Camille Pissarro Rue Saint-Lazare, Paris 1897

Britain and many other countries. Their economies are propped up by bubbles.

• Britain Can’t Cope With A Fall In House Prices (Ind.)

[..] most properties in the UK still belong to households. Families, by and large, don’t need to sell. So what would falling property prices mean for them? First, many pension funds and investment bonds rely on UK property to generate income for their beneficiaries. Second, we have what economists call the wealth effect. Economists have long associated consumers’ perceived real estate wealth with spending behaviour: if you believe your house is worth a lot, you feel financially secure. And then you allow yourself to save less and spend more. Just consider the rising number of people who plan to subsidise their retirement with wealth generated by their homes. If their assumed valuations start to look shaky, these people will spend less to build up their savings. The pain would be felt by many: about 64% of households in England are owner-occupiers.

The wealth effect is important in most developed economies but even more so in the UK which relies on ever-rising levels of consumer spending for its growth. A 10% fall in the value of dwellings in the UK would correspond to a loss of wealth equivalent to more than the value of all the cars exported from the UK in a decade. The climate of economic uncertainty, reduced consumption and falling real estate values brings an additional problem for the UK. Britain has long had a trade deficit, but it has also benefited from positive foreign direct investment. The current account itself has been in the red for nearly 20 years now but the hundreds of billions of inward foreign investment channelled to UK property over the same period meant that this deficit remained manageable – just about.

According to the Bank of England, overseas companies have accounted for roughly half of all UK commercial real estate transactions since 2013. If international investors expect prices to fall in any sustained way, the inflow of money would stop and many would sell up. Why buy or hold an asset just at the start of what might be a long decline? This would not only put pressure on real estate prices but would affect UK GDP, reduce government revenues and worsen the UK current account position. The credit rating of the UK would come under more pressure, and trillions of UK government debt would cost more to refinance. Then the UK government deficit would deteriorate further, taxes might rise to cover for this and the domino effect would be in full cry, spreading to all sectors of the economy, similar to events in Greece.

Bloated. No heartbeat.

• A Remarkable Run for Stocks Gets More Extraordinary (BBG)

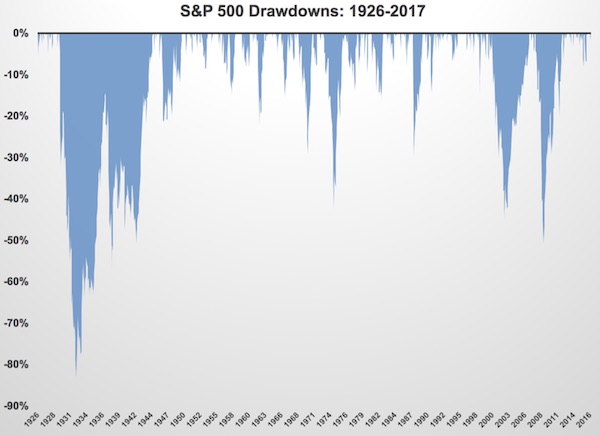

With a 2% gain in September, the S&P 500 Index has set a record: positive returns in each of the first 10 months of the year. There’s never been a full calendar year when this has happened every month. Going back to November 2016, the index has ripped off 12 consecutive monthly gains. The S&P hasn’t had a down quarter since the third quarter of 2015, a streak of eight in a row without a loss. Since the start of 2013, 18 of the past 19 quarters have been positive. And it’s not like stocks are melting up either. They are going up slowly as volatility is slowly going down. Not only have stocks been consistently profitable recently, but they have done so with remarkably low volatility. This year, there has yet to be a 2% move up or down on the S&P 500.

For a frame of reference, in 2009, there were 55 separate 2% up or down days and there were 35 in 2011. The annualized volatility of daily returns on stocks since 1928 has been 18.7%. For 2017, that number is 7%, a little more than one-third of the long-term average. The average absolute daily price change this year on the S&P 500 is just 31 basis points. If the year ended right now, that would be the lowest daily price change on record since 1965. The worst peak-to-trough drawdown is just 2.8% this year. Over the past 100 years, the average intrayear drawdown in stocks has been around 16%. The shallowest calendar-year peak-to-trough drawdown was in 1995, when the worst loss in stocks was just 3.3% for the year.

