Fred Stein Police car, New York 1942

As Trump sinks into opioids and nuke threats (talking to Kim in his own language, and no, Trump does not like the Korea thing), and Google sinks into its self-dug moral morass, let’s not forget this one thing: we would not have what poses as an economy if not for central banks buying anything not bolted down. And they cannot keep doing that. And what then?

“At current government debt net issuance rates and announced QE levels, the ECB will have been responsible for financing 100% of Italy’s deficits from 2014 to 2019”

• The Only Thing Keeping Italy’s Debt Alive is the ECB (DQ)

New statistical data from the investment bank Jefferies LLC has revealed a startling new trend that could have major implications for Europe’s economic future: Italian banks have begun dumping unprecedented volumes of Italian sovereign debt. Holdings of government debt by Italian financial institutions slumped by a record €20 billion in June – almost 10% of the total – after €9.4 billion of sales in May. As the FT reports, the selling by Italian banks is the most emphatic example yet of a broader trend: banks sold €46 billion of government paper in June across Europe, taking the total reduction since the start of this year to €257 billion. The banks’ mass sell-off is probably being driven by two main factors: first, as an attempt to preempt a pending Basel III reform package that could eliminate the equity capital privilege for EU government bonds and second, to position themselves for an anticipated autumn announcement from the ECB that it will begin tightening monetary policy.

“Maybe we are seeing an indication of Italian banks catching up with what their counterparts in Spain have known for a long time – that sovereign debt is not the place to be in a world of rising interest rates, said Jefferies’ senior European economist, Marchel Alexandrovich. But then: who’s buying it? The answer, in the case of Italy, is the ECB and its Italian branch office, the Bank of Italy, where Italian bank deposits rose by €22 billion in June and €50 billion since the start of 2017. The ECB “overbought” Italian government debt in July with purchases of €9.6 billion — its highest monthly quota since quantitative easing began. As Italian banks offload their holdings, the ECB, with Italian native and former Bank of Italy governor Mario Draghi at the helm, is picking up the slack.

In doing so, the central bank surpassed its own capital key rules by which member state debt is bought in proportion to the size of each country’s economy. By contrast, the ECB’s German Bund purchases slipped below its capital key rules for the fourth month in a row, which further depressed the spread between Italian and German 10-year debt to 152 basis points, its lowest level of the year. This spread is artificial, derived from the ECB’s binge buying of European sovereign bonds, particularly those belonging to countries on the periphery. A report published in May by Astellon Capital revealed that since 2008, 88% of Italy’s government debt net issuance was acquired by the ECB and Italian Banks. At current government debt net issuance rates and announced QE levels, the ECB will have been responsible for financing 100% of Italy’s deficits from 2014 to 2019. That was before taking into account the current sell-down of Italian bonds by Italian banks.

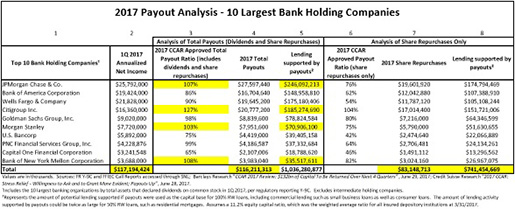

As central banks buy 100% of a country’s new debt, US banks pay out more than 100% of earnings, and “share buybacks represent 72% of the total payouts for the 10 largest bank holding companies”. What better way to characterize a non-functioning economy?

• Federal Bank Regulator Drops a Bombshell as Corporate Media Snoozes (Martens)

Last Monday, Thomas Hoenig, the Vice Chairman of the Federal Deposit Insurance Corporation (FDIC), sent a stunning letter to the Chair and Ranking Member of the U.S. Senate Banking Committee. The letter contained information that should have become front page news at every business wire service and the leading business newspapers. But with the exception of Reuters, major corporate media like the Wall Street Journal, Bloomberg News, the Business section of the New York Times and Washington Post ignored the bombshell story, according to our search at Google News. What the fearless Hoenig told the Senate Banking Committee was effectively this: the biggest Wall Street banks have been lying to the American people that overly stringent capital rules by their regulators are constraining their ability to lend to consumers and businesses.

