Russell Lee “Yreka, California, seat of a county rich in mineral deposits” 1942

“..the “ECB is ready to do its part” and would “not hesitate to act” to crisis-proof the eurozone.” You don’t crisis-proof by creating a crisis.

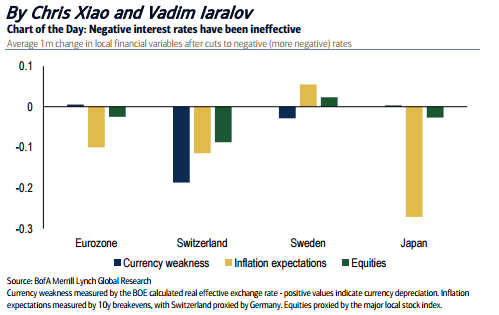

• Negative Interest Rates A ‘Dangerous Experiment’, Warns Morgan Stanley (MW)

After ECB chief Mario Draghi on Monday hinted more economic stimulus could be coming in March, expectations have risen that deposit rates will be pushed further into negative territory in a bid to fend off the impact from lower oil prices and world-wide economic jitters. While rate cuts usually are seen as a way to stimulate economic growth and weaken the currency, analysts at Morgan Stanley on Wednesday raised concerns that exactly the opposite would happen were the ECB to take rates even lower. Part of this is because investors already have rejigged their portfolios to account for the policy, they explained. Here’s the bank’s thinking:

“Further moves into negative rates will have much less of an impact on the euro, in our view, given that most of the portfolio adjustment is already complete. Rather, we are concerned it erodes bank profitability, creating other systemic risks,” they said in a note. “Could the most bullish ECB outcome be no rate cut?,” Morgan Stanley analysts asked. Calling negative interest rates a “dangerous experiment’, the economists argued such policy would erode bank profits 5%-10% and risk curbing lending across eurozone borders. European banks have already been off to a rough start to the year, down 21% on concerns about the fallout from negative rates, lackluster profits, tougher regulation and a slowdown in global growth. “The credit impulse has turned negative, new loan origination has slowed, and systemic stress in the financial system has risen,” the Morgan Stanley analysts said.

The comments come ahead of the ECB’s March 10 meeting, where investors increasingly are banking on some easing action. The central bank massively disappointed investors in December by introducing a smaller-than-expected rate cut and choosing not to pump more new money into the eurozone economy each month. But at the January meeting, Draghi opened the door for more easing if the economy and inflation showed no signs of improvement. Fast forward a few weeks, and markets have taken a serious beating as investors started to get really nervous about the impact of persistently low oil prices and a slowdown in the world economy.This didn’t go unnoticed by the ECB boss. At his quarterly hearing before the European Parliament on Monday he stressed the “ECB is ready to do its part” and would “not hesitate to act” to crisis-proof the eurozone.

Negative rates and the war on cash.

• Negative Interest Rates Are A ‘Gigantic Fiscal Failure’ (AEP)

[..] negative rates are a creeping threat to civil liberties since the only way to enforce such a regime over time is to abolish cash, for otherwise people will move their savings beyond reach. Mao Zedong briefly flirted with the idea during the Cultural Revolution in his bid to destroy every vestige of China’s ancient culture, but even he recoiled. The eurozone already plans to eliminate the €500 note – allegedly to hurt organized crime – and from there it is a slide down the scales to notes in daily use and then to curbs on quasi-money. It is a step to FDR’s gold embargo and Emergency Banking Act of 1933, when Americans were ordered to hand over their bullion or face 10 years in prison. One policymaker in Davos this year let slip that drastic action to scrap cash would be needed to fight a decade-long war against “secular stagnation” once rates test the limits of -1pc or -2pc.

The Bank of England’s Andrew Haldane floated the idea in a speech last September, suggesting that central banks may have to take radical action to circumvent the constraints of the “lower zero-bound”. Mr Haldane said NIRP reinforced by electronic money is a safer course than going down the “most slippery of slopes” by printing money to cover government spending. Here he is wrong. As Lord Turner argues, there is nothing inherently more slippery about direct monetary financing of fiscal stimulus than any other crisis measure. “Everything we are doing is risky,” he says. One can hardly claim that chronic use of QE to inflate asset prices and to stoke more credit is sound practice, or socially just. A monetary policy committee can calibrate what is judged to be the proper level of debt monetisation needed to avert deflation in exactly the same way as the MPC or the FOMC calibrate interest rates.

The money creation must be permanent to avoid “Ricardian Equivalence”, where people anticipate that more spending now merely mean more debt in the future. All debt accumulated by central banks under QE should be converted to perpetual non-interest bearing debt, and preferably burned on a pyre in public squares to the sound of trumpets to drive home the message that the debt has been eliminated forever. This will pre-empt the panic that might occur among investors and politicians should public debt ever cross some arbitrary totemic level. Any New Deal should be funded in the same way – partly or in whole – with the same vow that the debt will never be repaid. The money creation should continue at the therapeutic dose until the objective is achieved.

There is no technical objection to this form of “fiscal dominance”, as monetary guru Lars Svensson told the IMF forum. All that is missing is political will. Needless to say, the eurozone cannot venture down this path. Maastricht prohibits the ECB from overt financing of deficits and any such thinking in Frankfurt would lead to a court challenge and destroy German consent for monetary union. This augurs ill, because they will need it. Thankfully, those of us with our own currencies, central banks and fully sovereign governments always have the means to prevent the collapse of nominal GDP and to avert debt-deflation. We can run out of wit: we can never run out of monetary ammunition.

Japan exports to China down 18%. Japan imports also down 18%. World trade falls off a cliff.

