Marc Chagall The watering trough 1925

This morning: Explosions on the Kerch bridge (Crimean bridge), which connects Crimea with Russia.

Macgregor

Ed Dowd

“We are deciding which hotels to put them up in – one for Mr. Putin and one for Mr. Zelensky..”

“..his press secretary, Sergey Nikiforov, in a comment to Ukrainian media, denied the information that Zelensky had decided to visit the G20 summit..”

• Putin and Zelensky To Attend G20 – Indonesia (RT)

Russian President Vladimir Putin and his Ukrainian counterpart, Vladimir Zelensky, will both travel to Bali in November for the G20 summit, an Indonesian diplomat has told UAE’s The National newspaper. If true, the summit will be the first event attended by both leaders since Russia’s military operation in Ukraine began. “Both have agreed [to attend],”Indonesia’s ambassador to the United Arab Emirates, Husain Bagis, told The National on Friday. He conceded that “the situation isn’t easy because of the Ukraine-Russia war,” and said that his government is already planning how to manage the arrival of the two leaders. “We are deciding which hotels to put them up in – one for Mr. Putin and one for Mr. Zelensky,” he said.

The Kremlin confirmed in June that Putin would attend the summit, although spokesman Dmitry Peskov said on Friday that the format of Putin’s participation “is still not defined.” Kiev stated in August that Zelensky “believes that he should be on the territory of Ukraine,” but would “think about”making the trip if Putin were to attend in person. Today his press secretary, Sergey Nikiforov, in a comment to Ukrainian media, denied the information that Zelensky had decided to visit the G20 summit. US President Joe Biden and a number of other Western leaders urged Indonesian President Joko Widodo not to invite Putin to the summit in Bali.

However, Widodo resisted the pressure campaign and invited the Russian leader as planned. With Widodo having met both Zelensky and Putin earlier this summer in a bid to “invite the two leaders to open dialogue and stop the war,” Bagis told The National that Indonesia aims “to make the G20 a platform for peace, not conflict.” Biden also appears to have softened his exclusionary stance toward Putin, telling reporters on Thursday that it “remains to be seen” whether he would meet the Russian president on the sidelines of the summit. The State Department quickly stepped in to say that in the view of the entire government, “it cannot be business as usual when it comes to Russia.” Although Ukraine is not one of the world’s 20 largest economies, Zelensky was invited to Bali as a guest.

Sustainable peace = Green peace?!

Wonder if Merkel is involved in secret talks with Russia.

• Merkel: Lasting Peace In Europe Only Possible With Russia’s Input (RT)

Sustainable peace in Europe may only be achieved if Russia is part of it, former German Chancellor Angela Merkel said on Thursday. Speaking during the 77th anniversary of the German newspaper ‘Suddeutsche Zeitung,’ Merkel explained that while the West has been adamant in its support for Ukraine as the nation remains locked in conflict with Russia, it should also keep its mind open about what might seem as “unthinkable” now – Moscow’s future role in Europe’s affairs. She stressed that “a future European security architecture within international law will meet the requirements” only if it involves Russia. “As long as we haven’t achieved that, the Cold War is not really over either,” she added.

Merkel described February 24 – the day Russia launched its military campaign in Ukraine – as a “turning point,” adding that statements made by various parties to the conflict should be taken “seriously and not to be classified as a bluff from the start.” She was apparently referring to recent comments made by Russian President Vladimir Putin, who signaled that Moscow would use “all means to defend Russia and our people” if its territorial integrity was threatened. He also warned the West that those who use nuclear blackmail against Russia “should know that the wind rose can turn around.”

Merkel earlier urged the Western world to take Putin and his words seriously, arguing that such an approach is “by no means a sign of weakness,” but rather “a sign of political wisdom.” She also noted that former German chancellor Helmut Kohl, who before his death, was widely regarded as her political mentor, would have kept an open mind about “how relations to and with Russia could one day be redeveloped” after hostilities in Ukraine end. Such a stance, however, did not sit well with Ukrainian officials. Last week, Andrey Melnik, Kiev’s outgoing ambassador to Berlin, called Merkel’s attitude towards Russia and its role in European security “almost perverse.”

