Grete Stern Sueño No. 27: No destiñe con el agua 1951

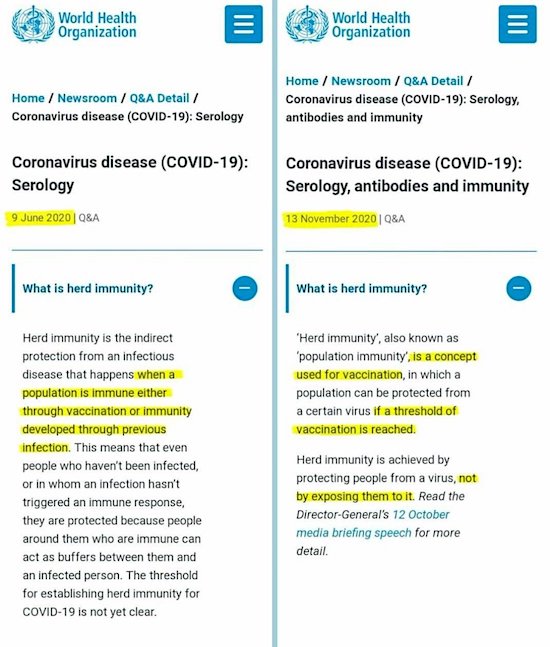

Something I’ve noted a few times: the changing definition of herd immunity. Pretty blatant.

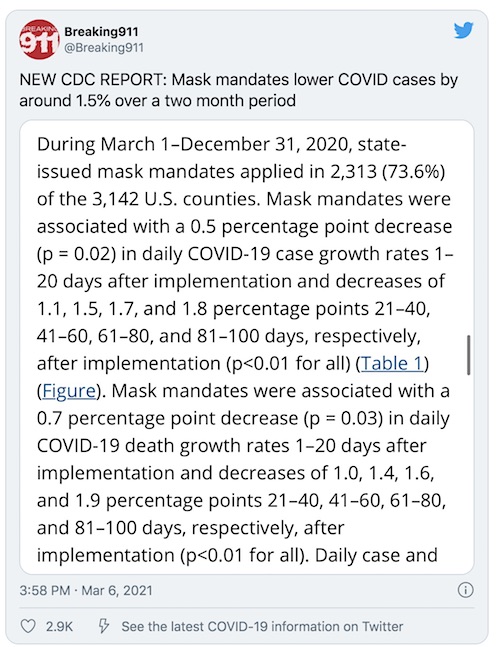

The report is here. Sometimes I feel these reports are written with the express intent to confuse. Entirely different conclusions of course ensue.

• CDC: Face Masks Have Negligible Impact On Coronavirus Numbers (OAN)

The CDC has admitted face masks do little to prevent the spread of COVID-19 amid mounting pressure to lift mask mandates across the U.S. In a new study, the CDC found face masks had a negligible impact on coronavirus numbers that didn’t exceed statistical margins of error. The study found that between March and December 2020, face mask orders reduced infection rates by 1.5 percent over the rolling periods of two months each. The masks were 0.5 percent effective in the first 20 days of the mandates and less than 2 percent effective after 100 days. The CDC added it still recommends wearing face masks, although it admitted such mandates do not make any statistical difference. In the meantime, some states across the nation have slowly returned to normalcy by putting an end to mask mandates.

Nature, not the least, also has some questions.

• Stay-at-Home Policy Is A Case Of Exception Fallacy (Nature)

A recent mathematical model has suggested that staying at home did not play a dominant role in reducing COVID-19 transmission. The second wave of cases in Europe, in regions that were considered as COVID-19 controlled, may raise some concerns. Our objective was to assess the association between staying at home (%) and the reduction/increase in the number of deaths due to COVID-19 in several regions in the world. In this ecological study, data from www.google.com/covid19/mobility/, ourworldindata.org and covid.saude.gov.br were combined. Countries with >100 deaths and with a Healthcare Access and Quality Index of ≥ 67 were included.

