Henri Gervex Rolla 1878

Yes, SPLC is a criminal organization https://t.co/JInhIgT6Ag

— Elon Musk (@elonmusk) June 5, 2026

The Russians are No Longer Playing by the Globalist Games

— MaggieWise ⭐️⭐️⭐️ (@maggiewise111) June 5, 2026

And neither is Donald Trump :

Russia Backs Trump in Fight Against British pic.twitter.com/VOucdeHPwN

Catherine Austin Fitts: "We don’t have a financial problem – we have a bank robbery." 55 trillion stolen by Washington DC since 2008, 21 trillion of that funneled into DUMBs pic.twitter.com/60LOrLVEQ8

— illuminatibot (@iluminatibot) June 5, 2026

NEW: President Trump announces a major shift in energy funding, revealing plans to completely dismantle a massive Green New Deal initiative in favor of revitalizing America's coal industry:

— Fox News (@FoxNews) June 4, 2026

"Finally, we're taking nearly $200 million — it was set aside for the 'Green New Scam.'"… pic.twitter.com/n396agWXNh

Putin: "One line of Nord Stream 2 is still intact. We could start supplying gas to Germany tomorrow – just push a button. The only obstacle is a political decision by the German government.

— Margarita Simonyan (@M_Simonyan) June 4, 2026

I was surprised to hear that Russia, this 'evil Russia', stopped supplying gas to Europe.… pic.twitter.com/uFpoqnHXg4

Why are they shooting paper planes then?

• Iran FM Warns American Bases Are Legitimate Targets (ZH)

At a moment it’s become more than clear that the US and Iran are not anywhere closer to the negotiating table, and after they’ve shown little progress after a week of clashes – as one Friday morning Bloomberg headline reads, Tehran has again putting US bases in the region on notice, while admitting “no tangible progress” in negotiations on ending the conflict. Iran’s Foreign Minister Abbas Araghchi in fresh remarks has said that “standing against the world’s greatest power, equipped with nuclear weapons, for 40 days is no joke,” and that “the world has realized the true power of the Iranian nation.”Read more …

Araghchi also again issued a direct warning to regional Gulf states: “We warned regional states that US bases used for any aggression against Iran are legitimate targets” – he was quoted Friday by Islamic Republic of Iran Broadcasting (IRIB) as saying. However, the Iranian foreign minister also cautioned that there is a way forward, stressing that despite conflict, “We are committed to fostering sustainable, constructive ties with Saudi Arabia.” The war is fast approaching the 100-day milestone, which comes Sunday, since Trump first initiated his Operation Epic Fury. He had in the opening ‘assured’ the American public of only a short conflict lasting but a few days or weeks.Iran’s supreme leader too has been signaling defiance while apparently in hiding, saying that the US and Israel had been dealt a “decisive blow”. Ayatollah Mojtaba Khamenei’s message was read out by a prayer leader at a ceremony marking the anniversary of the death of the Islamic republic’s founder on Thursday: In his message, Khamenei said his country’s enemies, after “facing a decisive blow,” were now “experiencing a deeply meaningful and profound humiliation.” He went on to accuse them of seeking to “plant the seeds of doubt, despair, fear, mistrust and division” among the public, calling for unity to “neutralize their sinister plot.”

Tehran is still seeking to integrate the Lebanon situation into a broader US-Iran peace deal. But in Lebanon itself, sporadic fighting has raged despite declaration of a ceasefire – of which Hezbollah has declared itself not part of. On Friday, “The Israeli military’s Arabic-language spokesman Avichay Adraee on Friday warned residents of six towns and villages including south Lebanon’s Sarafand, a town on the coastal road between Tyre and Sidon, to immediately evacuate,” according to CBS.More reports of mystery explosions in Strait of Hormuz, off Oman… https://twitter.com/DropSiteNews/status/2062748657443594744?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2062748657443594744%7Ctwgr%5E5a25d7e3b03e0a7aef3fe37321882469aeb8d725%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fwww.zerohedge.com%2Fgeopolitical%2Firan-fm-warns-american-bases-are-legitimate-targets-cites-no-tangible-progress-talks

“Lebanon’s state-run National News Agency reported mass displacement from the three villages named in the warning, and it subsequently reported a strike on one of the villages, Arqoun,” the report continues. And Al Jazeera also reports Friday that “Israel’s deadly strikes continue across Lebanon, killing at least six today, despite the announcement of a new US-brokered ceasefire agreed between Lebanese and Israeli officials in Washington, DC.”

Both sidea are lobbing softballs.

• US Military Shoots Down Inbound Iranian Attack Drones Over Hormuz (ZH)

Things are again popping off in the overnight hours in the Strait of Hormuz, but so far it may be looking like another limited action and exchange. The US military reportedly intercepted and shot down at least four Iranian one-way attack drones on Friday into possibly early Saturday (local). According to US Central Command (CENTCOM), the incoming unmanned aerial vehicles were heading directly toward the Strait of Hormuz and posed an “imminent threat to maritime traffic.”Read more …

Following the drone shootdowns, American forces immediately launched retaliatory strikes against key military targets inside Iranian territory. CENTCOM further detailed that American assets hit Iranian coastal surveillance radar sites located in Goruk, a city in the Hormozgan province, as well as on Qeshm Island, a strategically vital Iranian outpost in the mouth of the strait. The Pentagon justified the immediate counter-offensive by stating the radar sites were targeted specifically to “defend against further attacks.” One thing is clear: these ‘limited’ escalations are becoming more regular, and even almost nightly at this point, raising the stakes and possibility of a more full-on, dangerous renewed war. Currently, there are reports of air defenses active over Kuwait: KUWAITI AIR DEFENSE SYSTEMS INTERCEPTING DRONE, MISSILE ATTACKSIran Military Fires “Warning Missiles” At US Destroyers In Gulf of Oman