“A Greater Europe didn’t happen; a Greater Asia that includes Russia is de facto emerging.”

• Russia Abandons The Dream Of A Greater Europe (RT)

Re-uniting the divided people of Russia and gathering the lands where they live is essentially the core element of the new Russian idea that Putin is offering to his compatriots. The immediate task of course is to integrate the new territories that have just joined Russia following the referendums. This requires a major effort in many areas and at various levels. It is anything but easy. Russian forces, which for months have been advancing on Ukrainian territory, suddenly find themselves in a situation where they have to abandon some areas which are now legally Russian land, populated by Russian citizens who just voted in the referendums and now face severe reprisals at the hands of the counter-attacking Ukrainians.

Next comes the need to rebuild the cities and villages ravaged in the war, repair damaged infrastructure, restart the economy, provide communal services, and re-organize public administration, health services, and education. Of paramount importance is socializing the millions of residents of the four regions who were automatically granted Russian citizenship, in the Russian national environment. Moscow has some experience of that from 2014 when Crimea and Sevastopol joined Russia, but doing this in a wartime situation is more challenging. A lot will depend, of course, on how the Russian forces cope on the frontline that passes very close to Donetsk and Kherson, and which still leaves the city of Zaporozhiye in Ukraine’s rear.

Even if the Ukrainian counter-offensive runs out of steam and the Russians resume their advance, none of these tasks can be accomplished quickly. This part of the new Russian national idea will keep the nation busy for a long time. Putin’s concept, however, doesn’t stop there. It is not so much about restoring the Soviet Union: in Putin’s words, such a restoration is not Moscow’s objective. The Baltics, the South Caucasus and Central Asia are probably not envisaged as part of the new construct. However, as Foreign Minister Sergei Lavrov hinted on the State Duma floor, in future other Ukrainian regions might be given the chance to follow Kherson and Zaporozhiye. To Putin, Greater Russia is a distinct civilization which opposes not only America’s hegemonic policies, but also the West’s projection of its values as universal.

This is an about-face not only from Gorbachev’s musings about a common European home, but also from Putin’s own travails in trying to forge a Greater Europe from Lisbon to Vladivostok, and his efforts to find a way for Russia to join NATO. A Greater Europe didn’t happen; a Greater Asia that includes Russia is de facto emerging. As to a Greater Russia, this requires more than a leader’s imagination. The Soviet Union, as the living generations remember it, was very much the product of the Great Patriotic War. The hybrid war with the West, of which Ukraine is only a small part, will doubtless reshape Russia. The question is, will it also transform it to fit the vision of a powerful economy and a vibrant society, faithful to its declared values – the substance, rather than the form of a Greater Russia.

“A 2019 Pentagon-funded study from the RAND Corporation on how best to exploit “Russia’s economic, political and military vulnerabilities and anxieties” included a recommendation to “Reduce [Russian] Natural Gas Exports and Hinder Pipeline Expansions.”

• US Media’s Intellectual No-Fly-Zone on Nord Stream (FAIR)

Any serious coverage of the Nord Stream attack should acknowledge that opposition to the pipeline has been a centerpiece of the US grand strategy in Europe. The long-term goal has been to keep Russia isolated and disjointed from Europe, and to keep the countries of Europe tied to US markets. Ever since German and Russian energy companies signed a deal to begin development on Nord Stream 2, the entire machinery of Washington has been working overtime to scuttle it. A 2019 Pentagon-funded study from the RAND Corporation on how best to exploit “Russia’s economic, political and military vulnerabilities and anxieties” included a recommendation to “Reduce [Russian] Natural Gas Exports and Hinder Pipeline Expansions.”

