Lewis Wickes Hine Newsies in St. Louis, N. Broadway and De Soto. 1910

“..this borrowing to fund buybacks and dividends doesn’t last this long and it has never lasted three years..”

• Fed Creates Junk Bond And Stock Market Bubble (SA)

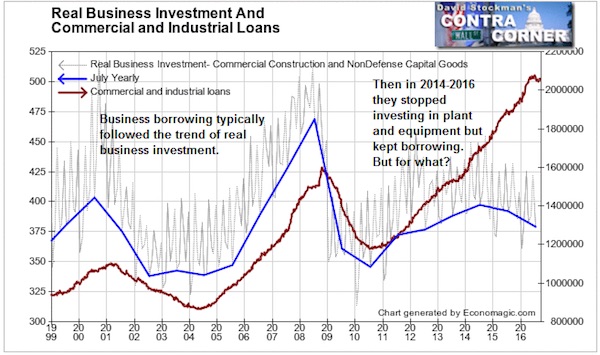

The chart below emphasizes the point that real business investment has declined while commercial and industrial loans are increasing. The leverage in the system is the highest ever as cheap money is not going to the right places. Businesses will only invest in new initiatives if they see sales growth in the future. Low interest rates will not cause a manager to invest in a new initiative. However, managers are still tempted to take the free money, so they pile it into the easiest place: dividends and buybacks.

As you can see, the total payout ratio of dividends and buybacks has exceeded 100% for the past two years. Usually, this borrowing to fund buybacks and dividends doesn’t last this long and it has never lasted three years, so leverage is near its brink.

The chart below shows how levered the balance sheets of corporations are. The leverage on investment-grade balance sheets is at a record high. The three bubbles that you can see in the chart below have all been created by the Federal Reserve’s easy money policies.

Super Clueless Mario surprises himself.

• Draghi Sends Corporate Yields So Negative the ECB Can’t Buy Them (BBG)

The European Central Bank is starting to price itself out of the corporate-bond market as yields plumb such lows that some notes are no longer eligible for its purchase program. ECB President Mario Draghi’s unprecedented buying of corporate debt has sent borrowing costs tumbling to a record and now yields on some securities are so low they fall outside the ECB’s own criteria. Yields on bonds from Paris’s public transport network have already dropped below the threshold of minus 0.4%, while those from Siemens, Europe’s biggest engineering company, France’s train operator SNCF and Sagess, which manages the nation’s strategic oil reserves, are also approaching the cut-off point.

The increasingly negative yields are raising questions about how much more the ECB can do in credit markets to stimulate growth. Yields on €2.6 trillion ($2.9 trillion) of government bonds in Europe have already turned negative after the central bank bought €1.3 trillion of fixed-income assets, including €32 billion of corporate bonds. “This is a sign of how much impact corporate bond buying has had on the credit market,” said Barnaby Martin at Bank of America. “If corporate yields continue to fall, then conceivably it could impact the ECB’s ability to buy bonds. It’s surprising how quickly we’ve reached this situation.”

“When a bubble pops, the first thing that stops is transactions..”

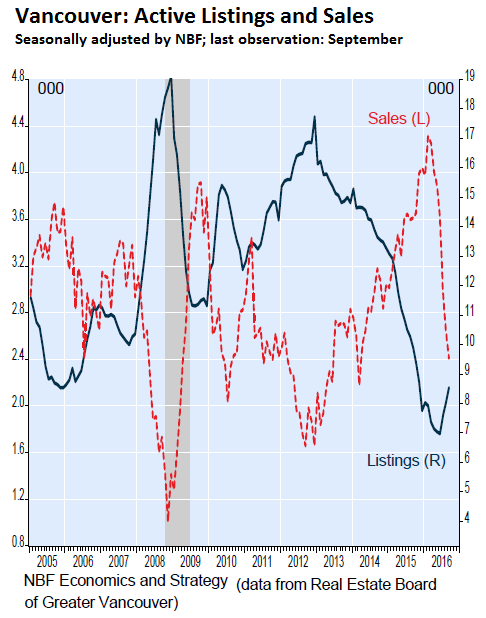

• There’s No Plateau in a Housing Bubble, Not Even in Canada (WS)