What’s really behind their inability to make more loans is the documented fact that the 10 largest banks in the country “will distribute, in aggregate, 99% of their net income on an annualized basis,” by paying out dividends to shareholders and buying back excessive amounts of their own stock. Hoenig writes that the banks are starving the U.S. economy through these practices and if “the 10 largest U.S. Bank Holding Companies were to retain a greater share of their earnings earmarked for dividends and share buybacks in 2017 they would be able to increase loans by more than $1 trillion, which is greater than 5% of annual U.S. GDP.” Backing up his assertions, Hoenig provided a chart showing payouts on a bank-by-bank basis. Highlighted in yellow on Hoenig’s chart is the fact that four of the big Wall Street banks are set to pay out more than 100% of earnings: Citigroup 127%; Bank of New York Mellon 108%; JPMorgan Chase 107% and Morgan Stanley 103%.

What’s motivating this payout binge at the banks? Hoenig doesn’t offer an opinion in his letter but he does state that share buybacks represent 72% of the total payouts for the 10 largest bank holding companies. What share buybacks do for top management at these banks is to make the share price of their bank’s stock look far better than it otherwise would while making themselves rich on their stock options. If just the share buybacks (forgetting about the dividend payouts) were retained by the banks instead of being paid out, the banks could “increase small business loans by three quarters of a trillion dollars or mortgage loans by almost one and a half trillion dollars.” Hoenig also urged in his letter that there be a “substantive public debate” on what the biggest banks are doing with their capital rather than allowing this “critical” issue to be “discussed in sound bites.” Most corporate media responded to this appeal by ignoring Hoenig’s letter altogether.

They all want to show nice numbers at the Congress. Shadow banks lend them the money to do it. In exchange for power.

• Officials Spend Big In The Run Up To China’s Communist Party Congress (BBG)

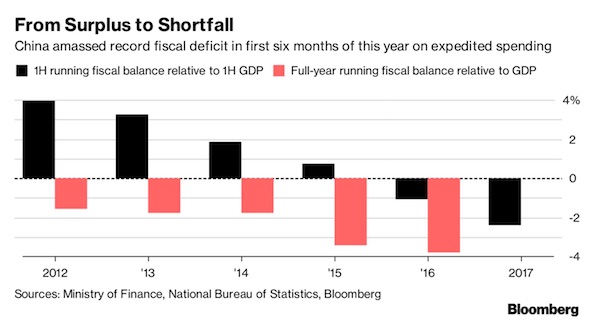

In the run up to China’s blockbuster Communist Party congress later this year, officials have spent big to ensure the economy is humming along nicely when the conclave begins. It’s after that that things get interesting. With the central government’s deficit limit capped at 3%, officials usually turn on the taps around November and December, once they know they’ll have raised enough to fund a late-year splurge. Not this time. A push to smooth out spending means the fiscal pump is unlikely to go into high gear at year end, which is when economists see growth moderating toward the government’s baseline of 6.5%. While policy makers have quasi-fiscal options up their sleeve – like accelerating infrastructure project approvals or ratcheting up lending via policy banks – efforts to curb profligate local governments and limit debt may restrain those channels too.

“It’s China’s political-business cycle: this year is very important for the political transition, so they front-loaded fiscal spending to ensure a stable economic backdrop,” Larry Hu, head of China economics at Macquarie in Hong Kong. “China’s economy has a fiscal system and a shadow fiscal system. If growth really slows to threaten the target, then we’re going to see spending.” The question is, how much. China ran a fiscal deficit of 918 billion yuan ($137 billion) in the first half, or more than 2% of economic output during the period, Bloomberg calculations show. That’s a record both by value and share. The spending fueled better-than-expected economic growth of 6.9% in the first six months, and infrastructure investment surging at over 20%.

China International Capital Corp. analysts led by Liu Liu say the budgeted deficit will be 1.46 trillion yuan in the second half, versus 2.46 trillion yuan in the same period last year. The world’s second-largest economy still depends on government spending at all levels, as construction of things like roads and railways can be a key buffer when private investors start pulling back or, as now, political sensitivities make robust growth especially important. But those priorities are now clashing with the need to clamp down on indebtedness at lower levels of government, and the desire to avoid a year-end spending glut. In the past, officials have been able to use off-balance sheet spending, such as policy bank loans and funds raised through local government financing vehicles, to keep their deep pockets open.

It’s starting to feel increasingly like a big fat Ponzi.