The study noted that a “first step would involve stopping Nord Stream 2,” and that natural gas “from the United States and Australia could provide a substitute.” This RAND study also prophetically recommended “providing more US military equipment and advice” to Ukraine in order to “lead Russia to increase its direct involvement in the conflict and the price it pays for it,” even though it acknowledged that “Russia might respond by mounting a new offensive and seizing more Ukrainian territory.” The Obama administration opposed the pipeline. As part of the major sanctions package against Russia in 2017, the Trump administration began sanctioning any company doing work on the pipeline. The move generated outrage in Germany, where many saw it as an attempt to meddle with European markets. In 2019, the US implemented more sanctions on the project.

Upon coming into office, President Joe Biden made opposition to the pipeline one of his administration’s top priorities. During his confirmation hearings in 2021, Secretary of State Anthony Blinken told Congress he was “determined to do whatever I can to prevent” Nord Stream 2 from being completed. Months later, the State Department reiterated that “any entity involved in the Nord Stream 2 pipeline risks US sanctions and should immediately abandon work on the pipeline.” In July 2021, the sanctions were relaxed only after contentious negotiations with the German government. The New York Times (7/21/21) reported that the administration and Germany still had “profound disagreements” about the project.

“We all remember how [Zelensky] declared in January Ukraine’s intention to acquire nuclear weapons. Apparently, this idea has long been stuck in his mind..”

• Lavrov Explains Why Russia Sees Ukraine As A Threat (RT)

A call by Ukrainian President Vladimir Zelensky for NATO members to deploy nuclear weapons against Russia is a reminder of why Moscow launched military action against his country, Russian Foreign Minister Sergey Lavrov has said. “Yesterday, Zelensky called on his Western masters to deliver a preemptive nuclear strike on Russia,” Moscow’s top diplomat stated during a media conference on Wednesday. In doing so, the Ukrainian leader “showed to the entire world the latest proof of the threats that come from the Kiev regime.” Lavrov said Russia’s special military operation had been launched to neutralize those threats. He dismissed as “laughable” an attempt to downplay Zelensky’s words made by his press secretary, Sergey Nikoforov. “We all remember how [Zelensky] declared in January Ukraine’s intention to acquire nuclear weapons. Apparently, this idea has long been stuck in his mind,” the Russian minister said.

On Thursday, Zelensky told the Australian Lowy Institute that NATO must carry out preemptive strikes against Russia so that it “knows what to expect” if it uses its nuclear arsenal. He claimed that such action would “eliminate the possibility of Russia using nuclear weapons,” before recalling how he urged other nations to preemptively punish Russia before it launched its military action against his country. “I once again appeal to the international community, as it was before February 24: Preemptive strikes so that [the Russians] know what will happen to them if they use it, and not the other way around,” he said. His spokesman then claimed that people interpreting Zelensky’s words as a call for a preemptive nuclear strike were wrong, and that Ukraine would never use such rhetoric.

Cold and hunger and billions for Azov. A winning model.

• EU Again Urged To Open Wallet For Kiev (RT)

Josep Borrell, the EU High Representative for Foreign Affairs, will urge member states to set aside more funds to cover enhanced military assistance for Ukraine. The top diplomat shared his plan with reporters at an informal EU summit in Prague on Friday. “I will ask the leaders to support the proposal for a new tranche for European Peace Facility to continue providing military support to Ukraine, also to the training mission,” Borrell said, as quoted by Reuters. Earlier this week Borrell expressed hope that at the next Foreign Affairs Council gathering on October 17, the EU will be able to “formally launch” its training mission for Ukrainian armed forces. Writing in his blog, the diplomat also claimed that the EU would “reinforce” its strategy of supporting Ukraine – “militarily, financially and politically.”

The European Peace Facility (EPF) that Borell referred to, is a mechanism created last year to enhance the EU’s ability to act as a global security provider. The EPF reimburses governments for military equipment supplied to Kiev, “including items designed to deliver lethal force for defensive purposes.” The latest round of funding for Ukraine under the EPF, worth €500 million, was agreed by the European Council in July. With this package, the total EU contribution for the country within this framework amounts to €2.5 billion. The EPF has a ceiling of about €6 billion and is supposed to support not only Ukraine but also other countries. As EU nations face an energy and cost-of-living crisis, exacerbated by anti-Russia sanctions and a reduction in Russian energy supplies, Borrell earlier urged people in the bloc to combat “the temptation to abandon Ukraine.”

