Marion Post Wolcott Negro woman carrying laundry between Durham and Mebane, NC 1939

Absolute must read. And then a second time.

• The Committee To Destroy The World (Michael Lewitt)

Last month, the world mourned the death of beloved actor Leonard Nimoy. Mr. Nimoy, of course, was renowned for his portrayal of the iconic character Mr. Spock on the 1960s television series Star Trek. One of the most memorable Star Trek inventions was the transporter that allowed human beings to be beamed through space and time like light and energy. Investors expecting central bankers to solve the world’s economic problems might as well believe that Janet Yellen is capable of beaming them straight into the Marriner S. Eccles Building in Washington, D.C. Their failure to acknowledge that the Fed is failing to generate sustainable economic growth while contributing to income inequality and crushing debt burdens is inexplicable.

Central banks that purport to be promoting financial stability are actually undermining it – with the able assistance of regulators who have drained liquidity from the world’s most important markets. Negative interest rates on $3 trillion of European debt are an obvious sign of policy failure, yet the policy elite stands mute. Actually that’s not correct – the cognoscenti is cheering on Mario Draghi as he destroys the European bond markets just as they celebrated Janet Yellen’s demolition of the Treasury market. Negative interest rates are not some curiosity; they represent a symptom of policy failure and a violation of the very tenets of capitalist economics. The same is true of persistent near-zero interest rates in the United States and Japan.

Zero gravity renders it impossible for fiduciaries to generate positive returns for their clients, insurance companies to issue policies, and savers to entrust their money to banks. They are a byproduct of failed economic policies, not some clever device to defeat deflation and stimulate economic growth. They are mathematically doomed to fail regardless of what economists, who are merely failed monetary philosophers practicing a soft social science, purport to tell us. The fact that European and American central banks are following the path of Japan with virtually no objection represents one of the most profound intellectual failures in the history of economic policy history.[..]

Christopher Whalen, one of the best bank analysts on Wall Street, argued that global banks face trillions of bad off-balance sheet debts that must eventually be resolved (i.e. written off) and are dragging on economic growth. These debts include everything from loans by German banks to Greece to home equity loans in the U.S. for homes that are underwater on their first mortgage. Banks and governments refuse to restructure (i.e. write off) these bad debts because doing so would trigger capital losses for banks and governments. As Mr. Whalen explains, “the Fed and ECB have decided to address the issue of debt by slowly confiscating value from investors via negative rates, this because the fiscal authorities in the respective industrial nations cannot or will not address the problem directly.”

But in addition to avoiding the bad debt problem, these policies are causing further economic damage by depressing growth and starving savers. Per Mr. Whalen: “ZIRP and QE as practiced by the Fed and ECB are not boosting, but instead depressing, private sector economic activity. By using bank reserves to acquire government and agency securities, the FOMC has actually been retarding private economic growth, even while pushing up the prices of financial assets around the world.”

Read more …

“Massive layoffs in the energy sector are now a certainty. Few realize that most of the gains in employment in the US since 2008 have been in shale states. Yet the carnage is not over.”

• Our Current Illusion Of Prosperity (Mises Inst.)

President Obama and Fed Chair Janet Yellen have been crowing about improving economic conditions in the US. Unemployment is down to 5.5% and growth in 2014 hit 2.2%. Journalists and economists point to this improvement as proof that quantitative easing was effective. Unfortunately, this latest boom is artificial and has been built by adding debt on top of debt. Total household debt increased 2.5% in 2014 — the highest level since 2010. Mortgage loans increased 1.5%, student loans 6.6% while auto loans increased a hefty 9.6%. The improving auto sales are built mostly on a bubble of sub-prime borrowers. Auto sales have been brisk because of a surge in loans to individuals with credit scores below 620. Since 2010, such loans have increased over 100% and have gone from 20% of originations in 2009 to 27% in 2013.

Yet, auto loans to individuals with strong credit scores, above 760, have barely budged over the last year. Subprime consumer borrowing climbed $189 billion in the first eleven months of 2014. Excluding home mortgages, this accounted for 41% of total consumer lending. This is exactly the kind of lending that got us into trouble less than a decade ago, and for many consumers, this will only end in tears. But we need to ask ourselves: is the current boom built on sound foundations? In other words, do we have sharp increases in productivity or real wage growth? Productivity increased less than 1% on average in the last three years and real wages have flat lined or declined for decades. From mid-2007 to mid-2014, real wages declined 4.9% for workers with a high school degree, dropped 2.5% for workers with a college degree and rose just 0.2% for workers with an advanced degree.

