John Vachon Rain. Pittsburgh, Pennsylvania Jun 1941

US Q3 GDP was revised up by the BEA to 3.89%, but that’s no longer what financial markets react to. They sit and wait for more QE somewhere on the planet to be doled out. Will Americans, if they see this at all, take those numbers, add them to the sweet drop in prices at the pump and spend what they save on more holiday purchases? I’m not saying I know, but I do see that US consumer confidence is down, as is global business confidence – the latter at a five year low.

The Case/Shiller index reports a “broad-based slowdown” for US home prices, and that in the rear view mirror that looks at Q3. So that’s not where those 3.89% came from, it wasn’t housing (wonder what it was). The Gallup Christmas survey lost 8% of exuberance in one month. What this adds up to is that Americans may not spend all of that saved gas money, and that means there’s a real danger of deflation coming to America too – as if Japanese and European attempts to export their own were not enough yet.

While the media continue to just about exclusively paint a picture of recovery and an improving economy, certainly in the US – Europe and Japan it’s harder to get away with that rosy image -, in ordinary people’s reality a completely different picture is being painted in sweat, blood, agony and despair. Whatever part of the recovery mirage may have a grain of reality in it, it is paid for by something being taken away from people leading real lives. US unemployment numbers are being massages three ways to Sunday, as is common knowledge, or should be; the amounts of working age people not working, and not being counted as unemployed either, is staggering.

But there’s a very large, and growing, number of people who do work, but find it impossible to sustain either themselves or their families on their wages. That’s how the recovery, fake as it even is, is paid for. And this will have grave consequences for many years, if not decades, to come.

If a government would come clean with its citizens, explain the overwhelming debt situation a nation is in, that everyone will have to do with less at least for a while, and then openly start restructuring the debts, those consequences would be much less damaging. But all governments choose to talk about only recovery and growth, and to let their people suffer the consequences of the policies enacted to achieve these goals, even if after 6-7 years of crisis and dozens of trillions in stimulus, we’re no closer to either. Quite the contrary. We’re not in ‘drive’, we’re stuck in ‘reverse’. We’re backing up. We’re moving backwards.

Lance Roberts at StreetTalkLive provides stats on how many Americans have been made dependent on some sort of handout:

The Dismal Economy: 148 Million Government Beneficiaries

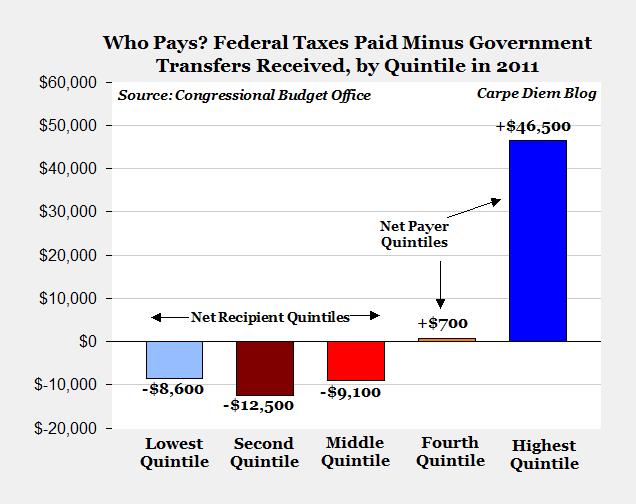

.. the Federal Reserve has stopped their latest rounds of bond buying and are now starting to discuss the immediacy of increasing interest rates. This, of course, is based on the “hopes” that the economy has started to grow organically as headline unemployment rates have fallen to just 5.9%. If such activity were real then both inflation and wage pressures should be rising – they are not. According to the Congressional Budget Office study that was just released, approximately 60% of all U.S. households get more in transfer payments from the government than they pay in taxes.

