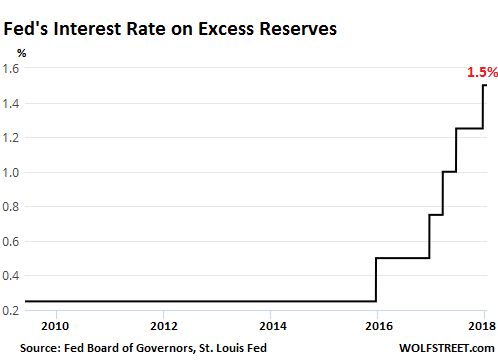

When the Federal Open Markets Committee (FOMC) meets to hash out its monetary policy, it also considers what to do with the interest rates that it pays the banks on “Required Reserves” and on “Excess Reserves.” In this cycle so far, every time the Fed has raised its target range for the federal funds rate (now between 1.25% and 1.50%) it also raised the interest rates it pays the banks on “required reserves” and on “excess reserves,” which went from 0.25% since the Financial Crisis to 1.5% now:

They’ve been working to achieve it for a decade, and now they manage to fool themselves into thinking they got it, it’s not what they want.

• Fed’s Rosengren Faults Inflation Target, Warns Of Harm (R.)

“I‘m disagreeing with that framework,” Rosengren said at the Global Interdependence Center in San Diego, referring to the Fed’s “balanced” approach to achieving a 2% inflation target and full employment. The Fed adopted this framework six years ago and has reaffirmed it each year since. Now, as Fed Governor Jerome Powell prepares to take the reins as Fed chief from Janet Yellen when her term ends early next month, a growing number of Fed policymakers want to rethink that framework. Rosengren’s comments Friday put the sharpest point to date on the debate, suggesting that a strict 2-percent inflation target could force the Fed to slam the brakes on the economy with aggressive rate hikes if the unemployment rate, now at 4.1%, continues to sink. It is already below the level that many economists think can be sustained without putting upward pressure on inflation.

While inflation running stubbornly below 2% has so far allowed the Fed to lift rates only gradually, that may change, Rosengren warned. “My concern is if we get too far away from where we want to be on a sustainable unemployment rate, and we use this current framework, then we will get to a situation where we have to raise rates fast enough that we will actually find it very difficult to get back to full employment without causing a recession,” Rosengren said. Rosengren suggested replacing the 2% inflation target with a target range for inflation of between 1.5% and 3%, in line with actual experience over the last 20 years. Under current conditions of low productivity and labor force growth, he said, the Fed would target inflation at the upper end of that range, and would be more patient with rate hikes.

“Marketable borrowings..”

• Goldman Warns Treasury Issuance To More Than Double In 2019 (ZH)

During yesterday’s surprisingly candid remarks by Bill Dudley, the second most important person in the Federal Reserve – the organization that is responsible for the third consecutive and largest ever yet asset bubble in history – said that one risk he was increasingly worried about was, drumroll, elevated asset prices. Because, supposedly, the Fed has little to input in how asset prices came to be where they are… Just as ominous was Dudley’s admission that the second risk he was concerned about is “the long-term fiscal position of the United States” i.e. US debt. Specifically, Dudley said that the Trump tax cut “will increase the nation’s longer-term fiscal burden, which is already facing other pressures, such as higher debt service costs and entitlement spending as the baby-boom generation retires.”

Oddly there was no mention of which administration doubled US debt from $10 trillion to $20 trillion in under a decade, and which organization enabled this to happen by keeping rates at record low levels, while crushing savers, and bailing out habitual gamblers. In any case, now that the narrative has shifted, and Donald Trump will be scapegoated not only for the upcoming “tremendous” market crash – something he has made especially easy by taking credit for every single uptick in the S&P – but also for the inevitable fiscal collapse of the United States, it is time to provide the backing for this particular strawman, and to do that, this morning Dudley’s former employer, Goldman Sachs released a report in which the bank’s chief economist said the he is updating his Treasury issuance forecast to account for recent revised deficit projections.

As a result, US marketable borrowings will more than double from below $500 billion in 2018 to over $1 trillion in 2019 as the debt tsunami finally get going. To build up the strawman, Goldman explains that US borrowing needs will rise for three reasons: First, recently enacted tax reform legislation is estimated to raise the deficit by more than $200bn, on average, each of the next four years, and Congress looks likely approve substantial new spending as well. Second, Fed portfolio runoff will increase the amount of debt the Treasury must issue to the public. Third, the Treasury’s cash balance is likely to rise by around $200bn once a longer-term debt limit suspension is enacted, which will also necessitate additional borrowing.