So investors in U.S. stocks have had double-digit gains three-quarters of the way through the year, with increases every month, nonexistent volatility, and nothing even approaching a 5% correction. It’s looking like a record-breaking year in terms of a calm market. As far as investing in stocks goes, this year has been about as good as it gets – so far. It’s worth remembering that stocks are cyclical, even if those cycles don’t run on set schedules. The following shows the historical drawdown profile of the S&P 500 going back to just before the Great Depression:

There are no investors: “There is no real advantage in the global marketplace. Everything is so tight, it is hard to pick a winner from a group that is fake.”

• Bill Gross Blames Fed For ‘Fake Markets’ (R.)

Influential bond investor Bill Gross of Janus Henderson Investors said on Monday that financial markets are artificially compressed and capitalism distorted because of the U.S. Federal Reserve’s loose monetary policy. “I think we have fake markets,” Gross said at a Janus Henderson event. Investors should brace for higher Treasury bond yields as the Fed begins to unwind its quantitative easing program but yields will edge up “only gradually,” he said. Gross, who oversees the $2.1 billion Janus Henderson Global Unconstrained Bond Fund, said the Fed’s loose monetary policy had resulted in investors chasing yield and thus producing tight corporate spreads everywhere around the globe.

“Even China and South Korea – perfect examples of the risk trade – are at very narrow (corporate spread) levels. There is no real advantage in the global marketplace. Everything is so tight, it is hard to pick a winner from a group that is fake.” Gross reiterated his warning that Fed Chair Janet Yellen and other global policy makers should not rely on historical models such as the Taylor Rule and the Phillips curve “in an era of extraordinary monetary policy.” Economists John Taylor and A.W. Phillips devised models for guiding interest-rate policy based, respectively, on inflation and the unemployment rate. Those models disregard the importance of private credit in the economy, according to Gross.

In complete denial of what they have wrought.

• ECB’s Knot Warns of Market Correction as Risk May Be Underpriced (BBG)

Financial markets may be underpricing global risks, leaving them vulnerable to a major correction, according to European Central Bank Governing Council member Klaas Knot warned. As global stocks surge, measures of volatility suggest unprecedented calm even as crises around the world – including the Catalan separatists in Spain, Turkey’s diplomatic row with the U.S., North Korea’s missile tests and the danger of a hard Brexit – make political headlines. “It increasingly feels uncomfortable to have low volatility in the markets on the one hand while on the other hand there are risks in the global economy,” said Knot, who is also the president of the Dutch Central Bank.

Similarly, a sooner-than-expected normalization of U.S. monetary policy – where financial markets see a slower pace of rate hikes than what the Federal Reserve communicates – would quickly turn investor sentiment, the DNB wrote in a report on financial stability which Knot presented in Amsterdam on Monday. That makes the “risk of sharp market corrections real,” it said. Still, Knot said there’s “no one within the context of the ECB already talking about an increase of interest rates. Rates will “stay low for a long time.” In the run-up to the next policy decision on Oct. 26, ECB officials are showing differing preferences for the way forward with quantitative easing, which is set to run at €60 billion a month and total almost €2.3 trillion by the end of December.

Executive Board member Peter Praet, who crafts the policy proposals, said last week that calm markets may allow the final stages of the bond-buying plan to be dragged out. “The program has achieved what realistically could be expected from it,” Knot said about QE, adding that it supported growth, reduced investment costs and ended deflationary risks.

Talk!

• Catalan President To Declare “Gradual Independence” On Tuesday (ZH)

In the latest twist ahead of tomorrow’s much anticipated “next step” announcement to be made by the Catalan secessionists, which is still to be formalized, Spain’s EFE newswire reports that Catalonian President Carles Puigdemont has reportedly drafted a declaration of “gradual independence”, that will be “gradually effective” and which will plan to start a constituent process. The declaration, which will cap what El Periodico dubbed “the most critical moment for Catalonia” will allegedly insist on Catalonia’s wish to negotiate with central government and the need for mediation, although in an indication that Puigdemont may be back tracking from his hard-line “binary” stance, EFE adds that the Declaration won’t lead to parliamentary vote, and as such may be non-binding. The news is the latest development in a fast-paced day, in which as we reported earlier this morning, the ruling People’s Party issued a thinly veiled death threat to the President of Catalonia.