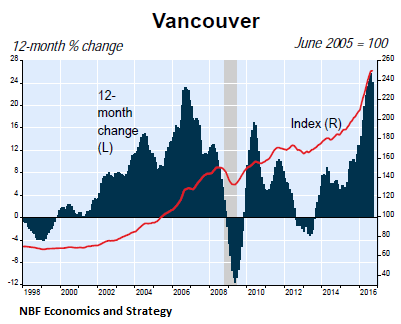

Once enough people are priced out of the housing market, demand collapses. This would normally be where housing bubbles deflate in a very painful manner for lenders, homeowners, and everyone getting their cut, including governments and the real estate industry. But there has been a strong influx of mostly Chinese investors that need to get their money, however they obtained it, out of harm’s way at home, and they pile into the market, and they don’t care what a property costs as long as they think they can sell it for more later. But British Columbia threw a monkey wrench in to the calculus this summer when it adopted a 15% real estate transfer tax and other measures aimed squarely at non-resident investors. It hit home, so to speak.

Total sales in Vancouver plunged 32.5% in September from a year ago, with sales of detached homes falling off a cliff – down 47%. Home sales have fallen every month since their all-time crazy peak in February on a seasonally adjusted basis, for a cumulative decline of 44%, according to Marc Pinsonneault, Senior Economist at Economics and Strategy at the National Bank of Canada. But home prices have not yet fallen, he wrote in the note, “because market conditions have just started to loosen from the tightest conditions on records. We see home price deflation starting soon (10% expected over twelve months).” His chart shows the plunge in sales (red line, left scale, in thousands of units) even as active listings have started to rise (blue line, right scale):

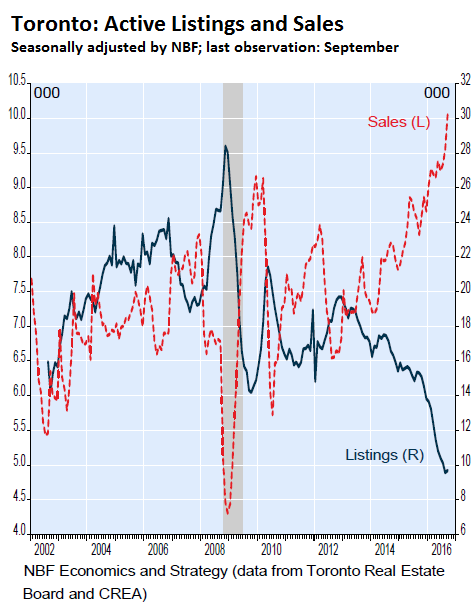

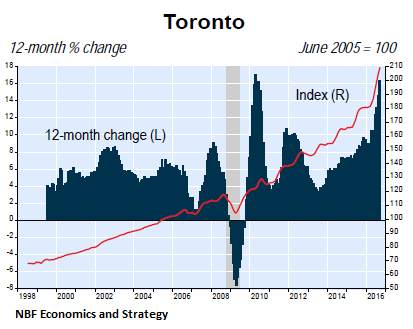

In Toronto, the opposite is happening, with sales spiking on a seasonally adjusted basis way past prior record levels, even as new listings have plunged.

For now, “Toronto is now the red hot market,” explains Pinsonneault: “Home sales broke records in each of the last three months. But the historically low supply (in terms of the number of homes listed for sale) is also contributing to market conditions that are the tightest on records.” But the situation can turn on a dime, as Vancouver demonstrated. When a bubble pops, the first thing that stops is transactions. This happens suddenly. Sellers refuse to cut their prices, while buyers refuse to step up to the plate. Things grind to a halt.

Once sellers are forced to relent on price, transactions start rolling again, at lower prices, and each lower price, due to the metrics of comparable sales, pressures down future prices of other transactions. Once Chinese investors figure out that they’re likely to lose a ton of money in Canadian real estate, because their compatriots who’ve piled into the market before them have already lost a ton of money, they’re going to lose their appetite. This is the hot money. It evaporates suddenly and without a trace. As Vancouver shows, bubbles don’t end in a plateau.

Chasing yield doesn’t look like the best way forward.

