Jackson Pollock Pasiphae 1943

PCR short and to the point. And don’t you ever forget it.

• House of Cards (Paul Craig Roberts)

Despite unrealistic plots and weak characterization (except for Francis Urquhart), Michael Dobbs’ books, House of Cards, Play the King, and The Final Cut were best sellers that provided the basis for a long-running TV series. I haven’t seen the films, but I have read the books. I conclude that plot and characters are mere props for the didactic lesson of the novels: Democratic politics is concerned only with power and sex. Nothing else is in the picture. There is no such thing as a politician concerned with the people’s well being or capable of marital fidelity.

The media are as bad as the politicians. Female journalists use their bodies for access to power and become accomplices in political intrigues. Idealism is merely another vehicle used in the competition for power. I suspect the novels and TV series were popular because they expose politics for what it is. Politics serves only personal ambition. This is a lesson that liberals and progressives, who present government as a public-spirited alternative to private greed, need to learn. In showing politics in service to personal ambition, Dobbs is a master of truth despite his shortcoming as a novelist.

Yeah, the future of the world depends on the definition of “tight”. Do you buy it?

• Deeply Flawed Western Economic Models Undermine Worst Recovery In History (CNBC)

The Western economic system is deeply flawed with countries such as the U.S. and Britain contributing to the lowest quality economic recovery the world has ever seen, Chris Watling, chief executive of Longview Economics, told CNBC on Friday. “The economic model is deeply flawed and the system in the west is deeply flawed, particularly in the English speaking part of the world and it needs to change,” Watling said. “I think this is undoubtedly the lowest quality economic recovery we have seen globally… full stop,” he added. The Longview Economics CEO explained that a debt-laden global economy could be vulnerable to looming interest rate hikes. The Federal Reserve is on a course to gradually increase interest rates, with financial markets expecting it to approve one more rate hike this year.

In addition, other central banks are pulling the reins on bond-buying and other liquidity programs aimed at injecting cash into their respective economies. “This is a world that is more indebted than it was before the global financial crisis in 2007, there’s no productivity growth, asset prices are very elevated, a lot of debt that corporates have built up has gone to share buy backs (and) the number of ‘zombie companies’ has doubled since 2007,” Longview Economics’ CEO explained. In the U.S. alone, households have $14.9 trillion in debt while businesses owe $13.7 trillion, according to the Federal Reserve.

Bond guru Bill Gross also warned that the course of global central banks toward tightening policy could be detrimental for the economic recovery. He argued that raising interest rates would increase the cost of short-term debt that corporations and individuals currently hold. When asked whether an imperfect system constituted a clear and present danger for the financial markets, Watling replied, “Whatever you want to call it doesn’t really matter but these sorts of things always unwind when you tighten money. The problem is judging what is tight? And that is sort of the million dollar question.”

What are shorts worth in a world without price discovery? Shorts are there to chase off zombies. But central banks keep them alive.

• Short Sellers Give Up as Stocks Run to New Records (WSJ)

Times are tough for skeptics of the bull market. Flummoxed by the endurance of a 2017 rally that produced its 27th S&P 500 record this week, investors are backing off bets that major indexes are headed downward. Bets against the SPDR S&P 500 exchange-traded fund, the largest ETF tracking the broad index, fell to $38.9 billion last week, the lowest level of short interest since May 2013, and remained near those levels this week, according to financial-analytics firm S3 Partners. Short sellers borrow shares and sell them, expecting to repurchase them at lower prices and collect the difference as profit. Bearish investors say they are scaling back on these bets not because their view of the market has fundamentally changed, but because it is difficult to stick to a money-losing strategy when it seems stocks can only go up.

They believe the market moves are at odds with an economy that remains lukewarm as it enters its ninth year of growth, stock valuations that are historically high and a delay of business-friendly policies in Washington like tax cuts and infrastructure spending. “There seems to be an overall view that people are invincible, that things will always go up, that there are no risks and no matter what goes on, no matter what foolishness is in play, people don’t care,” said Marc Cohodes, whose hedge fund focused on shorting stocks closed in 2008. Mr. Cohodes is now a chicken farmer based in California who is looking to get into goat herding in Canada. He shorts a handful of individual stocks personally, but isn’t focused on the broader market.

