DPC Launch of freighter Howard L. Shaw, Wyandotte, Michigan 1900

All we have left is debtors though.

• Debtor Days Are Over As BIS Calls Time On World Credit Binge (Tel.)

The world’s credit boom is beginning to show dangerous signs of unraveling, ushering in a period of fresh turmoil for the over-indebted global economy, the Bank of International Settlements has warned. The globe’s top financial watchdog called time on the world’s debt binge, noting that debt issuance and cross border flows in emerging economies slowed for the first time since the aftermath of the global credit crunch at the end of last year. With financial markets thrown into fresh paroxysms in 2016, oscillating between extremes of “hope and fear”, the over-leveraged world was finally approaching a day of reckoning, said Claudio Borio, the bank’s chief economist. “We may not be seeing isolated bolts from the blue, but the signs of a gathering storm that has been building for a long time”, he said.

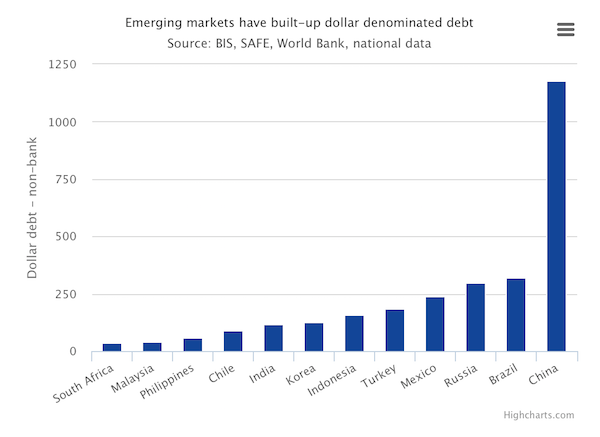

The Swiss authority – known as the “central bank of central banks” – has long rang the alarm bell over the state of global indebtedness, warning that unprecedented monetary policy was storing up problems in a world which still lumbers under weak productivity, insipid growth, and has no appetite for major reforms. In its latest quarterly review, the BIS said some of its starkest warnings were now coming into fruition. It noted that international securities issuance turned negative at the end of last year to the tune of -$47bn – the sharpest contraction since the third quarter of 2012. The retrenchment was largely driven by the financial sector, said the BIS. Meanwhile emerging market debtors – who have embarked on a $3.3 trillion dollar denominated debt spree in the wake of the financial crisis – saw issuance ground to a halt in the second half of the year.

This provided a “telltale” sign that the financial conditions were reaching an inflection point, accompanied by large depreciations in emerging market currencies and slowing domestic growth. “It is as if two waves with different frequencies came together to form a bigger and more destructive one”, said Mr Borio. Global debt now stands at over 200pc of GDP, exceeding levels seen before the financial crash in 2007. Any turning in the credit cycle risks imperiling debtor companies and governments, raising the chances of default and corporate bankruptcies, said the BIS. “If they persist, tighter global liquidity conditions may raise stability risks in some countries, especially those where other indicators already point to a heightened risk of financial stress”, they said.

Ahead of the US Federal Reserve’s landmark decision to raise interest rates for the first time in eight years last December, the BIS had forewarned of an “uneasy market calm” that could quickly turn to debtor distress. This prophecy is seemingly playing out in the first three months of 2016. “The tension between the markets’ tranquility and the underlying economic vulnerabilities had to be resolved at some point,” said Mr Borio. “In the recent quarter, we may have been witnessing the beginning of its resolution.” Debt binges have also been exacerbated by a historic collapse in oil prices. Energy companies from Brazil to Russia are scrambling to service $3 trillion of dollar debt as prices languish at around $30 a barrel – a 70pc decline since late 2014.

More BIS.

• ‘Gathering Storm’ For Global Economy As Markets Lose Faith (AFP)

A fragile calm in global financial markets has given way to all-out turbulence, the Bank of International Settlements has said, warning of a “gathering storm” which has long been brewing. In its latest quarterly report, watched closely by investors, the BIS – which is known as the central bank of central banks – also warned that investors were concerned governments around the world were running out of policy options. BIS chief Claudio Borio said the “uneasy calm” of previous months had given way to turbulence and a “gathering storm”. “The tension between the markets’ tranquillity and the underlying economic vulnerabilities had to be resolved at some point. In the recent quarter, we may have been witnessing the beginning of its resolution,” he added.

“We may not be seeing isolated bolts from the blue, but the signs of a gathering storm that has been building for a long time,” he warned. Although Asian markets enjoyed another strong day on Monday and continued to claw back the losses of January, the report said said that investors were concerned about what central banks could do in the event of another crisis. “Underlying some of the turbulence was market participants’ growing concern over the dwindling options for policy support in the face of the weakening growth outlook,” the report said. “With fiscal space tight and structural policies largely dormant, central bank measures were seen to be approaching their limits.”

