Broadway, New York 1954

Question is whether that is a bad thing. Or you could say: Trump brings along his own orthodoxy.

• Trump’s Historic Bet on Kim Summit Shatters Decades of Orthodoxy (BBG)

Donald Trump took the biggest gamble of his presidency on Thursday, breaking decades of U.S. diplomatic orthodoxy by accepting an invitation to meet with North Korean leader Kim Jong Un. The bet is that Trump’s campaign to apply maximum economic pressure on Kim’s regime has forced him to consider what was previously unthinkable: surrendering the illicit nuclear weapons program begun by his father. If the president is right, the U.S. would avert what appeared at times last year to be a steady march toward a second Korean War. It was classic Trump, showing an unerring confidence to get the better end of any negotiation.

But it was also Trump in another way: high risk and high reward, with little regard for those in the foreign policy establishment who worry it’s too much, too soon. “He’s taking a risk,” said Patrick Cronin, senior director of the Asia-Pacific Security Program at the Center for a New American Security. “By seizing an opportunity for a summit meeting, a decision that would have taken much more time in another administration, the president has said, ‘I’m going to go right now. And we’re going to test this.”’

“If you don’t want to pay tax, bring your plant to the USA..”

• Trump Sets Steel And Aluminum Tariffs; Canada, Mexico Exempted (R.)

U.S. President Donald Trump pressed ahead on Thursday with import tariffs of 25% on steel and 10% for aluminum but exempted Canada and Mexico and offered the possibility of excluding other allies, backtracking from an earlier “no-exceptions” stance. Describing the dumping of steel and aluminum in the U.S. market as “an assault on our country,” Trump said in a White House announcement that the best outcome would for companies to move their mills and smelters to the United States. He insisted that domestic metals production was vital to national security. “If you don’t want to pay tax, bring your plant to the USA,” added Trump, flanked by steel and aluminum workers.

Plans for the tariffs, set to start in 15 days, have stirred opposition from business leaders and prominent members of Trump’s own Republican Party, who fear the duties could spark retaliation from other countries and hurt the U.S. economy. Within minutes of the announcement, U.S. Republican Senator Jeff Flake, a Trump critic, said he would introduce a bill to nullify the tariffs. But that would likely require Congress to muster an extremely difficult two-thirds majority to override a Trump veto. Some Democrats praised the move, including Senator Joe Manchin of West Virginia, who said it was “past time to defend our interests, our security and our workers in the global economy and that is exactly what the president is proposing with these tariffs.”

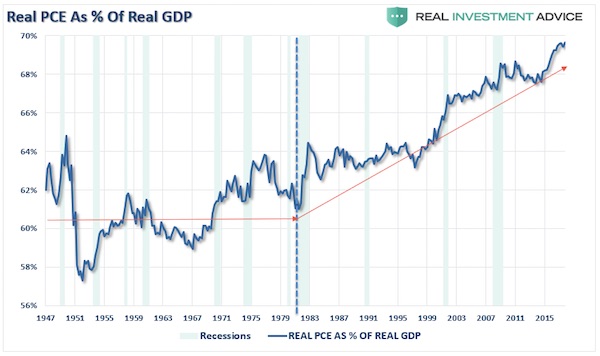

Perhaps somewhat surprising: The consumer spending part of GDP only rises.

• There Will Be No Economic Boom – Part II (Roberts)

When the “tax cut” bill was being passed, everyone from Congress to the mainstream media, and even the CFP’s I spoke with yesterday, regurgitated the same “storyline:” “Tax cuts will lead to an economic boom as corporations increase wages, hire and produce more and consumers have extra money in their pockets to spend.” As I have written many times previously, this was always more “hope” than “reality.” The economy, as we currently calculate it, is roughly 70% driven by what you and I consume or “personal consumption expenditures (PCE).” The chart below shows the history of real, inflation-adjusted, PCE as a percent of real GDP.