• China Is Taking on the ‘Original Sin’ of Its Mountain of Debt (BBG)

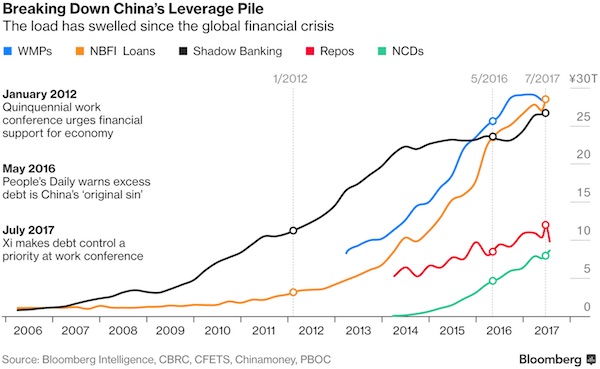

China’s much-vaunted campaign to tackle its leverage problem has captured headlines this year. But to understand why they’re taking on the challenge – and the threat it could pose to the world’s second-largest economy – you need to dig into the mountain. Characterized in state media as the “original sin” of China’s financial system, leverage has swelled over the past decade – partly because policy makers were trying to cushion a slowdown in growth from the old normal of 10% plus. What’s fueled the leverage has been a rapid expansion in household and corporate wealth looking for higher returns in a system where bank interest rates have been held down. The unprecedented stimulus unleashed since 2008 effectively brought to life the “monster” China’s leadership is now trying to tackle, says Andrew Collier at Orient Capital Research in Hong Kong and author of “Shadow Banking and the Rise of Capitalism in China.”

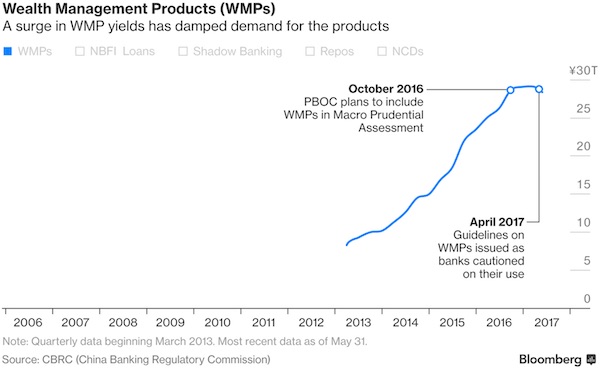

Implicit backing from the central government meant borrowers had free license to take on debt. “You basically have anybody selling anything they want as they think they can’t lose,” Collier said. Deleveraging – championed by President Xi Jinping and the Communist Party Politburo in April – hasn’t truly begun, as “they’re trying to forestall the pain as long as possible,” he said. The equivalent of trillions of dollars are now held in all manner of assets in China, from high-yielding wealth management products to so-called entrusted investments. Taking the heftiest piece of the leverage mountain first, wealth management products had a precipitous rise over the past several years.

A way for borrowers who have trouble getting traditional bank loans to win funding, WMPs have grown in popularity as they typically offer savers much higher yields than banks offer on deposits. WMPs are also a hit because they give lenders a way to keep loans off of their balance sheets, and to skirt regulatory requirements when channeling funds to borrowers, according to Raymond Yeung at Australia & New Zealand Banking in Hong Kong. The regulatory crackdown this year — mostly in the form of more stringent guidelines on use of financial products — has seen the amount of WMPs outstanding taper off from a peak in April, while yields on them have surged as providers competed for funds. In July, the bank watchdog is said to have told some lenders to cut the rates they offered on the products.

“It’s not really a bear call on the S&P 500. It’s more of a bull call on volatility..”

• Jeff Gundlach Predicts He Will Make 400% On Bet Against Stock Market (CNBC)

DoubleLine CEO Jeffery Gundlach expects his bet for a decline in the S&P 500 will return 400%. “I’ll be disappointed if we don’t make 400% on the puts, and we don’t even need a big market decline for that to happen,” Gundlach said Tuesday on CNBC’s “Halftime Report.” He said that in his firm’s analysis, volatility is so low that it can make a big return by buying put options — bets for a decline — on the S&P 500 for December. “It’s not really a bear call on the S&P 500. It’s more of a bull call on volatility,” he said. In its slow grind higher, the S&P 500 has only closed more than 1% higher or lower on four trading days this year.

As a result of the muted market performance, the CBOE Volatility Index (.VIX), widely considered the best gauge of fear in the market, has persistently held near historical lows around 10 or below this year and hit an all-time low of 8.84 on July 26. The VIX was near 10.1 midday Tuesday as the S&P 500 edged up to a record high. “I think going long the VIX is really sort of free money at a 9.80 VIX level today,” Gundlach said. “I believe the market will drop 3% at a minimum sometime between now and December. And when it does I don’t think the VIX will be at 10.” Gundlach reiterated his expectations for a snap higher in the VIX once volatility picks up, since hedge funds have piled heavily into bets that volatility will remain low.

