Arthur Rothstein Texas Panhandle Dust Bowl Mar 1936

I already proposed a few days ago that the recent ECB stress test exercise was such a shambles, it may well have been designed to fail on purpose. In order for Mario Draghi and his Goldman made men to be freed from that pesky German resistance against full blown QE, i.e. large scale purchases of government bonds from the 18 countries that make up the eurozone.

And perhaps the other 10 that are part of the EU without using the common currency. The sky’s the limit. Just how bad that would be is hinted by Tracy Alloway for the FT as she describes how QE tempts investors into asset classes with far more risk than they should have on their hands, simply because they feel the Fed – or some other central bank – has their back.

Sounds like the perfect way to separate a whole lot of people from their money. Which is why Draghi is so tempted to try it on. QE destroys societies, economies and financial systems, it doesn’t heal them. So maybe it’s a touch of genius that the great powers of global finance have first pushed Keynes into the academic world and then academics like Bernanke and Yellen into positions such as head of the Fed, making everyone blind to the fact that what they think is beneficial, including many who think they’re real smart, actually hurts them most.

When you looked at it in that light, you would be forgiven for thinking Draghi had better hurry, because higher rates and a higher dollar will give away much of that game. And not just in America.

But Stupor Mario has one great excuse left: his hands are tied. Not for long anymore, perhaps, since the ECB is set to become the sole EU banking supervisor, but that is not the same as having a full banking union, the prize the real big banking boys have their eyes on. Control over all EU banks from one central point, with the power to shut them down, squeeze them dry, and make them beg for mercy. Athens, Greece based economics professor Yanis Varoufakis has some words on how Mario’s hands are tied:

The ECB’s Stress Tests And Our Banking Dis-Union: A Case Of Gross Institutional Failure

What gives the Fed-FDIC power over banks is the common knowledge that, when it assesses that a bank is insolvent, it has no serious qualms saying so. The reason, of course, is that it not only has powers of supervision (i.e. access to their books) but, crucially, powers of resolution and, if it so judges, the power to force mergers or to recapitalise the failing bank.

Suppose that, instead, the Fed-FDIC had, as the ECB does, only the power to scrutinise the banks’ books. Imagine now that, with only this power, the Fed-FDIC were to discover that some bank in Nevada or Missouri is in trouble. If the Fed-FDIC’s charter precluded it from doing anything else other than to announce the bank’s insolvency, its supervisory power would mean little.

For if it were common knowledge that the fiscally stressed State of Nevada or Missouri would have to borrow from money-markets to pay for the depositors’ guaranteed deposits, as well as for any new capital the banks needed to be salvaged, the rest of the state’s banks would face a run, the states would see their borrowing costs skyrocket and, soon, a combined banking and fiscal crisis could be rummaging throughout the ‘dollar zone’.

To put this crudely, the good people at the Fed would have no alternative than to keep their mouths shut, to conceal the bad news, to cover up for the bank’s problems and try to find some hush-hush way of bolstering its capitalisation.

This is precisely the sad state our so-called Banking Union has pushed the ECB’s supervisors into. As long as the ECB is not the sole authority on bank resolution, and as long as funds for dealing with insolvent banks are to come (in the final analysis) from the fiscally stressed states, the death embrace between weak states and fragile banks will continue.

If the ECB guys have too narrow a mandate for their own taste, or they don’t like their salaries or perks, they should speak out about that. Not behind closed doors, but in public. And not only in general terms, but in specifics, if it leads to situations like this where an entire year and millions of euros are spent on an audit that they know beforehand will be way less than truthful, let alone useful. These people receive generous salaries provided by European taxpayers, and the least they should do is be honest. I know, who am I kidding, right?

So what’s the solution for Europe, handing over the whole shebang to Draghi and his ilk? No, it isn’t, but they’re getting real close to achieving just that. And once the banking union is a fact, it will be that much harder – and expensive – for Greece and Italy and Cyprus and Spain and Portugal to wrestle themselves out of the straightjacket the EU has become.

