Johannes Vermeer View of Delft 1660-61

https://twitter.com/MAGAVoice/status/1941219409860887018

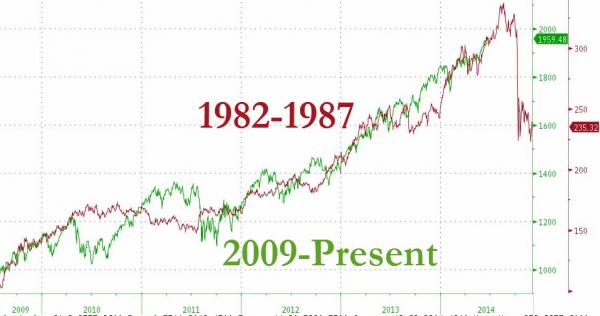

Stone

These people orchestrated the single greatest abuse of power in American history-the Russian collusion hoax. When are they going to prison? pic.twitter.com/s0294a9V10

— Roger Stone (@RogerJStoneJr) July 4, 2025

RFK

. @RobertKennedyJr is right. pic.twitter.com/WTTXfbol03

— Died Suddenly (@DiedSuddenly_) July 5, 2025

— David Wolfe (@DavidWolfe) July 5, 2025

Scott

Why are only Western countries expected to have open borders?@ScottAdamsSays: “It’s basically English-speaking, white countries that are being asked to destroy themselves with unlimited immigration.”

Watch the video for his full take! pic.twitter.com/zL9HZCa4as

— jay plemons (@jayplemons) July 4, 2025

“The goal of the operation was to “prevent the Iranians from building a nuclear weapon in the near term – a year or so – with the hope they would not try again,”

• Iran Moved Its Enriched Uranium Before US Strikes – Seymour Hersh (RT)

Last month’s US strikes on Iran’s nuclear facilities failed to hit the country’s stockpile of highly enriched uranium, Pulitzer Prize-winning journalist Seymour Hersh has claimed, citing US officials. The attack, which involved seven US B-2 ‘Spirit’ bombers carrying 30,000-pound bunker busters, was not even expected to “obliterate” the Iranian nuclear program, one of the journalist’s sources admitted. “The centrifuges may have survived and 400 pounds of 60% enriched uranium are missing,” one of the officials said, adding that the US bombs “could not be assured to penetrate the centrifuge chamber . . . too deep.”

The lack of radioactivity at the targeted Iranian nuclear sites – specifically Fordow and Isfahan – following the attack suggest that the enriched uranium stockpile had been moved ahead of time, one US official familiar with the matter said. Fordow, an underground complex built deep inside a mountain that many believed housed the stockpiles, was a particular focus of the attack.

The US officials cited by Hersh nevertheless believe that the location of the stockpile and its fate are “irrelevant” because of the serious damage the strike allegedly dealt to another Iranian nuclear site near the city of Isfahan. The goal of the operation was to “prevent the Iranians from building a nuclear weapon in the near term – a year or so – with the hope they would not try again,” a US official told Hersh. This could translate into “a couple of years of respite and uncertain future,” the official added. Following the strikes, US President Donald Trump claimed that the attack “completely and totally obliterated” Iran’s nuclear program. CIA Director John Ratcliffe also told lawmakers that several key sites had been completely destroyed and would take years to rebuild.

However, intercepted communications suggested that Tehran had expected a worse impact from the strikes and that the real damage was limited, the Washington Post reported. The strikes were part of a coordinated American-Israeli military campaign launched in mid-June. The Israel Defense Force bombed Iranian targets, claiming that Tehran was close to being able to build a nuclear weapon. Hersh believes that Israel was the “immediate beneficiary” of the US strike. West Jerusalem does not officially acknowledge possessing nuclear weapons. The Jewish State may still have up to 90 nuclear warheads at its disposal, according to a recent report by the Stockholm International Peace Research Institute (SIPRI).

The two-party system is very well protected.

• Musk Unveils ‘America Party’ To Challenge ‘One-Party System’ (ZH)

One day after his latest poll asking his followers on X whether the USA needs a new political party, Elon Musk announced on Saturday that the “America party has formed.” “By a factor of 2 to 1, you want a new political party and you shall have it!” Musk wrote. “Today, the America Party is formed to give you back your freedom.” The announcement comes after 1,248,856 people voted ‘yes’ to whether he should “create the America Party.”

Independence Day is the perfect time to ask if you want independence from the two-party (some would say uniparty) system!

Should we create the America Party?

— Elon Musk (@elonmusk) July 4, 2025

The announcement comes one day after President Donald Trump signed his signature tax and spending bill, which Musk has vehemently opposed for weeks, and which resulted in a very public falling out with Trump – whose campaign Musk spent hundreds of millions of dollars promoting. Musk also led the Department of Government Efficiency (DOGE), which found billions of dollars in waste, fraud and abuse – virtually none of which was included in Trump’s so-called “Big Beautiful Bill.” While the Trump-Musk spat has simmered in recent weeks, Trump earlier this week threatened to cut off billions of dollars in subsidies to Musk’s companies.

Meanwhile, Musk foe Steve Bannon tore into the plan for a third political party – saying on his “War Room” podcast on Friday: “The foul, the buffoon. Elmo the Mook, formerly known as Elon Musk, Elmo the Mook. He’s today, in another smear, and this — only a foreigner could do this — think about it, he’s got up on, he’s got up on Twitter right now, a poll about starting an America Party, a non-American starting an America Party.” “No, brother, you’re not an American. You’re a South African and if we take enough time and prove the facts of that, you should be deported because it’s a crime of what you did — among many,” Bannon added.