Responding earlier this week to the EU’s plan of creating a training mission for Kiev’s armed forces, Russian Foreign Ministry spokeswoman Maria Zakharova said that such a move would only “fix the EU in the status of a participant in the conflict.” In April, she accused the bloc of turning into “NATO’s economic relations department.” This followed Borrell’s tweet that “This war (in Ukraine) must be won on the battlefield.” Moscow has consistently warned Western countries against providing military support to Kiev. It argues that such assistance would only prolong the conflict and will lead to unnecessary casualties. Ukraine, in turn, has repeatedly claimed that the EU is too slow in its weapons supplies and that it doesn’t always provide what Kiev had requested.

I found this strange. Macron wanted a new club, the European Political Community (EPC), which is EU plus some others?! Why? Betcha it’s so Ukraine can be part of some club too.

• Belgium Fails To Support New Round Of Sanctions Against Russia (RT)

The Belgian government decided against endorsing a new round of EU anti-Russia trade restrictions, the local press reported on Thursday, citing remarks made by Prime Minister Alexander De Croo. Speaking on the sidelines of the European Political Community (EPC) summit in Prague, Czech Republic, the head of the Belgian government explained that “as the economic cost of sanctions becomes higher, it becomes difficult to show solidarity” with Ukraine. “The sanctions have worked very well so far,” the prime minister said, “but the further we go, the more we talk about sanctions that hurt our own economy more than Russia’s.” His country therefore declined to support the eighth package of sanctions when EU member states voted on it this week.

Belgium didn’t vote against it either, because “we do not want to break European solidarity,” De Croo was quoted as saying. A vote against the proposal any EU member state would have blocked the package from being approved. Belgium was reportedly the only nation to abstain. Earlier this week, Belgian MP Andre Flahaut, who represents the province of Walloon Brabant, expressed concerns about the impact of the upcoming sanctions on his constituents. Two factories owned by the Russian metals giant NLMK, which are located in the Belgian province, may have to shut down, the lawmaker warned. The EU ultimately allowed a transition period of two years to switch from semi-finished steel products originating in Russia to alternative supplies.

There were also concerns in Belgium that the EU would try to restrict trade in Russian diamonds, potentially impacting the jewelry businesses of Antwerp. Some news outlets reported that the country blocked the proposed inclusion of such sanctions in the package. When asked about Russian gemstones, Prime Minister De Croo said his government would not have opposed a ban, if it were necessary, but the European Commission decided against it because imports from Russia had fallen significantly without any formal restrictions. The EPC is a new political club proposed earlier this year by French President Emmanuel Macron. The forum is supposed to bring together EU member states and nations that aspire to become part of the economic bloc, plus its traditional allies like the UK and Norway. The meeting of EPC leaders in Prague is the first of its kind.

Orban could soon walk out. They refuse to give him his money anyway. Why stay?

• Orban Urges Changes To EU Sanctions Policy (RT)

Sanctions imposed by the EU on Russia over the conflict in Ukraine have failed, Hungarian Prime Minister Viktor Orban said on Thursday, urging Brussels to change its policy. “The sanctions didn’t fulfill the hopes that were pinned on them, the war hasn’t ended,” Orban wrote on Facebook. “Europe is slowly bleeding and Russia is making money in the meantime,” he pointed out. The Hungarian leader said that it was obvious to him that “the failed policy of Brussels must be changed.” The statement was made on the same day that the EU announced an eighth round of sanctions on Russia. The new curbs include an oil price cap, trade restrictions amounting to 7 billion euros and individual sanctions against 30 people and seven entities. The move comes after the official inclusion of Donetsk and Lugansk People’s Republics as well as Kherson and Zaporozhye Regions into Russia [..]