Is the boom being built on broad base investment in plant and equipment? The current average age of working plants and equipment in the US is one of the oldest on record. Meanwhile, it is now clear that the shale boom was an illusion of prosperity. Oil prices have dipped below $50 with some analysts calling for $20 oil by the end of the year. This is a drop from over $100 from last year. Many shale outfits need oil above $65 just to break even. Massive layoffs in the energy sector are now a certainty. Few realize that most of the gains in employment in the US since 2008 have been in shale states. Yet the carnage is not over. Induced by low interest, investment banks loaned over $1 trillion to the energy industry. The impact on the financial sector is still to be felt.

Read more …

Do read.

• Economic Inequality: It’s Far Worse Than You Think (Scientific American)

In a candid conversation with Frank Rich last fall, Chris Rock said, “Oh, people don’t even know. If poor people knew how rich rich people are, there would be riots in the streets.” The findings of three studies, published over the last several years in Perspectives on Psychological Science, suggest that Rock is right. We have no idea how unequal our society has become. In their 2011 paper, Michael Norton and Dan Ariely analyzed beliefs about wealth inequality. They asked more than 5,000 Americans to guess the%age of wealth (i.e., savings, property, stocks, etc., minus debts) owned by each fifth of the population. Next, they asked people to construct their ideal distributions. Imagine a pizza of all the wealth in the United States. What%age of that pizza belongs to the top 20% of Americans?

How big of a slice does the bottom 40% have? In an ideal world, how much should they have? The average American believes that the richest fifth own 59% of the wealth and that the bottom 40% own 9%. The reality is strikingly different. The top 20% of US households own more than 84% of the wealth, and the bottom 40% combine for a paltry 0.3%. The Walton family, for example, has more wealth than 42% of American families combined. We don’t want to live like this. In our ideal distribution, the top quintile owns 32% and the bottom two quintiles own 25%. As the journalist Chrystia Freeland put it, “Americans actually live in Russia, although they think they live in Sweden. And they would like to live on a kibbutz.” Norton and Ariely found a surprising level of consensus: everyone — even Republicans and the wealthy—wants a more equal distribution of wealth than the status quo.

This all might ring a bell. An infographic video of the study went viral and has been watched more than 16 million times. In a study published last year, Norton and Sorapop Kiatpongsan used a similar approach to assess perceptions of income inequality. They asked about 55,000 people from 40 countries to estimate how much corporate CEOs and unskilled workers earned. Then they asked people how much CEOs and workers should earn. The median American estimated that the CEO-to-worker pay-ratio was 30-to-1, and that ideally, it’d be 7-to-1. The reality? 354-to-1. Fifty years ago, it was 20-to-1. Again, the patterns were the same for all subgroups, regardless of age, education, political affiliation, or opinion on inequality and pay. “In sum,” the researchers concluded, “respondents underestimate actual pay gaps, and their ideal pay gaps are even further from reality than those underestimates.”

Read more …

Can man stop himself?

• Burning Down The House: Land, Water & Food (Eastwood)

I’m sure when Talking Heads wrote “Burning Down The House” that they didn’t exactly have financial collapse and environmental degradation in mind. Although with a verse like “Hold tight wait till the party’s over. Hold tight we’re in for nasty weather. There has got to be a way. Burning down the house” it’s hard not to see that song as strangely prophetic. What we are now doing to the planet and to human society is exactly that – burning down the house while we are still living in it. Everyone needs fuel, especially during a bitter winter, but only a mad man starts deconstructing the house in order to burn bits of it in the stove or fireplace. Almost as mad as that is stealing bits of other people’s houses to burn, but that at least is not soiling your own doorstep – well not at first.

In a world of limited resources and limited space we’ve now reached the point where raiding our neighbours’ houses is the same thing as raiding our own house, because the net effect is the same – disaster on an unprecedented level. Of course it’s easier to live in denial and keep on cannibalising the world’s vital resources at an ever-increasing rate and pretend that it’s business as usual, but in reality it is anything but that. The alarm bells from commentators from all sectors: science, economics, religion etc. are getting louder and more frequent, better argued and with the raw data to back it up, but we are still not listening. Of course, the alarm bell was being rung fifty or more years ago by people such as Admiral Hyman Rickover in 1957, the now retiring Lester Brown and the late Rachel Carson (author of Silent Spring).

