It’s never easy to gauge what exactly is happening in China, or why the CCP Politburo takes the decisions it does. Today, or overnight, is no exception to that. However, one thing that appears certain, but which I don’t see reflected in all the analyses, is that Beijing pushing the value of the renminbi (yuan) down below 7 to the USD in one fell swoop, is a major setback for Xi Jinping and his government.

Yes, China may have given up hope of reaching positive conclusions in its trade talks with the US. And yes, some may think, even in China itself, that devaluing the currency is a tool that can be useful in a potential currency war. But there’s another side to this coin. It’s not even about the value itself, or the change in it, it’s the heavy-handed way it’s executed.

China wants, and desperately needs too, for the yuan to be a force in global financial markets. In very simple terms this is true because if it then wants to buy something, it can simply print the money for it. But only about 1% of global trade today is executed in yuan. That is not nearly enough. It means China needs dollars and euros, all the time. And devaluing the yuan means the country needs even more of those.

You’d almost think: why would you want to do that? What are the long-term prospects for a move like this? You’re telling forex markets that the value of the yuan is not trustworthy, because if Xi or the PBOC decides in the next five minutes that it should go up or down by 10% or 20%, they can do it. The Fed and ECB also have tools to manipulate their currencies (re: interest rates), but none of that magnitude.

The crux of the dilemma probably lies in the Belt and Road Initiative (BRI), which I’ve been saying for years is just China’s way to sell its overcapacity and overproduction abroad. Sure, there may be loftier goals, and surely in the glitzy brochures, but the fact remains that China has tried to be an economic miracle, doing in 10 years what took the US a century, and it never slowed down its growth, at least not voluntarily, even if that might have been a wise move.

Already lately, purchases by Chinese citizens and companies of real estate and businesses abroad have been curtailed, and not a little bit, by Beijing. There’s no better way to convince Chinese people of the miracle’s success than to let them travel the world and spend there, but that, too, may well soon be cut. It kills foreign reserves.

If Beijing could charge participating countries in the Belt and Road Initiative in yuan, and they could pay for the overcapacity’s steel and cement and what not in yuan, that could be a game-changing program for the entire planet. But these countries have no reason to hold yuan, other than the BRI itself. And they, too, were watching the overnight move above 7 and must have thought: let’s be careful now.

And to top it all off, China right now needs for these countries to pay in dollars instead of yuan, because its foreign reserves are shrinking so fast. It’s Catch-22 all the way down. China’s need for dollars goes against everything BRI stands for.

Could the move hurt the US as well? Absolutely. But the long-term view behind the tariffs, and the talks China appears to have lost faith in, is to move the US away from its near all-encompassing addiction to Chinese production, and to move at least some of that production back home. Problem of course is, that is precisely what China’s miracle growth has been built on.

If the US starts bringing production home, who is Beijing going to sell its (over-)production to? Yes, I hear you, to the BRI countries. But there it runs into the currency problems mentioned before. To Europe? The top of that trade route is also behind us. Europe will have to follow the US to an extent, and also bring factories back to the continent (and not just to Germany either).

China could perhaps sell more than it does today to Russia. But that country still does produce a lot of things, and has been forced to be much more self-sufficient due to US and EU sanctions. It’s also a mighty small market compared to 350 million North Americans and 500 million Europeans, who are on average much richer than your average Russian to boot.

There is a way for China to make the yuan more important in global trade (but devaluation is definitely not that way): Beijing could let go of its central and total control over the value of its currency, and let forex markets figure it out. That would give traders -and everyone else- faith in the value. Problem with that is, this is not how central control communist governments think.

Beijing wants both: central total control AND a prominent place in world trade. And it may take them a long time to figure out that is not going to happen, unless of course they first conquer the entire world militarily. That is not an option, at least not for the foreseeable future. Come see me next century.

It wouldn’t be the first time for me to say I can see China retreat into itself, into its own borders and culture and market (1.3 billion people!). If the Communist Party wants to remain in power, and there’s no doubt it does, this may be only possible choice going forward. If growth has indeed left the miracle -as many observers think-, it can implode in very rapid succession. And even if growth hasn’t yet evaporated, it may well very soon. Without the growth, there is no miracle anymore.

And if China can no longer grow its exports, its domestic growth will also become a thing of the past. Domestic consumption can only grow as long as exports do too. Seen from that angle, the problems with trade and the currency look downright ominous. If you need dollars that badly, and you notice that you’re already getting fewer of them, not more, you’re in trouble.