Data were preprocessed and analyzed using the difference between number of deaths/million between 2 regions and the difference between the percentage of staying at home. The analysis was performed using linear regression with special attention to residual analysis. After preprocessing the data, 87 regions around the world were included, yielding 3741 pairwise comparisons for linear regression analysis. Only 63 (1.6%) comparisons were significant. With our results, we were not able to explain if COVID-19 mortality is reduced by staying at home in ~98% of the comparisons after epidemiological weeks 9 to 34.

But the WHO stays the panic course.

• World On Brink Of Fourth Wave Of Coronavirus (Hill)

A year after the frightening beginning of the coronavirus pandemic, the world stands on the brink of a fourth wave of infection as nations race to vaccinate their populations and stave off a new surge in hospitalizations and deaths. Total reported cases rose across the globe in the last week of February after six weeks of decline, driven in part by new, more virulent variants that transmit between people at startlingly higher rates than the initial strains out of Wuhan, China, and northern Italy. “This is disappointing, but not surprising,” World Health Organization Director-General Tedros Adhanom Ghebreyesus told reporters last week. “This is a global crisis that requires a consistent and coordinated global response.”

The United States recorded about 66,000 new cases a day over the last week, according to the Centers for Disease Control and Prevention (CDC), down 73 percent from the apex reached in early January and similar to levels of transmission from October. But the precipitous decline of late January and early February has plateaued in recent days, raising fears that a new wave is just around the corner. “We could not have made a more wonderful environment for this virus to take off than we have right now,” said Michael Osterholm, director of the Center for Infectious Disease Research and Prevention at the University of Minnesota. “We are not driving this tiger, we’re riding it. And the first time we may be able to drive it is with widespread use of the vaccine, and we’re not there yet.”

A total of 107 million doses of the three vaccines approved by the Food and Drug Administration have been shipped to states across the nation, according to CDC data. About 53 million people have received at least one dose, 16 percent of the population, while 27 million have received two doses. The first doses of the one-shot vaccine developed by Johnson & Johnson were administered last week. Globally, 115 million coronavirus cases have been confirmed, a quarter — 28.7 million — in the United States. The 518,000 Americans who have died represents about 20 percent of the global death toll. The latest data from the CDC shows 41,000 are still hospitalized.

[..] Some models show an increase in cases just around the corner. One model maintained by the PolicyLab at the Children’s Hospital of Philadelphia shows reproduction rates — the measure of how many people are infected by someone who has the virus — rising in three quarters of the counties surveyed. States in the Northeast, Mid-Atlantic and Midwest showed higher transmission rates last week. Several states have loosened restrictions on businesses and gatherings imposed over the summer, even though infections continue at higher levels today than when those mandates were initially put in place. “You’re seeing a lot of states loosening mask restrictions at a point where they’re having more cases per day than they had over the summer when they put the mask restrictions in place,” said Rich Besser, a former CDC director who now runs the Robert Wood Johnson Foundation. “That just doesn’t make sense.”

A heathen pagan virologist? What’s next?

• Dutch Virologist Asks Cabinet For More Guts: “Open Terraces And Gyms” (P.)

Wanted: more risk, more guts with the corona approach. “Not every relaxation should be seen as a step closer to the abyss.” Louis Kroes is not alone in pushing for a less restrictive policy in the corona crisis. But within the world of virologists and epidemiologists, where the emphasis is usually on reducing the number of infections, arguments that criticize the current lockdown are not really common. Nevertheless, as professor of clinical virology (Leiden University Medical Center), Kroes sees room for relaxation. If the omens do not deceive, he will again be disappointed by the cabinet on Monday, which finds the figures in terms of infections and hospital admissions still too worrying. It confirms Kroes’s idea that a “zero-risk policy” is being pursued, in which every corona death is one too many.

“You shouldn’t look for just maximizing this security. You are also not going to stop motorized traffic because there are road deaths every year. A zero-risk policy for IC occupancy is not realistic. ” The alarming forecasts by the RIVM about the British variant of the coronavirus, which in reality has less drastic consequences, confirm in Kroes’ eyes that policymakers and their advisers always assume the worst case. Under that pressure, the Dutch are locked up at home after nine in the evening. According to Kroes, the cabinet assumes “extremely gloomy scenarios with” large margins of uncertainty “. “The simple idea is then: better safe than sorry; just assume the worst case, then it can only be better than expected. But that is also risky.