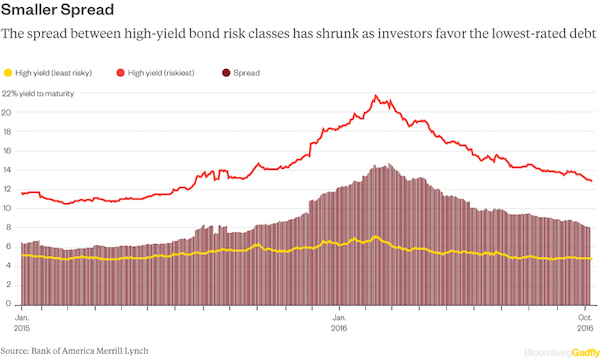

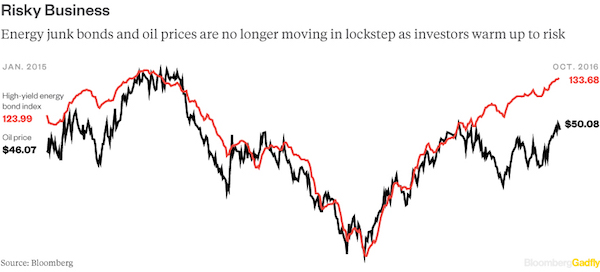

• 30% Junk Rally Gives Traders Heartburn (BBG)

It’s becoming difficult to see how the lowest-rated U.S. junk bonds can continue to rally. They’ve posted their best performance since 2009, with more than a 30% return so far this year. And now investors from Goldman Sachs Asset Management to Highland Capital are starting to become nervous about this debt, and with good reason: If there’s any sort of economic shock at all, these notes are poised to lose a lot. And some sort of shock is entirely possible in the near future. These notes have benefited from two overwhelming factors this year:

1) New stimulus efforts in Japan and Europe have pushed investors into the most-speculative notes, especially those in the U.S.

2) Oil prices have rallied from the lows reached earlier this year, giving some highly indebted energy companies more time to survive after seeing their corporate lives flash before their eyes last year.There are signs that both dynamics are reaching their limits.Central bankers in Europe and Japan are running out of ways to stimulate their economies after deploying negative-rate policies that are eroding the stability of their financial systems. Instead of trying to add stimulus, policy makers in both regions are being forced to tweak existing bond-buying programs to keep them viable. And oil prices have rallied, but not as much as energy junk bonds, which have gained more than 49% since the end of February. This has propelled gains on the broader high-yield market.

[..] current prices aren’t high enough to sustain the current momentum in these bonds. That’s because a “significant amount” of the lowest-rated unsecured bonds of energy companies are pricing in oil at $70 a barrel over the longer term, Jefferies analyst Michael Carley said. Taking a step back, why should the lowest, most-leveraged junk bonds continue to do well? This debt should do best when an economy is steadily growing, interest rates are low and companies have bright futures. But U.S. companies are facing an earnings recession, the Federal Reserve is poised to raise rates again within the next few months and companies are borrowing at a faster pace than they’re increasing their incomes.

The choice China refuses to make; they do both and run only to move backwards.

• China’s Tough Choice: Supporting Growth Or Controlling Debt (CNBC)

China’s economic transition has caused a problem for the government—how to avert a sharp slowdown while keeping a lid on ballooning debt. In a report Thursday, rating agency Standard and Poor’s highlighted the “tough choice between supporting growth and controlling debt sustainability” as China tries to find new ways to fund public investments. “Although aggregate and provincial GDP growth stabilized in the first two quarters of 2016, we believe the fiscal conditions of Chinese local governments are under more pressure given the weakened economy,” S&P analysts wrote in a report. The rising debt pile of local government financing vehicles (LGFV) raised questions on credit risks, said S&P.

“As long as investments remain a growth impetus, it is very hard to shift away from the old public financing model to weaken the LGFVs’ role in public investment,” said S&P credit analyst, Xin Liu. “The growing pile of LGFV debt will add to the fiscal vulnerability of local governments, which already rely on these financing vehicles to execute public investment mandates,” she added. S&P’s warning on local government debt comes amid concerns about overall debt levels in the country as the world’s second-largest economy begins to slow after years of boisterous growth. Corporate debt is also under focus. In another report released on Tuesday, S&P warned that the “unabated growth” of China’s corporate debt could cost the country’s bank “dearly”.