Orban has frequently criticized the EU’s sanctions on Russia, calling them counterproductive. Hungary, which is heavily dependent on Russian energy, has maintained a relatively neutral stance during the conflict in Ukraine, condemning the use of force by Moscow, but refusing to supply weapons to Kiev. Brussels expected that the unprecedented restrictions would cripple Russia’s economy and prevent it from funding its military operation. But Moscow was able to redirect its oil and gas to Asian markets, while also profiting from growing energy prices. The policy has also largely backfired for the EU, causing a spike in inflation, and putting Europe into an energy crisis. The situation deteriorated even further in late September when the Nord Stream pipelines were sabotaged.

“Biden Threatening Nuclear Armageddon After Six Years of Media Freakout Over Trump Tweets”

• Joe Biden Is Not A Real President (Scarry)

Did anyone else burst into a bout of uncontrollable, psychotic laughter upon reading the report that President Biden just told a room full of Democrat donors that the risk of nuclear “armageddon” has arrived? I can’t be the only one. Here are some headlines from the not-too-distant past that immediately came to mind: • We must Trump-proof the nuclear codes before 20243 NBC News, March 12, 2022 • Gen. Milley feared Trump might launch nuclear attack, made secret calls to China, new book says USA Today, Sept. 14, 2021 • Trump is leading us into nuclear war, says Daniel Ellsberg (and he should know, he used to plan them) Canadian Broadcasting Corporation, Feb. 1, 2018 • Donald Trump s Nuclear-War Threat The New Yorker, Aug. 9, 2017 • Clinton Says Trump Could Lead US Into Nuclear War Roll Call, June 2, 2016.

So, wait a second. You mean we just spent the last six years with all of Washington and the national media swearing to voters that Trump had us on the brink of nuclear annihilation, only for it to be Biden, their choice for president, to get us right up on the cliff’s edge? If that doesn’t have you pulling tufts of hair out of your scalp until it bleeds, check your pulse. This can’t be real. Biden has to be fake. This must be a computer simulation. For four years under Trump, gas was cheap, the stock market was booming, and a trip to the grocery store didn’t require customers to take out a second mortgage.

Now under Biden, OPEC is gratuitously choking the energy supply, basic necessities are scarce, and a major war has American taxpayers spending more than $67 billion (and counting) to a country that’s 5,000 miles away. Oh, and now we have to worry about a nuclear confrontation with a global superpower! sIf it were a movie script, not a single producer would find it believable. The writer would never work again. But this is real? We elected a president, in earnest, who is this incompetent and terrible? It’s nuclear war he’s warning of! This is the absolute worst-case scenario. The severity can’t be overstated. There aren’t enough mean Trump tweets in the world to excuse the state of things under this “president.” I refuse to believe it. Biden isn’t a real president.

“..they 1) are not our friends, 2) do not care what we want, 3) do not take us seriously and 4) are not here to help us and/or Biden get re-elected by lowering prices..”

• OPEC Humiliates President Biden On A Global Stage (QTR)

[..] yesterday OPEC humiliated President Biden on a global stage by cutting oil production after he specifically lobbied them not to. There’s no “nice” way of putting it – they straight-up snubbed the U.S. and have now, in my opinion, made it officially clear that they 1) are not our friends, 2) do not care what we want, 3) do not take us seriously and 4) are not here to help us and/or Biden get re-elected by lowering prices. To use Biden’s parlance, “Let me tell you something, Jack – we’re not in bed with the Saudis anymore. They are more allied with China and Russia than they have ever been, at arguably the most crucial moment in recent history for our global economy.”

As I pointed out last night on my podcast, there was nothing quite like the “fist bump heard round the world” a couple months ago when President Biden – who spends his time here domestically fighting for “equality” and human rights – decided to embrace the Saudis, and their track record of disapproving of gay rights, murdering journalists and multiple other human rights violations – instead of simply ramping up domestic oil production here in the U.S. Biden probably went into the meeting he had with MBS months ago thinking we had some type of leverage, like we have had decades ago. The sad reality is that we simply don’t anymore: the Saudis have the oil, they have gold, and now they have allies just as big and powerful as the U.S. when combined. And those allies provide financial and military support at a crucial juncture for geopolitics.

