Jack Delano Foggy night in New Bedford, Massachusetts 1941

It’s very hard not to wonder what everyone would have been writing and talking about in these first few days of 2020 if Australia weren’t burning and the US hadn’t killed Soleimani. Because this is all people are on about. Nobody talks about impeachment, for one thing.

It’s a shame that virtually all use the two events to reaffirm their prior positions, that they see to tweak events to reinforce their prior positions. It’s nigh impossible not to read that Trump will start a grand war, or the US will. This first article by Hassan Hassan is a rare exception.

Something else that crossed my mind: Soleimani’s death has -perhaps greatly- increased the chance that US troops will have to leave Iraq. Who would want that to happen?

• Suleimani’s Death Huge Blow To Iran’s Plans For Regional Domination (Hassan)

The killing of the Iranian general Qassem Suleimani could prove to be the most consequential US slaying of an enemy operative in recent memory. It will eclipse in its significance the killing of Osama bin Laden almost a decade ago or Abu Bakr al-Baghdadi in October. Not because it might spark another Middle East war, as many have warned, or merely because Suleimani was irreplaceable. Rather, his killing came at a time when the project he had led – to create an Iranian hegemony in the region – is facing unprecedented challenges in Iraq and Lebanon, through cross-sectarian and grassroots protests, while in Syria the project is still in its infancy. One can add to this picture a more aggressive policy adopted by the US.

Indeed, Suleimani was killed while he was trying to deal with these very challenges. His successor is unlikely to be able to complete that mission and contain the spiral of events in countries where, only a year ago, Iran declared major victories – in Syria against the rebels, in Lebanon through a Hezbollah-friendly government and in Iraq and Syria against Isis. In the short term, doomsday scenarios seem far-fetched. Neither side is interested in an outright war, even if developments over the past few years indicate that both have been caught in an unpredictable cycle of escalation and mounting tension. Crucially, nearly all the most influential public figures in Iraq, so far the main battle-space for the two powers, have called for a restrained and clear-headed response to prevent the situation in their country from spinning out of control.

These calls reduced significantly the chances for the worst-case scenario – of Iraq’s public figures mobilising impulsively and collectively against the United States in a way that might spark attacks and retaliations. Such scenarios would have made the US presence in Iraq unsustainable, at best. Grand Ayatollah Ali al-Sistani, Iraq’s most revered cleric, condemned Washington for its “flagrant aggression” but, in the same breath, he also called for restraint. What’s more, he cited the Iran-linked attack on the US embassy in Baghdad as part of a dangerous whirlwind of events that could steer Iraq into renewed chaos.

Beyond the extreme scenarios, Iran’s options for retaliation seem limited to familiar patterns of proxy and asymmetric warfare. Even Iranian officials have suggested any response to Suleimani’s killing would have to come later; foreign minister, Mohammad Javad Zarif, said that Tehran would launch “legal measures” at international level to hold the US to account. While a future response is possible, alarmism about a spiral into confrontation between Iran and the US is misplaced.

Hmmm. Yes, Trump was the first to use Twitter, social media the way he does. because they didn’t exist the way they do. Presidents, CIS etc., would use the NYT and WaPo to start wars, sell them to voters. Does any of this mean Twitter should censure Trump? Or that not doing it makes them warmongers?

• Trump Could Start A War Via Twitter; The Social Network Is OK With That (Keys)

Lost in the back-and-forth over the legality of the assassination and whatever future consequences it may hold is that Trump may be the first president to stoke, and perhaps even declare, war through the Internet. [..] Since taking office, Trump has used Twitter to antagonize North Korea, start false rumors about Russia, intimidate witnesses, harass journalists, slander political rivals and — perhaps we should have seen it coming — threaten Iran. For its part, Twitter seems okay — maybe even pleased — that Trump has selected their platform to connect directly with the public. To date, no other social media platform has been able to boast that two sitting presidents have actively used their platform with the level of tenacity seen on Twitter.

That was likely the thought in mind when Twitter responded to criticism over its selective enforcement of its own terms of service — the kind that prohibit direct harassment against a person, incitement of violence, certain slurs and other acts of malfeasance — by saying it would give greater leniency to world leaders because what they have to tweet is important for people to read. “Twitter is here to serve and help advance the global, public conversation,” a blog post published in January 2018 said. “Elected world leaders play a critical role in that conversation because of their outsized impact on our society. Blocking a world leader from Twitter or removing their controversial Tweets would hide important information people should be able to see and debate.”