Goldman expects that the “substantial increase” in borrowing needs will be announced by the Treasury when it lays out its plans at the February quarterly refunding. What Goldman has left unsaid is what happens to interest rates at a time when on one hand US debt supply is set to double and on the other the Fed is set to continue shrinking its balance sheets, the ECB and BOJ are set to accelerate (and begin) tapering their own QEs and when global inflation is expected to keep rising. What is also unsaid is just who will be the marginal buyer of this debt tsunami when central banks increasingly shift away from debt monetization.

2018 will show us just what bad shape Britain is in.

• The Company That Runs Britain Is Near To Collapse. Watch And Worry (G.)

You may never have heard of Carillion. There’s no reason you should have. Its lack of glamour is neatly summed up by the name it sported in the 90s: Tarmac. But since then it has grown and grown to become the UK’s second-largest building firm – and one of the biggest contractors to the British government. Name an infrastructure pie in the UK and the chances are Carillion has its fingers in it: the HS2 rail link, broadband rollout, the Royal Liverpool University Hospital, the Library of Birmingham. It maintains army barracks, builds PFI schools, lays down roads in Aberdeen. The lot. There’s just one snag. For over a year now, Carillion has been in meltdown. Its shares have dropped 90%, it’s issued profit warnings, and it’s on to its third chief executive within six months. And this week, the government moved into emergency mode.

A group of ministers held a crisis meeting on Thursday to discuss the firm. Around the table, reports the FT, were business secretary Greg Clark, as well as ministers from the Cabinet Office, health, transport, justice, education and local government. Even the Foreign Office sent a representative. Why did Chris Grayling give the HS2 contract to a company that was already in existential difficulties? That roll call says all you need to know about the public significance of what happens next at Carillion. This is a firm that employs just under 20,000 workers in Britain – and the same again abroad. It has a huge chain of suppliers – and its habit of going in for joint ventures with other construction businesses means that a collapse at Carillion would send shockwaves through the industry and through the government’s public works programme.

To see what this means, take the HS2 rail link, where Carillion this summer was part of a consortium that won a £1.4bn contract to knock tunnels through the Chilterns. If Carillion goes under, what happens to the largest infrastructure project in Europe? What happens to its partners on the deal, British firm Kier, and France’s Eiffage? The project will need to be put back and the taxpayer will almost certainly have to step in. Imagine that same catastrophe befalling dozens of other projects across the UK and you get a sense of what’s at stake. Jobs will be cut, schools will go unbuilt (just a couple of months ago, Oxfordshire county council pulled the plug on a 10-year schools project) – and the government’s entire private finance initiative (PFI) model for building this country’s essential services will be shaken to the core.

Good cop bad cop.

• Spanish and Dutch Agree to Seek Soft Brexit Deal (BBG)

Spanish and Dutch finance ministers have agreed to push for a Brexit deal that keeps Britain as close to the European Union as possible, according to a person familiar with the situation. Spanish Economy Minister Luis de Guindos and his Dutch counterpart Wopke Hoekstra met earlier this week and discussed their common interests in Brexit, according to the person, who declined to be identified. Both have close trade and investment ties and are concerned about the impact of tariffs. They are also worried about losing U.K. contributions to the EU budget, the person said. The pound jumped to the strongest level since the referendum in 2016, trading 1.2% higher at $1.3690.

A spokeswoman for the Spanish Economy Ministry stressed that both ministers support chief EU negotiator Michel Barnier’s efforts, and said they’re not working together toward a soft Brexit deal. Earlier, a Spanish economy ministry official said that the two finance chiefs had underlined the importance of U.K. ties for both countries, and agreed to keep track of their common interests. A spokesman for Hoekstra declined to comment. The 27 remaining EU nations maintained a united front in the first phase of divorce talks, though the solidarity is already showing signs of strain as national interests diverge in the face of future trade discussions. French President Emmanuel Macron has warned countries to be disciplined and stick together to protect all their interests, in a kind of prisoner’s dilemma. EU countries have delegated the job of negotiations to Barnier.