Devaluing your currency may afford you some temporary respite, but it can’t possibly solve your troubles. It can make them much worse though.

I think China has wanted too much too fast, got carried away and forgot to take care of a few potential barriers to its growth, in particular the standing its currency had and still has in the world, and the grinding need for dollars that stems from it. And the Communists have no answer to this problem.

U.S. President Donald Trump said on Wednesday the United States and the European Union were kicking off talks aimed at lowering trade barriers as officials looked to head off a brewing trade war. “This was a very big day for free and fair trade, a very big day indeed,” Trump told reporters at the White House after meeting with European Commission President Jean-Claude Juncker. “We are starting the negotiation right now but we know very much where it’s going,” Trump said. Speaking with Juncker at his side, Trump said they had agreed in talks to “work together toward zero tariffs, zero non-tariff barriers, and zero subsidies on non-auto industrial goods.”

“We will also work to reduce barriers and increase trade in services, chemicals, pharmaceuticals, medical products, as well as soybeans; soybeans is a big deal,” he said, adding that Europe would also step up purchases of liquefied natural gas from the United States. “They are going to be a massive buyer of LNG,” Trump said. Trump said the talks would “resolve” both the hefty tariffs the United States had placed on imports of steel and aluminum from the EU and the tariffs Europe had slapped on U.S. goods in response. It was not clear whether the two sides made any progress on the contentious issue of possible U.S. tariffs on imports of automobiles from Europe. But Juncker said they had agreed not to impose any new tariffs while talks were taking place.

House GOP members led by Freedom Caucus Chairman Mark Meadows (NC) have filed formal articles of impeachment against Deputy Attorney General Rod Rosenstein, according to a late Wednesday announcement by Meadows over Twitter. News of the resolution comes after weeks of frustration by Congressional investigators, who have repeatedly accused Rosenstein and the DOJ of “slow walking” documents related to their investigations. Lawmakers say they’ve been given the runaround – while Rosenstein and the rest of the DOJ have maintained that handing over vital documents would compromise ongoing investigations. Not even last week’s heavily redacted release of the FBI’s FISA surveillance application on former Trump campaign Carter Page was enough to dissuade the GOP lawmakers from their efforts to impeach Rosenstein.

In fact, its release may have sealed Rosenstein’s fate after it was revealed that the FISA application and subsequent renewals – at least one of which Rosenstein signed off on, relied heavily on the salacious and largely unproven Steele dossier. In late June, Rosenstein along with FBI Director Christopher Wray clashed with House Republicans during a fiery hearing over an internal DOJ report criticizing the FBI’s handling of the Hillary Clinton email investigation by special agents who harbored extreme animus towards Donald Trump while expressing support for Clinton. Republicans on the panel grilled a defiant Rosenstein on the Trump-Russia investigation which has yet to prove any collusion between the Trump campaign and the Kremlin. “This country is being hurt by it. We are being divided,” Rep. Trey Gowdy (R-SC) said of Mueller’s investigation. “Whatever you got,” Gowdy added, “Finish it the hell up because this country is being torn apart.”

Well, lordy be. A lawyer for The New York Times has figured out that prosecuting WikiLeaks publisher Julian Assange might gore the ox of The Gray Lady herself. The Times’s deputy general counsel, David McCraw, told a group of judges on the West Coast on Tuesday that such prosecution would be a gut punch to free speech, according to Maria Dinzeo, writing for the Courthouse News Service. Curiously, as of this writing, McCraw’s words have found no mention in the Times itself. In recent years, the newspaper has shown a marked proclivity to avoid printing anything that might risk its front row seat at the government trough.

Stating the obvious, McCraw noted that the “prosecution of him [Assange] would be a very, very bad precedent for publishers … he’s sort of in a classic publisher’s position and I think the law would have a very hard time drawing a distinction between The New York Times and WikiLeaks.” That’s because, for one thing, the Times itself published many stories based on classified information revealed by WikiLeaks and other sources. The paper decisively turned against Assange once WikiLeaks published the DNC and Podesta emails. More broadly, no journalist in America since John Peter Zenger in Colonial days has been indicted or imprisoned for their work.