Borio surveyed the major disruptions over the last three months, from the first post-crisis interest rate hike by the US Federal Reserve in December, to accumulating signs of China’s slowdown. In what he termed the second phase of turbulence in the last quarter, Borio said markets were plagued by fears about the health of global banks and the Bank of Japan’s shock decision to impose negative policy rates.

Japan deserves a lot more scrutiny.

• The Bank Of Japan Has Turned Economics On Its Head (BBG)

Call me old fashioned, but I still think prices matter. I vividly recall the first time I studied those simple supply-and-demand graphs as a college freshman, and today, far too many years later, their basic logic remains undeniable. When prices are right, money flows to the most productive endeavors and economies work efficiently. When prices are wrong, crazy things eventually happen, with potentially dire consequences. That’s why we should be very worried about Japan, where things are getting crazy. On March 1, the Japanese government sold benchmark, 10-year bonds at a negative yield for the first time ever. Think about that for a minute. The investors who bought these bonds not only loaned the Japanese government their money. They’re paying for the privilege of doing so.

Why would any sane person do such a thing? A government with debt equivalent to more than 240% of national output – the largest load in the developed world – should surely have to pay investors a tidy sum to convince them to part with their money, not the other way around. But the bond market in Japan has become so distorted that investors believe it’s in their interests to lend money at a cost to themselves. The only explanation is that prices in Japan have gone horribly, horribly awry, and that has made the illogical logical. The culprit is the Bank of Japan. The entire purpose of its unorthodox stimulus programs – QE, negative interest rates – is, in effect, to get prices wrong: to press down interest rates below where they would normally go and force banks to lend money in ways they normally wouldn’t.

The BOJ, in other words, is trying to alter prices to change the incentive structure in the economy in order to engineer certain results – to increase inflation, encourage investment and spark growth. The problem is that the BOJ hasn’t achieved any of those objectives. Inflation in January, by one commonly used measure, was a pathetic zero. GDP has contracted in two of the past three quarters. Instead, the BOJ is creating new problems by undermining the price mechanism. The central bank is buying up so many government bonds that it has effectively stripped them of risk to the investor and cost to the borrower. Investors probably bought up the bonds with negative yields speculating that they could flip them to the BOJ. Meanwhile, since the government can now earn money while borrowing it, the BOJ is removing any urgency for Japan’s politicians to control debt and reduce budget deficits.

Worse, the central bank is undercutting the very goals it’s trying to achieve. By wiping out returns to investors on safe investments like government bonds – the yield curve on them is as flat as a pancake – the BOJ is straining the incomes of savers and dampening the consumption that might help the economy revive. If debt pressures finally do push the government to hike taxes again, spending will take another hit.

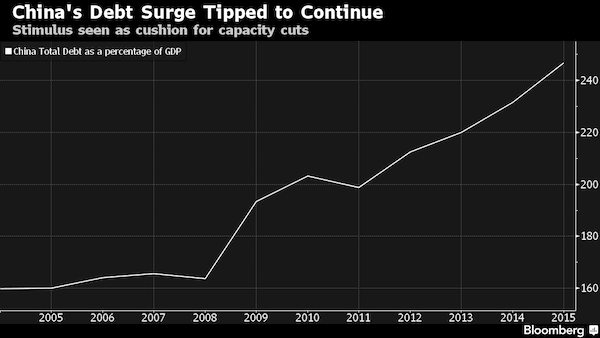

“Li signaled the prospect for more debt days after Moody’s Investors Service lowered its outlook on China’s credit rating to negative from stable because of a surge in borrowing.”

• China Growth Addiction Leaves Deleveraging, Reform in Back Seat (BBG)

Rule No.1 in China’s blueprint for the next five years: “give top priority to development.” That’s the word from Premier Li Keqiang’s work report delivered Saturday at the start of the annual National People’s Congress in Beijing. Li acknowledged there would be some difficult battles ahead as he outlined plans to clean up the environment, boost innovation, further urbanize and cut excess capacity in industries like coal and steel. Yet the firmest target remains on the one thing he has the least control over – the nation’s economic growth rate. For 2016, a 6.5% to 7% growth range was outlined, with 6.5% pegged as the baseline through 2020. That would be less than last year’s 6.9% rate, the slowest growth in a quarter century. To reach the new target, the government will permit a record high deficit and has raised its money supply expansion target.

The upshot: debt grows even as growth slows. “The risk is that if stimulus is accelerated but reform continues to lag, the government could end the year with growth on target but even bigger structural problems to deal with,” Bloomberg Intelligence economists Tom Orlik and Fielding Chen wrote in a note. The report “confirms that the focus is firmly on supporting short-term growth, with the deleveraging can kicked further down the road.” Li’s plan suggests debt may rise to 258% of GDP this year, from 247% at the end of 2015, they estimate. Li signaled the prospect for more debt days after Moody’s Investors Service lowered its outlook on China’s credit rating to negative from stable because of a surge in borrowing. “Development is of primary importance to China and is the key to solving every problem we face,” Li said in the work report. “Pursuing development is like sailing against the current: you either forge ahead or you drift downstream.”