Twitter goes on to argue that removing a world leader like Trump from the platform would not silence them as some would wish, but rather “hamper necessary discussion around their words and actions.” “We review Tweets by leaders within the political context that defines them, and enforce our rules accordingly,” Twitter said. So far, that enforcement has amounted to a blank check for Trump to say whatever he want with impunity, with the social network apparently figuring that whatever Trump has to say — on his personal account that he used for several years before he became president — has roots in political discourse. And, hey, it’s not like anyone has died from a president’s tweet before.

But the assassination of Gen. Soleimali at Trump’s direction changes everything. Nowhere has Trump’s trademark approach to public discourse — filterless, unhinged, often ignorant and without regard to consequence — played out more than on Twitter. Now, people are paying closer attention to what Trump has to say, particularly on Iran, and a lot of the focus is on what Trump will tweet next. Certainly among those waiting with baited breath are world leaders — allies who are trying hard to prepare for what’s ahead with virtually little advance notice and foes who are looking for any excuse to attack.

As the crisis between the United States and Iran over the killing of Gen. Soleimali intensifies, it’s not unreasonable to assume Trump will, at some point, tweet something that instigates an attack or declaration of war. When that happens, Americans will die. By choosing not to enforce its terms equitably across users and show privilege and favor to world leaders, Twitter — as a platform and as a company — will play a role in whatever comes next.

Trump alos said he wants no war with Iran. Biden and Mayor Pete are twisting like pretzels, Warren has a hard time keeping up with events.

• Sanders, Warren Want No War With Iran, Biden, Buttigieg Better-Run Wars (IC)

Warren, who faced criticism from the left for initially prefacing her alarm at the threat of “another costly war” with the statement that Suleimani was “a murderer, responsible for the deaths of thousands, including hundreds of Americans,” amplified Sanders’s anti-war message more clearly on Friday. “Donald Trump is dangerous and reckless,” she wrote. “He’s escalated crises and betrayed our partners. He’s undermined our diplomatic relationships for his own personal, political gain. We cannot allow him to drag us back into another war. We must speak out.”

Biden also criticized the killing of the general as needlessly provocative, but issued a statement that embraced the Trump administration’s argument that Suleimani, who orchestrated deadly attacks on U.S. soldiers during the post-war occupation of Iraq, “deserved to be brought to justice for his crimes against American troops.” The former vice president — who voted to authorize the use of military force in Iraq when he was still in the Senate, and later authored a bizarre plan to partition the country along ethnic and sectarian lines — was critical mainly of what he called Trump’s failure to explain his “strategy and plan to keep safe our troops and embassy personnel” and Trump’s lack of a “long-term vision” for the U.S. military’s role in the region.

Warren, who faced criticism from the left for initially prefacing her alarm at the threat of “another costly war” with the statement that Suleimani was “a murderer, responsible for the deaths of thousands, including hundreds of Americans,” amplified Sanders’s anti-war message more clearly on Friday. “Donald Trump is dangerous and reckless,” she wrote. “He’s escalated crises and betrayed our partners. He’s undermined our diplomatic relationships for his own personal, political gain. We cannot allow him to drag us back into another war. We must speak out.”

Biden also criticized the killing of the general as needlessly provocative, but issued a statement that embraced the Trump administration’s argument that Suleimani, who orchestrated deadly attacks on U.S. soldiers during the post-war occupation of Iraq, “deserved to be brought to justice for his crimes against American troops.” The former vice president — who voted to authorize the use of military force in Iraq when he was still in the Senate, and later authored a bizarre plan to partition the country along ethnic and sectarian lines — was critical mainly of what he called Trump’s failure to explain his “strategy and plan to keep safe our troops and embassy personnel” and Trump’s lack of a “long-term vision” for the U.S. military’s role in the region.

Propaganda is what it is.

• Lies, the Bethlehem Doctrine, and the Illegal Murder of Soleimani (Murray)

In one of the series of blatant lies the USA has told to justify the assassination of Soleimani, Mike Pompeo said that Soleimani was killed because he was planning “Imminent attacks” on US citizens. It is a careful choice of word. Pompeo is specifically referring to the Bethlehem Doctrine of Pre-Emptive Self Defence. Developed by Daniel Bethlehem when Legal Adviser to first Netanyahu’s government and then Blair’s, the Bethlehem Doctrine is that states have a right of “pre-emptive self-defence” against “imminent” attack. That is something most people, and most international law experts and judges, would accept. Including me.