AFP is reporting that Iranian military forces fired “warning missiles” at two U.S. Navy destroyers transiting the Gulf of Oman, citing Iranian state media. “In continuation of operations to counter maritime misconduct and harassment, as well as the hijacking of commercial vessels and oil tankers by the terrorist naval forces of the United States, following the firing of warning missiles, the hostile destroyers DDG-103 and DDG-8 have left the Gulf of Oman towards the Indian Ocean,” Iranian military forces wrote in a statement published by state news agency IRNA.Meanwhile… “US DENIES REPORT IRAN ATTACKED OR FIRED AT US NAVAL SHIPS”

https://twitter.com/CENTCOM/status/2062886477105623083?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2062886477105623083%7Ctwgr%5Eac16e3c58d0adaebd213ee136b0e6e52cdece1c7%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fwww.zerohedge.com%2Fgeopolitical%2Firan-fm-warns-american-bases-are-legitimate-targets-cites-no-tangible-progress-talks

“Trump remarks suggest the fate of Iran’s stockpile of enriched uranium is no longer be the central issue it once was.”

Is this new info for him, that it’s entombed? You’d almost think so.

• Trump Softens Red Line: Iran’s Nuclear ‘Dust’ ‘Effectively ‘Entombed’ (ZH)

Trump’s Thursday late afternoon remarks to reporters suggested that the fate of Iran’s stockpile of enriched uranium may no longer be the central issue it once was. Asked about reports that the US could attempt to seize or recover Iran’s remaining nuclear material, Trump repeatedly downplayed the prospect, saying there was “no reason” to retrieve what he called Iran’s nuclear “dust” because it is now effectively “entombed.”Read more …

The president stressed that Washington is “not considering” any covert operation to seize Iran’s uranium, adding that the US already has “powerful cameras watching Iran’s uranium” and remains confident in its ability to monitor the situation. While Trump at one point boasted that America and China are the only countries capable of recovering the material and suggested “we’ll get Iran’s nuclear dust,” his broader message now seems that the stockpile no longer represents an urgent concern. Instead, Trump framed the dispute around a much simpler objective: ensuring that Iran never obtains a nuclear weapon. He reiterated that the “main part” of any agreement would be that Iran “can’t have a nuclear weapon,” while adding that a broader deal could also include guarantees regarding the Strait of Hormuz remaining open to global commerce.Expressing optimism about diplomacy, Trump again said talks with Tehran are “going well” and suggested that a successful agreement could even lead to a personal meeting with Iran’s supreme leader. “I would be honored to meet the Ayatollah,” he remarked, adding that if a deal is reached, Iran “won’t have a nuclear weapon.”

At the same time, Trump declared in an oddly stated reference that the US would ultimately prevail “on paper, or militarily.” He warned that any future attack resulting in the deaths of American troops would trigger a rapid return to hostilities, while asserting that Iran’s military capabilities have been severely degraded. Trump claimed Tehran has only a handful of missiles remaining, reiterated that Iran effectively has “no navy” and “no air force,” and even said the US possesses photographs of sunken Iranian vessels. He further boasted that Washington had “wiped out almost all” of Iran’s leadership during the conflict.

On regional tensions, Trump linked developments in Lebanon directly to the broader confrontation with Iran, saying the various fronts are “interconnected.” He disclosed conversations with Israeli Prime Minister Benjamin Netanyahu regarding Lebanon and expressed hope that the country could finally enjoy “some peace.” Trump also claimed that Hezbollah had contacted the United States during the crisis.

Impressive.

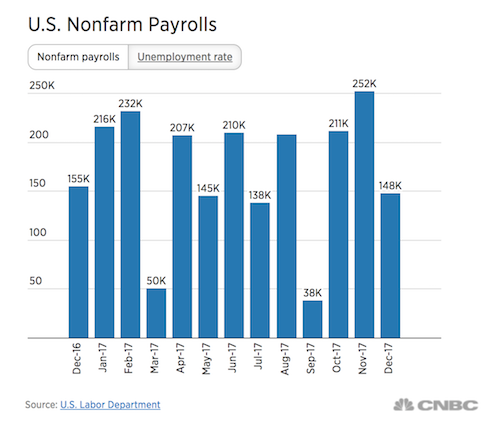

• May Jobs Report Crushes Expectations (Matt Margolis)

Friday’s May jobs report landed like a gut punch to every Democrat who thought he could run on the economy this midterm cycle. The Bureau of Labor Statistics reported 172,000 jobs added in May 2026, more than double the 85,000 economists had forecast. To say that the report significantly beat forecasts is an understatement.Read more …https://twitter.com/WhiteHouse/status/2062884560006701316?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2062884560006701316%7Ctwgr%5E7006456454e8392fc7f843038a0d6a9d90933d30%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fpjmedia.com%2Fmatt-margolis%2F2026%2F06%2F05%2Fmay-jobs-report-crushes-expectations-democrats-most-hurt-n4953630

Of those 172,000 jobs, the private sector is responsible for 120,000. And if the headline number wasn’t impressive enough on its own, April’s figures got revised upward by more than 60,000 jobs, jumping from 115,000 to 179,000. That’s three straight months of robust job growth, with each revision reinforcing a trend that’s getting harder for the left to explain away. The unemployment rate held steady at 4.3%.https://twitter.com/EricLDaugh/status/2062906789004300682?s=20

“Thanks to President Trump and Republicans, the number of new jobs in May more than DOUBLED expectations,” RNC Chairman Joe Gruters said in a statement. “Jobs are up, small businesses are growing again, and wages and paychecks are rising. Democrats sabotaged our economy for four years, but President Trump is fixing it.” “Senate Republicans and President Trump’s pro-growth policies continue delivering more jobs, lower taxes, and higher wages. Jon Ossoff voted in lockstep with the Biden-Harris administration’s reckless tax and spending agenda that left Georgians with less money in their pockets,” said NRSC Regional Press Secretary Nick Puglia.