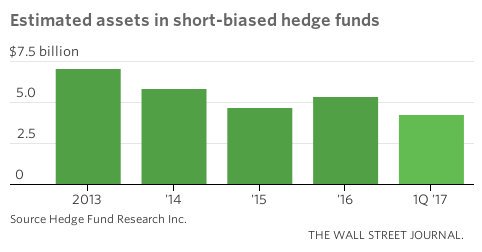

[..] The practice of shorting companies is also going by the wayside as stocks continue to notch records. Short-biased hedge funds had $4.3 billion in assets at the end of March, down from $7.1 billion at the end of 2013, according to HFR Inc. The difficulty for stock-market bears stems from a Goldilocks-like market environment, in which the economy is expanding fast enough to support corporate earnings, but slow enough for the Federal Reserve to keep rates relatively low. Years of low rates and easy-money policies have boosted stocks, defying forecasts for a steep, prolonged downturn. “The shorts have been frustrated now for quite a while,” said Scott Minerd, global chief investment officer at Guggenheim Partners, which has $260 billion in assets under management. The scenarios that might lead to a payout for market bears—an economic recession or a sharp rise in interest rates—don’t seem imminent, either, Mr. Minerd added.

Sure, I believe you.

• Greed Is No Longer Good – Bond Boom Comes To An End (G.)

City bond traders have put the champagne on ice. They had a good run. For some it lasted almost a year. But it’s over now and the “new normal” of low trading volumes and weak profits is reasserting itself. On Wall Street, Goldman Sachs took the biggest hit. This week the firm reported profits had plunged 40% in the second quarter on its bond, currency and commodities trading desks. All the other big names in the US investment banking world saw bond trading profits dive in the three months to the end of June, save for age-old Goldman rival Morgan Stanley, which restricted the loss to 4%. Lloyd Blankfein, the Goldman boss who rose through the ranks of bond traders to the top job, was unlikely to be sanguine about the turn of events amid concerns that his bank suffered more than most for relying on out-of-favour hedge funds as clients.

Back in October 2016 the story was very different. Barclays was on a high after what it said was a summer bonanza for its bond traders, pushing quarterly profits to a two-year high. Likewise Goldman, Deutsche Bank, Bank of America and JPMorgan were raking in the trades. Much of the reason for their optimism was a change of stance at the Federal Reserve. The US central bank signalled in late 2015 that the post-crash era of low inflation and low interest rates was coming to an end. To combat the threat of inflation, it would start to raise rates consistently through 2016 and 2017. This move put two trends in motion that spelled a big payday for the banks. First, the price of bonds started to fall, making them more attractive to buy. Second, not long afterwards, it became clear the other central banks were not going to follow suit in raising rates.

That broke seven years of agreement among the major central banks to hold interest rates at near zero as a way to boost economic activity. The Bank of England, the European Central Bank and the Bank of Japan were still on board, but Janet Yellen at the Fed had broken away. Without a consistent story, investors in fixed-income securities, the jargon name for bonds, found themselves needing to back several horses. And investors demanded the banks buy and sell their securities more frequently as uncertainty translated into an ever-changing mood in the market. The main measure of volatility – the Vix index – was still well below the 2009 peak, but it was elevated in 2016. And traders make money in periods when uncertainty and confusion raise levels of volatility.

Thomas Frank (re-)writes my article from a few weeks ago, Feeding Frenzy in the Echo Chamber.