Because in addition to the group of vulnerable people at risk from the corona virus, there are also the interests of millions of Dutch people who are at risk due to the stringent corona approach. Their health suffers from passivity, for entrepreneurs income is at stake, for pupils and students their future, people become lonely. You have to take those risks into account. ” Kroes therefore believes that the margin that he believes there is for easing should be maximized. “I understand the principles of the policy. In the first wave, with the doom of ICU flooding, I found the lockdown understandable. But that extreme scenario is no longer clearly visible. That does not happen overnight either. That is no reason to go to great lengths to contain the pandemic. ”

Greece can no longer afford the policies that failed so miserably, which they will never admit. Like all other governments. No, it’s the new variants, it’s the young people, it’s general behavior.

I think this is not an incident, but our overall approach to healthcare. We don’t encourage people to be healthy, we don’t prevent illness, we treat them only when they are already sick. Is this just a GDP thing, or does it go deeper?

• Pressure To Reopen Greek Society Mounts As Virus Holds (K.)

With health officials unable at the moment to predict when the viral load in Attica and other badly affected areas will start to subside, the government is striving to chart the way forward under pressure from the heavy economic and social toll exacted by successive lockdowns. What is clear is that the ominous daily rates of hospitalizations, intubations and deaths make any plans for the resumption of retail on March 16, immediately after Clean Monday, highly unlikely. Bearing this in mind, the most optimistic scenario for the government foresees the opening of retail stores with limits to the numbers of customers per square meter by the end of the March. This scenario also provides for the opening of restaurants, but only with outdoor seating, some time in April.

What’s more, with the completion of the first round of vaccinations in May, it is hoped that it will be possible to return to some form of normalcy for the economy. Any decision taken will depend on the resilience of the national health system and not so much on the infection rate, which is growing among younger age groups and is likely to continue in the foreseeable future though it is not, however, expected to burden hospitals to a large degree. Although the current restrictive measures are not very different form the ones last March – with the exception that more economic activities are now allowed – they have failed to yield the desired results for two main reasons.

Firstly, because a sense of fatigue has set in among the public, which has also impacted inspection mechanisms. A second reason that has been postulated is that, compared to last March, fear of the coronavirus has subsided, especially among younger people. Prime Minister Kyriakos Mitsotakis’ aides say that the rationale behind not adopting a tough general lockdown and why an attempt will be made to open retail and then catering is that the financial costs of supporting workers and businesses affected by the existing constraints are already untenable. The 2021 budget provided €7.5 billion for support measures. However, the relevant budget has already reached €11.5 billion. At the same time, only from the suspension of the operation of the retail trade, the state is losing about €1.1 to €1.2 billion per month in revenues.

“Americans who wish to travel to North Korea are obliged to do just that.”

• Leaving UK Now Requires A ‘Special Validation To Travel’ (Calder)

Imagine being told you must have a “special validation to travel”. Americans who wish to travel to North Korea are obliged to do just that. Prospective visitors, says the US State Department, must also “discuss a plan with loved ones regarding care/custody of children, pets, property, belongings, non-liquid assets, funeral wishes, etc” and “draft a will and designate appropriate insurance beneficiaries”. That’s enough to make you lose the will to travel. Which is exactly what the UK’s home secretary had in mind when she decided to impose a special validation to travel on anyone seeking to leave the country. “There are still too many people coming in and out of our country each day,” Priti Patel told parliament in January.

UK residents are entitled to return home, making the inbound portion of that “too many” difficult to suppress – though deterrents such as the prospect of hotel quarantine are working some magic. Instead, the home secretary set about increasing controls on anyone seeking to leave the UK. She decided to impose a requirement for a “Declaration to Travel” – a very British version of that “special validation”. With just 58 hours remaining before it became a criminal offence even to turn up at an airport, railway station or ferry port without a completed form, the document was finally published. It does not involve a side order of custody of children, funeral wishes and a last will and testament – though given the increasingly draconian travel restrictions put in place by the government, I wouldn’t have put it past them.

