Unknown GMC truck Associated Oil fuel tanker, San Francisco 1935

So there.

• I Don’t Think The US Should Remain As One Political Entity – Casey (IM)

What’s going on in the US now is a culture clash. The people that live in the so-called “red counties” that voted for Trump—which is the vast majority of the geographical area of the US, flyover country—are aligned against the people that live in the blue counties, the coasts and big cities. They don’t just dislike each other and disagree on politics; they can no longer even have a conversation. They hate each other on a visceral gut level. They have totally different world views. It’s a culture clash. I’ve never seen anything like this in my lifetime.

There hasn’t been anything like this since the War Between the States, which shouldn’t be called “The Civil War,” because it wasn’t a civil war. A civil war is where two groups try to take over the same government. It was a war of secession, where one group simply tries to leave. We might have something like that again, hopefully nonviolent this time. I don’t think the US should any longer remain as one political entity. It should break up so that people with one cultural view can join that group and the others join other groups. National unity is an anachronism.

Credibility.

• Trump Tantrum Looms On Wall Street If Healthcare Effort Stalls (R.)

The Trump Trade could start looking more like a Trump Tantrum if the new U.S. administration’s healthcare bill stalls in Congress, prompting worries on Wall Street about tax cuts and other measures aimed at promoting economic growth. Investors are dialing back hopes that U.S. President Donald Trump will swiftly enact his agenda, with a Thursday vote on a healthcare bill a litmus test which could give stock investors another reason to sell. “If the vote doesn’t pass, or is postponed, it will cast a lot of doubt on the Trump trades,” said the influential bond investor Jeffrey Gundlach, chief executive at DoubleLine Capital. U.S. stocks rallied after the November presidential election, with the S&P 500 posting a string of record highs up to earlier this month, on bets that the pro-growth Trump agenda would be quickly pushed by a Republican Party with majorities in both chambers of Congress.

The S&P 500 ended slightly higher on Wednesday, the day before a floor vote on Trump’s healthcare proposal scheduled in the House of Representatives. On Tuesday, stocks had the biggest one-day drop since before Trump won the election, on concerns about opposition to the bill. Investors extrapolated that a stalling bill could mean uphill battles for other Trump proposals. Trump and Republican congressional leaders appeared to be losing the battle to get enough support to pass it. Any hint of further trouble for Trump’s agenda, especially his proposed tax cut, could precipitate a stock market correction, said Byron Wien, veteran investor and vice chairman of Blackstone Advisory Partners. “The fact that they are having trouble with (healthcare repeal) casts a shadow over the tax cut and the tax cut was supposed to be the principal fiscal stimulus for the improvement in real GDP,” Wien said. “Without that improvement in GDP, earnings aren’t going to be there and the market is vulnerable.”

“This is particularly interesting because student loans essentially have no collateral.”

• The US Student Debt Bubble Is Even Bigger Than The Subprime Fiasco (Black)

In 1988, a bank called Guardian Savings and Loan made financial history by issuing the first ever “subprime” mortgage bond. The idea was revolutionary. The bank essentially took all the mortgages they had loaned to borrowers with bad credit, and pooled everything together into a giant bond that they could then sell to other banks and investors. The idea caught on, and pretty soon, everyone was doing it. As Bethany McLean and Joe Nocera describe in their excellent history of the financial crisis (All the Devils are Here), the first subprime bubble hit in the 1990s. Early subprime lenders like First Alliance Mortgage Company (FAMCO) had spent years making aggressive loans to people with bad credit, and eventually the consequences caught up with them. FAMCO declared bankruptcy in 2000, and many of its competitors went bust as well.

Wall Street claimed that it had learned its lesson, and the government gave them all a slap on the wrist. But it didn’t take very long for the madness to start again. By 2002, banks were already loaning money to high-risk borrowers. And by 2005, all conservative lending standards had been abandoned. Borrowers with pitiful credit and no job could borrow vast sums of money to buy a house without putting down a single penny. It was madness. By 2007, the total value of these subprime loans hit a whopping $1.3 trillion. Remember that number. And of course, we know what happened the next year: the entire financial system came crashing down. Duh. It turned out that making $1.3 trillion worth of idiotic loans wasn’t such a good idea. By 2009, 50% of those subprime mortgages were “underwater”, meaning that borrowers owed more money on the mortgage than the home was worth.