• The Media’s War On Trump Is Destined To Fail. Why Can’t It See That? (Frank)

These are the worst of times for the American news media, but they are also the best. The newspaper industry as a whole has been dying slowly for years, as the pathetic tale of the once-mighty Chicago Tribune reminds us. But for the handful of well funded journalistic enterprises that survive, the Trump era is turning out to be a “golden age” – a time of high purpose and moral vindication. The people of the respectable east coast press loathe the president with an amazing unanimity. They are obsessed with documenting his bad taste, with finding faults in his stupid tweets, with nailing him and his associates for this Russian scandal and that one. They outwit the simple-minded billionaire. They find the devastating scoops. The op-ed pages come to resemble Democratic fundraising pitches. The news sections are all Trump all the time. They have gone ballistic so many times the public now yawns when it sees their rockets lifting off.

A recent Alternet article I read was composed of nothing but mean quotes about Trump, some of them literary and high-flown, some of them low-down and cruel, most of them drawn from the mainstream media and all of them hilarious. As I write this, four of the five most-read stories on the Washington Post website are about Trump; indeed (if memory serves), he has dominated this particular metric for at least a year. And why not? Trump certainly has it coming. He is obviously incompetent, innocent of the most basic knowledge about how government functions. His views are repugnant. His advisers are fools. He appears to be dallying with obviously dangerous forces. And thanks to the wipeout of the Democratic party, there is no really powerful institutional check on the president’s power, which means that the press must step up.

But there’s something wrong with it all. The news media’s alarms about Trump have been shrieking at high C for more than a year. It was in January of 2016 that the Huffington Post began appending a denunciation of Trump as a “serial liar, rampant xenophobe, racist, birther and bully” to every single story about the man. It was last August that the New York Times published an essay approving of the profession’s collective understanding of Trump as a political mutation – an unacceptable deviation from the two-party norm – that journalists must cleanse from the political mainstream. It hasn’t worked. They correct and denounce; they cluck and deride and Trump seems to bask in it. He reflects this incredible outpouring of disapprobation right back at the press itself.

Contemplating the horrors of bankers leaving your society.

• Goldman Sachs Boss Urges Long Brexit Transition. Is Anyone Listening? (Ind.)

I’ve no fondness for wealthy bankers, but that doesn’t mean to say they aren’t sometimes right. An example of that is Goldman Sachs International chief executive Richard Gnodde, who has just entered the Brexit debate to urge a “significant” transition period. Mr Gnodde is currently pouring money down a bottomless pit labelled “Brexit Contingency Plans”. There aren’t many Britons who will feel all that much sympathy for him over that. That money pit will mean less is available for the bonuses he and his colleagues are so fond of. So tough luck. Trouble is, his masters in New York won’t see it that way. They will eventually say that’s enough of that, start moving your people over to Frankfurt. Actually, the process has already begun. Some jobs are moving over to Germany.

Still more are simply staying in New York, which, for all the scrambling being done by Frankfurt, and Paris, and Dublin, has quietly become the biggest winner from this whole sorry affair. There are many who would shrug some more. What do we lose by inconveniencing a few thousand wealthy bankers anyway. They don’t exactly contribute much to society. Well, they pay a lot of tax for starters. It’s also true that they should pay more. But that’s just another debate. Despite that, I have for years argued that London’s financial centre has played too central a role in the nation’s economy, and that it would be a good idea for the Government to pursue a more balanced economic approach rather than coddling it (as it did until recently).

The trouble is it is now happening at a dangerously fast pace and it is impossible to see, as things stand, quite what is going to replace those tax revenues, which contribute to things like the NHS, schools, roads without potholes, and any number of other things. There are also a lot of support staff who work for banks like Goldman in the City. They’re not rich, by any means, and they’re unlikely to be able to move like the bankers so they’ll just lose their jobs. If it’s unpalatable hearing about this from Mr Gnodde – as it will be to an awful lot of people – consider also that the CBI has said much the same thing as have most sensible, and even semi-sensible, businesses both in the square mile of the City of London and beyond.

Everyone walks. Yawn.

• US To Drop Criminal Charges In ‘London Whale’ Case (R.)

