New York City Under 26 Inches Of Snow, 1947

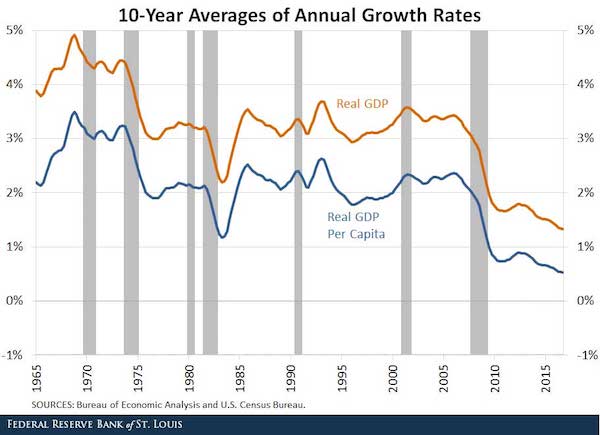

Even though the St. Louis Fed people can’t seem to read their own numbers properly, or at least interpret them, here it is. As the Automatic Earth has said for many years: the peak of our wealth was sometime in the 1970’s or even late 1960’s.

Everything after that was borrowed or printed. Here’s the proof. Sent this to Nicole earlier saying ‘We’ve been vindicated by the Fed itself.’ “Real GDP growth fell and leveled off in the mid-1970s, then started falling again in the mid-2000s”

• Why Does Economic Growth Keep Slowing Down? (StLouisFed)

The U.S. economy expanded by 1.6% in 2016, as measured by real GDP. Real GDP has averaged 2.1% growth per year since the end of the last recession, which is significantly smaller than the average over the postwar period (about 3% per year). These lower growth rates could in part be explained by a slowdown in productivity growth and a decline in factor utilization. However, demographic factors and attitudes toward the labor market may also have played significant roles. The figure below shows a measure of long-run trends in economic activity. It displays the average annual growth rate over the preceding 40 quarters (10 years) for the period 1955 through 2016. (Hence, the first observation in the graph is the first quarter of 1965, and the last is the fourth quarter of 2016.)

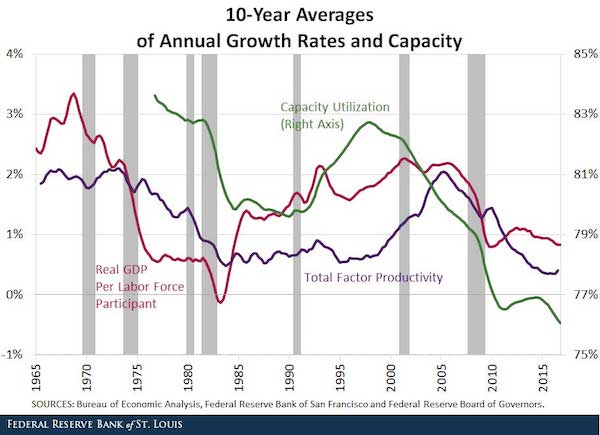

Long-run growth rates were high until the mid-1970s. Then, they quickly declined and leveled off at around 3% per year for the following three decades. In the second half of the 2000s, around the last recession, growth contracted again sharply and has been declining ever since. The 10-year average growth rate as of the fourth quarter of 2016 was only 1.3% per year. Total output grows because the economy is more productive and capital is accumulated, but also because the population increases over time. The next figure compares long-run growth rates of real GDP and real GDP per capita. Both series display similar behavior. Although population growth has been slowing, the effect is not big enough to change the qualitative results described above. The third figure adds long-run growth rates of real GDP divided by the labor force. Dividing by the labor force instead of the total population accounts for the effects of changing demographics and labor market attachment.