“Let’s hope that nothing is declared tomorrow because perhaps the person who makes the decalartion will end up like the person who made the declaration 83 years ago.” Additionally, perhaps as a Plan B, Catalan secessionists opened a second-front in their campaign against the government in Madrid, urging the opposition Socialists to forge a coalition to oust Spanish Prime Minister Mariano Rajoy, Bloomberg reported and added that while the Socialists have so far refused to sign up to the plan, the Catalan groups pushing it have already persuaded the populist Podemos party to back and accept a Socialist-only government. Should the Socialists get on board, the alliance would have 172 seats in the 350-strong chamber and would look to add the Basque Nationalists to form a majority. Rajoy heads a minority administration with 134 deputies and can be toppled with a no-confidence motion.

Meanwhile, as reported overnight, Catalan secessionist leader Carles Puigdemont faced increased pressure on Monday to abandon plans to declare independence from Spain, with France and Germany expressing support for the country’s unity. The Madrid government, grappling with Spain’s biggest political crisis since an attempted military coup in 1981, said it would respond immediately to any such unilateral declaration.

But then there’s this.

• Dear Catalans – A Message From The Chairman (Ren.)

Dear Catalans, I must confess that I feel rather like St. Paul must have felt when he wrote to the Corinthians – the need to address an entire region is a grave affair. But the matter I must address today is of great importance to our community of nations: Enough is enough. We need to get a few things cleared up before this regrettable idea of independence goes any further. There are a number of things that have been rather opaque since we set up the EU. This was deliberate – there was simply no reason for you to know until now. There should never have been any need to disclose this information, and indeed there wouldn’t have been, were it not for those tiresome Brits setting such a terrible example for everyone last year. We must resolve this matter quickly so that we can all get back to the business of being one big happy family again. Here’s what you need to know: We ‘own’ Spain, and Spain ‘owns’ you.

Since you have seen reason to doubt the binding nature of this arrangement, perhaps I should explain to you how it works: Catalonia is a wholly owned subsidiary of Spain – this is all covered in the constitution, and is totally binding, although you may not have realised that when you voted upon it. 1) It was democratic you see – one simply must read the small print, but of course one never does, does one? 2) Spain is a subsidiary of the EU – this is all covered by EU treaty, which of course is also binding, as has been explained on a number of occasions by our Head of European Political Operations, dear Jean-Claude. The following points may be difficult for you to understand, because we’ve never had to explain the structure beyond this point.

3) The EU is not owned by anyone, but of course ‘ownership’ and ‘control’ are really the same thing, but without all the legal drudgery that has become so tiresome of late. 4) The EU is controlled by the monetary system that we put in place. I am not referring to the euro, which is simply the local mechanism for this region. I am referring to the banking system, which over-arches everything. The banks are the organisations that loan the money into existence in the first place. You didn’t know that did you? Don’t worry, very few people do…and that’s worked very well until now. This is how it works: a) Governments don’t actually buy anything with taxes. They spend money that the banks loan to them by buying their IOUs, AKA sovereign bonds. b) When governments eventually get round to collecting taxes they use them to cancel some of their IOUs, plus they pay interest on all of them – naturally.

c) Since all politicians inevitably make promises that they can’t afford in order to get elected – a practice that we encourage by funding both sides – there is never enough taxation collected to fully redeem the IOUs, and there never will be. Why not? Because of the 8th wonder of the world – compound interest! Governments across the globe are paying the banks interest on interest on interest on money that they could have just printed for themselves in the first place!

Major demo’s all over France today. Macron plans to fire 100,000+ civil servants.

• The Rise and Fall of Emmanuel Macron (Steve Keen)

Since his election, Macron’s popularity has plunged faster than any French president in history. Attempts to explain this decline have focused on his pompous approach to governance—literally professing to want to govern like Jupiter. But there is a deeper cause. He has misdiagnosed the origins of the French economic malaise, and therefore his Jovian economic thunderbolts will do more harm than good. It’s easy to show the blatant errors in the president’s perspective by merely looking at the data. Macron’s economic agenda cites an excessively large public sector as the fundamental cause of France’s malaise, and the main ‘Evidence for the Prosecution’ is the towering level of government debt: as of March 2017, this was 111% of GDP, almost twice the 60% of GDP maximum allowed by the Maastricht Treaty.