Sorry, boys, confidence is in the gutter.

• China Defends Veracity Of Foreign Exchange Reserves Data (FT)

China’s official foreign exchange reserves only include highly liquid assets, a top central banker said on Sunday, seeking to reassure investors that authorities have enough ammunition to prevent a sharp fall in the renminbi. Investor sentiment towards China’s currency has turned sharply negative since a surprise devaluation in August, amid unprecedented capital outflows and concern about the health of the economy. Concern over China’s currency policy sparked a global market sell-off early this year. The People’s Bank of China has drawn on its foreign exchange reserves to curb renminbi weakness, but analysts believe the central bank may soon be forced to abandon this policy to prevent reserves dropping below dangerous levels.

Some bearish investors have also expressed skepticism about the reliability of China’s official foreign exchange reserves data, which showed reserves at $3.2tn at the end of January — still the world’s largest despite declining for 19 months. Skeptics say the headline total of reserves exaggerates the resources available to support the renminbi since they suspect it includes illiquid assets such as foreign real estate and private-equity investments that cannot be readily deployed in currency markets. Kyle Bass, the US hedge fund manager who has wagered billions that the renminbi and other Asian currencies will fall, believes China’s true reserves are more than $1tn below the government’s official total. Veteran investor George Soros has also suggested the renminbi may fall further.

Yi Gang, PBoC deputy governor who until January was also head of the foreign exchange regulator, said on Sunday that only highly liquid assets are included in the closely watched headline reserves figure. “I can clearly tell everyone here, those assets that don’t meet liquidity standards are entirely deducted from official foreign exchange reserves,” Mr Yi said. “For example, some illiquid equity investments, some capital injections and some other assets where liquidity isn’t good are entirely outside our foreign exchange reserves.” Beyond foreign real estate and private equity, analysts have questioned whether PBoC’s recent use of foreign currency to inject capital into state-owned policy banks, including at least $93bn injected into China Development Bank and the Export-Import Bank of China last year. There is also uncertainty about whether China’s capital contributions to two newly launched multilateral development banks, the Asia Infrastructure Investment Bank and the Brics bank, have been deducted.

While continuing to inflate history’s biggest bubble even further.

• China’s Leaders Put the Economy on Bubble Watch (WSJ)

China’s leaders made clear they are emphasizing growth over restructuring this year, but suggested they are trying to avoid inflating debt or asset bubbles as they send massive amounts of money coursing through the economy. The government’s announcement of a 6.5% to 7% growth target for 2016 at the start of the National People’s Congress over the weekend came with subtle acknowledgment that some of its efforts to jump-start a persistently decelerating economy have misfired, failing to steer stimulus to the most productive sectors. In his report to the annual legislative session, which opened Saturday, Premier Li Keqiang promised tax cuts that could leave companies with more money to invest.

And for the first time, the Chinese government specified total social financing—a broad measure of credit that includes both bank loans and nonbank lending—as a metric for helping determine monetary policy. In the past, leaders have just said total social financing should be kept at an appropriate level, while they have set clear targets for M2 money supply, which covers all cash in circulation and most bank deposits. Both measures have increased sharply in recent months. But the money-supply measure fails to capture how banks and financial institutions use the funds. For instance, M2 jumped 13.3% last year while total social financing grew 12.4%, according to official data. The discrepancy indicates not all deposits were used by banks to make loans to companies; instead, some of the funds were tapped for such purposes as margin loans for stock-market speculation.

This year, the two targets are paired, with both set to rise 13%. “The government seeks to more accurately show where the money is going, and whether credit is being used to support the real economy,” said Sheng Songcheng, head of the central bank’s survey and statistics department, in an interview. China’s past efforts to direct credit to entrepreneurs and other desired sectors of the economy have fallen short. And its loose monetary policy risks giving inefficient companies more room to avoid shutting down or retooling. Much of China’s breakneck growth over the past two decades has been fueled by state-led investment and debt. Concerns about a credit buildup have grown as the economy has slowed.

Prices in Shanghai and Shenzhen are totally crazy. And that’s the government’s doing.

• China Plans Crackdown on Loans for Home Down-Payments (BBG)

Chinese regulators plan to impose new rules to end the practice of homebuyers taking out loans to cover down-payments, as they step up scrutiny of financing risk in the property market, according to people familiar with the matter. The rules will bar lenders including developers, housing agencies, small-loan companies and peer-to-peer networks from offering loans for down-payments, said the people, who asked not to be named because the matter isn’t yet public. Regulators including the central bank and the China Banking Regulatory Commission will also ask commercial banks to scrutinize mortgage applications and reject those where down-payments come from loans offered by such institutions, the people said.