From the 1970s until the 2000s, long-run growth rates of real GDP divided by the labor force remained well below those of real GDP per capita. There are two main factors that explain this: 1) Lower fertility and longer lifespans steadily increased the potential labor force relative to the total population. 2) Labor force participation increased significantly from the 1960s until 2000, largely driven by increased female labor force participation. When accounting for both of these factors, economic activity from 1975 to 1985 looks more depressed than in the two decades that followed. This seems consistent with the negative effects that the 1970s oil shocks and efforts to reduce inflation in the early 1980s had on the economy.

The trend in labor force participation reversed in 2000, as participation rates have been steadily decreasing since then. This explains why real GDP divided by labor force growth rates are now higher than real GDP per capita growth rates. Having accounted for the long-term effects of changes in demographics and labor market attitudes, we can now look at the effects of productivity growth and factor utilization. The final figure compares long-run growth rates in real GDP divided by the labor force with long-run growth rates in total factor productivity and long-run averages of capacity utilization (i.e., the actual use of installed capital relative to potential use). Note that data for capacity utilization are only available since 1967.

“The market is apparently pricing in a huge Trump stimulus. But if you just look at the real world out there, the only thing that’s going to happen is a fiscal bloodbath and a White House train wreck like never before in U.S. history.”

• The Market Will Be Repricing Dramatically Downward – Stockman (CNBC)

Stocks are booming under President Donald Trump, but long-time critic David Stockman warns traders are living in a “fantasy land” that can’t last —and Trump’s policies will derail the market for years to come. The former Reagan administration OMB director appeared on CNBC’s “Futures Now”last week to emphasize that Trump has become seemingly distracted by issues other than his proposed economic agenda. That should be a particular point of worry for investors, who Stockman argued have been far more optimistic about Trump’s presidency than might be warranted by the facts. In other words, while all three major market indexes continued to hit record highs last week, the former Reagan aide sees the current market rally as moot and not reflective of the current political climate.

“What’s going on today is complete insanity,” said Stockman. “The market is apparently pricing in a huge Trump stimulus. But if you just look at the real world out there, the only thing that’s going to happen is a fiscal bloodbath and a White House train wreck like never before in U.S. history.” Since the election, the S&P 500 Index has rallied more than 8%, the Nasdaq about 6% and the Dow Jones Industrial Average a whopping 10%. Last week, all three benchmarks rallied to new record highs. Yet if anything, according to Stockman’s predictions, those gains may be lost. Most of Trump’s actions “[have] nothing to do with the economic agenda” he’s proposed, Stockman told CNBC. That, along with a debt ceiling debate that will take place on March 15 in Congress, and a market rally that has gone on for a while, leads Stockman to think that a big downturn is on the way.

“There’s going to be no tax action this year,” said Stockman, echoing the concerns of Goldman Sachs and a few other Wall Street economists who say Trump’s plans for the economy are facing mounting political risks. Last week, the president vowed that tax reform could happen this year, and promised an announcement within the next few weeks. “If there’s any next year it will be deficit neutral, which means it’s not going to add the $15 to earnings like these people expect,” Stockman said, speaking of the rosy expectations of some analysts who think tax reform could boost corporate earnings in the medium-term. “My argument is there is not going to be any economic rebound, there is not going to be any profit surge,” Stockman added. “Therefore the market will be repricing dramatically downward once it’s clear that that’s the case.”

Rogers adds a new dimension of doom: “..a lot of institutions, people, companies even countries, certainly governments and maybe even countries are going to disappear.”

• Jim Rogers: “A Lot Of People Will Disappear” (ZH)

On the Greater Depression… …get prepared because we’re going to have the worst economic problems we’ve had in your lifetime or my lifetime and when that happens a lot of people are going to disappear. In 2008 Bear Stearns disappeared, Bear Stearns had been around over 90 years. Lehman Brothers disappeared. Lehman Brothers had been around over 150 years. A long, long time, a long glorious history they’ve been through wars, depression, civil war they’ve been through everything and yet they disappear. So the next time around it’s going to be worse than anything we’ve seen and a lot of institutions, people, companies even countries, certainly governments and maybe even countries are going to disappear.