But private liabilities are worse still: 187% of GDP. So, why does Macron, in common with politicians of almost all stripes, not worry about this far higher level of debt? The reason is that, given he was schooled in mainstream economics for his Master’s degree at ENA (École Nationale d’administration), Macron accepts the argument that private debt doesn’t matter. It’s just a “pure redistribution”, to quote Ben Bernanke, which “absent implausibly large differences in marginal spending propensities” between savers and lenders, “should have no significant macroeconomic effects.” This comforting belief is sharply contradicted by the data for countries which, like France, have a private debt ratio well in excess of 100% of GDP. If Bernanke’s assumption were correct, there would be little or no correlation between credit (the annual change in private debt) and unemployment.

However, in his home country of the USA, the relationship between credit and unemployment since 1990 is minus 0.91: meaning rising credit reduces unemployment, and falling credit increases it. In France’s case, the correlation is lower but still substantial at minus 0.62, when according to mainstream economics, it should be close to zero. So credit matters, not merely because savers are much less likely to consume than debtors, but because bank credit creates new money. Since this new cash is spent by the borrowers, it adds to aggregate demand. And falling credit over time—which France has generally been experiencing since the early 1970s—therefore implies rising unemployment.

This could spiral out of control. Why would any company take the risk of deadly incidents, instead of demanding recalls?

• Kobe Steel Faked Data For Metals Used In Planes And Cars (BBG)

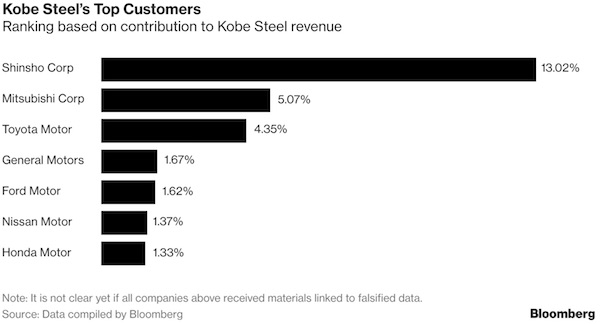

Kobe Steel unleashed an industrial scandal that reverberated across Asia’s second-largest economy after saying its staff falsified data related to strength and durability of some aluminum and copper products used in aircraft, cars and maybe even a space rocket. The Japanese company’s stock ended 22% lower in Tokyo as customers including Toyota, Honda and Subaru said they had used materials from Kobe Steel that were subject to falsification. Boeing, which gets some parts from Subaru, said there’s nothing to date that raises any safety concerns. Rival aluminum makers gained. Kobe Steel’s admission raises fresh concern about the integrity of Japanese manufacturers, and follows Takata misleading automakers about the safety of its air bags, and last week’s recall by Nissan of cars after regulators discovered unauthorized inspectors approved vehicle quality.

Kobe Steel said on Sunday the products were delivered to more than 200 companies but didn’t disclose customer names, with the falsification intended to make the metals look as if they met client quality standards. Chief Executive Officer Hiroya Kawasaki is now leading a committee to probe quality issues. The fabrication of figures was found at all four of Kobe Steel’s local aluminum plants in conduct that was systematic, and for some items the practice dated back some 10 years ago, Executive Vice President Naoto Umehara said on Sunday. Toyota said it has found Kobe Steel materials, for which the supplier falsified data, in hoods, doors and peripheral areas. “We are rapidly working to identify which vehicle models might be subject to this situation and what components were used,” Toyota spokesman Takashi Ogawa said. “We recognize that this breach of compliance principles on the part of a supplier is a grave issue.”

Kobe Steel said it discovered the falsification in inspections on products shipped from September 2016 to August 2017, adding there haven’t been any reports of safety issues. The products account for 4% of shipments of aluminum and copper parts as well as castings and forgings. “The incident is serious,” said Takeshi Irisawa at Tachibana Securities. “At the moment, the impact is unclear but if this leads to recalls, the cost would be huge. There’s a possibility that the company would have to shoulder the cost of a recall in addition to the cost for replacement.”

