DPC Grace Church, New York 1905

How QE will tear societies apart.

• Majority Fears Future Generations ‘Will Never Be Able To Buy A Home’ (G.)

A large majority of people in Britain fears that future generations will never be able to buy or rent a home to settle down in. Research published on Monday shows three-quarters of people worry that long-term homes are out of reach, with the level of concern highest among members of generation X, now aged between 37 and 50, and generation Y, aged between 15 and 36. The poll by Ipsos/ Mori for the housing charity Shelter also found that 25- to 34-year-olds have moved more than twice as frequently per year of their lifetime as pensioners. Shelter said the findings were “alarming” and warned the country was at the “mercy of the housing crisis”, which has left millions facing a “lifetime of instability”.

The survey came as the average house price in England passed the £300,000 mark for the first time, increasing from £299,287 in February to £303,190, according to the property website Rightmove. Asking prices have jumped by more than £100,000 typically over the last decade, it said. In March 2006, the average price was £200,980. Average prices hit new heights across six regions. A typical home now costs £644,045 to buy in London; £399,680 in the south-east; £326,836 in east England; £292,251 in the south-west; £204,140 in the West Midlands; and £177,437 in the north-west. Rents rose on average by 4.8% last year across the UK, according to data from Homelet, an insurance company. They rose 7.7% in London, 6.7% in the east Midlands and 6.5% in the south-east.

Campbell Robb, chief executive of Shelter, said the nation’s housing system was broken. “The fact that vast numbers of people fear their grandchildren will never have a home to put down roots highlights the sad truth that this country is once again at the mercy of a housing crisis. Our current housing shortage means millions are facing a lifetime of instability and, understandably, people are giving up hope. But if our history tells us anything, it’s that together we can make things change. For the sake of future generations we cannot make this crisis someone else’s problem.” He added: “You have graduates starting on £40,000 to £45,000 in London, and they don’t take the jobs because they can’t afford to live in London or can’t afford to buy because it is so expensive. We are seeing a generation of people now in their 50s or 60s who are looking at their children, and their children will be worse off than they are. That is the first generation since WWII that we are seeing that happen to, and that is primarily because of the housing market.”

More of the above.

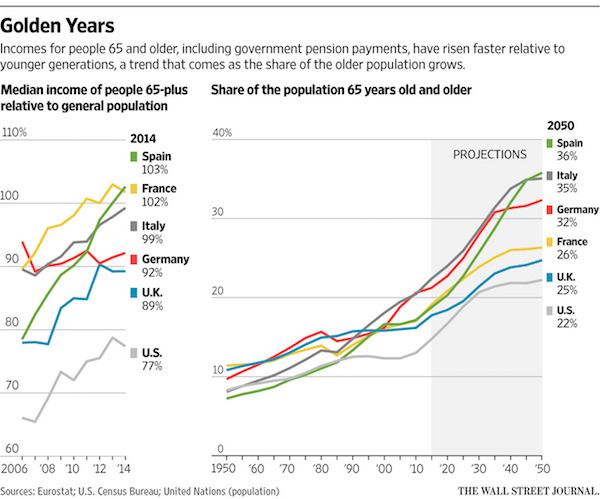

• When Older People Do Better Than Those of Working Age (WSJ)

In deciphering the many forces behind income inequality, economists are flagging a widening shift in the economic fortunes of the old and everyone else. Older people typically have lower incomes than the general population because many of them have stopped working. But the gap between the incomes of those 65 and older and the rest of the population has narrowed significantly in Europe and the U.S. since the recession. The divergence is exacerbating generational imbalances in government pension systems while highlighting the wage struggles of younger workers. Seniors in the U.S. have recently enjoyed healthier income gains—from government and private pensions, investments and, for those still working, salaries—than their younger counterparts, census data shows.

In some countries, France and Spain among them, people 65 and older now earn more on average than younger people do. The average person 65 and older in the U.S. earns 77% of the income of the average citizen, up from 69% in 2008, at the start of the recession. In the U.K. the figure is 89%, up from 78%. In Spain and France, seniors now earn about 103% and 102% of the average worker’s income, respectively, according to an analysis of data from the EU’s official statistics agency. That’s up from 86% in Spain and 96% in France in 2008. This divergence between generations is in part a reflection of demographic shifts that have been brewing for years, as populations grow older and the wealthy postwar baby boomers in particular reach their golden years.