More numbers:

January Exports from Asia’s Largest Economies

Singapore -9.9%

China -11.2%

Japan -12.9%

Taiwan -13%

Korea -18.5%

Indonesia -20.7%

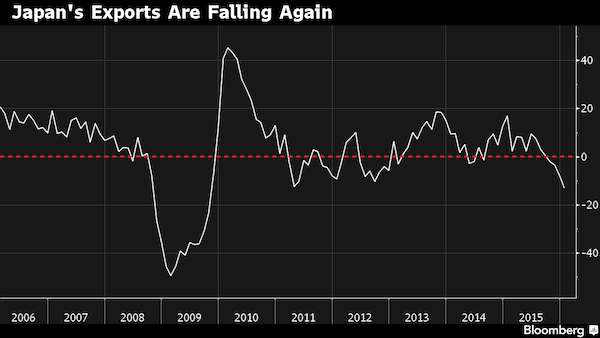

• Japan’s Exports Drop Most Since 2009 as Sales to China Fall (BBG)

Japan’s exports fell for a fourth consecutive month and dropped the most since 2009, underscoring continued weakness in an economy that contracted in the final months of 2015. Exports to China, Japan’s largest trading partner, were down almost 18%, driving an overall decline of nearly 13% in the value of overseas shipments in January from a year earlier. Imports dropped 18%, leaving a 645.9 billion yen ($5.7 billion) trade deficit, the Ministry of Finance said on Thursday. Falling exports compound poor sentiment in Japan, where wage gains have stagnated, consumer prices are barely rising and households are reluctant to spend. This year stocks have plunged and the yen has gained more than 5% against the dollar amid concerns over China’s slowdown and U.S. growth.

This adds to worries about the seesawing nature of Japan’s economy between modest growth and contraction. “The environment for Japanese exports is looking bad as Japanese companies shift production abroad, the global economy slows and the yen strengthens,” said Yasunari Ueno at Mizuho. “It’s becoming clear that that there is no driver to support Japan’s economy.” While exports to China typically ease in the weeks before lunar new year holidays, and the break came earlier this year, shipments to Japan’s neighbor have dropped for six straight months. Part of the weakness in the export figure is also because Japanese companies received lower prices for sales of steel and chemical products amid the general downturn in commodity and energy markets, said Atsushi Takeda at Itochu in Tokyo.

By volume, exports fell 9.1% in January from a year earlier, the biggest drop since February 2013, while import volumes declined 5.1%. Earlier this week, GDP data showed the Japanese economy shrank an annualized 1.4% in the three months ended Dec. 31. After that, Nomura cut its forecast for Japan’s fiscal 2016 GDP to 1% from a previous projection of 1.4%. The firm sees a high chance that the Bank of Japan will expand monetary stimulus at its March meeting if the market turmoil continues. Itochu’s Takeda doesn’t think it is likely that Japan will fall into a recession though he said “there are growing downside risks to the economy.” “Should gains in the yen and declines in stocks continue, they may take a toll on capital spending, exports and consumption,” he said.

A sign of Abe’s waning clout?!

• Japan Shelves Plan to Let Pension Fund Directly Invest in Stocks (WSJ)

Japan’s government has put off a plan to let its $1.1 trillion public pension fund buy and sell stocks directly, following criticism that the move could lead to excessive state influence on the market. The decision dashes the hopes of the Government Pension Investment Fund’s chief investment officer and some foreign money managers who believed that a direct role in the stock market could make the fund a more effective investor and improve corporate governance in Japan. A committee in Prime Minister Shinzo Abe’s ruling Liberal Democratic Party decided Tuesday to postpone consideration of the issue for three years, said LDP lawmaker Shigeyuki Goto, the committee’s secretary-general. “There won’t be any in-house stock investing, but it remains to be debated in the future,” Mr. Goto said. “The stock issue was the biggest sticking point for those involved in the discussions.”

The GPIF currently outsources decisions on its nearly ¥60 trillion ($520 billion) stock portfolio to more than a dozen outside asset managers. It handles domestic bonds in-house. Mr. Abe’s government has pushed to make the GPIF a more sophisticated investor in line with its overseas peers. The fund has moved more money into stocks and foreign bonds. Yet opposition from business and union leaders shows concern about allowing too much change at the GPIF, whose investment decisions ultimately affect how much Japan’s pensioners can receive. Recent market turmoil has made the fund a politically sensitive subject. The GPIF was criticized by opposition politicians after losing nearly ¥8 trillion in the third quarter of 2015 as global stock prices fell, and it is expected to post more losses in the coming months.

Mr. Abe was asked about the issue in parliament Monday and responded, “If expected returns aren’t met, that will of course impact pension payments.” Japan’s leading business group, Keidanren, as well as Rengo, an umbrella group for labor unions, both opposed letting the fund directly invest in stocks. They expressed concern about the GPIF being used to influence management at Japanese companies by using its voting rights as a shareholder. “It’s a very serious issue if the GPIF were to become a direct shareholder,” said Keidanren official Susumu Makihara at a meeting to debate the change in January. He said “a massive state organization would become a market player” under the proposal and it wasn’t clear how it would use its clout at companies.

“We tend to think that the Chinese government is likely to provide support if there is any sign of a crisis.” Well, they would like to, but can they?

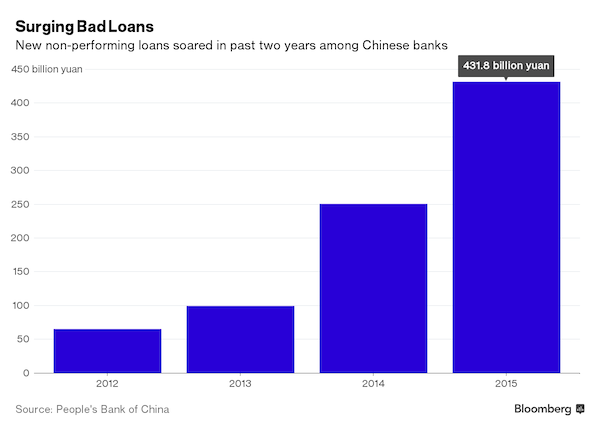

• China’s Banks May Be Getting Creative About Hiding Their Losses (BBG)

Chinese lenders are reacting to a regulatory crackdown on shadow financing by increasing activity in their more opaque receivables accounts, a practice Commerzbank estimates may result in losses of as much as 1 trillion yuan ($153 billion) over five years. Banks are increasingly using trusts or asset management plans to lend and recording them as funds to be received rather than as loans, which are subject to stricter regulatory oversight and capital limits. The German bank’s forecast is based on total outstanding receivables of around 11.5 trillion yuan. “Chinese banks haven’t provisioned for receivables and those are essentially riskier loans,” said Xuanlai He at Commerzbank. “The eventual losses will have significant impact on China’s economy because you could have contagion risk in banking sector.”