In fact, delinquency rates for ALL mortgages across the country peaked at 11.5% in 2010, which only extended the crisis. But hey, at least that’s never going to happen again. Except… I was looking at some data the other day in a slightly different market: student loans. Over the last decade or so, there’s been an absolute explosion in student loans, growing from $260 billion in 2004 to $1.31 trillion last year. So, the total value of student loans in America today is LARGER than the total value of subprime loans at the peak of the financial bubble. And just like the subprime mortgages, many student loans are in default. According to the Fed’s most recent Household Debt and Credit Report, the student loan default rate is 11.2%, almost the same as the peak mortgage default rate in 2010. This is particularly interesting because student loans essentially have no collateral. Lenders make loans to students… but it’s not like the students have to pony up their iPhones as security.

You have to wonder what exactly is keeping the US economy afloat.

• US Auto-Loan Quality To Deteriorate Further, Forcing Tighter Underwriting (MW)

Auto loan and lease credit performance will continue to deteriorate in 2017, led by the vulnerable subprime sector, Fitch Ratings said in a report released Wednesday. “Subprime credit losses are accelerating faster than the prime segment, and this trend is likely to continue as a result of looser underwriting standards by lenders in recent years,” said Michael Taiano, a director at the credit-ratings agency. Banks are starting to lose market share to captive auto finance companies and credit unions as they begin to tighten underwriting standards in response to deteriorating asset quality, Fitch said. According to the Federal Reserve’s January 2017 senior loan officer survey, 11.6% of respondents (net of those who eased) reported tightening standards, compared with the five-year average of 6.1%.

“This trend is consistent with comments made by several banks on earnings conference calls over the past couple of quarters,” Fitch said in the report. Fitch considers continued tightening by auto lenders as a credit-positive but it’s also paying attention to market nuances. The tightening, to date, primarily relates to pricing and loan-to-value (how much is still owed on the car compared to its resale value), but average loan terms continue to extend into the 72- to 84-month category. “The tightening of underwriting standards is likely a response to expected deterioration in used vehicle prices and the weaker credit performance experienced in the subprime segment,” added Taiano. Used-car price declines have accelerated more recently, which will likely pressure recovery values on defaulted loans and lease residuals, the analysts said.

Might as well call off the theater.

• Oil Price Drops Below $50 For First Time Since OPEC Deal (Tel.)

The oil price has fallen back below the key $50 a barrel mark for the first time since November after surging US oil supplies dealt a blow to OPEC’s plan to erode the global oversupply of crude. The flagging oil price bounded above $50 a barrel late last year after a historic co-operation deal between OPEC and the world’s largest oil producers outside of the cartel to limit output for the first half of this year. The November deal was the first action taken by the group to limit supply for over eight years but since then the quicker than expected return of fracking rigs across the US has punctured the buoyant market sentiment of recent months. Brent crude prices peaked at $56 a barrel earlier this year and were still above $52 this week.

But by Wednesday the price fell to just above $50 a barrel and briefly broke below the important psychological level to $49.86 on Wednesday afternoon. Market analysts fear that a more sustained period below $50 could trigger a sell-off from hedge funds which would drive even greater losses in the market. The price plunge was sparked by the latest weekly US stockpile data which revealed a bigger than expected increase of 5 million barrels a day compared to a forecast rise of 1.8 million barrels. The flood of US shale emerged a day after Libya announced that would increase its output to take advantage of higher revenues from its oil exports. “The market is increasingly worried that the continued overhang of supply is not being brought down fast enough,” said Ole Hansen, a commodities analyst with SaxoBank.