It said the current growth rate of China’s debt “is not sustainable for long”. S&P said if the growth in debt doesn’t slow, the ratio of problem credit to total credit facing China’s banks could triple to 17% by 2020. The banks may then need to raise fresh capital of up to 11.3 trillion Chinese yuan ($1.7 trillion), which is equivalent to 16% of China’s 2015 nominal GDP. The Bank of International Settlements warned recently excessive credit growth in China will increase the country’s risk of a banking crisis in the next three years.

A plunging reserve currency. What’s not to like?

• China Export Dip Tempts Policy Makers to Keep Weakening Yuan (BBG)

China’s renewed export weakness is coinciding with a clampdown on surging home prices and corporate debt, stoking expectations policy makers will allow further yuan depreciation to buffer the economy. Exports in September dropped the most since February amid anemic global demand (-10%), while imports declined 1.9%, leaving a $42 billion trade surplus. Analysts at Bank of America, RBC and Capital Economics estimate further depreciation for the yuan, already near a six-year low. With S&P Global Ratings and the International Monetary Fund among those warning about the threats from rapid credit expansion, policy makers risk cooling the economy with new property restrictions. But their plan for economic growth of at least 6.5% this year leaves little room for maneuver.

The upshot: a weaker yuan is needed to support an industrial sector that’s returning to profitability as it emerges from four years of deflation. “China is running out of options and letting the yuan go is the lowest-cost option for them,” said Sue Trinh, head of Asia FX strategy at RBC Capital Markets in Hong Kong. “We’ve seen them move in this direction. There’s more work to do.” The yuan is headed for the biggest weekly decline since January as mainland markets returned from holiday to face intensified depreciation pressures from a rising dollar. The yuan has dropped 3.4% against the dollar this year, the biggest decline in Asia. While depreciation’s not helping exporters in dollar terms, it cushions the blow when their shipments are counted in local currency terms, underpinning a recovery in industrial profits.

What’s Chinese for whack-a-mole?

• Shanghai Banks Told To Limit Loans To Property Developers (R.)

Banks in China’s financial hub Shanghai have been asked by authorities to limit loans to property developers for land purchases and to scrutinize would-be borrowers suspected of trying to access mortgages by getting divorced, the Shanghai Daily reported on Friday. The steps were the latest in a string of measures around the country to try to cool a property market seen at risk of overheating. Quoting unidentified commercial bankers, the newspaper said banks were told that housing developers should pay at least 30% down on residential projects instead of relying on bank loans.

It said some developers had put only 10% down on projects and raised the remaining funds through bank and gray-market loans. Banks were also asked to reject mortgage applications of people who had divorced within three months, it quoted an internal filing from a Shanghai-based rural commercial bank as saying. A property price rally has prompted a home buying frenzy in parts of China, in some cases prompting couples to get divorced to circumvent buying restrictions and invest in multiple homes. Police last month detained seven property agents in Shanghai for spreading rumours of plans for a new government regulation that caused a rash of divorces and a rush to buy new homes.

More cause for finger pointing.

• Standard & Poor’s Warns On UK Reserve Currency Status As Brexit Hardens (AEP)

Britain is in danger of misreading the political landscape in Europe and faces the possible loss of its reserve currency status if it fails to secure full access to the European single market, Standard & Poor’s has warned. The powerful US rating agency said the British government is treading into hazardous waters in negotiations with the EU and is risks serious damage to economy’s future growth trajectory, with long-term implications for the debt profile and the country’s credit-worthiness. S&P fears that loss of unfettered access to the single market would have incalculable consequences for business, yet the Government so far appears almost insouciant about this.

“There seems to be this view that ‘we’re a big important economy, the Europeans export a lot to us, so they have got to give us what we want’, but is that really true?” said Ravi Bhatia, the director of sovereign ratings in charge of Britain. “Individually most of these countries don’t export that much to the UK, and were seeing a hardening of attitudes,” he said. Mr Ravi said Britain has limited scope for a spree on infrastructure projects and is walking a fine line on budget policy. “Before Brexit, the trajectory was planned fiscal consolidation, but we’re no longer certain we’re going to see that,” he said. “If they ramp up fiscal spending they’ll get a stimulus and that is good in one way as it will help boost growth, but they have to finance that spending; it will raise the deficit, and the debt stock is already high,” he told the Daily Telegraph.