Steve reply to the one-dimensional Oxford Review of Economic Policy’s latest issue.

• Economics Is Too Important To Be Left To The -Academic- Economists (Steve Keen)

Modern Economics is as conformist, and bland, as country and western music. This leaves radical thinkers singing the Blues as their voices go unheard. I’ve had an epiphany about my place in the Universe, and I owe it to the Oxford Review of Economic Policy and its special issue on “Rebuilding Macroeconomic Theory.” I am Elwood Blues, and the Universe (the part I inhabit anyway) is Bob’s Country Bunker. Halfway through the classic movie The Blues Brothers, Jake Blues cons the band into performing at a bar called Bob’s Country Bunker. When his incredulous brother Elwood asks the bar owner’s wife “What kind of music do you usually have here?” she cheerily replies “Oh, we got both kinds. We got Country and Western”.

So that’s it. I’m a Blues singer, and I’m surrounded by Country and Western fans—otherwise known as Mainstream Economists. Their musical spectrum ranges from Hank Williams to Dolly Parton, and if I play anything outside it — say, some Otis Redding or Muddy Waters — they’ll throw beer bottles at me. Sometimes, even full ones. Suddenly, it all makes sense. This epiphany arrived, not as a Divine revelation, but as a tweet (as they would, were Moses alive today; so much more convenient than stone tablets) on January 1, as the Review touted its soon-to-be-released special issue.

“..how much of a “shithole” is our own country these days?”

• Who Moved My Xanax? (Jim Kunstler)

The moral panic of “the Resistance” is back in DefCon 1 mode overnight just as the righteousness orgasm of the Golden Globe Awards was wearing off. Mr. Trump’s casual question to a couple of Senators vis-à-vis immigration policy — “Why do we want all these people from ‘shithole countries’ coming here?” — pushed the “racism” button at Resistance Central and CNN staged yet another of the orchestrated anxiety attacks it has perfected over the past year. The spotlight in this three-ring circus of perpetual offense, indignation, and alarm shifts back from the alleged sufferings of movie actresses to another intersectional victim group from the Dem/Prog pantheon of oppressed minorities: would-be immigrants-of-color. The President’s vulgar animus proves the charge that at least half the country is a lynch mob.

Of course, the most interesting feature of this neurotic zeitgeist is the displacement dynamic among the political Left as its frantic virtue-signaling attempts to distract everybody else in the room from its own dark and shameful emotions about the composition of American culture. As a born-and-bred Boomer (ex-)liberal from Manhattan’s Upper East Side, I can assure you from direct experience that this group has, at best, ambiguous feelings about the lower orders of mankind — my Gawd, did he actually say that? — and, at worst, a certain unmanageable contempt that stirs deep fears of moral failure. Mr. Trump’s remark raises another interesting question that has not received much analysis amidst the latest panic: namely, how much of a “shithole” is our own country these days?

I would avouch, contrary to the limp narrative of boom times, that the USA is visibly whirling around the drain in just about every way that matters. Except for the centers of financialization — New York, Washington, San Francisco — most of our cities are hollowed-out wrecks, and visitors to San Francisco will tell you that the place is literally a shithole, from the army of homeless people who, by definition, have no bathrooms. Our ghastly suburbs, where so many formerly middle-class Americans are now marooned in debt, despair, and civic alienation, have no prospects for serving as a plausible living arrangement anymore, and were so badly built in the first place that their journey to ruin is destined to be an epically short leap that will amaze historians of the future roasting ‘possums around their campfires.

All of the important activities in this land have been converted into odious rackets, by which I mean nakedly dishonest money-grubbing scams, especially the two sectors that used to be characterized by first, doing no harm (medicine), and seeking the truth (education). But everything else we do is infected by engineered falsehood and mendacity, including the news media, the law, banking, government, retail commerce, you name it. We’re living in a culture of pervasive control fraud, in which authorities set up looting and asset-stripping operations without any restraint.

They should be testing us, not the other way around.

• Dolphins Show Self-Recognition Earlier Than Human Children (NYT)

Humans, chimpanzees, elephants, magpies and bottle-nosed dolphins can recognize themselves in a mirror, according to scientific reports, although as any human past age 50 knows, that first glance in the morning may yield ambiguous results. Not to worry. Scientists are talking about species-wide abilities, not the fact that one’s father or mother makes unpredictable appearances in the looking glass. Mirror self-recognition, at least after noon, is often taken as a measure of a kind of intelligence and self-awareness, although not all scientists agree. And researchers have wondered not only about which species display this ability, but about when it emerges during early development. Children start showing signs of self-recognition at about 12 months at the earliest and chimpanzees at two years old.