The fat, drunken slob called Bannon will go back to prison and this time for a long time. He has a lifetime of crime to pay for.

— Elon Musk (@elonmusk) July 4, 2025

Musk, meanwhile, wrote on Friday that “The fat, drunken slob called Bannon will go back to prison and this time for a long time. He has a lifetime of crime to pay for.”

Trump, too, will have to realize the changed ‘realities on the ground”.

And Putin is far more than a professional; he truly loves his country. Just like Trump.

• Putin Is ‘A Professional’ – Trump (RT)

Russian President Vladimir Putin is “a professional” who has learned how to handle Western sanctions, but he understands that more could come if the Ukraine conflict is not settled, US President Donald Trump has said. Speaking to reporters aboard Air Force One on Friday, Trump confirmed that the two leaders discussed potential sanctions during Thursday’s phone call. “I would say he [Putin] is not thrilled with it, but you know, he’s been able to handle sanctions, but these are pretty biting sanctions.” The Russian president, he added, is fully aware that the US could ramp up the pressure. “You know, he’s a professional. It may be coming,” he added.

In a one-hour phone call, Putin and Trump discussed the Ukraine conflict, the volatile state of affairs in the Middle East, and Russia-US cooperation, according to Kremlin aide Yury Ushakov. Ushakov said Trump raised the issue of ending the hostilities as soon as possible, adding that while Moscow is open to finding a political solution, it will not back down from its goals, including addressing the root causes of the conflict. Later, Trump said he was “unhappy” with the lack of progress towards peace.

US lawmakers have introduced a bill that proposes a 500% tariff on imports from countries that continue to purchase Russian oil and energy products. Introduced by US Senator Lindsey Graham and backed by at least 81 senators, it also proposes extending sanctions on Russia, including its sovereign debt. Last month, Graham claimed that Trump told him “it’s time to move the bill” to a vote. At the time, Kremlin spokesman Dmitry Peskov said Graham’s views are “well known to the whole world,” adding that “he belongs to a group of inveterate Russophobes,” and that he would have imposed new sanctions on Russia long ago if he were in charge.

“Would that have helped the [Ukraine] settlement? That is a question that those who initiate such events should ask themselves,” Peskov said. The US imposed sanctions on Russia in 2014 following the start of the Ukraine crisis. After the conflict escalated in 2022, they were drastically expanded to include financial and energy sanctions, as well as asset freezes. Russian officials have described the sanctions as “illegal,” while highlighting Russia’s economic resilience, arguing that they have strengthened domestic production.

“..a remarkable display of bipartisan support for an agency plagued by mission creep that has been almost entirely left-wing..”

• Bush’s, Obama’s ‘Farewell’-Style Wishes for USAID Staff (DS)

Former Presidents George W. Bush’s and Barack Obama’s farewell messages to staffers of the U.S. Agency for International Development this week reinforce the perception that critics have called the “uniparty” culture in Washington. On Monday, the staff of USAID received video messages from the two former presidents, along with one from Bono, the ultraliberal Irish frontman of the rock band U2. Monday was the last day for foreign assistance programming by USAID, which Secretary of State Marco Rubio announced would be moved under the purview of the State Department. The former presidents and Bono spoke with thousands in the USAID community in a videoconference.

The messages were a remarkable display of bipartisan support for an agency plagued by mission creep that has been almost entirely left-wing. “You had a one-sided uniparty apparatus here [in the State Department and USAID] funding only one side of the political equation,” Max Primorac, who previously served as USAID’s chief operating officer, explained in an interview with “The Signal Sitdown” podcast in February.“You’ve shown the great strength of America through your work, and that is our good heart,” Bush said in his video message to the staff. The Republican ex-president then went on to praise the President’s Emergency Plan for AIDS Relief (PEPFAR), which he launched in 2003.

“Is it in our interest that 25 million people who would have died now live? I think it is,” Bush concluded in an apparent dig at Rubio’s emphasis on putting American interests first in the country’s foreign aid allocation at the direction of President Donald Trump, a fellow Republican. Bush’s critique of his GOP successor’s efforts at realigning PEPFAR with its stated mission is surprising, given that under Democrat President Joe Biden, the program also began to promote abortion. PEPFAR funding had even been used to perform 21 abortions in Mozambique, despite being against U.S. law, Reuters reported in January. “Ending your presence and your programs out in the world hurts the most vulnerable, and it hurts the United States,” Obama, a Democrat, said in his statement to the staff.

“If this isn’t murder, I don’t know what is,” Bono concurred. The Irish singer then subjected the gathered staff to what appeared to be an attempt at making a song about their plight. “They called you crooks—when you were the best of us, there for the rest of us. And don’t think any less of us, when politics makes a mess of us,” he rhymed. Bono was awarded the Presidential Medal of Freedom by Biden in January. At the ceremony, he was cited as having “brought together politicians from opposing parties to create the United States PEPFAR AIDS program.” A senior State Department official told The Daily Signal in February that Rubio had identified and cut almost 5,800 awards worth about $54 billion from USAID that he said didn’t fit with the core mission of protecting American interests. The State Department has already said a reformed version of PEPFAR will continue to be supported by the federal government.

“..often the best of the best in the military come from the heartland, from working on the shop floors to defending the country. They understand that the planes might have been made by a member of their community or even their family.”