It’s no coincidence that it was Greek and Italian banks who got hit hardest by the tests, flawed and fake as these were. The EU has become a power game more than anything, a ploy to induce so much fear into the financially weakest they’ll lose the belief that they can stand their own legs. And then they can be subordinated slaves forever.

As I said Sunday in Europe Redefines ‘Stress’, the stress tests were little more than a joke. They were designed that way.

In that article, I referred to Bloomberg’s Mark Whitehouse writing about a different, more or less parallel stress test, performed by the Center for Risk Management in Lausanne, inTesting Europe’s Stress Tests. My comment then:

The ECB’s Comprehensive Assessment says $203 billion was raised since 2013, leaving ‘only’ €25 billion yet to be gathered. The Swiss report says €487 billion is needed just for 37 of the 130 banks the ECB stress-tested. Of the banks the Swiss identify as having the greatest capital shortfalls, most passed the EU tests. Judging from the graph, the 7 banks in need of most capital have an aggregate shortfall of some €300 billion alone.

Among them the 3 main, and TBTF, French banks, who all passed with flying colors and got complimented for it by French central bank governor Christian Noyer today, but according to the Center for Risk Management are about €200 billion short between them. Which means France as a nation has a stressed capital shortfall of over 10% of its GDP, more than twice as much as the next patient.

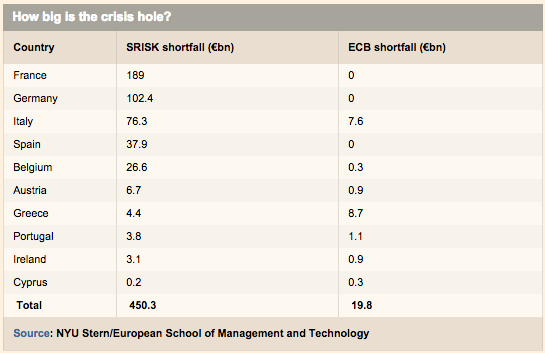

Turns out, the Swiss were not the only ones doing an alternative stress test. Sachsa Steffen at the European School of Management (ESMT) in Berlin, and Viral Acharya at the Stern School of Business in New York did one as well. And the similarities between the two alternative ones, as well as the differences between both their results and the ‘official test’ are so big it’s ludicrous. Tom Braithwaite in an excellent piece for FT:

Alternative Stress Tests Find French Banks Are Weakest In Europe

On Sunday, Christian Noyer, governor of the Banque de France, was crowing about the “excellent” performance of French banks on the European stress tests Many of their Italian and Greek counterparts might have flunked but France could be proud of its banking sector. “The French banks are in the best positions in the eurozone,” said Mr Noyer. Not so fast.

Two days earlier, a different test found that the French financial sector was the weakest in Europe. The team with the temerity to deliver this bucket of cold water to Paris works at the wonderfully named Volatility Institute at New York University’s Stern school and presented its findings from a safe distance – a financial conference at the University of Michigan. The chief architect, Viral Acharya, has worked on systemic risk ever since the last crisis, attempting to design a bank safety test that can be run all the time – not at the whim of regulators.

Using his methodology, which he calls SRISK, Mr Acharya found that in a crisis French financial institutions would have a capital shortfall of almost $400bn, worse than the US and UK despite their much bigger financial sectors. Looking just at the French banks tested in the ECB stress tests, which found zero capital shortfall, SRISK came up with €189bn. Mr Acharya did not have access to the 6,000 officials who scoured balance sheets across Europe to gauge the health of the continent’s banks. But his results, which have implications for other countries, including China, should not be ignored. How big is the crisis hole?

Take Société Générale. France’s second-biggest bank by market value did fine on the ECB’s stress test. But on Mr Acharya’s measure, the bank has a large capital shortfall in a crisis. There are a couple of big reasons for the difference. First, SRISK takes into account the banks’ total balance sheet without regard for risk: unlike the ECB, it does not attempt to distinguish between €1m of German Bunds and a €1m loan to a dipsomaniac farmer with a rusty tractor. Second, it does not care what banks’ book value of equity is; it uses what the stock market says it is.