Standard & Poor’s stripped Britain of its AAA status immediately after the Brexit vote in June, slashing the rating by two notches to AA, although the move was well-flagged in advance. It described the vote as seminal event that would lead to a “less predictable, stable, and effective policy framework in the UK”. The agency will issue its next verdict at the end of this month. Any further downgrade at this delicate juncture would be more serious, amounting to a red card on the Government’s hard-nosed rhetoric and negotiating tactics It is unprecedented for a AAA state to lose three notches in a matter on months.

First they invite them in…

• Hundreds Of Properties Could Be Seized In UK Corruption Crackdown (G.)

Hundreds of British properties suspected of belonging to corrupt politicians, tax evaders and criminals could be seized by enforcement agencies under tough new laws designed to tackle London’s reputation as a haven for dirty money. Huge amounts of corrupt wealth is laundered through the capital’s banks. The National Crime Agency believes up to £100bn of tainted cash could be passing through the UK each year. Much of it ends up in real estate, and in other assets such as luxury cars, art and jewellery. The criminal finances bill, published on Thursday, is designed to close a loophole which has left the authorities powerless to seize property from overseas criminals unless the individuals are first convicted in their country of origin.

It will introduce the concept of “unexplained wealth orders”. The Serious Fraud Office, HM Revenue and Customs and other agencies will be able to apply to the high court for an order forcing the owner of an asset to explain how they obtained the funds to purchase it. The orders will apply to property and other assets worth more than £100,000. If the owner fails to demonstrate that a home or piece of jewellery was acquired using legal sources of income, agencies will be able to seize it. The law targets not just criminals, but politicians and public officials, known as “politically exposed persons”. Depending on how quickly it passes through parliament, the bill could come into force as early as spring 2017.

“There are some hundreds of properties in the UK strongly suspected to have been acquired with the proceeds of corruption,” said the campaign group Transparency International, which has been pressing for the new measures. “This will provide low-hanging fruit for immediate action by law enforcement agencies, if those agencies are properly resourced.”

Whaddayaknow? The WSJ has a Trump story that’s not about genitals. Surrounding yourself with people who don’t agree with you is often not a bad sign.

• Some of Donald Trump’s Economic Team Diverge From Candidate (WSJ)

Advisers concede there is a tug-of-war between the supply-siders and the protectionists, but Mr. Kudlow said he saw similar disagreements in the White House as a budget official for President Ronald Reagan. And Mr. Navarro, whose trade skepticism closely reflects Mr. Trump’s public views, said the campaign is “very much united” on trade. When Mr. Navarro ran for Congress two decades ago, Hillary Clinton, then the first lady, campaigned at one of his San Diego rallies. “Pure serendipity—sweet manna from heaven,” he wrote in a book recounting the campaign. He sought to oust the Republican incumbent by making the race a referendum on then-GOP House Speaker Newt Gingrich. Last month, Mr. Navarro flew with Messrs. Trump and Gingrich to a rally in Fort Myers, Fla. He now says he was “seduced” by the Clintons and “over time, that seduction has turned into betrayal and ultimately disbelief.”

Other top advisers include David Malpass, a Reagan administration official, who as chief economist of Bear Stearns in 2007 dismissed concerns that the housing sector would take the economy into a recession, let alone cause the financial crisis that brought down his bank. When he first met Mr. Trump before a rally in an airplane hangar at Dallas’ Love Field last year, conservative economist Stephen Moore pushed back against Mr. Trump’s invitation to join the campaign. “I can’t work for you because I’m free trade, and I know you’re more of a protectionist,” Mr. Moore recalled saying. Mr. Trump said they could “agree to disagree on that issue,” Mr. Moore said. Advisers say Mr. Trump’s decision to hire people he doesn’t fully agree with shows maturity. “Hillary is more like the red army, with everyone marching in lockstep,” said Mr. Kudlow.

No. 1 concern in Berlin and Brussels.

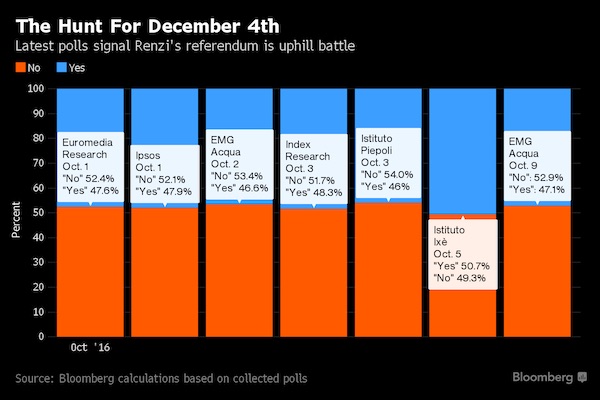

• Renzi Gambles All on Referendum Haunted by Weak Italian Economy (BBG)

Italians are about to have their say on Prime Minister Matteo Renzi and the economy isn’t doing him any favors. When the country holds a referendum on a key constitutional change Dec. 4, many voters will have more than “Yes” or “No” on their mind. They’ll probably take the opportunity to vent their frustration over the snail’s pace of growth after the latest recession. [..] All but one of Italy’s main polling firms signaled this month that “No” will prevail in the referendum, with surveys saying on average that the reform will be rejected by 52.2% of voters, up from 50.4% in September. To make things potentially worse for Renzi, just three days before the vote, Italians will learn whether the recovery resumed after stalling in the three months through June, when the national statistics office publishes its final reading of third quarter GDP.

“We might go to the polling stations in the wake of a negative GDP figure,” said Alberto Bagnai, who teaches economics at Gabriele d’Annunzio University in Pescara. “That could have a direct impact on the vote.” While recent industrial data have exceeded expectations, confidence among households and executives about the outlook is not very optimistic. Renzi himself acknowledged that economic concerns might influence voters and has tried to reassure them. Last week, the premier and his Finance Minister Pier Carlo Padoan repeatedly defended the government’s above-consensus target of 1% growth next year. The central bank called the goal “very optimistic” – a code phrase signaling difficulties ahead.

A sorrowful bunch.

• Walloon Revolt Against Canada Deal Torpedoes EU Trade Policy (Pol.)

The EU’s once-mighty trade negotiators never dreamed that their powers would be stripped from them so unceremoniously – and possibly for good. The Francophone parliament of the Federation of Wallonia-Brussels – only 10 minutes’ walk from EU headquarters — stands to win a place in history for sinking the EU’s landmark trade deal with Canada and potentially for scuppering the European Commission’s ability to lead the world’s biggest trade bloc for many years. Failure to conclude the Comprehensive Economic and Trade Agreement (CETA) by this month’s deadline would be a devastating blow to the EU, which has spent seven years working on the tariff-slicing agreement with Ottawa.

“It’s crazy. If we allow a regional parliament to block a trade deal that will benefit the whole EU, where does this lead us to?” said Christoph Leitl, president of the Global Chamber Platform, a worldwide alliance of business chambers. “CETA is not just a deal with Canada, it has model character for Europe’s future trade relations.” The Federation of Wallonia-Brussels parliament, which focuses on the cultural and educational concerns of 4.5 million French speakers in Belgium, voted Wednesday evening to reject CETA because of worries about public services and agriculture. [..] Unless the Belgian central government can find an imaginative compromise quickly, the EU will be unable to corral the signatures of all 28 EU countries before an EU-Canada summit on October 27.

German efficiency. Send them where you can’t see them.

• Germany Proposes North Africa Centers For Rescued Migrants (AFP)

Migrants rescued at sea should be taken to centers in north Africa where their claims for asylum in EU countries can be studied, German interior minister Thomas de Maiziere proposed Thursday. De Maiziere made the suggestion as he arrived for a Luxembourg meeting of EU interior ministers who are trying to slow the migrant flow from Libya to Italy after a March deal with Turkey sharply reduced the influx to Greece, the main entry point for Europe last year. “People who are rescued in the Mediterranean should be brought back to safe accommodation facilities in northern Africa,” de Maiziere told reporters. “Their need for protection would be verified and we would put into place a resettlement to Europe with generous quotas, fairly divided between the European countries,” the minister said.

“The others have to go back to their home countries,” he added. EU countries, confronting populist opposition to refugees, have long feuded over quotas for relocating asylum seekers from Greece and Italy as well as for resettling people from refugee camps. De Maiziere did not mention a specific country in north Africa but EU officials have been discussing efforts to curb the migrant flow with Libya, the main transit point for African migrants heading to Europe. However, Libya’s new national unity government last week rejected calls from some EU countries to build refugee camps on its shores, saying the bloc could not “shirk its responsibility” while it struggled to restore peace and stability.

Encore.

• There’s No Plateau in a Housing Bubble, Not Even in Canada (WS)

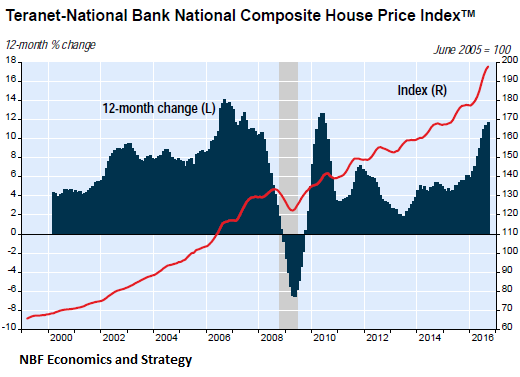

Canadian house prices jumped 11.7% in September from a year ago, according to The Teranet–National Bank National Composite House Price Index released today. But the index papers beautifully over the dynamics in each metro. In six of the 11 metro markets of the index, prices have been languishing or even declining over the past couple of years, as they’ve hit the wall of reality after often stupendous price gains in the prior decade: Montreal, Calgary, Edmonton, Quebec City, Halifax, and Ottawa-Gatineau. In the two largest markets – Toronto and Vancouver, which combined account for 54% of the index – prices have blown through the roof. Both markets are among the hottest, most over-priced housing bubbles in the world.

UBS recently ranked Vancouver Number 1 globally on that honor roll. But suddenly the dynamics have changed. Vancouver’s housing market is in turmoil, to use a mild word, as sales have crashed, after the implementation of a real-estate transfer tax this summer by British Columbia, aimed squarely at non-resident investors. In Vancouver, those investors are mostly Chinese. And where do these folks now go to inflate prices? Toronto. Still, the national house price index (red line, right scale), after the 11.7% jump over the past 12 months (blue columns, left scale), has doubled since 2005!

The index, similar to the Case-Shiller Home Price index in the US, is based on repeat sales. It looks at properties that sold at least twice over the years to establish “sales pairs.” It then uses a proprietary formula to deduct price changes from these transactions and extrapolate them into an index for each of the 11 markets and nationally. It’s not perfect, but it offers an alternative view to median prices or Canada’s “benchmark” prices. Prices in Toronto have been spiking (red line, right scale), with double-digit year-over-year%age gains (blue columns, left scale) so far this year, including a breath-taking 16% in September.

Vancouver makes Toronto look practically tame. Vancouver went completely crazy, with year-year-over price gains reaching 26% in the summer. Now a new reality went into effect. Market activity has collapsed, as no one knows what anything is worth, with buyers and sellers jockeying for position. And on a monthly basis, the index was essentially flat (+0.2%):

Most Canadians have not seen their incomes rise anywhere near the rate of the house price inflation of the past many years, if their incomes rose at all. Thus, many of them have been priced out of the housing market, or have access to it only via highly risky financing schemes that put both lenders and borrowers at risk, despite historically low interest rates. Once enough people are priced out of the housing market, demand collapses. This would normally be where housing bubbles deflate in a very painful manner for lenders, homeowners, and everyone getting their cut, including governments and the real estate industry. But there has been a strong influx of mostly Chinese investors that need to get their money, however they obtained it, out of harm’s way at home, and they pile into the market, and they don’t care what a property costs as long as they think they can sell it for more later.

Home › Forums › Debt Rattle October 14 2016