William Blake Europe Supported by Africa and America 1796

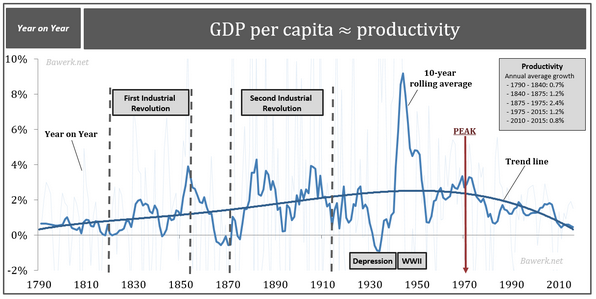

Earlier this week I was struck by the similarities and differences between two graphs I saw float by. And the thought occurred that they are as scary as they are interesting. The graphs show eerily similar trends. And complement each other. The first graph, which Tyler Durden posted, shows productivity, defined as more or less the same as GDP per capita. It goes all the way back to 1790 and contends that 2017 productivity is about back to the level it was at in 1790. In the article, Tyler suggests a link with the amount of time people spend on Instagram et al, but perhaps there is something more going on.

That is, America and Western Europe exported almost their entire manufacturing capacity to China etc. And how can you be productive if you don’t manufacture anything? Yeah, I know, ‘knowledge economy’ and ‘service economy’ and all that, but does anyone still really believe those terms? Sure, that may have worked for a while as others were still actually making stuff (and nobody really understood the idea anyway), but it’s a sliding scale. As productivity plunged, so did GDP per capita. We can all wrap our heads around that.

America’s Productivity Plunge Explained

For the first time since the financial crisis, US multifactor productivity growth turned negative last year, mystifying economists who have struggled to find something to blame for the fact that worker productivity is declining despite a technology boom that should make them more efficient – at least in theory. To be sure, economists have struggled to find explanations for the exasperating trend, with some arguing that the US hasn’t figured out how to properly measure productivity growth correctly now that service-sector jobs proliferate while manufacturing shrinks. But what if there’s a more straightforward explanation? What if the decline in US productivity measured since the 1970s isn’t happening in spite of technology, but because of it?

To wit, Facebook has just released user-engagement data for its popular Instagram photo-sharing app. Unsurprisingly, the data show that the average user below the age of 25 now spends more than 32 minutes a day on the app, while the average user aged 25 and older. The last time Facebook released this data, in October 2014, its users averaged 21 minutes a day on the app. According to Bloomberg, “time spent is an important metric for advertisers, which like to hear that users are browsing an app beyond quick checks for updates, making them more likely to run into some marketing.” Maybe they should matter more to economists, too.

When asking the question “What if the decline in US productivity measured since the 1970s isn’t happening in spite of technology, but because of it?”, a next question should be: what is the technology used for? And if the answer to that is not “for making things”, then what do you think could its effect on productivity could possibly be?

Tyler took that graph from an article posted August 22, 2015, also on Zero Hedge, by Eugen Bohm-Bawerk, who at the time had some interesting things to say about it:

Productivity In America Now On Par With Agrarian Slave Economy

[..] it is time to take a closer look at productivity measured in terms of GDP per capita. While this is not an entirely correct way to measure productivity, it does adhere to new classical growth model theories which posit that in a developed economy, reached steady state, the only way to increase GDP per capita is through increased total factor productivity. In plain English, growth in GDP per capita equals productivity growth. The reason we use this concept instead of more advanced productivity measures is to get a long enough time series to properly understand the underlying fundamental forces driving society forward.

In our main chart we have tried to see through all the underlying noise in the annual data by looking at a 10-year rolling average and a polynomial trend line. In the period prior to the War of 1812 US productivity growth was lacklustre as the economy was mainly driven by agriculture and slaves (slaves have no incentive to work hard or innovate, only to work just hard enough to avoid being beaten). From 1790 to 1840 annual growth averaged only 0.7%. As the first industrial revolution started to take hold in the north-east, productivity growth rose rapidly, and even more during the second industrial revolution which propelled the US economy to become the world largest and eventually the global hegemon [..]

Adjusting for the WWII anomaly (which tells us that GDP is not a good measure of a country’s prosperity) US productivity growth peaked in 1972 – incidentally the year after Nixon took the US off gold. The productivity decline witnessed ever since is unprecedented. Despite the short lived boom of the 1990s US productivity growth only average 1.2% from 1975 up to today. If we isolate the last 15 years US productivity growth is on par with what an agrarian slave economy was able to achieve 200 years ago.