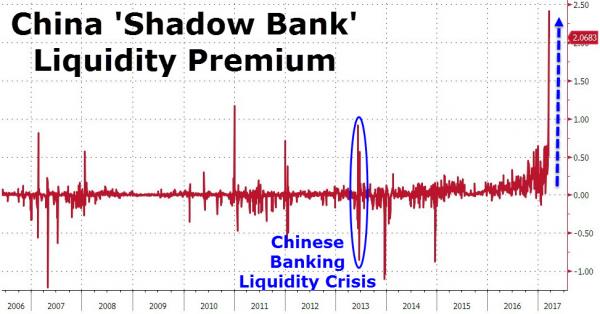

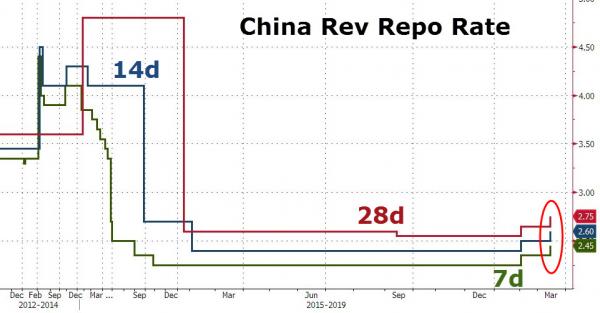

Beijing forced to save the shadows.

• China Shadow Banks Hit by Record Premium for One-Week Cash (ZH)

During the so-called Chinese Banking Liquidity Crisis of 2013, the relative cost of funds for non-bank institutions spiked to 100bps. So, the fact that the ‘shadow banking’ liquidity premium has exploded to almost 250 points – by far a record – in the last few days should indicate just how stressed Chinese money markets are. While interbank borrowing rates have climbed across the board, the surge has been unusually steep for non-bank institutions, including securities companies and investment firms. They’re now paying what amounts to a record premium for short-term funds relative to large Chinese banks, according to data compiled by Bloomberg.

The premium is reflected in the gap between China’s seven-day repurchase rate fixing and the weighted average rate, which, by Bloomberg notes, widened to as much as 2.47 percentage points on Wednesday after some small lenders were said to miss payments in the interbank market. Non-bank borrowers tend to have a greater influence on the fixing, while large banks have more sway over the weighted average. “It’s more expensive and difficult for non-bank financial institutions to get funding in the market,” said Becky Liu at Standard Chartered. “Bigger lenders who have access to regulatory funding are not lending much of the money out.” Without access to deposits or central bank liquidity facilities, many of China’s non-bank institutions must rely on volatile money markets. As Bloomberg points out, The People’s Bank of China has been guiding those rates higher in recent months to encourage a reduction of leverage, while also stepping in at times to prevent a liquidity crunch.

State owned zombies.

• Zombie Companies are China’s Real Problem (BBG)

China needs to take on its state-owned “zombie companies,” which keep borrowing even though they aren’t earning enough to repay loans or interest, says Nicholas Lardy of the Peterson Institute for International Economics. “That’s where the real problem is,” Lardy said Thursday in a Bloomberg Television interview from the Boao Forum for Asia, an annual conference on the southern Chinese island of Hainan. “It’s a component of the run-up in debt that they really have to focus on.” While flagging this concern, Lardy, a senior fellow at Peterson in Washington and author of “Markets Over Mao: The Rise of Private Business in China,” said anxiety over China’s debt growth is overstated. Household deposits will continue to underpin the banking and financial system, which means the situation with zombie firms is unlikely to reach a critical point.

Household savings are “very sticky, they’re not going anywhere, and the central bank can come in to the rescue if there are problems,” he said. Chinese corporate profits will probably continue to recover this year and after-tax earnings needed to service the debt load is improving, Lardy said. Another positive sign is a slowdown in the buildup of debt outstanding to non-financial companies. The combination of that slackening and companies’ increasing earning power “is improving the overall situation,” he said. When it comes to U.S. President Donald Trump’s negative rhetoric on China, the country’s leaders deserve “very high marks so far” for their cool reaction. “They’ve been waiting to see what Mr. Trump is actually going to do as opposed to what he’s talked about, so they haven’t overreacted,” he said. “They’ve made very careful preparations for the worst case if Trump does move in a very strong protectionist direction.”