But it is also widening as a consequence of forces bearing down on the earnings of the young, creating a growing imbalance that threatens to undermine the promise that market economies will deliver rising living standards for successive generations. Younger workers are grappling with flat or falling pay, decreased job security and less-affordable housing, sapping the spending power that helps fuel the economy. As the elderly population increases, younger workers also face a rising bill for the extra tax dollars needed to fulfill past governments’ promises to retirees. In parts of Europe, especially, older generations’ incomes are growing in excess of their children’s, often as a direct result of postcrisis government policy, economists say. Consider the U.K. Between 2008 and 2014, the average annual income of seniors in Britain rose 7.3%, or £1,400. Over the same period, the average annual income of working households fell by 5.5%, or £1,600.

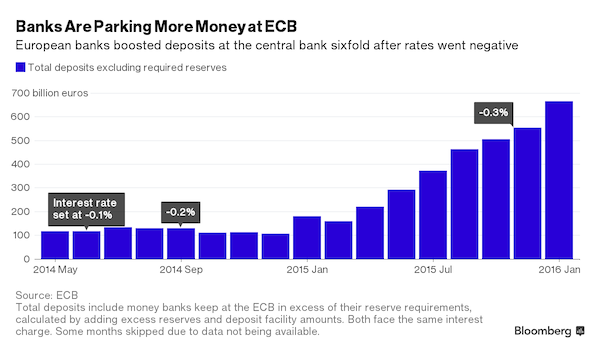

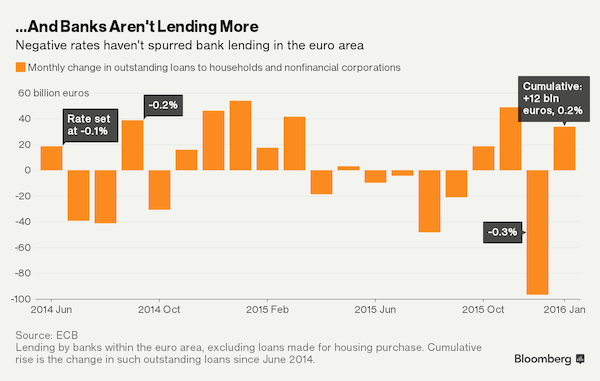

ECB buys €60 billion (now $80 billion) per month, but: “..Lending to nonfinancial companies and consumers, excluding mortgages, has been stuck at about €6.8 trillion since June 2014..”

• ECB Doing Whatever It Takes Can’t Push Euro-Area Banks to Lend (BBG)

The European Central Bank began charging banks interest on deposits in June 2014 to encourage them to lend more to companies and consumers. It hasn’t worked. Deposits at the ECB by euro-area banks in excess of required reserves have jumped sixfold since the introduction of negative interest rates, while lending within the currency bloc has barely budged. Of the €646 billion that banks added in assets during the period, about 85% has ended up as deposits at the central bank.

One reason banks are paying to keep money idle is a lack of demand for loans in an economy still recovering from a double-dip recession and a sovereign-debt crisis. Another is that banks saddled with bad loans or low capital levels and those in the midst of restructuring are reluctant to increase lending. Even the ECB’s latest offer to pay banks interest on money they borrow from the central bank may not do the trick. “They’re not profitable enough to substantially increase lending, so even the negative rate for lending by the ECB to the banks probably won’t help much,” said Jan Schildbach at Deutsche Bank in Frankfurt. “It’s not lack of liquidity or its price that’s the problem.”

Lending to nonfinancial companies and consumers, excluding mortgages, has been stuck at about €6.8 trillion since June 2014, ECB data show, despite the central bank’s liquidity programs to encourage more of those loans. Policy makers have looked at those figures when determining how much cheap money to provide lenders. Banks that increase such loans qualify for more funds. When it went deeper into minus territory on March 10, the ECB said it would use similar criteria to determine if a bank qualifies for negative rates on money it borrows from the central bank. That means the ECB is now willing to pay banks to borrow at the same rate it charges for excess deposits they hold there. And it’s willing to do so even if a bank isn’t increasing lending, as long as the firm is reducing lending at a slower rate than in the previous 12 months.