OK, got it. Now what?

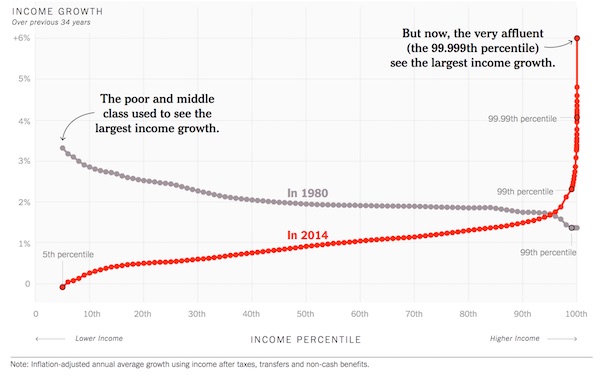

• Our Broken Economy, in One Simple Chart (NYT)

Many Americans can’t remember anything other than an economy with skyrocketing inequality, in which living standards for most Americans are stagnating and the rich are pulling away. It feels inevitable. But it’s not. A well-known team of inequality researchers — Thomas Piketty, Emmanuel Saez and Gabriel Zucman — has been getting some attention recently for a chart it produced. It shows the change in income between 1980 and 2014 for every point on the distribution, and it neatly summarizes the recent soaring of inequality.= The line on the chart (which we have recreated as the red line above) resembles a classic hockey-stick graph. It’s mostly flat and close to zero, before spiking upward at the end. That spike shows that the very affluent, and only the very affluent, have received significant raises in recent decades.

This line captures the rise in inequality better than any other chart or simple summary that I’ve seen. So I went to the economists with a request: Could they produce versions of their chart for years before 1980, to capture the income trends following World War II. You are looking at the result here. The message is straightforward. Only a few decades ago, the middle class and the poor weren’t just receiving healthy raises. Their take-home pay was rising even more rapidly, in%age terms, than the pay of the rich. The post-inflation, after-tax raises that were typical for the middle class during the pre-1980 period — about 2% a year — translate into rapid gains in living standards. At that rate, a household’s income almost doubles every 34 years. (The economists used 34-year windows to stay consistent with their original chart, which covered 1980 through 2014.)

In recent decades, by contrast, only very affluent families — those in roughly the top 1/40th of the income distribution — have received such large raises. Yes, the upper-middle class has done better than the middle class or the poor, but the huge gaps are between the super-rich and everyone else. The basic problem is that most families used to receive something approaching their fair share of economic growth, and they don’t anymore.

Nice try, Ann. But people have no political power left. Just look at the mess that all parties are in, in both the UK and US. So are you going to break the power of finance?

• The Economic Crash, Ten Years On (Pettifor)

Challenging and dismantling gargantuan financial markets that operate beyond democratic regulatory oversight will not be easy, but it is long overdue. Some believe that the management of financial markets by governments will never be restored. I do not agree. Because of global imbalances, economic and financial tensions could lead to the onset of wars. These could dismantle global financial markets just as the two world wars did. There is a more peaceful way of restoring finance to the role of servant to, and not master of, economies and regions. For that to happen the public must realise that citizens can exercise economic power over global financial markets. The global ‘House of Finance’ is almost entirely dependent, and indeed largely parasitic, on the public sector. In other words, private finance is largely dependent for its capital gains on taxpayers like you and me.

Commercial banks do not need savings or tax revenues to lend. All they need is to provide finance to viable projects that will generate employment and income in the future – which will repay the loans. The most viable projects today are those needed to protect Britain from climate change. Any government with political spine would have insisted that the banks lend, at low affordable rates, to transformative projects in the real, productive economy where jobs are created, income generated, and society protected. And if shareholders and executives object to such conditions, then politicians should withdraw access to the Bank of England’s QE and low interest rates, and to government guarantees for deposits.

Quantitative easing – the creation of liquidity currently directed only at the financial sector – is only possible because central banks, if not directly publicly owned, are dependent for their legitimacy and money-creation powers, on taxpayers. The Federal Reserve is ultimately backed by US taxpayers. The Bank of England is a nationalised bank, whose authority is derived from Britain’s 31 million-plus taxpayers.

” ..in 2015, the amount of opioids prescribed in the US was enough for every American to be medicated around the clock for three weeks.”