Nobody really listened that well back then, although governments paid lip-service to these troublesome do-gooders. Now we know that what they said was entirely true, that we are headed for disaster and yet will still only get the tired old lip-service, as before or Koch Brother inspired denial. The evidence is clearly there that we are depleting all of our resources far too quickly, especially the land we use to produce food and draw raw materials from. In part a consequence of this, the fresh water supplies that are even more vital are also being depleted way too fast. Devastation of the land, especially deforestation exacerbates water loss and soil erosion. Couple this with increased damming of rivers, pollutant run-off into rivers, fracking and mining and you’ve a recipe for a water crisis, which will, in turn, lead to a food crisis.

Read more …

Amen.

• The Warren Effect: Here Is A Bluff That Needs To Be Called (Esquire)

Let us be quite definite about this. Any Democratic politician who thinks this is a bad situation – or, worse, will not stand by a Democratic colleague in this situation – is not worth the hankie to blow Joe Lieberman’s nose.

Representatives from Citigroup, JPMorgan, Goldman Sachs and Bank of America, have met to discuss ways to urge Democrats, including Warren and Ohio Senator Sherrod Brown, to soften their party’s tone toward Wall Street, sources familiar with the discussions said this week. Bank officials said the idea of withholding donations was not discussed at a meeting of the four banks in Washington but it has been raised in one-on-one conversations between representatives of some of them. However, there was no agreement on coordinating any action, and each bank is making its own decision, they said.

My god, what a prodigious bluff. Also, my god, what towering arrogance? These guys own half the world and have enough money to buy the other half, and they’re threatening the party still most likely to control the White House because they don’t like the Senator Professor’s tone? Her tone? Sherrod Brown’s tone? These are guys who should be worried about the tone of the guard who’s calling them down to breakfast at Danbury and they’re concerned about the tenderness of their Savile Row’d fee-fees? Honkies, please.

The tensions are a sign that the aftermath of the 2008 financial crisis – the bank bailouts and the fights over financial reforms to rein in Wall Street – are still a factor in the 2016 elections. Citigroup has decided to withhold donations for now to the Democratic Senatorial Campaign Committee over concerns that Senate Democrats could give Warren and lawmakers who share her views more power, sources inside the bank told Reuters.

Tensions? These are the guys who should have spent the last six years going door to door apologizing to every American for blowing up the world economy and then buying up the splinters. That is, they should have been going door-to-door to apologize to all those Americans who still have doors they can call their own. Call this. Do it now. Tell them their money is no good here any more. Give these brigands the 86 the way any respectable saloonkeeper gives the heave to a chronic deadbeat who’s run up an unpayable tab. Show the country in simple (and not necessarily civil) words what these people really are.

Demonstrate, speech by speech, that they have no loyalty to the political entity that is the United States of America, that they are stateless gombeen bastards who would sell this country’s democracy off like a subprime mortgage to put another ten bucks into their pockets. They are threatening the people whom they still should be thanking for saving them from themselves. And Senator Professor Warren is only their most conspicuous target. Don’t kid yourselves, this is a message they’re sending to every politician, up and down the line, national and local. Don’t cross us. We own you. There is only one response for a democratic people to make to this ongoing gross obscenity. Bring it, motherfkers. Bring your lunch. And your lawyers.

Read more …

What could possibly go wrong?

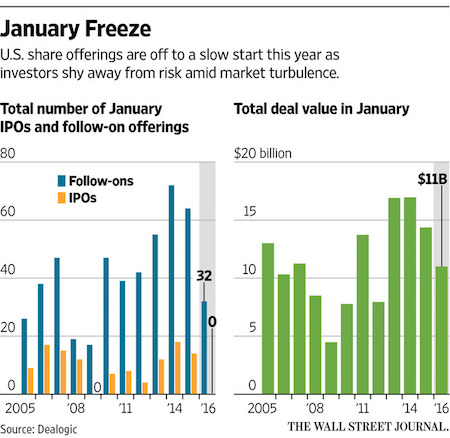

• Companies Go All-In Before Rate Hike, Issue Record Debt In Q1 (Zero Hedge)

It should come as no surprise that Q1 was a banner quarter for corporate debt issuance as struggling oil producers tapped HY markets to stay afloat, companies scrambled to max out the stock-buyback-via-balance-sheet re-leveraging play before a certain “diminutive” superwoman in the Eccles Building decides to do the unthinkable and actually hike rates, and there was M&A. As we discussed last week, rising stock prices have tipped investors’ asset allocation towards equities even as money continues to flow into bonds, meaning that yet more money must be funneled into fixed income for rebalancing purposes, which ironically drives demand for the very same debt that US corporates are using to fund the very same buy backs that are driving equity outperformance in the first place. Put more simply: the bubble machine is in hyperdrive. Not only did Q1 mark a record quarter for issuance, March supply also hit a record at $143 billion, tying the total put up in May of 2008. Here’s more from BofAML:

1Q set records for both supply and trading volumes in high grade, as new issue supply volumes reached $348bn, up from the previous record of $310bn in 1Q- 2014, whereas trading volumes averaged 15.6bn per day, up from the previous record of $14.3bn during the same quarter last year… Issuance in March totaled $143bn and it tied with May 2008 and September of 2013 for the highest monthly supply on record going back to at least 1998. September of 2013 was the month when the record $49bn VZ deal was priced… Supply in March was supported by low interest rates (encouraging opportunistic issuance on the supply side and supporting investor demand by diminishing interest rate risk concerns) and a busy M&A-related calendar. Some of these trends will continue in April, although investors are becoming more concerned about the Fed hiking cycle…

Read more …

The China casino.

• Shanghai Traders Make Trillion-Yuan Stock Bet With Borrowed Cash (Bloomberg)

Shanghai traders now have more than 1 trillion yuan ($161 billion) of borrowed cash riding on the world’s highest-flying stock market. The outstanding balance of margin debt on the Shanghai Stock Exchange surpassed the trillion-yuan mark for the first time on Wednesday, a nearly fourfold jump from just 12 months ago. The city’s benchmark index has surged 86% during that time, more than any of the world’s major stock gauges. While the extra buying power that comes from leverage has fueled the Shanghai Composite Index’s rally, it’s also sending equity volatility to five-year highs and may accelerate losses if a market reversal forces traders to sell.

Margin debt has increased even after regulators suspended three of the nation’s biggest brokers from adding new accounts in January and said securities firms shouldn’t lend to investors with less than 500,000 yuan. “It’s like a two-edged sword,” said Wu Kan, a money manager at Dragon Life Insurance Co. in Shanghai, which oversees about $3.3 billion. “When the market starts a correction or falls, it will increase the magnitude of declines.” In a margin trade, investors use their own money for just a portion of their stock purchase, borrowing the rest from a brokerage. The loans are backed by the investors’ equity holdings, meaning that they may be compelled to sell when prices fall to repay their debt.

Chinese investors have been piling into the stock market after the central bank cut interest rates twice since November and authorities from the China Securities Regulatory Commission to central bank Governor Zhou Xiaochuan endorsed the flow of funds into equities. Traders have opened 2.8 million new stock accounts in just the past two weeks, almost on par with Chicago’s entire population. The outstanding balance of the margin debt on China’s smaller exchange in Shenzhen was 493.8 billion yuan on March 31. That puts the combined figure for China’s two main bourses at the equivalent of about $241 billion. In the U.S., which has a stock market almost four times the size of China’s, margin debt on the New York Stock Exchange was about $465 billion at the end of February.

Read more …

Strong effort by Ambrose. He manages to look behind the obvious veil: “When Warren Buffett suggests that Europe might emerge stronger after a salutary purge of its weak link in Greece, he confirms his own rule that you should never dabble in matters beyond your ken.”

• Greek Defiance Mounts As Alexis Tsipras Turns To Russia And China (AEP)

Two months of EU bluster and reproof have failed to cow Greece. It is becoming clear that Europe’s creditor powers have misjudged the nature of the Greek crisis and can no longer avoid facing the Morton’s Fork in front of them. Any deal that goes far enough to assuage Greece’s justly-aggrieved people must automatically blow apart the austerity settlement already fraying in the rest of southern Europe. The necessary concessions would embolden populist defiance in Spain, Portugal and Italy, and bring German euroscepticism to the boil. Emotional consent for monetary union is ebbing dangerously in Bavaria and most of eastern Germany, even if formulaic surveys do not fully catch the strength of the undercurrents. This week’s resignation of Bavarian MP Peter Gauweiler over Greece’s bail-out extension can, of course, be over-played. He has long been a foe of EMU.

But his protest is unquestionably a warning shot for Angela Merkel’s political family. Mr Gauweiler was made vice-chairman of Bavaria’s Social Christians (CSU) in 2013 for the express purpose of shoring up the party’s eurosceptic wing and heading off threats from the anti-euro Alternative fur Deutschland (AfD). Yet if the EMU powers persist mechanically with their stale demands – even reverting to terms that the previous pro-EMU government in Athens rejected in December – they risk setting off a political chain-reaction that can only eviscerate the EU Project as a motivating ideology in Europe. Jean-Claude Juncker, the European Commission’s chief, understands the risk perfectly, warning anybody who will listen that Grexit would lead to an “irreparable loss of global prestige for the whole EU” and crystallize Europe’s final fall from grace.