China is planning the crackdown amid concerns about rising risks in the loan markets and warnings from officials that home prices in some top-tier cities are rising too fast. Shanghai’s most-senior official said the city’s property market has “overheated” and should be more tightly controlled after a recent surge in residential housing prices. As part of the latest moves, regulators will also strengthen the stress tests of property loans, the people said, without offering details. Representatives at the People’s Bank of China and the CBRC didn’t immediately respond to faxed requests for comment. China in November 2014 started easing property curbs amid efforts to revive the world’s second-largest economy. The measures – intended to ease a glut of unsold homes in smaller cities – have instead lifted prices in the country’s biggest population centers.

Prices in Shenzhen jumped 4% in January from a month earlier and have gained 52% over the past year. Values in the financial center of Shanghai have increased 18% in the last 12 months, while those in Beijing advanced about 10%. Regulators last month allowed commercial banks to cut the minimum mortgage down-payment for first-home purchases to 20% from 25% and to 30% from 40% for second homes, except in five big cities with home-buying restrictions. Demand for real estate is also getting a boost from monetary stimulus after the PBOC cut benchmark lending rates six times since 2014, lowered banks’ reserve requirements and flooded the financial system with cash to keep borrowing costs low.

“Home prices in the city surged 370% from their 2003 trough through the September peak..”

• Hong Kong Homes Sales Tumble 70% (BBG)

Hong Kong residential home sales plunged 70% in February from a year earlier to a 25-year low, as falling prices and economic uncertainty deterred buyers. In February, 1,807 homes were sold in Hong Kong, compared with 6,027 a year earlier, according to government statistics. Home sales fell from 2,045 in January, the data show. “The newspapers keep on saying the market is going down and buyers think they can get a cheaper house half-a-year later or one year later so are waiting,” said Thomas Fok, a property agent at Centaline Property Agency in Hong Kong’s upscale Mid-levels West district where he hasn’t made one sale this year.

Property prices have declined 10% from their September highs amid uncertainty over the economy at home and in China, possible interest-rate increases and plans by the government to boost housing supply in the next five years. Senior Hong Kong government officials have ruled out relaxing property curbs, which include extra stamp duties and caps on mortgage levels. [..] Home prices in the city surged 370% from their 2003 trough through the September peak, spurred by low mortgage rates, tight supply of new units and buying from mainland Chinese. This year, BOCOM International Holdings Co. property analyst Alfred Lau has said prices could fall 30% amid a slowdown.

“I think the situation right now is more dangerous than it was last summer..”: former finance minister Gikas Hardouvelis.

• Grexit Back On The Agenda Again As Greek Economy Unravels (Guardian)

European finance ministers will once again deliberate over how to treat Greece’s ongoing debt crisis this week despite the country desperately grappling with refugees pouring across its borders. A meeting on Monday of finance ministers from the eurozone will determine whether creditors are to be given the green light to complete a long-delayed review of Greek economic recovery plans. The review has been held up by disagreement among lenders over how much more Athens needs to cut from public spending. It is seen as key to reviving Greece’s banking sector and restoring business and consumer confidence. “I think the situation right now is more dangerous than it was last summer,” the former finance minister Gikas Hardouvelis told the Guardian.

“Then it was a question of the political will of a few people,” he said, referring to the tumultuous negotiations that paved the way to Athens receiving a third bailout in August. “Now it’s a question of implementing reforms and working hard and if a government doesn’t believe in them and implements them begrudgingly, progress becomes very difficult.” Monday’s meeting comes at an especially sensitive time. Greek unemployment remains the highest in Europe at almost 25% – and just under 50% among the young. Many companies are relocating to Bulgaria, Albania, Romania and Cyprus as a result of over-taxation. Meanwhile, the once booming tourism trade has taken a hit as bookings to Aegean isles have collapsed because of refugee arrivals. Last week, it was announced by Greece’s official statistics agency, Elstat, that the debt-stricken nation had dipped back into recession.

After three emergency bailouts and the biggest debt restructuring in history, talk once again has turned to the country dropping out of the single currency. Businessmen and bankers in private concede that as the economy disintegrates the possibility of a parallel currency is now openly being discussed. “The probability of Grexit is still there,” added Hardouvelis. “It has not gone away. Just look at the yield investors are required to pay on Greek bonds.” Everyone agrees that time is of the essence. Further delays make potentially explosive reforms – starting with the overhaul of the pension system – harder to sell for a leftist-led government that in recent months has faced protest on the streets. “We have no time,” finance minister Euclid Tsakalotos told the European parliament’s economics committee last week. “We hope the IMF will become more reasonable.”

Europe’s a zombie financially and politically.