Bubble.

• Emerging-Market Currencies Fall Back to Earth After Fed Euphoria (BBG)

Emerging-market currencies retreated from multi-month highs as commodity prices fell and the dollar reasserted itself after the Federal Reserve’s dovish turn pushed it down last week. Malaysia’s ringgit led declines, falling from a seven-month high as a drop in Brent crude worsened the outlook for the oil exporter. Currencies from nations dependent on raw materials weakened, including South Africa’s rand and Mexico’s peso. China cut the yuan fixing by the most in three months, while South Korea’s won retreated from the strongest level since December as a technical indicator suggested it’s been overbought against the dollar. The MSCI Emerging Markets Index of stocks declined after entering a bull market Friday.

A gauge of the greenback against its major peers extended its rebound into a second day after slumping to a five-month low last week as the Federal Reserve pared its interest-rate outlook for 2016. That spurred a retreat in the prices of raw materials that have tracked gains in oil this month, damping the export outlook for many developing nations. While China’s economy has stabilized, the longer-term story of slowing growth remains unchanged, according to Bank of Singapore. “The market is making sense of the dovish Fed surprise and thinking that perhaps data in the U.S. will eventually force the Fed’s hand to raise rates more and faster,” said Sim Moh Siong at Bank of Singapore. “I don’t think emerging-market fundamentals have changed all that much.”

Ouch!: “About one-third of listed Chinese companies owe at least three times as much in debt as they own in assets..”

• China Central Bank Governor Warns Over Corporate Debt (FT)

China’s central bank governor has warned that the country’s corporate debt levels are too high and are stoking risks for the economy, just as highly-leveraged Chinese companies have gone on an overseas takeover binge. Adding his voice to a recent chorus of concern by senior Chinese officials, Zhou Xiaochuan, governor of the People’s Bank of China (PBoC), told global business leaders meeting in Beijing that the ratio of lending to gross domestic product was becoming excessive. “Lending and other debt as a share of GDP, especially corporate lending and other debt as a share of GDP, is on the high side,” he said, adding that a highly leveraged economy was more prone to macroeconomic risk. Corporate debt in China has risen to about 160% of GDP, while total debt is about 230%.

The Bank for International Settlements warned this month that a steep rise in private and corporate debt in emerging market economies -“including the largest”- was “eerily reminiscent” of the pre-crisis financial boom in advanced economies. Mr Zhou’s comments came at the end of a week of extraordinary dealmaking by Chinese companies overseas, with Anbang, the Chinese insurance company, bidding nearly $20bn for Starwood Hotels & Resorts and Strategic Hotels & Resorts. Total outbound Chinese merger and acquisitions spending since January is over $100bn, according to figures from Dealogic. Data from 54 Chinese companies that did overseas deals last year show that many are “highly leveraged”, according to S&P.

Chinese officials are concerned that the stability of China’s financial system could be threatened if Chinese companies are unable to repay a large amount of debt, which in turn can threaten economic growth. And as recent months have shown, instability in Chinese financial markets and risks to mainland economic growth rapidly feed through into global markets. [..] Last week China’s chief banking regulator announced a move to try to tackle the country’s bad debt problem by opening the way for the country’s lenders to use debt-for-equity swaps to rid themselves of some of the $200bn of bad bank loans on their balance sheets. Shang Fulin, chairman of the China Banking Regulatory Commission, raised the idea at the closing session of the annual meeting of parliament in Beijing.

The plan has been put forward as a way of tackling the trillions of renminbi of debt that have built up in the Chinese economy as a result of decades of debt-fuelled stimulus and easy credit. Chinese banks’ bad debts stand at Rmb1.27tn, according to official figures, although some analysts believe the real number is many times higher. About one-third of listed Chinese companies owe at least three times as much in debt as they own in assets, according to figures from Wind.