When Warren Buffett suggests that Europe might emerge stronger after a salutary purge of its weak link in Greece, he confirms his own rule that you should never dabble in matters beyond your ken. Alexis Tsipras leads the first radical-Leftist government elected in Europe since the Second World War. His Syriza movement is, in a sense, totemic for the European Left, even if sympathisers despair over its chaotic twists and turns. As such, it is a litmus test of whether progressives can pursue anything resembling an autonomous economic policy within EMU. There are faint echoes of what happened to the elected government of Jacobo Arbenz in Guatemala, a litmus test for the Latin American Left in its day. His experiment in land reform was famously snuffed out by a CIA coup in 1954, with lasting consequences. It was the moment of epiphany for Che Guevara, then working as a volunteer doctor in the country.

Read more …

Believe it or not, this thing will have to reach a conclusion soon.

• Greece Threatens Default As Fresh Reform Bid Falters (Telegraph)

The Greek government has threatened to default on its loans to the International Monetary Fund, as Athens continued its battle to convince creditors for a fresh injection of bail-out cash. Greece’s interior minister told Germany’s Spiegel magazine, his country would not respect a looming €450m loan repayment to the fund on April 9, without a release of much-needed bail-out funds. “If no money is flowing on April 9, we will first determine the salaries and pensions paid here in Greece and then ask our partners abroad to achieve consensus that we will not pay €450 million to the IMF on time,” said Nikos Voutzis. The cash-strapped government has struggled to keep up with its wage and pensions obligations having agreed a bail-out extension on February 20.

Athens insists it has enough money to last it until the middle of April, but a final agreement on any deal is unlikely to be secured before the end of the month. A Greek government spokesperson later denied the reports of a deliberate default, saying the country still hoped for a “positive outcome” to its debt negotiations. The comments came as the eurozone’s working group discussed a new 26-page plan of reforms from Athens on Wednesday. Aiming to generate an estimated €6bn in 2015, Athens has pledged a range of revenue-raising measures including cracking down on tax evasion, carrying out an audit on overseas bank transfers, and introducing a “luxury tax”. The document also warned brinkmanship on the part of the eurozone meant the “viability” of the currency union was now “in question.”

“It is necessary now, without further delay to turn a corner on the mistakes of the past and to forge a new relationship between member states, a relationship based on solidarity, resolve, mutual respect,” said the proposal. The Leftist government has continually fallen short of creditor demands, who hold the purse strings on €7.2bn in bail-out cash the government requires over the next three months. However, the latest blueprint is unlikely to satisfy lenders as it lacks details on labour market liberalisation or pensions reforms. Previous privatisations of the country’s assets were also described as a “spectacular” failure, generating far less in revenues for the state than first envisaged..

Read more …

Wrong on purpose?

• China’s Fuel Demand to Peak Sooner Than Oil Giants Expect (Bloomberg)

China’s biggest oil refiner is signaling the nation is headed to its peak in diesel and gasoline consumption far sooner than most Western energy companies and analysts are forecasting. If correct, the projections by China Petroleum & Chemical, or Sinopec, a state-controlled enterprise with public shareholders in Hong Kong, pose a big challenge to the world’s largest oil companies. They’re counting on demand from China and other developing countries to keep their businesses growing as energy consumption falls in more advanced economies. “Plenty of people are talking about the peak in Chinese coal, but not many are talking about the peak in Chinese diesel demand, or Chinese oil generally,” said Mark C. Lewis at Kepler Cheuvreux. “It is shocking.”

Sinopec has offered a view of the country that should serve as a reality check to any oil bull. For diesel, the fuel that most closely tracks economic growth, the peak in China’s demand is just two years away, in 2017, according to Sinopec Chairman Fu Chengyu, who gave his outlook on a little reported March 23 conference call. The high point in gasoline sales is likely to come in about a decade, he said, and the company is already preparing for the day when selling fuel is what he called a “non-core” activity. That forecast, from a company whose 30,000 gas stations and 23,000 convenience stores arguably give it a better view on the market than anyone else, runs counter to the narrative heard regularly from oil drillers from the U.S. and Europe that Chinese demand for their product will increase for decades to come.

“From 2010 to 2040, transportation energy needs in OECD32 countries are projected to fall about 10% while in the rest of the world these needs are expected to double,” Exxon Mobil said in a December report on its view of the future. “China and India will together account for about half of the global increase.” Exxon expects most of that growth to be driven by commercial transportation for heavy-duty vehicles, specifically ships, trucks, planes and trains that run on diesel and similar fuels. BP’s latest public projection for China, released in February, sounds a similar note. “Energy consumed in transport grows by 98%. Oil remains the dominant fuel but loses market share, dropping from 90% to 83% in 2035.”

