Paul Gauguin The Vision after the Sermon (Jacob wrestling with the Angel) 1888

This is physically sickening. Checked front web pages of BBC, Guardian and Independent today: not a word. Hence: another gag order. Yes, there are journalists who don’t like Assange, but it’s not about liking him. It’s about your own freedom to speak. Guess that’s already gone then. I feel sick to my stomach.

• Ecuador Will Imminently Withdraw Asylum for Julian Assange (Greenwald)

Ecuador’s president Lenin Moreno traveled to London on Friday for the ostensible purpose of speaking at the 2018 Global Disabilities Summit (Moreno has been using a wheelchair since being shot in a 1998 robbery attempt). The concealed, actual purpose of the President’s trip is to meet with British officials to finalize an agreement under which Ecuador will withdraw its asylum protection of Julian Assange, in place since 2012, eject him from the Ecuadorian Embassy in London, and then hand over the WikiLeaks founder to British authorities. Moreno’s itinerary also notably includes a trip to Madrid, where he will meet with Spanish officials still seething over Assange’s denunciation of human rights abuses perpetrated by Spain’s central government against protesters marching for Catalonia independence.

Almost three months ago, Ecuador blocked Assange from accessing the internet, and Assange has not been able to communicate with the outside world ever since. The primary factor in Ecuador’s decision to silence him was Spanish anger over Assange’s tweets about Catalonia. A source close to the Ecuadorian Foreign Ministry and the President’s office, unauthorized to speak publicly, has confirmed to the Intercept that Moreno is close to finalizing, if he has not already finalized, an agreement to hand over Assange to the UK within the next several weeks. The withdrawal of asylum and physical ejection of Assange could come as early as this week. On Friday, RT reported that Ecuador was preparing to enter into such an agreement.

The consequences of such an agreement depend in part on the concessions Ecuador extracts in exchange for withdrawing Assange’s asylum. But as former Ecuadorian President Rafael Correa told the Intercept in an interview in May, Moreno’s government has returned Ecuador to a highly “subservient” and “submissive” posture toward western governments.

The only thing left on the menu is nothingburgers.

• In Historic First, DOJ Releases Carter Page FISA Application (ZH)

The Department of Justice late Friday released via the FBI’s FOIA Vault a redacted copy of the Carter Page FISA warrant application and several renewals, which accuse Page of being a Russian spy, as summarized by the New York Times – which obtained a copy of the materials through a Freedom of Information Act (FOIA) lawsuit. Of note, in the nearly two years since the application was filed, Page hasn’t been charged with any of the allegations contained within it. The previously top-secret document is the first such release by the DOJ in the 40 years since the surveillance law was enacted. In April, the DOJ said they were “processing for potential redaction and release certain [Foreign Intelligence Surveillance Act] materials related to Carter Page,” after watchdog group Judicial Watch and several other organizations filed similar lawsuits.

The application reads in part: “Identity of the target The target of this application is Carter W. Page, a U.S. person, and an agent of a foreign power, described in detail below.” “The F.B.I. believes Page has been the subject of targeted recruitment by the Russian government,” the warrant application continues. A line was then redacted, and then it picked up with “undermine and influence the outcome of the 2016 U.S. presidential election in violation of U.S. criminal law. Mr. Page is a former foreign policy adviser to a candidate for U.S. president.” -NYT. The document then concludes that Page was allegedly “collaborating and conspiring with the Russian government,” which they viewed as probably cause to spy on him – and again, which Page has never been charged with.

Page – who has repeatedly denied being a Russian spy, said in April that the FISA application was “beyond words,” and a “Joke,” while claiming that he has never served as an agent for a foreign government. We would also note that he hasn’t been charged as one. Page was targeted months earlier by FBI informant Stefan Halper, who formed a relationship with Page and several other Trump aides as part of the Obama administration’s active counterintelligence operation on the Trump campaign. While President Trump has characterized the entire counterintelligence operation as a “witch hunt,” an increasing chorus of frustrated GOP lawmakers have begun to echo his sentiment, as we are now in month 18 of post-inaugural investigation by the Department of Justice.

When intelligence becomes partisan political, that’s a big problem.

• Breannan And The 2016 Spy Scandal (Strassel)

Mr. Comey stands accused of flouting the rules, breaking the chain of command, abusing investigatory powers. Yet it seems far likelier that the FBI’s Trump investigation was a function of arrogance and overconfidence than some partisan plot. No such case can be made for Mr. Brennan. Before his nomination as CIA director, he served as a close Obama adviser. And the record shows he went on to use his position—as head of the most powerful spy agency in the world—to assist Hillary Clinton’s campaign (and keep his job).