• Opioid Deaths In US Break New Record: 100 People A Day (RT)

The first nine months of 2016 saw a sharp increase in opioid drug overdoses in the US compared to the prior year, according to new data by the National Center for Health Statistics (NCHS). The government is struggling to respond to the crisis. Deaths due to drug overdose peaked in the third quarter of last year – 19.7 cases for every 100,000 people, compared to 16.7 in the same period the year before, according to newly released numbers from the NCHS, which is part of the US Centers for Disease Control and Prevention (CDC). The Centers attributed 33,000 deaths in 2015 to opioid drugs, including legal prescription painkillers as well as illicit drugs like heroin and street fentanyl. “Opioid prescribing continues to fuel the epidemic. Today, nearly half of all US opioid overdose deaths involve a prescription opioid,” according to the CDC.

A new study published in the American Journal of Preventive Medicine says actual opioid mortality rate changes are on average 22% higher than federal statistics indicate, due to information missing from CDC records. “Opioid mortality rate changes were considerably understated in Pennsylvania, Indiana, New Jersey and Arizona,” said the study’s author, Dr. Christopher Ruhm, a health economist at the University of Virginia. Top US officials have consistently raised the alarm about the addiction crisis in the US, but a solution is yet to be found. [..] Last week, the Trump-appointed commission on combating the drug addiction crisis in America called on the president to declare “a national emergency.”

After the meeting with Trump on Tuesday, Price said the administration will act without such a declaration. “Here is the grim reality,” the commission wrote in their letter to Trump. “Americans consume more opioids than any other country in the world. In fact, in 2015, the amount of opioids prescribed in the US was enough for every American to be medicated around the clock for three weeks.”

And this is how the opioid disaster started, and still rolls on. Easy fix (pun intended), but who’s going to do it?

• New Hampshire Sues Purdue Pharma Over Opioid Marketing Practices (R.)

New Hampshire sued OxyContin maker Purdue Pharma LP on Tuesday, joining several state and local governments in accusing the drugmaker of engaging in deceptive marketing practices that have helped fuel a national opioid addiction epidemic. The lawsuit filed in Merrimack County Superior Court claimed that Purdue Pharma significantly downplayed the risk of addiction posed by OxyContin and engaged in marketing practices that “opened the floodgates” to opioid use and abuse. The lawsuit came after the state’s top court in June overturned a ruling that barred the enforcement of subpoenas against Purdue and four other drugmakers because of the use of a private law firm by the office of the attorney general.

The complaint said the Stamford, Connecticut-based company had spent hundreds of millions of dollars since the 1990s on misleading marketing that overstated the benefits of opioids for treating chronic, rather than short-term, pain. Purdue and three executives in 2007 pleaded guilty to federal charges related to the misbranding of OxyContin, and agreed to pay a total of $634.5 million to resolve a U.S. Justice Department probe. That year, the privately held company reached a $19.5 million settlement with 26 states and the District of Columbia. It agreed in 2015 to pay $24 million to resolve a lawsuit by Kentucky. The lawsuit by New Hampshire, which was not among those settled, said Purdue has continued to benefit from its earlier misconduct and has since 2011 expanded the market for opioids in the state.

No wonder with the opioid cases.

• Americans Are Dying Younger, Saving Corporations Billions (BBG)

Steady improvements in American life expectancy have stalled, and more Americans are dying at younger ages. But for companies straining under the burden of their pension obligations, the distressing trend could have a grim upside: If people don’t end up living as long as they were projected to just a few years ago, their employers ultimately won’t have to pay them as much in pension and other lifelong retirement benefits. In 2015, the American death rate—the age-adjusted share of Americans dying—rose slightly for the first time since 1999. And over the last two years, at least 12 large companies, from Verizon to General Motors, have said recent slips in mortality improvement have led them to reduce their estimates for how much they could owe retirees by upward of a combined $9.7 billion, according to a Bloomberg analysis of company filings.

“Revised assumptions indicating a shortened longevity,” for instance, led Lockheed Martin to adjust its estimated retirement obligations downward by a total of about $1.6 billion for 2015 and 2016, it said in its most recent annual report. Mortality trends are only a small piece of the calculation companies make when estimating what they’ll owe retirees, and indeed, other factors actually led Lockheed’s pension obligations to rise last year. Variables such as asset returns, salary levels, and health care costs can cause big swings in what companies expect to pay retirees. The fact that people are dying slightly younger won’t cure corporate America’s pension woes—but the fact that companies are taking it into account shows just how serious the shift in America’s mortality trends is.

