William Henry Jackson Portales of the market of San Marcos, Aguascalientes, Mexico 1890

Next weekend: the big National People’s Congress votes on XI’s five-year plan. Pie in the sky.

• China Stocks Tumble Toward 15-Month Low as Stimulus Bets Unwind (BBG)

Chinese stocks sank, with the benchmark index approaching the lowest level since November 2014, as some investors were disappointed by a lack of specific measures to boost growth during the Group of 20 meetings in Shanghai. The Shanghai Composite Index dropped as much as 4.4% as almost 20 stocks fell for each that rose. The measure has declined 24% this year, the worst performer among 93 global equity indexes, on concern capital outflows will accelerate as the economic slowdown deepens. The yuan headed for its longest losing streak this year. Investors had hoped the government would announce measures to bolster the economy over the weekend, according to JK Life Insurance, after People’s Bank of China Governor Zhou Xiaochuan said on Friday there is room for more easing.

There are also increasing signs funds are shifting from equities to housing, according to Steve Wang, chief China economist at Reorient Financial Markets Ltd. “Investors feel disappointed over the lack of good news from the G-20, while the yuan has started to weaken again,” Wang said in Hong Kong. “There are signs of panic buying in China’s property market as prices in large cities continue to rise. A hazy economic outlook prompted some people to sell shares and buy homes, while many stocks remain overvalued.” [..] Increased volatility in stocks threatens to undo policy makers’s efforts to project an image of stability in the nation’s financial markets after months of turbulence reverberated across the world. Investors are also selling before the nation’s legislators meet on Saturday for the annual National People’s Congress, where economic policies for the next five years will be approved

They should have pushed for a devaluation deal this weekend. Now it’s back to all out beggar thy neighbor.

• China Devalues Most In 8 Weeks, Offshore Yuan Slides To 3-Week Lows (ZH)

Following USD strength last week, China has come back to work after the disappointment of the Shanghai non-accord and weakened the Yuan fix by 0.2% – the most since January 7th.

This move follows pressure from offshore Yuan weakness since traders returned from Golden Week – driving the onshore-offshore spread out to its widest since The PBOC stepped in and stomped the shorts.

After a few weeks of stability, it appears China is forced to let the Yuan slip back out to where its CDS (a market it is notr manipulating directly yet) implied it to be after shaking out some weak shorts at the end of January.

And those are not the only sectors with overcapacity.

• China Expects To Lay Off 1.8 Million Coal, Steel Workers (Reuters)

China said on Monday it expects to lay off 1.8 million workers in the coal and steel sectors as part of efforts to reduce industrial overcapacity, but no timeframe was given. China has vowed to deal with excess capacity and eliminate hundreds of so-called “zombie enterprises” – loss-making firms in struggling sectors that are being kept alive by local governments trying to avoid job losses. Yin Weimin, the minister for human resources and social security, told a news conference that 1.3 million workers in the coal sector could lose jobs, plus 500,000 from the steel sector. It was the first time a senior government official has given a number for job losses as China deals with industrial overcapacity amid slowing growth. “This involves the resettlement of a total of 1.8 million workers. This task will be very difficult, but we are still very confident,” Yin said.

For China’s stability-obsessed government, keeping a lid on unemployment and any possible unrest that may follow has been a top priority. The central government will allocate 100 billion yuan ($15.27 billion) over two years to relocate workers laid off as a result of China’s efforts to curb overcapacity, officials said last week. China’s vice finance minister Zhu Guangyao quoted Premier Li Keqiang as telling U.S. Treasury Secretary Jack Lew on Monday that the fund would mainly focus on the steel and coal sectors. “The economy faces relatively big downward pressures and some firms face difficulties in production and operation, which would lead to insufficient employment,” Yin said, adding that increasing graduates this year would also add pressure in the job market.

Whether or not concerns are deflected is not in their hands.

• China Central Bank Deflects Concerns Over Forex Reserves (Reuters)

The vice-governor of China’s central bank on Sunday deflected concerns over the possibility of an extended fall in the country’s foreign exchange reserves and reaffirmed confidence in the strength of the Yuan. China still owns the world’s largest currency reserves but has been burning through them at such a pace that some economists and foreign exchange professionals have been questioning how low can they go before Beijing is forced to choose between fresh capital controls or giving upselling dollars to defend the yuan, also known as the renminbi. Foreign exchange reserves in China declined by $99.5 billion in January to $3.23 trillion after a record fall the previous month. Reserves have shrunk by $762 billion since mid-2014, more than the gross domestic product of Switzerland.