Pushed it up to the highest this year on Friday, takes it down again today. Yeah, credibility…

• PBOC See-Saws -Again- On Yuan Rate Guidance (CNBC)

Strategists are back to debating the direction of China’s currency after the central bank guided the yuan lower on Monday, having let it rise to its highest level of the year against the dollar on Friday. Jan Lambregts, Rabobank’s global head of financial markets research, told CNBC on Monday that he’s anticipating a ten to fifteen% depreciation over the next twelve months. The world’s second-largest economy is facing an unprecedented set of economic and policy challenges and in order to overcome them, the government will have to start making more bold moves in the currency, he explained. “We feel that [yuan depreciation] is a relatively easy step for China compared to the hard, structural reforms they need to do.”

Beijing is expected play down the significance of currency weakness but the country’s rising economic challenges, including a long-awaited restructuring of state-owned enterprises, leave policymakers with little choice, he continued. Following a volatile start to the year, the yuan hit a 2016 high last week following dovish remarks from the U.S. Federal Reserve but recent fixings by the People’s Bank of China revived speculation that authorities may prefer a weaker currency. Monday’s mid-point level was 6.4824 per dollar, 0.3% weaker than the Friday’s mid-point rate of 6.4628. China’s central bank lets the yuan spot rate rise or fall a maximum of 2% against the dollar, relative to the official fixing rate.

Like Lambregts, Michael Heise, chief economist at Allianz, said the yuan could drop to around 7 per dollar as soon as this year. In a recent CNBC editorial, he explained that would bode well with the government’s objective of a market-driven exchange rate.

Should these predictions come true however, it would further damage Beijing’s credibility in the eyes of global markets. Ever since the yuan’s landmark devaluation last August, speculation for further weakness was rife but Beijing has repeatedly shut down those assumptions, warning that it was not targeting more depreciation.

Look, this is simply an economy in deep trouble.

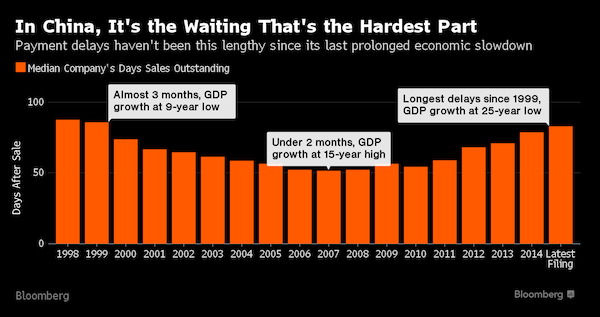

• China Has a $590 Billion Problem With Unpaid Bills (BBG)

Not since 1999 have China’s companies had so much trouble getting customers to actually pay for what they’ve bought. It now takes about 83 days for the typical Chinese firm to collect cash for completed sales, almost twice as long as emerging-market peers. As payment delays spread from the industrial sector to technology and consumer companies, accounts receivable at the nation’s public firms have swelled by 23% over the past two years to about $590 billion, exceeding the annual economic output of Taiwan. The raft of unpaid bills – bigger than at any time since former Premier Zhu Rongji shuttered thousands of state-run companies at the turn of the century – shows how cash shortages at the weakest firms threaten not only banks and bondholders, but also China’s vast web of interconnected supply chains.

With corporate bankruptcies projected to climb 20% this year, more Chinese businesses may be forced to choose between two unpleasant options: keep extending credit to potentially insolvent customers, or cut off the taps and watch sales sink. “There is a knock-on effect through the economy,” said Fraser Howie, the Singapore-based co-author of “Red Capitalism: The Fragile Financial Foundation of China’s Extraordinary Rise,” who has followed the nation’s markets for more than two decades. “Part of the end game is default and closure.” It’s easy to see why collecting payments is getting harder in China. Businesses and consumers have been squeezed by the deepest economic slowdown since 1990, while overcapacity has fueled an unprecedented stretch of declines in producer prices. Record corporate debt levels have left many firms struggling to meet their liabilities, with corporate insolvencies jumping by 25% in 2015, according to Euler Hermes.