U.S. prosecutors have decided to drop criminal charges against two former JPMorgan Chase derivatives traders implicated in the “London Whale” trading scandal that caused $6.2 billion of losses in 2012. In seeking the dismissal of charges against Javier Martin-Artajo and Julien Grout, the Department of Justice said it “no longer believes that it can rely on the testimony” of Bruno Iksil, a cooperating witness who had been dubbed the London Whale, based on recent statements he made that hurt the case. Prosecutors also said efforts to extradite Martin-Artajo and Grout, respectively citizens of Spain and France, to face the charges have been “unsuccessful or deemed futile.” Acting U.S. Attorney Joon Kim in Manhattan asked a federal judge for permission to drop charges that included securities fraud, wire fraud and falsifying records. Martin-Artajo and Grout were indicted in September 2013.

“After four long years of protracted litigation, we are very pleased that the government has decided to do the right thing, and dismiss the criminal case,” Grout’s lawyer, Edward Little, said. The dismissal request marks a fresh setback in U.S. efforts to prosecute individuals for financial crimes. This has included the undoing of several insider trading convictions and pleas that had been won by Kim’s predecessor Preet Bharara. It has also included this week’s overturning of the convictions of two former Rabobank NA traders for rigging the Libor interest rate benchmark. Martin-Artajo and Grout were accused of hiding hundreds of millions of dollars of losses within JPMorgan’s chief investment office (CIO) in London by marking positions in a credit derivatives portfolio at inflated prices.

At risk of, you said? Weird that if you let investors and analysts discuss this, turns out they have no idea what’s really going on. But doesn’t that cluelessness hurt their investments. their clients?

• A Third Of Greeks At Risk Of Poverty As Athens Wants Return To Bond Market

The Greek government might be preparing to return to the bond market but there are many structural problems that have yet to be resolved to make the economy more sustainable, an analyst told CNBC on Friday. Greece is currently on a third financial program since 2010, due to expire next year. According to James Athey, fixed income investment manager at Aberdeen Asset Management, despite the reforms implemented until now, “it still doesn’t seem we are particularly far down the road in solving the structural issues of Greece.” “Until the Greek economy has got a business model which works and it’s productive and it’s creating stable, secure growth that it’s not reliant on debt relief, external support and constantly bailouts from the Europeans, then it’s difficult to believe that the path is towards something more healthy rather than something less healthy,” Athey told CNBC on Friday.

The IMF agreed Thursday to make a loan of $1.8 billion to Greece as part of its current bailout program, but warned that the country will have to continue reforming in order to receive that money. Greece has to continue focusing on reducing the level of bad loans in its financial sector and extend labour market reform to liberalize Sunday trade and allow for collective dismissals, the fund said. However, with the bailout program due to end in 2018, Greece wants to come back to bond markets to show the rescue has been successful and the economy is able to fund itself. The government is studying when and how such a comeback will be more appropriate. Though Athens refuses to comment on this issue, it is widely expected that Greece will issue bonds next week.

The move is somewhat confusing given that Greek government bonds do not qualify for the ECB’s asset purchase program. They are considered junk by credit rating agencies, and thus cannot feature on the central bank’s balance sheet. When asked how Greece would convince investors to buy bonds if the ECB isn’t buying these assets, Athey said: “I don’t know.” “I guess from a Greek perspective it seems to be a window of opportunity, we’ve seen Greek yields have fallen fairly consistently throughout the year…the fact that Greece might come to market at what optically looks like an attractive yield for a Greek issuer must be tempting to them, especially considering that we are expecting the QE program to ultimately come to a conclusion over the next 6 to 12 months, they certainly would not want to wait until then,” he suggested.

Absolute fantasy predictions. That’s the only way left to sell their stories. They all want Greece back in ‘markets’ before the next bailout expires next year.

• No Surprises From IMF Report On Greek Debt (K.)