Roughly 70% of all government spending now goes toward dependence-creating programs. From 2009 through 2013, the U.S. government spent an astounding 3.7 trillion dollars on welfare programs. In fact, today, the percentage of the U.S. population that gets money from the federal government grew by an astounding 62% between 1988 and 2011. Recent analysis of U.S. government numbers conducted by Terrence P. Jeffrey, shows that there are 86 million full-time private sector workers in the United States paying taxes to support the government, and nearly 148 million Americans that are receiving benefits from the government each month.

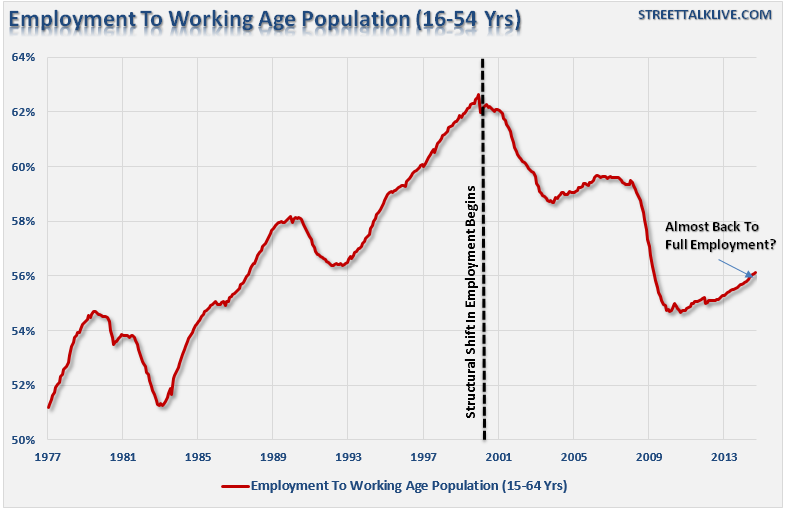

Yet Janet Yellen, and most other mainstream economists suggests that employment is booming in the U.S. Okay, if we assume that this is indeed the case then why, according to the Survey of Income and Program Participation conducted by the U.S. Census, are well over 100 million Americans are enrolled in at least one welfare program run by the federal government. Importantly, that figure does not even include Social Security or Medicare. (Here are the numbers for Social Security, Medicaid and Medicare: More than 64 million are receiving Social Security benefits, more than 54 million Americans are enrolled in Medicare and more than 70 million Americans are enrolled in Medicaid.) Furthermore, how do you explain the chart below? With roughly 45% of the working age population sitting outside the labor force, it should not be surprising that the ratio of social welfare as a percentage of real, inflation-adjusted, disposable personal income is at the highest level EVER on record.

Tyler Durden addresses deteriorating wages in America with a great metaphor:

The Mystery Of America’s “Schrodinger” Middle Class, Which Is Either Thriving Or About To Go Extinct

On one hand, the US middle class has rarely if ever had it worse. At least, if one actually dares to venture into this thing called the real world, and/or believes the NYT’s report: “Falling Wages at Factories Squeeze the Middle Class.” Some excerpts:

For nearly 20 years, Darrell Eberhardt worked in an Ohio factory putting together wheelchairs, earning $18.50 an hour, enough to gain a toehold in the middle class and feel respected at work. He is still working with his hands, assembling seats for Chevrolet Cruze cars at the Camaco auto parts factory in Lorain, Ohio, but now he makes $10.50 an hour and is barely hanging on. “I’d like to earn more,” said Mr. Eberhardt, who is 49 and went back to school a few years ago to earn an associate’s degree. “But the chances of finding something like I used to have are slim to none.” Even as the White House and leaders on Capitol Hill and in Fortune 500 boardrooms all agree that expanding the country’s manufacturing base is a key to prosperity, evidence is growing that the pay of many blue-collar jobs is shrinking to the point where they can no longer support a middle-class life.

In short: America’s manufacturing sector is being obliterated: “A new study by the National Employment Law Project, to be released on Friday, reveals that many factory jobs nowadays pay far less than what workers in almost identical positions earned in the past.