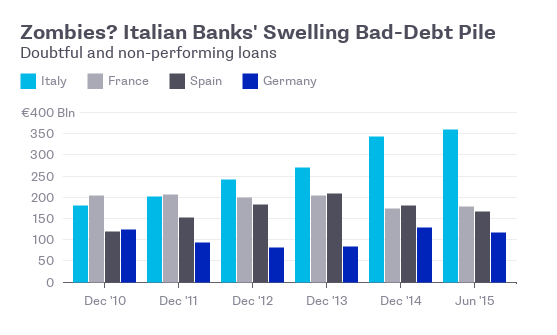

• Zombie Banks Are Stalking Europe (BBG)

Zombies are stalking Europe — zombie banks that are solvent in name only. The phenomenon is not new. Zombies weighed down Japan for almost 20 years after a real estate bust. They are usually born of financial panics, when loans go bad, capital flees and the value of assets tumbles. There are no good choices when zombie banks are on the march. Shutting them down can cause further panic. Restoring them to health can require hundreds of billions of dollars. But letting them fester can cripple an economy for years, because zombies don’t make the loans healthy businesses need to grow and consumers need to spend. No place has been cozier for zombies since the 2008 global financial crisis than Europe, and no economy has been slower to recover.

Europe has been slow and piecemeal in its approach to the region’s troubled banks. Lenders in Greece received their third cash infusion from the government in 2015. In Italy, the government developed a plan in early 2016 to relieve banks of their soured loans, though it’s expected to have only a limited impact because the program is voluntary. Investors are concerned that Europe’s banks are so weak that they still pose a risk to the economy and financial stability, after crippled banks in Ireland, Portugal, Greece and Spain threatened to pull down their indebted governments between 2010 and 2012. Even after multiple rescues and capital injections, almost a fifth of 130 banks failed a ECB stress test in October 2014, with a total capital shortfall of €25 billion. In an effort to coordinate the response, the ECB was given the job of the central banking regulator at the end of 2014. But even the ECB wasn’t bold enough to put a bullet to zombies’ heads, only requiring banks to be more aggressive on provisioning for bad loans.

One thing about old-fashioned bank runs — when they killed banks they stayed dead. The panics that followed, however, could bring down healthy banks as well, so tools for supporting banks grew up, most notably deposit insurance. Those developments brought with them a thorny question — when to pull the plug. The term “zombie banks” was coined by Edward J. Kane of Boston College in 1987 to refer to U.S. savings and loans institutions that had essentially been wiped out by commercial-mortgage losses but were allowed to stay in business, as regulators put off the pain of shutting them down in the hope that a market rebound would make them whole. By the time they gave up and cleaned up the mess, the losses of the zombies had tripled.

In Japan, zombie banks propped up zombie companies rather than write down their loans, while the banks themselves were kept alive through “regulatory forbearance” — a tacit agreement by the government to pretend that their bad loans were still worth something, an approach that kept the markets calm but contributed to a “lost decade” of economic stagnation. The prime example of a tough approach is Sweden, which in the 1990s responded to a financial crisis by nationalizing its ailing banks — and quickly rebounded.

After the 2008 crisis, the U.S. pumped $300 billion into its banks, but it also conducted stress tests that were more rigorous than Europe’s and forced low-scoring banks to raise private capital. In Europe, countries from Germany to Spain plugged holes in their banks and failed year after year to force losses and recapitalizations as the U.S. had. As a result, European lenders still sit on more than $1 trillion of dud loans, which don’t earn them any money and prevent them from making new loans that the region’s economy needs desperately to grow.

QE in a nutshell: “..the benefits from these wealth effects will accrue to those households holding most financial assets.”

• Threat Of A Synchronised Downturn (Pettifor)

“For the proposition that supply creates its own demand, I shall substitute the proposition that expenditure creates its own income” JM Keynes Collected Writings, Volume XXIX, p. 81

G20 Finance Ministers met in Huangzhou, China recently and refused appeals from both the IMF and the OECD for “urgent collective policy action” that focussed “fiscal policies on investment-led spending”. Instead the world’s finance ministers concluded that “it’s every country for themselves”. Keynes’s simple proposition is compelling: that expenditure will expand national (and international) income (including tax income) and thereby reduce the deficit. But it is a proposition that is anathema to OECD politicians, their friends in the finance sector and their advisers. Instead they adhere stubbornly to the antiquated classical economics embodied in Say’s Law.

Rather than relying on expenditure or investment, the British 2010-2015 Coalition government and then the 2015 Conservative government placed excessive reliance on monetary policy to revive aggregate demand for goods and services. The consequences were predictable. Loose monetary policy enriched those that owned assets – stocks and shares, bonds or property. The evidence of this grotesque enrichment is clearest in London. According to the FT (20 Feb 2016) the owners of South Kensington residential properties have seen “substantial capital appreciation – 45 % over the past five years and a remarkable 155% since 2006.” And as the Bank of England concluded back in 2012 in its paper on the Distributional Effects of Asset Purchases” (i.e. QE): “the benefits from these wealth effects will accrue to those households holding most financial assets.”