Bond markets responded calmly on Friday to the debt sustainability analysis (DSA) of the IMF, which found Greece’s debt exceptionally unsustainable, while deciding to participate in the Greek bailout program with 1.6 billion euros. The markets’ reaction allows for the government to issue the five-year bond as early as on Monday. The DSA reiterates that the eurozone’s commitments to secure the sustainability of the Greek debt are not sufficient. The IMF estimates the debt will slide to 160% of GDP in 2020 and to 150% in 230, before soaring to 190% in 2060. Servicing the debt will exceed 15% of GDP in 2028, reaching as high as 45% in 2060.

The Fund argues that the estimates of Athens and the eurozone on growth rates, primary surpluses and other parameters affecting the debt are optimistic and insists its own views are realistic, saying that Greece has historically been weak in implementing reforms and cannot support high primary surpluses for many years. It goes on to say that revenues from privatizations will not exceed €2 billion by 2030 and believes that the state will not collect any substantial funds from the sale of the bank shares it acquired in the last few share capital increases. It therefore calls on the eurozone to reach an agreement on a realistic strategy for easing Greece’s debt.

The IMF’s proposal for a new stress test on Greek banks and a fresh asset quality review were met with a clear dismissal on Friday by a ECB spokesman, who pointed to Frankfurt being the sole monitoring authority that decides on such issues. The strong ECB response was also addressed at the IMF’s estimate that Greek lenders will require fresh recapitalization to the tune of €10 billion. On Friday Standard & Poor’s stopped short of raising the country’s credit rating, affirming it at ‘B-,’ but pointed to an upcoming upgrade switching Greece’s outlook from stable into positive.

How much longer? We know there are reports.

• The Kingdom Whose Name We Dare Not Speak At All (Robert Fisk)

Theresa May has oddly declined to comment on the reported arrest of the mini-skirted lass who was videotaped cavorting through an ancient Najd village this week, provoking unexpected roars of animalistic male fury in a kingdom known for its judicial leniency, political moderation, gender equality and fraternal love for its Muslim neighbours. May should, surely, have drawn the attention of the rulers of this normally magnanimous state to the extraordinarily uncharacteristic behaviour of the so-called religious police – hitherto regarded as extras in the very same kingdom’s growing tourism industry which is supported by its newly appointed peace-loving and forward-thinking young Crown Prince.

But of course, since May cannot possibly believe that a single person in this particular national entity would give even a riyal or a halfpenny to “terrorists” – of the kind who have been tearing young British lives apart in Manchester and London – she’s hardly likely to endanger the “national security” of said state by condemning the arrest of the aforementioned young lady. In any event, a woman so proper that she would not risk soiling her hands by greeting the distraught survivors of the Grenfell Tower fire has no business shedding even a “little tear” for middle class girls who upset what we must now call The Kingdom Whose Name We Dare Not Speak At All. Or at least, we do not dare to speak its name.

It’s now a week since this extraordinary woman – our beloved May, not the cutie of Najd – declined to publish perhaps the most important, revelatory document in the history of modern “terrorism” on the grounds that to identify the men who are funding the killers running Isis, al-Qaeda, al-Nusrah and sundry other chaps, would endanger “national security”. Note that Amber Rudd, May’s amanuensis, intriguingly declined to specify whose “national security” was at risk. Ours? Or that of The Kingdom Whose Name We Dare Not Speak At All – henceforth, for brevity’s sake, the KSA – which must surely be well aware which of its illustrious citizens (peace-loving, moderate, gender-equalised, etc) have been sending their lolly to the Isis lads.

If you read carefully, you see that it’s all been a mess for many years. The only difference is Trump doesn’t try to hide that.

• EPA Will Allow Fracking Waste Dumping in the Gulf of Mexico (TO)

As the Trump administration moves to gut Obama-era clean water protections nationwide, an environmental group is warning the Environmental Protection Agency (EPA) that its draft pollution discharge permit for offshore drilling platforms in the Gulf of Mexico violates clean water laws because it allows operators to dump fracking chemicals and large volumes of drilling wastewater directly into the Gulf. In a recent letter to the agency, the Center for Biological Diversity told the EPA that the dumping of drilling wastewater – which can contain fracking chemicals, drilling fluids and pollutants, such as heavy metals – directly into Gulf waters is unacceptable and prohibited under the Clean Water Act.