Yi Gang, vice governor of the People’s Bank of China (PBOC), told state news agency Xinhua that part of the recent reductions in China’s massive forex reserve was down to higher holdings by companies and individuals. The interview, shortly after the G20 financial ministers’ meeting in Shanghai, was posted on the central bank’s website www.pbc.gov.cn. “The falls in forex reserve was mainly because residents increased their holdings and cut their forex debts. This process has a limit and the capital outflow will gradually slow down,” Yi was quoted as saying. “On the other hand, China still enjoys high trade surplus and direct foreign investment, resulting in still-fast capital inflow,” Yi said.

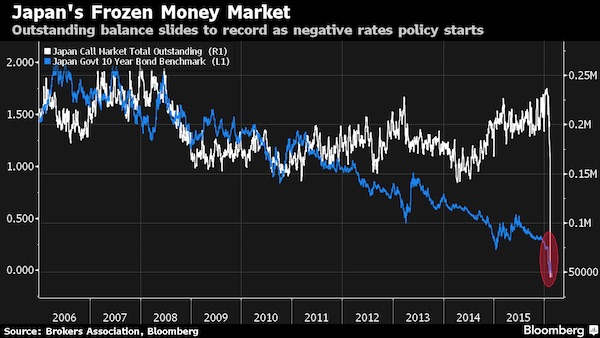

The Boomerang Bazooka.

• Kuroda Negative Rate Bazooka Fizzles on Overnight Lending Freeze (BBG)

Japan’s banks have almost stopped lending to one another in the overnight market, threatening to undermine the impact of the central bank’s negative-rates stimulus. The outstanding balance of the interbank activity plunged 79% to a record low of 4.51 trillion yen ($40 billion) on Feb. 25 since Bank of Japan Governor Haruhiko Kuroda on Jan. 29 announced plans to charge interest on some lenders’ reserves at the monetary authority. Bond volatility has soared to a 2 1/2-year high as the evaporation of trading volumes in the call market dislocates funding of a range of debt investments. While Kuroda wants to lower the starting point of the yield curve to reduce borrowing costs and spur shift of funds into riskier assets, the interbank rate has fallen only about as far as minus 0.01%, above the minus 0.1% charged on some BOJ reserves.

The swings on bond yields will make it harder for financial institutions to determine how much business risks they can take, weighing on lending in a weak economy even as they are penalized for keeping some of their money at the central bank. “It is still uncertain how deep into the negative the overnight call rates will sink,” said Naomi Muguruma at Mitsubishi UFJ Morgan Stanley Securities. “It won’t settle until funding flows in the new scheme become clear. That may pressure volatility to stay high for government bonds.” The overnight rate was the BOJ’s main policy target until Kuroda switched it to monetary base growth in April 2013. The central bank said the initial amount to which its minus rate would be applied to is about 10 trillion yen of financial institutions’ reserves held at the BOJ. Reflecting the confusion among traders about the unprecedented negative-rate policy, the one-month premium for one-year interest-rate swaps have surged.

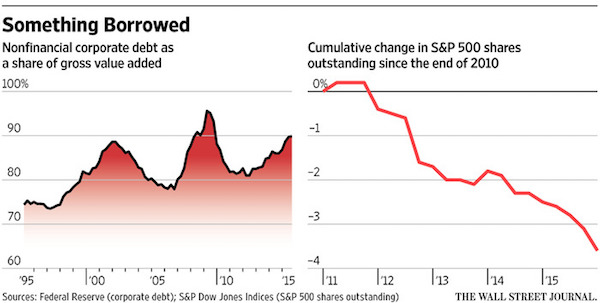

More boomerangs: “Nonfinancial corporations owed $8 trillion in debt..”

• Share Buybacks: The Bill Is Coming Due (WSJ)

Low rates alone aren’t enough to make it easy to pay off a loan. Many companies may find that out the hard way, especially as high-yield debt markets show signs of strain lately. U.S. companies went on a borrowing binge in recent years. Nonfinancial corporations owed $8 trillion in debt in last year’s third quarter, according to the Federal Reserve, up from $6.6 trillion three years earlier. As a share of gross value added—a proxy for companies’ combined output—corporate debt is approaching levels hit in the financial crisis’s aftermath. Most of the debt increase came from bond issuance, as nonfinancial companies took advantage of the lowest rates on corporate bonds since the mid-1960s. That is a plus as companies in many cases extended the maturity of their debt and lowered borrowing costs.