It’s not just corporate pensions, either; the shift also affects Social Security, the government’s program for retirees. The most recent data available “show continued mortality reductions that are generally smaller than those projected,” according to a July report from the program’s chief actuary. Longevity gains fell short of what was projected in last year’s report, leading to a slight improvement in the program’s financial outlook. [..] Absent a war or an epidemic, it’s unusual and alarming for life expectancies in developed countries to stop improving, let alone to worsen. “Mortality is sort of the tip of the iceberg,” says Laudan Aron, a demographer and senior fellow at the Urban Institute. “It really is a reflection of a lot of underlying conditions of life.” The falling trajectory of American life expectancies, especially when compared to those in some other wealthy countries, should be “as urgent a national issue as any other that’s on our national agenda,” she says.

Not sure where this article aims to go, but Americans entering another dimension is a nice starting point.

• Unlearning The Myth Of American Innocence (G.)

I grew up in Wall, a town located by the Jersey Shore, two hours’ drive from New York. Much of it was a landscape of concrete and parking lots, plastic signs and Dunkin’ Donuts. There was no centre, no Main Street, as there was in most of the pleasant beach towns nearby, no tiny old movie theatre or architecture suggesting some sort of history or memory. Most of my friends’ parents were teachers, nurses, cops or electricians, except for the rare father who worked in “the City”, and a handful of Italian families who did less legal things. My parents were descendants of working-class Danish, Italian and Irish immigrants who had little memory of their European origins, and my extended family ran an inexpensive public golf course, where I worked as a hot-dog girl in the summers. The politics I heard about as a kid had to do with taxes and immigrants, and not much else. Bill Clinton was not popular in my house. (In 2016, most of Wall voted Trump.)

We were all patriotic, but I can’t even conceive of what else we could have been, because our entire experience was domestic, interior, American. We went to church on Sundays, until church time was usurped by soccer games. I don’t remember a strong sense of civic engagement. Instead I had the feeling that people could take things from you if you didn’t stay vigilant. Our goals remained local: homecoming queen, state champs, a scholarship to Trenton State, barbecues in the backyard. The lone Asian kid in our class studied hard and went to Berkeley; the Indian went to Yale. Black people never came to Wall. The world was white, Christian; the world was us. We did not study world maps, because international geography, as a subject, had been phased out of many state curriculums long before. There was no sense of the US being one country on a planet of many countries. Even the Soviet Union seemed something more like the Death Star – flying overhead, ready to laser us to smithereens – than a country with people in it.

I have TV memories of world events. Even in my mind, they appear on a screen: Oliver North testifying in the Iran-Contra hearings; the scarred, evil-seeming face of Panama’s dictator Manuel Noriega; the movie-like footage, all flashes of light, of the bombing of Baghdad during the first Gulf war. Mostly what I remember of that war in Iraq was singing God Bless the USA on the school bus – I was 13 – wearing little yellow ribbons and becoming teary-eyed as I remembered the video of the song I had seen on MTV. “And I’m proud to be an American; Where at least I know I’m free”. That “at least” is funny. We were free – at the very least we were that. Everyone else was a chump, because they didn’t even have that obvious thing. Whatever it meant, it was the thing that we had, and no one else did. It was our God-given gift, our superpower.

Because Greece has the absolutely worst accomodations for them.

• EU Nations Start Process Of Returning Refugees, Migrants To Greece (AP)

European Union countries have begun the process of sending migrants who arrived in Europe via Greece over the last five months back to have their asylum applications assessed there. EU rules oblige migrants to apply for asylum in the country they first enter. But the rules were suspended as hundreds of thousands of people, many of them Syrian refugees, entered Greece in 2015. The European Commission recommended in December that EU countries gradually resume transfers to Greece of unauthorized migrants arriving from March 15 onwards. “Some member states have made requests but transfers have not begun. Greece has to give assurances that they have adequate reception conditions,” European Commission spokeswoman Tove Ernst said Tuesday.

“Reception conditions in Greece have significantly improved since last year, which is why the Commission recommended a gradual resumption of transfers,” she said. The recommendation is not binding on EU countries. Greece’s asylum service says requests have been made to return more than 400 migrants. Seven requests have been accepted so far. In Athens, Greece’s migration minister said the returns would involve “tiny numbers.” “We will accept a few dozen people in coming months,” Yiannis Mouzalas told private Skai TV Tuesday. “This will be done provided we have the proper conditions to receive them.” Mouzalas said it was a “symbolic move” dictated by Greece’s EU obligations.

Home › Forums › Debt Rattle August 9 2017