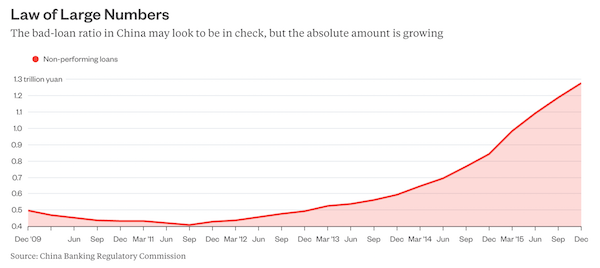

Official data show nonperforming loans at Chinese commercial banks jumped 51% last year to a decade-high of 1.27 trillion yuan amid a stock market rout and the worst economic growth in a quarter century. While Moody’s Investors Service doesn’t expect a banking crisis in China in the next 12 to 18 months, it said in a Jan. 26 note that it does see higher loan delinquencies, more defaults on corporate debt and some losses in wealth-management products. “The receivables portfolio in Chinese banks is opaque so we can’t make an assumption on the asset quality,” said Christine Kuo, analyst at Moody’s in Hong Kong. “Provisions for receivables are indeed very low compared to that for loans. We tend to think that the Chinese government is likely to provide support if there is any sign of a crisis.”

China CITIC Bank’s assets under receivables tripled to 900 billion yuan by June 30, from 300 billion yuan at the end of 2013, according to the bank’s financial statements. Concerns about Chinese banks’ creditworthiness are mounting with the cost of insuring Industrial & Commercial Bank of China’s debt against default reaching an all-time high of 199.5 basis points on Jan. 21. The bank’s 6% perpetual notes that count as Additional Tier 1 capital fell to a record low of 99.5 cents last Thursday. The securities traded at 102.5 cents on the dollar Wednesday. The yield spread on China CITIC’s $300 million 6% 2024 notes surged to a one-year high of 336 basis points over U.S. Treasuries Wednesday.

How afraid is Beijing of deflation? Apparently enough to blow another bubble.

• China Central Bank Takes Another Step To Guide Interest Rates Lower (BBG)

China’s central bank took another step to guide interest rates lower, offering to reduce the medium-term borrowing cost it charges lenders in the second such move this year. The People’s Bank of China has told banks it can provide cash through its Medium-term Lending Facility at 2.85% for six-month loans, down from 3%, according to a person with direct knowledge of the matter. The one-year borrowing rate would be eased to 3% from 3.25%, according to the person, who asked not to be identified because the plans aren’t public. Such a reduction would amount to a kind of monetary easing outside of traditional tools such as lowering benchmark lending or deposit rates or the reserve-requirement ratio for the biggest banks.

Overuse of RRR cuts may add too much pressure on short-term interest rates and would therefore be bad for stabilizing capital flows and the exchange rate, PBOC researcher Ma Jun said in a China Business News report published last month. “The PBOC is trying to find ways for monetary easing without making a high-profile interest-rate cut,” said Louis Kuijs at Oxford Economics in Hong Kong. “There’re likely to be more following steps in a similar direction, since a single move will not be enough to turn around the momentum of the economy.” China’s consumer price index climbed 1.8% in January from a year earlier, the National Bureau of Statistics said on Thursday. That was below the medium estimate of 1.9%.

The producer-price index fell 5.3%, extending declines to a record 47 months. “The data show that the economy is pretty weak,” said Larry Hu at Macquarie Securities in Hong Kong. The central bank is attempting to square the circle of supporting growth without using up limited monetary policy space or putting more downward pressure on the yuan, said Bloomberg Intelligence economist Tom Orlik. “That means more use of low-visibility instruments like the MLF to guide rates lower, rather than cuts in benchmark rates,” he said. “The trade off for low visibility, is the confidence boosting effect on the market is reduced.”

Very high.

• High Chance of China Hard Landing, Says Adviser to Japan’s Abe (BBG)

The chances are high China will have a hard landing, and it must undergo a severe adjustment period, an economic adviser to Japanese Prime Minister Shinzo Abe said. “There’s a high possibility of a hard landing in China” as its economy is oversupplied and adjusting demand and supply will cause a shock, Etsuro Honda said in an interview late Tuesday in Tokyo. The problem is more acute as “China can’t use monetary policy for quantitative easing as it has been used to stabilize its currency.” While officials from the IMF to the Bank of Japan have said China will avoid an economic crash, Honda’s comments echo concerns among investors about the direction of China’s economy.

A surprise currency devaluation, the slowest growth in a quarter century and perceived policy missteps are raising anxiety about the world’s second-largest economy. Unlike the idea of capital controls suggested by BOJ Governor Haruhiko Kuroda, Honda recommended China adopt a floating exchange rate system. Otherwise, China’s economy will suffer from a problem of oversupply for quite a while, he said. Honda, 61, is an academic and has been an adviser to Abe for the past three years. “I really don’t think that China’s economic fundamentals are good and it’s just real estate markets and stock markets that are panicking,” Honda said. “China has to go through massive structural reforms and its impact on other economies is quite large. That’s different from other nations.”