The negative: Rather than investing the funds they raised back into their businesses, companies in many cases bought back stock instead. That was something that many investors welcomed, but it may have come with future costs that they didn’t fully appreciate. In aggregate, nonfinancial companies’ cash flows over the past three years were enough to cover capital spending. That is unusual—typically, capital spending outstrips cash flows as companies invest for growth—and is reflective of how muted business investment has been since the financial crisis. Over the same period, the companies repurchased $1.3 trillion in shares. Because those stock buybacks helped reduce companies’ total shares outstanding, earnings per share got a boost. Indeed, absent the past three years’ share-count reductions, S&P 500 earnings per share would have been 2% lower in the fourth quarter than what companies are reporting, according to S&P Dow Jones Indices.

The major reason companies plowed money into buybacks rather than capital spending was that, in a low-growth environment, the returns from investing in expansion didn’t seem as attractive as in the past. This is a big part of why companies were able to borrow cheaply: In a low-growth, low-inflation environment, investors were willing to accept lower returns on corporate bonds than if the economy was moving at a more rapid clip. The sticking point is that in a low-growth environment, paying down debt also may be harder. Especially because companies weren’t putting the money they borrowed into capital investments, which provide cash flows to help service debt. The stock they bought back won’t do that for them.

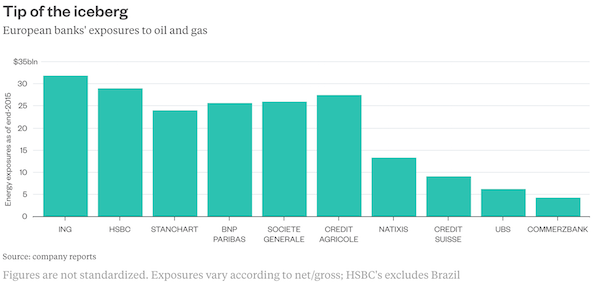

“..$200 billion. That’s more than the U.S. banks’ estimated $123 billion of outstanding loans and lending commitments to the industry..”

• European Banks’ $200 Billion Oil Slick (BBG)

The European earnings season isn’t over yet – but already banks have given some disclosure about the size of their loans to the oil and gas industry: almost $200 billion. That’s more than the U.S. banks’ estimated $123 billion of outstanding loans and lending commitments to the industry, and a sign of how Europe’s lenders face risks far beyond their home turf as oil lingers near a historic low.The problem is that this may be the tip of the iceberg.Disclosure so far has been inconsistent – some firms provide net exposures and others gross. Others, like Deutsche Bank, haven’t given any precise numbers at all.The direct exposures only capture part of the picture though. Firms like HSBC and Standard Chartered, face a double helping of pain as the falling price of commodities rips through the economies of energy-exporting countries where they have ramped up lending in recent years.

There’s also the risk that attention shifts away from oil and gas producers to other industries tied to commodities. Signs of stress are already appearing among traders and miners: Noble Group on Thursday posted its first annual loss in almost two decades, while Anglo American’s credit rating was cut to junk earlier this month. While commodities trading exposure is usually included in banks’ overall portfolio, the companies often class it as immune to oil-price fluctuations. That suggests losses in this space would come as a nasty surprise. As for metals and mining, that exposure is worthy of its own iceberg: HSBC alone booked about $100 million in provisions on its $18 billion metals and mining loan book in 2015.The U.S. banks, which are closer to the threat of their domestic shale boom turning into a bust, are leading the way in terms of transparency.

And they’re being more realistic. JPMorgan CEO Jamie Dimon warned this week that if oil prices held at around $25 per barrel over 18 months then the bank’s loan-loss reserves would go up by $1.5 billion.European banks are assuming oil will stay at about $30 a barrel, a forecast that appears too benign when compared with predictions of $20 oil from Goldman Sachs and Morgan Stanley.European optimists counter that falling commodity prices should be a zero-sum game. Energy exposures at most banks are around the three to five% mark relative to overall group lending, which looks manageable. If cheaper commodities lead to lower costs for consumers and non-energy companies, they say, that should more than offset the pain. Look at ING, a Dutch lender with a big consumer operation: while oil-and-gas loan losses rose in the fourth quarter, overall group loan losses fell. But economists don’t seem to be showing much faith in the growth outlook.

Got to love Ambrose’s insistence on counter-intuitive intuition. However….