• A Very Consequential 2 Weeks for Trump’s Presidency (Zito)

When the active-duty Air Force and Missouri Air National Guard bomber crews who attacked the Fordow uranium enrichment plant in Iran went to work on June 20, they kissed their loved ones goodbye, not knowing when or if they’d be home. That’s when their families became aware something was happening. “When those jets returned [to Whiteman Air Force Base in Missouri on June 22], their families were waiting, flying American flags and shedding tears of pride and relief,” said Gen. Dan Caine, the chairman of the Joint Chiefs of Staff. The jets rejoined into a formation of four, pitching out to land right over the base—a landing Caine said was greeted by incredible cheers and tears from the families who sacrifice and serve right alongside the pilots.

“One commander told me this is a moment in the lives of our families that they will never forget,” Caine said at a press conference Thursday at the Pentagon. “That, my friends, is what America’s joint force does. We think, we develop, we train, we rehearse, we test, we evaluate every single day. And when the call comes to deliver, we do so.” It was a moment of consequence, excellence, leadership, and guts. In the past 12 days, some of the most consequential decisions in American history, those that will affect generations and leave a substantial impact on our culture, economy, and political alignment, have been made either by President Donald Trump or because of him. But they have been largely either downplayed or not fully analyzed in terms of how they all connect.

The U.S. Steel deal between the iconic American company and Nippon Steel happened because of Trump’s ability to apply pressure through negotiations that sometimes bewildered everyone involved. But they led to the literal reversal of fortune of an industry, from the additional supply industries that include mechanics, construction workers, transportation systems, such as railways, and energy. The 50% tariffs Trump announced the day he visited the U.S. Steel plant in West Mifflin, Pennsylvania, were also seen by American manufacturers as a signal that Trump was committed to revitalizing American steel mills. It also signaled an overall mandate to reshore manufacturing in the country.

While much of Wall Street warned that the tariffs would cause a widespread recession, a former critic of the tariffs, Torsten Slok, chief economist at Apollo Global Management, did an about-face and wondered if Trump outsmarted everyone, laying out a scenario that keeps tariffs well below Trump’s most aggressive rates long enough to ease uncertainty.

That a steelworker or a welder working for a defense contractor would watch what happened to Iran’s nuclear program and feel a part of it is a nuance in American journalism that is often missed. Sen. David McCormick, R-Pa., told the Washington Examiner that it is an integrated story, both in terms of the consequences of those decisions, bolstering our economic capability and our independence. “But it’s a confidence in leadership story, too,” McCormick said. McCormick, who took office in January after winning against an entrenched Democrat few thought he could defeat, said the nuance of how intertwined moments such as these are is often missed. “These are reinforcing themes,” he said.

McCormick, who grew up in Bloomsburg, Pennsylvania, argues that often the best of the best in the military come from the heartland, from working on the shop floors to defending the country. They understand that the planes might have been made by a member of their community or even their family. “That is where the grit of the country lies,” McCormick said. “Of course, they see what they do as part of something bigger than self, because often people don’t understand the vitality of their profession.” McCormick, who served in the Army and was part of the 82nd Airborne Division deploying to Iraq during the Gulf War, was joined by Sen. John Fetterman, D-Pa., in praising Trump’s Iran airstrikes. McCormick said he talked to Trump about the historic strikes on June 22.

“I just called him and just said, ‘Man, so when I put boots on the ground myself personally 30 years ago, I never imagined we’d have this kind of terrorist threat, the risk of a nuclear weapon, and this kind of leadership and competence,’” McCormick said. The president told McCormick something profound about the people who were part of the operation. “The president said, ‘Those young people are magnificent.’ And I said, ‘You know what, Mr. President, the thing about them is, my heart swells when I see that kind of leadership with those 40 kids shooting the Patriots in Qatar,’” McCormick said of the soldiers fighting to intercept Iranian missiles that targeted the U.S. base at Al Udeid in Qatar. McCormick recalled that Trump said, “These are the best America has to offer, and every time I’ve interacted with them, that’s what I said.”

“President Trump didn’t just listen—he acted, giving his word that his administration would enforce the law as it was intended, not as the swamp wished it would be. That commitment swung the votes.”

• Here’s How Conservatives Can Keep the Momentum Going (Margolis)

It’s not every day that conservatives have a reason to break out the confetti in Washington, but today is one of those rare, glorious moments. The One Big Beautiful Bill—President Trump’s signature legislative achievement—has finally crossed the finish line and now awaits his signature tomorrow. It’s time to celebrate with the gusto this victory deserves. For months, the OBBB wound its way through the Capitol, battered by the usual suspects: Democrat obstructionists, media naysayers, and even a handful of Republican holdouts who needed a little extra convincing. But in the end, it was the steady hand and relentless persuasion of President Trump that brought the House conservatives on board and delivered this win for the American people.

The turning point? It wasn’t a backroom deal or a last-minute concession to the left. It was a meeting at the White House, where President Trump sat down with key conservative lawmakers and laid out exactly how he would enforce the bill’s provisions. No more games from green energy companies trying to siphon off taxpayer dollars with phony construction starts. Trump promised to use the full force of the executive branch to make sure that only those who actually deliver get a dime. This wasn’t just about technical tweaks or bureaucratic fine print. Conservatives had real concerns about loopholes in the Senate’s version of the bill—especially when it came to renewable energy credits and the potential for abuse.

Conservatives pushed back, demanding real, verifiable progress before any federal money changed hands. President Trump didn’t just listen—he acted, giving his word that his administration would enforce the law as it was intended, not as the swamp wished it would be. That commitment swung the votes. Rep. Burchett called it “huge,” and he’s right. When the President of the United States looks you in the eye and promises to hold the line, it means something. That’s leadership. That’s why the OBBB passed, and that’s why conservatives are celebrating today. And let’s not forget the spectacle on the House floor. Speaker Mike Johnson, never one to miss a moment, took a well-earned victory lap, reminding the country that this wasn’t just a win for Trump or for Republicans—it was a win for America.