Ms Patel calls the Declaration to Travel “a necessary step to protect the public and our world-class vaccination programme”. I call it the antithesis of the “Global Britain” for which we are expected to strive after Brexit – as well as an unnecessary and alarming extension of the government’s powers. The four UK nations share a perfectly powerful law at present: stay at home, and venture outside only if you can claim exemption such as caring, shopping for essentials, exercise or education. Heading for an airport and hoping to board a plane somewhere warmer (and possibly less in tune with North Korea) is most definitely not on the list of excuses for being out of the house.

Brilliant. The Swiss ban face coverings just when their own laws make them mandatory.

• Swiss Voters Support ‘Burqa Ban’ (RT)

Covering your face in public for non-medical reasons will become illegal in Switzerland after a proposal dubbed a “burqa ban” was accepted by a narrow margin of voters in a binding national referendum on Sunday.

Supporters of the “burqa ban” have prevailed in the Alpine country, with 51.2 percent being in favor and 48.8 percent being against, official data showed after votes were counted. In line with the Swiss system of direct democracy, the country’s constitution will now be amended to forbid face coverings in public places for all but three specific reasons. The legislation, which had been promoted by the right-wing Swiss People’s Party (SVP) since 2016, did not mention Islam directly and was claimed by proponents to be aimed at preventing violent rioters from hiding their identities.

It was nonetheless dubbed the “burqa ban” by the media and politicians due to also restricting the face coverings worn by Muslim women. Back in 2009, the SVP initiated a referendum on preventing the construction of new minarets in Switzerland, and also won that vote. There are several exceptions to the “burqa ban” – it allows the covering of one’s face for security, climate, or health reasons. As such, it wouldn’t contradict the anti-coronavirus measures that oblige Swiss citizens to wear face masks in public places, on public transport, and in indoor workspaces. Muslim women would also be allowed to don burqas and niqabs in places of worship. By greenlighting the ban, Switzerland has joined France, where full-face veils in public were outlawed in 2011, and such countries as Denmark, Austria, the Netherlands and Bulgaria, where full or partial bans on face coverings are currently in place. Two Swiss cantons had already introduced similar restrictions on burqas some years back.

Meanwhile, in CNN’s parallel universe, there’s apparently also a parallel president….

• Biden’s Historic Victory For America – No Thanks To GOP (CNN)

President Joe Biden is on the cusp of a major legislative victory. If all goes according to plan and the $1.9 trillion American Rescue Plan is signed into law, Biden will have scored an early triumph in his presidency. The Covid-19 relief bill will provide a wide range of benefits, from direct payments to American families, money for vaccine development and distribution, small business relief, more substantial subsidies for the Affordable Care Act, a child tax credit, a higher Earned Income Tax Credit, federal funds for state and local governments and much more. Given the scale and scope of this measure, it is an accomplishment that will cement Biden’s historic role in overseeing the country’s recovery from the Covid-19 pandemic.

Despite last minute concessions to appease moderate Democrats on Friday night, as journalist Ezra Klein tweeted, “This still looks like the most ambitious and progressive economic package Congress has passed in my lifetime. It will do more to cut poverty, and push full employment, than anything else I’ve covered.” So far, it looks like Biden has learned some important lessons on how to deal with the modern Republican Party. After Biden watched congressional Republicans obstruct the agenda of his former boss, Barack Obama, he saw Obama’s successor, Donald Trump, whose presidency was capped off with a violent insurrection against Congress, expose the radicalization of the GOP.

[..] There were certainly defeats along the way. The amendment to raise the minimum wage to $15 an hour by 2025 failed. On Friday night, Senate Democrats finally won over Sen. Joe Manchin — a moderate Democrat who threatened to derail the relief bill — by dropping the bid to increase unemployment benefits from $300 a week to $400. To satisfy moderate Democrats, Biden had also agreed to narrow the income eligibility for the $1400 stimulus checks, cutting off couples who earn more than $160,000 a year or individuals who earn more than $80,000 a year. But most of the package has remained intact. While Biden was certainly open to Republican support, he did not cater to their demands in the elusive hope that they would join him.