[..] With hindsight we know that finance did more harm than good so we can conservatively deduct finance from the GDP calculations and by doing so we essentially end up with no growth per capita at all over a timespan of more than 15 years! US real GDP per capita less contribution from finance increased by an annual average of 0.3% from 2000 to 2015. From 2008 the annual average has been negative 0.5%!

In other words, we have seen a progressive (pun intended) weakening of the US economy from the 1970s and the reason is simple enough when we know that monetary policy broken down to its most basic is a transaction of nothing (fiat money) for something (real production of goods and services). Modern monetary policy thereby violates the most sacred principle in a market based economy; namely that production creates its own demand. Only through previous production, either your own or borrowed, can one express true purchasing power on the market place.

The central bank does not need to worry about such trivial things. They can manufacture the medium of exchange at zero cost and express purchasing power on the same level as the producer. However, consumption of real goods and services paid for with zero cost money must by definition be pure capital consumption. Do this on a grand scale, over a long period of time, even a capital rich economy as the US will eventually be depleted. Capital per worker falls relative to competitors abroad, cost goes up and competitiveness falls (think rust-belt). Productive structures cannot be properly funded and the economy must regress to align funding with its level of specialization.

Eugen gets close to what I said earlier about productivity. That is, you have to make stuff, to manufacture things, in order to have, let alone grow, productivity (aka GDP per capita). An economy based -too heavily- on services and finance is not going to do it for you. Because “the most sacred principle in a market based economy” is that “production creates its own demand.”

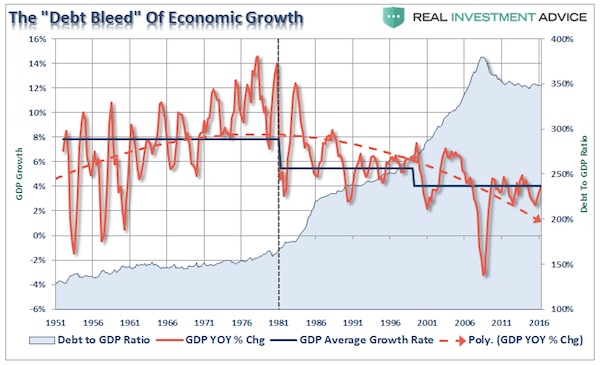

Now, combine that graph with the next one, from Lance Roberts, which unmistakably depicts the same trendline, though on a different -shorter- time scale. Lance’s graph shows more or less the same as Tyler’s, if you allow me that freedom, namely: GDP per capita growth equals productivity equals GDP growth, but it adds a crucial component (unless you ask someone like Paul Krugman): debt.

Together, the graphs show how we have ‘solved’ the issue of falling growth and productivity: with debt. It doesn’t get simpler than that. We exported our productive capacity to China, and now we can only afford to buy their products -which are mostly inferior in quality to what our ancestors once made- by getting into -more- debt. Big simplification, granted, but we’re doing broad strokes here.

All this is simple enough for a 6-year old to grasp. It’s actually likely easier for them than for most trained economists. Problem is, the 6-year olds are probably busy on Instagram. Tyler’s right on that one. But then, at least they’re not stuck in outdated modelling.

Ergo: we have a precipitous decline in productivity, which also translates into a decline in GDP. Even if we come up with all sorts of accounting tricks to hide this fact. And what do we do, or rather, what have we done? Enter central banks, stage right. That second graph inevitably raises the question: Without all the debt, where would the growth rate stand today? And I know what you want to say, because just like you, I am afraid to ask.

We’ve used all those trillions in new debt to, as far as productivity is concerned, run to not even stand still: productivity (GDP per capita) continues to decline despite all the debt. Why is that? Well, Bohm-Bawerk answers that question earlier: “.. consumption of real goods and services paid for with zero cost money must by definition be pure capital consumption.” In other words, as I said before, if you don’t use it to actually make things, you’re basically just burning it. Plus, in the process, as we see ever clearer in the effects of QE, you can grossly distort an economy, by blowing bubbles, propping up zombies etc.

Things would look different if we used the “zero cost money” for production instead of consumption. But that’s not what the central bank money is used for at all. The net effect of all that debt, be it QE or new mortgage debt, is less than zero. Quite a bit less, actually. How do we solve that problem? The answer is deadly simple, though not easy to put into practice: start making stuff again! Or put it this way: debt must be used to raise production, not consumption.

Home › Forums › Productivity and Debt