Meanwhile, our President remains tone deaf and while his supporters remain immune to what can only be described as blatantly obvious double standards. With the left hand, Biden was vilifying Exxon and Chevron here in the U.S., basically encouraging them to not bring more supply online, whilst blaming “gas station owners” and other people who don’t set the price of refined fuels. With the right hand, he was fist bumping a man who publicly disapproves of gay rights and ordered the murder of a critical journalist, in order to try and get him to unleash more oil on the global stage. And instead of him taking us seriously, he did the exact opposite of what Biden wanted yesterday – cut oil production, raising prices – and humiliated Biden on the global stage.

“Serbian Interior Minister Aleksandar Vulin has described the eighth package of anti-Russia penalties as the “first EU sanctions package” against Serbia.”

• Luxembourg Raises Red Flag Over Energy Price Caps (RT)

The European Union may be left with no energy supplies after introducing gas price caps, Luxembourg’s Prime Minister Xavier Bettel said as he arrived at the bloc’s summit in Prague on Friday. “Implementing a price cap is not the only thing,” Bettel said. “Because, after, maybe we can’t get energy. So then, maybe we have a price cap but no energy.” EU leaders are expected to discuss how to deal with gas prices to curb soaring energy bills during their informal summit in the Czech capital. The talks will include a proposal on a gas price cap. “We have to know we’re not the only customers in the world,” he added. “So, we have to be very careful about decisions that we take that sound good on paper but where consequences can be problematic.”

The issue has been hotly contested for weeks, with Germany, Denmark, and the Netherlands in opposition to any form of cap due to concerns regarding security of supply. On Thursday, Brussels announced the eighth package of restrictions on Russia, which includes a price cap and “further restrictions” on the maritime transportation of Russian crude oil and petroleum products to third countries. The latest batch of penalties has been blasted by several EU nations, including Hungary and Serbia. Earlier, Hungarian Prime Minister Viktor Orban said that anti-Russia sanctions had failed, adding that the bloc was “slowly bleeding” due to the drastic steps. Meanwhile, Serbian Interior Minister Aleksandar Vulin has described the eighth package of anti-Russia penalties as the “first EU sanctions package” against Serbia.

“The euro area is at risk of a financial meltdown on the same scale as the crisis it suffered a decade ago..”

They should be so lucky.

• Citi: Financial Crisis May Surprise EU (RT)

The euro area is at risk of a financial meltdown on the same scale as the crisis it suffered a decade ago, Citi analysts have told CNBC. They cited Germany’s massive energy relief plan as the major threat to the bloc’s stability, the media outlet reports on Friday. According to the report, Wall Street bank analysts have raised concerns about the violent bond market moves and the European governments’ plans to borrow vast sums of money. They said that German Chancellor Olaf Scholz’s relief package, worth €200 billion ($195 billion) and aimed at tackling soaring energy prices, “may soften the coming recession but also poses risks.” Those risks relate to the question of how the package will be financed and what that could do to inflation, to Germany’s sovereign bond yields, to the ECB’s benchmark rate, and to the borrowing plans of other euro nations that may do the same.

“The risk is that others may follow that example,” Christian Schulz, deputy chief European economist at Citi, told CNBC, citing the UK’s recent bond market meltdown after unfunded tax cuts by the government. Schulz explained that Germany could “afford” any debt financing thanks to its low debt-to-GDP ratio and lower external funding needs, but the package could open the door for less fiscally prudent countries to want to borrow large amounts and issue new debt. That could potentially lead to trouble like that seen in Britain.

Citi analysts forecast that German debt financing could force tighter ECB policy, which could then also send yields surging in the euro area. “The risk is that this same dynamic [as seen in Britain] evolves on the continent as well now,”Schulz warned. Meanwhile, data by Saxo Bank show that an ECB stress indicator for the Eurozone’s financial system – which looks at tensions in bond, equity and money markets – has risen from below 0.1 at the start of the year to almost 0.5 so far. During the Eurozone debt crisis in 2009-2010, the index exceeded 0.6.