By contrast fiscal consolidation (austerity) has since 2010 hurt those that do not own assets – i.e. those who live by hand or by brain, or who are dependent on welfare, and do not benefit from the rent generated by the ownership of assets. Now, the British government is set to impose the largest fiscal consolidation of all OECD countries. Worryingly, it proposes to do so at a time of global economic and financial fragility. But the British government has not been alone in pursuing policies that enrich the already rich, while contracting wider economic activity. Over-reliance on central bankers and monetary policy, coupled with deflationary and contractionary fiscal policy is the cause both of ongoing weakness in OECD countries and of the slow but inexorable decline in world trade since 2011.

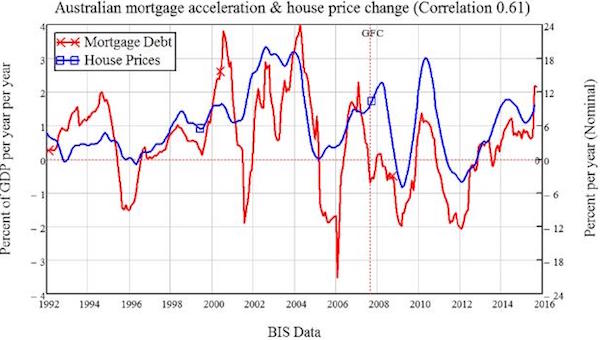

“The problem is that nothing — not even Donald Trump’s popularity — accelerates forever.”

• Why The House Price Bubble Still Hasn’t Burst (Steve Keen)

The standard retort to those who claim that Australia has a housing bubble is that it’s all just supply and demand. I can happily agree that it is indeed all just supply and demand and still prove that there is a bubble. Understanding my argument might force you to think more than you normally have to, in which case, tough: it’s about time Australians did some thinking. Fundamentally, the demand for housing comes from the flow of new mortgages. Only the super-rich or the well-heeled offshore buyer can afford to buy property without a mortgage, and the importance of mortgage debt has increased dramatically over time. In the 1970s, you couldn’t get a mortgage without a 30% deposit, so cash made up 30% of the purchase price; now it’s closer to 10%.

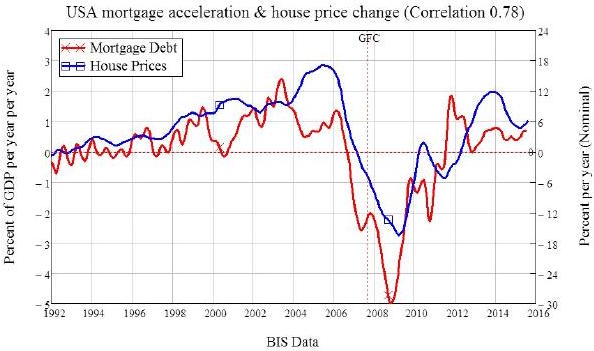

So, on the demand side of the supply and demand equation, we have the flow of new mortgage debt. On the supply side, we have two factors: the number of properties for sale and their prices. There is, therefore, a “dynamic tension” (to quote Rocky Horror) between the rate of change of mortgage debt, and the level of house prices: if the monetary value of the flow of new mortgage debt equals the monetary value of the flow of supply, then there’s no pressure forcing prices to change. It follows that there is a relationship between the acceleration of mortgage debt and the rate of change of house prices. So for house prices to rise, the flow of new mortgage debt needs to be not merely positive, but accelerating — growing faster over time.

Lest that sound like standard economic mumbo-jumbo — as Ross Gittins pointed out very well recently, most so-called economic modelling is no more than fantasy (“Tax modelling falls down at the household level”)—Figure 1 shows the empirical evidence for America, where not even Alan Greenspan disputes that there was a bubble. Similar relationships apply for all countries — and for the econometrically minded, the causal relation (as tested on US data) is from accelerating mortgage debt to house prices, not vice-versa.

Is Australia different? No. The same relationship applies here and now: though foreign buyers have certainly played a part, the key factor driving rising Australian house prices in the last three years has been accelerating mortgage debt.

So what’s the problem? The problem is that nothing — not even Donald Trump’s popularity — accelerates forever. At some point, the level of mortgage debt relative to income will stabilise; well before that happens, the acceleration of mortgage debt will decline, and prices will fall. This has already happened twice in recent history in Australia: in 2008 and in 2010. On both occasions, deliberate government policy stopped the fall in prices by encouraging Australians back into mortgage debt — firstly via the First Home Vendors Boost under Rudd and secondly via the RBA’s rate cuts from 2012 which were undertaken with the hope they would encourage more household borrowing. In both cases the acceleration of mortgage debt resumed, as did the bubble in prices.

Europe’ disgrace.

• Turkey Steps Up Crackdown on Erdogan Foes on Eve of EU Meetings (BBG)

Turkish authorities are escalating a crackdown on President Recep Tayyip Erdogan’s opponents, undeterred by possible risks to the nation’s renewed attempts to join the EU. In two days, authorities seized control of the company that owns a leading newspaper, and signaled the possibility of stripping prominent Kurdish lawmakers of their parliamentary immunity. The moves come on the eve of talks on Monday in Brussels between Turkish and EU officials to discuss ways to handle the influx of refugees from Syria. With the EU increasingly seeking Turkey’s help to contain Europe’s worst refugee crisis since World War II, and Ankara’s membership talks at an early stage, Erdogan’s allies are betting that the escalation won’t damage Turkey’s ties with the bloc.