Read more …

“Asian-Pacific refiners are forecast to add 5.4 million barrels a day of capacity in the next five years..”

• The Saudis Are Losing Their Lock on Asian Oil Sales (Bloomberg)

Ships carrying oil from Mexico docked in South Korea this year for the first time in more than two decades as the global fight for market share intensifies. Latin American producers are providing increasing amounts of heavy crude to bargain-hungry Asian refiners in a challenge to Saudi Arabia, the world’s largest exporter and the region’s dominant supplier. “By diversifying, more Asian refiners will be able to reduce the clout that Saudi Arabia has on the market,” said Suresh Sivanandam, a refining and chemical analyst with Wood Mackenzie Ltd. in Singapore. “They will be getting more bargaining power for sure.”

The U.S., enjoying a surge of light oil from shale formations, has raised imports of heavy grades from Canada, displacing crude from nations such as Mexico and Venezuela. That’s boosting South American deliveries to Asia even after Saudi Arabia cut prices for March oil sales to the region, its largest market, to the lowest in at least 14 years. The shale boom also has transformed the flow of oil to Asia. South Korea received its first shipment of Alaskan crude in at least eight years as output from Texas and North Dakota displaces oil that fed U.S. refineries for years. The country was one of the first to receive a cargo of the ultralight U.S. crude known as condensate after export rules were eased.

Petrobras and partner operators are also shipping to Asia and were scheduled to load nine tankers bound for the region in March, according to Energy Aspects, as Latin American oil’s discount to Middle East benchmark Dubai widens to almost double the average of the past year. Asian-Pacific refiners are forecast to add 5.4 million barrels a day of capacity in the next five years, according to Gaffney, Cline & Associates, a petroleum consultant.

Read more …

“April is a crucial month for the industry because it’s when lenders are due to recalculate the value of properties that energy companies staked as loan collateral.” Calculations until now are stil based on $90 oil.

• Reckoning Arrives for Cash-Strapped Oil Firms Amid Bank Squeeze (Bloomberg)

Lenders are preparing to cut the credit lines to a group of junk-rated shale oil companies by as much as 30% in the coming days, dealing another blow as they struggle with a slump in crude prices, according to people familiar with the matter.

Sabine Oil & Gas became one of the first companies to warn investors that it faces a cash shortage from a reduced credit line, saying Tuesday that it raises “substantial doubt” about the company’s ability to continue as a going concern. About 10 firms are having trouble finding backup financing, said the people familiar with the matter, who asked not to be named because the information hasn’t been announced. April is a crucial month for the industry because it’s when lenders are due to recalculate the value of properties that energy companies staked as loan collateral.

With those assets in decline along with oil prices, banks are preparing to cut the amount they’re willing to lend. And that will only squeeze companies’ ability to produce more oil. “If they can’t drill, they can’t make money,” said Kristen Campana at Bracewell & Giuliani LLP’s finance and financial restructuring groups. “It’s a downward spiral.” Sabine, the Houston-based exploration and production company that merged with Forest Oil Corp. last year, told investors Tuesday that it’s at risk of defaulting on $2 billion of loans and other debt if its banks don’t grant a waiver. Publicly traded firms are required to disclose such news to investors within four business days, under U.S. Securities and Exchange Commission rules.

Some of the companies facing liquidity shortfalls will also disclose that they have fully drawn down their revolving credit lines like Sabine, according to one of the people. The credit discussions are ongoing and a number of banks may opt to be more lenient, giving companies more time to prepare for bigger cuts later in the year, the people said. Credit lines for some of the companies may be reduced by as little as 10%, they said. The companies are among speculative-grade energy producers that were able to load up on cheap debt as crude prices climbed above $100 a barrel. The borrowing limits are tied to reserves, the amount of oil and gas a company has in the ground that can profitably be extracted based on its land holdings. With oil prices plunging below $50 from last year’s peak of $107 in June, some are now fighting to survive.

Read more …

Commodities have been overvalued for a long time, due to crazy expectations for China growth.