Zombies and junk.

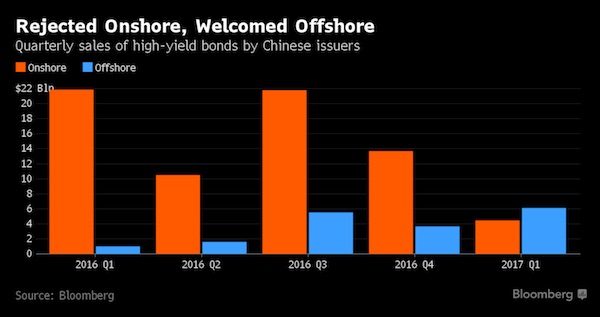

• China Debt Risks Go Global Amid Record Junk Sales Abroad (BBG)

China’s riskiest corporate borrowers are raising an unprecedented amount of debt overseas, leaving global investors to shoulder more credit risks after onshore defaults quadrupled in 2016. Junk-rated firms, most of which are property developers, have sold $6.1 billion of dollar bonds since Dec. 31, a record quarter, data compiled by Bloomberg show. In contrast, such borrowers have slashed fundraising at home as the central bank pushes up borrowing costs and regulators curb real estate financing. Onshore yuan note offerings by companies with local ratings of AA, considered junk in China, fell this quarter to the least since 2011 at 31.3 billion yuan ($4.54 billion). Global investors desperate for yield have lapped up offerings from China. Rates on dollar junk notes from the nation have dropped 81 basis points this year to 6.11%, near a record low, according to a Bank of America Merrill Lynch index.

Some investors have warned of froth. Goldman Sachs Group Inc. said last month that it sees little value in the country’s high-yield property bonds. Hedge fund Double Haven Capital (Hong Kong) has said it is betting against Chinese junk securities. “Today’s market valuations are tight and investors are focusing on yields without taking into account credit risks,” said Raja Mukherji at PIMCO. “That’s where I see a lot of risk, where investors are not differentiating on credit quality on a risk-adjusted basis.” Lower-rated issuers turning to dollar debt after scrapping financing at home include Shandong Yuhuang Chemical on China’s east coast. The chemical firm canceled a 500 million yuan local bond sale in January citing “insufficient demand.” It then issued $300 million of three-year bonds at 6.625% this week. Some developers have grown desperate for cash as regulators tighten housing curbs and restrict their domestic fundraising. That’s raising concern among international investors in China’s real estate sector who have been burned before.

Priceless humor: “Congress has already raised the alarm.” After three decades, that is.

• A Fake $3.6 Trillion Deal Is Easy to Sneak Past the SEC

A few hours after the New York market close on Feb. 1, an obscure Chicago artist by the name of Antonio Lee told the world he had become the world’s richest man. The 32-year-old painter said Google’s parent, Alphabet Inc., had bought his art company in exchange for a chunk of stock that made him wealthier than Bill Gates, Warren Buffett and Jeff Bezos – combined. Of course, none of it was true. Yet, on that day, Lee managed to issue his fabricated report in the most authoritative of places: The U.S. Securities and Exchange Commission’s Edgar database – the foundation of hundreds of billions of dollars in financial transactions each day. For more than three decades, the SEC has accepted online submissions of regulatory filings – basically, no questions asked.

As many as 800,000 forms are filed each year, or about 3,000 per weekday. But, in a little known vulnerability at the heart of American capitalism, the government doesn’t vet them, and rarely even takes down those known to be shams. “The SEC can’t stop them,” said Lawrence West, a former SEC associate enforcement director. “They can only punish the filer afterward and remove the filing from the system. So, caveat lector – let the reader beware.” Congress has already raised the alarm. For its part, the SEC, which declined to comment, has said those who make filings are responsible for their truthfulness and that only a handful have been reported as bogus. Submitting false information exposes the culprit to SEC civil-fraud charges, or even federal criminal prosecution.