The president expects EU leaders “to turn a blind eye” in return for his “cooperation in curbing Syrian refugee flows to the continent,” said Aykan Erdemir at the Foundation for Defense of Democracies, a policy institute. On Friday, Turkey seized control of the Zaman newspaper, the latest twist in a 2 1/2-year campaign against Fethullah Gulen, a former ally of Erdogan accused of running a “parallel state” to undermine the government. The move sparked clashes between police and anti-government protesters. EU governments revived the entry talks, dormant since November 2013, as part of a package of economic and political incentives to encourage Erdogan to host refugees in Turkey instead of pointing them to Europe.

German Finance Minister Wolfgang Schaeuble said in an interview recorded last week and broadcast on Sunday on BBC’s Andrew Marr show that “it will be a long time before we reach the end of negotiations with Turkey about accession to the EU.” “Actually, the German government has major doubts about whether Turkey should be a full member of the EU, but this is a question for the coming years,” said Schaeuble. “It is not a worry at the present time.” [..] Erdogan knows that the “EU can’t really stop him from eradicating followers of Gulen to putting Kurdish lawmakers on trial for ties to the PKK,” Nihat Ali Ozcan at the Economic Policy Research Foundation in Ankara said. “The EU’s criticism of Erdogan’s policies is not very meaningful at a time when the country’s membership bid is not high on the public’s agenda, and the reliance of the EU on Turkey to handle the refugee crisis and protect Europe against terrorism leaves more room for Erdogan to pursue his own agenda at home.”

Simmering tensions flare up. Better be careful.

• Turkey Disputes Greek Sovereignty Via NATO Patrols (Kath.)

Turkey is disputing Greece’s territorial sovereignty over a string of tiny islands and a part of its air space over the Aegean Sea, according to a confidential document, obtained by Kathimerini, that was submitted to NATO’s Military Committee last month. The 17-point document, which is expected to further strain relations between the neighboring countries, was submitted on February 15, during heated discussions between Greece and Turkey over the terms of deployment of a German-led NATO patrol in the Aegean to stem the flow of refugees. It was the first time that had Turkey disputed Greek sovereignty via an official NATO document.

Turkey’s demands from the Alliance included replacing the term “Aegean air space” with “NATO air space” and refraining from using the Greek names of several tiny islands “that may been seen as the promotion of national interest” – an apparent reference to 16 small islets whose Greek sovereignty has been repeatedly disputed by Ankara. Turkey also disputed Greece’s 10-mile national air space and demanded permission to enter the Athens Flight Information Region (FIR) without submitting flight plans. It further requested that NATO ships do not dock at ports of the Dodecanese islands in the southeast Aegean and claimed supervision of almost half the Aegean Sea for search and rescue operations.

The terms of the NATO patrol in the Aegean were agreed on February 25 after overcoming territorial sensitivities of the two neighbors. The agreement stipulated that the two countries would not operate in each other’s territorial waters and air space. According to several NATO diplomats, one of the stumbling blocks had been where Greek and Turkish ships should patrol and whether that would set a precedent for claims over disputed territorial waters. EU leaders will hold a special meeting Monday in a bid to hammer out a deal that would help contain the number of refugees entering Greece and the rest of the EU.

They’re really planning to do it: turn Greece into a concentration camp. This will not go well.

• EU To Focus On Greek Aid, Closing Balkan Migrant Route At Summit (AP)

European Union leaders will be looking to boost aid to Greece as the Balkan migrant route is effectively sealed, using Monday’s summit as an attempt to restore unity among the 28 member nations after months of increasing bickering and go-it-alone policies, according to a draft statement Sunday. The leaders will also try to persuade Turkey’s prime minister to slow the flow of migrants travelling to Europe and take back thousands who don’t qualify for asylum. In a draft summit statement produced Sunday and seen by The Associated Press, the EU leaders will conclude that “irregular flows of migrants along the Western Balkans route are coming to an end; this route is now closed.”

Because of this, the statement added that “the EU will stand by Greece in this difficult moment and will do its utmost to help manage the situation.” “This is a collective EU responsibility requiring fast and efficient mobilization,” it said in a clear commitment to end the bickering. It said that aid to Greece should centre on urgent humanitarian aid as well as managing its borders and making sure that migrants not in need of international protections are quickly returned to Turkey. The statement will be assessed by the 28 leaders after they have met with Turkish Prime Minister Ahmet Davutoglu. Late Sunday evening, German Chancellor Angela Merkel and Dutch Premier Mark Rutte met with Davutoglu to prepare for the summit.