Drip drip.

• 5 Women Now Accuse Cuomo Of Inappropriate Behavior (NYP)

Two more women came forward Saturday to accuse Gov. Cuomo of sexually harassing behavior, including a former press aide who describes struggling to free herself from his repeated hugs, and a young assistant who now says he left her feeling like “just a skirt.” Former press aide Karen Hinton endured a “very long, too long, too tight, too intimate” embrace from Cuomo in a dimly lit Los Angeles hotel room in December 2000, she told the Washington Post. The married Hinton pulled away, but “he pulls me back for another intimate embrace,” she told the paper. “I thought at that moment it could lead to a kiss, it could lead to other things, so I just pull away again, and I leave.” At the time, Cuomo led the U.S. Department of Housing and Urban Development. A current rep for Cuomo strongly denied Hinton’s allegation to the newspaper, claiming “this did not happen.”

Hinton’s claims are made all the more startling given that her husband is lobbyist Howard Glaser, a longtime Cuomo ally and confidante who worked as his director of state operations and senior policy advisor until 2014. The other new accuser, Ana Liss, a policy and operations aide who worked for the governor from 2013 to 2015, said he’d behaved inappropriately while on the job in Albany. The governor called her “sweetheart” and asked if she had a boyfriend, Liss recalled to the Wall Street Journal. Liss said Cuomo touched her on her lower back during an event, once kissed her hand and asked her if she was dating. “It’s not appropriate, really, in any setting,” she told the newspaper. Liss is the third former state employee and fourth woman overall to accuse the governor of varying degrees of sexual harassment. Hinton brings the total of accusers to five.

“Cuomo Says There’s ‘No Way’ He’ll Resign After Fifth Accuser Comes Forward”

• New York State Senate’s Top Democrat Calls On Cuomo To Resign (F.)

The top-ranking democrats who lead New York’s State Senate and State Assembly both signaled Gov. Andrew Cuomo (D) should resign following a wave of new allegations from two of the governor’s former aides. New York State Majority Leader Andrea Stewart-Cousins said in a statement Sunday afternoon that Cuomo “must resign” for “the good of the state,” adding: “Everyday there is another account that is drawing away from the business of government. State Assembly Speaker Carl Heastie (D) said soon after that he shared the sentiment of Stewart-Cousins “regarding the governor’s ability to continue to lead this state.” “We have many challenges to address, and I think it is time for the governor to seriously consider whether he can effectively meet the needs of the people of New York,” Heastie said.

These statements from the top-ranking democrats come hours after Cuomo, speaking to reporters on a phone call prompted by the new allegations from two former aides (compounding allegations from three other women over the past few weeks), reiterated that he has no plans to resign. “I’m not going to resign because of allegations,” Cuomo said during a Sunday afternoon phone presser, asking the public to wait until the New York Attorney General’s office finishes its investigation into the claims. Cuomo called the new allegations from Karen Hinton—one of the governor’s former press aides—that he called her to his hotel room and acted inappropriately toward her after a work event in 2000 “not true,” labeling Hinton a “long-time political adversary of mine.”

Responding to separate allegations from Anna Liss, another former aide, who said she felt patronized and diminished by the governor, recounting questions about her love life, Cuomo kissing her hand and touching her lower back at a reception, Cuomo said he would often engage in “friendly banter” with staff, but did not have malicious intent.

“As a member of one of New York’s best known political dynasties, Cuomo is a protected species..”

“I personally find it difficult to imagine such a deeply entrenched political animal of the swamp variety facing any serious repercussion..”

• Cuomo Nursing Home Scandal May Trigger Domino Effect (Sp.)

Andrew Cuomo has found himself in a heap of trouble over long-term care facility residents’ COVID-related deaths and sexual harassment allegations. Although Cuomo is not going to resign, his cases may have repercussions for his political future and hit Democratic governors who issued similar nursing home orders during the pandemic. On 5 March, New York Governor Andrew Cuomo, whose time in office has recently been mired by two separate scandals, was stripped of emergency powers by the Democratic-dominated state legislature. The same day, the Democratic majority’s leader in New York’s state Senate said that the governor should resign if “any further people” come forward to accuse him of sexual misconduct.