Kevin Hassett, Director of the National Economic Council, went deep on what’s driving the numbers. “You know, I think that basically what we’re seeing is an enormous amount of positive momentum in hiring,” Hassett said. He pointed to the back-to-back strength: “Obviously, you’re right that a couple of hundred and seventies in a row, that’s a great couple of months.”

He added, “But then having upper divisions of around 100,000 means that this is a job market that’s hitting on all cylinders. And it’s our belief that this is happening because of all of the supply-side policies that the president has put in place,” Hassett said. “We’ve got the Big, Beautiful Bill with the, you know, expensing for new factories. We’ve got, you know, no tax on tips, no tax on overtime. So people are out there working harder. We’ve got quit rates down to about as low as we’ve ever seen. We’ve got layoffs about as low as we’ve ever seen. This is about the strongest market of my lifetime and of your lifetime.”

The state-level picture is worth sitting with. Sixteen of the top 21 states with the lowest unemployment rates have Republican governors. Nine of the 10 states with the highest unemployment rates have Democrat governors. The left’s economic model produces the same result wherever its governors apply it. Heading into the 2026 midterms, Democrats need an economic message that resonates. Right now, all they have is a streak of solid job numbers that belong to President Donald Trump and the GOP.

“Republican Steve Hilton was actually in the lead, but ever since election night, the number of votes that authorities say they still have to count has been suspiciously increasing each day..”

• US Attorney to Expose ‘Dumocrats’ California Fraud, Sketchy Elections (Salgado)

A hardcore warrior against all criminal fraud in California is on the case to discover exactly what Democrats are doing in controversial primary elections that first trended in Republicans’ favor, but after days of “counting” are now phasing Republicans out. Bill Essayli, first assistant U.S. attorney for the Central District of California, confirmed on Friday that there is evidence of election fraud in California, and he is certainly investigating the ongoing primary counts for governor, Los Angeles mayor, and other key state and city positions.Read more …

Yes. There is evidence of election fraud in California. Here’s a case we charged just last month. More investigations are underway. https://t.co/sdvTPuTpXk

— F.A. United States Attorney Bill Essayli (@USAttyEssayli) June 5, 2026

Essayli highlighted a recent case of voter fraud in California, where Brenda Lee Brown Armstrong pleaded guilty to spending decades bribing homeless people to register to vote and often used her address so she could receive their ballots. But Essayli also addressed the election uppermost in so many people’s minds, the one California Democrats are trying to drag out until they find enough ballots to squeeze Republicans out of runoffs.On June 5, Essayli posted more at length about his efforts. “Protecting the integrity of California’s elections is a top priority for my office,” he stated. “California’s election system has serious structural vulnerabilities. Universal vote-by-mail with no voter ID requirements creates conditions where fraud can go undetected and unpunished, eroding public confidence.” He cautiously continued, “Without commenting on any specific investigation, my office has multiple election fraud investigations underway in coordination with @FBILosAngeles. We will follow the evidence wherever it leads and prosecute any violations of federal election law to the fullest extent.”

He confirmed that he is also working with Harmeet Dhillon, assistant attorney general for the Justice Department’s Civil Rights Division, “to conduct a comprehensive audit of California’s voter rolls. The state has stonewalled every effort to verify that only eligible U.S. citizens are registered to vote. This case is now before the Ninth Circuit Court of Appeal.” The only reason to oppose an investigation into whether illegal aliens are voting is if you know that illegal aliens are voting and in your favor.

Essayli promised, “My office will not look the other way. We will investigate and prosecute. Every legal vote deserves to be counted. Every illegal vote cancels one out.” Some interesting facts that have raised suspicions in California include that in the Los Angeles mayor race, only a few hundred thousand votes are involved, and yet authorities are stubbornly refusing to declare that registered Republican Spencer Pratt made it into a runoff against Democrat Mayor Karen Bass as they sit on the last batch of votes.

In the governor’s race, Republican Steve Hilton was actually in the lead, but ever since election night, the number of votes that authorities say they still have to count has been suspiciously increasing each day, according to the counter on NBC News. And as more votes are added, Democrat Xavier Becerra narrows Hilton’s lead. More votes have also magically appeared in the mayoral race as of Friday morning. Amazing how some countries can count all their votes in one night, but California can’t do it in a week.

“I don’t believe I will ever see Fannie and Freddie released from conservatorship, at least not in my lifetime.”

• Fannie, Freddie Jump After Trump Floats $1 Trillion Valuation (ZH)

Fannie Mae and Freddie Mac shares jumped on Friday morning after President Trump said late Thursday that the mortgage giants were “probably worth $1 trillion,” reviving Wall Street hopes for a long-awaited exit from government control. President Trump praised FHFA Director Bill Pulte on Thursday for turning around Fannie Mae and Freddie Mac, saying the mortgage giants “probably have $1 trillion in value.” Full transcript:Read more …

“…a person who’s got high integrity. He’s done a phenomenal job at Fannie Mae, Freddie Mac. You probably have $1 trillion in value there. When he took over it was much less, and I guess I’m responsible for that too because everybody wanted me to sell it in my first term for 10% of what it’s worth right now. If I would’ve sold it, we would’ve lost $900 billion. We would’ve lost. Think about it. It’s probably worth $1 trillion. People want me to sell it at $100 billion — a very small percentage of what it’s worth now. And he built up a lot. Did a great job. And it’s an acting position. He is not going to be permanent because I don’t think you’d want to be. But he was a smart guy. You may find out some things about the rigged elections, etc. etc. I think he wants to do it. He’s got a lot of energy but will be very good. He’s not a permanent position. We’re looking at — we are interviewing people right now. But it is somebody just to take over for a little while.”