The world’s largest trade credit insurer sees another 20% increase in Chinese bankruptcies this year, the most among 43 major markets. “It’s a big problem when you have rising insolvencies, a bad economic environment and less liquidity for small companies,” said Mahamoud Islam, the firm’s senior Asia economist in Hong Kong. Those headwinds are increasingly visible in Chinese financial statements, where the accounts receivable and sales entries allow analysts to calculate “days sales outstanding,” or how long it takes a firm to get paid. The median collection time of 83 days has climbed from 79 days in 2014 and 55 days in 2010. It’s higher than in any of the world’s 20 biggest economies except Italy, and compares with the 44-day median for companies in the MSCI EM Index. Chinese industrial firms take longest to convert sales into cash, at 131 days, followed by 120 days for technology companies and 118 days for telecommunications firms.

“The reality is that TTIP is being pushed through in the EU by US authorities and we have no choice in the matter.”

• TTIP: Fake Freedom Moves Closer To Open Slavery (Gerrans)

The new trade negotiations – TTIP – sound dull. It combines the US and EU markets to make the process of fleecing the sheep simpler and cheaper for the wolves. Standard procedure, you may say – and you would be right. But what is interesting is that any pretense at democracy has been dropped from the propaganda song sheet. The Telegraph summarized TTIP thus: “The Transatlantic Trade and Investment Partnership is a series of trade negotiations being carried out mostly in secret between the EU and US. As a bi-lateral trade agreement, TTIP is about reducing the regulatory barriers to trade for big business, things like food safety law, environmental legislation, banking regulations and the sovereign powers of individual nations. It is, as John Hilary, Executive Director of campaign group War on Want, said: “An assault on European and US societies by transnational corporations.”

The advantage of TTIP branding from a population-management point of view is that it sounds so boring; a bit like a truncated version of Tippex as envisaged by someone with dyslexia – how evil can it be? The answer is: more evil than drinking noxious white fluid designed to correct typing errors. Under TTIP, public services, education and health services will be open for tender. EU food and cosmetics standards will be brought in line with the much lower standards in operation in the US. What banking protections exist after the last collapse will likely be removed. The walls in data privacy will become porous between the two blocs. And since the US is party to NAFTA, it will mean that EU workers will be in competition with Mexico. Nothing will be allowed to stand in the way of making a buck.

As the Telegraph puts it: “One of the main aims of TTIP is the introduction of Investor-State Dispute Settlements (ISDS), which allow companies to sue governments if those governments’ policies cause a loss of profits. In effect it means unelected transnational corporations can dictate the policies of democratically elected governments.” Put nicely, then, TTIP is a drive to the lowest common denominator between the laws which currently exist in the EU and the US combined with the creation of an unaccountable executive branch committed only to the interests of corporations. This means the workers in both areas will be on an accelerated race to the bottom, able only to compete on the basis of slave wages.

Put more generally, it is the creation of a mega-bloc designed to subsume the EU by stealth and place it in the thrall of the powers which control the US. Of course, those tasked with selling TTIP to the people it is going to fleece, claim nothing but upside. They cite the usual carrots: more jobs, higher wages, lower prices. But then they would say that, wouldn’t they? The reality is that TTIP is being pushed through in the EU by US authorities and we have no choice in the matter. This is where a modern commentator is supposed to be outraged: corporations and government cabals are in collusion – how could they! But I don’t see it that way. This isn’t a freak occurrence. Socrates placed democracy one step away from tyranny. What’s happening now isn’t democracy warping into something fiendish and weird. This is democracy’s natural pathway; where it was always going.

The classes themselves are being redefined.

• The New Class Warfare In America (Luce)

Say what you like about Donald Trump, he knows his market. “I love the poorly educated,” he said recently to cheers from those he loves. The rest of America inhaled sharply. Welcome to a very un-American debate. Once redundant, the term “working class” is now part of everyday conversation. In an age of stifling political correctness, the only people who are fair game in polite society are blue-collar whites. How absurd these people are, we tell each other, and how ignorant. Don’t they know Mr Trump was born rich? Can they really be so stupid as to fall for his con trick? The derision is not limited to liberal elites. Educated conservatives are just as scathing. Take the National Review, a flagship of thinking conservatives, that described Mr Trump as a “ridiculous buffoon with the worst taste since Caligula”.

In January it pulled together 22 intellectuals to condemn Mr Trump’s candidacy as an existential threat to conservatism. Their efforts had no impact on Mr Trump’s fan base. Now the magazine has switched to damning his supporters. By declaring open season on blue-collar whites, Kevin Williamson’s widely read essay on “white working class dysfunction” marks a turning point. Yet he is only putting into writing what many conservatives say. “The truth about these dysfunctional, downscale communities is that they deserve to die,” Mr Williamson writes. “Economically, they are negative assets. Morally, they are indefensible . . . the white American underclass is in thrall to a vicious, selfish culture whose main products are misery and used heroin needles. Donald Trump’s speeches make them feel good. So does OxyContin.”

Margaret Thatcher’s acolyte, Norman Tebbit, once sparked fury by implying the jobless should get on their bikes to find work. Mr Williamson says America’s benighted working classes should hire a U-Haul and move on. As an exercise in condescension, Mr Williamson’s words rival the most inbred hereditary peer. As an economic prescription, it is wide of the mark. Millions of Americans are anchored to blighted neighbourhoods by negative equity, or other ties that bind. Their life expectancy is falling. Their participation in the labour market is dropping. The numbers signing up to disability benefits is rising. Opioid prescription drugs are rife. Those that are white tend to vote for Mr Trump. On Super Tuesday this month, the counties with the highest rates of white mortality – whether to overdoses, suicide or other symptoms of community breakdown – came out heavily for Mr Trump. The correlation was almost exact, according to a Wonkblog study.

“..corals in the remote far north of the reef, where surface sea temperatures reached 33C in February..”

• Great Barrier Reef Coral Bleaching Threat Raised To Highest Level (G.)

Australian environment minister Greg Hunt has been accused of going silent on climate change as the cause of dying coral in the Great Barrier Reef after a bleaching alert was raised to its highest level. Hunt, who surveyed the widespread death of coral in the far north of the reef by plane on Sunday, announced plans for more monitoring and programs to tackle run-off pollution and crown-of-thorns starfish outbreaks. But critics including conservationists and the Queensland environment minister, Steven Miles, said Hunt’s response sidestepped the central role of climate change and heat stress as the cause of the bleaching. Miles said Hunt’s announcements were “window dressing” that duplicated state efforts and ignored the need for a “credible federal government climate policy to address the cause”.

The Great Barrier Reef marine park authority raised the threat level of coral bleaching to a peak of three on Sunday, triggering its highest level of response to “severe regional bleaching” in the northernmost quarter of the 344,400 sq km marine park. The authority’s chairman, Russell Reichelt, said corals in the remote far north of the reef, where surface sea temperatures reached 33C in February, were “effectively bathed in warm water for months, creating heat stress that they could no longer cope with”. “We still have many more reefs to survey to gauge the full impact of bleaching, however, unfortunately, the further north we go from Cooktown the more coral mortality we’re finding,” he said.

Hey, it’s simple, you just redefine anything you don’t like: “..several European countries recently began screening Syrians to determine whether the cities they came from were buffeted by conflict or considered “safe,” meaning that not all Syrians will be eligible for asylum.”

• Greece Struggles To Enforce Migrant Accord On First Day (NY Times)

Greece and the EU scrambled on Sunday to put in place the people and the facilities needed to carry out a new deal intended to address the refugee crisis that is roiling Europe, as hundreds of migrants in rubber dinghies continued to land on the Greek islands from Turkey. The accord, struck between the union and Turkey on Friday, set a 12:01 a.m. Sunday deadline for Turkey to stem the flow of people making clandestine journeys across the Aegean Sea to Greece in an attempt to enter Europe, and required Greece to begin sending back migrants who are not eligible for asylum. Yet processing centers on the Greek island of Lesbos and on several other Greek islands were not adequately staffed to comply immediately with the new measures, and officials said they were waiting for the EU to follow through on a pledge to send at least 2,300 European police and asylum experts to help.

By Sunday afternoon, around 875 migrants in rubber boats had reached the Greek islands since midnight, the government said, despite an operation in Turkey that began Friday to detain migrants and the smugglers who make their journeys possible. Many migrants landing in Lesbos on Sunday appeared to be unaware of the new policies and were reeling from their harrowing journey. Greek television showed black and gray rafts arriving at the island laden with people, some sobbing with relief at having reached Europe, and others nearly unconscious. Two little girls were found drowned, and two Syrian refugees died in the crossings over the weekend. On Sunday, the Greek government began clearing out more than 6,000 migrants who had been waiting at processing centers and camps on several Greek islands, and transporting them on large ferries to Piraeus, the port of Athens, and to Kavala, a port in northern Greece.

From there, they are to be sent to refugee camps recently set up around the country. Nearly 50,000 migrants are stuck on the Greek mainland at camps, in Piraeus and on Greece’s northern border with Macedonia. More than 10,000 people have been living in miserable conditions in the Idomeni camp, on the Macedonian border, after west Balkan countries sealed their borders last month to cut the flow of migrants making their way to Germany and northern Europe. Once emptied of their previous occupants, the migrant centers on the Greek islands are to be used only to process those who make it across the Aegean Sea through a phalanx of patrols run by Frontex, Europe’s border agency, as well as NATO and the Greek and Turkish Coast Guards The Greek authorities will register the migrants and process asylum applications.

Migrants who do not apply for asylum or whose applications are rejected are to be returned to Turkey within two weeks. Under the accord, for every Syrian refugee returned to Turkey, the European Union will resettle one refugee directly from Turkey. For the 10s of 1000s of other migrants stuck in camps around Greece, the situation is less clear. Many of them are Syrian and Iraqi nationals who, for the most part, are considered eligible for political asylum and a program that would relocate them across Europe. Yet governments in several European countries recently began screening Syrians to determine whether the cities they came from were buffeted by conflict or considered “safe,” meaning that not all Syrians will be eligible for asylum. In addition, around one-third of migrants in Greece are from Afghanistan. After several European countries last month abruptly reclassified them as “economic migrants,” most were disqualified from political asylum, and will most likely be repatriated. That process could be lengthy, even after help from other EU countries arrives in Greece.

Sorry, Wolfgang, way ahead of you on this one.

• The EU Sells Its Soul To Strike A Deal With Turkey (Münchau)

The EU had two assets I have always considered un≠assailable, however much I may have questioned various decisions. The first is a lack of alternatives. How else can Europeans confront climate change, a refugee crisis or an over-assertive Russian president if not through the EU? The second is the moral high ground. Compared with the majority of its member states, the EU is less corrupt, more principled and rules-driven. Whereas the world of national politics is full of tacticians out to seek short-term gain, the bloc manages a better mix of politics and policies. It builds broad coalitions and formulates strategic policy objectives. Its horizon extends beyond the life of a parliament. Within a few years those assets have been demolished. The mismanagement of the eurozone crisis made it possible to formulate a rational economic argument for an exit.

Then, on Friday the EU lost its other key asset. The deal with Turkey is as sordid as anything I have seen in modern European politics. On the day that EU leaders signed the deal, Recep Tayyip Erdogan, the Turkish president, gave the game away: Democracy, freedom and the rule of law … For us, these words have absolutely no value any longer. At that point, the European Council should have ended the conversation with Ahmet Davutoglu, the Turkish prime minister, and sent him home. But instead they made a deal with him money and a lot more in return for help with the refugee crisis. Turkey will relocate some 72,000 refugees to the EU a one-for-one swap for every illegal immigrant whom the Turks pick up on smuggler boats in the Aegean Sea. In return, the EU is paying Turkey €6bn and opening up a new chapter in EU accession negotiations -this with a country whose leadership has just abrogated democracy.

The EU is further set to allow visa-free travel to 75m inhabitants of Turkey. The EU not only sold its soul that day, it actually negotiated a pretty lousy deal. I am not in a position to judge whether this deal complies with the Geneva Convention and other parts of international law. I assume that the European Council has made sure it would stand up in court. But even if it is judged to be legal, I have doubts whether it can be implemented. It will be interesting to watch whether the EU will renege on its promises to Turkey if Ankara fails to deliver. Even if the deal is implemented in full, it will not lighten the pressure much. The expected number of refugees making their way into the EU will be a large multiple of the 72,000 agreed with Turkey. A German think-tank has done the maths on refugee flows for this year and has come up with an estimated range of 1.8m-6.4m. The latter figure is a worst-case scenario that would include large numbers from Northern Africa.