I hope you get very worried. When you start having bear markets as you I’m sure well know one bad thing happens and another bad thing happens and these things snowball just like in bull markets good news comes out then more good news comes out the next thing you know you’re five or six or seven years into a bull market. Well bear markets do the same thing and so we have a lot of bad news on the horizon. I haven’t even gotten to war. I haven’t even gotten to trade war or anything like that but you know things do go wrong.

On Trump and the possibility of trade wars…and real wars Mr. Trump has also said he’s going to have trade war with China, Mexico, Japan, Korea a few other people that he has named. He swore that on his first day in office he would impose 45% tariffs against China. He’s been there three weeks, two or three weeks and he hasn’t done it yet but he still got it in his head I’m sure or maybe he’s just another politician like all the rest of them. He says one thing and he doesn’t mean it at all but he does have at least three people in high levels in his group who are very, very keen to have trade wars with China and other people.

If he does that Eric, it’s all over. I mean history is very clear that trade wars always lead to problems, often to disaster, sometimes even to real war, a shooting war. So I don’t know, I’m not sure Mr. Trump knows. He said so many things and many of the things are contradictory. Now if he’s not going to have trade wars with various people then chances are for a while happy days are here… [The dollar is] going to go too high, may turn into a bubble, at which point I hope I’m smart enough to sell it because at some point the market forces are going to cause the dollar to come back down because people are going to realize, oh my gosh, this is causing a lot of turmoil, economic problems in the world and it’s damaging the American economy. At that point the smart guys will get out. I hope I’m one of them.

Sputtering engines all around.