Mr. Brennan has taken credit for launching the Trump investigation. At a House Intelligence Committee hearing in May 2017, he explained that he became “aware of intelligence and information about contacts between Russian officials and U.S. persons.” The CIA can’t investigate U.S. citizens, but he made sure that “every information and bit of intelligence” was “shared with the bureau,” meaning the FBI. This information, he said, “served as the basis for the FBI investigation.” My sources suggest Mr. Brennan was overstating his initial role, but either way, by his own testimony, he was an Obama-Clinton partisan was pushing information to the FBI and pressuring it to act.

More notable, Mr. Brennan then took the lead on shaping the narrative that Russia was interfering in the election specifically to help Mr. Trump – which quickly evolved into the Trump-collusion narrative. Team Clinton was eager to make the claim, especially in light of the Democratic National Committee server hack. Numerous reports show Mr. Brennan aggressively pushing the same line internally. Their problem was that as of July 2016 even then-Director of National Intelligence James Clapper didn’t buy it. He publicly refused to say who was responsible for the hack, or ascribe motivation. Mr. Brennan also couldn’t get the FBI to sign on to the view; the bureau continued to believe Russian cyberattacks were aimed at disrupting the U.S. political system generally, not aiding Mr. Trump.

The UK already agreed to pay it.

• UK To Refuse To Pay Brexit Bill Without Trade Deal (AFP)

Britain will only pay its EU divorce bill if the bloc agrees the framework for a future trade deal, the new Brexit Secretary warned in an interview published Sunday. Dominic Raab, who replaced David Davis after he quit the role earlier this month in protest over the government’s Brexit strategy, said “some conditionality between the two” was needed. He added that the Article 50 mechanism used to trigger Britain’s imminent exit from the European Union provided for new deal details. “Article 50 requires, as we negotiate the withdrawal agreement, that there’s a future framework for our new relationship going forward, so the two are linked,” Raab told the Sunday Telegraph.

“You can’t have one side fulfilling its side of the bargain and the other side not, or going slow, or failing to commit on its side. “So I think we do need to make sure that there’s some conditionality between the two.” The British government has sent mixed signals so far on the divorce bill. Prime Minister Theresa May agreed in December to a financial settlement totalling £35 to £39 billion ($46-51 billion, 39-44 billion euros) that ministers said depended on agreeing future trade ties. But cabinet members have since cast doubt on the position. Finance minister Philip Hammond said shortly afterwards he found it “inconceivable” Britain would not pay its bill, which he described as “not a credible scenario”.

The country is set to leave the bloc on March 30, but the two sides want to strike a divorce agreement by late October in order to give parliament enough time to endorse a deal. Raab met the EU’s top negotiator Michel Barnier for the first time on Friday, where he heard doubts over May’s new Brexit blueprint for the future relationship. But Barnier noted the priority in talks should be on finalising the initial divorce deal. A hardline stance by the British government on the financial settlement could complicate progress, with Raab insisting on the link with the bill and a future agreement. “Certainly it needs to go into the arrangements we have at international level with our EU partners,” he told the Telegraph. “We need to make it clear that the two are linked.”

Australia’s bad, but not the only country with an interest-only problem.

• Warning On Australia’s Looming Interest-Only Crisis (SMH)

Australia’s version of the sub-prime crisis that ushered in the global financial crisis could be looming, with a significant number of the 1.5 million households with interest-only loans likely to struggle with higher repayments, experts warn. Martin North, the principal at consultancy Digital Finance Analytics, said interest-only loans account for about $700 billion of the $1.7 trillion in Australian mortgage lending and it was “our version of the GFC”. “My view is we’re in somewhat similar territory to where the US was in 2006 before the GFC,” Mr North said.

Craig Morgan, managing director of Independent Mortgage Planners, said one in five people who took a loan two or three years ago would not qualify for the same loan now, because of the crackdown on lending by the regulator and ongoing fallout from the Royal Commission into financial services. “In the last six months lenders have had this lightbulb moment of what ‘responsible lending’ means,” Mr Morgan said. One of the triggers for the GFC was rising defaults from over-leveraged borrowers who were unable to refinance when their honeymoon rates ended. However, the sub-prime lending in the United States before the GFC included large mortgages being given to people without jobs or on minimum wage.