• Appalachia Miners Wiped Out by Coal Glut That They Can’t Reverse (Bloomberg)

Douglas Blackburn has been crawling in and out of the coal mines of Central Appalachia since he was a boy accompanying his father and grandfather some 50 years ago. The only time that Blackburn, now a coal industry consultant, remembers things being this bad was in the 1990s. Back then, he estimates, almost 40% of the region’s mines went bankrupt. “It’s a similar situation,” said Blackburn, who owns Blackacre, a Richmond, Va consulting firm. Now, like then, the principal problem is sinking coal prices. They’ve dropped 33% over the past four years to levels that have made most mining companies across the Appalachia mountain region unprofitable. To make matters worse, there’s little chance of a quick rebound in prices. That’s because idling a mine to cut output and stem losses isn’t an option for many companies.

The cost of doing so – even on a temporary basis – has become so prohibitive that it can put a miner out of business fast, Blackburn and other industry analysts say. So companies keep pulling coal out of the ground, opting to take a small, steady loss rather than one big writedown, in the hope that prices will bounce back. That, of course, is only adding to the supply glut in the U.S., the world’s second-biggest producer, and driving prices down further. It’s become, in essence, a trap for miners. “You have this really perverse situation where they keep producing,” James Stevenson at IHS said in a telephone interview. “You’re just shoveling coal into this market that’s oversupplied.” Companies will dig up at least 17 million tons more coal than power plants need this year, Morgan Stanley estimates. Coal is burned at the plants to generate electricity. That’s creating the latest fossil fuel glut in the U.S., joining oil and natural gas.

Read more …

I was just sent this. Don’t know enough about it, I must admit. The article suggests that prices are still 11% higher than 3 months ago. That would seem to mean they rose 20% or so in 2015. It doesn’t make much sense to me right now.

• World Dairy Prices Slide 10.8% On Supply Concerns (NZ Herald)

International dairy prices continued to reverse gains made early this year at this morning’s GlobalDairyTrade (GDT) auction, putting downward pressure on Fonterra’s $4.70 a kg farmgate milk price forecast and raising concerns about next season’s likely payout. The GDT price index fell by 10.8% compared with the last sale a fortnight ago, when prices dropped by 8.8%. Big falls were recorded for the key products of wholemilk powder – down 13.3% to US$2,538 a tonne, skim milk powder – down 9.9% to US$2,467/tonne. Wholemilk prices are now just 11% higher than than they were by the end of 2014. ANZ rural economist Con Williams said that with milk powder making up the bulk of New Zealand’s product mix, the GDT result suggested a payout of $4.50-4.70 a kg this year.

The largest price falls at the auction were generally seen in the longer-dated contracts, up to 6 months out – into the new season. “While these prices remain higher than those for the end of this season, the curve has flattened, suggesting less price recovery is now anticipated – not boding well for next year’s payout,” Williams said. The fall comes as the New Zealand season enters its final phase, with about 80% of production now out of the way. Most of the price weakness was put down to better-than-expected supply, with the effects of this year’s drought being offset by rain in many parts of the country.

Read more …

Warren!

• CFTC Charges Kraft, Mondelez With Manipulating Wheat Futures (MarketWatch)

The Commodity Futures Trading Commission on Wednesday charged Kraft Foods and Mondelez Global with manipulating wheat futures and cash wheat prices. The CFTC says that, in response to high cash wheat prices in summer 2011, the two companies developed and executed in early December 2011 a strategy to buy $90 million of wheat futures they didn’t intend on receiving. The companies expected the market would react to their “enormous” long position in futures by lowering cash prices, the CFTC said. They later earned more than $5.4 million in profits, according to the CFTC’s complaint. The agency says litigation is continuing against the companies and it is seeking disgorgement and civil monetary penalties.

Read more …

“3G, co-founded by Lemann, eliminated more than 7,000 Heinz jobs in 20 months..”

• Brazil’s Richest Man May Reap $5.6 Billion in Kraft-Heinz Merger

Brazil’s richest man Jorge Paulo Lemann may add more than $5 billion to his personal fortune after ketchup maker H.J. Heinz merges with Kraft Foods. Heinz, controlled by Lemann’s 3G Capital and Warren Buffett’s Berkshire Hathaway, agreed last week to buy the macaroni-and-cheese maker Kraft in a cash-and-stock deal. Heinz’s 51% of the combined company will be worth about $45 billion, valuing Lemann’s stake at about $9.6 billion, said Kevin Dreyer, a portfolio manager at Gabelli Equity. Lemann has invested about $4 billion through 3G Capital, according to data compiled by Bloomberg.

“A combination of synergies from the deal and the sprinkling of the magic 3G dust is giving Kraft a higher valuation than it would otherwise have,” Dreyer said in a phone interview from New York. “3G has a track record of drastically expanding margins. There’s an expectation they’ll achieve the number they put in and then some.” 3G, co-founded by Lemann, eliminated more than 7,000 Heinz jobs in 20 months after taking the company over with Berkshire Hathaway. Buffett defended the job reductions his partners at 3G have taken when they buy businesses during a March 31 interview on CNBC.