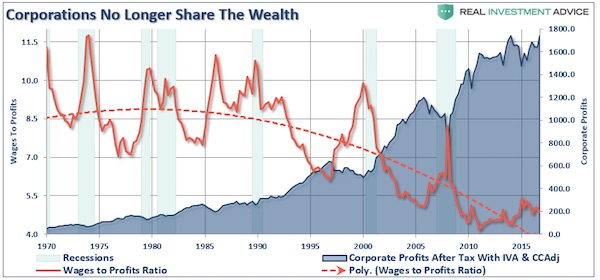

If “tax cuts” are going to substantially increase the growth rate of the U.S. economy, as touted by the current Administration, then PCE has to be directly targeted. However, while the majority of consumers will receive an “average” of $1182 in the form of a tax reduction, (or $98.50 a month), the increase in take-home pay has already been offset by surging health care cost, rent, energy and higher debt service payments. [..] But this is nothing new as corporations have failed to “share the wealth” for the last couple of decades.

Those crazy earnings numbers WILL come crashing down.

• “Gary Cohn, We Hardly Knew Ya” (David Stockman)

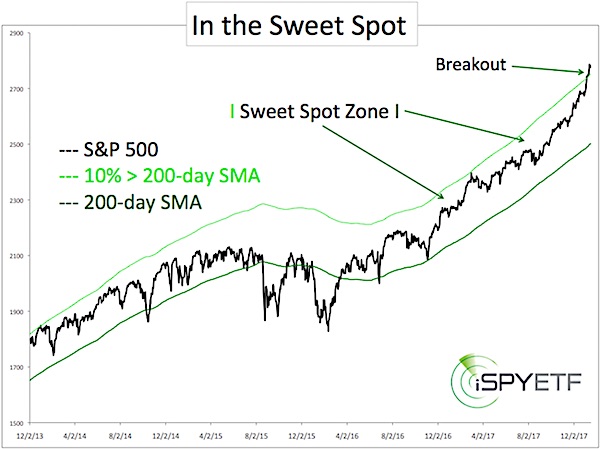

That was quick. The trade war scare was over by noon yesterday, and by the market close they were singing “Gary Cohn, we hardly knew ya”. Folks, what more evidence do you need that the financial markets are completely uncoupled from reality and that these feeble bounces between the 50-day and 20-day chart points are essentially the rigor mortis of a dead bull? At the moment, the 50-day stands at 2740 on the S&P 500 and is functioning as “resistance” according to the chart mavens, while the 20-day at 2700 is purportedly acting as “support”. So there’s that, but also this: At the exact mid-point of 2720, the broad market is currently trading at 25.6X reported earnings for 2017.

That’s the nosebleed section of history no matter how you slice it – and most especially in the context of an earnings growth trend that is shackled to the flat line, and which has no prospect of breaking away before the next recession, either. With virtually every company having reported, it turns out that GAAP earnings for 2017 came in at $109.46 per share on the S&P 500. Then again, 40 months earlier in September 2014 reported LTM earnings were $105.96 per share. That tabulates to a 1.0% per year gain during what will surely prove to have been the sweet spot (month #63 to month #102) of the current long-in-the-tooth business expansion.

Non-banks. How is that different from China?

• The Risk Lurking In The US Mortgage Market (CNN)

Low interest rates. Easy credit. Poor regulation. Toxic mortgages. These were just a few reasons regulators gave for the collapse of the US housing market a decade ago. Since then, regulators have improved the standards that lenders use when Americans apply for mortgages. But today increasing danger lurks in the mortgage market, and economists say it could put the financial system at “even greater risk” when the next recession strikes or too many borrowers fall behind on their mortgage payments. A growing segment of the mortgage market is being financed by so-called non-bank lenders — financial institutions that offer loans to consumers but don’t provide saving or checking accounts.

Borrowers with poor credit have increasingly turned to these alternative lenders instead of traditional banks. The alternative lenders are subject to far less regulation and have fewer safeguards when borrower defaults start to pile up. “A collapse of the non-bank mortgage sector has the potential to result in substantial costs and harm to consumers and the US government,” economists at the Federal Reserve and the University of California, Berkeley, write in a paper released Thursday at a Brookings Institution conference. As of 2016, non-bank financial institutions originated close to half of all mortgages. They originated three-quarters of mortgages with explicit government backing, underscoring the risk to taxpayers.