.@POTUS on @pulte: "He's very smart. He's a person who's got high integrity. He's done a fantastic job… and it's an Acting position. He's not going to be permanent because I don't think he'd want to be permanent. But he's a very smart guy." pic.twitter.com/2wqOy7VtaS

— Rapid Response 47 (@RapidResponse47) June 4, 2026Fannie and Freddie were both up in the early cash session, rising 5% and 3%, respectively. Shares in both mortgage giants tumbled earlier this week after Trump named Pulte as acting Director of National Intelligence, raising concerns that the dual role could delay the sale of the government’s stake. As of Friday morning, Fannie shares are down 34% YTD, while Freddie has slumped 38% YTD, as traders grow uneasy over the pace of the Trump administration’s privatization plans. Optimism around potential share sales drove large gains in 2025.

Bose George, managing director at Keefe, Bruyette & Woods (KBW), wrote in a note, “We’re comfortable with our most recently published numbers on the valuation—a current combined fair value in the $200–$250 billion range.” Christopher Maloney, mortgage strategist at BOK Financial, noted, “I don’t believe I will ever see Fannie and Freddie released from conservatorship, at least not in my lifetime.”

The title originally included “Leftists Are Crying Over “. Let’s cut out that stuff. Let’s just agree the pool is beautiful.

• Trump’s Beautifully Restored Reflecting Pool (Tim O’Brien)

You just knew this day would come. President Donald Trump is really sprucing up the nation’s capital ahead of the country’s celebration of its 250th anniversary. One of the signature improvements has been the restored reflecting pool that sits between the Lincoln Memorial and the Washington Monument. As I noted on April 25, the very act of fixing this deteriorated site was universally attacked by the left, which is par for the course when it comes to leftist reaction to everything Trump does. Keep in mind, earlier reports indicated that traditional Washington had this project pegged at a cost of $300 million and years to complete.Read more …

Trump got it done in months at a fraction of the cost – somewhere around $13 million when all is said and done. Perhaps most significantly, the pool is stunningly beautiful. The navy blue that Trump chose as the base color for the pool’s sealant adds to the richness of the entire look of it. Knowing that the people who repaired the pool sealed all of the leaks and addressed infrastructure problems provides reassurance that, with some basic routine maintenance, this iconic landmark will shine for years to come.https://twitter.com/WhiteHouse/status/2062652076862157126?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2062652076862157126%7Ctwgr%5E5682aee8970a5769f1ce5715f6b2a346130a5987%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fpjmedia.com%2Ftim-o-brien%2F2026%2F06%2F05%2Fwatch-trumps-restored-lincoln-memorial-reflecting-pool-makes-leftists-cry-n4953627

In the process, Trump is making leftists cry. Not tears of joy: tears of regret that they have to admit they actually like it.

A Democrat in DC says she hates she’s forced to admit the Reflecting Pool now looks good.

— Right Angle News Network (@Rightanglenews) June 5, 2026

“I thought it was a stupid idea to paint the Reflecting Pool, but it looks really good. It makes the reflection look extraordinarily prominent in a way it did not before, and I hate that.” pic.twitter.com/yVTHm4rHUhYou may remember that when the project was first launched, leftists came up with every excuse in the book as to why it was a dumb idea. The blue color was a problem, with leftists turning to AI to come up with gaudy swimming pool blue renditions of the project, and then reacting negatively to their own fake imagery. They were still using their AI pics up until the water was turned on. As the project proceeded and it appeared the final product might actually be tasteful, leftists then started to complain about the cost. That’s right: Something they were willing to spend $300 million on over a period of years under a Democrat administration now costs too much at $13 million over a couple of months.

The same leftists who want to give millions of illegals free housing, free food, free health insurance, thanks to you, the taxpayer, all of a sudden care about a project that wouldn’t be necessary if the Obama administration didn’t already screw it up. Barack Obama spent $34 million over a couple of years on this, and it was a mess in the end. In a “feel-good Friday” Truth Social post, the president kind of punctuated the whole event in Trump style. https://twitter.com/EricLDaugh/status/2062922835387982001?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2062922835387982001%7Ctwgr%5E5682aee8970a5769f1ce5715f6b2a346130a5987%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fpjmedia.com%2Ftim-o-brien%2F2026%2F06%2F05%2Fwatch-trumps-restored-lincoln-memorial-reflecting-pool-makes-leftists-cry-n4953627

What’s the moral of this story? The left will never be happy about anything, but on the rare chance you catch them liking something that Trump did, it will most certainly bring them to tears.

“[Democrats] don’t care about ICE and ICE operations,” he added. “They just wanna stop ICE from doing what they are required to do, which is deport illegal aliens.”

• Trump Just Got the Last Laugh on Immigration (Cameron Arcand)

The reconciliation bill to fund ICE and Customs and Border Protection (CBP) is now headed to the House after most Senate Republicans passed the proposal on Thursday night, and it ultimately accomplished funding through 2029 for the agencies and sidelined Democrats’ immigration enforcement demands. Many Democrats were calling for the use of judicial warrants for immigration-related arrests as opposed to administrative ones, as well as an end to masked agents and roving patrols.Read more …

Republicans opted to pursue reconciliation to fund the immigration enforcement agencies to get DHS reopened after a lengthy shutdown of the department, as reconciliation allows for only 51 votes for Senate passage as opposed to the standard 60-vote threshold. “Democrats side with illegals over American citizens every chance they get. But thanks to reconciliation, we didn’t need their votes or have to accept their radical demands that would have tied the hands of federal law enforcement,” Sen. Jim Banks (R-IN) told Townhall in an exclusive statement Friday.“Now ICE and CBP have the funding they need to keep the border secure and continue mass deportations through the end of President Trump’s term,” he added.= A significant portion of funding for Trump’s immigration goals was already obtained through the “One Big Beautiful Bill Act” last July, but other DHS agencies like FEMA were hung out to dry when the DHS shutdown ran from February through April. Meanwhile, the reconciliation bill is expected to close other immigration-specific funding gaps that were not covered when DHS reopened in April.