Meanwhile, Democrat Minority Leader Hakeem Jeffries could do little more than rant and rave for hours as the conservative majority delivered a resounding rebuke to the left’s agenda. This is what happens when conservatives stand together and refuse to be bullied by the media or the establishment. The OBBB is more than just a legislative victory—it’s a sign that the conservative movement is alive, well, unified, and ready to keep winning. So yes, let’s take a moment to celebrate the passage of the OBBB—a clear, decisive victory for common sense and conservative leadership. This is what happens when Republicans stop playing defense and actually fight back. Real change can happen when we stop caving to the radical left’s hysterics and start standing on principle. And let’s be clear: this is only the beginning.

“Supreme Court, Congress, president. Executive, legislative, judicial. All equal branches. All checking each other and balancing each other..”

• A Reminder of What the 4th of July Means (Victor Davis Hanson)

Today is the 4th of July, and I’d like to remind everybody what the 4th of July is. It’s the formal date when the Second Continental Congress—about a year and four months after the shots heard around the world, the first shots of the Revolutionary War at Lexington and Concord, were fired—the Second Continental Congress decided to formally disband the 13 colonies from Great Britain. Now, two days earlier, Richard Henry Lee of the famous Lee family—he was the first cousin of Light Horse Harry Lee, the father of Robert E. Lee—had introduced an amendment called the Lee Resolution that formally was approved and said we are divorcing ourselves from Great Britain. But two days later, John Adams and mostly Thomas Jefferson decided they needed a more holistic document that would list 23 grievances, why it was necessary. So that version of Jefferson, and to a lesser extent, Adams, became the formal Declaration of Independence. And it was ratified on July 4th.

And we all know it from our high school days, or we should. The first famous line, “When in the course of human events it becomes necessary to disband …” And then, “We hold these truths to be self-evident, that all men are created equal,” the first line of the second paragraph. So, it’s a foundational document.

And it doesn’t mean that men are God. When Jefferson wrote “that all men are created equal,” it doesn’t mean that they were equal at that time. But it gave an aspirational goal that, if you think about it, would put the Founders out of business, so to speak. Because if all men are created equal and you create this wonderful place, and you don’t have a blood and soil argument that only the people who were here and related to the Founders by race and ethnicity are Americans, but all men are equal, people will flock to the United States. And they might not look like the original Founders. But they would represent the original Founders. They would be the same type of people by ideas and values.

And so the idea of America was really established with the 4th of July. And we’re going to have the 250th anniversary a year from now that will celebrate the 250 years of the United States of America. Today, it’s the 249th anniversary of the 4th of July. This is not the Constitution that will be ratified in 1787 and will formally establish the government. Fourth of July declares that the 13 colonies who have been at war with Great Britain for about 14 or 15 months, and are operating on what we will call the Articles of Confederation, will then free themselves at the Battle of Yorktown. And then they will have a new type of government, which we now call the U.S. Constitution.

There’s a couple of other things to remember on the 4th of July. The British have a very different idea than we do when they look at the 23 grievances. They said, “Wow, you guys have it pretty easy. We’ve been as nice to you, or better, than the people in Canada. And we have all these Commonwealths and they’re not revolting.” And if you want to look at an interesting document, read “The Great Historian.” A good friend of mine, Andrew Roberts, has addressed all 23 grievances from the British point of view and said, “Ah, that was nothing. Oh, they were crybabies. You shouldn’t have done it.”

It was an interesting argument. But it has a phenomenal effect on history because if you look at Canada, if you look at New Zealand, if you look at the former South Africa, if you look at any of the British commonwealths, or for that matter, any country in Europe, they follow a parliamentary system. But the Founders who created the United States—and through this Revolutionary War learned about what was wrong with the British and what were the alternatives for consensual government, came up with this tripartite based on Montesquieu and the separation of powers. It goes back to the Spartan and Cretan constitution, antiquity. They came up with a unique government of checks and balances—Supreme Court, Congress, president. Executive, legislative, judicial. All equal branches. All checking each other and balancing each other, based on a system of federalism, that each state would have the right to be autonomous and free, as long as it did not contradict or conflict with the laws of the union itself. And they solve that problem of the Articles of Confederation.

And this system, 249 years ago, whether it persevered—I don’t know how it persevered in the Revolutionary War. The Americans didn’t have a lot of assets. The French helped a great deal. But then we had the War of 1812. The War of 1848. And of course, the American Civil War, where 700,000 Americans died trying to abolish slavery, and some trying to perpetuate it. And then, of course, we had the Spanish-American War. And then World War I, where 117,000 Americans died. Two million of them went across the Atlantic Ocean to save France and Britain from German precisionism or German autocracy.

And yet, less than 22 years later, the United States would be in another world war, and we would lose about 420,000. And then the Korean War, 1950 to 1953—35,000. Fifty-six thousand in Vietnam. So, it’s very valuable on this date, to realize that from time to time, from generation to generation, thousands of Americans have fought to protect the ideas of the American Revolution and the United States itself. And on this July 4th, we need to give them a due. And remember what they did, who they were, and why they did it.

“Russia will end the conflict that Macron and other NATO powers started illegally, and the ending of it will be on Russia’s terms.”

“When discussing the situation surrounding Ukraine, Vladimir Putin reiterated that the conflict was a direct consequence of the policies pursued by the Western countries, which had for years been ignoring Russia’s security interests, creating an anti-Russia staging ground in the country..”