“The experience of the financial crisis suggests that the government will be pressured to backstop the sector in a time of stress,” the authors write. The danger is that non-banks may have fewer resources to weather economic shocks to the mortgage market, like a rise in interest rates or a decline in house prices. “What happens if interest rates rise and non-bank revenue drops? What happens if commercial banks or other financial institutions lose their taste for extending credit to non-banks? What happens if delinquency rates rise and servicers have to advance payments to investors?” the authors write. “We cannot provide reassuring answers to any of these questions,” they write.

The entire Green Facade depends on cheap credit. And subsidies.

• The End of Cheap Debt Will Bring a Wave of – Green- Bankruptcies (Mises)

The end of the era of cheap money highlights the risk of “Enron-style” bankruptcies in many sectors, including renewable energy. With the path of three rate hikes in the United States in 2018 confirmed by the Federal Reserve and a nervous equity market, the challenges are more evident than ever. The past eight years of massive liquidity and low rates have not helped deleverage, and many companies have used this period to increase imbalances and create complex debt structures. In fact: • Corporate net debt to EBITDA levels is at record highs. About 20% of US corporates face default if rates rise, according to the IMF. • The number of zombie companies has risen above pre-crisis levels according to the Bank of International Settlements (BIS). • This is particularly evident in the renewable sector where, even in the years of high liquidity and low rates, bankruptcies soared.

The renewable sector has undergone an absolutely spectacular transformation in the past eight years. Technology advanced, costs fell and global leaders strengthened when their strategy was to develop an energy model. Understanding that disruptive technologies cannot be more leveraged than traditional ones was key. When technology reduces costs and disrupts inflationary models, basing the business on ever-increasing subsidies and higher prices and financing it with massive debt is suicidal. In the era of cheap money and extreme liquidity, many companies used the “green” subterfuge to implement an extremely leveraged builder-developer model, ignoring demand, costs, and competition. A model whose sole objective was to install for the sake of installing capacity, whether there was a demand or not, and that pursued subsidies while stating that it is very competitive.

Even in a period of falling interest rates and very high liquidity, there have been spectacular bankruptcies, so imagine what can happen when rates rise. [..] If a technology is viable, it does not need subsidies. If it is unviable, no subsidies will change it. Bankruptcies in the solar sector exceed all those of the inefficient coal and fracking companies combined. This domino of bankruptcies, which includes more than 120 corpses of large companies around the world, was self-inflicted. And now, winter is coming. [..] The global renewable sector faces refinancing needs in the next seven to eight years that exceed its entire market capitalization (134 billion euros, Renixx Index).

It is not a problem of technology, it is the addiction to cheap debt and growth for growth sake. And it’s not just a problem in the renewable sector. The combination of lower revenues and increased debt costs is a danger. Cost of debt rises, and cost of equity soars due to higher perceived risk, which in turn can dry up the market for capital increases and refinancing. It is not just renewables, but it is worth highlighting that energy is -again- the most vulnerable sector due to the cyclical nature of its revenues and the perpetuation of overcapacity of the past eight years.

Musk is the leader of the Green Facade.

• Tesla Chief Musk Says China Trade Rules Uneven, Asks Trump For Help (R.)

Tesla CEO Elon Musk took to Twitter on Thursday to call on U.S. President Donald Trump to challenge China’s auto trade rules, which limit foreign ownership of Chinese ventures and impose steep tariffs on imported cars. In a series of tweets aimed at the president, Musk said he was “against import duties in general, but the current rules make things very difficult. It’s like competing in an Olympic race wearing lead shoes.” Tesla has been pushing hard to build cars in China, the world’s largest auto market, but has hit roadblocks in negotiations with local authorities, in part because Musk is keen to keep full control of any local venture. “No U.S. auto company is allowed to own even 50% of their own factory in China, but there are five 100% China-owned EV (electric vehicle) auto companies in the U.S.,” Musk wrote in another tweet.