Unless American prosecutors could prove that Assange personally took part in the theft of classified material or someone’s emails, rather than just receiving and publishing them, prosecuting him merely for his publications would be a first since the British Governor General of New York, William Cosby, imprisoned Zenger in 1734 for ten months for printing articles critical of Cosby. Zenger was acquitted by a jury because what he had printed was proven to be factual—a claim WikiLeaks can also make. McCraw went on to emphasize that, “Assange should be afforded the same protections as a traditional journalist.”

Facebook Inc. is evidently not bulletproof. The social-media behemoth’s stock lost roughly one-fifth of its value in the extended session Wednesday after its earnings report missed expectations on revenue and showed slowing user growth. Weak guidance also rattled investors. Facebook stock dropped about 7% immediately after the earnings report was released, then plummeted to a loss of more than 20% as a conference call with analysts progressed. Close to 34 million shares changed hands in the extended session, well above the average volume of 17 million shares for a regular trading session over the past month. Should the losses hold into Thursday’s regular session, Facebook would lose more than $100 billion in market capitalization and lose the stock’s gains for the year thus far.

As the after-hours session wrapped up, Facebook was trading at $173.50, down 20%. Facebook stock had recovered from a decline earlier this year in the wake of the Cambridge Analytica scandal, one of several controversies and warning signs that the company had managed to weather with little damage to its stock. But declining revenue and user growth, topped by a warning from executives that it will continue, seemed to end that run. “The guidance, it’s nightmare guidance,” GBH Insights head of technology research Daniel Ives said. “If you look at their forecast for the second half of the year in terms of user growth, and the expense profile, it refuels the fundamental worries about Facebook post-Cambridge Analytica.”

China has withdrawn its approval for Facebook Inc’s plan to open a new venture in the eastern province of Zhejiang, the New York Times reported on Wednesday, citing a person familiar with the matter. A Chinese government database showed that Facebook had gained approval to open a subsidiary, but the registration has since disappeared, according to checks made by Reuters. The move is a setback for Facebook, which has been struggling to gain a foothold in China, the most populous country in the world, where its website and messaging app Whatsapp remain blocked.

The incident also illustrates how difficult it can be for a U.S. company to navigate the government bureaucracy in a country where so many technology firms have tried and failed. “Terms like ‘The Great Firewall’” often gives outsiders the impression that the Chinese government is totally united on technology policy,” said Matt Sheehan, an expert on China-California relations and fellow at The Paulson Institute think tank. “In reality, within that Firewall are lots of competing fiefdoms and ongoing turf wars.” China’s decision comes amid escalating tensions with the United States after the world’s two largest economies imposed tariffs on each other’s imports.

Don’t be fooled. This market is weaker than it seems, according to David Rosenberg, chief economist and strategist at Gluskin Sheff. The S&P 500 is up more than 5% in 2018, recovering from a correction earlier in the year. The broad index was also just 1.9% removed from an all-time high reached in late January as of Tuesday’s close. However, Rosenberg notes that while momentum stocks are lifting the market, “many subsectors are well off their highs: Homebuilders. Autos. Banks. Insurance. Consumer products. Telecom. Media. Transports. Utilities. Pharma. And many more.” The S&P automobiles and components industry group is nearly 20% below its 52-week high, while insurance stocks are down 10.8% from their one-year high. The Dow transports index, meanwhile, is 6.5% below its one-year high.

“What has kept the market near record terrain are a mere six stocks — Alphabet, Apple, Amazon, Netflix, Microsoft and Facebook,” Rosenberg said in a note to clients Wednesday. “Strip out these six flashy stocks, and the overall market has done practically nothing year-to-date.” Through mid-July, Alphabet, Apple, Amazon, Netflix, Microsoft and Facebook had contributed nearly 80% to the S&P 500’s gains. These six names have been on fire this year. Netflix and Amazon are up 86% and 57% in 2018, respectively. Microsoft and Facebook have both risen more than 20% while Alphabet and Apple have jumped 19.8% and 14%, respectively. Rosenberg said such concentration in the stock market has not been seen since the late 1990s, just before the dot-com bubble burst. “We know from history how these cycles typically end.”