On May 14, 2015, Nedko Nedev, a dual citizen of the United States and Bulgaria, filed an SEC form indicating he was making a tender offer – an outright purchase – for Avon, the cosmetics company. Avon’s shares jumped 20% before trading was halted, and the company denied the news. (A federal grand jury later indicted Nedev on market manipulation and other charges.) After the fraudulent Avon filing, U.S. Senator Chuck Grassley, the Iowa Republican and former chairman of the Finance Committee, told the SEC it must review its posting standards. “This pattern of fraudulent conduct is troubling, especially in light of the relative ease in which a fake posting can be made,” Grassley wrote in a letter to the agency. In response, Mary Jo White, who then chaired the SEC, said it wouldn’t be feasible to check information. She noted that there were on average 125 first-time filers daily in 2014, and the agency was studying whether its authentication process could be strengthened without delaying disclosure of key information to investors.

Only a major reset will do.

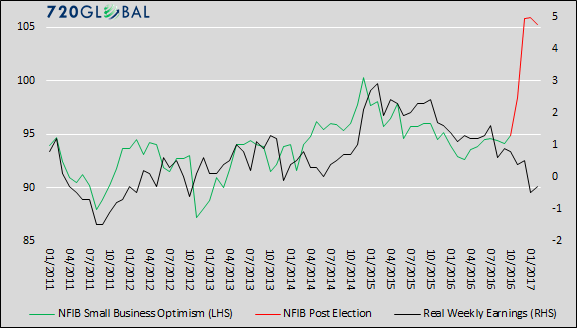

• Elite Economists: Often Wrong, Never In Doubt (720G)

Since the U.S. economic recovery from the 2008 financial crisis, institutional economists began each subsequent year outlining their well-paid view of how things will transpire over the course of the coming 12-months. Like a broken record, they have continually over-estimated expectations for growth, inflation, consumer spending and capital expenditures. Their optimistic biases were based on the eventual success of the Federal Reserve’s (Fed) plan to restart the economy by encouraging the assumption of more debt by consumers and corporations alike. But in 2017, something important changed. For the first time since the financial crisis, there will be a new administration in power directing public policy, and the new regime could not be more different from the one that just departed. This is important because of the ubiquitous influence of politics.

The anxiety and uncertainties of those first few years following the worst recession since the Great Depression gradually gave way to an uncomfortable stability. The anxieties of losing jobs and homes subsided but yielded to the frustration of always remaining a step or two behind prosperity. While job prospects slowly improved, wages did not. Business did not boom as is normally the case within a few quarters of a recovery, and the cost of education and health care stole what little ground most Americans thought they were making. Politics was at work in ways with which many were pleased, but many more were not. If that were not the case, then Donald Trump probably would not be the 45th President of the United States. Within hours of Donald Trump’s victory, U.S. markets began to anticipate, for the first time since the financial crisis, an escape hatch out of financial repression and regulatory oppression.

As shown below, an element of economic and financial optimism that had been missing since at least 2008 began to re-emerge. What the Fed struggled to manufacture in eight years of extraordinary monetary policy actions, the election of Donald Trump accomplished quite literally overnight. Expectations for a dramatic change in public policy under a new administration radically improved sentiment. Whether or not these changes are durable will depend upon the economy’s ability to match expectations.

I find the Trump bashing parade very tiresome, but Matt’s funny.

• Trump the Destroyer (Matt Taibbi)

There is no other story in the world, no other show to watch. The first and most notable consequence of Trump’s administration is that his ability to generate celebrity has massively increased, his persona now turbocharged by the vast powers of the presidency. Trump has always been a reality star without peer, but now the most powerful man on Earth is prisoner to his talents as an attention-generation machine. Worse, he is leader of a society incapable of discouraging him. The numbers bear out that we are living through a severely amplified déjà vu of last year’s media-Trump codependent lunacies. TV-news viewership traditionally plummets after a presidential election, but under Trump, it’s soaring. Ratings since November for the major cable news networks are up an astonishing 50% in some cases, with CNN expecting to improve on its record 2016 to make a billion dollars – that’s billion with a “b” – in profits this year.