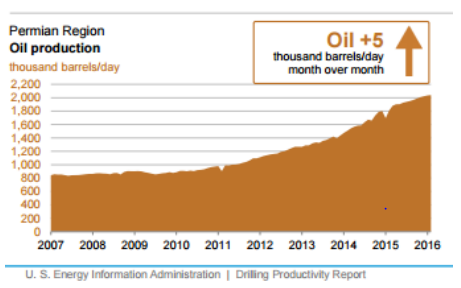

• US Shale Frackers Eye World Conquest Despite Bloodbath (AEP)

Dozens of indebted US shale companies face annihilation over coming months as their hedge protection runs out and creditors pull the plug, but veteran frackers insist defiantly that the slump will not stop the industry’s march to world conquest. “What is happening scares the heck out of you. We’re going to see a decimation for the industry, with bodies and corpses all over the place,” said Mark Papa, the former head of EOG Resources. “Lower for longer, is starting to feel like the Great Depression. You run for cash. You ride out the storm,” said John Hess, founder of the Hess Corporation. “It is probably a three-year process and we’re in the middle of it. The impact on investment has been devastating,” he told the IHS CERAWeek summit of energy leaders in Houston.

“Our activity is at a bare minimum, and we’re just preserving our operational capability. We had 17 rigs two years ago, eight last year, and now we’re running two. Very few things make sense at $30. It’s better to leave the oil in the ground,” he said. Mr Papa said the 70pc crash in oil prices since mid-2014 will wipe out those companies that leveraged to the hilt betting that crude prices would stay above $100 forever. Survivors will “rise from the ashes” – chastened but wiser. “They’re not going to stretch their balance sheets so much or make acquisitions based on false promises,” he said. Yet Mr Papa, a legendary figure in the shale fraternity and now at Riverstone Holdings, said OPEC’s price war against shale will not stop the US juggernaut. Oil giants with deep pockets are waiting in the wings to “gobble up” distressed assets, and America’s nimble mid-cost frackers will have an edge when the cycle turns.

Oil and gas investment has collapsed from $700bn in 2014 to nearer $400bn this year. IHS estimates that planned spending by 2020 will be $1.8 trillion less than forecast two years ago, almost guaranteeing an oil shortage as global demand keeps growing by 1.2m barrels per day (b/d) each year and existing wells deplete at an annual rate of 3m b/d. Mr Papa expects the global balance of supply and demand to tighten by 1.6m b/d this year. This would mop up the glut, before gradually eating into record stocks next year. “The market is going to grow to 100m b/d. Where is the quantity going to come from Capital spending on mega-projects has stopped cold,” he said. “I can see a case where US shale is the biggest supplier of oil in the world by 2020. We could turn the whole thing on its ear, producing 13-14m b/d. But it will be really ugly getting through this valley,” he said.

This would amount to 16m b/d if all liquids are included, more than the combined crude exports of Saudi Arabia and Russia. The International Energy Agency forecast this week that the US would account for much of the growth in world output by 2020 – after dropping 600,000 b/d this year, and 200,000 next year. Mr Papa said it will not be long before engineers work out how to double the efficiency of shale extraction to the 50pc levels seen in conventional oil wells. “It’ll probably come in the next ten years. That’s the next big break-through,” he said. David Hager, head of Devon Energy, said shale frackers have slashed cuts costs my more than outsiders generally realize since the heady days of the boom, when service fees and wages were rocketing. “A lot of plays work at $45-$50, and the vast majority from $55-$60. They certainly don’t need $90,” he said.

All that past revenue, and $100 billion in debt. That’s saying a few things.

• Arab States Face $94 Billion Debt Crunch (BBG)

Gulf Cooperation Council countries may struggle to refinance $94 billion of debt in the next two years as the region faces slowing growth, rising rates and rating downgrades, according to HSBC. Oil-rich GCC states have to refinance $52 billion of bonds and $42 billion of syndicated loans, mostly in the United Arab Emirates and Qatar, HSBC said in an e-mailed report. The countries also face a fiscal and current account deficit of $395 billion over the period, it said. Expectations that these funding gaps “will be part financed through the sale of sovereign U.S. dollar debt will complicate efforts to refinance existing paper that matures over 2016 and 2017,” Simon Williams, HSBC’s chief economist for the Middle East, said in the report.

“With the Gulf acting as a single credit market, the refinancing challenge will likely be much more broadly felt” and “compounded by tightening regional liquidity, rising rates and recent downgrades,” he said. GCC states, which collectively produce about a quarter of the world’s oil, are taking unprecedented measures to shore up their public finances as crude prices struggle to rebound from the lowest levels in 12 years. The countries, which include Saudi Arabia and Oman, have also been hit by a series of rating cuts, while billions of dollars have been drained from the region’s banking system.