What very few people, and almost no international lawyers, accept is the key to the Bethlehem Doctrine – that here “Imminent” – the word used so carefully by Pompeo – does not need to have its normal meanings of either “soon” or “about to happen”. An attack may be deemed “imminent”, according to the Bethlehem Doctrine, even if you know no details of it or when it might occur. [..] The truth of the matter is that if you take every American killed including and since 9/11, in the resultant Middle East related wars, conflicts and terrorist acts, well over 90% of them have been killed by Sunni Muslims financed and supported out of Saudi Arabia and its gulf satellites, and less than 10% of those Americans have been killed by Shia Muslims tied to Iran.

This is a horribly inconvenient fact for US administrations which, regardless of party, are beholden to Saudi Arabia and its money. It is, the USA affirms, the Sunnis who are the allies and the Shias who are the enemy. Yet every journalist or aid worker hostage who has been horribly beheaded or otherwise executed has been murdered by a Sunni, every jihadist terrorist attack in the USA itself, including 9/11, has been exclusively Sunni, the Benghazi attack was by Sunnis, Isil are Sunni, Al Nusra are Sunni, the Taliban are Sunni and the vast majority of US troops killed in the region are killed by Sunnis.

Precisely which are these hundreds of deaths for which the Shia forces of Soleimani were responsible? Is there a list? It is of course a simple lie. Its tenuous connection with truth relates to the Pentagon’s estimate – suspiciously upped repeatedly since Iran became the designated enemy – that back during the invasion of Iraq itself, 83% of US troop deaths were at the hands of Sunni resistance and 17% of of US troop deaths were at the hands of Shia resistance, that is 603 troops. All the latter are now lain at the door of Soleimani, remarkably.

“One short week ago, for example, Iran launched its first joint naval exercises with Russia and China in the Gulf of Oman, in an unprecedented challenge to the U.S. in the region.”

• Doubling Down Into Yet Another ‘March of Folly,’ This Time on Iran (VIPS)

MEMORANDUM FOR: The President FROM: Veteran Intelligence Professionals for Sanity (VIPS) SUBJECT: Doubling Down Into Another “March of Folly”?

The drone assassination in Iraq of Iranian Quds Force commander General Qassem Soleimani evokes memory of the assassination of Austrian Archduke Ferdinand in June 1914, which led to World War I. Iran’s Supreme Leader Ayatollah Ali Khamenei was quick to warn of “severe revenge.” That Iran will retaliate at a time and place of its choosing is a near certainty. And escalation into World War III is no longer just a remote possibility, particularly given the multitude of vulnerable targets offered by our large military footprint in the region and in nearby waters. What your advisers may have avoided telling you is that Iran has not been isolated. Quite the contrary. One short week ago, for example, Iran launched its first joint naval exercises with Russia and China in the Gulf of Oman, in an unprecedented challenge to the U.S. in the region.

Cui Bono? It is time to call a spade a spade. The country expecting to benefit most from hostilities between Iran and the U.S. is Israel (with Saudi Arabia in second place). As you no doubt are aware, Prime Minister Benjamin Netanyahu is fighting for his political life. He continues to await from you the kind of gift that keeps giving. Likewise, it appears that you, your son-in-law, and other myopic pro-Israel advisers are as susceptible to the influence of Israeli prime ministers as was former President George W. Bush. Some commentators are citing your taking personal responsibility for providing Iran with a casus belli as unfathomable. Looking back just a decade or so, we see a readily distinguishable pattern.

Former Israeli Prime Minister Ariel Sharon payed a huge role in getting George W. Bush to destroy Saddam Hussein’s Iraq. Usually taciturn, Gen. Brent Scowcroft, national security adviser to Presidents Gerald Ford and George H.W. Bush, warned in August 2002 that “U.S. action against Iraq … could turn the whole region into a cauldron.” Bush paid no heed, prompting Scowcroft to explain in Oct. 2004 to The Financial Times that former Israeli Prime Minister Ariel Sharon had George W. Bush “mesmerized”; that Sharon has him “wrapped around his little finger.” (Scowcroft was promptly relieved of his duties as chair of the prestigious President’s Foreign Intelligence Advisory Board.)