Even the long-suffering newspaper business is crawling off its deathbed, with The New York Times adding 132,000 subscribers in the first 18 days after the election. If Trump really hates the press, being the first person in decades to reverse the industry’s seemingly inexorable financial decline sure is a funny way of showing it. On the campaign trail, ballooning celebrity equaled victory. But as the country is finding out, fame and governance have nothing to do with one another. Trump! is bigger than ever. But the Trump presidency is fast withering on the vine in a bizarre, Dorian Gray-style inverse correlation. Which would be a problem for Trump, if he cared. But does he? During the election, Trump exploded every idea we ever had about how politics is supposed to work. The easiest marks in his con-artist conquest of the system were the people who kept trying to measure him according to conventional standards of candidate behavior.

You remember the Beltway priests who said no one could ever win the White House by insulting women, the disabled, veterans, Hispanics, “the blacks,” by using a Charlie Chan voice to talk about Asians, etc. Now he’s in office and we’re again facing the trap of conventional assumptions. Surely Trump wants to rule? It couldn’t be that the presidency is just a puppy Trump never intended to care for, could it? Toward the end of his CPAC speech, following a fusillade of anti-media tirades that will dominate the headlines for days, Trump, in an offhand voice, casually mentions what a chore the presidency can be. “I still don’t have my Cabinet approved,” he sighs. In truth, Trump does have much of his team approved. In the early days of his administration, while his Democratic opposition was still reeling from November’s defeat, Trump managed to stuff the top of his Cabinet with a jaw-dropping collection of perverts, tyrants and imbeciles, the likes of which Washington has never seen.

En route to taking this crucial first beachhead in his invasion of the capital, Trump did what he always does: stoked chaos, created hurricanes of misdirection, ignored rules and dared the system of checks and balances to stop him. By conventional standards, the system held up fairly well. But this is not a conventional president. He was a new kind of candidate and now is a new kind of leader: one who stumbles like a drunk up Capitol Hill, but manages even in defeat to continually pull the country in his direction, transforming not our laws but our consciousness, one shriveling brain cell at a time.

Tourism is a very big source of income for Turkey. Erdogan’s killing it off with a vengeance.

• Erdogan Warns Europeans ‘Will Not Walk Safely’ If Attitude Persists (R.)

President Tayyip Erdogan said on Wednesday that Europeans would not be able to walk safely on the streets if they kept up their current attitude toward Turkey, his latest salvo in a row over campaigning by Turkish politicians in Europe. Turkey has been embroiled in a dispute with Germany and the Netherlands over campaign appearances by Turkish officials seeking to drum up support for an April 16 referendum that could boost Erdogan’s powers. Ankara has accused its European allies of using “Nazi methods” by banning Turkish ministers from addressing rallies in Europe over security concerns. The comments have led to a sharp deterioration in ties with the European Union, which Turkey still aspires to join.

“Turkey is not a country you can pull and push around, not a country whose citizens you can drag on the ground,” Erdogan said at an event for Turkish journalists in Ankara, in comments broadcast live on national television. “If Europe continues this way, no European in any part of the world can walk safely on the streets. Europe will be damaged by this. We, as Turkey, call on Europe to respect human rights and democracy,” he said. Germany’s Frank-Walter Steinmeier used his first speech as president on Wednesday to warn Erdogan that he risked destroying everything his country had achieved in recent years, and that he risked damaging diplomatic ties. “The way we look (at Turkey) is characterized by worry, that everything that has been built up over years and decades is collapsing,” Steinmeier said in his inaugural speech in the largely ceremonial role. He called for an end to the “unspeakable Nazi comparisons.”

Can’t let a little crisis get in the way of your champagne and caviar.