“This is absolutely not ‘sub-prime’ in the US definition but there were people [in Australia] who were being encouraged to get very big loans on the fact that principal & interest was impossible to service but they could service interest-only,” Mr North said. “We also know that some interest-only loans were not investors but they are actually first-home buyers encouraged to go in at the top of the market.” The Reserve Bank has previously warned $500 billion in interest-only loans are set to expire in the next four years, causing a significant jump in repayments of 30-40 per cent when borrowers are forced to start paying back the principal.

The car industry may be too complex for simple tariffs.

• German Industry Groups Warn US On Tariffs Ahead Of EU-US Meeting (R.)

German industry groups warned on Sunday, ahead of a meeting between European Commission President Jean-Claude Juncker and U.S. President Donald Trump, that tariffs the United States has recently imposed or threatened risk harming the U.S. itself. The U.S. imposed tariffs on EU steel and aluminum on June 1 and Trump is threatening to extend them to EU cars and car parts. Juncker will discuss trade with Trump at a meeting on Wednesday. Dieter Kempf, head of Germany’s BDI industry association, told the Welt am Sonntag newspaper it was wise for the European Union and United States to continue their discussions.

“The tariffs under the guise of national security should be abolished,” Kempf said, adding that Juncker needed to make clear to Trump that the United States would harm itself with tariffs on cars and car parts. He added that the German auto industry employed more than 118,000 people in the United States and 60 percent of what they produced was exported to other countries from the U.S. “Europe should not let itself be blackmailed and should put in a confident appearance in the United States,” he added. EU officials have sought to lower expectations about what Juncker can achieve, and downplayed suggestions that he will arrive in Washington with a novel plan to restore good relations.

Eric Schweitzer, president of the DIHK Chambers of Commerce, told Welt am Sonntag he welcomed Juncker’s attempt to persuade the U.S. government not to impose tariffs on cars. “All arguments in favor of such tariffs are … ultimately far-fetched,” he said.

Pentagon just delivered $200 million in deadly weapons to Ukraine. Madness.

• NATO: Doomed To Destruction By Its Own Growth (SCF)

In the 1960s, Marvel Comics writer Stan Lee and artist/co-plotter Jack Kirby in the United States created a superhero with a novel twist. He was called Giant-Man, and the bigger he got, the weaker he became. Today that character is a prophetic parable about the future of the post- Cold War “super-NATO” that has expanded to include 29 nations compromising more than 880 million people. First it absorbed all the former Warsaw Pact member states in Central Europe. Then it absorbed the three tiny and virulently anti-Russian Baltic states of Lithuania, Latvia. Now NATO is looking to embrace former Soviet Georgia and Ukraine.

As if all this was not enough, some genius at NATO Supreme Headquarters in Brussels came up with the idea of calling the alliance’s June 2016 military exercises in Eastern Europe ANACONDA. An anaconda is a gigantic carnivorous snake in the Amazon rain forest that first encircles its victims, crushes them to death and then devours them. What message was Russia meant to take from such tasteless nomenclature? However, it will not happen. Far from burying Russia, the US-led NATO alliance has been burying itself instead through its reckless, unending and remorseless growth. The curse of Giant Man is upon it. When the comic book hero Giant Man grew to 50 or 60 feet tall, he collapsed under his own weight. Such a fate is already happening to NATO.

The fundamental problem of the NATO alliance is that it is simultaneously too big and too diverse. The bigger it gets, the weaker it gets. This is because, with every state that joins the Alliance, the only militarily significant power within it, the United States, takes on an additional commitment to defend it. What does the United States get in return for its reckless bestowal of such earth shaking commitments? It gets nothing at all. When a tiny nation like Lithuania or Estonia boasts about meeting the 2 percent of GDP defense spending requirement of NATO this is ludicrous. The armed forces and GDP’s of such countries are so small as to be nonexistent. The much larger nations in the Alliance in Western Europe make no pretense of coming remotely close to their two percent defense spending pledge.

No, not a daring escape, as I read somewhere. Negotiated by Russia.

• Hundreds of Syrian ‘White Helmets’ Evacuated By Israel to Jordan (R.)

About 800 members of Syria’s White Helmets civil defense group and their families were evacuated via Israel to Jordan on Sunday from southwest Syria, where a Russian-backed Syrian government offensive is under way, media said. In a statement, the Israeli military said it had completed “a humanitarian effort to rescue members of a Syrian civil organization and their families … due to an immediate threat to their lives”. It said they were transferred to a neighboring country, which it did not identify, and that the evacuation came at the request of the United States and several European countries.