Gulf countries have about $610 billion outstanding in FX-denominated bonds and syndicated loans, HSBC said. This includes financial and corporate debt, as well as sovereign debt, mainly in the U.A.E., Bahrain and Qatar, it said. HSBC is confident that the funding gaps will be covered and expects a “raft” of foreign sovereign bond issuance to fund budget deficits. Any new issuance will have to compete with upcoming refinancing needs, the bank said. Almost half of the maturities due in the next two years are in the banking sector, HSBC said, “suggesting any increase in costs at refinancing could quickly feed through into a broader monetary tightening.”

“..the stupid is not impossible..”

• SocGen’s Albert Edwards Is Rethinking His ‘Ice Age’ Theory (MW)

Uber-bear Albert Edwards says his famous/infamous “Ice Age” investment theory may need a major rethink after a further drop in yields for Japanese government bonds. The Société Générale equity strategist first introduced his flagship piece of glacial advice, which urges an underweight on equities and heavily long position on bonds, in 1996. It was devised from his long-standing position that deflationary pressures will trigger a stock-market collapse and a bond-market boom. Edwards had this to say in a note to investors on Thursday: “With [10-year Japanese government bonds] yesterday falling to record-low negative yields of minus 0.06% and Switzerland [10-years] having already fallen to minus 0.5%, I’m now in the process completely rethinking my Ice Age investment thesis,” he said.

The contrarian investor still seems to hate stocks, though. In January, he predicted that “another leg in the secular equity valuation bear market,” would take the S&P 500 down 75% from its recent peak to around 550. “I haven’t changed my view on that at all and look forward to the opportunity of buying lots of cheap equities in the months and years ahead,” he wrote in this latest note. “But it is our overweight long bond position that has me a bit flummoxed.” On one hand, he openly questioned how long Japanese bonds can continue their uninterrupted rally that has been going on for nearly a decade and has pushed yields to record-low negative territory. Yet he seemed to imply that yields practically have nowhere else to go but lower.

“How low can they go?” he asked, adding that Japanese 10-years are “the only major global asset class that [has] not seen a negative year-over-year return at any time since the Global Financial Crisis at the start of 2007.” Given that Japanese 10-year bonds have been eking out positive returns for nearly a decade while their yields have already crashed below zero to a record low of minus 0.06%, a further move lower would imply interest rates would fall further into negative territory, Edwards’ rationale continued. But that could have disastrous consequences, the doomsday thinker suggested. Edwards quoted a recent article by Edward Chancellor at Breaking Views that argues that negative interest rates “undermine bank profitability, threaten the stability of bank liabilities, force households to save more, and discourage credit creation.”

Nor, Edwards said, are negative policy rates good in fighting deflation. But even as negative interest rates make little sense to him, Edwards concluded that “the stupid is not impossible,” quoting SocGen analyst Andrew Lapthorne.

And yet another boomerang.

• Negative Rates = Deleveraging (Tonev)

While conventional theory suggests that central banks set base interest rates and that negative rates are a result of low inflation and slow economic growth, we suggest there may be an alternative explanation. Drawing on historical and cultural analogies, we view negative rates as a possible market response to the growing levels of debt and inequality in income and wealth. In April last year, Switzerland became the first country to issue a 10-year sovereign bond at a negative yield. By the end of 2015, about a third of newly issued eurozone sovereign bonds came with a negative yield. Investors who buy these bonds and hold them to maturity will receive less than they put in and the issuer will ultimately pay back less than borrowed. Through this mechanism, we believe that negative interest rates can be a useful tool for deleveraging.

We recognise that the challenge to this view is that the objective of this policy has been to encourage even more leverage; the case of the Swedish housing market comes to mind. The majority of the countries with negative yields on their government bonds have high levels of either government or private debt (or in some cases both). Historically, one would expect government yields to go up to discourage the issuance of more debt. This is not happening now. Why? We suggest that, precisely because of the high level of debt and the need to deleverage, nominal yields in those countries have become more and more negative to encourage the issuance of more debt and slowly roll down the existing debt stock.

This suggests the market may be indicating there is too much debt. But this has an implication for the creation of new money, which is essential for the normal functioning of the economy. Most of the money creation in the developed world is done by the private banking system through issuing loans. If there is no demand for new debt, the money creation process stalls. In other words, while under the gold standard our money creation was constrained by the availability of gold, in the current “fiat” monetary system, we cannot issue new money without the issuance of new debt. However, the system after 1971 was much more flexible than the metallic standard before because, as long as the economy was expanding, the banks could always find someone willing to borrow from them and thus increase the money supply.

But not as wrong as Australians will turn out to be.