We might be in for some crazy surprises in the UK. They’ve lost the script.

• Prepare For No-Deal Brexit, Theresa May Warns Britain (Ind.)

Theresa May has warned the British public to prepare for crashing out of the EU with no deal, setting out emergency plans to avoid border meltdown for businesses and travellers. As hopes of an agreement appeared to fade at home and abroad, the Prime Minister – for the first time – set out detailed “steps to minimise disruption” on Brexit day in 2019. They included plans for huge inland lorry parks to cope with the lengthy new customs checks that will be needed – to avoid ports becoming traffic-choked. The move came as Ms May admitted she expected the deadlocked negotiations to drag on for another year before any possible breakthrough. At Westminster, Brexiteer Tories exploited the Prime Minister’s weakness – after last week’s attempted coup – to demand that Chancellor Philip Hammond, and other voices of compromise, be sidelined.

Bernard Jenkin attacked the EU for “refusing to discuss the long term relationship between the EU and the UK”, asking the Prime Minister: “When does she call time?” Meanwhile, in Brussels, Ms May’s insistence that she would make no further compromises in the talks – she told the EU “the ball’s in their court” – was firmly rebuffed. “There has been, so far, no solution found on step one, which is the divorce proceedings, so the ball is entirely in the UK’s court for the rest to happen,” said Margaritis Schinas, the European Commission’s chief spokesman. Laying bare the impasse, Brexit Secretary David Davis did not attend the first day of the resumed talks, although he is expected to be in Brussels on Tuesday.

In the Commons, the Prime Minister continued to insist that “real and tangible progress” towards an agreement had been made since her high-profile speech in Florence last month. But she also made clear that new policy papers on trade and customs were intended to show Britain could operate as an “independent trading nation” – even if no trade deal was reached.

Always Pilger.

• The Rising Of Britain’s ‘New Politics’ (John Pilger)

Delegates to the recent Labour Party conference in Brighton seemed not to notice a video playing. The world’s third biggest arms manufacturer, BAE Systems, supplier to Saudi Arabia, was promoting guns, bombs, missiles, naval ships and fighter aircraft. It seemed a perfidious symbol of a party in which millions of Britons now invest their political hopes. Once the preserve of Tony Blair, it is now led by Jeremy Corbyn, whose career has been very different and is rare in British establishment politics. Addressing the conference, the campaigner Naomi Klein described the rise of Corbyn as “part of a global phenomenon. We saw it in Bernie Sanders’ historic campaign in the US primaries, powered by millennials who know that safe centrist politics offers them no kind of safe future.”

In fact, at the end of the US primary elections last year, Sanders led his followers into the arms of Hillary Clinton, a liberal warmonger from a long tradition in the Democratic Party. As President Obama’s Secretary of State, Clinton presided over the invasion of Libya in 2011, which led to a stampede of refugees to Europe. She gloated at the gruesome murder of Libya’s president. Two years earlier, Clinton signed off on a coup that overthrew the democratically elected president of Honduras. That she has been invited to Wales on 14 October to be given an honorary doctorate by the University of Swansea because she is “synonymous with human rights” is unfathomable. Like Clinton, Sanders is a cold-warrior and “anti-communist” obsessive with a proprietorial view of the world beyond the United States.

He supported Bill Clinton’s and Tony Blair’s illegal assault on Yugoslavia in 1998 and the invasions of Afghanistan, Syria and Libya, as well as Barack Obama’s campaign of terrorism by drone. He backs the provocation of Russia and agrees that the whistleblower Edward Snowden should stand trial. He has called the late Hugo Chavez – a social democrat who won multiple elections – “a dead communist dictator”. While Sanders is a familiar American liberal politician, Corbyn may be a phenomenon, with his indefatigable support for the victims of American and British imperial adventures and for popular resistance movements. [..] And yet, now Corbyn is closer to power than he might have ever imagined, his foreign policy remains a secret. By secret, I mean there has been rhetoric and little else. “We must put our values at the heart of our foreign policy,” he said at the Labour conference. But what are these “values”?

Stop!