Former Acting ICE Director Jonathan Fahey explained to Townhall on Friday morning that the movement on reconciliation showed that Democrats “gave up the game on this thing with their list of demands.” “Because when there were situations where the Republicans were willing to concede or to give them some of the things they wanted, they rejected that in favor of just shutting down the agency,” Fahey said. “[Democrats] don’t care about ICE and ICE operations,” he added. “They just wanna stop ICE from doing what they are required to do, which is deport illegal aliens.”

Fahey explained that some of the Democrats’ wishes, like judicial warrants, were some of the “problematic” points for potential compromise. “As probably most people know, you can’t get a judicial warrant from these ICE arrests. They’re issued out of the Executive Branch. So it didn’t even mechanically make any sense,” Fahey said, calling it an “unworkable part” of the party’s demands.Senate Minority Leader Chuck Schumer fired back against the proposal early Friday morning, saying that Republicans “pumped another $70 billion into Trump’s personal police force.”

Senate Republicans just passed a rotten bill that makes their priorities painfully clear:

— Chuck Schumer (@SenSchumer) June 5, 2026

More money for Donald Trump, more power for Donald Trump, and nothing to lower costs for working families. pic.twitter.com/keisHYfXVu“The Republican agenda is now written in black and white: a slush fund for Trump, tax dodges for Trump, a ballroom for Trump, a private militia for Trump,” Schumer stated. “For hard-working Americans? Nothing.” The Republican-majority House is expected to pass the legislation before it heads to Trump’s desk for a final signature. A third reconciliation bill is expected to be pushed by congressional Republicans this summer, which is expected to focus on anti-fraud policy and other budgetary proposals.

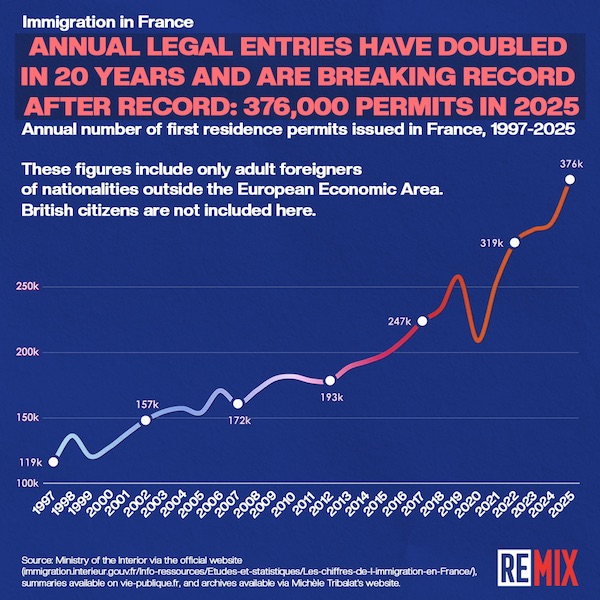

“.. there are now fewer foreigners in all of China, at 845,000, than there are in just one European city, Berlin.”

• The French Never Wanted Mass Immigration (RMX)

French leaders know how to manipulate their voters, but the voters are also apparently easily manipulated. Every leader from French President Emmanuel Macron to François Mitterrand in the 1980s has decried immigration numbers and promised a crackdown, all while allowing immigration numbers to continuously climb year after year. Here are just some relevant quotes:Read more …

• Emmanuel Macron said in 2023: “There is an immigration problem in France.”

• In 2016, then French President François Hollande said, “There are too many arrivals, immigration that shouldn’t be there.”

• In 2023, then leader Nicolas Sarkozy said: “There are too many immigrants in France.”

• In 1991, former leader Jacques Chirac said, “We must stop family reunification. We must completely revise the right of asylum. We must open the debate on the right of all foreigners to social benefits.”

• In 1989, the famous leader François Mitterrand said, “On immigration matters, we have crossed the tolerance threshold.”The age-old adage is that “nobody voted for this.”It is true that the specific question of mass immigration never came to a referendum, but it is also fair to say that some very pro-migrant candidates, such as Macron, have continuously made it into office. Still, one would assume that in a democratic system, with leader after leader calling for a halt to immigration, that immigration levels would tend to trend lower. However, this is not how Western democracy has worked over the last decades. The same developments have been seen in the United Kingdom, Germany, and the United States.

Leaders know the masses are unhappy about immigration, so they make proclamations against immigration to placate the masses, all while actual policy serves an entirely different purpose. Macron is arguably the worst offender the French have ever seen when it comes to migration. In 2023, he said France must reduce immigration, beginning with legal entrants in a wide-ranging interview with weekly political magazine Le Point. Macron’s remark comes after he said in 2022 that migration “is part of France’s DNA” and oversaw a record increase in immigrants in 2022.

What has his record been since then? Well, Macron was lying, as this chart clearly shows:

The foreign population has soared year after year, reaching record after record. In 2025, a record number of first-time legal residence permits were issued, totaling 384,000. In short, France is being buried in a wave of mass immigration that only a minority of French actually wanted. The estimates of how many foreigners are now living in France varies wildly, with some figures going as high as 9 million. However, there are also millions of legal French citizens who also have a migration background, which has led to a massive demographic shift.Poll after poll has shown the French are remarkably opposed to mass immigration.