• I Was Wrong On Australian House Prices (Steve Keen)

“I was hopelessly wrong on house prices. Ask me how.” It’s about time I answered that question, isn’t it? In a nutshell, I got the cause of the Aussie House Price Bubble right, but the direction of the cause wrong. The fundamental determinant of house prices is mortgage debt. I thought that – as had happened in Japan after its bubble economy burst – the Australian economy would start to de-lever after the GFC, and that this process would take house prices down with it. This is what happened in the USA and most of the First World. But in Australia, the rate of change of mortgage debt never went negative and deliberate government policy played a major role in stopping that from happening on two separate occasions: The Rudd stimulus package in October 2008 and the reversal of the RBA’s “fight the inflation bogeyman” policy of rising interest rates in November 2011.

Both policies allowed – and indeed encouraged – mortgage growth to continue long after it would have stopped without government intervention, and long after it did stop in most of the rest of the First World. Though they didn’t quite know why it worked, Treasury knew from experience that a boost to the housing market stimulated the economy – so they advised Rudd to throw in what I nicknamed the “First Home Vendors Boost” into his rescue package. The $7,000 Federal Government grant doubled to $14,000 for buyers of existing properties, and trebled to $21,000 for those buying new properties (State governments threw in their own debt sweeteners as well – with Victoria purchasers being given up to $36,500 in total). First home buyers flooded into the market, leveraging up the grant by a factor of ten or more in additional mortgage debt.

This stopped the decline in mortgage debt in its tracks and growth in mortgage lending – and house prices – resumed until the grant ended in mid-2010. The RBA’s policy intervention was even more shambolic – but, ultimately, even more effective – than Treasury’s. With its conventional economic mind set, the RBA not only failed to see the GFC coming but continued to put interest rates up after it struck (unlike all other Central Banks, save the equally incompetent ECB). Like a general determined to win the last war, Stevens continued to build his Maginot line against the inflation demon, only to belatedly concede that deflation was the actual foe. Fully one year after the GFC began, the RBA reluctantly joined the global surrender of central banks to this unexpected enemy and dropped its reserve rate from 7.25% to 3% in a mere 8 months.

But then, confident that the war it hadn’t seen coming was over, the RBA resumed its struggle to win the previous one against inflation. It put its rate up from 3% to 4.75% in 14 months – at the same time as the stimulus from Rudd’s ‘First Home Vendors Boost’ was ending. By this time, Australia’s prosperity stood on the twin pillars of China’s export demand – thanks to its huge post-GFC stimulus package – and the investment boom this induced in Australia’s mining sector. Since even those enormous injections weren’t enough to keep the economy on the mend, the RBA was again forced to reverse direction and began cutting its rate in late 2011 – this time with the deliberate hope that a restored housing bubble would take the place of an unexpectedly unfulfilling mining boom.

Better get that UN emergency summit set up, Angela.

• Egypt Migrant Departures Stir New Concern In Europe (Reuters)

The EU fears Mediterranean migrant smuggling gangs are reviving a route from Egypt, officials told Reuters, putting thousands of people to sea in recent months as they face problems in Libya and Turkey. “It’s an increasing issue,” an EU official said of increased activity after a quiet year among smugglers around Alexandria that has raised particular concerns in Europe about Islamist militants from Sinai using the route to reach Greece or Italy. Departures from Egypt were a tiny part of the million people who arrived in Europe by sea last year; more than 80% came from Turkey to Greece and most others from Libya to Italy. Detailed figures on Egypt are not available. But as security in anarchic Libya has worsened, EU officials say, more smugglers are choosing to bring African and Middle East refugees and migrants to the Egyptian coast.

Voyages from Egypt are long, but smugglers mainly count on people being rescued once in international shipping lanes. Brussels, engaged in delicate bargaining with Turkey to try and stem the flow of migrants from there, is concerned that the Egyptian authorities are not stopping smugglers. But it is reluctant to use aid and trade ties to pressure Cairo to do more when Egypt remains an ally in an increasingly troubled region. “Our major concern is that among smugglers and migrants there may also be militants from the Sinai, affiliated to al Qaeda or Islamic State,” a second EU official said. “Controls in Egypt are strict, which limit the activities of smugglers … But sometimes we suspect that they turn a blind eye to let migrants go somewhere else.” An Egyptian security official told Reuters that Cairo had more pressing concerns, limiting resources to control migrants.

Let him do something. He has the clout, and the Vatican has the resources.

• Pope Urges United Response To Refugee ‘Drama,’ Praises Greece (Reuters)

Pope Francis called on Sunday for a united response to help flows of people into Europe fleeing war and suffering, as the region argues over sharing the burden of looking after them. Addressing crowds in St. Peter’s Square at the Vatican, Francis, who decried the suffering of migrants at the border between Mexico and the United States this month, said the “refugee drama” was always in his prayers. “Greece and other countries on the front line are giving these people generous help, which needs the collaboration of all countries. A response in unison could be effective and distribute the load fairly,” the pontiff said. “To do this, we need to push decisively and unreservedly in negotiations,” he added.