• Saudi Arabia In Huge Arms Deals With US AND Russia (N.au)

Saudi Arabia has been quietly planning to build its own military empire and over the last week, it’s announced how it plans to do so. With Donald Trump and Vladimir Putin’s help. Despite increasing criticism over the United States’ military sales to Saudi Arabia, the US State Department has paved the way for the potential purchase of controversial — and expensive — military equipment. On Saturday, the US State Department announced the approval to sell Saudi Arabia 44 THAAD anti-missile defence systems, 360 interceptor missiles, 16 mobile fire-control and communication stations and seven THAAD radars at an estimated price tag of $US15 billion, according to a press release from the Pentagon’s Defence Security Cooperation Agency.

The sale, supplied by Lockheed Martin and Raytheon – also includes 43 trucks, generators, electrical power units, communications equipment, tools, test and maintenance equipment and “personnel training and training equipment”. The department said the sale of the equipment to the Saudi people would help provide a balance to a relatively unstable environment in the Gulf and to help the US forces enlarge its allied grip on the region. “THAAD’s exo-atmospheric, hit-to-kill capability will add an upper-tier to Saudi Arabia’s layered missile defence architecture.” Meanwhile, King Salman of Saudi Arabia has entered into a preliminary agreement to purchase Russia’s S-400 surface-to-air missile defence system, he announced in Moscow last week. The king has been visiting Russian President Vladimir Putin in talks over oil and Syria, Saudi’s al Arabiya television reported. It is the first visit of a Saudi monarch to visit Mr Putin. It is expected the sale will beef-up security in the nuclear-hungry Middle East.

The US sale has not yet “concluded”, it confirmed. US Congress has 30 days to object. The THAAD – Terminal High Altitude Area Defence – missile system is used to defend against incoming missile attacks and “is one of the most capable defensive missile batteries in the US arsenal and comes equipped with an advanced radar system”, according to AFP. “This sale furthers US national security and foreign policy interests, and supports the long-term security of Saudi Arabia and the Gulf region in the face of Iranian and other regional threats,” the State Department said in a statement.

“Manufacturing jobs are forecast to fall about 30% this year..”

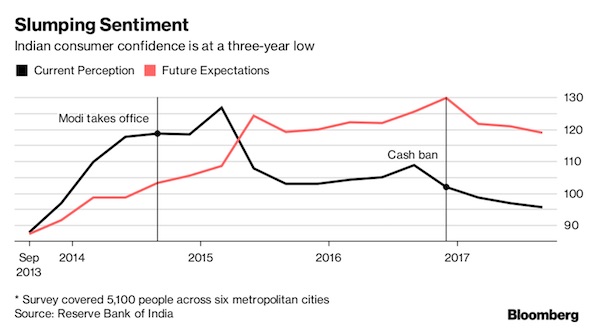

• India Had The Most Confident Consumers. Then Their Cash Disappeared (BBG)

Consumption was India’s big story. Its 1.3 billion population was expected to guzzle everything from iron to iPhones, driving global growth and cheering investors such as Apple and Goldman Sachs. For a while everything seemed smooth. Indians were the world’s most confident consumers and the $2 trillion economy was the fastest-growing big market. Then, last November, Prime Minister Narendra Modi voided 86% of currency in circulation, worsening a slowdown that had started earlier in the year. Climbing global oil prices and a tightening Federal Reserve could also complicate domestic policy making. “There are a number of uncertainties which are clouding the short-term outlook of the Indian economy,” said Kaushik Das, Mumbai-based chief economist at Deutsche Bank. “Risk of policy error remains high.”

Indians fell off the top of Mastercard’s Asia Consumer Confidence Index in the first half of 2017, and a report from the nation’s central bank last week confirmed the bleak outlook. About 27% of Indians surveyed said incomes have fallen, pushing overall sentiment into the “pessimistic zone.” Employment “has been the biggest cause of worry,” the Reserve Bank of India said. Government data show food price deflation, hurting rural incomes, and supply of new houses in India’s top eight cities falling 33% January-September, hit by a demand slowdown. Convincing Indians to consume would first require assuring them they’ll have a job. It won’t be easy for Modi to do so. Manufacturing jobs are forecast to fall about 30% this year and broader surveys show the hiring outlook is near a 12-year low. There was an absolute decline in employment between March 2014 and 2016, “perhaps happening for the first time in independent India”.