The share price of Kraft, which surged 36% the day of the deal, can be used to estimate the future value of closely held Heinz, Dreyer said. His calculation takes into account the ketchup maker’s special dividend payment and assumes a market capitalization of about $87 billion for the new company. 3G owns 48% of Heinz, co-founder Alex Behring told reporters March 25. The buyout firm contributed $4.25 billion to Heinz in 2013 and another $4.8 billion in the Kraft deal. Lemann hasn’t disclosed his personal stake in Heinz. His investments in publicly traded companies show he tends to have a larger stake than Brazilian 3G partners Marcel Telles and Carlos Alberto Sicupira..

Read more …

Multiple currencies. Looks inevitable for Greece too.

• The Cuban Money Crisis (Bloomberg)

The currency crisis starts about 75 feet into Cuba. I land in the late afternoon and, after clearing customs, step into the busy arrivals hall of Havana’s airport looking for help. I ask a woman in a gray, military-like uniform where I can change money. Follow me, she says. But she doesn’t turn left, toward the airport’s exchange kiosk. Called cadecas, these government-run currency shops are the only legal way, along with banks, to swap your foreign money for Cuba s tourist tender, the CUC. Instead, my guide turns right and only comes clean when we reach a quiet area at the top of an escalator. The official rate is 87 for a hundred, she whispers, meaning CUCs to dollars. I’m giving you 90. So it’s a good deal for you.

I want to convert $500, and she doesn’t blink an eye. Go in the men’s room and count your money out, she instructs. I’ll do the same in the ladies room. The bathroom is crowded, with not one but two staff and the usual traffic of an airport in the evening. There s no toilet paper. In an unlit stall I try counting to 25 while laying $20 bills on my knees. There’s an urgent knock, and under the door I see high heels. I’m still counting, I say. She’s back two minutes later and pushes her way into my stall. We trade stacks, count, and the tryst is over. For my $500, I get 450 CUCs, the currency that’s been required for the purchase of almost anything important in Cuba since 1994. CUCs aren’t paid to Cubans; islanders receive their wages in a different currency, the grubby national peso that features Che Guevara’s face, among others, but is worth just 1/25th as much as a CUC.

Issued in shades of citrus and berry, the CUC dollarized, tourist-friendly money has for 21 years been the key to a better life in Cuba, as well as a stinging reminder of the difference between the haves and the have-nots. But that’s about to change: Cuba is going to kill the CUC. Described as a matter of fairness by President Raul Castro, the end of the two-currency system is also the key to overhauling the uniquely incompetent and centrally planned chaos machine that is the Cuban economy.

Even in Cuba there are markets, and the effects of Castro’s October announcement of a five-step plan for phasing out the CUC are already rippling out to every wallet in the country. The government has issued notifications and price conversion charts, and introduced new, larger bills to supplement the low-value national peso. Over the next year, the CUC will be invalidated what Cuban economists call Day Zero and then, in steps four and five, the regular Cuban peso will become exchangeable and be floated against a basket of five currencies: the yuan, the euro, the U.S. dollar, and two others to be named later.

Read more …

But still in complete denial: “..the governor’s action won’t mean mandatory rationing for households.”

• California Orders Mandatory Water Cuts Of 25% Amid Record Drought (WSJ)

California Gov. Jerry Brown ordered unprecedented mandatory water cuts across the Golden State after the latest measurements show the state’s mountain snowpack – which accounts for roughly a third of California’s water supply – has shrunk to a record low of 5% of normal for this time of year. The Democratic governor took the action on Wednesday after accompanying state surveyors into the Sierra Nevada mountains to manually verify electronic readings that show an average snow water equivalent of 1.4 inches, the lowest ever recorded on April 1. “Today we are standing on dry grass where there should be five feet of snow,” the governor said. “This historic drought demands unprecedented action.”

Gov. Brown directed the State Water Resources Control Board to implement mandatory water reductions of 25%. Details on how the cuts would be implemented weren’t immediately released, although the governor said in his order that reductions would fall hardest in water districts that haven’t adequately followed his voluntary calls for conservation last year. According to monthly surveys of water use, conservation levels have varied widely around the state. In general, reductions have been lower in Southern California than the rest of the state, in part because of the region’s concentration of estate-sized lots homes and golf courses. A spokesman for the state water control board, which has already ordered limits in outdoor lawn watering, said the governor’s action won’t mean mandatory rationing for households.

Read more …