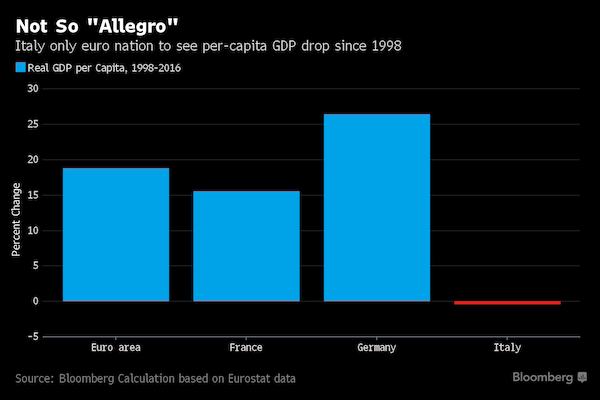

• Lavish EU Rome Treaty Summit Will Skirt Issues in Stumbling Italy (BBG)

As leaders celebrate the European Union’s 60th birthday in Rome this weekend, the host nation may be hoping that a pomp-filled ceremony distracts from any probing questions. Overshadowed by the sting of Brexit and elections in the Netherlands, France and Germany, Italy’s lingering problems have left it as the weak link among Europe’s powerhouse economies. It’s stumbling through a stop-start slow recovery from a record-long recession, unemployment is twice that of Germany’s, and voters, weary of EU institutions, are flirting with the same kind of populism grabbing attention elsewhere. The gathering on Saturday on the city’s Capitol hill is to celebrate the Treaty of Rome, the bedrock agreement signed on March 25, 1957 for what is now the EU.

From its beginnings as the European Economic Community – with Italy among the six founding members – it has since grown to a union of 28 nations stretching 4,000 kilometers from Ireland in the northwest to Cyprus in the southeast. The U.K. is heading toward a lengthy exit from the EU known as Brexit, raising questions among the remaining 27 about the bloc’s long-term future. “Italy was until very recently at the forefront of the European integration process,” Luigi Zingales, professor of finance at University of Chicago Booth School of Business, said in an interview. “Today it’s undoubtedly Europe’s weakest link.” The economy grew just 0.9% last year, below the euro area’s 1.7%, and unemployment is at 11.9%. A recent EU poll put Italy as the monetary union’s second-most euro-skeptic state after Cyprus with only 41% saying the single currency is “a good thing.” The average in the 19-member euro area is 56%.

That widespread disenchantment may be felt at elections due in about one year. A poll published on Tuesday by Corriere della Sera put support for the Five Star Movement, which calls for a referendum to ditch the euro, at a record 32.3%, well ahead of the ruling Democratic Party. Summit host Prime Minister Paolo Gentiloni has only been in power since December, when Matteo Renzi resigned after losing a constitutional reform referendum. For Zingales, Italy has problems that European policy makers “would rather not talk about now as they don’t want to scare people.” That’s because across the bloc, politicians are still fighting voter resentment over the loss of wealth since the financial crisis, bitterness about bailouts and anger over a perceived increase in inequality. “Sixty years after the signing of the Treaties of Rome, the risk of political paralysis in Europe has never been greater,” Bank of Italy Governor Ignazio Visco told a conference in Rome this month.

The EU can celebrate only because it’s murdering one of its members. Greece needs stimulus but gets the opposite.

• Greek Consumption Slumps Further In 2017 (K.)

The year has started with some alarm bells regarding the course of consumer spending, generating concern not only about the impact on the supermarket sector and industry, but also on the economy in general. In the first week of March the year-on-year drop in supermarket turnover amounted to 15%, while in January the decline had come to 10%. Shrinking consumption is a sure sign that the economic contraction will be extended into another year, given its important role in the economy. The new indirect taxes on a number of commodities, the increased social security contributions, the persistently high unemployment and the ongoing uncertainty over the bailout review talks have hurt consumer confidence and eroded disposable incomes.

In this context, it will be exceptionally difficult to achieve the fiscal targets, especially if the uncertainty goes on or is ended with the imposition of additional austerity measures that would only see incomes shrink further. According to projections by IRI market researchers, supermarket sales in 2017 are expected to decline 3.6% from last year, with the worst-case scenario pointing to a 4.4% drop. Supermarket sales turnover dropped at the steepest rate seen in the crisis years in 2016, down 6.5%, after falling 2.1% in 2015, 1.4% in 2014, 3.5% in 2013 and 3.4% in 2012.