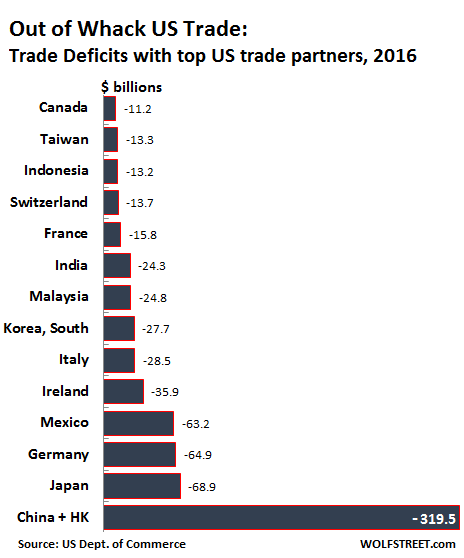

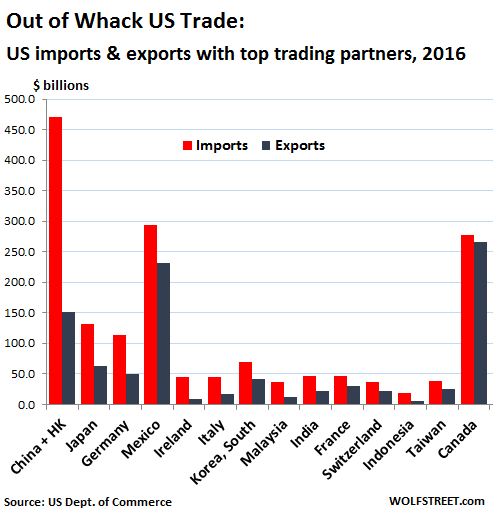

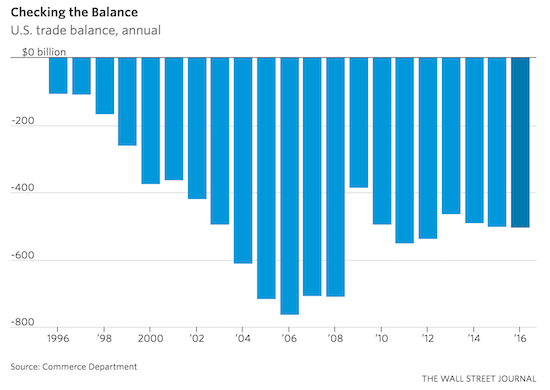

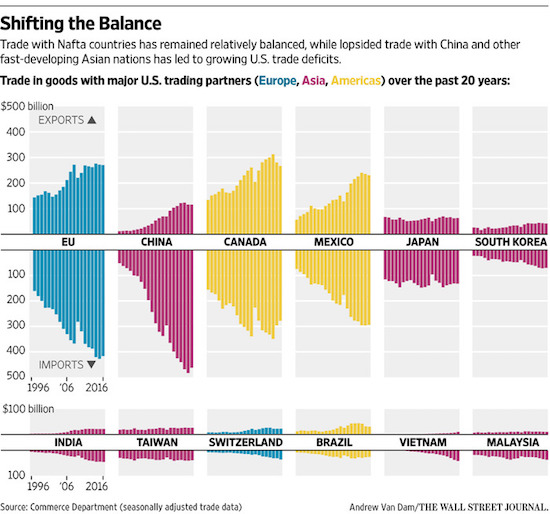

• US Trade Deficit Last Year Was Widest Since 2012 (WSJ)

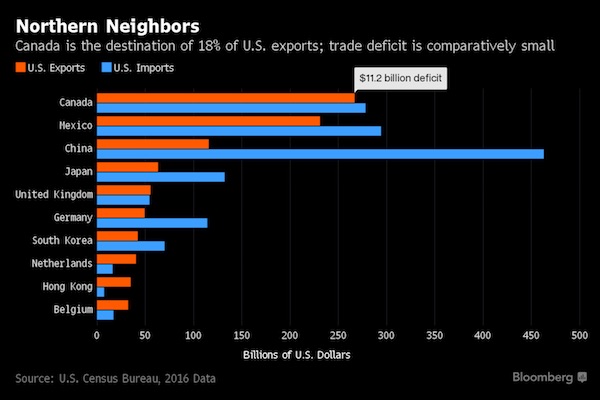

The U.S. logged a $502.25 billion trade deficit in 2016, the largest in four years and a gap President Donald Trump is setting out to narrow to bolster the U.S. economy. The new president faces obstacles in the coming months and years, including the potential for a stronger dollar, larger federal budget deficits and low national saving rates compared with much of the rest of the world, all of which could force trade deficits to widen. As in past years, the 2016 gap reported Tuesday by the Commerce Department reflected a large deficit for U.S. trade in goods with other countries, offset in part by a trade surplus for services. The gap in terms of goods only was $347 billion with China last year, $69 billion with Japan, $65 billion with Germany and $63 billion with Mexico.

For December, the total trade gap decreased 3.2% from November to a seasonally adjusted $44.26 billion. Exports rose 2.7%, including increased sales of civilian airplanes and aircraft engines. Imports were up 1.5% in December, including a rise in car imports. [..] The interplay between trade, growth and employment is complex and difficult to manage. The U.S. has run trade deficits for decades, during periods of expansion and low unemployment as well as during recessions and high unemployment. The gap widened starting in the late 1990s with China’s emergence as a world trading power and recent research shows a surge of imports from China put downward pressure on U.S. wages and manufacturing employment.

Economists generally say trade has overall if uneven benefits, including lower prices for consumers.In 2016, the total deficit rose modestly from the prior year to its highest dollar level since 2012. But it shrank slightly to 2.7% as a share of U.S. economic output after hovering at 2.8% of GDP in 2013 through 2015. The gap fundamentally reflects the fact that Americans consume more than they produce relative to the rest of the world. To shrink the gap, they would either have to produce more or consume less. If Americans consumed less, the deficit could contract along with the broader economy, as happened during the 2001 and 2007-2009 recessions, leaving workers no better off. To produce more, U.S. firms could export more or take market share from imports. Tariffs could help that happen, but other countries might retaliate.