[..] The EU summit, the second of three in Brussels in just over a month, comes just days after a Turkish court ordered the seizure of the opposition Zaman newspaper. The move has heightened fears over deteriorating media freedom in the country and led to calls for action from the international community, but they will most likely be brushed aside at the high-stakes talks. “In other words, we are accepting a deal to return migrants to a country which imprisons journalists, attacks civil liberties, and with a highly worrying human rights situation,” said Guy Verhofstadt, leader of the ALDE liberal group in the European Parliament on Sunday.

“We will continue to save lives … and defend the human face of Europe.”

• Tsipras: “We Will Continue To Save Lives” (Reuters)

Greece will press for solidarity with refugees and fair burden-sharing among European Union states at Monday’s emergency EU summit with Turkey, Prime Minister Alexis Tsipras said on Sunday, lashing out at border restrictions that led to logjams. Tsipras has accused Austria and Balkan countries of “ruining Europe” by slowing the flow of migrants and refugees heading north from Greece, where some 30,000 are now trapped, waiting for Macedonia to reopen its border so they can head to Germany. With more arriving in the mainland from Greek islands close to Turkish shores, the numbers could swell by 100,000 by the end of this month, EU Migration Commissioner Dimitris Avramopoulos projected on Saturday. “Europe is in a nervous crisis,” Tsipras told his leftist Syriza party’s central committee. “Will a Europe of fear and racism overtake a Europe of solidarity?”

He said central European countries with serious demographic problems and low unemployment could benefit in the long term by taking in millions of refugees, but austerity policies have fed a far-right “monster” opposing the inflows. “Europe today is crushed amidst austerity and closed borders. It keeps its border open to austerity but closed for people fleeing war,” Tsipras said. “Countries, with Austria in the front, want to impose the logic of fortress Europe.” Austrian Chancellor Werner Faymann has urged Germany to set a clear limit on the number of asylum seekers it will accept to help stem a mass influx of refugees that is severely testing European cohesion in the midst of the worst refugee crisis in generations. Tsipras told his party “unilateral” actions to close borders to refugees were condemned by all European institutions. “We are not pointing the finger to any other peoples or countries of Europe. We are against those who succumb to xenophobia and racism,” Tsipras said. “We will continue to save lives … and defend the human face of Europe.”

Merkel is losing her wits: “Greece should have created 50,000 accommodation places for refugees by the end of 2015..” Why Greece, Angela?

• Surge Of 100,000 Refugees Building In Greece (AFP/L)

As EU members continued to bicker, Dimitris Avramopoulos, in charge of migration at the powerful Brussels executive, pointed to upcoming measures, including an overhaul of asylum rules, to help ease tensions. “Hundreds are arriving on a daily basis and Greece is expected to receive another 100,000 by the end of the month,” Avramopoulos told a conference in Athens. Greece lies at the heart of Europe’s greatest migration crisis in six decades after a series of border restrictions on the migrant trail from Austria to Macedonia caused a bottleneck on its soil. Over 30,000 refugees and migrants are now trapped in the country, desperate to head northwards, especially to Germany and Scandinavia. “In a few weeks,” the EU will announce a revision of its asylum regulations to ensure a “fairer distribution of the burden and the responsibility,” Avramopoulous told the conference.

The huge influx of refugees and migrants has caused major divisions within the EU, although European President Donald Tusk on Friday struck an upbeat note about Monday’s summit in Brussels, which will include Turkey. European leaders are expected to use the summit to press Ankara to take back more economic migrants from Greece and reduce the flow of people across the Aegean Sea. Finger-pointing continued within the 28-nation EU bloc on Saturday. German Chancellor Angela Merkel – a key player in the drama – said Greece should have been quicker in preparing to host 50,000 people under an agreement with the European Union in October. “Greece should have created 50,000 accommodation places for refugees by the end of 2015,” Merkel told Bild newspaper in an interview to appear Sunday. “This delay must be addressed as soon as possible as the Greek government must provide decent lodgings to asylum claimants”, she said.

Safe passage is very possible. But we prefer to let them drown.

• Refugee Boat Sinks Off Turkey’s Western Coast, 25 Dead, 15 Rescued (DS)

25 refugees drowned off Turkey’s Aegean coast on Sunday after their boat sank off the western province of Aydin’s district of Didim, Anadolu Agency reported. The Turkish Coast Guard has rescued 15 of the refugees and launched a search and rescue operation to find the other missing refugees with three boats and one helicopter. The total number of refugees is not yet known. The refugees’ nationalities were not immediately released, but they are likely to be Syrians, who comprise the majority of refugees attempting to sneak to the Greek islands from Turkey. Media outlets said three children were among the casualties. It is not known what caused the boat to sink, although a mix of strong winds and boats carrying passengers over their capacities are often the causes of similar tragedies. The local Ihlas News Agency reported that passenger overload was the cause of the disaster.

Home › Forums › Debt Rattle March 7 2016