• Oh La La… Putin Drops Truth Bomb On Macron (SCF)

NATO started the conflict in Ukraine, but Russia will end it on its terms, Russian President Vladimir Putin told his French counterpart this week in a wake-up call. It’s always refreshing and necessary to bring reality into a conversation, assuming, of course, that the purpose of the dialogue is genuinely to resolve a problem. France’s Emmanuel Macron requested the phone call with Putin this week. It was the first time the two leaders had spoken in nearly three years. The long absence was due to Moscow claiming that Macron breached diplomatic protocol after the last phone call in 2022 by leaking details to the media. In any case, Putin showed magnanimity and a willingness to engage diplomatically by taking the call this week from Macron. The two leaders talked for over two hours.

Apart from Ukraine, another topic discussed was the outbreak of war between Israel and Iran, and the U.S. bombing of Iran’s nuclear sites. Macron agreed with Putin that Iran has the right to pursue civilian nuclear energy production, and both appealed for diplomacy to prevent escalation, according to the Kremlin’s statement on the phone conversation. Critics might note, however, that France, Britain, Germany, and the other European states have played a double game with Iran, undermining Iran’s legitimate rights under the Non-Proliferation Treaty and giving political cover for the unlawful Israeli and US aggression against Tehran. Therefore, Macron’s concern for peace in the Middle East sounds hollow, if not hypocritical.

The Ukraine conflict was also discussed. But here, there was no pretense of diplomatic accord. Macron urged Putin to “call a ceasefire as soon as possible” and to proceed with peace talks, said the Elysee Palace, as reported by French media. For his part, Putin rebuffed the trite talk. He reminded Macron of some necessary reality.

According to the Kremlin’s statement: “When discussing the situation surrounding Ukraine, Vladimir Putin reiterated that the conflict was a direct consequence of the policies pursued by the Western countries, which had for years been ignoring Russia’s security interests, creating an anti-Russia staging ground in the country, and condoning violations of rights of Ukraine’s Russian-speaking citizens, and at present were pursuing a policy of prolonging hostilities by supplying the Kiev regime with a variety of modern weaponry. Speaking about the prospects of a peaceful settlement, the president of Russia has confirmed Moscow’s stance on possible agreements: they are to be comprehensive and long-term, provide for the elimination of the root causes of the Ukraine crisis, and be based on the new territorial realities.”

In other words, Russia will end the conflict that Macron and other NATO powers started illegally, and the ending of it will be on Russia’s terms. Who does Macron think he is? Telling Russia to call a ceasefire as soon as possible? Earlier this year, in March, Macron gave a televised nationwide address declaring Russia to be an existential threat to Europe. He even made the madcap suggestion of France using its nuclear weapons to protect all of Europe. Such crazed talk by Macron is irresponsible and reprehensible. Macron, along with Britain’s Starmer and Germany’s Merz, are prolonging the more-than-three-year war in Ukraine by pledging more military aid to the NeoNazi Kiev regime.

That regime owes its existence to an illegal coup d’état that the Americans and Europeans orchestrated in 2014. The ongoing conflict, which has slaughtered more than one million Ukrainian soldiers and burdened Europe with huge immigration costs, is the responsibility of Macron and other NATO states. They are the instigators, not Russia. If Macron genuinely wants peace in Ukraine, there is a straightforward solution. Stop arming the NeoNazi regime and stop telling lies about “defending democracy in Ukraine” from alleged “Russian aggression.” Macron and his gang of NATO war criminals could end the bloodshed promptly if they dropped the evil charade.

Replacing a 1,000-year old church with a newly invented one is an idea that always backfires.

• No Weapons For Kiev Over Christian Church Persecution – US Congresswoman (RT)

Kiev’s persecution of the country’s largest Christian church is reason enough for Washington to halt military assistance to Ukraine, US Representative Anna Paulina Luna has said, pledging to personally oppose any future weapons shipments. The Florida Republican accused Ukrainian President Vladimir Zelensky of banning the Orthodox Church in a post on X on Friday, apparently referring to ongoing actions against the Ukrainian Orthodox Church (UOC) – the largest religious organization in the country. “I can promise there will be no weapons funding for you,” wrote Luna, who serves on the House Foreign Affairs Committee. “We are not your piggy bank,” she added, calling on Zelensky to “negotiate for peace” instead.

Kiev has accused the UOC of maintaining ties with Moscow to justify its crackdown, even though the church declared its independence from the Russian Orthodox Church in May 2022. Responding to criticism in the comments under her post, Luna added, “The Ukraine bots are big mad about this one.” “All of a sudden these pro-war shills are religion experts and also telepathic, as they are CERTAIN not one Christian went to those churches to worship God. Imagine if we did that in the States. Hypocrites,” she said. According to Ukraine Oversight, an official US government portal tracking aid disbursements, Washington allocated a total of $182.8 billion in assistance to Ukraine between 2022 and the end of 2024.

In May, President Donald Trump expressed concern over what he described as billions of dollars being wasted on Ukraine aid. He said Congress was “very upset about it” and that lawmakers were demanding answers about how the money was being spent. Earlier this week, the Pentagon reportedly halted shipments of certain weapons and ammunition to Ukraine, citing the need to review remaining stockpiles as part of Trump’s ‘America First’ policy. Kiev’s persecution of the canonical Orthodox Church has received limited attention from US politicians and public figures. In late May, American journalist Tucker Carlson raised the issue in an interview with former Ukrainian MP Vadim Novinsky.