Politics can’t and won’t keep up.

• The Big Amazon Subsidy is Doomed (WS)

Amazon battled states for years to avoid having to collect sales taxes. Walmart was on the other side of the fight, along with state revenue offices. Walmart had to add sales taxes to all its sales in California, whether online or brick-and-mortar, which at the time ranged from 7.25% to 9.75% depending on location. For shoppers, that price difference was reason enough to switch to Amazon. It was in essence a massive taxpayer subsidy for Amazon. But Amazon lost that battle and started charging sales taxes in California in September, 2012. State after state followed. By early 2017, Amazon was charging sales taxes in all 45 states that have state-wide sales taxes and in Washington DC.

Still, even in 2016, online retailers dodged paying $17.2 billion in sales taxes on out-of-state sales, according to the National Conference of State Legislatures. For them, it’s a massive price advantage that other retailers didn’t get. The fight over sales taxes is based on a Supreme Court case of 1992 – Quill Corp. v. North Dakota – that barred states from forcing companies to collect sales taxes if they didn’t have physical facilities in those states, such as stores or warehouses. For Amazon, this got increasingly complicated as it is building out its distribution network, with warehouses and facilities around the country. So now Amazon is collecting sales taxes. Problem solved? Nope.

Amazon only collects sales taxes on sales of inventory that it owns (first-party sales). But Amazon is also a platform that sells merchandise owned by other sellers (third-party sales). About half of the goods sold on the Amazon platform fall into this category. Amazon leaves sales tax collections to the 2 million merchants on its platform. But they claim that it’s not their job to collect sales taxes, and most of them don’t collect them. Hence, third-party sales still get the taxpayer subsidy. Amazon isn’t the only out-of-state retailer or platform. It’s just the biggest one. eBay and many others are impacted by it too. Legally, this remains murky. But states and brick-and-mortar retailers are fighting to get the subsidy scrapped. “It’s a fairness issue,” Minnesota Senator Roger Chamberlain told Bloomberg. “Right now, there’s an unlevel playing field that disadvantages brick-and-mortar stores.”

“History is a trickster.”

• No Joy in Trumpville (Kunstler)

I took advantage of the calm before the storm, to pay a visit on Saturday to my hometown, Trumpville, a.k.a. Manhattan. My college buddy had a son who was acting in an off-Broadway play (closing night, so don’t bother asking). The city I knew as a kid — which, frankly, I never liked very much — seemed as lost and far away as Peter Stuyvesant’s quaint Dutch colonial outpost did to me in 1962. That lost city of my childhood was one in which a boy could breeze right into the Metropolitan Museum of Art on a weekday afternoon — my school was one block away from it — without the least hindrance. The place was free. There was no “donation” shakedown at the entrance. And hardly anyone was there. Do you know why? Answer: because most of the adults on the island were at work. It was a mostly middle-class city back then.

I know. It’s hard to believe, given the more recent developments in American life — the salient one being the extreme and perverse financialization of the economy. That is actually what you see manifested on-the-ground (and up-in-the-air) when you visit New York these days. To be specific, what I saw sitting on a bench along the High Line — a walking trail built on an old railroad trestle through the former Meatpacking District into Chelsea — was all the wealth of the flyover states funneled into a few square miles of land on the edge of the Atlantic Ocean. As I watched the endless stream of tourists and hipsters stride by in their selfie raptures, I pictured the various downtowns of the Midwest I’ve visited over the years — St Louis, Kansas City, Minneapolis, Detroit, Akron, Dayton, Cleveland, Louisville, Tulsa, and many more — and remembered the incredible desolation of their centers.

There was no one there, certainly no tourists or hipsters, really no activity to speak of. They were ghost cities. The net effect of financialization has been the asset-stripping of every other place in America for the benefit of a very few cities on the coasts, and especially the financial engineers within them. Thus, the ironic rise of New Yorker Trump as the avatar and supposed savior of all those people “out there” in their dying hometowns and beyond. And their tremendously bitter enmity against the “blue” coastal elites, of which Trump is a nonpareil exemplar. History is a trickster.

Home › Forums › Debt Rattle October 10 2017