This was always going to happen. It’s been clear from the start that not all these people would last very long. It’s Trump-style: throw out some stuff and see what sticks. And this is where the anti-Trump stance of the media bites: WaPo or CNN or NYT or in this case Politico have lost any and all signs of objectiveness. Which colors their reporting on this too, or so one must assume. We could have done with some credible sources.

• Trump Reviews Top White House Staff After Tumultuous Start (Pol.)

President Donald Trump, frustrated over his administration’s rocky start, is complaining to friends and allies about some of his most senior aides — leading to questions about whether he is mulling an early staff shakeup. Trump has told several people that he is particularly displeased with national security adviser Michael Flynn over reports that he had top-secret discussions with Russian officials about and lied about it. The president, who spent part of the weekend dealing with the Flynn controversy, has been alarmed by reports from top aides that they don’t trust Flynn. “He thinks he’s a problem,” said one person familiar with the president’s thinking. “I would be worried if I was General Flynn.”

Yet Trump’s concern goes beyond his embattled national security adviser, according to conversations with more than a dozen people who have spoken to Trump or his top aides. He has mused aloud about press secretary Sean Spicer, asking specific questions to confidants about how they think he’s doing behind the podium. During conversations with Spicer, the president has occasionally expressed unhappiness with how his press secretary is talking about some matters — sometimes pointing out even small things he’s doing that he doesn’t like. Others who’ve talked with the president have begun to wonder about the future of Chief of Staff Reince Priebus. Several Trump campaign aides have begun to draft lists of possible Priebus replacements, with senior White House aides Kellyanne Conway and Rick Dearborn and lobbyist David Urban among those mentioned.

Gary Cohn, a Trump economic adviser who is close with senior adviser Jared Kushner, has has also been the subject of chatter. For now, Priebus remains in control as chief of staff. He was heavily involved in adviser Stephen Miller’s preparation for appearances on Sunday morning talk shows, which drew praise from the president. If there is a single issue where the president feels his aides have let him down, it was the controversial executive order on immigration. The president has complained to at least one person about “how his people didn’t give him good advice” on rolling out the travel ban and that he should have waited to sign it instead of “rushing it like they wanted me to.” Trump has also wondered why he didn’t have a legal team in place to defend it from challenges.

A very strange position to be in for a career intelligence man.

• Mike Flynn’s Position as National Security Adviser Grows Tenuous (WSJ)

The White House is reviewing whether to retain National Security Adviser Mike Flynn amid a furor over his contacts with Russian officials before President Donald Trump took office, an administration official said Sunday. Mr. Flynn has apologized to White House colleagues over the episode, which has created a rift with Vice President Mike Pence and diverted attention from the administration’s message to his own dealings, the official said. “He’s apologized to everyone,” the official said of Mr. Flynn. Mr. Trump’s views toward the matter aren’t clear. In recent days, he has privately told people the controversy surrounding Mr. Flynn is unwelcome, after he told reporters on Friday he would “look into” the disclosures.

But Mr. Trump also has said he has confidence in Mr. Flynn and wants to “keep moving forward,” a person familiar with his thinking said. Close Trump adviser Steve Bannon had dinner with Mr. Flynn over the weekend, according to another senior administration official, and Mr. Bannon’s view is to keep him in the position but “be ready” to let him go, the first administration official said. Mr. Trump’s son-in-law and senior adviser, Jared Kushner, as of Sunday evening hadn’t yet weighed in, the official said. Mr. Flynn initially said that in a conversation Dec. 29 with the Russian ambassador, Sergey Kislyak, he didn’t discuss sanctions imposed that day by the outgoing Obama administration, which were levied in retaliation for alleged Russian interference in the 2016 presidential election.