“I think very few Americans understand the degree to which the Ukrainian government under Zelensky has persecuted the Ukrainian Orthodox Church,” Carlson said during the broadcast. Years of state pressure on the church have included the arrests of clergymen and raids on monasteries, including a high-profile incident at the Kiev-Pechersk Lavra, where religious relics are kept. Last year, Zelensky signed legislation allowing the government to ban religious organizations deemed affiliated with so-called “aggressor” states, effectively targeting the UOC. Earlier this week, he also stripped the church’s senior bishop, Metropolitan Onufry, of his citizenship, citing his previously acquired Russian passport.

“The Trump administration “was a notable absence from the fund’s backers in December..”

• BlackRock Drops Ukraine Fund (RT)

US investment holding BlackRock stopped its search for investors to back a multi-billion dollar fund for rebuilding Ukraine earlier this year, Bloomberg has reported. Interest reportedly dropped after President Donald Trump retook the White House. The fund was set to be unveiled at the Ukraine Recovery Conference in Rome next week. It had been close to securing backing from firms supported by the governments of Germany, Italy, and Poland, the outlet wrote on Saturday, citing anonymous sources. Nevertheless, BlackRock reportedly decided to shelve the talks early this year “due to a lack of interest amid increased uncertainty over Ukraine’s future,” after the US changed its stance towards Kiev under the current administration.

Trump has long promised to end the Russia-Ukraine conflict and has sought avenues to reach a peace deal. He has also pushed European NATO allies to take over the burden of militarily supporting Ukraine. Earlier this week, Washington reportedly froze critical arms deliveries to Kiev to focus on replenishing its own stockpiles, although the US president has insisted some military aid still continues.The Trump administration “was a notable absence from the fund’s backers in December,” Bloomberg added. In March of last year, BlackRock vice chairman Philipp Hildebrand indicated that the Ukraine Development Fund was on track to secure at least $2.5 billion from private investors, countries and other grant lenders. A consortium of such investors could finance at least $15 billion towards reconstruction work in Ukraine, he said.

However, a BlackRock spokesperson indicated that the firm is no longer engaged in “any active mandate” with Kiev, having finished its pro-bono consulting work with the Ukraine Development Fund last year, Bloomberg wrote. The investment firm, which controls roughly $11.6 trillion in assets, owns substantial shares in military-industrial giants such as Lockheed Martin, Raytheon, and Northrop Grumman, among many others. Armaments produced by these firms, which are supplied to Kiev by its Western backers, have seen extensive use in the conflict. Moscow has repeatedly condemned foreign arms supplies to Kiev, arguing that they make pro-Ukrainian Western nations party to the conflict, which Russia views as a NATO proxy war. The Kremlin has stated that the recent freeze in US military aid to Kiev will accelerate settlement of the conflict.

Every single day, the EU fights rebel countries.

• Slovakia Blocks New EU Russia Sanctions (RT)

Slovakia has blocked the EU’s 18th round of sanctions targeting Russia for the second time due to concerns about the planned phase-out of Russian energy, Slovak media has reported, citing the Foreign Ministry. According to TASR news agency, Bratislava vetoed the package on Friday during a vote by the EU’s Committee of Permanent Representatives. The ministry said Slovakia will continue to oppose the package until it receives firm guarantees from Brussels that the phase-out will not harm its economy. The dispute centers on the European Commission’s RePowerEU plan, which aims to eliminate Russian energy imports by 2028. The plan is being discussed alongside the new sanctions package targeting Russia’s energy and financial sectors. While Brussels reportedly plans to present the phase-out as trade legislation – requiring only a qualified majority – Slovak Prime Minister Robert Fico insists it should be treated as sanctions, requiring unanimous approval.

The Foreign Ministry said the Slovak authorities, energy companies, and industry leaders consider the phase-out “a major challenge for the competitiveness of the economy, especially from the perspective of energy prices and energy security.” It added that while Bratislava is open to further talks, the current negotiations have not addressed its “fundamental concerns and reservations.” It stressed the need for a plan that “benefits citizens and businesses.” A group of European Commission experts reportedly arrived in Slovakia this week for talks on energy. Fico previously warned that the phase-out would jeopardize energy security and raise prices. He also cited the risk of arbitration with Russia’s Gazprom if Slovakia breaks its long-term contract, which could cost up to €20 billion ($23 billion) in penalties.

Hungary also opposes the plan. Foreign Minister Peter Szijjarto said Budapest and Bratislava jointly blocked the package at last week’s foreign ministers’ meeting, warning that the energy cuts would “destroy Hungary’s energy security” and cause sharp price hikes. The European Commission unveiled its 18th sanctions package in early June, framing it as an attempt to pressure Russia to end the Ukraine conflict. The proposed measures include lowering the Russian oil price cap from $60 to $45 per barrel, banning the future use of the Nord Stream pipeline, restricting imports of refined products made from Russian crude, and sanctioning 77 vessels which the West claims are part of a so-called Russian ‘shadow fleet’. The bloc also extended existing sanctions for another six months earlier this week.

Moscow has condemned the sanctions, calling them illegal and counterproductive. Russian officials warned that the EU’s rejection of Russian energy will force it to rely on costlier imports or rerouted Russian energy via intermediaries, driving up prices.

Israel’s idea of a ceasefire: “‘This is the time to finish the job, reach a comprehensive deal and ensure full Israeli victory.'”