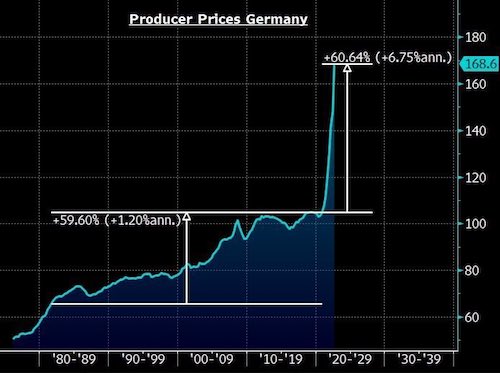

German producer prices. Past 2 years: up 60%. Past 40 years before that: up 60%.

“His staff must be marinated in evidence of the RussiaGate misdeeds — reams of which have been independently documented in the public record..”

• November Surprise? (Jim Kunstler)

Adults understand that politics is a crooked business, but through the whole of US history until now filters existed in the public arena that allowed for enough sorting out of truth from untruth to enable the formation of a reality-based consensus — which, in turn, allowed daily life to operate coherently. The Party of Chaos has thrown the kill-switch on that crucial function by corrupting the news business and subverting the new social media. The result is a public culture of pervasive and immersive lying, and a stupendous institutional failure of the courts to correct any of that behavior. Case-in-point: the John Durham Special Counsel Investigation on the origin of the RussiaGate fraud. It now apparently terminates in the prosecution of the tiniest minnow (Igor Danchenko) in that vast inland sea of corruption.

Some of the figures who carried out the perfidious seditions of RussiaGate are still employed in the Department of Justice and the FBI, and to this day are active in the continued cover-up of the crimes committed to overthrow President Trump, notably: Deputy Attorney General Lisa Monaco, Associate Attorney General Vanita Gupta, DOJ Inspector General Michael Horowitz, FBI Director Christopher Wray, and others. Mr. Durham is supposedly among the highest officers of the federal courts charged with enforcing a very particular region of criminality.

His staff must be marinated in evidence of the RussiaGate misdeeds — reams of which have been independently documented in the public record, ranging from (just for example) the nefarious activities of figures like Nellie Ohr, wife of DOJ higher-up Bruce Ohr, working as go-between with Christopher Steele and the FBI, to the spectacular failures of Judge James Boasberg and his FISA court, not to mention the well-known machinations of Peter Strzok, Lisa Page, Andrew McCabe, Rod Rosenstein, Dana Boente, James Baker, Andrew Weissmann, Jeannie Rhee, Aaron Zebley, Brandon Van Grack, Robert Mueller, and other top officials who worked sedulously against the public interest. All these remain apparently off-the-hook for their sketchy activities.

“Peskov told the Post that disagreement between Putin and his aides is “part of the usual working process.”

• Washington Post Lying About Kremlin ‘Turmoil’ – Moscow (RT)

Kremlin spokesman Dmitry Peskov said on Friday that a Washington Post report alleging “turmoil” and confrontation in Russian President Vladimir Putin’s inner circle is “absolutely not true.” The report in question was attributed to anonymous US spies. “A member of Vladimir Putin’s inner circle has voiced disagreement directly to the Russian president” over the conflict in Ukraine, the report stated, alleging that “the criticism marks the clearest indication yet of turmoil within Russia’s leadership.” No source was given for this report, which was attributed to “information obtained by US intelligence.” Peskov told the Post that disagreement between Putin and his aides is “part of the usual working process.”

“There are working arguments: about the economy, about the conduct of the military operation. There are arguments about the education system. This is part of the normal working process, and it is not a sign of any split,” he said, adding that the information supposedly obtained by American intelligence is “absolutely not true.” American officials have previously boasted about waging an “info war”against Russia by leaking false intelligence reports to the media, NBC News reported in April. Intelligence officials, for example, admitted to fabricating a warning that Russia was preparing to use chemical weapons in Ukraine in March, leaking the story to the Washington Post despite it being based on “low confidence” intelligence.