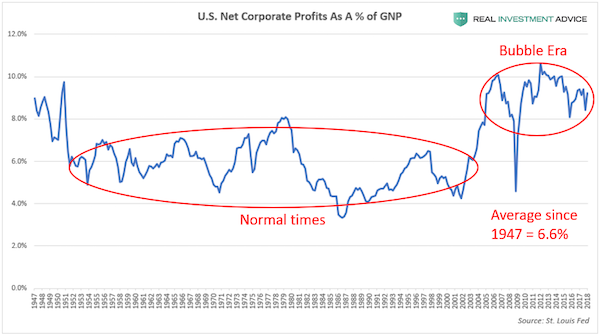

While above-average corporate profitability may sound like a good thing when taken at face value, I view it as another worrisome sign because it’s further evidence of an economy and financial markets that are being juiced by cheap credit and financial engineering. Ultra-low interest rates help to boost corporate profitability by reducing borrowing costs. Cheap credit also gives consumer spending a strong boost, which has a significant effect on our economy that is heavily driven by consumer spending. Low interest rate environments allow the government (federal, state, and local) to borrow more cheaply in the bond market and use it to boost spending, which gives the overall economy a shot in the arm. In addition, artificially-inflated financial markets boost the profitability of the financial sector.

A major risk for the stock market is the mean reversion of corporate profitability, which is a nightmarish prospect when considering how overpriced stocks currently are relative to earnings. This mean reversion is likely to occur as the result of the ending of ultra-cheap credit conditions (when corporate bonds fall back to earth) and through increased competition, which is what Milton Friedman warned about. (Note: critics may try to rebut my assertions by claiming that U.S. corporate profitability is unusually high due to corporations earning a higher percentage of earnings overseas. I’ve accounted for this by using gross national product as the denominator instead of the more commonly used GDP.)

What is particularly alarming about the current U.S. stock market bubble is the fact that it’s driven by a very narrow group of stocks, which means that there isn’t a healthy breadth, or broad strength, behind the bull market. In general, tech stocks have been leading the way – in particular, a group of stocks known as FAANG, which is an acronym for Facebook, Apple, Amazon, Netflix, and Google. The chart below compares the performance of the FAANG stocks to the S&P 500 during the bull market that began in March 2009. While the S&P 500 is up approximately 300%, the FAANGs are up significantly more, with Apple rising by over 1,000%, Amazon rising more than 2,000%, and Netflix surging by over 6,000%.

If Trump imposes 25% tariffs on Chinese goods, China could simply devalue their currency by 25%. That would make Chinese goods cheaper for U.S. buyers by the same amount as the tariff. The net effect on price would be unchanged and Americans could keep buying Chinese goods at the same price in dollars. The impact of such a massive devaluation would not be limited to the trade war. A cheaper yuan exports deflation from China to the U.S. and makes it harder for the Fed to meet its inflation target. Also, the last two times China tried to devalue its currency, August 2015 and December 2015, U.S. stock markets crashed by over 11% in a matter of a few weeks.

So, if the trade war escalates as I expect, don’t worry about China dumping Treasuries or imposing tariffs. Watch the currency. That’s where China will strike back. When they do, U.S. stock markets will be the first victims. Maybe you think that’s unlikely because it would be such an extreme reaction by China. But you have to put yourself in the shoes of China’s leadership. These aren’t academic issues to China’s leaders. They go to the heart of the government’s very legitimacy. China’s economy is not just about providing jobs, goods and services. It is about regime survival for a Chinese Communist Party that faces an existential crisis if it fails to deliver. The overriding imperative of the Chinese leadership is to avoid societal unrest.

If China encounters a financial crisis, Xi could quickly lose what the Chinese call, “The Mandate of Heaven.” That’s a term that describes the intangible goodwill and popular support needed by emperors to rule China for the past 3,000 years. If The Mandate of Heaven is lost, a ruler can fall quickly. Up to half of China’s investment is a complete waste. It does produce jobs and utilize inputs like cement, steel, copper and glass. But the finished product, whether a city, train station or sports arena, is often a white elephant that will remain unused. Chinese growth has been reported in recent years as 6.5–10% but is actually closer to 5% or lower once an adjustment is made for the waste.

The US dollar has become the safest asset in the face of mounting evidence that the “beggar thy neighbor” policy and drowning structural problems in liquidity is coming to a close. The reality is that the US dollar is strengthening because of the evidence of a deeper slowdown in China and the massive imbalances built by some emerging economies in the past -large fiscal and trade deficits financed with the cheap inflow of dollars-. As the US economy improves and others face the saturation of past stimuli, it is only logical that the United States sees a high inflow of funds from abroad. And that is good. Keeps US treasury yields low, a high demand for bonds and equities, and a steady increase in capital investment into the US economy.