Greece has been inundated with refugees and migrants after Balkan countries shut their borders and Austria restricted entry for the hundreds of thousands aiming for Europe, which is in the second year of its biggest migration crisis since World War Two. Francis welcomed a cessation of hostilities deal in Syria, where five years of civil war have killed more than 250,000 people and driven 11 million from their homes, swelling the tide of refugees. “I have greeted with hope the news about a stop to hostilities in Syria, and I invite everyone to pray that this glimmer can give relief to the suffering population, enable necessary humanitarian aid and open the way to dialogue and longed-for peace.” Guns fell mostly silent in Syria when the truce came into effect on Saturday, but reports of violations have come from both sides.

The crisis it created itself.

• EU Warns Of Humanitarian Crisis As Emergency Measures Prepared (Kath.)

Migration Commissioner Dimitris Avramopoulos has warned of an imminent humanitarian crisis in Greece unless “all sides assume their responsibilities” in the coming days, as both the European Union and Athens hammered out emergency measures. “There is no point in playing the blame game any more. We simply have to do everything possible to control the situation,” Avramopoulos said in an interview with Kathimerini’s Sunday edition, pointing at the conclusions reached at last week’s EU meeting of interior ministers. The Greek official called for the implementation of a deal signed between Brussels and Ankara in November to slow the migrant flow; he urged EU states to fulfill pledges to accept asylum-seekers for relocation; and condemned “unilateral actions” taken by several countries, such as the introduction of border controls and Vienna’s cap on asylum seeker numbers.

“Time is no longer on our side,” Avramopoulos said ahead of a crucial meeting of EU leaders with Turkey on March 7. More than 25,000 migrants and refugees were stranded in Greece over the weekend as neighboring states shut down their borders. An estimated 2,000-3,000 reach the country’s islands every day. Speaking to Kathimerini on condition of anonymity, a senior European official said that the Commission is preparing a package of measures to be activated in the event of a humanitarian crisis in Greece or other nations along the Balkan migrant route. These, the official said, include providing funding to an international organization to set up a refugee camp as well as vouchers for refugees to acquire food and accommodation. Similar aid has been provided to African countries, as well as Lebanon and Jordan.

Meanwhile, the Greek government last week requested 228 million euros in emergency aid from the Commission to be spend on infrastructure for the ballooning number of migrants. An emergency plan submitted by Athens foresees the creation of new reception places in addition to the 50,000 Athens has already pledged to the Europeans.

At least someone calls a spade a spade. “Even at this late stage, Europe’s governments must realise where their fragmented response is heading.”

• Europe Turns Its Back On Greece Over Refugees (FT)

Time is running out for the EU’s 28 member states to take the co-ordinated action that is needed to start bringing Europe’s migrant crisis under control. At the beginning of this year, Donald Tusk, the EU president, warned the bloc’s leaders that they must implement an EU-wide solution to the crisis when they meet in Brussels on March 17, or face “grave consequences” as summer begins and refugee flows from the Middle East and north Africa accelerate. With less than three weeks left to the summit, his warning is being wilfully disregarded by EU governments who prefer unilateral action to the collective effort that is sorely needed. In recent days, more and more member states have swept aside the Schengen system for border-free travel in the EU and acted alone. France and Belgium have engaged in verbal sparring after a Belgian decision to impose border controls on their common border.

Hungary has pledged a referendum on European Commission plans to share out refugees, currently in Greece and Italy, across the bloc — a severe blow to common action. Most strikingly, Austria, once a strong supporter of a collective EU stance, has joined ranks with nine neighbouring states to impose border controls that will stop refugees coming from Greece into Europe through the “Western Balkans route”. These moves are unlikely to deter the flight of more desperate refugees from Syria and other failed states into Europe. In the first two months of this year, more than 100,000 crossed into Greece, compared with 5,000 in the same period in 2015. The UN predicts that another 1m refugees will travel into Europe in the course of 2016.

What is far more worrying is that the action by Austria and its Balkan allies to seal their southern border risks creating a humanitarian emergency in Greece. The Greek government has a contingency to shelter 70,000 migrants, but more than 2,000 are arriving each day on Greek territory. Greece’s difficulty is all the more acute because, after six years of recession, it is now struggling with the punishing fiscal retrenchment imposed in last year’s bailout deal. Even at this late stage, Europe’s governments must realise where their fragmented response is heading. Greece cannot be condemned by the rest of the EU to becoming a migrant holding pen or, as prime minister Alexis Tsipras has put it, “a warehouse of souls”. Instead, the bloc should adopt the collective approach advocated by Mr Tusk and German chancellor Angela Merkel.