Five women have made sexual harassment or bullying claims against Cuomo so far. NY Attorney General Letitia James has requested that the governor and his staff preserve all records that may be relevant to the sexual harassment probe. A day earlier, The New York Times broke that top members of Gov. Cuomo’s COVID-19 taskforce rewrote a report from the state’s health department to hide the real number of deaths among nursing home residents last June. The FBI and federal prosecutors in Brooklyn are investigating the governor’s handling of nursing homes amid the coronavirus pandemic, according to an 18 February ABC News report. Although Cuomo has repeatedly tried to downplay both scandals, he has nevertheless hired Elkan Abramowitz, a prominent criminal defence lawyer and former federal prosecutor, to represent his office in the investigation into New York’s misreporting of COVID-19 deaths among nursing home residents.

Hiring a prominent criminal defence attorney is an indication that Governor Cuomo is taking the growing scandal seriously, suggests Jason Goodman, US investigative journalist and Crowdsource the Truth founder. “So far, no significant information about the probe has been revealed to the public beyond the fact that it is underway or at least being contemplated”, Goodman says. “It is difficult to say at this point what federal prosecutors may do or what determinations may be made”. Still, one needs to keep in mind that previously Andrew Cuomo served as the state’s attorney general, the secretary of housing and urban development, and campaign manager for his own father’s gubernatorial campaign, so he likely knows or has worked with many of those who would be investigating him, according to Goodman.

“I personally find it difficult to imagine such a deeply entrenched political animal of the swamp variety facing any serious repercussions”, the journalist remarks. Previously, Charles Ortel, a Wall Street analyst who exposed General Electric’s massive financial discrepancies in 2008, raised serious questions about Cuomo’s non-profit, Housing Enterprise for the Less Privileged, but no investigation has come about, Goodman recalls. “As a member of one of New York’s best known political dynasties, Cuomo is a protected species”, the journalist adds.