But dolphins, researchers reported Wednesday, start mugging for the mirror as early as seven months, earlier than humans. Diana Reiss a psychologist at Hunter College, and Rachel Morrison, then a graduate student working with Reiss, studied two young dolphins over three years at the National Aquarium in Baltimore. Dr. Reiss first reported self-recognition in dolphins in 2001 with Lori Marino, now the head of The Kimmela Center for Animal Advocacy. She and Dr. Morrison, now an assistant professor in the psychology department at the University of North Carolina Pembroke collaborated on the study and published their findings in the journal PLoS One. Dr. Reiss said the timing of the emergence of self-recognition is significant, because in human children the ability has been tied to other milestones of physical and social development.

Since dolphins develop earlier than humans in those areas, the researchers predicted that dolphins should show self-awareness earlier. Seven months was when Bayley, a female, started showing self-directed behavior, like twirling and taking unusual poses. Dr. Reiss said dolphins “may put their eye right up against the mirror and look in silence. They may look at the insides of their mouths and wiggle their tongues.” Foster, the male, was almost 14 months when the study started. He had a particular fondness for turning upside down and blowing bubbles in front of the one-way mirror in the aquarium wall through which the researchers observed and recorded what the dolphins were doing.

The animals also passed a test in which the researchers drew a mark on some part of the dolphin’s body it could not see without a mirror. In this so-called mark test, the animal must notice and pay attention to the mark. Animals with hands point at the mark and may touch it. The dolphins passed that test at 24 months, which was the earliest researchers were allowed to draw on the young animals. Rules for animal care prohibited the test at an earlier age because of a desire to have the animals develop unimpeded. During testing, the young animals were always with the group of adults they live with, and only approached a one-way mirror in the aquarium wall when they felt like it.

A loss of 2% oxygen is all it takes.

• The Ocean Is Suffocating—But Not For The First Time (Atlantic)

The ocean is losing its oxygen. Last week, in a sweeping analysis in the journal Science, scientists put it starkly: Over the past 50 years, the volume of the ocean with no oxygen at all has quadrupled, while oxygen-deprived swaths of the open seas have expanded by the size of the European Union. The culprits are familiar: global warming and pollution. Warmer seawater both holds less oxygen and turbocharges the worldwide consumption of oxygen by microorganisms. Meanwhile, agricultural runoff and sewage drives suffocating algae blooms. The analysis builds on a growing body of research pointing to increasingly sick seas pummeled by the effluent of civilization. In one landmark paper published last year, a research team led by the German oceanographer Sunke Schmidtko quantified for the first time just how much oxygen human civilization has already drained from the oceans.

Compiling more than 50 years of disparate data, gathered on research cruises, from floating palaces of ice in the arctic to twilit coral reefs in the South Pacific, Schmidtko’s team calculated that the Earth’s oceans had lost 2% of their oxygen since 1960. Two% might not sound that dramatic, but small changes in the oxygen content of the Earth’s oceans and atmosphere in the ancient past are thought to be responsible for some of the most profound events in the history of life. Some paleontologists have pointed to rising oxygen as the fuse for the supernova of biology at the Cambrian explosion 543 million years ago. Similarly, the fever-dream world of the later Carboniferous period is thought to be the product of an oxygen spike, which subsidized the lifestyles of preposterous animals, like dragonflies the size of seagulls.

On the other hand, dramatically declining oxygen in the oceans like we see today is a feature of many of the worst mass extinctions in earth history. “[Two%] is pretty significant,” says Sune Nielsen, a geochemist at the Woods Hole Oceanographic Institution in Massachusetts. “That’s actually pretty scary.” Nielsen is one of a group of scientists probing a series of strange ancient catastrophes when the ocean lost much of its oxygen for insight into our possible future in a suffocating world. He has studied one such biotic crisis in particular that might yet prove drearily relevant. Though little known outside the halls of university labs, it was one of the most severe crises of the past 100 million years. It’s known as Oceanic Anoxic Event 2.

Home › Forums › Debt Rattle January 13 2018