The yuan has turned toxic.

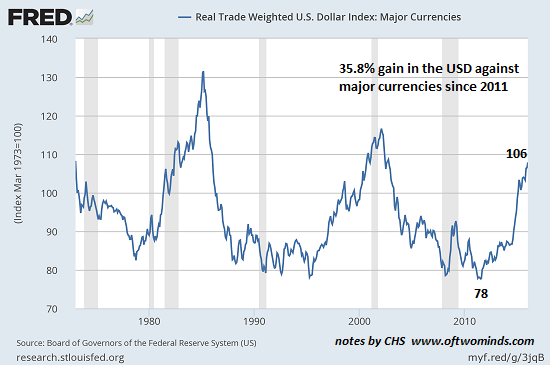

• Why the Chinese Yuan Will Lose 30% of its Value (CHS)

The U.S. dollar has gained over 35% against major currencies since 2011. China’s government has pegged its currency, the yuan (renminbi) to the USD for many years. Until mid-2005, the yuan was pegged at about 8.3 to the dollar. After numerous complaints that the yuan was being kept artificially low to boost Chinese exports to the U.S., the Chinese monetary authorities let the yuan appreciate from 8.3 to about 6.8 to the dollar in 2008. This peg held steady until mid-2010, at which point the yuan slowly strengthened to 6 in early 2014. From that high point, the yuan has depreciated moderately to around 6.5 to the USD. Interestingly, this is about the same level the yuan reached in 2011, when the USD struck its multiyear low.

Since 2011, the USD has gained (depending on which index or weighting you choose) between 25% and 35%. I think the chart above (trade-weighted USD against major currencies) is more accurate than the conventional DXY index. Due to the USD peg, the yuan has appreciated in lockstep with the U.S. dollar against other currencies. On the face of it, the yuan would need to devalue by 35% just to return to its pre-USD-strength level in 2011. This would imply an eventual return to the yuan’s old peg around 8.3–or perhaps as high as 8.7.

[..] Here’s the larger context of China’s debt/currency implosion. From roughly 1989 to 2014 -25 years- the “sure bet” in the global economy was to invest in China by moving production to China. This flood of capital into China only gained momentum as the yuan appreciated in value against the USD once Chinese authorities loosened the peg from 8.3 to 6.6 and then all the way down to 6 to the dollar. Every dollar transferred to China and converted to yuan gained as much as 25% over the years of yuan appreciation. Those hefty returns on cash sitting in yuan sparked a veritable tsunami of capital into China. Now that the tide of capital has reversed, nobody wants yuan: not foreign firms, not FX punters and not the Chinese holding massive quantities of depreciating yuan.

This is why “housewives” from China are buying homes in Vancouver B.C. for $3 million. That $3 million could fall to $2 million as the yuan devalues to the old peg around 8.3 to the USD. Who’s left who believes the easy money is to be made in China? Nobody. Anyone seeking high quality overseas production is moving factories to the U.S. for its appreciating dollar and cheap energy, or to Vietnam or other locales with low labor costs and depreciated currencies. For years, China bulls insisted China could crush the U.S. simply by selling a chunk of its $4 trillion foreign exchange reserves hoard of U.S. Treasuries.

Now that China has dumped over $700 billion of its reserves in a matter of months, this assertion has been revealed as false: the demand for USD is strong enough to absorb all of China’s selling and still push the USD higher. The stark truth is nobody wants yuan any more. Why buy something that is sure to lose value? the only question is how much value? The basic facts suggest a 30% loss and a return to the old peg of 8.3 is baked in. But that doesn’t mean the devaluation of the yuan has to stop at 8.3: just as the dollar’s recent strength is simply Stage One of a multi-stage liftoff, the yuan’s devaluation to 8 to the USD is only the first stage of a multi-year devaluation.

“China’s bad loans have grown 256% in six years even as their ratio to total lending dropped.”

• China’s $600 Billion Subprime Crisis Is Already Here (BBG)

Sorry, Kyle Bass, you’re a bit late to the game. The debt problem in China has already reached the proportions of the U.S. subprime mortgage debacle. Don’t worry, though: Chinese authorities are on the case – discussing reducing the required coverage for bad loans so that banks can keep booking profits and lending. Including “special-mention” loans, which are those showing signs of future repayment risk, the industry’s total troubled advances swelled to 4.2 trillion yuan ($645 billion) as of December, representing 5.46% of total lending. That number is already higher than the $600 billion total subprime mortgages in the U.S. as of 2006, just before that asset class toppled the world into the worst financial crisis since 1929.

The amount of loans classed as nonperforming at Chinese commercial banks jumped 51% from a year earlier to 1.27 trillion yuan by December, the highest level since June 2006, data from the China Banking Regulatory Commission showed on Monday. The ratio of soured debt climbed to 1.67% from 1.25%, while the industry’s bad-loan coverage ratio, a measure of its ability to absorb potential losses, weakened to 181% from more than 200% a year earlier. The news looks to have scared Chinese authorities into reacting. Note that they aren’t curbing the ability of Chinese banks to lend or asking them to write off bad credit. Instead they’re considering putting aside checks already in place that are aimed at ensuring the health of the financial system: by reducing the ratio of provisions that banks must set aside for bad debt, currently set at a minimum 150%.

Perhaps, they’re hoping banks will lend even more if they ease the rules. That’s one way to keep the ratio of nonperforming loans under control. As the denominator increases the ratio remains steady or even drops. The absolute number of bad loans, however, keeps swelling. Guess what? Banks are lending more. China’s new yuan loans jumped to a record 2.51 trillion yuan in January, the People’s Bank of China reported on Tuesday. Aggregate financing, the broadest measure of new credit, also rose to a record, at 3.42 trillion yuan. China’s bad loans have grown 256% in six years even as their ratio to total lending dropped. The true amount of debt that isn’t being repaid is open for debate.