There are many who think that the US economy will not accept a strong dollar. Allow me to doubt it. The US only exports around 10% of GDP and less than 30% of the profits of the S & P 500 come from exports. In the past nine years, devaluing and lowering rates has hurt the middle class, savers, workers, and high productivity companies. Those that voted for the current administration to make a drastic change on the past mistakes. A devaluation policy hurts more Americans than it helps. Devaluation is simply stealing from your citizens’ savings and disposable income. A strong US dollar reduces inflationary pressures and keeps interest rates low. Both effects are positive for savers, workers, and families as the economy strengthens and wages improve.

Theresa May has urged voters not to worry about Brexit, despite her government setting out plans to stockpile food, blood and medicine in case it goes badly. She said people should take “reassurance and comfort” from news of the plans, to be implemented if the UK crashes out of the EU without an agreement in March next year. The scenario is looking increasingly likely given deep divisions in the Conservatives over Ms May’s approach, her wafer thin commons majority and the EU’s on-going resistance to what the prime minister is proposing. It comes as The Independent launched a campaign to give the British people a Final Say in a referendum on whatever is proposed at the end of Brexit negotiations, with thousands flocking to sign a petition supporting the cause.

Ireland’s deputy prime minister accused the PM of “bravado” in talking up the dangers of a no-deal Brexit, while Tory insiders claim the PM is doing so to warn her rebellious MPs of the consequence of failing to back her unpopular Brexit plans. Ms May confirmed in a TV interview that plans for stocking up on essential goods are underway, in case imports from the EU are cut off by clogged ports or regulatory disputes. But, asked if it was “alarming” for people, the prime minister told Channel 5: “Far from being worried about preparations that we are making, I would say that people should take reassurance and comfort from the fact that the government is saying we are in a negotiation, we are working for a good deal. “I believe we can get a good deal, but, it’s right that we say – because we don’t know what the outcome is going to be – let’s prepare for every eventuality.”

Imagine you’re back at school and you can’t be bothered to do any work for the most important exams of your entire academic career. Alarmed by your indifference, your parents ask what you propose to do. Imagine how they would react if you told them you were thinking of having an extended summer holiday, to put off the moment of reckoning for as long as possible. Quite frankly, this is where our government now is in the Brexit negotiations. A longer than usual summer recess seems to be the best these great minds can come up with. The problem is we are not in school, Brexit is not homework and the bullies will do more than give us a bloody nose.

The EU is like the strict exam board of governors and appears to have no time for excuses or interest in making Theresa May’s sloppy government look good. It is a measure of May’s desperation that she said in Belfast last week that the EU was trying to achieve an “economic and constitutional dislocation” of our country. That kind of talk may play well with the hard-right Brexiteers who are too painfully holding her and her government hostage, but it doesn’t impress Brussels. May needs to realise that we can all see she is now merely playing for time and there are only a finite number of options open to her: a general election, a leadership challenge or a people’s vote.

[..] The plain truth is that there is no majority in parliament for any deal. The EU thinks the prime minister’s Chequers plan is too favourable to the UK, and the Brexiteers think it’s too favourable to Brussels. A Norway deal would mean accepting free movement and paying large amounts to Brussels; a Canada-style deal means the prospect of a hard border returning to the line on the map that separates Eire and Northern Ireland. Viewed through the lens of May’s parliamentary party, there is no consensus, no coming together on any of these options. Brexit is collapsing under the weight of its own contradictions.

A US state lawmaker is resigning after a humiliating appearance on comedian Sacha Baron Cohen’s television show during which he exposed himself and shouted racial slurs. Jason Spencer, a Republican member of the Georgia House of Representatives, had been under pressure from his own party to step down following the embarrassing appearance on Cohen’s series “Who Is America?” Spencer, 43, finally announced on Wednesday that he planned to resign on July 31. He had already lost a primary in May but he could have remained in office until November. Spencer was one of several Republican figures pranked by Cohen on the Showtime series.

Others included former vice president Dick Cheney, who signed a “waterboarding kit” and former Republican vice presidential nominee Sarah Palin. In the episode of “Who Is America” with Spencer, Cohen pretends to be an Israeli anti-terrorism expert, Colonel Erran Morad, offering self-defense training. At one point, Spencer is persuaded to expose his buttocks and chase Cohen while yelling “USA” and racial slurs. Spencer, in a statement this week to The Washington Post, said Cohen “took advantage of my paralyzing fear that my family would be attacked.” Spencer told the Post he had received death threats after introducing a bill that would ban Muslim women from publicly wearing burqas. Palin, the former governor of Alaska, denounced the show as “evil, exploitive, sick ‘humor.'”