Israeli media identified the Syrians as belonging to the White Helmets organization. Officially called the Syrian Civil Defense but known by their distinctive white helmets, the group has operated a rescue service in rebel-held parts of Syria. Jordan’s official Petra news agency said on its website the kingdom “authorized the United Nations to organize the passage of about 800 Syrian citizens through Jordan for resettlement in Western countries”. The agency identified the Syrians as civil defense workers who fled areas controlled by the Syrian opposition after attacks there by the Syrian army. Petra said they would remain in a closed area in Jordan and that Britain, Germany and Canada had agreed to resettle them within three months.

Poison to feed ourselves.

• Our Vanishingly Pleasant Land (McCarthy)

It’s bizarre: in what seems like a display of obtuseness on a nationwide scale, it is still not generally realised or admitted that across huge swathes of the land, the biodiversity that at the end of the second world war was giving animation and vibrant life to the countryside as it had always done has simply vanished. By the government’s own admission, farmland birds have declined by 56% just since 1970; and the wild flowers have gone, and the butterflies have disappeared in their turn. Farewell to the spotted flycatcher, adios to the corncockle, goodbye to the high brown fritillary: what remains may be green, at least in spring, but that is mainly the pesticide-saturated crops; in wildlife terms, the landscape is now grossly impoverished, beyond any other one in Europe.

In his important new book, Cocker, one of our leading Nature writers, tackles head-on this remarkable twin phenomenon of destruction and ignorance, and he does so on an ambitious scale, seeking to explain and understand it by looking back in detail over a century of growing conservation efforts by individuals, charities, quangos and governments. How have they failed? In particular he is preoccupied with a paradox: how can our Nature have been so devastated, when there are more people who are members of green organisations in Britain than anywhere else? How can it have happened at the very moment in history that saw the rise of a new popular philosophy, environmentalism?

The simple answer is that this moment in history also saw the rise of intensive farming, a juggernaut beyond the power of green groups to control – and indeed beyond the power of individual governments once the Common Agricultural Policy of the European Union was fixed in place. It is modern industrial agriculture, above all by its immense reliance on poisons to boost crop yields, that has wiped out the wildlife of our countryside on a scarcely believable scale.

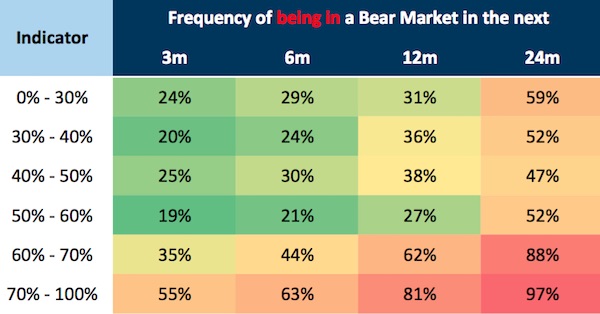

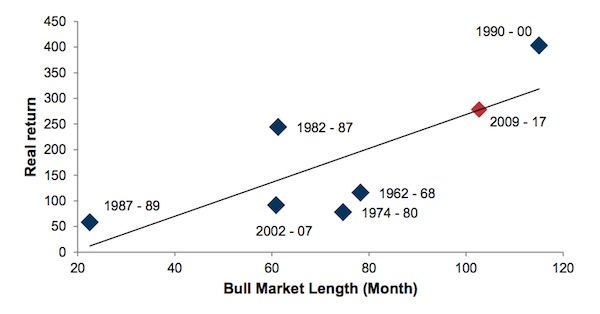

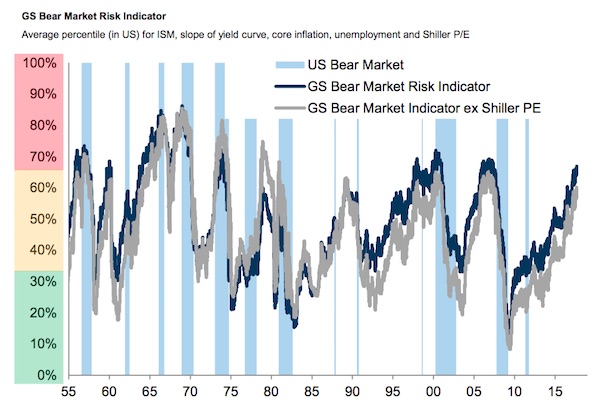

Historically, when the indicator is at 67%, there is an 88% chance of stocks falling into a bear market in two years’ time, the Goldman analysts say:

Historically, when the indicator is at 67%, there is an 88% chance of stocks falling into a bear market in two years’ time, the Goldman analysts say: