US President Donald Trump will meet Russia’s Vladimir Putin later on Monday, ending a tumultuous European tour in which he criticised his allies. Mr Trump said he had “low expectations” ahead of the talks in the Finnish capital, Helsinki, but added that “maybe some good” would come of them. The summit comes after 12 Russians were charged with hacking in the 2016 US elections. Mr Trump says he will raise the issue, but there is no formal agenda. The two leaders will meet one-on-one, and will be joined only by their interpreters. It is the first-ever summit between Mr Putin and Mr Trump – although they have previously met on the sidelines of multilateral talks.

There have been calls in the US for Mr Trump to cancel the meeting altogether over the indictments of Russian military intelligence agents, announced on Friday. Russia denies the allegations, and says it is looking forward to the talks as a vehicle for improving relations. US National Security Adviser John Bolton has said both sides have agreed the meeting will have no set agenda. But he said he found it “hard to believe” Mr Putin did not know about the alleged election hacking and the subject would be mentioned. “That’s what one of the purposes of this meeting is, so the president can see eye to eye with President Putin and ask him about it,” he told ABC News.

U.S. President Donald Trump’s criticism of Russia’s Nord Stream-2 gas pipeline to Europe is an egregious example of unscrupulous competition and it worries Moscow, Kremlin spokesman Dmitry Peskov was quoted as saying on Monday. Speaking shortly before Trump and Russian President Vladimir Putin sit down together for a summit in the Finnish capital, Peskov also said discussions between the two on Syria would be difficult because of the U.S. stance on Iran, Russia’s ally and a major player in the Syrian conflict. Russia’s RIA news agency quoted Peskov as saying he hoped the Helsinki talks would represent some kind of step away from the current crisis in U.S.-Russian relations.

Donald Trump described the European Union one of his greatest “foes” in another extraordinary diplomatic intervention on Sunday, just hours before sitting down to a high-stakes summit with Russian president Vladimir Putin. Asked in a TV interview to name his “biggest foe globally right now”, the US president started by naming the European Union, calling the body “very difficult” before ticking off other traditional rivals like Russia and China. Hours earlier, British prime minister Theresa May revealed that Trump suggested she “sue the EU” rather than go into negotiations over Brexit. “Well I think we have a lot of foes,” Trump told CBS News at his Turnberry golf resort in Scotland. “I think the European Union is a foe, what they do to us in trade. Now you wouldn’t think of the European Union but they’re a foe.”

Apparently taken aback, anchor Jeff Glor replied: “A lot of people might be surprised to hear you list the EU as a foe before China and Russia.” But Trump insisted: “EU is very difficult. I respect the leaders of those countries. But – in a trade sense, they’ve really taken advantage of us.” Trump’s controversial tour through Europe has turned postwar western relations inside out, the president sparring with Nato leaders in Brussels and blasting May’s Brexit strategy in the Sun newspaper. His remarks have reflected one of this president’s core beliefs: that America is exploited by its allies. Donald Tusk, president of the European council, tweeted: “America and the EU are best friends. Whoever says we are foes is spreading fake news.”

China ranges over the global economy like a bull elephant roams the savanna. Other grassland wildlife is sensitive to this mammoth’s slightest moves. The ferocious lion, the U.S., is no exception. China has yet to become fully aware that it is the elephant in the global economy’s boardroom. But in Washington, Trump was cognizant that he could not stand idly by after China vowed to knock the U.S. off its economic pedestal in just 17 years from now. He campaigned for the presidency by promising voters he would put “America first.” News of China’s decision to bring forward its modernization target date emerged at a bad time. It came shortly after Xi had promised Trump business deals worth $250 billion.

That pledge came in November, when Trump was visiting Beijing, and was portrayed as a salve that would help to heal the U.S.’s massive trade deficit with China. As expected, it was little more than talk. The trade gap continues to quickly widen. Alarmed by China’s ambitions and frustrated by the lack of progress in narrowing the U.S. trade deficit, Trump went on the offensive in the spring. There are good reasons for China coming under U.S. trade fire. It has been the biggest beneficiary of the global trade system since it became a member of the World Trade Organization at the end of 2001. All the while, it has imposed strict foreign ownership limits in each industrial sector, forced foreign companies that enter China to transfer technologies and has set up various other barriers to its markets.

Backed by huge amounts of government funds, Chinese companies have made splashy acquisitions of U.S. and European companies that own key technologies, especially in the auto and information technology sectors. Chinese companies can quickly obtain technologies by acquiring or taking equity investments in U.S. and European companies. In the U.S. and Europe, any company can acquire any other company as long as it can obtain the necessary funds. But it is difficult for U.S. and European companies to acquire Chinese companies. Chinese authorities have numerous regulations at their disposal to block any such attempt.

When Xi bared China’s sharp claws, declaring China would overtake the U.S. economically by 2035, he did so for the benefit of a domestic audience and to aid his fierce power struggle with the political factions that had run China for decades. China is now beginning to realize the high price it is having to pay for Xi’s declaration.

“When the monster, ‘everything’ bubble pops, so will the paper markets in gold, silver, and other precious metals. The size of this market is at least 100-times bigger than the physical market.”

“It is absolutely unreal how the world pays so much respect to mediocrity or even incompetence when it comes to running the financial system. Central banks and their heads have created this monster balloon which is now waiting to be popped. They have given the world the impression that they have been instrumental in saving the world economy. The central bank chiefs that managed to retire before the balloon burst can count themselves lucky. In my view, the luck is now in the process of running out for the present ones. These chiefs believe so much in their own ability as saviors of the world that they don’t understand that all they are doing is creating a much bigger monster by printing and printing and printing.

[..] When the monster, ‘everything’ bubble pops, so will the paper markets in gold, silver, and other precious metals. The size of this market is at least 100-times bigger than the physical market. The rise of this market is very much linked to manipulation of the precious metals by central banks, the Bank for International Settlements (BIS), and bullion banks. When the paper metals markets pop, there will be no gold (or silver) offered at any price. This is the time when overnight or over a weekend the price will go from $1,250 to $10,000 or even $100,000. This might sound totally unreal to some, but this will be the most likely consequence of the monster bubble popping and everyone in markets running for the exit.

Most people believe that the status quo can go on forever and that central banks will continue their ridiculous game of pretending that air is real money that can create wealth. The few people who believe that there is a serious risk that the system will not survive in its present form, and that their assets — be it cash, bonds, or stocks — could decline substantially in value, must seriously consider insurance.

The next decline in financial markets is likely to start in late 2018 or early 2019. And this will not be an ordinary decline or normal correction. Instead, it will be the beginning of the biggest global bear market in history. And this time central banks and governments will fail in their attempts to save the system. They will, however, certainly print a lot of money and try to reduce interest rates. But as global bond markets collapse, rates will go up rapidly. This means that bonds and stocks will both crash along with most assets.

Lyndon Johnson, who was majority leader in the US Senate before he became his country’s president, once declared that the most important talent in politics is “the ability to count”. There aren’t enough people who can count around Mrs May. The fatal flaw in her plan is that there is no majority for it in the House of Commons. The Brexit ultras are crying treachery and promising havoc. They both express and feed the furies of Tory activists. The Brextremists don’t have an alternative plan, other than to crash out of the EU without any deal at all, a catastrophic outcome that some of them actually wish for, but that hasn’t stopped them before and won’t curb them now.

Jacob Rees-Mogg and his cabal can muster the 48 signatures of Tory MPs that they need to trigger a confidence vote in Mrs May. They do not sound confident that they have the numbers – they require 159 – to oust her from the premiership. What the ultras can do is make the government’s life even more hellish by prosecuting a “guerrilla war” in parliament. Even if Mrs May could get the EU to accept her plan, 60-plus Conservative MPs are opponents of her version of a Brexit deal. That number will climb if, as is inevitable, she has to make further concessions in Brussels to secure an agreement. There are more than enough Brextremist rebels to block the prime minister in the Commons unless she can get some assistance from the opposition.

She needs the help of Labour MPs and she is not going to get it. Jeremy Corbyn won’t give her any succour. He is more interested in bringing down the Tories than helping them to solve a mad riddle of their own making. The Labour leadership calculates that defeating Mrs May in Brexit votes is their best chance of collapsing the government and precipitating an early general election. But Number 10 clearly harboured hopes that centrist Labour MPs might embrace her plan as the least worst version of Brexit that they are likely to get in the circumstances.

Theresa May faces a concerted rebellion from the hard Brexit wing of the Conservative party on Monday, as MPs unhappy with her Chequers compromise prepare to mount a show of strength by voting for their amendments on the customs bill. The party’s European Research Group says it will reject any last attempts at compromise by Number 10 as they hope to force May to change course over Brexit or risk a no-confidence vote before the summer break by demonstrating the depth of their support. A special ERG whipping operation, using the WhatsApp messaging service, has been created by Steve Baker, the former Brexit minister who resigned from the government last week, although ERG insiders would not put a number on how many they expected to rebel in the Commons.

Jacob Rees-Mogg, the chairman of the ERG, told the BBC “we’ll have an idea of the numbers at 10pm on Monday evening” while one ERG insider added that they were “intensely relaxed” about the number of rebels they had signed up. Last week, members of the hard Brexit group put down four amendments to the taxation (cross-border trade) bill due to be debated on Monday evening, aimed at halting the customs plan announced by May at Chequers nine days ago. The level of support they attract will draw intense focus, particularly if the number significantly exceeds the 48 required to call for a vote of no confidence in May’s leadership of the Conservative party.

Britain’s housing market saw a glut of new property offered for sale this month, keeping a lid on prices at a time when sales typically suffer from a seasonal lull, property website Rightmove said on Monday. Real estate agents now have the highest amount of stock since September 2015, Rightmove said. “While an increase in seller numbers is a welcome sign of more liquidity in a generally stock-starved market, it has unfortunately come at a quieter time of year,” Rightmove director Miles Shipside said. The number of homes advertised by Rightmove, Britain’s largest property website, is 8.6 percent higher than the same month a year ago, but the number of sales is virtually unchanged from a year earlier, down 0.2 percent.

Average asking prices for new sellers are down 0.1 percent since June, typical for the time of year, Rightmove added. But in a sign that previous sellers had priced their property too high, a third of stock being advertised had seen at least one price reduction, the highest proportion for the time of year since 2011. Other industry data has shown British house price growth has slowed sharply since the June 2016 Brexit vote, though with marked regional variation. The slowdown is most marked in London and neighbouring areas, where demand has been hit by higher tax on expensive property and reduced demand from foreign investors. In other parts of Britain, prices are still rising moderately.

The European Union on Monday called on the United States, China and Russia to work together to avoid trade “conflict and chaos” to prevent it spiralling into violent confrontation. “It is the common duty of Europe and China, but also America and Russia, not to destroy (the global trade order) but to improve it, not to start trade wars which turned into hot conflicts so often in our history,” EU Council President Donald Tusk said in Beijing. “There is still time to prevent conflict and chaos.” Tusk spoke after meeting with Chinese Premier Li Keqiang as part of an annual EU-China summit that opened against the backdrop of the growing China-US economic confrontation and wider global trade discord.

The EU — the world’s biggest single market with 28 countries and 500 million people — is trying to buttress alliances in the face of the protectionism unleashed by US President Donald Trump’s “America First” administration. The meeting between Chinese and European officials in Beijing, which also included European Commission head Jean-Claude Juncker, comes as Trump prepared to hold talks in Helsinki with Russian leader Vladimir Putin. The world needed trade reform, rather than confrontation, Tusk said. “This is why I am calling on our Chinese hosts, but also on Presidents Trump and Putin, to jointly start this process from a thorough reform of the WTO.”

Tuesday is a red-letter day for international law: from then on, political and military leaders who order the invasion of foreign countries will be guilty of the crime of aggression, and may be punishable at the international criminal court in The Hague. Had this been an offence back in 2003, Tony Blair would have been bang to rights, together with senior numbers of his cabinet and some British military commanders. But if that were the case, of course, they would not have gone ahead; George W Bush would have been without his willing UK accomplices. The judgment at Nuremberg declared that “to initiate a war of aggression … is the supreme international crime”.

But this concept never entered UK law (as the misguided crowdfunded effort to prosecute Blair discovered last year). International acceptance of it stalled until states could agree on an up-to-date definition. The crime was included in the ICC jurisdiction back in 1998, but was suspended until its elements could be decided (in 2010) then ratified by at least 30 states (in 2016). At last it is finally being “activated”. In the meantime, Iraq and Ukraine have been invaded and other countries threatened, while Donald Trump attacked Syria last year. Now, the very existence of the crime of aggression offers some prospect of deterrence, and some degree of certainty in identifying the criminals.

How many people remember it was the US that drove Castro into Russian arms? He visited the US shortly after becoming president. Eisenhower refused to talk. Everything after that is propaganda and fake news.

Guerrilla revolutionary and communist idol, Fidel Castro was a holdout against history who turned tiny Cuba into a thorn in the paw of the mighty capitalist United States. The former Cuban president, who died aged 90 on Friday, said he would never retire from politics. But emergency intestinal surgery in July 2006 drove him to hand power to Raul Castro, who ended his brother’s antagonistic approach to Washington, shocking the world in December 2014 in announcing a rapprochement with US President Barack Obama. Famed for his rumpled olive fatigues, straggly beard and the cigars he reluctantly gave up for health reasons, Fidel Castro kept a tight clamp on dissent at home while defining himself abroad with his defiance of Washington.

In the end, he essentially won the political staring game, even if the Cuban people do continue to live in poverty and the once-touted revolution he led has lost its shine. As he renewed diplomatic ties, Obama acknowledged that decades of US sanctions had failed to bring down the regime – a drive designed to introduce democracy and foster western-style economic reforms – and it was time to try another way to help the Cuban people. A great survivor and a firebrand, if windy orator, Castro dodged all his enemies could throw at him in nearly half a century in power, including assassination plots, a US-backed invasion bid, and tough US economic sanctions.

Born August 13, 1926 to a prosperous Spanish immigrant landowner and a Cuban mother who was the family housekeeper, young Castro was a quick study and a baseball fanatic who dreamed of a golden future playing in the US big leagues. But his young man’s dreams evolved not in sports but politics. He went on to form the guerrilla opposition to the US-backed government of Fulgencio Batista, who seized power in a 1952 coup. That involvement netted the young Fidel Castro two years in jail, and he subsequently went into exile to sow the seeds of a revolt, launched in earnest on December 2, 1956 when he and his band of followers landed in southeastern Cuba on the ship Granma. Twenty-five months later, against great odds, they ousted Batista and Castro was named prime minister.

Once in undisputed power, Castro, a Jesuit-schooled lawyer, aligned himself with the Soviet Union. And the Cold War Eastern Bloc bankrolled his tropi-communism until the Soviet bloc’s own collapse in 1989. Fidel Castro held onto power as 11 US presidents took office and each after the other sought to pressure his regime over the decades following his 1959 revolution, which closed a long era of Washington’s dominance over Cuba dating to the 1898 Spanish-American War.

Wisconsin’s election board agreed on Friday to conduct a statewide recount of votes cast in the presidential race, as requested by a Green Party candidate seeking similar reviews in two other states where Donald Trump scored narrow wins. The recount process, including an examination by hand of the nearly 3 million ballots tabulated in Wisconsin, is expected to begin late next week after Green Party candidate Jill Stein’s campaign has paid the required fee, the Elections Commission said. The state faces a Dec. 13 federal deadline to complete the recount, which may require canvassers in Wisconsin’s 72 counties to work evenings and weekends to finish the job in time, according to the commission. The recount fee has yet to be determined, the agency said in a statement on its website.

Stein said in a Facebook message on Friday that the sum was expected to run to about $1.1 million. She said she has raised at least $5 million from donors since launching her drive on Wednesday for recounts in Wisconsin, Michigan and Pennsylvania – three battleground states where Republican Trump edged out Democratic nominee Hillary Clinton by relatively thin margins. Stein has said her goal is to raise $7 million to cover all fees and legal costs. Her effort may have given a ray of hope to dispirited Clinton supporters, but the chance of overturning the overall result of the Nov. 8 election is considered very slim, even if all three states go along with the recount. The Green Party candidate, who garnered little more than 1 percent of the nationwide popular vote herself, said on Friday that she was seeking to verify the integrity of the U.S. voting system, not to undo Trump’s victory.

A series of informal but concerted efforts by pro-remain politicians to reshape or even derail the Brexit process is under way and gaining momentum, according to people involved. MPs from across the parties had discussed how to push the government into revealing its Brexit plans and to ensure continued single market access, sources said, as a series of senior political figures made public interventions suggesting the result of the EU referendum could be reversed. Tony Blair and John Major both suggested this week that the public should be allowed to vote on or even veto any deal for leaving the EU. However, those connected to efforts by serving pro-remain MPs say the former prime ministers’ views had little support in the Commons.

More significant, they argued, were strategy discussions involving MPs from all parties “caught between their own views and those expressed at the ballot box” in the referendum. “It’s a long process of gradually bringing people round to our way of thinking, on all sides,” said someone who works closely with pro-remain figures. “A lot of people are a bit unsure what to do – they’re caught between their own views and those expressed at the ballot box, often by their own constituents. “There’s a growing realisation that this is a long game. There’s actually very little information out there, and very little substance to get into. It’s hard to coalesce people around particular policy positions when the government has no policy to speak of. That’s quite a challenge.”

Major told a private dinner that there was a “perfectly credible case” for holding a second referendum on the terms of a Brexit deal. He said the views of the 48% of people who voted to remain should be taken into account and warned against the “tyranny of the majority”. Blair, in particular, is known to be sounding out opinion on Brexit as part of his re-emergence into political life. The former Labour prime minister’s office said he had discussed the issue with the former chancellor George Osborne, among “many people”.

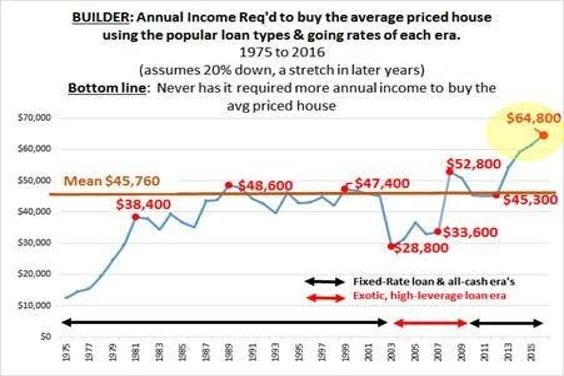

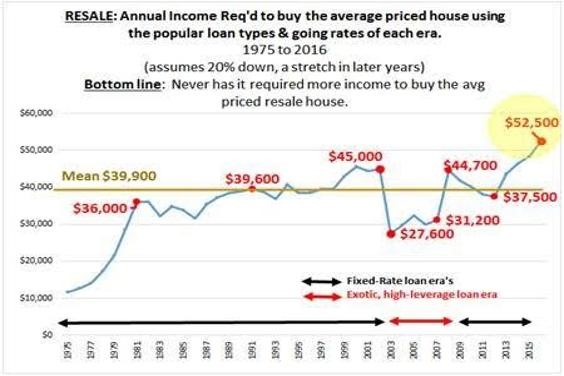

Houses have NEVER BEEN MORE EXPENSIVE to end-user, mortgage-needing shelter buyers. The recent rate surge crushed what little affordability remained in US housing. It now it requires 45% more income to buy the average-priced house than just four years ago, as incomes have not kept pace it goes without saying. The spike in rates has taken “UNAFFORDABILITY” to such extremes that prices, rates, and/or credit are now radically out of scope. At these interest rate levels house prices are simply not sustainable even in the lower-end price bands, which were far more stable than the middle-to-higher end bands (have been under significant pressure since spring). [..] The Data (note, for simplicity my models assume best-case 20% down and A-grade credit, which is the “minority” of lower-to-middle end buyers).

1) The average $361k builder house requires nearly $65k in income assuming a 4.5% rate, 20% down, and A-grade credit. Problem is, 20% + A-credit are hard to come by. For buyers with less down or worse credit, far more than $65k is needed. For the past 30-YEARS income required to buy the average priced house has remained relatively consistent, as mortgage rate credit manipulation made houses cheaper. Bottom line: Reversion to the mean will occur through house price declines, credit easing, a mortgage rate plunge to the high 2%’s, or a combination of all three. However, because rates are still historically low and mortgage guidelines historically easy, the path of least resistance is lower house prices.

2) The average $274k builder house requires nearly $53k in income assuming a 4.5% rate, 20% down, and A-grade credit. Problem is, 20% + A-credit are hard to come by. For buyers with less down or worse credit, far more than $53k is needed. For the past 30-YEARS income required to buy the average priced house has remained relatively consistent, as mortgage rate credit manipulation made houses cheaper. Bottom line: Reversion to the mean will occur through house price declines, credit easing, a mortgage rate plunge to the high 2%s, or a combination of all three. However, because rates are still historically low and mortgage guidelines historically easy, the path of least resistance is lower house prices.

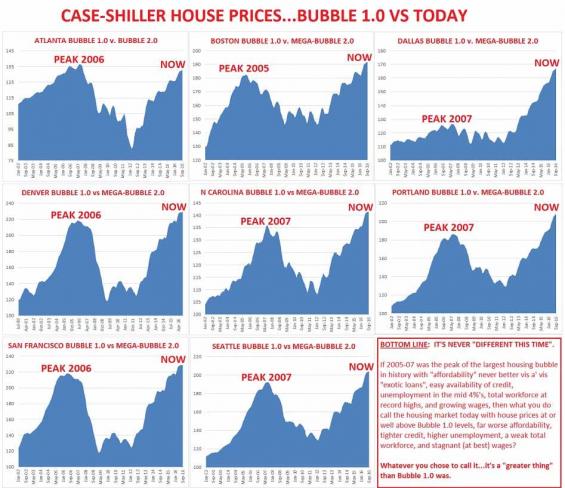

3) Bonus Chart … Case-Shiller Coast-to-Coast Bubbles Bottom line: IT’S NEVER DIFFERENT THIS TIME. Easy/cheap/deep credit & liquidity has found its way to real estate yet again. Bubbles are bubbles are bubbles. And as these core housing markets hit a wall they will take the rest of the nation with them; bubbles and busts don’t happen in “isolation.”

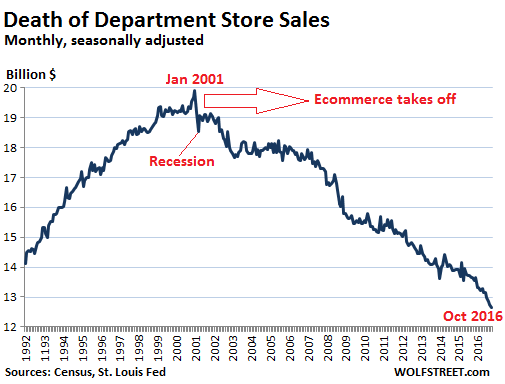

There are still four weeks left to pull out the year. And hopes persists that this year will be decent. But online sales are hot, according to Adobe Digital Index, cited by Reuters. Online shoppers blew $1.15 billion on Thanksgiving Day, between midnight and 5 pm ET, according to Adobe Digital Index, up nearly 14% from a year ago. Sales by ecommerce retailers have been sizzling for years, growing consistently between 14% and 16% year-over-year and eating with voracious appetite the stale lunch of brick-and-mortar stores, particularly department stores. The lunch-eating process began in 2001. The chart below shows monthly department store sales, seasonally adjusted, since 1992. Note the surge in sales in the 1990s, driven by population growth, an improving economy, and inflation (retail sales are mercifully not adjusted for inflation). But sales began to flatten out in 1999. The spike in January 2001 (on a seasonally adjusted basis!) marked the end of the great American department store boom.

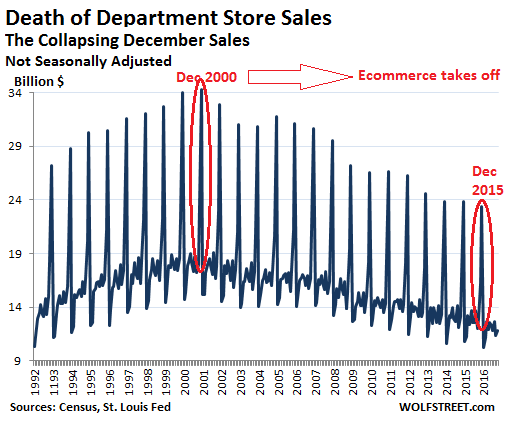

Even as the US fell into a recession in March 2001, ecommerce took off. But department store sales began their long decline, from nearly $20 billion in January 2001 to just $12.7 billion in October 2016, despite 14% population growth and 36% inflation! The decline of department stores is finding no respite during the holiday season. Not-seasonally-adjusted data spikes in October, November, and December. But these spikes have been shrinking, from their peak in December 2000 of $34.3 billion to $23.4 billion in December 2015, a 32% plunge, despite, once again, 14% population growth and 36% inflation!

In other words: the brick-and-mortar operations of department stores are becoming irrelevant. Ecommerce sales include all kinds of merchandise, not just the merchandise available in department stores. So it’s a broader measure. They have skyrocketed from $4.5 billion in Q4 1999 ($1.5 billion a month on average) to $101 billion in Q3 2016 ($33.7 billion a month on average).

Payday lenders asked a federal judge in Washington, D.C., for emergency relief to stop what they called a coordinated effort by U.S. regulators to stop banks from doing business with them, threatening their survival. In Wednesday night filings, the Community Financial Services Association of America (CFSA) and payday lender Advance America, Cash Advance Centers Inc said a preliminary injunction was needed to end the “back-room campaign” of coercion by the Federal Reserve, the Federal Deposit Insurance Corp and the Office of the Comptroller of the Currency. Advance America said its own situation became dire after five banks decided in the last month to cut ties, including a 14-year relationship with U.S. Bancorp, putting it “on the verge” of being unable even to hold a bank account.

Payday lenders make small short-term loans that can help tide over cash-strapped borrowers. But critics say fees can drive effective interest rates well into three digits, and trap borrowers into an endless debt cycle in which they use new payday loans to repay older loans. The CFSA said other payday lenders are also losing banking relationships as a result of “Operation Choke Point,” a 2013 Department of Justice initiative meant to block access to payment systems by companies deemed at greater risk of fraud. “Protecting consumers from credit fraud is, of course, a commendable goal,” Charles Cooper, a lawyer for the CFSA, wrote. “But the manner in which the defendant agencies have chosen to pursue that ostensible goal betrays that their true intent has always been to eradicate a disfavored industry.”

I don’t know to what extent Modi is the psychopath he’s made out to be here, but I do like the decentralization described (fits in with my end of centralization themes). “What a crazy idea it is to have a State monopoly on money..” [..] “In a tribalistic and irrational society, decentralization makes life much safer and makes the market more free, as complex decisions will be taken on the local level, where they belong”

Most people — particularly the salaried middle class – still seem to have a favorable opinion of Mr. Modi. They have been indoctrinated – in India’s extremely irrational and superstitious society – to believe that this demonetization will somehow alleviate corruption and that anything but support of Modi’s actions is anti-national and unpatriotic. This gives me pause to reflect. What a crazy idea it is to have a State monopoly on money, particularly a money that carries no inherent value and depends on regulatory edicts. On a deeper level, it makes me reflect on why for the culture of India – which is tribalistic, nativistic, superstitious and irrational – “India” is actually an unnatural entity. Such a society should consist of hundreds of tribes and countries, which is what “India” was before the British consolidated it.

In a tribalistic and irrational society, decentralization makes life much safer and makes the market more free, as complex decisions will be taken on the local level, where they belong . India’s institutions – not just organizations, but larger socio-political beliefs – have begun to decay and crumble after the British left, losing their underlying essence, the reason for which they had been institutionalized in the first place. This degradation is now picking up pace. They must eventually fall apart – including the nation-state of India – to adjust to the underlying culture. Let us consider some of these institutions. Western education implanted in India has mutated. It is making individuals cogs in a big machine, all for the service of one great leader. Public education and the mass-media have become instruments of propaganda.

Complexity and the diversity of options that technology brings make an irrational thinker extremely confused, forcing him to seek sanity in ritualistic religion —hence the increase in religiosity in India and elsewhere in the region. This has happened despite the explosion in information technology. The concept of the nation-state, when it took hold in Europe, was about the values the emergent rational and enlightened societies of Europe shared and had collectively come to believe in, at least among their elites. In India, the idea of the nation-state has morphed into a valueless thread, which binds people together through nothing but a flag and an anthem, symbols completely devoid of any values. It has collectivized tribalistic and irrational people (an irrationality that is amply epitomized by the negative force Islam has become in the last two decades).

In India and many similarly constituted countries, institutions that are not natural to their culture – the nation state, education, monetary system, etc. must eventually face entropy, slowly at first, and then rapidly. India has now entered the rapid phase. The death of money – amid a lack of respect for property rights (which again are a purely European concept that emerged from the intellectual revolutions of the last 800 years) – has been sudden and will very likely be catastrophic. It is a man-made disaster of gargantuan proportions. It will fundamentally change India in a very negative way, particularly if the demonetization effort succeeds, as it will have created the foundations enabling the rapid emergence of a police state.

In late January of the year 98 AD, after decades of turmoil, instability, inflation, and war, Romans welcomed a prominent solider named Trajan as their new Emperor. Prior to Trajan, Romans had suffered immeasurably, from the madness of Nero to the ruthless autocracy of Domitian, to the chaos of 68-69 AD when, in the span of twelve months, Rome saw four separate emperors. Trajan was welcome relief and was generally considered by his contemporaries to be among the finest emperors in Roman history. Trajan’s successors included Hadrian and Marcus Aurelius, both of whom were also were also reputed as highly effective rulers.

But that was pretty much the end of Rome’s good luck. The Roman Empire’s enlightened rulers may have been able to make some positive changes and delay the inevitable, but they could not prevent it. Rome still had far too many systemic problems. The cost of administering such a vast empire was simply too great. There were so many different layers of governments—imperial, provincial, local—and the upkeep was debilitating. Rome had also installed costly infrastructure and created expensive social welfare programs like the alimenta, which provided free grain to the poor. Not to mention, endless wars had taken their toll on public finances. Romans were no longer fighting conventional enemies like Carthage, and its famed General Hannibal bringing elephants across the Alps.

Instead, Rome’s greatest threat had become the Germanic barbarian tribes, peoples viewed as violent and uncivilized who would stop at nothing to destroy Roman way of life. Corruption and destructive bureaucracy were increasingly rampant. And the worse imperial finances became, the more the government tried to “fix” everything by passing debilitating regulation and debasing the currency. In his seminal work The History of the Decline and Fall of the Roman Empire, Edward Gibbon wrote: “The story of its ruin is simple and obvious; and instead of inquiring why the Roman empire was destroyed, we should rather be surprised that it had subsisted so long.”

Progress as a blind faith. “Critics wondered if Nixon was wise to point to modern appliances such as blenders and dishwashers as the emblems of American superiority.”

Innovation is a dominant ideology of our era, embraced in America by Silicon Valley, Wall Street, and the Washington DC political elite. As the pursuit of innovation has inspired technologists and capitalists, it has also provoked critics who suspect that the peddlers of innovation radically overvalue innovation. What happens after innovation, they argue, is more important. Maintenance and repair, the building of infrastructures, the mundane labour that goes into sustaining functioning and efficient infrastructures, simply has more impact on people’s daily lives than the vast majority of technological innovations. The fates of nations on opposing sides of the Iron Curtain illustrate good reasons that led to the rise of innovation as a buzzword and organising concept.

Over the course of the 20th century, open societies that celebrated diversity, novelty, and progress performed better than closed societies that defended uniformity and order. In the late 1960s in the face of the Vietnam War, environmental degradation, the Kennedy and King assassinations, and other social and technological disappointments, it grew more difficult for many to have faith in moral and social progress. To take the place of progress, ‘innovation’, a smaller, and morally neutral, concept arose. Innovation provided a way to celebrate the accomplishments of a high-tech age without expecting too much from them in the way of moral and social improvement.

Before the dreams of the New Left had been dashed by massacres at My Lai and Altamont, economists had already turned to technology to explain the economic growth and high standards of living in capitalist democracies. Beginning in the late 1950s, the prominent economists Robert Solow and Kenneth Arrow found that traditional explanations – changes in education and capital, for example – could not account for significant portions of growth. They hypothesised that technological change was the hidden X factor. Their finding fit hand-in-glove with all of the technical marvels that had come out of the Second World War, the Cold War, the post-Sputnik craze for science and technology, and the post-war vision of a material abundance.

Robert Gordon’s important new book, The Rise and Fall of American Growth, offers the most comprehensive history of this golden age in the US economy. As Gordon explains, between 1870 and 1940, the United States experienced an unprecedented – and probably unrepeatable – period of economic growth. That century saw a host of new technologies and new industries produced, including the electrical, chemical, telephone, automobile, radio, television, petroleum, gas and electronics. Demand for a wealth of new home equipment and kitchen appliances, that typically made life easier and more bearable, drove the growth. After the Second World War, Americans treated new consumer technologies as proxies for societal progress – most famously, in the ‘Kitchen Debate’ of 1959 between the US vice-president Richard Nixon and the Soviet premier Nikita Kruschev. Critics wondered if Nixon was wise to point to modern appliances such as blenders and dishwashers as the emblems of American superiority.

The federal government has announced it will make it easier for foreigners to buy new apartments amid concerns of a looming glut that will drive down prices. Treasurer Scott Morrison said the government will make changes to the foreign investment framework to allow foreign buyers to buy an off-the-plan dwelling that another foreign buyer has failed to settle as a new dwelling. Previously, on-sale of a purchased off the plan apartment was regarded as a second hand sale, which is not open to foreign buyers. Foreign buyers can only buy new dwellings. The move effectively opens up the pool of buyers who can soak a potential flood of apartments hitting the residential markets due to failed settlements.

“This change addresses industry concerns, and means property developers won’t be left in the lurch when a foreign buyer pulls out of an off-the-plan purchase,” Mr Morrison said in an announcement. “It is common sense that an apartment or house that has just been built, or is still under construction and for which the title has never changed hands, is not considered an established dwelling.” The policy change comes after Mirvac said it experienced a rise in the default rate for the settlement of off-the-plan residential sales, above its historic average of 1%. The changes will apply immediately and regulation change will be made soon to enable developers to acquire “New Dwelling Exemption Certificates” for foreign buyers of these recycled off-the-plan homes.

On top of defaults, the Australian apartment markets – which boomed in the last four years – are facing other fresh risks. On Friday, HSBC said an oversupply of apartments in Melbourne and Brisbane could send unit prices down by as much as 6% in 2017. The apartment building boom, an ongoing concern for the Reserve Bank of Australia, especially in inner city Melbourne is likely to “start showing through” in price drops of between 2% and 6% in that city next year, HSBC chief economist Paul Bloxham said in a note. It’s a similar story in Brisbane where apartment prices are forecast to fall by as much as 4%. “A national apartment building boom, which has been part of the rebalancing act, is likely to deliver some oversupply in the Melbourne and Brisbane apartment markets, which is expected to see apartment price falls in these markets,” Mr Bloxham said.

The Clinton Foundation has a rocky past. It was described as “a slush fund”, is still at the centre of an FBI investigation and was revealed to have spent more than $50 million on travel. Despite that, the official website for the charity shows contributions from both AUSAID and the Commonwealth of Australia, each worth between $10 million and $25 million. News.com.au approached the Department of Foreign Affairs and Trade for comment about how much was donated and why the Clinton Foundation was chosen as a recipient. A DFAT spokeswoman said all funding is used “solely for agreed development projects” and Clinton charities have “a proven track record” in helping developing countries. Australia jumping ship is part of a post-US election trend away from the former Secretary of State and presidential candidate’s fundraising ventures.

Norway, one of the Clinton Foundation’s most prolific donors, is reducing its contribution from $20 million annually to almost a quarter of that, Observer reported. One reason for the drop-off could be increased scrutiny on international donors. The International Business Times reported in 2015 on curious links between donors and State Department approval. IBT wrote that the State Department approved massive commercial arms sales for countries which had donated to the Clinton charity. More than $165 billion worth of arms sales were approved by the State Department to 20 nations whose governments gave money to the Clinton Foundation, data shows. The countries buying weapons from the US were the same countries previously condemned for human rights abuses. They included Algeria, Saudi Arabia and Kuwait.

But what does Australia gain from topping up the Clinton coffers? The Australian reported in February that Australia was “the single biggest foreign government source of funds for the Clinton Foundation” but questions remain unanswered about the agreement between the two parties. “It’s not clear why Canberra had to go through an American foundation to deliver aid to Asian countries (including Indonesia, Papua New Guinea and Vietnam). There is now every chance the payments will become embroiled in presidential politics.” The Daily Telegraph wrote in October that “Lo and behold, (Julia Gillard) became chairman (of the Clinton-affiliated Global Partnership for Education) in 2014”, one year after being defeated in a leadership ballot by Kevin Rudd.

“After contributing $88mm to the Clinton Foundation over the past 10 years, making them one of the Foundation’s largest contributors, Australia has decided to pull all future donations.

But why would they stop funding now that Hillary has so much more free time to focus on her charity work?”

For months we’ve been told that the Clinton Foundation, and it’s various subsidiaries, were simple, innocent “charitable” organizations, despite the mountain of WikiLeaks evidence suggesting rampant pay-to-play scandals surrounding a uranium deal with Russia and earthquake recovery efforts in Haiti, among others. Well, if that is, in fact, true perhaps the Clintons could explain why wealthy foreign governments, like Australia and Norway, are suddenly slashing their contributions just as Hillary’s schedule has been freed up to focus exclusively on her charity work. Surely, these foreign governments weren’t just contributing to the Clinton Foundation in hopes of currying favor with the future President of the United States, were they? Can’t be, only an useless, “alt-right,” Putin-progranda-pushing, fake news source could possibly draw such a conclusion.

Alas, no matter the cause, according to news.com.au, the fact is that after contributing $88mm to the Clinton Foundation, and its various affiliates, over the past 10 years the country of Australia has decided to cease future donations to the foundation just weeks after Hillary’s stunning loss on November 4th. And just like that, 2 out of the 3 largest foreign contributors to the Clinton Foundation are gone with Saudia Arabia being the last remaining $10-$25mm donor that hasn’t explicitly cut ties or massively scaled by contributions. [..]

News.com.au confirmed Australia’s decision to cut future donations to the Clinton Foundation earlier today. When asked why donations were being cut off now, a Department of Foreign Affairs and Trade official simply said that the Clinton Foundation has “a proven track record” in helping developing countries. While that sounds nice, doesn’t it seem counterintuitive that these countries would pull their funding just as Hillary has been freed up to spend 100% of her time helping people in developing countries?

“Australia has finally ceased pouring millions of dollars into accounts linked to Hillary Clinton’s charities. Which begs the question: Why were we donating to them in the first place? The federal government confirmed to news.com.au it has not renewed any of its partnerships with the scandal-plagued Clinton Foundation, effectively ending 10 years of taxpayer-funded contributions worth more than $88 million. News.com.au approached the Department of Foreign Affairs and Trade for comment about how much was donated and why the Clinton Foundation was chosen as a recipient. A DFAT spokeswoman said all funding is used “solely for agreed development projects” and Clinton charities have “a proven track record” in helping developing countries.”

A group of distinguished former newspaper editors has launched a scathing attack on plans for New Zealand’s largest print media companies to merge, calling it a threat to democracy which could see a concentration of power exceeded “only in China”. The merger of NZME and Fairfax Media, which was proposed in May, would not be healthy in a country that “already suffers from a dearth of serious content and analysis”, the editors say in a submission to the commerce commission. The group, which includes Suzanne Chetwin, former Dominion chief Richard Long and ex-New Zealand Herald editor Gavin Ellis, also criticise the trend towards “click-bait stories” at a time when television has “all but abandoned current affairs and our public discourse is increasingly glib”.

“The merger would see one organisation controlling nearly 90% of the country’s print media market (and associated websites), the greatest level of concentration in the OECD and one that is exceeded only by China. “That cannot be healthy, particularly in a society like New Zealand’s that has so few checks and balances in its constitutional arrangements.” The submission went on to state the greatest threat to New Zealand media came from off-shore publishers who had “no feel for New Zealand’s social fabric”, and urged the commerce commission to decline the merger. The merger was sold as an attempt by both companies to stem revenue losses and drastic staff and budget cuts, particularly to rural and regional newsrooms.

Dunedin’s The Otago Daily Times would be the only newspaper in the country to remain independent, although it too could be affected as they have content sharing agreements with NZME’s The New Zealand Herald. Radio stations and magazines owned by both companies would also be affected.

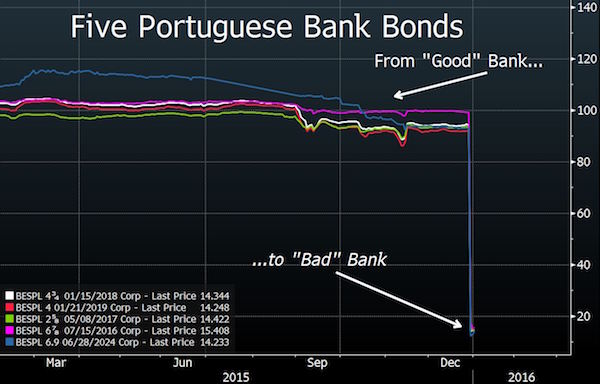

Greece’s battered banks are being asked to swap about 33 billion ($35 billion) euros in floating-rate bonds for 30-year, fixed-rate securities under a euro-area plan to shield Athens from future interest rate increases, three people with knowledge of the matter said. The swap is part of a package of debt-relief proposals for Greece to be presented at a Dec. 5 meeting of euro-area finance ministers, according to the people, who asked not to be named because they weren’t authorized to speak publicly about the matter. The notes were issued by the European Financial Stability Facility, the region’s crisis-fighting fund, to re-capitalize Greek lenders in 2013.

While the current EFSF holdings of Greek banks fall due between 2034 and 2046, the fixed-rate notes will expire in 2047, the people said. That will reduce Greece’s interest rate risk, but it may come at a cost for its four systemically important lenders, which could be left with securities that are more difficult to trade. The technical aspects of the operation are still being hashed out. “There are discussions going on as to proposals which will improve the sustainability of the Greek debt,” Piraeus Bank Chairman George Handjinicolaou said in an interview Thursday. “Part of this proposal is a change in the EFSF bonds for something else, some form of fixed-rate debt, which would improve the predictability of the sustainability of the Greek debt profile.”

Shvets says the world should have actually delevered or paid down the debt to return initiative to the private sector, but thinks people could not accept the levels of pain associated with it. “You could eliminate the impact of the overcapacity through deflation. Nobody is prepared to accept that we might have to wipe out decades of growth just to eliminate leverage. Banks go, there are defaults, bankruptcies, layoffs,” he said. He thinks the Biblical debt jubilee, where slaves would be freed and debt would be forgiven every 50 years is a nice idea that would also work today if it weren’t for entrenched special interests. “The debt is not spread evenly, we still live in a tribal world, and it’s easier to start a war than to forgive debt,” Shvets said.

Global central banks with their easy money policies of negative interest rates and quantitative easing are working against a debt deflation scenario, with limited success, according to Shvets. “That was the entire idea of aggressive monetary policies: Stimulate investment and consumption. None of that works, there is no evidence. It can impact asset prices, but they don’t flow into the real economy,” he said. “Remember, the people at the Fed and the Bank of England are not supermen, they are people with an above average IQ trying to do a very difficult job in a highly complex environment.” Both overleveraging, easy money policies, and technological shifts are responsible for increasing levels of income inequality across the globe, another hallmark of the previous two industrial revolutions. Fewer people control more of the wealth.

The Federal Reserve signals a reluctance to raise interest rates. The yen strengthens to 90 per dollar. Haruhiko Kuroda decides to act. Helicopter money is coming, says Mark Mobius, even as soon as next month. The 80-year-old investment veteran is outlining how he expects central banks to respond to sluggish economic growth. For Mobius, executive chairman of Templeton Emerging Markets Group, traditional easing measures have just made people save instead of spend or borrow. Combined with a stronger yen, he says that’s going to force the Bank of Japan governor to contemplate a policy he’s repeatedly ruled out. “They’re really beginning to think what ammunition they have,” he said in an interview on a visit to a typhoon-struck Tokyo this week.

“The first reaction is to say, OK, let’s go for helicopter money, let’s get money directly into the hands of consumers,” he said. “I think that would probably be the next step.” Central bankers have flooded their economies with monetary stimulus in the eight years since the global financial crisis, driving up asset prices – including the stock markets that Mobius invests in – while struggling to kickstart global growth. A foray into negative interest rates in Japan has been met with the yen surging to about 100 per dollar, falling stocks and dwindling bank profits.

While markets wait for Janet Yellen’s latest message about the direction of monetary policy, the Federal Reserve chief and her colleagues already have one for politicians: the U.S. economy needs more public spending to shift into higher gear. In the past few weeks, Yellen and three of the Fed’s other four Washington-based governors have called in speeches and Congressional hearings for government infrastructure spending and other efforts to counter weak growth, sagging productivity improvements, and lagging business investment. The fifth member has supported the idea in the past. The Fed has no direct influence over fiscal policy and its officials traditionally refrain from discussing it in detail.

Having its top officials – from Yellen to former investment banker and Bush administration official Jerome Powell – speak in one voice sends a strong signal to the next president and Congress about the limits they face in setting monetary policy and what is needed to improve the economy’s prospects. The Fed’s annual conference in Jackson Hole, Wyoming, where Yellen speaks on Friday, is due to focus on how to improve central banks’ “toolkit,” but the unanimous message from the Fed’s top policymakers is that those tools are not enough. “Monetary policy is not well equipped to address long-term issues like the slowdown in productivity growth,” Fed vice chair Stanley Fischer said on Sunday. He said it was up to the administration to invest more in infrastructure and education.

Behind Fischer’s statement lies a troubling feature of the recovery – business investment has fallen below levels in prior years and companies seem to have stopped responding to low borrowing costs. As a share of GDP, U.S. annual business investment since 2008 has averaged nearly a full percentage point below the previous decade’s average, government data shows. Reuters calculations indicate the investment shortfall has blown a hole in annual GDP that has grown to as much as one trillion dollars a year compared with what it would have been if the previous trend continued.

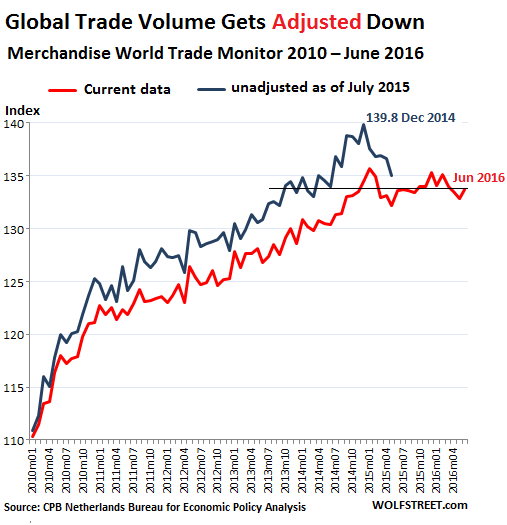

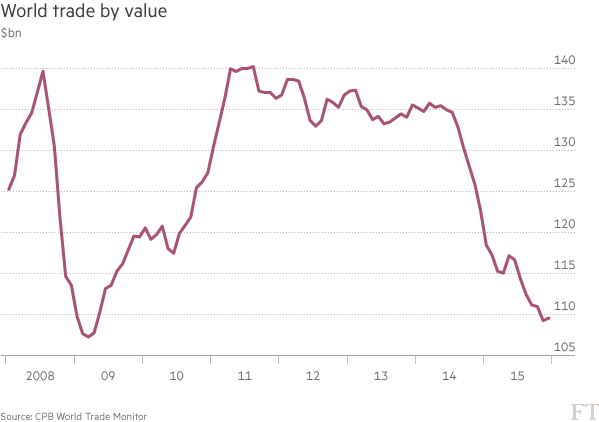

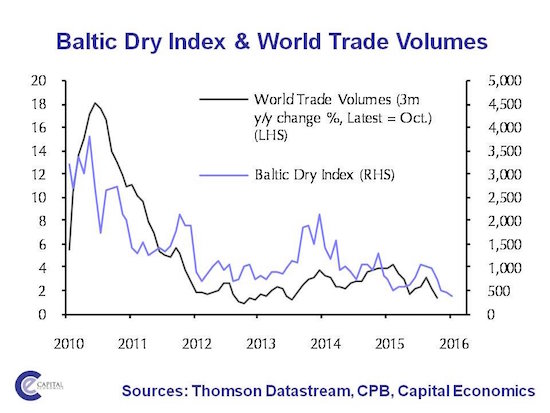

Adding to the picture of crummy demand for goods around the world, the CPB Netherlands Bureau for Economic Policy Analysis, a division of the Ministry of Economic Affairs, just released its preliminary data of its Merchandise World Trade Monitor for June. Trade volumes rose 0.7% in June from May, after falling 0.5% in May, but were about flat year-over-year, and below the volumes of December 2014! On a quarterly basis – it averages out the monthly ups and downs – world trade fell 0.8%, contracting for the second quarter in a row. The CPB recently adjusted its world trade data down, going back many years.

The new data now depicts a post-Financial Crisis recovery of global trade that was a lot weaker than the original data had indicated. These downward adjustments of 2% to 3% came in a world where economic growth, according to the IMF, is stuck at 3.1% in 2016. This chart of the CPB’s World Trade Monitor index shows the old data released as of July 2015 (blue line) and the newly adjusted data released today (red line). Note the 4.4% drop from the peak in global trade volumes in the original data for December 2014 and in the current data for June 2016!

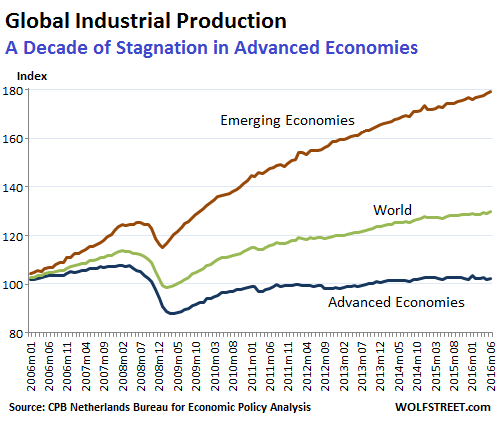

World trade is a reflection of the goods-producing economy. Services don’t get shipped around the world. Goods do. So industrial production, excluding construction, is key. And here the trend is awful for advanced economies. Global industrial production, excluding construction, rose 0.6% in June, after a 0.3% decline in May. The index for industrial production in advanced economies rose to 102.5, below where it had been in January (103.4), a level it had hit after the Financial Crisis in December 2012, but down from the glory days before the Financial Crisis when the index peaked in February 2008 (107.8). And here’s a tidbit: the first time that the index hit the current level had been in April 2006. A full decade of stagnation.

Industrial production has shifted to emerging economies (“cheap labor” economies) for many years, such as China, as companies in the US, decades ago, and eventually in Europe and Japan began outsourcing and offshoring production to emerging economies. Hence, industrial production in emerging economies has surged over this period. This was particularly the case after the Financial Crisis when companies in the US, Europe, and Japan redoubled their efforts to get production relocated offshore. This chart shows the CPB’s industrial production index globally (green line), and also separated by advanced economies (the dismally flat-ish blue line at the bottom) and emerging economies (brown line at the top):

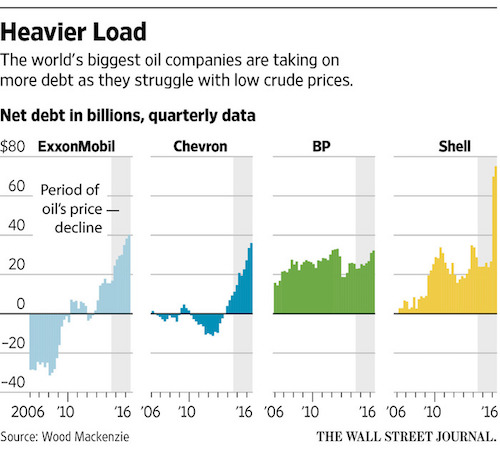

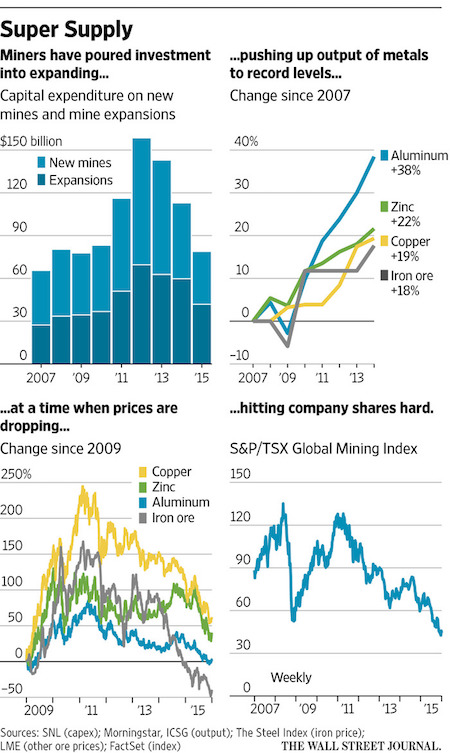

Some of the world’s largest energy companies are saddled with their highest debt levels ever as they struggle with low crude prices, raising worries about their ability to pay dividends and find new barrels. Exxon Mobil, Shell, BP and Chevron hold a combined net debt of $184 billion—more than double their debt levels in 2014, when oil prices began a steep descent that eventually bottomed out at $27 a barrel earlier this year. Crude prices have rebounded since, but still hover near $50 a barrel. The soaring debt levels are a fresh reminder of the toll the two-year price slump has taken on the oil industry. Just a decade ago, these four companies were hauled before Congress to explain “windfall profits” but now can’t cover expenses with normal cash flow.

Executives at BP, Shell, Exxon and Chevron have assured investors that they will generate enough cash in 2017 to pay for new investments and dividends, but some shareholders are skeptical. In the first half of 2015, the companies fell short of that goal by $40 billion, according to a Wall Street Journal analysis of their numbers. “Eventually something will give,” said Michael Hulme, manager of the $550 million Carmignac Commodities Fund, which holds stakes in Shell and Exxon. “These companies won’t be able to maintain the current dividends at $50 to $60 oil—it’s unsustainable.” BP has said it expects to be able to pay for its operations, make new investments and meet its dividend at an oil price of between $50 and $55 a barrel next year.

The debt is piling up despite cuts of billions of dollars on new projects and current operations. Repaying the loans could weigh the companies down for years, crimping their ability to make investments elsewhere and keep pumping ever more oil and gas. “They are just not spending enough to boost production,” said Jonathan Waghorn at Guinness Atkinson Asset Management.

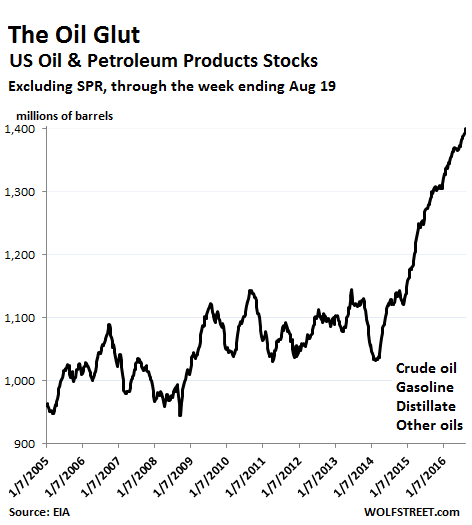

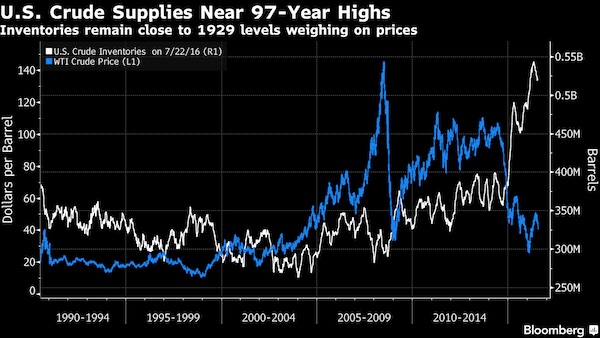

Soothsayers out there have been prophesying time and again, for over a year, that very soon, in fact next week, the supply glut will start to unwind; that production in the US is already coming down sharply, that demand is up, or whatever…. In the end, a glut comes down to whether inventories are rising, particularly during a time of the year when they’re supposed to be falling (glut gets worse), or whether they’re falling (glut stabilizes or abates). It’s not just crude oil, but also the products that crude oil gets refined into for eventual use. And these stocks of petroleum products have been a doozie, particularly gasoline.

Gasoline stocks were essentially unchanged for the week, at 232.7 million barrels, a record for this time of the year, and up 8.5% from the already elevated inventory levels last year. Distillate fuels rose by 200,000 barrels to 153.3 million barrels. And “all other oils” jumped by a total of 3.9 million barrels to 490.6 million barrels. So total petroleum products stocks rose by 6.6 million barrels during the week, or 0.5%. Once again, this small-ish number, but over the period of the oil bust, total petroleum products stocks have soared by 30% and now exceed for the first time ever another huge milestone: 1.4 billion barrels. This chart shows what a truly relentless glut looks like:

Scotland’s revenues from North Sea oil have collapsed by 97% in the past year as oil prices have plummeted, reigniting a fierce debate over whether an independent Scotland could finance itself. Scottish Liberal Democrat leader Willie Rennie said: “The nationalists’ case for independence has been swallowed up by a £14bn black hole.” Taxes collected from oil production fell from £1.8bn in 2015 to just £60m in 2016. The gap between tax revenues and what Scotland spends is now 9.5%, or £14.8bn, compared to a 4% deficit for the UK as a whole. Scotland’s public sector now spends £12,800 per person, but collects just £10,000 each, the figures reveal. In 2008-9, as oil peaked at almost $150 per barrel, the Scottish government brought in a record £11.6bn from North Sea fields.

Russian markets are red hot again. Two years after plunging oil prices and Western economic sanctions fueled an investor exodus, the Micex stock index on Tuesday hit an all-time high. It is up 25% this year in dollar terms, making Russia the sixth-best performer among 23 emerging countries tracked by MSCI Inc. The ruble has gained 13% against the dollar this year, ranking third among all emerging currencies. Russia’s local-currency bonds rank third this year in performance out of 15 countries tracked by JP Morgan Chase. Many investors credit central-bank chief Elvira Nabiullina for Russia’s resurgence. They cite her surprise decision to end the ruble’s peg to the dollar in November 2014 and then sharply raise interest rates to combat capital flight and knock down inflation.

The moves were painful for Russia’s economy, which went into a sharp recession as the value of the ruble slumped, reducing consumer and business purchasing power. But over time they have helped to restore some international-investor faith in a country still shadowed by its 1998 default. “The correct steps taken by the Russian central bank have restored confidence in the ruble and its macroeconomic policy,” said Andrey Kutuzov, an associate portfolio manager of the Wasatch Emerging Markets Small Cap fund. Global investors this year have added $1.3 billion to funds that invest in Russian bonds and stocks, according to EPFR Global. The share of foreigners among government bondholders rose to 24.5% as of June 1, its highest level since late 2012, according to the Russian central bank.

China imposed limits on lending by peer-to-peer platforms to individuals and companies in an effort to curb risks in one part of the loosely-regulated shadow-banking sector. An individual can borrow as much as 1 million yuan ($150,000) from P2P sites, including a maximum of 200,000 yuan from any one site, the China Banking Regulatory Commission said in Beijing on Wednesday. Corporate borrowers are capped at five times those levels. Tighter regulation may encourage consolidation that aids the industry long-term, said Wei Hou at Sanford C. Bernstein in Hong Kong. China’s authorities are concerned about defaults and fraud among the nation’s 2,349 online lenders. In December, the country’s biggest Ponzi scheme was exposed after Internet lender Ezubo allegedly defrauded more than 900,000 people out of the equivalent of $7.6 billion.

The nation has 1778 “problematic” online lenders, according to the CBRC. The P2P lenders are barred from taking public deposits or selling wealth-management products and must appoint qualified banks as custodians and improve information disclosure, the regulator said. [..] China’s P2P industry brokered 982 billion yuan of loans in 2015, almost quadruple the amount in 2014 and an approximately 10-fold increase from 2013, according to Yingcan. P2P firms attracted more than 3.4 million investors and 1.15 million borrowers in July, with loans extended at an average interest rate of 10.3%, according to Yingcan. Products offered by P2P platforms in China can include anything from loans for weddings, guaranteed against the cash gifts that couples expect to receive, to high-yield lending for risky property or mining projects.

Wanted posters for fugitive debtors, not commercials, are the main images that flash up on a big electronic screen in downtown Yixing, in the heart of the faltering Chinese industrial powerhouse that is the Yangtze River Delta. The posters, from the local courts, show the identity card numbers and pictures of dozens of people who have fled unpaid debts. Rewards ranging from 20,000 yuan (HK$23,000) to 330,000 yuan are offered to anyone reporting their whereabouts. But Hengsheng Square is the glitziest part of Yixing – with the most luxury stores, the brightest lights and the priciest office buildings – and few passers-by, their attention directed elsewhere, heed the wanted posters. They have little novelty value in any case, with the “runaway debtor” phenomenon now just part of daily life in the small city as economic growth slows.

In many ways, the square stands as a metaphor for the overall health of the Chinese economy. Under a prosperous surface, deep cracks have begun to emerge in its investment-led model, casting a shadow over the country’s economic growth prospects and even giving rise to doubts about the fundamental soundness of the world’s second-biggest economy. “The economic dynamics are waning,” said Professor Hu Xingdou, an economist at Beijing Institute of Technology. “China’s economic growth in recent years was powered by massive money printing, which is dangerous and unsustainable.”

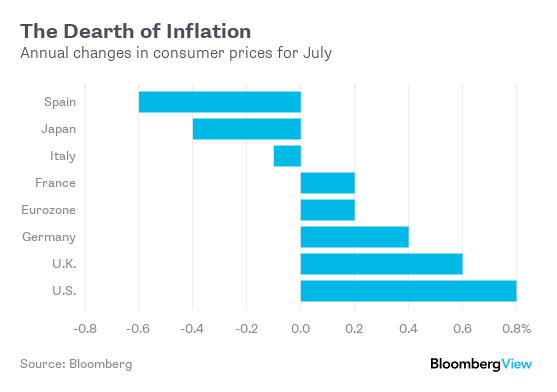

Jacob Rothschild, the billionaire scion of arguably Europe’s greatest banking dynasty says we’re living through “the greatest experiment in monetary policy in the history of the world.” There’s a major flaw in the experiment, though: the real world isn’t responding to policy in the way that the textbooks say it should. Moreover, it seems increasingly evident that the fears that led to zero interest rates and quantitative easing were at best overblown, if not entirely unjustified. The economic quandary is easy to parse. Central banks almost everywhere have sanctioned a 2% inflation target as signifying financial Nirvana. But, as the table below shows, consumer prices in the world’s major economies are rising much slower than that arbitrary ideal:

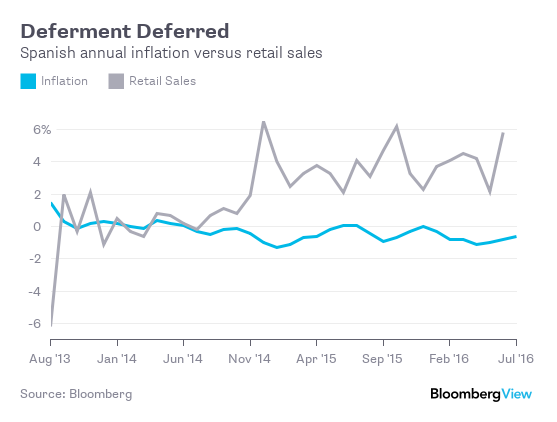

Spain has emerged as the poster child for deflation. Prices fell by 0.6% in July, the country’s 12th consecutive month with no increase in inflation. The textbooks suggest that when there’s a prolonged period of falling prices – the definition of deflation – the economy can quickly find itself in a tailspin. Businesses and consumers will defer purchases in the expectation that goods and services will be even cheaper in the future. So if Spain has had an average inflation rate of -0.4% since the end of 2013, and has seen lower prices in 23 of the past 30 months, consumers will have responded by shunning the shops and curtailing their spending, right? Wrong:

International credit rating agency S&P Global Ratings has warned of the increasing risks facing New Zealand banks as a result of the continuing rise in house prices. In a new report, S&P has downgraded its Banking Industry Country Risk Assessment (BICRA) for NZ’s banks by a notch, dropping it from 3 to 4, on a scale where 1 is the lowest risk and 10 is the highest risk. However it has not changed the individual credit ratings of any New Zealand banks. [..] .. our ratings on all the financial institutions operating in New Zealand remain unchanged. “This reflects our expectation that despite some weakening in the capital levels of all these financial institutions, their stand alone credit profiles (SACPs) would remain unchanged.

However S&P did downgrade the SACPs of ASB and Rabobank by one notch each, although it did not downgrade the two banks’ credit ratings, “… reflecting our assessment of timely financial support from their respective parents, if needed,” S&P said. S&P said the increased risks to this country’s banking sector had been driven by “…continued strong growth in residential property prices nationally, coupled with an increase in private sector credit growth.” “We believe the risk of a sharp correction in property prices has further increased and, if it were to occur – with about 56% of registered banks’ lending assets secured by residential home loans – the impact on financial institutions would be amplified by the New Zealand economy’s external weaknesses, in particular its persistent current account deficit and high level of external debt.”

There’s a giant pot of corporate gold sitting outside the United States, and the U.S. Treasury and the European Commission are squabbling over how to get their hands on it. American multinational corporations have stashed more than $2 trillion in profits and assets outside to avoid paying what many companies argue are unduly high U.S. corporate tax rates. Over the past few years, the European Commission has opened investigations into a handful of those companies, including Apple, Starbucks and Amazon, to determine whether they owe taxes to European countries. But the Treasury Department, in a “white paper” released Wednesday, said those investigations have gone too far.

The paper attacked the legal approach the EU is using to determine tax liabilities on American companies, saying it targets “income that (European) Member States have no right to tax under well-established international tax standards.” The paper also argued that taxes collected by European countries could, in effect, come right out of the pockets of American taxpayers. That’s because taxes collected by European countries could be deducted from any future payments to the Treasury. “That outcome is deeply troubling, as it would effectively constitute a transfer of revenue to the EU from the U.S. government and its taxpayers,” the paper said. The report urged the European Commission to “return to the system and practice of international tax cooperation that has long fostered cross-border investment between the United States and EU Member States.”

The drama of Brexit may soon be matched or eclipsed by crystallizing events in France, where the Long Slump is at last taking its political toll. A democracy can endure deflation policies for only so long. The attrition has wasted the French centre-right and the centre-left by turns, and now threatens the Fifth Republic itself. The maturing crisis has echoes of 1936, when the French people tired of ‘deflation decrees’ and turned to the once unthinkable Front Populaire, smashing what remained of the Gold Standard. Former Gaulliste president Nicolas Sarkozy has caught the headlines this week, launching a come-back bid with a package of hard-Right policies unseen in a western European democracy in modern times.

But the uproar on the Left is just as revealing. Arnaud Montebourg, the enfant terrible of the Socialist movement, has launched his own bid for the Socialist Party with a critique of such ferocity that it bears examination. The former economy minister says France voted for a left-wing French manifesto four years ago and ended up with a “right-wing German policy regime”. This is objectively true. The vote was meaningless. “I believe that we have reached the end of road for the EU, and that France no longer has any interest in it. The EU has left us mired in crisis long after the rest of the world has moved on,” he said. Mr Montebourg stops short of ‘Frexit’ but calls for the unilateral suspension of EU labour laws. “As far as I am concerned, the current treaties have elapsed.

I will be inspired by the General de Gaulle’s policy of the ’empty chair’, a strike against the EU. I am not in favour of a French Brexit, but we can longer accept a Europe like that,” he said. In other words, he wishes to leave from within – as Poland, and Hungary are doing – without actually triggering any legal or technical clause. Mr Montebourg is unlikely to progress far but his indictment of president François Hollande is devastating. The party leadership was warned repeatedly and emphatically that contractionary policies would inevitably lead to another million jobless but the economic was swept aside. “They never budged from their Catechism and their false certitudes,” he said.

The tweet was sent by Germany’s ministry for migration and refugees a year ago today. “The #Dublin procedure for Syrian citizens is at this point in time effectively no longer being adhered to,” the message read. With 175 retweets and 165 likes, it doesn’t look like classic viral content. But in Germany it is being spoken of as the first post on social media to change the course of European history. Referring to an EU law determined at a convention in Dublin in 1990, the tweet was widely interpreted as a de facto suspension of the rule that the country in Europe where a refugee first arrives is responsible for handling his or her asylum application.

By this point in 2015, more than 300,000 asylum seekers had reached Europe by boat – a figure that was already 50% higher than even the record-breaking number of arrivals in 2014. Although the German ministry’s intervention certainly did not start the crisis, it did make Germany the first-choice destination for Syrians who previously might have aimed for other countries in Europe, such as Sweden, which at the time offered indefinite asylum to Syrians. It also created an impression of confusion and loss of political control, from which Angela Merkel’s government has at times struggled to recover. Twelve months on, politicians and officials at the centre of Berlin’s bureaucratic machine are still trying to figure out how the tweet came about.

Four days previously, Angelika Wenzl, the executive senior government official at the refugee ministry, which in Germany is known as BAMF, had emailed out an internal memo titled “Rules for the suspension of the Dublin convention for Syrian citizens” to its 36 field bureaux around the country, stating that Syrians who applied for asylum in Germany would no longer be sent back to the country where they had first stepped on European soil. [..] By channels that officials and journalists have so far failed to pinpoint, Wenzl’s internal memo was leaked to the press.

When Charles Dickens, the English novelist, was detailing the “soft black drizzle” of pollution over London, he might inadvertently have been chronicling the early signs of global warming. New research led by Australian scientists has pegged back the timing of when humans had clearly begun to change the climate to the 1830s. An international research project has found human-induced climate change is first detectable in the Arctic and tropical oceans around the 1830s, earlier than expected. That’s about half a century before the first comprehensive instrumental records began – and about the time Dickens began his novels depicting Victorian Britain’s rush to industrialise.

The findings, published on Thursday in the journal Nature, were based on natural records of climate variation in the world’s oceans and continents, including those found in corals, ice cores, tree rings and the changing chemistry of stalagmites in caves. Helen McGregor, an ARC future fellow at the University of Wollongong and one of the paper’s lead authors, said it was “quite a surprise” the international research teams of dozens of scientists had been able to detect a signal of climate change emerging in the tropical oceans and the Arctic from the 1830s. “Nailing down the timing in different regions was something we hadn’t expected to be able to do,” Dr McGregor told Fairfax Media.

Interestingly, the change comes sooner to northern climes, with regions such as Australasia not experiencing a clear warming signal until the early 1900s. Nerilie Abram, another of the lead authors and an associate professor at the Australian National University’s Research School of Earth Sciences, said greenhouse gas levels rose from about 280 parts per million in the 1830s to about 295 ppm by the end of that century. They now exceed 400 ppm.

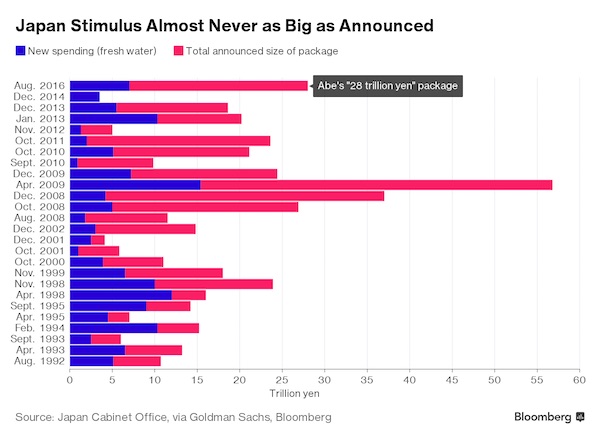

Prime Minister Shinzo Abe’s “bold” plan to revive the economy with a $273 billion package leaves him traveling down a well-trod path: it marks the 26th dose of fiscal stimulus since the country’s epic markets crash in 1990, in a warning for its effectiveness. The nation has had extra budgets every year since at least 1993, and even with that extra spending, it has still had six recessions, an entrenched period of deflation, soaring debt and a rapidly aging population that has left the world’s third-largest economy still struggling to get off the floor. While some analysts say the latest round of spending may buy the economy time, few are convinced it will be enough to dramatically change the course.

First off, much of the 28 trillion yen announced by Abe last week won’t be spending, but lending. And if previous episodes are any guide, an initial sugar hit to markets and growth will quickly fade amid a realization that extra spending does little to cure the economy’s underlying problems. A Goldman Sachs study found that markets gave up their gains in the first month after the cabinet approved the stimulus in 18 of the 25 packages it studied since 1990. Skeptics of Abe’s latest plan aren’t hard to find. Instead of adding to a debt pile already more than twice the economy’s size, more should be done to tackle thorny structural problems such as a declining labor force and protected industries, according to Naoyuki Shinohara, a former Japanese finance ministry official.

“Looking at the history of the Japanese economy, there have been lots of fiscal stimulus packages,” according to Shinohara, who was a top official at the IMF until last year. “But the end result is that it didn’t have much impact on the potential growth rate.”

Activity in China’s manufacturing sector eased unexpectedly in July as orders cooled and flooding disrupted business, an official survey showed, adding to fears the economy will slow in coming months unless the government steps up a huge spending spree. While a similar private survey showed business picked up for the first time in 17 months, the increase was only slight and the much larger official survey on Monday suggested China’s overall industrial activity remains sluggish at best. Both surveys showed persistently weak demand at home and abroad were forcing companies to continue to shed jobs, even as Beijing vows to shut more industrial overcapacity that could lead to larger layoffs.

And other readings on Monday pointed to signs of cooling in both the construction industry and real estate, which were key drivers behind better-than-expected economic growth in the second quarter. The official Purchasing Managers’ Index (PMI) eased to 49.9 in July from the previous month’s 50.0 and below the 50-point mark that separates growth from contraction on a monthly basis. While the July reading showed only a slight loss of momentum, Nomura’s chief China economist Yang Zhao said it may be a sign that the impact of stimulus measures earlier this year may already be wearing off. That has created a dilemma for Beijing as the Communist Party seeks to deliver on official targets, even as concerns grow about the risks of prolonged, debt-fueled stimulus.

“The government has realized the downward pressure is great but they’ve also realized that stimulus to stimulate the economy continuously is not a good idea and they want to continue to focus on reform and deleveraging,” Zhao said.