In Sept. 2002, well before the attack on Iraq, Philip Zelikow, who was Executive Secretary of the 9/11 Commission, stated publicly in a moment of unusual candor, “The ‘real threat’ from Iraq was not a threat to the United States. The unstated threat was the threat against Israel.” Zelikow did not explain how Iraq (or Iran), with zero nuclear weapons, would not be deterred from attacking Israel, which had a couple of hundred such weapons.

Guess who the main Democratic donors are. Except for Bernie and Warren, but she’s already in funding trouble.

• To Stop Trump’s War with Iran, We Must Also Confront the Democrats (ITT)

Since President Trump took office in 2017, the leadership of the Democratic Party has overwhelmingly supported the precursors to today’s dangerous U.S. escalation towards Iran: sanctions, proxy battles and a bloated military budget. Yet, now that we stand on the brink of a possible U.S. war of aggression, Democratic leaders are feigning concern that Trump is leading a march to war without congressional approval, and using a faulty strategy to do so. These objections, however, are grounded in process critiques, rather than moral opposition—and belie Democrats’ role in helping lay the groundwork for the growing confrontation.

The U.S. drone assassination of Maj. Gen. Qassim Suleimani, the commander of Iran’s Quds Force and a ranking official of the Iranian government, takes confrontation with Iran to new heights, inching the U.S. closer to the war the Trump administration has been pushing for. While Trump deserves blame for driving this dangerous escalation, he did not do it on his own.

As recently as December 2019, the House overwhelmingly passed the National Defense Authorization Act (NDAA) for Fiscal Year 2020 with a vote of 377-48. Two amendments were stripped from that bill before it went to a vote: Rep. Ro Khanna’s (D-Calif.) amendment to block funding for a war with Iran barring congressional approval and Rep. Barbara Lee’s (D-Calif.) amendment to repeal 2001’s “Authorization for Use of Military Force Against Terrorists” (AUMF). That AUMF effectively allows the government to use “necessary and appropriate force” against anyone suspected of being connected to the 9/11 attacks, and has been interpreted broadly to justify U.S. aggression around the world. Officials from the Trump administration have suggested that the 2001 AUMF may give them authority to go to war with Iran.

Of the 377 Representatives who voted for the $738 billion defense bill, 188 were Democrats. Just 41 Democrats opposed the legislation. The bill cleared the Senate with a tally of 86-8, with just four Democrats voting against it. None of the Senators running for the 2020 Democratic nomination were present for the vote. Before the vote, Sen. Majority Leader Mitch McConnell (R-Ky.) took to the Senate floor to brag about the fact that “partisan demands” had effectively been removed from the bill and declared that “sanity and progress” had won out. “Reassuringly, the past few days have finally brought an end to bipartisan talks and produced a compromise NDAA,” said McConnell.

Talk about propaganda. Hollow words.

• PBOC Says Will Keep Monetary Policy Prudent, Flexible And Appropriate (R.)

China will keep monetary policy prudent, flexible and appropriate, and continue to deepen financial reforms, the central bank said on Sunday, reiterating previous policy statements. After a work meeting chaired by People’s Bank of China Governor Yi Gang, the central bank also vowed to prevent any financial crisis, and said it would continue to help small companies seeking financing, according to a statement posted on PBOC’s website. It also said it will continue to let market play a decisive role in the currency exchange rate, but would keep the yuan exchange rate stable within a reasonable range. China’s economic growth cooled to a near 30-year low of 6% in the third quarter, but is expected to meet the government’s full-year 2019 target of 6%-6.5%. The PBOC on Wednesday cut the amount of cash that banks must hold as reserves for the eighth time in nearly two years…

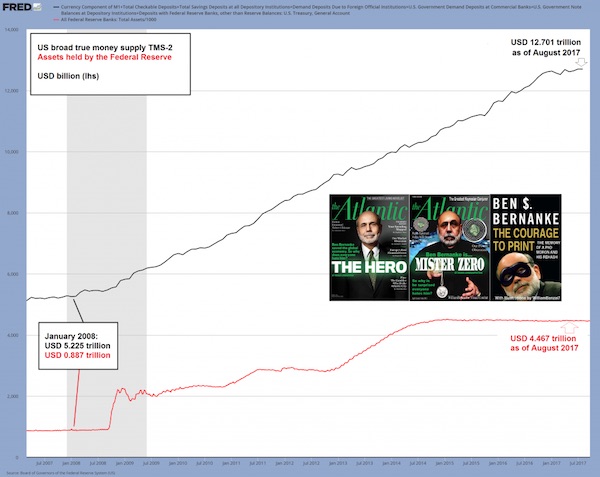

And there’s more where that came from. The rate cuts Bernanke once labeled “uncharted territory”, he now calls “conventional”.