Tesla “raised this with the prior administration and nothing happened. Just want a fair outcome, ideally where tariffs/rules are equally moderate. Nothing more. Hope this does not seem unreasonable,” he said. Trump quoted one of Musk’s tweets in his announcement on new tariffs and said American automakers have not been treated fairly by trade rules around the world. Trump announced steep tariffs on steel and aluminum imports on Thursday. Politicians “have known it for years and never did anything about it. It’s got to change,” Trump said, saying he plans to impose a “reciprocal tax” on other countries. “We’re changing things,” Trump added. “We just want fairness.”

Yeah, we all believe that.

• China Will Rely Less On Stimulus As It Battles Risks From Debt – PBOC (CNBC)

China has moved away from its old growth model which was heavily reliant on investment and will rely less on stimulus to boost the economy in future, People’s Bank of China governor Zhou Xiaochuan said on Friday. Zhou’s comments echoed those of other top officials at China’s parliament this week which suggested that Beijing will be more cautious about spending this year while it focuses on reducing the risks from a rapid build-up in debt. After years of heavy pump-priming, markets worry less generous stimulus could retard the pace of growth not only in China but globally. But analysts believe Beijing will continue to keep the system well supplied with cash to avoid the risk of a sharp slowdown in economic growth, even as they continue to tighten the screws on financial regulations.

“We now emphasize the new normal of the economy, shifting from the past growth model of quantitative growth… referring to the accumulation of capital and investment to boost economic growth,” Zhou told reporters on the sidelines of the annual parliament session. “While pursuing higher quality growth, we will have to reduce our reliance on the old growth model of investment,” said Zhou, in what was likely his last news briefing before his expected retirement this month. Zhou said China needs to improve its regulatory supervision as soon as possible to curb risks to the financial system. He said China has begun to make progress in reducing such risks, but numerous threats remain, such as a lack of transparency at financial holding companies and digital currencies.

The Brexit fiasco continues to expose the hidden weaknesses. Which in the case of pensions are global, but mostly remain hidden.

• UK Retirement Bill Rises More Than £1 Trillion In Five Years (Ind.)

The UK’s pension funding crisis reached a new crisis milestone this week as the Office for National Statistics revealed the UK’s pension funding liabilities rose to £7.6 trillion at the end of 2015. The figure – the total amount promised to pay Brits’ future retirement income – includes £5.3 trillion of pension entitlements that were the responsibility of central and local government, most of which – around £4 trillion – came from State Pension entitlements. The remaining £2.3 trillion were private sector employee pension entitlements with £2 trillion due to final salary pensions, up from £1.4 trillion in 2010. As things stand, expert commentators suggest there is only around a third of that ‘in the bank’ in company pension funds.

The remainder, it is hoped, will be generated by future working populations. The figures are designed to provide a snapshot of household retirement entitlements, though they don’t include self-invested personal pensions, which have grown significantly in recent years thanks to legislative changes known as pensions freedoms. “While these are obviously large amounts of money, it is important to remember that the payments will be drawn over many years,” says Darren Morgan, head of national accounts for the ONS. “The figures say nothing about the sustainability of our pension system in future.”

In fact, pensions experts have been shocked by the statistics, which come just days after official warnings from the Government Actuary that National Insurance may have to increase by 5% to pay for future state pay outs. “The figures published by the ONS today are astonishing and bring into sharp relief the reasons behind proposed increases in the state pension age,” adds Tom Selby, senior analyst at AJ Bell. “Unfunded state pension entitlements are worth more than double UK GDP – these are promises that will, ultimately, have to be paid for by future generations either through higher taxes, a lower state pension income or a later retirement age.

Why not say it like it is?

• Shares, Profits Of Britain’s Largest Estate Agent Countrywide Plummet (G.)