• Hamas’ Has ‘Positive Response’ To Ceasefire, Pressure Mounts On Netanyahu (ZH)

Hamas announced on Friday that it had delivered a “positive” response to the latest US-backed ceasefire and hostage release proposal for Gaza, stating it was ready to begin proximity talks with Israel “immediately” to resolve outstanding issues. But just like with prior instances of being near the “goal line” – a phrase often heard during the Biden administration – Hamas has put forth several key conditions which could prove serious obstacles toward finalizing a deal. Still, global media is saying this is the closest the warring parties have been to reaching an agreement in a long time. Israeli media, citing one mediation source, has said that one of Hamas’s main demands is clearer assurances about what happens if negotiations on a permanent ceasefire are not concluded by the end of the proposed 60-day truce.

The militant group’s official statement said, “The movement has delivered its response to the brotherly mediators, which was characterized by a positive spirit.” “Hamas is fully prepared, with all seriousness, to immediately enter a new round of negotiations on the mechanism for implementing this framework,” it added. The current draft presented to Hamas says the ceasefire could be extended as long as both sides are negotiating in good faith, but Hamas reportedly wants that clause removed, fearing it gives Israeli Prime Minister Benjamin Netanyahu an opening to resume military action. This is precisely what ensued in March when a previous deal unraveled. Instead, Hamas is pushing for language that guarantees negotiations on a permanent ceasefire will continue until a final agreement is reached, and this is something which Israel has resisted.

Meanwhile, pressure on Netanyahu continues to grow domestically, as The Times of Israel details: “Tens of thousands of Israelis are set to join hostage families at mass rallies on Saturday night to urge the government to reach a deal that will free all the remaining captives held in Gaza after Israel and Hamas accepted the outlines of a US truce deal. The rallies will be held as the security cabinet gathers to discuss Hamas’s response to the emerging ceasefire-hostage deal, ahead of Prime Minister Benjamin Netanyahu’s trip to the White House on Monday. The Hostages and Missing Families Forum demanded a comprehensive deal to end the war and release the remaining 50 hostages, at least 28 of whom are dead, even as Israeli officials are reportedly working to see which living hostages to prioritize in the partial, phased release under discussion.”

Prior statements of Israeli leaders have presented a grim outlook, with the possibility that less than twenty captives taken on Oct.7, 2023 might still be alive. The Hostages and Missing Families Forum said in its official statement, “Amid reports of a partial deal, and the prime minister’s trip to the United States, hostage families invite Israelis of all stripes to come to Hostages Square and join them in a clear call: ‘This is the time to finish the job, reach a comprehensive deal and ensure full Israeli victory.'”

Icebreakers “R” Us.

• US Plans Massive Arctic Investment (RT)

The US plans to invest billions in expanding its icebreaker fleet for which funding was included in President Donald Trump’s budget bill approved by Congress on Thursday. Trump previously admitted that the US lags behind Russia, which has the world’s largest and most advanced fleet of ice-capable vessels. Washington has of late sought to increase its influence in the Arctic. Vice President J.D. Vance stated in March that the government needs to “ensure that America is leading” in the region due to the presence of Russia and China. Trump’s so-called ‘One Big Beautiful Bill’ includes funding through 2029 for ice-capable vessels.

The US Coast Guard will receive nearly $25 billion to buy 16 new icebreakers and ten light and medium icebreaking cutters, among other equipment, according to Senator Dan Sullivan from Alaska. Sullivan described the allocation as the largest investment in Coast Guard history and a “game-changer.” The US currently operates only two functional polar-class icebreakers, whereas Russia maintains a fleet of over 50, including several nuclear-powered ships. In 2022, NATO countries had 47 icebreakers in total. Eight countries have territory that extends into the Arctic: Russia, the US, Canada, Denmark, Finland, Iceland, Norway, and Sweden – all but Russia are NATO members.

Trump has also revived his interest in Greenland, the vast resource-rich Arctic territory governed by Denmark. He has refused to rule out acquiring the island by force. As warming temperatures make the Arctic more accessible, the region’s potential for resource exploitation and emerging shipping lanes has drawn heightened attention from global powers. The largest portion of the Arctic region lies within Russian territory. In March, President Vladimir Putin called the Arctic a zone of “enormous potential” for trade and development but warned that geopolitical rivalry was intensifying.

“The plans of more than 500,000 people have been disrupted because of the strike in France, which involved 272 employees of the industry..”

• Head of Ryanair Airline Calls Ursula Von Der Leyen ‘Useless Politician’ (Sp.)

Ryanair said on Thursday that it was forced to cancel 170 flights, disrupting over 30,000 passengers, due to the French unions’ strike on Thursday and Friday. Ryanair’s chief executive officer Michael O’Leary told Politico on Friday that he had to cancel “400 flights and 70,000 passengers” and that “360, or 90 percent of those flights, would operate if the Commission protected the overflights as Spain, Italy and Greece do during air traffic control strikes.” Several airlines have accused France of failing to protect airlines during the protest action, while O’Leary criticized European Commission President Ursula von der Leyen.

Almost 1,000 flights were canceled in France on Friday: half at Nice airport, 40 percent at Paris airports, and 30 percent at airports in Lyon, Marseille, Montpellier, Ajaccio, Bastia, Calvi and Figari due to the air traffic controllers’ strike. On Thursday, 933 flights were cancelled. “Ursula von der Leyen, being the useless politician that she is, would rather sit in her office in Brussels, pontificating about Palestine or US trade agreements or anything else. Anything but take any effective action to protect the flights of holidaymakers,” O’Leary said.