• Bernanke: Fed Has Ample Clout To Fight Downturn If Toolkit Used Properly (R.)

The U.S. Federal Reserve still has enough clout to fight a future downturn, but policymakers should state in advance the mix of policies and policy promises they plan to use to get the most bang for their buck, former Fed chief Ben Bernanke said on Saturday. In an address to the American Economics Association, Bernanke pushed back on the notion that central banks have lost influence over the economy, and laid out his thoughts about how the Fed in particular could change its monetary policy “framework” to be sure that is not the case. Citing new research of his own and others at the Fed and elsewhere, Bernanke said the bondbuying programs known as “quantitative easing” were effective in lowering long-term interest rates even after the Fed’s target policy rate had been cut to zero.

Several rounds of QE were rolled out in response to the deep 2007-2009 financial crisis and recession, and Bernanke said bondbuying should be made a permanent part of the U.S. central bank’s toolkit. Similarly, “forward guidance,” or promises about future policy, proved effective particularly as those pledges became more specific and tied to particular goals like reaching a certain level of unemployment. “Forward guidance in the next downturn will be more effective – better understood, better anticipated, and more credible – if it is part of a policy framework clearly articulated in advance,” Bernanke said. “Both QE and forward guidance should be part of the standard toolkit going forward.” “The room available for conventional rate cuts is much smaller than in the past,” Bernanke said, but “the new policy tools are effective.”

You can talk about the Framers all you want, but the country has changed a lot since them.

• How the Two-Party System Broke the Constitution (Atlantic)

From the mid-1960s through the mid-’90s, American politics had something more like a four-party system, with liberal Democrats and conservative Republicans alongside liberal Republicans and conservative Democrats. Conservative Mississippi Democrats and liberal New York Democrats might have disagreed more than they agreed in Congress, but they could still get elected on local brands. You could have once said the same thing about liberal Vermont Republicans and conservative Kansas Republicans. Depending on the issue, different coalitions were possible, which allowed for the kind of fluid bargaining the constitutional system requires.

But that was before American politics became fully nationalized, a phenomenon that happened over several decades, powered in large part by a slow-moving post-civil-rights realignment of the two parties. National politics transformed from a compromise-oriented squabble over government spending into a zero-sum moral conflict over national culture and identity. As the conflict sharpened, the parties changed what they stood for. And as the parties changed, the conflict sharpened further. Liberal Republicans and conservative Democrats went extinct. The four-party system collapsed into just two parties.

The Democrats, the party of diversity and cosmopolitan values, came to dominate in cities but disappeared from the exurbs. And the Republicans, the party of traditional values and white, Christian identity, fled the cities and flourished in the exurbs. Partisan social bubbles began to grow, and congressional districts became more distinctly one party or the other. As a result, primaries, not general elections, determine the victor in many districts.

Nice find, dark humor.

• Bushfire Turns Aussie Sky Into A Re-Creation Of The Aboriginal Flag (DMA)

An amazing photo taken by a woman as fires raged nearby seemed to mimic the Aboriginal flag. South Australian woman Rose Fletcher took the photo at Victor Harbour as the sun rose on New Year’s Day when fires near her home were at their worst. ‘It was taken on New Year’s Day, just after sunrise, when the fires were arguably at their worst, and hearts were heavy and people were frightened – me included,’ Mrs Fletcher told Daily Mail Australia. ‘The rising sun was just a pale disc behind the layers of smoke over the Southern Ocean – and then, for just a few magic seconds, as it moved up through successively dense layers, it formed the Aboriginal flag.’

Towns on Australia’s east coast have been plunged into darkness in the middle of the day recently, while others have witnessed the sky turn apocolyptic red as the fire front approached. At least 24 people have died so far and dozens more are still missing so far this fire season. Authorities predict that number will rise. In addition to the death toll, more than 1,500 homes and four million hectares of land have been wiped out. More than 500 million animals are feared to have perished. Ms Fletcher said she recognised right away the power of the image and immediately went home to share it. ‘So I went home and put it up on Facebook, hoping that those moments would speak to other people as they spoke to me, and the rest is history,’ she said.

Include the Automatic Earth in your 2020 charity list. Support us on Paypal and Patreon.