• In a CSA poll for CNews in 2023, 64 percent of French said “we should stop non-European immigration to France.”

• In a CSA poll for Europe 1 in 2024, 48 percent of French people said they wanted zero immigrants coming to the country, including 53 percent of women respondents.

• In an Ifop poll in 2026, 60 percent of French people said they believe France is witnessing “a replacement of the French population by non-European populations, mainly from the African continent.”

• In a poll from Odoxa-Backbone Consulting for Le Figaro in 2023, 74 percent of French said they believe there are too many migrants in France and 72 percent said they want a referendum on immigration.

• In a CSA poll for CNews in 2023, 80 percent of French said they support a total ban on more immigration.

Meanwhile, in communist China, where there is not even an illusion of a democratic vote, foreigners only make up 0.06 percent of the population of 1.4 billion people. It may be hard to believe for many, but there are now fewer foreigners in all of China, at 845,000, than there are in just one European city, Berlin. The political leaders that have governed the West have lied every step of the way on immigration, and in the process, they have gravely imperiled democracy. Many looking to authoritarian China see a country on the rise, where high-speed trains and critical infrastructure are quickly and efficiently erected, where crime is low, and social cohesion generally high.

Meanwhile, Europe is throwing up protectionist barriers against China at a time when China is pulling ahead in green energy, automobile manufacturing, machine tools, and AI. Mass immigration has been an unmitigated economic, educational, security, and budget disaster for the West. Democracy itself should not necessarily be condemned, however. Japan, Taiwan, and South Korea, all thriving democracies, have managed to keep their borders almost entirely closed to mass immigration while growing their economies, all based on the will of the people.

In the end, it may have something to do with Europeans themselves and their culture of guilt, self-righteousness, and virtue signaling, which are attitudes that tend to dominate amongst European populations. The trend has been remarkably uniform across the Western world. It is not only France, but also the Netherlands, Germany, Spain, and the United Kingdom, all marching in lockstep. While we can point our fingers at the mass media and academia, we also have to look at ourselves in the mirror and ask how we collectively allowed this to happen.

“..or maybe is this letter meant to make sure that no personal meetings can take place at all,” he remarked, concluding: “I think it’s the second.”

I think he’s right,

• Putin Rejects Open Letter By Zelensky Urging Meet: ‘Pointless’ (ZH)

Russian President Vladimir Putin has responded dismissively to Ukrainian President Volodymyr Zelensky’s open letter issued the day prior, which urged that the two leaders meet in order to finally forge a peace deal and bring an end to the war, now it its fifth year. Putin made clear Friday that he sees no point in holding a personal meeting with Zelensky. He was asked directly about the letter while attending the St. Petersburg International Economic Forum (SPIEF). In response the Russian leader addressed not the “authors of the epistolary genre,” but to Russian soldiers on the frontline: “The whole country is proud of you and is counting on you. Keep up the good work, brothers!” And then, per TASS:Read more …

“Asked to clarify if this response means that he doesn’t plan to meet with the letter’s author, Putin said, “So far, I see no point in this.” He went on to reject the idea of “meeting just for the sake of meeting” – but did reveal for the first time that only last month he sent an informal envoy to Ukraine at Kiev’s request. Apparently that was the opening of a serious diplomatic overture. But then, he noted, Ukrainian forces bombed a college dormitory in Lugansk merely soon after the Russian envoy arrived. The brutal attack killed 21 people, mostly teenage girls – and injured many dozens more. The Kremlin was outraged at the ‘terrorist act’ and the following week heavily bombed various Ukrainian cities, especially the capital.State media featured more of Putin’s response: The letter is either “a means to create an environment for a personal meeting, or maybe is this letter meant to make sure that no personal meetings can take place at all,” he remarked, concluding: “I think it’s the second.” Zelensky’s lengthy Thursday letter had said Ukraine is also ready for a “full ceasefire.” Zelensky wrote: “Ukraine proposes ending this war through direct engagement between us – and you. I am proposing a meeting. Ukraine is ready for a full ceasefire for the duration of the negotiations,” he added.

The letter also at one point said, “The choice is yours now. Enough of war” and then spells out that “Ukraine proposes to end this war.” “This must be done honestly, with dignity, and with guarantees that the war will not be reignited,” Zelensky added. And then interestingly, “We see that the United States is fully focused on the issue of Iran, and it would be wrong to simply wait until the war in Europe returns to the center of its attention.” Despite the long appeal, President Putin and the Kremlin have demonstrated a willingness to allow a long war to drag on, and are unlikely to be moved. Putin has said there’s no need for a truce unless a deal is already close or about to be signed. But the two sides aren’t any closer to being at the negotiating table as yet.

The reactions are about as uglyas the actual episode.

• British Witness DEI Outcome and Two-Tiered Policing in Brutal Murder (CTH)

New information about the brutal stabbing murder of 18-year-old Henry Nowak continues to surface, and each revelation is seemingly worse than the last. In the latest development the Daily Mail now outlines that Nowak’s killer, Vickrum Digwa, actually recorded his victim lying on the ground in agony as the murderer mocked him. Incredibly the judge in the trial ruled the killer’s own recording of his murder, “too disturbing to be shown” in court. Digwa did not call for an ambulance after stabbing his victim but did take pictures and record Henry Nowak. However, the killer’s own video was NOT shown in court! The footage the court ruled too disturbing to show was five minutes of Vickrum Digwa filming the 18-year-old as he bled to death on the pavement.Read more …

The entire event is highlighting a two-tiered policing system in the U.K, and now police are revealing documents and training material that specifically tell them to treat encounters with racial minorities differently than encounters with white people. The outrage is growing and British politicians are afraid to talk about it. Reform party leader Nigel Farage did not stay silent, and immediately he began facing backlash for speaking truthfully about the murder of Henry Nowak and the circumstances that led to a horrific encounter with police. WATCH:

Below is the initial statement from Nigel Farage that was mentioned in the interview above.