“For a continent that has been at war with itself for 10 centuries and only managed to play nice for the last 30 or so years, it’s foolish to expect these bailouts to last forever.”

• Nine Years Later, Greece Is Still In A Debt Crisis.. (Black)

Greece has had nine different governments since 2009. At least thirteen austerity measures. Multiple bailouts. Severe capital controls. And a full-out debt restructuring in which creditors accepted a 50% loss. Yet despite all these measures GREECE IS STILL IN A DEBT CRISIS. Right now, in fact, Greece is careening towards another major chapter in its never-ending debt drama. Just like the United States, the Greek government is set to run out of money (yet again) in a few months and is in need of a fresh bailout from the IMF and EU. (The EU is code for “Germany”…) Without another bailout, Greece will go bust in July– this is basic arithmetic, not some wild theory. And this matters. If Greece defaults, everyone dumb enough to have loaned them money will take a BIG hit. This includes a multitude of banks across Germany, Austria, France, and the rest of Europe.

Many of those banks already have extremely low levels of capital and simply cannot afford a major loss. (Last year, for example, the IMF specifically singled out Germany’s Deutsche Bank as being the top contributor to systemic risk in the global financial system.) So a Greek default poses as major risk to a number of those banks. More importantly, due to the interconnectedness of the financial system, a Greek default poses a major risk to anyone with exposure to those banks. Think about it like this: if Greece defaults and Bank A goes down, then Bank A will no longer be able to meet its obligations to Bank B. Bank B will suffer a loss as well. A single event can set off a chain reaction, what’s called ‘contagion’ in finance. And it’s possible that Greece could be that event. This is what European officials have been so desperate to prevent for the last nine years, and why they’ve always come to the rescue with a bailout.

It has nothing to do with community or generosity. They’re hopelessly trying to prevent another 2008-style meltdown of the financial system. But their measures have limits. How much longer do Greek citizens accept being vassals of Germany, suffering through debilitating capital controls and austerity measures? How much longer do German taxpayers continue forking over their hard-earned wages to bail out Greek retirees? After all, they’ve spent nine years trying to ‘fix’ Greece, and the situation has only become worse. For a continent that has been at war with itself for 10 centuries and only managed to play nice for the last 30 or so years, it’s foolish to expect these bailouts to last forever. And whether it’s this July or some date in the future, Greece could end up being the catalyst which sets off a chain reaction on both sides of the Atlantic.

It’s time for lawyers to step in.

• In Greece, Europe’s New Rules Strip Refugees Of Right To Seek Protection (K.)

EU leaders are celebrating a year since they carved out the agreement with Turkey that stemmed the flood of refugees seeking to escape war and strife on Europe’s doorstep. But the importance of the agreement goes far beyond the fact that it has contributed to deterring refugees from coming to Greece. At the Norwegian Refugee Council, we fear that the system Europe is putting in place in Greece is slowly stripping people of their right to seek international protection. Greece took the positive step to enshrine in law some key checks and balances to protect the vulnerable – a victim of torture, a disabled person, an unaccompanied child – so they could have their asylum case heard on the Greek mainland rather than remaining on the islands.

But a European Commission action plan is putting Greece under pressure to change safeguards enshrined in Greek law. NRC, along with other human rights and humanitarian organizations, wrote an open letter to the Greek Parliament this month urging lawmakers to keep that protection for those most in need. Importantly, this is just another quiet example of how what is happening in Greece is setting precedents that may irrevocably change the 1951 Refugee Convention. Europe is testing things out in Greece. [..] It was Europe and its postwar crisis that led to the 1951 convention that protects those displaced by war. Now that convention risks expiring on the doorstep of the same continent that gave birth to it – Europe is in danger of becoming, as NRC’s Secretary-General Jan Egeland has said, the convention’s “burial agent.”

Home › Forums › Debt Rattle March 23 2017