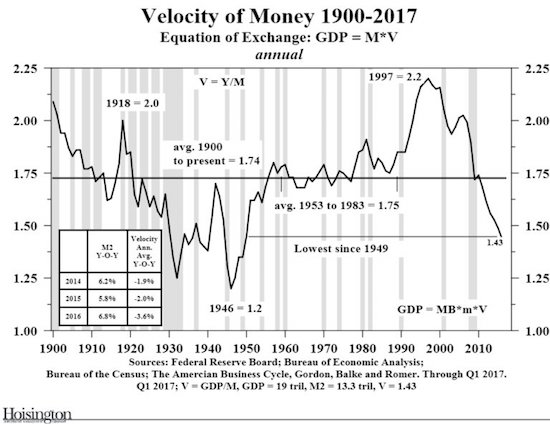

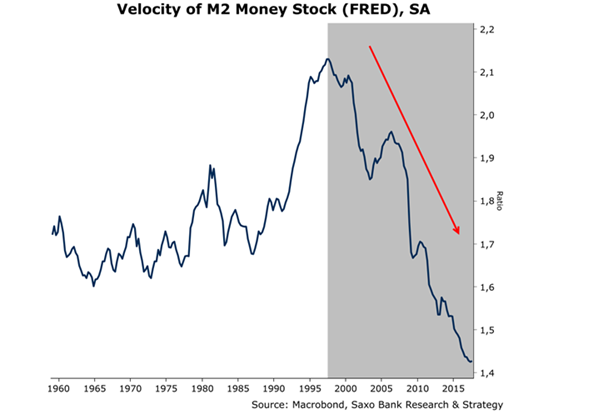

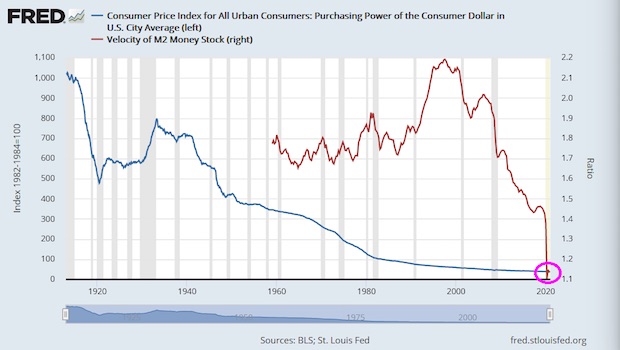

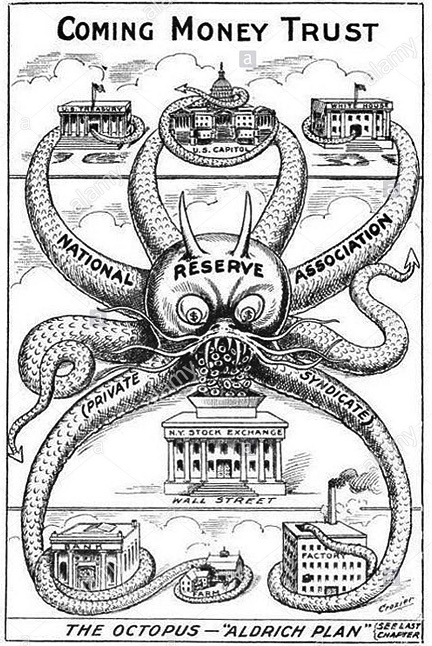

Money ain’t moving anywhere.

• Approaching Zero Velocity! (CI)

Since its creation in 1913, The Federal Reserve has helped obliterate the purchasing power of the US Dollar.

And just wait for Biden’s $1.9 trillion in government spending (the first of many) to hit the economy.

Now you can see why investors seek out gold, silver, Bitcoin and other sources of protection from The Federal Reserve.

Inequality explained.

• Forget $15 an Hour — the Minimum Wage Should Be $24 (IC)

The coronavirus pandemic relief bill passed by the House of Representatives this week would raise the federal minimum wage in steps until it reached $15 an hour in 2025. But an increase in the minimum wage has been removed from the Senate’s legislation. At least for now, it is stuck at $7.25. This is bad enough in itself, but even worse is that almost no Americans understand how low we’ve allowed our aspirations to become. Our country’s productivity gains in recent decades should have translated into a minimum wage today of $24 an hour — and by 2025, it should be almost $30. This may sound preposterous. But in fact, U.S. society was once on a path to this destination. We simply chose to step off that path.

From both a moral and practical perspective, the minimum wage should go up in step with the productivity of the U.S. economy — that is, our ever-increasing ability to create more wealth with the same amount of work. Morally, as a country grows richer, everyone should share in the increased wealth. Practically, companies that sell things need lots of people with the money to buy them. We know that this can work because it already did. During the 30 years from the establishment of a minimum wage in 1938 to 1968, Congress repeatedly upped the minimum wage so that it did in fact go up hand in hand with U.S. productivity. By the end of that period, it was worth the equivalent of $12 per hour today.

Since 1968, American productivity has substantially increased. Dean Baker, senior economist at the Center for Economic and Policy Research, points out that if the minimum wage had gone up at the same rate, it would now be over $24. At that level, as Baker says, a couple who both worked full time at minimum-wage jobs would take home $96,000 a year. Baker also calculates that by 2025, rising productivity would bring the minimum wage close to $30 an hour. But instead we’ve gone in the other direction. After the late 1960s, Congress stopped raising the minimum wage in step with productivity. Instead, over the past 50 years, Congress has allowed the minimum wage to plummet in real terms. That is, minimum-wage workers of the past were actually paid more than minimum-wage workers make today — even though today’s workers live in a much richer society.

Indeed, since 1950, the hourly minimum wage has almost never been lower than it is now. Of course, 1950 is literally a lifetime ago, and the U.S. is now a completely different country. Our per capita GDP is now four times greater.

We try to run the Automatic Earth on donations. Since ad revenue has collapsed, you are now not just a reader, but an integral part of the process that builds this site. Thank you for your support.

Support the Automatic Earth in virustime. Click at the top of the sidebars to donate with Paypal and Patreon.