One example of how the data can be distorted: Banks are making increasing use of their more opaque receivables accounts to mask loans and potential losses. Still, adding special-mention loans to those classed as nonperforming gives some measure of the size of the bad-debt problem. Unfortunately, the CBRC started to publish special-mention loan numbers only last year, so it’s hard to put them in historical context. The dynamic is clear. A splurge of new lending can help to dilute existing bad loans, but only at a cost. This is a game that can’t continue forever, particularly if credit is being foisted on to an already over-leveraged and slowing economy. At some point, the music will stop and there will have to be a reckoning. The longer China postpones that, the harder it will be.

Selling at a loss is often preferable over not selling at all, because of sunk costs or expected restart costs.

• Not Even a Wave of Oil Bankruptcies Will Shrink Crude Production (WSJ)

More than one-third of oil and natural-gas producers around the world are at risk of declaring bankruptcy this year, according to a new report from Deloitte. Oil prices have plunged from more than $100 a barrel in mid-2014 to about $30 a barrel today. Yet just 35 so-called exploration and production companies filed for bankruptcy between July 2014 and the end of last year, Deloitte says. Most producers managed to stay afloat by raising cash through capital markets, asset sales and spending cuts. Those options are running out.

The only moves left for most producers are dividend cuts and share buybacks, Deloitte says. The firm estimates that 175 companies, or 35% of the E&Ps listed world-wide, are in danger of declaring bankruptcy this year. The conundrum for many investors is that a slew of bankruptcies won’t necessarily shrink the global glut of crude. Companies need cash to repay their debts, so their existing wells are unlikely to stop operating throughout the bankruptcy process. In fact, those wells will probably be sold to better-financed buyers, who can afford to keep production going or even increase it.

“Given the cost of restarting production, many producers will continue to take the loss in the hope of a rebound in prices.” (h/t ZH)

• Less Than 4% Of World Oil Supply In The Red At $35/b (Platts)

Fears of a deepening non-OPEC supply crunch in response to the latest oil price slump may be overdone as many producers are absorbing short-term losses in the hope of a price rebound, according a new study by research group Wood Mackenzie. Citing up-to-date analysis of production data and cash costs from over 10,000 oil fields, Wood Mac said it believes 3.4 million b/d, or less than 4% of global oil supply, is unprofitable at oil prices below $35/b. Even the majority of US shale and tight oil, which has been under the spotlight due to higher-than-average production costs, only becomes cash negative at Brent prices “well-below” $30/b, according to the study.

For many producers, being cash negative is not enough of an incentive to shut down fields as restarting flow can be costly and some are able to store output with a view to selling it when prices recover. “Curtailed budgets have slowed investment, which will reduce future volumes, but there is little evidence of production shut-ins for economic reasons,” Wood Mac’s vice president of investment research Robert Plummer said in a note. “Given the cost of restarting production, many producers will continue to take the loss in the hope of a rebound in prices.” Even since oil prices began sliding in late 2014, there have been relatively few outright field production halts due to low prices, with only around 100,000 b/d shut in globally, according to the study.

Despite widespread fears of a major supply collapse, the US’ shale oil output since late 2014, sharp deflation in service sector costs and greater drilling efficiencies have seen shale oil output remain more resilient to lower prices than first thought. Wood Mac said falling production costs in the US over the last year have resulted in only 190,000 b/d being cash negative at a Brent price of $35/b. The latest study contrasts with a similar report from the research group a year ago when it estimated that up to 1.5 million b/d of output – focused in the US – was vulnerable to being shut in at $40/b Brent.

Count the failed states the west has created.

• Venezuela Lifts Gasoline Price by 6,200% and Devalues Currency by 37% (BBG)

Venezuela hiked gasoline prices for the first time in almost two decades and devalued its currency as President Nicolas Maduro attempts to address triple-digit inflation and the economy’s deepest recession in over a decade. The primary exchange rate used for essential imports, such as food and medicine, will weaken to 10 bolivars per dollar from 6.3, Maduro said in a televised address to the nation. The government will also eliminate an intermediate rate that last sold dollars for about 13 bolivars and improve an alternative “free-floating, complementary” market that trades around 203 bolivars per dollar. The devaluation will ease the drain on government coffers by giving state oil company Petroleos de Venezuela more bolivars for each dollar of oil revenue, while higher gasoline prices will reduce expenditure on subsidies.

At the same time, the devaluation will probably force the government to raise the cost of staple foods such as rice and bread that most of the country now depends on to eat. “Faced with a criminal, chaotic inflation induced a long time ago, we must act with the power of the state to control and regulate markets,” Maduro said below a portrait of South American independence leader Simon Bolivar. While Maduro’s measures may fall short of fully addressing Venezuela’s ailing economy, the announcements may “bring some relief that it’s something after months (years) of nothing,” Sibohan Morden at Nomura Securities said in a note to clients published prior to Maduro’s speech. “It is also important that Chavismo shifts toward pragmatism and finally realizes that the Bolivarian revolution has failed.”

Something had to change after the bolivar lost 98% of its value on the black market since Maduro took office in 2013. The government was hemorrhaging funds as it struggled to meet international debt obligations and maintain the supply of essential items amid the collapse in oil prices. By long subsidizing the cost of fuel, the government has ensured that Venezuelans enjoy the cheapest gasoline in the world. Gasoline prices on Thursday will leap more than 60-fold to 6 bolivars a liter from 9.7 centavos. That’s equal to about 11 U.S. cents per gallon using the weakest legal exchange rate of 202.94 bolivars per dollar, up from about 0.2 U.S. cents per gallon. The price of 91-octane gasoline will increase to 1 bolivar a liter from 7 centavos. Even after these increases, Venezuela still has the lowest gasoline prices in the world.

Then again, they’re not separate entities.