Mr. Flynn now concedes that he did, administration officials said, after transcripts of his phone calls show as much. He also admits he spoke with the ambassador more than once on Dec. 29, despite weeks of the Trump team’s insisting it was just one phone call, officials said. Mr. Pence, in television interviews, vouched for Mr. Flynn, based on a private conversation, and he was angered he repeated information publicly that turned out to be untrue, administration officials said. Messrs. Pence and Flynn spoke twice on Friday, one official said. If Mr. Flynn had promised any easing of sanctions once Mr. Trump took office, he may have violated a law that prohibits private citizens from engaging in foreign policy, legal experts have said.

Who does the headlines at Bloomberg?

• Refugee-Embracing Trudeau Set to Bite His Tongue on Trump Visit (BBG)

More than two decades ago, with Donald Trump already atop a real-estate empire, a young Justin Trudeau set out to explore the world. He toured Europe and Africa with friends, hiding their beer from customs agents before boarding the Trans-Siberian railway to China. On the train, he sketched, read “War and Peace” and gazed at the remnants of the Soviet Union. It was a defining trip, he’d later write, that left him praising both diversity and compromise. Both values will be tested Monday. The now-45-year-old Canadian prime minister – hailed by Joe Biden as one of the last champions of liberalism – heads to Washington for his first meeting with the new U.S. president, 70, whose bellicose statements and immigration restrictions reveal a deep gulf between the two leaders. But U.S. liberals hoping for Trudeau to emerge as Trump’s foil shouldn’t hold their breath.

He’s already bit his tongue and focused almost exclusively on an economic relationship that accounts for three-quarters of Canada’s exports. The White House visit will test just how far Trudeau can go to woo the president and preserve trade without selling out his core values. “We both got elected on commitments to strengthen the middle class, and support those working hard to join it,” Trudeau said last week. “And that’s exactly what we’re going to be focused on.” He has little choice. Nearly two-thirds of all Canadian trade is with the U.S., the highest ratio of Group of 20 nations and quadruple all but Mexico. Almost all of Canada’s oil goes to the U.S. and most of the country’s manufacturing is geared toward meeting U.S. demand. Americans hold C$2.3 trillion ($1.8 trillion) in Canadian assets, almost exactly the same amount held by Canadians in the U.S. A Deutsche Bank report this month that looked at the potential impact of Trump policies on all the U.S.’s major partners found Canada would be among the hardest hit, forcing the country to cede about $70 billion in trade to the U.S. [..]

The threats to Canada from Trump’s agenda go beyond trade. Trump has shown an interest in overhauling the U.S. tax system in a way that would impose financial disincentives against imports. The border-adjusted tax plan would focus levies on domestic income and imports while exempting exports and offshore income. It has met opposition from retailers and oil refiners but is supported by major exporters. It’s unclear whether the president fully favors that approach. All this, however, is unlikely to be detailed Monday. Instead, Trudeau will seek to lay out a joint economic narrative with Trump. The prime minister’s conciliatory spirit traces back to that Trans-Siberian railway trip. On New Year’s Eve 1994, Trudeau drank vodka with the conductor, captivated by stories but abhorred by “his casual racism to our fellow passengers,” he wrote in his autobiography.

Corruption interrupted.

• Romania Protests Enter Day 13, Call For Government Of ‘Thieves’ To Resign (G.)

Tens of thousands of Romanians have braved the cold and returned to the streets in protest, calling on the government to resign as they accused it of attempting to water down anti-corruption laws. “Thieves! Resign!” chanted protesters gathered in front of the seat of government in Bucharest on Sunday night, as they used the lights from their mobile phones to project the blue, yellow and red colours of the Romanian flag. Up to 50,000 protesters took part in the Bucharest march, according to Romanian media reports. The authorities did not give any estimate of their own. Some 20,000 more took to the streets in other major cities, calling on the government to stand down. “We want to give the government a red card,” one of the protesters, 33-year-old businessman Adrian Tofan, said.