A report claiming that Putin was “being misled by his own advisers” was also reportedly made up or exaggerated by US spies. “There’s no way you can prove or disprove that stuff,” a retired intelligence operative told NBC. The Post’s latest report was also received with doubt by the US’ European allies. According to the newspaper, “senior security officials in Europe said they were not aware that anyone had dared to challenge Putin directly over the course of events in Ukraine,” and said that they hadn’t seen the supposed US intelligence report that the article was based on.

Terrorists.

• When Anti-Government Speech Becomes Sedition (Whitehead)

Anti-government speech has become a four-letter word. In more and more cases, the government is declaring war on what should be protected political speech whenever it challenges the government’s power, reveals the government’s corruption, exposes the government’s lies, and encourages the citizenry to push back against the government’s many injustices. Indeed, there is a long and growing list of the kinds of speech that the government considers dangerous enough to red flag and subject to censorship, surveillance, investigation and prosecution: hate speech, conspiratorial speech, treasonous speech, threatening speech, inflammatory speech, radical speech, anti-government speech, extremist speech, etc.

Things are about to get even dicier for those who believe in fully exercising their right to political expression. Indeed, the government’s seditious conspiracy charges against Stewart Rhodes, the founder of Oath Keepers, and several of his associates for their alleged involvement in the January 6 Capitol riots puts the entire concept of anti-government political expression on trial. [..] In recent years, the government has used the phrase “domestic terrorist” interchangeably with “anti-government,” “extremist” and “terrorist” to describe anyone who might fall somewhere on a very broad spectrum of viewpoints that could be considered “dangerous.” The ramifications are so far-reaching as to render almost every American with an opinion about the government or who knows someone with an opinion about the government an extremist in word, deed, thought or by association.

You see, the government doesn’t care if you or someone you know has a legitimate grievance. It doesn’t care if your criticisms are well-founded. And it certainly doesn’t care if you have a First Amendment right to speak truth to power. What the government cares about is whether what you’re thinking or speaking or sharing or consuming as information has the potential to challenge its stranglehold on power. Why else would the FBI, CIA, NSA and other government agencies be investing in corporate surveillance technologies that can mine constitutionally protected speech on social media platforms such as Facebook, Twitter and Instagram? Why else would the Biden Administration be likening those who share “false or misleading narratives and conspiracy theories, and other forms of mis- dis- and mal-information” to terrorists?

3 weeks after the New England Journal of medicine said the vaccines destroy your immune system, the stupid circus just goes on.

• CDC: Record Number Of Children Hospitalized With Weakened Immune Systems (ZH)

Official data suggests that more children and young adults than ever have been hospitalized with colds and respiratory issues, according to the Daily Mail, which notes that “experts have repeatedly warned lockdowns and measures used to contain Covid like face masks also suppressed the spread of germs which are crucial for building a strong immune system in children.” According to a retrospective report by the Centers for Disease Control (CDC), levels of common cold viruses hit their highest level among non-adults in August 2021 – when levels had been much lower in previous years during the same month. According to the data which sampled nearly 700 children, nearly 55% tested positive for RSV in August 2021. Of that, 450 were moved to emergency departments where nearly 35% had RSV – which is comparable to the winter months when over 30% of patients regularly have the virus, according to the report.

“The CDC samples random pediatric hospitals across the US and makes national estimates to gauge how prevalent viruses are. There were nearly 700 children in hospital sick with a respiratory virus across the seven wards studied in August last year, of which just over half had tested positive for respiratory syncytial virus (RSV) – which is normally benign. This was the highest levels ever recorded in summer, and came off the back of a year and a half of brutal pandemic restrictions forcing many to stay indoors. The record all-time high is in December, when 60 per cent of children on wards with respiratory illnesses were infected with RSV.” -Daily Mail

Dance

https://twitter.com/i/status/1578392775367819264

Watters

Sources say hunter Biden rejected sweetheart deal from the feds…and new Biden family business partners will be going public which will link Joe Biden to scandal #TheFive pic.twitter.com/Zjgo6FOuCJ

— Jesse Watters (@JesseBWatters) October 7, 2022

Anthony Bourdain RIP

Support the Automatic Earth in virustime with Paypal, Bitcoin and Patreon.