• The Real Crisis is for Bank Bonds, Not Banks (WSJ)

The fall from grace has been swift and hard. Buying high-yielding subordinated bank bonds that count toward Tier 1 capital was a hot trade in a world where investors were scrambling for yield. This is a case where markets have been their own worst enemy. European banks have been at the center of the recent market storm, with Deutsche Bank’s bonds particularly in focus. The move in prices has been big, even with a bounce in the last couple of days. Bank of America Merrill Lynch’s index of contingent capital bonds—popularly known as CoCos—has dropped 7.6% this year. Europe clearly has unresolved issues to address in its fragmented banking system. But this is hardly news. The issue lies more with the securities and the investors that hold them than the balance sheets of the banks that issued them.

The big risk that investors have woken up to isn’t that these bonds can be bailed-in if a bank hits trouble—it is that interest payments on them can be skipped under certain circumstances. In turn, falling prices have raised concerns that banks won’t exercise their option to redeem them at the first opportunity, requiring a further repricing downwards. That has upset the apple cart of what had become a so-called crowded trade—one that caught many investors’ imagination as central banks poured liquidity into markets. During the good times these instruments looked like more lucrative versions of safer, lower-yielding senior debt. But now their equity-like features have come to the fore. That is a big shift for holders to take on board and one that is unlikely to be reversed quickly.

In the meantime, it isn’t clear that there is a natural buyer for these securities. For those holders who wish to sell, that poses an immediate problem: there is no way out, and the turmoil may not be over yet. Longer term, the economics of these hybrid structures may depend on buyers seeing them as safe debt while issuers consider them as quasi-equity. If they are priced more like equity, they may not be so attractive to issuers. Regulators may have helped create an instrument that is only truly viable in fair-weather conditions.

Kashkari seems to go mostly for the shock effect, and turns opaque as soon as he’s called on his words.

• Fed’s Kashkari: 25% Capital Requirement May Be Right for Banks (WSJ)

Q: You talk about higher capital requirements. How high should they be?

MR. KASHKARI: I don’t have a number in my head. I’ve seen some proposals for a 25% capital requirement. So leverage ratios, effectively, just to keep it simple, you know, 4:1. You know, I think that’s a place we could discuss. I don’t have that – I don’t have a magic number yet. And also, importantly, we’re not suggesting that we at the Minneapolis Fed necessarily have all the answers. What we’re trying to do is launch a process where we can bring all of these ideas out from across the country and give them the serious analysis and consideration that I feel like they deserve.

Because when I look at the Dodd-Frank Act – and I was – I had already left government by then – but from the outside, it appeared that the more transformational solutions were just taken off the table – like, OK, that’s too bold; let’s keep the financial system roughly in its current form, and let’s make it safer and stronger. And that’s not an irrational conclusion for legislators to have drawn at that time, because we were – the recovery was still so unclear. But here we are, six years later, the economy is a lot stronger than it was coming out of the crisis. In my judgment, we still have the problem of too-big-to-fail banks, and now feels like the right time to look at this again.

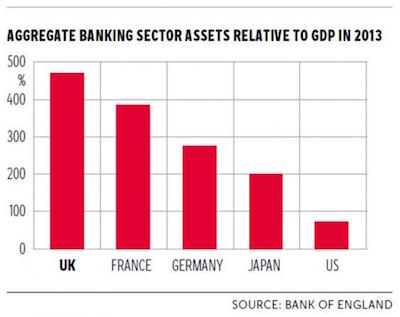

That second graphic here is very scary. The UK banking sector is 480% of GDP. With a reserve requirement of 3%, tops.

• Banking Reform Is More Complex Than It Needs To Be (Chu)

“All that is necessary for the triumph of evil is that good men do nothing.” There’s some uncertainty over whether Edmund Burke actually made this observation. But, regardless of its provenance, the wisdom merits a tweak for our times. Today the necessary condition for vested interests to prevail over the public interest is that good men don’t understand what the hell is going on. Something has happened in the UK banking reform debate. Sir John Vickers, a central figure in the Government’s post-crisis financial overhaul, has questioned whether the Bank of England’s latest proposals to shore up the sector go far enough. Yet this debate is perfectly impenetrable to the non-expert. Read the exchanges between Sir John and the Bank and you will soon slip into a numbing bath of acronyms and jargon from which you will very likely not resurface any the wiser.

G-SIBs, D-SIBs, SRBs, RWAs, Tier 1, Basel III, CoCos … These names will float across your vision, like the members of the world’s most boring rap group. You will read about the appropriate threshold for the activation of “a risk-weighted SRB rate of 3%” and the relevance of “counter-cyclical buffers” and, you will, quite understandably, conclude there is something better you could be doing with your time. But ignore the detail. This complexity is the outcome of years, perhaps even decades, of horse trading between bank lobbyists, regulators and politicians from all around the world. As a non-expert you’re not supposed to be able to follow it. It hasn’t been designed to confuse ordinary people. That’s just a happy side-effect (as far as the banks are concerned).

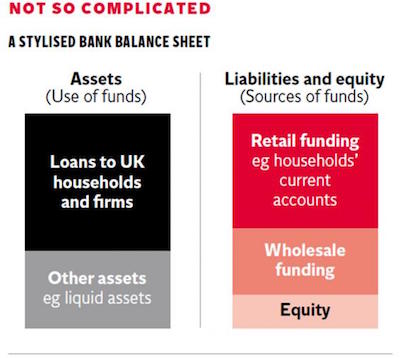

So clear it from your mind. Focus, instead, on the essentials. Banks are not as complex as they are made out to be by bankers and regulators. A bank has a balance sheet just like any other business. On the asset side of the balance sheet are its loans to customers. On the liabilities side are the current account deposits of customers, plus borrowings from the wholesale capital markets and, most importantly of all, the equity of its investors. The liabilities of a bank fund its assets. Equity is what gets eaten into first when a bank makes losses. If the equity is all used up, the bank is bust. And as we saw in 2008, that can mean taxpayers forced to step in to stop these institutions collapsing and taking the entire economy down with them. That’s why regulators must make sure banks have a sufficiently large tranche of equity financing on their balance sheets.