Sunday’s demonstrations, the 13th consecutive day of protests against the government, took place despite the administration backing down over a planned controversial decree which would have made abuse of power a crime punishable by jail only if the sums involved exceeded 200,000 lei ($47,500). The demonstrations, the largest since the ousting and summary execution of communist dictator Nicolae Ceausescu in 1989, have continued despite the resignation on Thursday of justice minister Florin Iordache. “The justice minister’s resignation isn’t enough after what they tried to do,” said Tofan. Another demonstrator also said he had completely lost faith in the government. “We want this government to stand down. We don’t trust it, they want us to go backwards,” said Bogdan Moldovan, a doctor.

Highly speculative, but….“..some economists in Germany say the repatriated gold may be needed to back a new deutschmark should the eurozone collapse..”

• Germany Repatriates Gold Faster Than Planned As Faith In Euro Plunges (RT)

Berlin is bringing home its gold reserves stored in New York, London and Paris faster than scheduled, Germany’s central bank said Thursday. The move is linked to surging euroskepticism, as new governments in France and Italy may ditch the single currency. The German Bundesbank has already moved 583 tons of gold out of New York and Paris, planning to have a half of its gold back in Germany by the end of 2017, which is ahead of the 2020 plan. The rest will be split between the Federal Reserve Bank of New York and the Bank of England. “We have a lot of discussions about Trump, regarding implications on monetary policy, macroeconomics, etc., but we trust the central bank of the US,” Bundesbank board member Carl-Ludwig Thiele told a news conference. “Trump has not triggered a discussion about the storage facility in New York,” he said.

As French presidential candidate Marine Le Pen and Italy’s 5-Star Movement are openly calling to pull out of the euro, some economists in Germany say the repatriated gold may be needed to back a new deutschmark should the eurozone collapse. During the Cold War, 98% of Germany’s bullion was stored abroad, and so far the biggest repatriation was in 2000 when the Bundesbank repatriated 931 tons from the Bank of England. When the relocation is complete, Germany will still have 1,236 tons in New York, 432 tons in London and the rest in Frankfurt. The current repatriation involves moving 300 tons from New York and 374 tons from Paris. The Bundesbank said it is not worried about keeping gold in England despite Brexit, as London remains a key gold trading market and a safe place. Germany has the second-largest gold reserves in the world after the US with 3,381 tons.

Amen.

• Brussels’ Hypocrisy Over The Closing Of Borders (Nikos Devletoglou)

Sir, It seems remarkable that today’s leaders of the EU, encouraged by the overreaction of the global mass media, reserve for themselves the appearance of virtue and goodness and generally resent the refreshing American principle summed up by president Donald Trump as America First. Americans have shed blood, along with vast material expense, defending human rights in Europe — regardless of ethnicity, geography, culture or religion, demonstrably having guaranteed the continent’s survival in freedom and subsequent prosperity, including that of Germany, after the second world war.

The EU’s hypocrisy offends. Indeed, it remains a mystery how Brussels feels justified in its heavy criticism of America’s increasing vigilance over its own borders when the EU itself continues to turn a blind eye to the formidable barbed-wire militarised fortifications erected all along the northern frontiers of Greece by its neighbours, pitilessly blocking the passage of hundreds of thousands refugees desperately fleeing the war in Syria. These refugees still dearly hope to reach Germany first and eventually other parts of Europe, but are instead inhumanely trapped in Greece practically under the authority of the EU — which, further, even condones the closing of borders in Austria and Hungary. These are provocative double standards. The scant remaining resources in Greece are already stretched to their limits.

Previously prosperous islands in the Aegean Sea – Chios, Samos and Lesbos were until recently celebrated high-profile tourist destinations worldwide – are currently overrun by multitudes of refugees, understandably aggressively inclined by now, at the expense of social cohesion elsewhere in Greece as well. Still worse, the country remains undeservedly caught in a deepening economic and financial crisis, a result of blind austerity policies inspired by Germany that the EU rigorously enforces to this day, manifestly ruling out growth and prosperity in Greece any time soon. Both the IMF and the European authorities still fail to appreciate that reducing Greek debt by one-third in the present circumstances would consistently reflect the social, economic and financial damage they themselves have caused by arbitrarily depressing the Greek economy since 2010.