Countrywide, Britain’s largest estate agent, has reported a 22.5% fall in core annual earnings and scrapped its dividend, sending its shares to record lows. It pledged to go “back to basics” to return its sales and lettings business to profitable growth after what it described as a disappointing year. “We have got to put our resources back in the front line and not at the head office,” said the executive chairman, Peter Long, adding that restructuring would reduce headcount to 350 from 400. Countrywide said its 2018 property pipeline was “significantly lower” and that it expected a fall of about 36% (£10m) in first-half adjusted earnings before interest, taxation and amortisation (Ebitda).

Its 2017 adjusted Ebitda fell 22.5% to £64.7m while group income fell almost 9% to £671.9m. Shares in Countrywide plunged to a record low of 66.64p before rising to 77p in mid-morning trading, down 13.4% . “The next few months will be messy as new plans are put into place,” Jefferies analysts said in a note to clients. “However, banks are lending their support to the new plan and we believe those equity investors who choose to do the same will have their patience rewarded.”

As sales are down 35%.

Greater Toronto Home Sales Down 35% From February 2017

• Toronto Home Builders Just Had Their Busiest February Since 1948 (BBG)

Toronto developers had one of their busiest months on record in February in another sign the condo market is alive and well in Canada’s biggest real estate market, even amid a broader slowdown. Builders began work on 5,677 units during the month, most of them multiple-unit projects like condos, the Canada Mortgage and Housing Corp. said Thursday in Ottawa. That’s the strongest February, and the sixth-highest figure for any month, in records back to 1948. The bulk of Toronto condo units are typically sold before construction begins, so the latest surge may simply reflect past sales. But the report also suggests developers are betting the condo market will be less affected by headwinds including higher borrowing costs and tighter mortgage qualification rules that are currently hitting Toronto housing.

“It’s probably lagging a little bit. Historically you tend to see supply follow demand,” said Robert Kavcic, an economist at Bank of Montreal. “The other nuance here is that a lot of the policy changes we’ve seen over the last year, they really had a bigger impact on the higher end of the single detached housing market.” [..] Construction is picking up in Toronto just as sales begin to slide, after various levels of government and regulators took measures to curb surging prices. Most recently, tougher mortgage guidelines came into play on Jan. 1, making it harder for prospective buyers to qualify for loans. Many buyers rushed into the market in December to get ahead of the rules.

Transactions fell 35% in February from a year earlier to 5,175 units, according to data released Tuesday by the Toronto Real Estate Board. It was the weakest February for sales since 2009. Prices are holding up better, particularly in the condo segment, which has gained consistently over the past year and is up 20% since last February. Prices for single-detached homes have fallen 12% since reaching a record last year. Fundamentals that favor condos seem to be at work, as rising immigration levels drive demand. And since the net effect of the new regulations is to limit the size of mortgage credit, the tougher rules may be buoying the less-expensive condo market.

Thumbscrews.

• EU Freezes Brexit Talks Until Britain Produces Irish Border Solution (Ind.)

The EU has thrown down an ultimatum to Theresa May in Brexit talks, warning that it will not open discussions about trade or other issues until the Irish border question is solved. Speaking in Dublin alongside the Irish Prime Minister Leo Varadkar, European Council President Donald Tusk said talks would be a case of “Ireland first” and that “the risk of destabilising the fragile peace process must be avoided at all costs”. “We know today that the UK Government rejects a customs and regulatory border down the Irish Sea, the EU single market, and the customs union,” the Mr Tusk said. “While we must respect this position, we also expect the UK to propose a specific and realistic solution to avoid a hard border.

“As long as the UK doesn’t present such a solution, it is very difficult to imagine substantive progress in Brexit negotiations. “If in London someone assumes that the negotiations will deal with other issues first before the Irish issue, my response would be: Ireland first.” British negotiators have long been keen to move to discussions about trade and had hoped to do so after the March meeting of the European Council in two weeks, but Mr Tusk’s latest ultimatum suggests further delays could be in store. The EU says a withdrawal agreement must be negotiated by October to give it time to ratify the deal before the UK falls out of the bloc in March 2019.