In support of his case Sir John has chosen to cite the analysis of the respected independent expert in finance, Anat Admati of Stanford University. This is interesting. Ms Admati has recommended that a private bank’s equity cushion should be equivalent to between 20 to 30% of its assets. So what would you guess is the current level of equity for banks being targeted by the Bank of England? 15%? 10%? Try 3%. Or 4% at most. And even Sir John’s report, despite his complaints today, only wanted banks to hold equity worth a maximum of around 4% of assets. Consider what this means: it implies that a mere 3 or 4% fall in the value of a bank’s assets would bankrupt it – and government ministers and regulators would, once again, need to consider whether to step in. To state what should be obvious: that’s not very much. And that simple ratio – known as the “leverage ratio” – should be focus of debate.

Bye bye banking union. Renzi’s clear: clean up Deutsche first.

• Italy Would Veto Any Cap On Banks’ Government Debt Holding (Reuters)

Italy would oppose capping banks’ holdings of domestic sovereign bonds, Prime Minister Matteo Renzi said on Wednesday, throwing down the gauntlet to European policymakers who are considering a cap to strengthen the euro zone banking system. The European Commission plans to review the current rules on banks’ exposure to their home countries’ debt as a way to reduce the risk that wobbly public finances might pose to a national financial system. “We will veto any attempt to put a ceiling on government bonds in banks’ portfolios,” Renzi told the upper house Senate. The European Central Bank’s chief supervisor has proposed a limit on national sovereign debt holdings at 25% of a bank’s equity, but the ECB vice president favours a risk-weighted approach.

Bond markets in Italy and Spain would likely see the biggest impact among major euro zone countries if a cap were imposed, as banks in both countries hold piles of state-issued bonds. Around €405 billion ($451 billion), or 21.6% of all Italian government debt, is owned by its banks. The 41-year-old prime minister said Italy would take a firm line on the issue, adding: “Rather than worrying about government bonds in the banks we should be strong enough to say that (banks elsewhere in Europe) hold too many toxic assets.” Renzi, who has recently taken several swipes at Germany’s banking sector, mentioned the case of Deutsche Bank, which said last week it would buy back more than $5 billion in senior debt.

Plus ça change..

• German Central Bank Chief On Collision Course With Draghi Over QE (T.)

Germany’s powerful central bank chief has said quantitative easing is no longer appropriate for Europe, putting Berlin on a collision course with the ECB over expanding stimulus measures to revive the single currency area. Jens Weidmann, head of the Bundesbank and a member of the ECB’s governing council, said QE was “no longer necessary” for the eurozone, despite the widespread expectation that more stimulus will be announced as early as next month. However, Mr Weidmann defended the ECB’s bond-buying scheme – launched in March last year – at a hearing at the German Constitutional Court on Tuesday, arguing that it did not contravene the principles of the German constitution. But his resistance to expanding QE suggests the ECB’s hawkish members are hardening in their stance against expanding the stimulus programme from its current €60bn a month.

Crucially, Mr Weidmann will not be able to take part in the March vote under the ECB’s rotating voting rules. The Bundesbank chief’s position is in stark opposition to that of ECB president Mario Draghi, who has repeated the central bank’s willingness to “do its part” to revive inflation and growth in the bloc as turmoil has engulfed global markets this year. Draghi’s failure to ramp up QE in December sent markets into a tailspin and has helped European equities plunge by as much 13pc this year. Mr Weidmann was speaking as a witness in front of Germany’s powerful constitutional court in Karlsruhe on Tuesday. The court – which has the power to strike down EU laws it deems incompatible with Germany’s supreme federal constitutional law – was meeting to consider the legality of the ECB’s landmark Outright Monetary Transactions scheme (OMT), first announced in 2012.

Mr Weidmann has been a vociferous opponent of OMT, which acts as a financial backstop for the euro’s distressed debtors but has never been deployed, arguing that it represents the illegal financing of government debt. But he refrained from repeating his criticisms on Tuesday, saying only that the QE measures were less “problematic” than the more ambitious OMT. ECB board member Yves Mersch said OMT was devised to “confront an extraordinary crisis situation” when the future of the eurozone was in doubt. “This crisis situation was characterised by massive distortions of the government bond market that developed their own momentum,” said Mr Mersch. “This in turn led to a disruption of the monetary policy transmission mechanism, which posed a threat for price stability.” The German court is not expected to make a formal ruling until later in the year.

Ukraine has been turned into a failed state. Even if Russia wins in court, what are the odds it will ever be paid?

• Russia Sues Ukraine in London High Court Over $3 Billion Default (BBG)

Russia said it filed a lawsuit against Ukraine in the High Court in London after the government in Kiev defaulted on $3 billion in bonds. Cleary Gottlieb Steen & Hamilton was hired to represent the government in Moscow in a case that will seek to recover the principal in full, $75 million of unpaid interest and legal fees, Russian Finance Minister Anton Siluanov said on Wednesday. The filing comes after Germany attempted to mediate talks between the two former-Soviet neighbors to try to reach an out-of-court settlement. “I expect that the process in the English court will be open and transparent,” Siluanov said. “This lawsuit was filed after numerous futile attempts to encourage Ukraine to enter into good faith negotiations to restructure the debt.”

The case brings to a head a standoff between the two countries after Russia declined to take part in a $15 billion restructuring that Ukraine negotiated with its other Eurobond holders last year. Siluanov reiterated that Russia was demanding better treatment than private creditors, which include Franklin Templeton, and wants to be treated as a sovereign debtor. Russia has to pursue legal action against Ukraine in the U.K. because the bond was structured under English Law. President Vladimir Putin bought the debt in December 2013 to bail out his former Ukrainian counterpart and ally, Viktor Yanukovych, just months before he was toppled and Russia annexed Crimea. The notes were priced to yield 5%, less than half the rate on Ukrainian debt at the time.