Ideological conditioning and two-tiered policing are glaring symptoms of civilizational decline. They must be rejected across the West.

— Department of State (@StateDept) June 4, 2026

The United States sends our condolences to the family of Henry Nowak and the people of the United Kingdom at this troubling time.

”In an exclusive interview with RT the US commentator joked that she would only run herself if voters accepted her as “dictator”

• Candace Owens Would Back Tucker Carlson For US President (RT)

Conservative US commentator Candace Owens would back journalist Tucker Carlson if he ran for US president, but would only run herself if voters accepted her as “dictator.” Speaking exclusively to RT’s Rick Sanchez at the St. Petersburg International Economic Forum (SPIEF), Owens was asked about speculation in the US that she could one day run for the White House. “I always tell my listeners I’d never run for president. I’d only run for dictator,” Owens said. “I’m not dealing with Congress, I’m not dealing with lobbying, I’m not dealing with Lindsey Graham calling for another war.”Read more …

She joked that if voters wanted her, they would have to accept the terms that she will be “dictator of the United States,” adding that she has no short-term interest in political office because of the “inauthenticity” of Washington. The former Daily Wire host said she would instead be willing to campaign for someone like Tucker Carlson if he chose to run. She added that she would be ready to travel the country on Carlson’s behalf, comparing the idea to her previous political partnership with Charlie Kirk.She said Carlson had also been one of the few prominent conservative voices willing to speak honestly about Charlie Kirk’s changing views toward the end of his life, alongside Megyn Kelly. Owens initially rose to prominence in the late 2010s by urging black voters to stop supporting the Democrats. She later became one of the most prominent voices in conservative media before splitting with the Daily Wire following a public dispute over Israel’s war in Gaza.

Warning for France and UK?!

• How Did Pakistan Become 96 Percent Muslim? (Uzay Bulut)

Today, 96% of Pakistan’s population follows Islam, with most of that percentage adhering to the Sunni tradition. According to Pakistan’s constitution, the right to free speech can be restricted to ensure “the glory of Islam.” However, Pakistan was once majority-Hindu. It was part of the Indian civilization with significant religious, ethnic, and cultural diversity. This is no longer the case. Native Hindu and other non-Muslim cultures were systematically and largely erased by the Islamic Republic of Pakistan. Moreover, attempts at reviving the Hindu and other pre-Islamic names of geographical locations are met with backlash from Muslims in the country.Read more …

India Today reported on May 27 that the provincial government of Pakistan’s Punjab has deferred its decision to restore several pre-Partition Hindu and British-era names of roads and localities in its capital of Lahore. The Punjab government is led by Maryam Nawaz, who in March proposed restoring several Lahore landmarks to their older (Hindu, Sikh-origin or British) names. This effort was cleared by the Nawaz-led Punjab Cabinet in May. However, retired Lahore Deputy Commissioner Captain Muhammad Ali Ijaz replied to the queries of the Pakistani daily, Dawn, by saying that “no such decision has been taken as yet.” According to reports, authorities in Lahore have made a U-turn: they are experiencing opposition from “extremists” and social media vloggers.“Even after partition, many colonial [British] and Hindu-era names continue to survive in public memory despite official changes of names by various governments in Pakistan,” India Today reported. Despite the denial of many in the region, present-day Pakistan was once predominantly Hindu. The Indian subcontinent was home to one of the oldest and most influential civilizations known as the Indus Valley civilization or Harappan civilization. This Bronze Age urban culture reached its peak around 2500 BC. The culture itself might have been older, as religious practices and farming settlements in the fertile region by the Indus River can be dated back thousands of years.

Before the arrival of Islam in the 8th century, the region that is now called Pakistan and the broader Indian subcontinent was exceedingly diverse. Throughout millennia, the region’s religious diversity included a rich mix of Hinduism, Buddhism, Jainism, other local/folk beliefs, and later, Judaism, Zoroastrianism, and Christianity. Throughout the last 14 centuries, the Islamization of the Indian subcontinent has been shaped by massacres, pogroms, persecutions, and forced conversions. This spans the initial Arab expansions, the Delhi Sultanate, the Mughal Empire, and the partition of India, up to the present.

The organization “Log Sabha” prepared a comprehensive report entitled “Hindu for Justice: A Historical Account of Genocides and Massacres Against Hindus.” It describes the long history of Hindu persecution in and outside of the Indian subcontinent at the hands of Islam. The report notes: Throughout various historical periods, forced conversions and the destruction of Hindu temples were recurring themes. In many cases, the violence was not only aimed at suppressing Hindu religious practices but also at erasing Hindu cultural heritage. This systematic approach to cultural destruction had long-lasting effects on Hindu communities.

The Indian subcontinent has been significantly impacted by the Islamic campaigns committed by various armies and empires. These invasions altered the political and demographic landscape of the region. They also brought widespread destruction to Hindu and other non-Muslim cultures, religious practices, and communities. The landscape began to shift in the early 8th century when the Umayyad Caliphate’s general Muhammad bin Qasim invaded the Sindh region. The local population’s conversion to Islam was a gradual process lasting several centuries. His campaign was characterized by both military conquests and acts of violence against Hindu populations.