Perhaps even more significant, while the typical production job in the manufacturing sector paid more than the private sector average in the 1980s, 1990s and early 2000s, that relationship flipped in 2007, and line work in factories now pays less than the typical private sector job. That gap has been widening — in 2013, production jobs paid an average of $19.29 an hour, compared with $20.13 for all private sector positions. Pressured by temporary hiring practices and a sharp decrease in salaries in the auto parts sector, real wages for manufacturing workers fell by 4.4% from 2003 to 2013, NELP researchers found, nearly three times the decline for workers as a whole.

How is this possible: aren’t post-bankruptcy GM, and Ford, now widely touted as a symbol of the New Normal American manufacturing renaissance? Well yes. But there is a problem: recall what we wrote in December 2010: ‘Charting America’s Transformation To A Part-Time Worker Society:”

.. one of the most important reasons for lower pay is the increased use of temporary workers. Some manufacturers have turned to staffing agencies for hiring rather than employing workers directly on their own payroll. For the first half of 2014, these agencies supplied one out of seven workers employed by auto parts manufacturers. The increased use of these lower-paid workers, particularly on the assembly line, not only eats into the number of industry jobs available, but also has a ripple effect on full-time, regular workers. Even veteran full-time auto parts workers who have managed to work their way up the assembly-line chain of command have eked out only modest gains.

And that’s not some isolated incident, as the Guardian makes clear, it’s the same thing in Britain.:

Record Numbers Of UK Working Families In Poverty Due To Low-Paid Jobs

Insecure, low-paid jobs are leaving record numbers of working families in poverty, with two-thirds of people who found work in the past year taking jobs for less than the living wage, according to the latest annual report from the Joseph Rowntree Foundation. The research shows that over the last decade, increasing numbers of pensioners have become comfortable, but at the same time incomes among the worst-off have dropped almost 10% in real terms. Painting a picture of huge numbers trapped on low wages, the foundation said during the decade only a fifth of low-paid workers managed to move to better paid jobs. The living wage is calculated at £7.85 an hour nationally, or £9.15 in London – much higher than the legally enforceable £6.50 minimum wage.

As many people from working families are now in poverty as from workless ones, partly due to a vast increase in insecure work on zero-hours contracts, or in part-time or low-paid self-employment. Nearly 1.4 million people are on the controversial contracts that do not guarantee minimum hours, most of them in catering, accommodation, retail and administrative jobs. Meanwhile, the self-employed earn on average 13% less than they did five years ago, the foundation said. Average wages for men working full time have dropped from £13.90 to £12.90 an hour in real terms between 2008 and 2013 and for women from £10.80 to £10.30.

Poverty wages have been exacerbated by the number of people reliant on private rented accommodation and unable to get social housing, the report said. Evictions of tenants by private landlords outstrip mortgage repossessions and are the most common cause of homelessness. The report noted that price rises for food, energy and transport have far outstripped the accepted CPI inflation of 30% in the last decade. Julia Unwin, chief executive of the foundation, said the report showed a real change in UK society over a relatively short period of time. “We are concerned that the economic recovery we face will still have so many people living in poverty. It is a risk, waste and cost we cannot afford: we will never reach our full economic potential with so many people struggling to make ends meet.

And it’s even worse in Greece and Spain and Italy, all so northern Europe and the Brussels politicos can keep alive the idea that Germany and Holland are doing well, and overall growth is almost at hand. That southern Europe must suffer for that idea has been justified away for years now, and it’s not even an issue deemed worth discussing anymore.

And that attitude will blow up in their faces, it’s inevitable that it will. Very few people understand how dangerous the games are that our governments and central banks play. And when the effects do play out, they will be blamed on other causes. Debt and propaganda rule our world supreme.

Excellent writer and great friend Jim Kunstler shows how simple the entire facade is to fathom, and how the next step away from the mess we’re in is so painfully obvious: downscale.

Buy the All Time High

Wall Street is only one of several financial roach motels in what has become a giant slum of a global economy. Notional “money” scuttles in for safety and nourishment, but may never get out alive. Tom Friedman of The New York Times really put one over on the soft-headed American public when he declared in a string of books that the global economy was a permanent installation in the human condition. What we’re seeing “out there” these days is the basic operating system of that economy trying to shake itself to pieces. The reason it has to try so hard is that the various players in the global economy game have constructed an armature of falsehood to hold it in place — for instance the pipeline of central bank “liquidity” creation that pretends to be capital propping up markets.

It would be most accurate to call it fake wealth. It is not liquid at all but rather gaseous, and that is why it tends to blow “bubbles” in the places to which it flows. When the bubbles pop, the gas will tend to escape quickly and dramatically, and the ground will be littered with the pathetic broken balloons of so many hopes and dreams. All of this mighty, tragic effort to prop up a matrix of lies might have gone into a set of activities aimed at preserving the project of remaining civilized. But that would have required the dismantling of rackets such as agri-business, big-box commerce, the medical-hostage game, the Happy Motoring channel-stuffing scam, the suburban sprawl “industry,” and the higher ed loan swindle.

All of these evil systems have to go and must be replaced by more straightforward and honest endeavors aimed at growing food, doing trade, healing people, traveling, building places worth living in, and learning useful things.

All of those endeavors have to become smaller, less complex, more local, and reality-based rather than based, as now, on overgrown and sinister intermediaries creaming off layers of value, leaving nothing behind but a thin entropic gruel of waste. All of this inescapable reform is being held up by the intransigence of a banking system that can’t admit that it has entered the stage of criticality. It sustains itself on its sheer faith in perpetual levitation. It is reasonable to believe that upsetting that faith might lead to war.

But that’s not yet where we are, though Ferguson sure looks close to that war Jim talks about. Our leading classes will not let us downscale, no matter how much sense that makes for the ‘lower’ 95% of the population, because that would risk their leading positions. And so we’ll have to deal with a lot more misery before the whole edifice finally blows up, and we’ll end up with huge swaths of traumatized people. In a great article, Lynn Stuart Parramore describes how that works:

So Many People Are Badly Traumatized by Life in America: It’s Time We Admit It

Recently Don Hazen, the executive editor of AlterNet, asked me to think about trauma in the context of America’s political system. As I sifted through my thoughts on this topic, I began to sense an enormous weight in my body and a paralysis in my brain. What could I say? What could I possibly offer to my fellow citizens? Or to myself? After six years writing about the financial crisis and its gruesome aftermath, I feel weariness and fear. When I close my eyes, I see a great ogre with gold coins spilling from his pockets and pollution spewing from his maw lurching toward me with increasing speed. I don’t know how to stop him. Do you feel this way, too?

All along the watchtower, America’s alarms are sounding loudly. Voter turnout this last go-round was the worst in 72 years, as if we needed another sign that faith in democracy is waning. Is it really any wonder? When your choices range from the corrupt to the demented, how can you not feel that citizenship is a sham? Research by Martin Gilens and Benjamin I. Page clearly shows that our lawmakers create policy based on the desires of monied elites while “mass-based interest groups and average citizens have little or no independent influence.” Our voices are not heard.

When our government does pay attention to us, the focus seems to be more on intimidation and control than addressing our needs. We are surveilled through our phones and laptops. As the New York Times recently reported, a surge in undercover operations from a bewildering array of agencies has unleashed an army of unsupervised rogues poised to spy upon and victimize ordinary people rather than challenge the real predators who pillage at will. Aggressive and militarized police seem more likely to harm us than to protect us, even to mow us down if necessary.

Our policies amplify the harm. The mentally ill are locked away in solitary confinement, and even left there to die. Pregnant women in need of medical treatment are arrested and criminalized. Young people simply trying to get an education are crippled with debt. The elderly are left to wander the country in RVs in search of temporary jobs. If you’ve seen yourself as part of the middle class, you may have noticed cries of agony ripping through your ranks in ways that once seemed to belong to worlds far away.

[..] A 2012 study of hospital patients in Atlanta’s inner-city communities showed that rates of post-traumatic stress are now on par with those of veterans returning from war zones. At least 1 out of 3 surveyed said they had experienced stress responses like flashbacks, persistent fear, a sense of alienation, and aggressive behavior. All across the country, in Detroit, New Orleans, and in what historian Louis Ferleger describes as economic “dead zones” — places where people have simply given up and sunk into “involuntary idleness” — the pain is written on slumped bodies and faces that have become masks of despair. We are starting to break down.

When our alarm systems are set off too often, they start to malfunction, and we can end up in a state of hyper-vigilance, unable to properly assess the threats. It’s easy for the powerful to manipulate this tense condition and present an array of bogeymen to distract our attention, from immigrants to the unemployed, so that we focus our energy on the wrong enemy. Guns give a false sense of control, and hatred of those who do not look like us channels our impotent rage. Meanwhile, dietary supplements and prescription painkillers lure us into thinking that if we just find the right pill, we can shut off the sound of the sirens. Popular culture brings us movies with loud explosions that deafen us to what’s crashing all around us.

The 21st century, forged in the images of flames and bodies falling from the Twin Towers, has sputtered on with wars, financial ruin and crushing public policies that have left us ever more shaken, angry and afraid. At each crisis, people at the top have seized the opportunity to secure their positions and push the rest of us further down. They are not finished, not by a long shot.

Trauma is not just about experiencing wars and sexual violence, though there is plenty of that. Psychology researchers have discussed trauma as something intense that happens in your life that you can’t adequately respond to, and which causes you long-lasting negative effects. [..] trauma comes with a very high rate of interest. The children of traumatized people carry the legacy of pain forward in their brains and bodies, becoming more vulnerable to disease, mental breakdown, addiction, and violence. Psychiatrist Bessel van der Kolk, an expert on trauma, emphasizes that it’s not just personal.

Trauma occupies a space much bigger than our individual neurons: it’s political. If your parents lost their jobs, their home or their sense of security in the wake of the financial crisis, you will carry those wounds with you, even if conditions improve. Budget cuts to education and the social safety net produce trauma. Falling income produces trauma. Job insecurity produces trauma.

There’s much more at the link, and every word is worth reading. The mental consequences of the gutting of our societies by governments and the financial industry does not get nearly enough scrutiny. We act, or politicians and media do, as if millions of people losing their jobs, and over half of young people in certain nations never having had a chance of a job, is just a matter of numbers, of mere statistics.

And then all sorts of ‘experts’ claim it’s all just the price to pay for technological progress, that will make everything so much better for everyone some sunny day soon. But that sunny say will never come, the techno happy ideal version of the future has already died with the debt incurred to facilitate it. We need to take a step backwards, or we’ll continue to drive backwards. Or be driven, to be more precise, since we’ve handed over the steering wheel to people who have no intention of taking us where we want to, and should, go. They are only intent on taking us where they can squeeze us most.

Thing is, there’s precious little left to squeeze. And they know that much better than most of us do. That’s why it’s imperative that we should get rid of these clowns, or there’ll be a whole lot more trauma. We can organize our societies, and we can even organize ways to downscale them peacefully . But not with those at the helm who see us only as mere entities to draw blood from.

We need to be a whole lot more assertive about this; we shouldn’t want to be surrounded by traumatized friends and family members and neighbors There’s nothing good for us in that. It’ll be used against us in increased surveillance and clampdowns and all that comes with it.

We can have good jobs for everyone, all it takes is to have what we need, produced in our own communities and societies, instead of having it shipped over from China. It’s not rocket science. It’s just that there’s a certain segment in society, which unfortunately happens to be the most powerful one, that doesn’t want us to do that. They want more and bigger, not smaller and better.

Until we solve that issue, things will keep getting worse. And not just a little bit. We need to find leaders that actually represent us, our needs and desires and ideas, and we need to find ways to elect them. If we don’t, we face a very bleak future in which there won’t be much left for us to choose. Or enjoy. We live in a pivotal moment in time, but we don’t recognize it for what it is. We seem to think it’s all some minor hiccup. We are dead wrong.