Under current rules established by the Obama administration, offshore oil and gas platforms can discharge well-treatment chemicals and unlimited amounts of “produced waters” from undersea wells directly into the Gulf as long as operators perform toxicity tests a few times a year and monitor for “sheens” on the water’s surface. About 75 billion gallons of produced water were dumped in the Gulf in 2014 alone, according to EPA records. Offshore fracking, which typically involves injecting water and chemicals at high pressure into undersea wells to improve the flow of oil and gas, has rapidly expanded in the Gulf of Mexico over the past decade.

The latest draft of the pollution discharge permit, which was largely prepared under the Obama administration, would require drillers to collect information on the fracking chemicals they dump overboard. Regulators want to know what these chemicals are; their catalogue of offshore fracking chemicals has not been updated since 2001, despite advancements in technology.

Here’s real collusion for you: “special committees of up to 200 employees”. It wasn’t just software, they also agreed to use too small versions of the ‘tanks’ that clean emissions. Now VW is talking, trying to get its own fines diminished.

Oh, and you think nobody in government ever knew about this? Prediction: Merkel will push EU into lower fines. Prediction 2: they will comply.

• German Carmakers Colluded On Diesel Emissions For Decades (Qz)

German magazine Der Spiegel reports that the country’s powerful automakers have been meeting in secret since the 1990s—and their joint decisions on dealing with diesel emissions may have laid the groundwork for Volkswagen’s massive emissions-cheating scandal. According to Der Spiegel, VW admitted to German authorities that it may have engaged in “anti-competitive behavior” with rivals BMW and Daimler via special committees of up to 200 employees that set prices, agreed on suppliers, and engaged in other forms of coordination. One major topic of the meetings was how to manage emissions from diesel engines. The result, as we now know in Volkswagen’s case, was the installation of emissions-cheating software, which was uncovered by American regulators in 2015 and has cost the automaker dearly since.

Daimler tried to get ahead of things this week by recalling 3 million diesel vehicles in Europe for a free emissions-system alteration. Audi followed suit today, with a similar offer to “improve emissions behavior” for 850,000 cars. Spiegel says that German regulators discovered signs of an illegal agreement between the automakers this summer, when they were investigating Volkswagen on suspicion that carmakers were fixing the price of steel. Volkswagen, Daimler, and BMW declined to comment on the Spiegel report, with the latter two calling it “speculation.” Germany’s automakers are anxious as a backlash against diesel motors gathers pace. Several European cities—including Stuttgart, the home of Porsche—have called for a ban on diesel cars, which accounted for around 47% of cars sold in Europe’s five biggest markets in the second quarter of this year.

Nice society you got there. Britain’s way overdue for a complete make-over.

• Number Of Homeless Children In Temporary Accommodation in UK Rises 37% (G.)

Councils across England are housing the equivalent of an extra secondary school of pupils per month as the number of homeless children in temporary accommodation soars, according to local government leaders. The Local Government Association (LGA) said councils are providing temporary housing for around 120,540 children with their families – a net increase of 32,650 or 37% since the second quarter of 2014. It said the increase equates to an average of 906 extra children every month. The LGA said placements in temporary accommodation can present serious challenges for families, from parents’ employment and health to children’s ability to focus on school studies and form friendships. The LGA, which represents 350 councils across England, said the extra demand is increasing the pressure on local government.

It said councils need to be able to build more “genuinely affordable” homes and provide the support that reduces the risk of homelessness. This means councils being able to borrow to build and to keep 100% of the receipts of any home they sell to reinvest in new and existing housing, the LGA said. Council leaders are also calling for access to funding to provide settled accommodation for families that become homeless. Martin Tett, the LGA’s housing spokesman, said: “When councils are having to house the equivalent of an extra secondary school’s worth of pupils every month, and the net cost for councils of funding for temporary accommodation has tripled in the last three years, it’s clear the current situation is unsustainable for councils, and disruptive for families.