Nicos E Devletoglou, Emeritus Professor of Economics, University of Athens, Greece

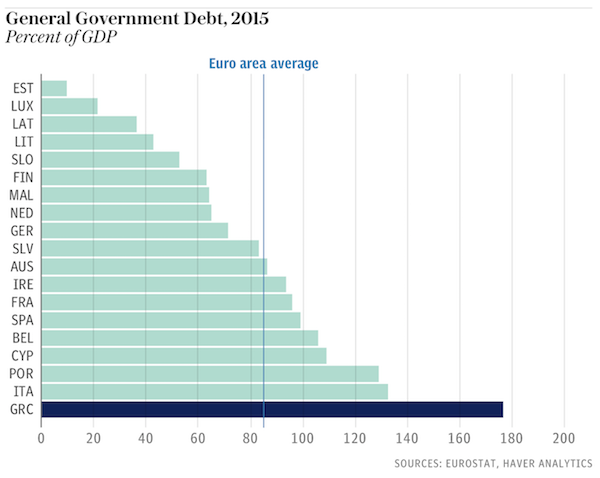

Bitter, bitter tragedy. “The human and social cost of this austerity policy is not included in the Excel tables of the Eurogroup. But it is paid cash by the population.”

• Greece: The Low-Noise Collapse Of An Entire Country (FE)

European officials may argue that their bailout is working, they welcome the recovery of Greece and the budget surpluses, but the situation is quite different: passively we are witnessing the low-noise collapse of a whole country. While forecasts foresee a rebound of the Greek economy in 2016, with growth of at least 2.6%, these risks once again prove to be false. If a slight start was recorded at the beginning of the year, it continued to slacken. In the last few months, the engine seems to have stalled. According to Markit figures published on February 1st, manufacturing activity recorded its largest decline in 15 months. “The decline is related to both the decline in production and new orders. While rising import prices have accelerated to their highest level in 70 months, companies nevertheless lower their selling prices,” explains the economic and financial institute, pointing to the fall in consumption and the lack of outlets.

In seven years Greece’s GDP decreased by a third. Unemployment affects 25% of the population and 40% of young people between 15 and 25 years. One third of companies have disappeared in five years. Successive cuts imposed everywhere in the name of austerity now bite in all regions. There are no more trains, no more buses in whole parts of the country. No more schools, sometimes. Many secondary schools had to close in the most remote corners because of lack of funding. Per capita spending on health has declined by a third since 2009, according to the OECD. More than 25,000 doctors were dismissed. Hospitals lack personnel, medicines, everything. The human and social cost of this austerity policy is not included in the Excel tables of the Eurogroup.

But it is paid cash by the population. One fifth of the population lives without heating or telephone. 15% of the population has now fallen into extreme poverty compared to 2% in 2009. The Bank of Greece, which cannot be suspected of complacency, has drawn up a report on the health of the Greek population, published in June 2016. The figures it gives are overwhelming: 13% of the population are excluded medical care; 11.5% cannot buy prescription drugs; People with chronic health problems are up to 24.2%. Suicides, depression, mental illness show exponential increases. Worse: while the birth rate has fallen by 22% since the beginning of the crisis, the infant mortality rate almost doubled in a few years to reach 3.75% in 2014.

After seven years of crisis, austerity and European plans, the country is exhausted, financially, economically and physically. “The situation is getting worse. What we need most now is food. This shows that the problems relate to the essential and not the quality of life. It’s about subsistence,” says Ekavi Valleras, head of the NGO Desmos. And it is to this country that Europe asks moreover to assume alone or almost the reception of the refugees coming to Europe.