And counting fast.

• More Than 50,000 Refugees Now Stranded In Greece (Kath.)

A total of 50,411 migrants and asylum-seekers are currently in Greece according to fresh data provided by the government. According to the data, which were made public Monday, 28,593 migrants and refugees are currently in northern Greece, 13,711 in Attica (Athens), 5,538 on the islands and the rest scattered around the country.

The Libya route is (re-)opening for real. Terribly predictably. Even more drownings, it’s much longer.

• Nine Refugees Trying To Reach Europe Drown Off Libya (AFP)

Nine migrants trying to reach Europe have drowned off Libya and hundreds more been rescued, the Red Crescent said on Sunday amid fears of an increase in crossing attempts as the route from Turkey closes. Leaders from six EU nations led by Britain held talks in Brussels on Friday on how to tackle the flow of migrants across the Mediterranean from Libya after a European naval task force plucked more than 3,100 from the water in just three days. The nine who died were among several hundred migrants who were discovered aboard dilapidated boats off the port of Zawiya, west of Tripoli, on Saturday, Libyan Red Crescent spokesman Malek Mersit said.

A total of 586 migrants were rescued, said Colonel Ayoub Qassem, spokesman for the navy of a Tripoli administration that has disputed power with Libya’s internationally recognised government since 2014. They included 11 children and 60 women, and were mainly Bangladeshis and Sudanese, he said. The drownings came just days after four migrants were killed in a boat fire off Libya and another 187 rescued. European leaders fear that a deal with Turkey to tackle the EU’s worst ever migrant crisis will spark an acceleration in the already large number of crossing attempts from Libya. Around 330,000 have landed in Italy from Libya since the start of 2014. The lawlessness that has reigned in the North African nation since the Nato-backed overthrow of veteran dictator Moamer Qadhafi in 2011 has made it a favoured jumping-off point.

Saw some BBC coverage of this. Looked like heart attacks perhaps.

• Two Refugees Die On Arrival On Greek Island (AP)

Two migrants have been found dead on a boat that arrived on the Greek island of Lesvos, on the first day of the implementation of an agreement between the EU and Turkey on handling the new arrivals. Medical personnel performed CPR on the two men but failed to revive them. The overcrowded boat was carrying dozens of migrants from nearby Turkey on Sunday, the first day for the implementation of the migration agreement between the EU and Turkey. It stipulates how the new arrivals from Turkey will be processed and returned. Some 2,500 migrants currently on Lesvos and other islands are being taken to mainland Greece where they are placed in shelters before EU-wide relocation.

First thing that happened when the deal came into force. Lovely. Thanks, Europe, you make us proud.

• Three Baby Syrian Refugee Girls Drown Between Turkey, Greece (AFP)

A 4-month-old baby girl drowned off the southwestern coast of Turkey when a vessel carrying refugees sank early on March 19, while two other girls, aged between 1 and 2 years-old, were found drowned by Greek Coast Guards off the tiny island of Ro. According to the Turkish Coast Guard, 21 refugees were rescued, but the infant was found dead. The refugee boat reportedly was en route to the Greek island of Chios when it sank off the coast of the Cesme district. Cesme is just 7 kilometers from the island of Chios, providing a tempting target for refugees mostly Syrians fleeing their country s civil war.

Two little girls were found drowned off Ro, while two Syrians suffered heart attacks on arrival at the island of Lesbos, Boris Cheshirkov, a spokesman for the U.N. refugee agency, told AFP. Of the more than 1 million refugees who arrived in the EU last year, more than 850,000 arrived by sea in Greece from Turkey, according to the International Organization for Migration (IOM). Up until mid-March, more than 144,000 arrivals to Greece by sea were reported by the UNHCR, while more than 400 people were reported either dead or missing perilous journey.

Home › Forums › Debt Rattle March 21 2016