Under the ECB’s methodology, SocGen has €36.6bn of equity today and, in a crisis, would have €30.7bn of equity against €377bn of risk-weighted assets. That equates to a passable 8.1% capital ratio even in a deep recession. According to Mr Acharya’s methodology, the bank has only €30bn of market equity today against €1,322bn of assets for a much weaker capital ratio of 2.3%. In a crisis, when market values would plunge further, SocGen would be left with a shortfall of more than €60bn.

Using the stock market to compute a bank’s equity makes SRISK vulnerable to irrational optimism or irrational pessimism of investors. But Mr Acharya finds three good reasons to use it. “Markets told us that subprime MBS [mortgage-backed securities] had become poor in quality and liquidity; book values and regulatory risk weights did not ..”

Market values are also harder to manipulate by management through understatement of losses or provisions. Finally, banking crises are caused by drying up of credit by financiers. Financiers are not interested in book values or regulatory capital per se, but whether the firm can raise capital if needed to repay them. This is best captured by market value.”

It is not just France’s regulators and banks that might be well-advised to stop patting themselves on the back and consider other measures of systemic risk. Europe’s aggregate SRISK has fallen since 2011, with the deleveraging of balance sheets following the eurozone crisis. Systemic risk in the US has also fallen by half since 2008. But risk in China has picked up significantly and now surpasses the US. If anything, Mr Acharya notes, the problem is likely to be understated because of the amounts of off-balance sheet debt in China.

In the US, JPMorgan Chase’s leverage might be much better than its French counterparts, but its SRISK is bigger: a $98.4bn shortfall in a crisis. MetLife, which is considering suing the US government over its designation as a systemically important company, is found to pose a bigger systemic risk than Goldman Sachs.

If you believe that financial companies always appropriately value their assets and never try to massage the value of their equity and if you believe that officials are always diligent in examining banks’ accounting then SRISK is a waste of time. But if you believe this you haven’t been paying attention for the last decade.

I’m tempted to say someone should save the Greeks and Italians from the power game that’s being played with them, but in reality they should save themselves. That French banks come out of the ECB test with flying colors, while in two separate other tests they look absolutely abysmal, should tell us all enough about what the game is here.

There are two major countries in the eurozone, and they have all the political power there is to go around. As they are sinking, the poorer nations will be forced to make up the difference. Just like the Romans squeezed their peripheral territories so much they caused the end of their empire, and were conquered and flattened by the peoples living there.

I know I’ve said it many times already, but I’m not going to give up: the EU should be broken up, and its delusional leadership structure torn to bits, as soon as possible, or Europe is once going to be a theater of war.

The very thing the EU was supposed to prevent, it will be the source of. In exactly the same way that QE tears apart economies and societies. Presented as the sole solution to the debt crisis, but in reality the driving force behind increased inequality, ever lower wages and ever fewer benefits, and perhaps most of all the nigh complete suffocation of the younger generations, so the older – and therefore richer – can enjoy their so-called well-deserved retirement.

This whole thing is so broken and perverted it’s getting hard to understand why anybody would want to continue clinging on to it. But then, what does anybody know? 95%+ of people have been reduced to pawns in someone else’s game, and they have no idea whatsoever.

And maybe that’s genius. If you see people’s ignorance as a sufficient reason to prey upon them, that is, as many of our ‘leaders’ do. It’s what gives them power, exploiting other people’s weaknesses. And that is then seen as everyone ‘obeying’ some sort of natural law.

That’s what QE and stress tests tell me. That Greeks and Italians are no longer just being preyed upon by their own people, but by others too, with different cultures and languages and entirely different goals and ideals. And that cannot end well. You might as well put them all to work in a chaingang right this moment.

Home › Forums › Life Lessons To Derive From QE And Stress Tests