Mr Tusk recalled that the Good Friday Agreement, whose 20th anniversary is next month, had been “ratified by huge majorities north and south of the border”. “We must recognise the democratic decision taken by Britain to leave the EU in 2016 – just as we must recognise the democratic decision made on the island of Ireland in 1998 with all its consequences,” he said, in a play on the rhetoric used by Brexiteers regarding the 2016 EU referendum. The EU27 nations granted the UK “sufficient progress” to move to the rest of Brexit talks in the December meeting of the European Council after the UK made a commitment to avoid a hard border on the island of Ireland at all costs.

30-mile lines of waiting trucks. That was reason no. 1 to establish the EU. Well, they’re back.

• Calais ‘To Be 10 Times Worse Than Irish Border’ After Brexit (G.)

The boss of the port of Calais has said there could be tailbacks up to 30 miles in all directions and potential food shortages in Britain if a Brexit deal involves mandatory customs and sanitary checks at the French ferry terminal. Jean-Marc Puissesseau made an impassioned plea to Theresa May and Michel Barnier to put plans in place immediately to avert congestion in Calais and Dover, where bosses have already warned of permanent 20-mile tailbacks. At the same time a leading politician for the Calais region said the problems in France would be 10 times worse than at the Irish border. At a private meeting at the European parliament, Xavier Bertrand, a former French health minister and the president of the Hauts-de-France political region, said politicians needed to grasp the magnitude of the problem.

“I know Ireland is going to be a real problem, but please remember the economic issues in Ireland are 10 times smaller than what is going to happen here,” he said. “This is a black scenario, but it is going to get darker and darker,” he said, urging politicians in Brussels and London to take urgent action by setting up working groups and listening to business. Bertrand angrily denounced those who had power to influence the Brexit outcome. It was not right that economic operators should be expected to “sit on their hands waiting very anxiously for something to happen”.

At the same meeting, Puissesseau said both sides would be affected by the problems at the ports, with suppliers from the UK trying to get their goods through strict EU controls treated no better than those from a developing country. “The UK is part of the 21st century. But this takes us back 100 years. This is sad,” he said. “From Brexit day, 100% of our traffic will be from outside the EU. I tell you honestly that GB will be a third country, this frightens me. There’s such a long history between the UK and EU.” “At the moment, 70% of food imported comes from the EU. Even if that goes down to 50% after Brexit because of controls, it still needs to flow smoothly; people still need to eat,” he said.

$8,500 as I write this, -8.46%.

• Bitcoin Tumbles Further In Broad Selloff For Cryptocurrencies (MW)

Selling intensified for digital currencies on Friday, as the price of the No.1 cryptocurrency bitcoin pushed below $9,000. The price of a single bitcoin fell 4.8% to $8,847.85, but bounced off a low of $8,370.80, according to CoinDesk. In a week, bitcoin has dropped around 20%. Losses were widespread across cryptocurrencies. Ether was down 4.5% to $671.66, bitcoin cash slid 6.4% to $970.66 and Litecoin fell 6.2% to $166.22, according to CoinDesk. Ripple tumbled 10% to $0.78, according to CoinMarketCap. The moves build on sharp drops on Thursday, which some suggested were due to technical factors.

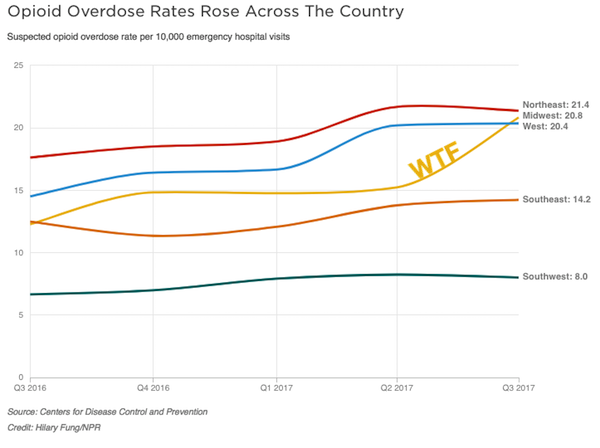

Winning.