The invasion led to the establishment of a Muslim administration and initiated a series of forced conversions, persecution, and the destruction of Hindu temples. One of the most brutal invaders was Mahmud of Ghazni, who raided the Indian subcontinent between 1000 and 1027 AD. His campaigns were characterized by the large-scale destruction of Hindu temples and cities, driven by both religious zeal and the lure of wealth. The city of Mathura, a sacred site for Hindus, faced massive devastation during one raid. Temples were razed to the ground, and countless Hindus were either massacred or enslaved. His most infamous attack occurred at Somnath, one of the most revered temples in Hinduism: tens of thousands of Hindus were slaughtered and the temple’s treasures looted.

Time is an important factor. He does’t want it all tomorrow morning.

And just think: a million humans on Mars. That will take a very long time.

• How Realistic Are Musk’s Visions for Mars? (Rainer Zitelmann)

In the current prospectus for the IPO, Musk reiterates that the goal of SpaceX is to make humanity a multi-planetary species and to colonize Mars. The company’s mission is described as follows: “Our mission is to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and extend the light of consciousness to the stars.”Read more …

But so far, only probes and robots have been to Mars, not humans. Many critics consider plans for Mars to be science fiction. Not so the renowned NASA Ames researcher Harry W. Jones, who says: “It has seemed there must be overwhelming difficulties preventing our going to Mars. We have not reached Mars even though it has been NASA’s horizon goal since Apollo. We do not have a detailed feasible mission plan. There has not been sufficient funding to make tangible progress. Mars plans usually propose developing advanced technology, before we can begin the mission.”Between the lines, you can sense his frustration – directed not only at politicians, but also at NASA itself. For over fifty years, there have been repeated excuses for indefinitely deferring a mission to Mars. And yet, there is no shortage of plans to reach Mars. Since the 1950s, over 1,000 plans have been devised. Even if you only count those that meet scientific standards, there are still 55 plans.

However, in a detailed analysis, Jones concludes that there are “no showstoppers” – that is, no insurmountable obstacles on the path to Mars. He identifies seven key challenges: hostile surface environment, human performance, life support, medical care, radiation exposure, reduced gravity, and telecommunication delays – and shows that there are viable solutions for each and every one of them based on the current state of technology. Solutions for all these problems exist today, he argues, in part thanks to the recent great reduction in launch costs.

The primary technical challenges for a Mars mission are long-term life support, radiation exposure, and reduced gravity. According to Jones, solutions for solar flares and cosmic microwave background radiation already exist, made possible by reduced launch costs. For instance, a small, shielded shelter within the spacecraft, measuring two meters in diameter with 7.5-centimeter-thick walls, could protect against solar storms during transit. Additionally, a shorter transit time and the use of Martian regolith to shield surface habitats could mitigate the effects of cosmic microwave background radiation.

Regarding the challenges of weightlessness during space travel and the more than 60 percent reduction in gravity on Mars: A rotating spacecraft, similar to those depicted in science fiction films, can generate artificial gravity during the journey. And there are also viable solutions for habitation on Mars itself: “One suggestion is a large rotating underground wheel. The floor must be tilted so that the 0.38 g Mars gravity pulling down combines with a 0.92 g horizontal spin force to provide 1 g. The rotating wheel would be underground to provide radiation shielding.”

All in all, yes, a flight to Mars, and even more so its colonization, presents substantial challenges – some we can anticipate, and many others will be unforeseen. But having developed countless plans for how it could be done, the time for action has come. If Roald Amundsen and his team, the first to reach the South Pole in 1911, had required the same level of safety and perfection as NASA demands for its mission to Mars, they certainly would never have launched their expedition.

If there are no “showstoppers,” as Harry W. Jones argues, why aren’t we already on our way to Mars? As so often, it is also a question of money and economic incentives. Elon Musk’s plans to bring one million settlers to Mars cannot possibly be financed through taxpayer money. But how could private financing become feasible?

The economic incentive is missing because, according to the 1967 Outer Space Treaty, nations are prohibited from owning celestial bodies or land on celestial bodies. Whether this also applies to private individuals and companies is disputed among legal scholars. In my book New Space Capitalism, I show how it could work: If the private appropriation of land on celestial bodies were possible, an enormous economic incentive would suddenly emerge — one that is currently absent. So, who should have the right to acquire property in space? My answer: Those who have the financial means to get there, develop, and use the land.

For instance, if SpaceX succeeds in reaching Mars and starts to build permanent settlements on the Red Planet, then the ownership of land should initially go to SpaceX. Not the entire planet, of course, but a practicable area, for example, the size of Singapore. The surface area of Mars is 200,000 times that of Singapore, so SpaceX would initially own only 0.0005 percent of Mars. That would be enough to develop multiple settlements, but not so much that others would no longer have a chance.

SpaceX could finance its flight and development costs by listing the land on Mars in a real estate investment trust (REIT). The price would then be determined by the market. Most people would buy shares not because they intend to live there themselves, but in the hope of future appreciation in value. It would be the greatest real estate story in history.

— Elon Musk (@elonmusk) June 4, 2026

https://twitter.com/MCarbonaraFL/status/2062525163518726520?s=20. @BarackObama needs to get more than a grand jury subpoena, he needs to be tried with grand conspiracy to commit treason against the United States of America!

— General Mike Flynn (@GenFlynn) June 5, 2026

Enough is enough!!!@realDonaldTrump pic.twitter.com/B3eXtetnmY

Dear vaccinated people,

— healthbot (@thehealthb0t) June 4, 2026

Your government gave you AIDS and is blaming “long COVID” for it. pic.twitter.com/s0Naa1roan

30,000 hours of footage, equivalent to 3 years and 7 months, were filmed to capture the blooming of 77 types of flowers, and the result is spectacular. pic.twitter.com/nOTYGlOwVr

— Massimo (@Rainmaker1973) June 5, 2026

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.