The filing poses another obstacle to Ukraine’s government as it faces political infighting that’s threatening to sink the ruling coalition and further stall a $17.5 billion IMF lifeline that the country needs to stay afloat. The IMF warned last week the aid package risked failure if the government doesn’t kick start an overhaul of its economy.

The smugglers are by now better funded than the military.

• WikiLeaks Releases Classified Data On EU Military Op Against Refugee Flows (RT)

WikiLeaks has released a classified report detailing the EU’s military operations against refugee flows in Europe. It also outlines a plan to develop a “reliable” government in Libya which will, in turn, allow EU operations to expand in the area. The leaked report, dated January 29, 2016, is written by the operation’s commander, Rear Admiral Enrico Credendino of the Italian Navy, for the EU Military Committee and the Political and Security Committee of the EU. The document gives refugee flow statistics and details of performed and planned operation phases of the joint EU forces operating in the Mediterranean. The report also places pressure on the responsible EU bodies to help speed up the process of forming a “reliable” government in Libya, which is expected to invite EU forces to operate within its territorial waters, and later give permission to extend EU military operations onshore.

“Through the capability and capacity building of the Libyan Navy and Coastguard we will be able to give the Libyan authorities something in exchange for their cooperation in tackling the irregular migration issue. This collaboration could represent one of the elements of the EU comprehensive approach to help secure their invitation to operate inside their territory during Phase 2 activities,” the document states. Admiral Credendino writes that the task force is ready to proceed to phase 2B despite political and legal challenges: “…We are ready to move to phase 2B (Territorial Waters) where we can make a more significant impact on the smuggler and traffickers business model.” “However, in order to move into the following phases we need to have a government of national accord with which to engage.” “A suitable legal finish is absolutely fundamental to the transition to phase 2B (Territorial Waters) as without this, we cannot be effective.”

“Central to this and to the whole transition to phase 2B, is an agreement with the Libyan authorities. Ultimately they have the casting vote on the legal finish which will in turn drive the transition to phase 2B and the appetite for Member States to provide assets. As a European Union, we must therefore apply diplomatic pressure appropriately to deliver the correct outcome,” the document states. The leak comes less than five months after it was reported that Operation Sophia would consist of 22 member states and 1,300 personnel which would board and seize suspect vessels in the Mediterranean. However, the document notes that when the operation progresses into phases 2B and 3, “the smugglers will again most likely adapt quickly to the changing situation. The primary concern for smugglers will likely remain to avoid being apprehended so they can continue their illegal activities.”

The operation’s objective is primarily to disrupt smuggling routes by human traffickers, rather than to stop migration flows, according to the European Union Institute for Security Studies, which wrote in a document that the operation began on July 27, 2015. The Institute noted, however, that there is a “real uncertainty on whether the operation will ever be able – for either legal or political reasons – to get to the core of its mandate, i.e. neutralising the smuggling networks through deterrence or open coercion, both off the Libyan coast and onshore.” It went on to note that regardless of the operation’s support for EU member states, only “a very few” are likely to “have the skills and experience for such missions, let alone the will.” It also stressed that the operation cannot be a “solution” to the refugee crisis, and that “no one in Brussels is contending that it could.”

They can talk for years and still won’t agree. Sticks and carrots galore, but those don’t keep the EU together.

• European States Deeply Divided On Refugee Crisis Ahead Of Summit (Guardian)

Europe’s deep divide over immigration is to be laid bare at an EU summit in Brussels on Thursday, with German chancellor Angela Merkel struggling to salvage her open-door policy while a growing number of countries move to seal borders to newcomers along the Balkan routes. A dinner debate on the migration crisis on Thursday evening will do little to resolve the differences, senior EU officials predict. Donald Tusk, the president of the European council, has avoided putting any new decisions on the agenda in an attempt to avoid fresh arguments. The leaders of four anti-immigration eastern European countries met in Prague on Monday and demanded alternative EU policies by next month.

Their plan amounts to exporting Hungary’s zero-immigration razor-wire model to the Balkans, sealing Macedonia’s border with northern Greece, and bottling up the vast numbers of refugees in Greece unless they are deported back to Turkey. Merkel, by contrast, is to lead a rival meeting of leaders of 10 countries on Thursday in an attempt to invigorate a pact with Turkey, which is aimed at trading money and refugee quotas for Ankara’s efforts to minimise the numbers crossing the Aegean to Greece. Merkel’s plan hinges on EU countries volunteering to take in quotas of refugees directly from Turkey. But even among her allies – a so-called coalition of the willing – support for the policy is fading. Austria, which is hosting Thursday’s meeting at its embassy in Brussels, announced much stiffer national border controls this week.

It has also told Brussels and Balkan governments that it could close its borders within weeks. France, also part of the coalition, announced that it would not participate in any new quotas system. “You can’t have 20 [EU] countries refusing to take in refugees,” said a European commissioner. But senior officials in Brussels admit that there is now a solid majority of EU states opposing Merkel. In a pre-summit statement to parliament in Berlin on Wednesday, Merkel stoutly defended the policies that are under fire at home and across Europe. Despite the problems, she said, 90% of Germans continued to support taking in people fleeing war, terror and persecution. “I think that’s wonderful,” Merkel said.

Her speech dwelt overwhelmingly on the faltering pact with Turkey, struck in November. Ahmet Davutoglu, the Turkish prime minister, is to attend the mini-summit in Brussels. The issue at the EU summit, Merkel said, will be whether to press ahead with the Turkey pact or whether to concentrate on the closed scenario of more fences and quarantining Greece.

Home › Forums › Debt Rattle February 18 2016