• US Is Experiencing The Highest Drug Overdose Death Rates Ever (ZH)

Across the United States, government officials are struggling to combat the next wave of the opioid epidemic, which is expected to deliver a massive blow to the heartland. A new report from the Centers for Disease Control and Prevention (CDC) confirms the opioid crisis has dramatically worsened since the second half of 2016. Raw data from hospital emergency rooms show a significant increase in drug overdoses across the U.S. In a press briefing on Tuesday, CDC Director Anne Schuchat, M.D., warned that the U.S. is currently experiencing the highest drug overdose death rates ever.

In the newly issued report, which examined data from 16 states, emergency department visits for suspected opioid overdoses jumped 30% from July 2016 through September 2017. In some regions of the country, overdoses were far more significant, but overall, data from most areas showed the opioid crisis is worsening, despite President Trump’s new initiative to tackle the epidemic.

Save the symbols?!

• Chinese Panda Conservation Park To Be Twice The Size Of Yosemite (G.)

The Bank of China has pledged at least 10bn yuan (£1.1bn) to create a vast panda conservation park in south-west Sichuan province, the Chinese forestry ministry has said. The Sichuan branch of the central bank signed an agreement with the provincial government to finance the vast national park’s construction by 2023. The park aims to bolster the local economy while providing the endangered animals with an unbroken range in which they can meet and mate with other pandas in order to enrich their gene pool.The ministry said the park will measure 2m hectares (5m acres), making it more than twice the size of Yellowstone national park in the US.

Zhang Weichao, a Sichuan official involved in the park planning, told the state-run China Daily the agreement would help alleviate poverty among the 170,000 people living within the project’s proposed territory. Plans for the park were initiated in January last year by the ruling Communist party’s central committee and the state council, the China Daily reported. Giant pandas are China’s unofficial national mascot and live mainly in the Sichuan mountains, with some in neighbouring Gansu and Shaanxi provinces. An estimated 1,864 live in the wild, where they are chiefly threatened by habitat loss. Another 300 live in captivity.

By treating the oceans as our garbage bin, we will make it exactly that.

• Discarded Fishing Gear Massacres Whales, Dolphins, Seals, Turtles, Birds (Ind.)

The world’s biggest seafood firms are all contributing to the deaths of more than 100,000 whales, dolphins, seals, turtles and seabirds that are killed in agony every year by discarded fishing equipment, according to a new report. Many of the creatures are drowned, strangled or mutilated by plastic gear lost or abandoned at sea, while others suffer “a prolonged and painful death, usually suffocating or starving” either because they cannot fish or their stomachs are full of plastic. Campaigners believe the fishing litter problem is becoming so bad that the oceans could end up unable to provide any catches for humans to eat.

They say “ghost gear” has become a huge but overlooked threat to marine life, and 640,000 tons of it are added to the oceans each year – a rate of more than a ton every minute. A new study analysed the approaches to fishing equipment of the world’s 15 biggest seafood companies, to rank them in five categories – but found that none could be ranked in the top two as having “best practice” or making “responsible handling” of their fishing gear integral to their business strategy. [..] The report, entitled Ghosts beneath the Waves, says abandoned and lost gear is four times more likely to trap and kill creatures than all other forms of marine debris combined, and more than 70% of visible plastic in the sea is fishing-related.

Microplastics – minuscule pieces – were found in the digestive tracts of 80% of seals tested off the coast of Ireland, while other research cited found that plastic accounted for 69% of the debris ingested by whales. Other studies said 98% of whale entanglements involved ghost gear, while 82% of North Atlantic right whales have become entangled at least once. “This is a huge crisis of animal suffering, yet hardly anyone is talking about it,” said World Animal Protection. In one deep water fishery in the north east Atlantic 25,000 nets have been recorded as lost or discarded each year, according to the report. “Even within small areas, the amount of ghost gear can be staggering,” it said. “The Florida Keys National Marine Sanctuary, for example, is estimated to be littered with 85,000 active ghost lobster and crab pots.