But Greece is already in chaos, thanks to EU economic policies.

• We Can’t Allow Refugee Crisis To Plunge Greece Into Chaos, Says Merkel (G.)

The German chancellor, Angela Merkel, has warned that European countries cannot afford to allow the continent’s continuing refugee crisis to plunge debt-stricken Greece into chaos by shutting their borders to migrants. With up to 70,000 refugees expected to become stranded on Greece’s northern borders in the coming days, Merkel warned that the recently bailed-out Athens government could become paralysed by the huge numbers of arrivals from war-torn areas of the Middle East and Africa. “Do you seriously believe that all the euro states that last year fought all the way to keep Greece in the eurozone – and we were the strictest – can one year later allow Greece to, in a way, plunge into chaos?” she said in an interview with public broadcaster ARD.

Merkel also defended her open-door policy for migrants, rejecting any limit on the number of refugees allowed into her country despite divisions within her government. Merkel said there was no “Plan B” for her aim of reducing the flow of migrants through cooperation with Turkey and warned that the efforts could unravel were Germany to cap the number of refugees it accepts. “Sometimes, I also despair. Some things go too slow. There are many conflicting interests in Europe,” Merkel told state broadcaster ARD. “But it is my damn duty to do everything I can so that Europe finds a collective way.“ Merkel spelled out her motivation to keep Germany’s borders open without limits on refugees, a policy which has damaged her once widespread popularity. “There is so much violence and hardship on our doorstep,” she said. “What’s right for Germany in the long term? There, I think it is to keep Europe together and to show humanity.

“In the next month 50,000-70,000 will come and then I believe [the flows] will stop there..” What will stop them?

• Up To 70,000 Migrants ‘May Soon Be Stranded In Greece’ (Guardian)

Up to 70,000 migrants and refugees could soon be stranded in Greece, the leftist-led government said as it considered enlisting the help of the army to deal with the emergency. The alarm was sounded as the EU’s top immigration policymaker warned the situation was at risk of becoming uncontrollable unless member states “assume their responsibilities”. “In the next month 50,000-70,000 will come and then I believe [the flows] will stop there,” Athens’ migration minister, Yannis Mouzalas, said. Admitting it would “be hard and very difficult” Mouzalas said it was also likely the Greek armed forces – recently brought in to build “hotspot” screening centres – would be deployed to tackle the crisis. “Wherever the army is needed it will play a role just as it does in all western democracies,” he added.

“Now we use it to build [camps and centres] and to distribute nutrition, tomorrow we don’t know, we may deploy trucks and use it in several other services.” The leftists, in power with the small rightwing Independent Greeks party, have so far resisted giving armed forces a more prominent role in handling the influx of people entering Europe across the Aegean from Turkey. In a country that experienced seven years of military dictatorship until 1974, many leftists have expressed consternation.

By Sunday 22,000 people were trapped in Greece with an estimated 6,000 stuck at the Macedonian border after restrictions were tightened – and frontiers effectively sealed to all but Syrians – by Balkan nations along the migrant route. But while Mouzalas insisted the increased numbers would be manageable, the EU’s migration commissioner Dimitris Avramopoulos spoke of an imminent humanitarian crisis if the 28-nation bloc continued to indulge in “unilateral actions.” “There is no point in playing the blame game any more. We simply have to do everything possible to control the situation,” he told the Sunday edition of Kathimerini. Enmeshed in its worst economic depression in modern times, debt-stricken Greece has requested emergency aid from the EU. As part of urgent plans to be put into immediate effect, Mouzalas said impromptu camps would be established that would also see tents erected in local sports grounds.

A further four hotspots will be set up in the northern Greek province of Macedonia. In anticipation of the influx, Athens has asked for tents, blankets, sleeping bags, transport vehicles, ambulances and other supplies. “In Germany we have taken the decision that we have to support Greece,” Berlin’s ambassador to Athens, Peter Schoof, announced at an economic forum held in Delphi. Germany’s hardline finance minister, Wolfgang Schäuble, hinted that Europe’s powerhouse might also be willing to cut Greece some slack as it struggles with the dual task of dealing with the refugee crisis and enacting punishing reforms. With divisions widening ahead of an emergency EU summit to discuss the crisis on 7 March anger is mounting with Berlin enraged at the way Balkan nations, led by Austria, have closed the refugee transit route.