“Councils are working hard to tackle homelessness, with some truly innovative work around the country – and we now need the Government to support this local effort by allowing councils to invest in building genuinely affordable homes, and taking steps to adapt welfare reforms to ensure housing remains affordable for low-income families.”

EU policies bring the vermin our of the woodwork.

• Sicilian Mayor Moves To Block Far-Right Plan To Disrupt Migrant Rescues (G.)

A Sicilian mayor is seeking to block a ship chartered by a group of far-right activists attempting to disrupt migrant rescues in the Mediterranean. Enzo Bianco, the mayor of Catania, has urged authorities in the port city on the island’s east coast to deny docking rights to C-Star, a 40-metre vessel hired by Generation Identity, a movement made up of young, anti-Islam and anti-immigration activists from across Europe, for its sea mission to stop migrants entering Europe from Libya. The ship is expected to arrive on Saturday, and the group intends to launch its mission next week. “I’ve told [the relevant] authorities that allowing the ship to dock in our port would be very dangerous for public order,” Bianco said in a statement to the Guardian.

“I also consider it to be a provocation by those involved, with their sole purpose being to fuel conflict by pouring fuel on the fire.” Under a vigilante scheme called “Defend Europe”, the activists crowdfunded more than €75,000 (£67,000) to hire the boat. In a “trial run” two months ago, the ship successfully intercepted a charity rescue ship off Sicily. The activists’ aim is to expose what they claim to be wrongdoing by “criminal” NGO search and rescue vessels, which they accuse of working with people smugglers to transport illegal immigrants to Europe. They also plan to disrupt the work of the crews by calling the Libyan coastguard and asking them to take migrants and refugees attempting to cross the Mediterranean back to war-torn Libya.

Anti-racism groups across Sicily have also urged authorities to take action against the group, to prevent them interfering in the life-saving missions. “Sicily is a place where every family has an emigration story,” Bianco said. “In recent years we have welcomed thousands of people fleeing from war and hunger, people who were saved from dying in the Mediterranean by European vessels, and those who have lost one or more family members crossing the sea. Talking about ‘defending Europe’ is not just demagogic, it’s unworthy.”

“Long dormant spores of the highly infectious anthrax bacteria frozen in the carcass of an infected reindeer rejuvenated themselves and infected herds of reindeer and eventually local people.”

• All Hell Breaks Loose As The Tundra Thaws (G.)

Strange things have been happening in the frozen tundra of northern Siberia. Last August a boy died of anthrax in the remote Yamal Peninsula, and 20 other infected people were treated and survived. Anthrax hadn’t been seen in the region for 75 years, and it’s thought the recent outbreak followed an intense heatwave in Siberia, temperatures reaching over 30C that melted the frozen permafrost. Long dormant spores of the highly infectious anthrax bacteria frozen in the carcass of an infected reindeer rejuvenated themselves and infected herds of reindeer and eventually local people. More recently, a huge explosion was heard in June in the Yamal Peninsula. Reindeer herders camped nearby saw flames shooting up with pillars of smoke and found a large crater left in the ground.

Melting permafrost was again suspected, thawing out dead vegetation and erupting in a blowout of highly flammable methane gas. Over the past three years, 14 other giant craters have been found in the region, some of them truly massive – the first one discovered was around 50m (160ft) wide and about 70m (230ft) deep, with steep sides and debris spread all around. There have also been cases of the ground trembling in Siberia as bubbles of methane trapped below the surface set the ground wobbling like an airbed. Even more dramatic, setting fire to methane released from frozen lakes in both Siberia and Alaska causes some impressive flames to erupt. Methane is of huge concern. It is more than 20 times more potent a greenhouse gas than carbon dioxide, and a massive release of methane in the Arctic could pose a significant threat to the global climate, driving worldwide temperatures even higher.