The plans of more than 500,000 people have been disrupted because of the strike in France, which involved 272 employees of the industry, Minister of Transport Philippe Tabarot said on Friday. Tabarot said on Thursday that losses related to the strike for airlines, including the country’s main carrier Air France, could amount to millions of euros. Last week, two French air traffic controllers’ unions, USAC-CGT and UNSA-ICNA, representing over 30 percent of the industry’s employees, called for protest action on July 3-4, demanding better working conditions, an end to structural staff shortages, failed technical projects and “toxic management.” The strike came as the French were preparing to go on summer school holidays.

“What was marketed as a smooth transition toward renewable energy has turned into a forced green agenda, with no viable alternatives and little regard for its impact on competitiveness, system stability, or citizens’ well-being.”

• Lights Out, Europe: The Cost of Brussels’ Energy Fantasy (Villamor)

Spain’s leading energy companies—Iberdrola, Endesa, and EDP—remain stunned. After the nationwide blackout that cut power across Spain on April 28, the government has yet to provide a clear explanation or take technical responsibility. The companies, represented by the employers’ association Aelec, have denounced “surprising omissions” in the official investigation. They demand that the extreme voltage spikes recorded in the days leading up to the collapse be included in the analysis. They have criticized the preliminary report from ENTSO-E—the European network of electricity operators—for claiming that “the system was operating normally” just seconds before the failure. Meanwhile, severe voltage swings were recorded, going beyond safety limits and triggering automatic shutdowns of high-voltage substations and key refineries.

This episode is far more than an isolated incident. It is a metaphor for the erratic direction taken by the European Union’s energy policy. In the name of climate change, Brussels has embarked on a radical overhaul of its energy model driven not by technical or economic realities, but by an ideological agenda imposed by political and bureaucratic elites. What was marketed as a smooth transition toward renewable energy has turned into a forced green agenda, with no viable alternatives and little regard for its impact on competitiveness, system stability, or citizens’ well-being.

At the root of this drift lies the REPowerEU plan, launched after the start of the war in Ukraine with the stated aim of “fully decoupling” Europe from Russian energy. What initially appeared to be a justified geostrategic measure quickly became, in the hands of the European Commission, a pretext to push through renewable energies at any cost. This led to a rushed and uneven transition, with citizens and businesses footing the bill. This leap into the void has destabilized key sectors such as agriculture, transport, and industry, forcing them to absorb rising costs without receiving real technological upgrades. Countries like Germany, which shut down their nuclear plants out of political conviction, have now had to reopen coal-fired stations in a contradictory reversal.

Meanwhile, state propaganda continues to promote green energy self-sufficiency, while households face record electricity bills and companies lose competitiveness. The structural failures of the European power grid are becoming increasingly evident. The continental grid was designed for stable and predictable hydro, gas, and nuclear sources. The mass introduction of intermittent sources like wind and solar makes imbalances difficult to manage: without wind or sun, generation collapses; with too much, the grid becomes dangerously overloaded.

On April 28th, the Iberian Peninsula experienced those consequences firsthand. Abnormal voltage levels were detected in several substations throughout the morning. To grasp the gravity: a “voltage oscillation” involves a sudden and significant fluctuation in the grid’s voltage, which can damage equipment, trigger automatic disconnections, or, in extreme cases, cause a total blackout. At the Lancha substation, voltage reached nearly 250 kV on a line rated for 220. Another line, rated at 400 kV, surpassed 470 kV just before the collapse. According to Aelec, these anomalies began as early as 10:00 a.m. While a sudden drop of 2,200 MW in generation has been cited as the trigger, the system is theoretically built to withstand a loss of up to 3,000 MW without shutting down. This was not a coincidental failure—it was a built-in weakness.

Beyond technical and political issues, the forced energy transition takes a human toll. European households are paying more for electricity, hitting middle- and lower-income families especially hard. Electrification of transport, promoted without adequate foresight, is raising the cost of mobility due to a lack of reliable charging infrastructure. Farmers and truckers, already squeezed by unmanageable climate regulations, face growing expenses while being pressured to make investments they cannot afford. Moreover, blackouts are no minor issue: their impact ranges from multimillion-euro industrial losses to the paralysis of hospitals, schools, and transport networks. In Spain, the outage even cost five people their lives. An energy model that cannot ensure a steady supply threatens the economy and public safety.

Imagine you’ve just returned successfully and alive from the greatest journey in Human history to embrace the Cameras about Mankind’s Greatest Ever Accomplishment…..and you look like this.

Please take all the time you need. pic.twitter.com/7XlIxdhaML

— Concerned Citizen (@BGatesIsaPyscho) July 4, 2025

Fish

https://twitter.com/IndianaGPA/status/1941261367207657862

Jeep

It was designed to be assembled in minutes by a few folks after being parachuted to an area.

This one was assembled in less than 3 minutes.

The Jeep was vital and a massive surplus inventory was given away for a few dollars by the 1970s.

— Brian Roemmele (@BrianRoemmele) July 4, 2025

Eagle

https://twitter.com/buitengebieden/status/1941395066800701569

School

https://twitter.com/Hoang_HQ/status/1941183156998242700

Octo

https://twitter.com/wmhuo168/status/1941351218544246839

Octopus opens a jar to get its food

pic.twitter.com/7l0dRulTEV— Science girl (@gunsnrosesgirl3) July 5, 2025

Eve

Eva Marie Saint is 101 years old today.

North By Northwest (1959)

Eva is the oldest living Oscar winner, and one of the last living stars from the Golden Age of Hollywood. This scene with Cary Grant is still one of the hottest scenes ever filmed. This is how you do it, kids. pic.twitter.com/C7Z5lrwf3C— The Sting (@TheStingisBack) July 4, 2025

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.