Plants and animals created by innovative gene-editing technology have been genetically modified and should be regulated as such, the EU’s top court has ruled. The landmark decision ends 10 years of debate in Europe about what is – and is not – a GM food, with a victory for environmentalists, and a bitter blow to Europe’s biotech industry. It also marks a setback for UK scientists who took advantage of a legal grey area to of gene edited camelina crops, augmented with Omega-3 fish oils. Greenpeace said that the ruling meant the British government – along with Belgium, Sweden and Finland – was now obliged to “revoke” the green light for the trials until appropriate precautions had been taken.

In their ruling, the EU judges said: “Organisms obtained by mutagenesis are GMOs [genetically modified organisms] … It follows that those organisms come, in principle, within the scope of the GMO directive and are subject to the obligations laid down [therein].” The court sided with the French agricultural trades union, Confédération Paysanne, which brought the case, arguing that new and unconventional in vitro mutagenesis techniques were likely to be used to produce herbicide-resistant plants, with potential health risks. A study published in the journal Nature last week found that the gene-editing technology Crispr-Cas9 can cause significantly greater genetic distortions than expected, with potential “pathogenic consequences”. Gene editing alters the genomes of a living species by slicing genome strands in a bid to remove undesirable traits, without inserting foreign DNA.

Israeli war planes have bombed a Syrian regime airbase east of the city of Homs, the Russian and Syrian military have said. The Russian military said that two Israeli F-15 war planes carried out the strikes from Lebanese air space, and that Syrian air defence systems shot down five of eight missiles fired. Asked about the Russian statement, an Israeli military spokesman said he had no immediate comment. Syrian state TV reported loud explosions near the T-4 airfield in the desert east of Homs in the early hours of Monday. State TV initially reported that the attack was “most likely” American, a claim the Pentagon has denied.

Video footage on social media in Lebanon showed aircraft or missiles flying low over the country, apparently heading east towards Syria. At least 14 people, mostly Iranians or members of Iran-backed groups, were killed, the UK-based Syrian Observatory for Human Rights monitoring group said. Donald Trump warned on Sunday that the regime and its backers would pay a “high price” for the use of chemical weapons in the attack on rebel-held Douma that killed 42 people, but the Pentagon denied US forces were involved in Monday’s strikes. “However, we continue to closely watch the situation and support the ongoing diplomatic efforts to hold those who use chemical weapons, in Syria and otherwise, accountable,” a Pentagon spokesman said.

Separately, the White House put out an account of a telephone conversation between Trump and Emmanuel Macron, in which the US and French presidents “agreed to exchange information on the nature of the attacks and coordinate a strong, joint response”. Macron has said chemical weapons attacks in Syria would cross a “red line” for France and that French forces would strike if the regime was proven to have been involved. However, the French army denied responsibility for Monday’s attack.

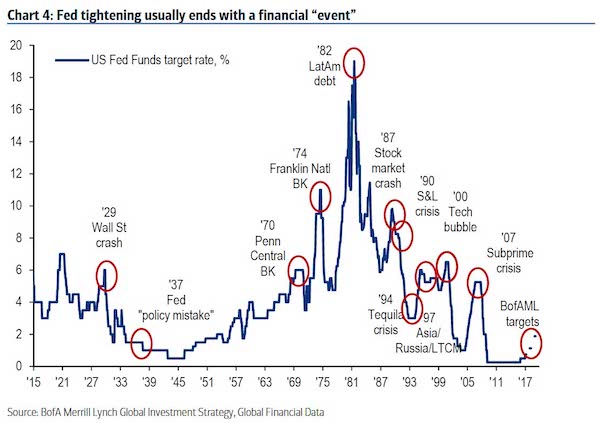

He’s a Wall Street bear who sees more monster market moves coming — with the majority of them leaving stocks deep in the red. The Bleakley Advisory Group’s Peter Boockvar warns there’s more trouble brewing, because the era of easy money is ending, thanks to global central banks hiking borrowing costs. And as fears intensify over a trade war, Boockvar expects a solution to the tariff issue will eventually come at the expense of rising rates. “We could get that resumption of higher interest rates which would then concern the markets, and then retest the [S&P 500 Index] 2500-ish type lows,” the firm’s chief investment officer told CNBC’s “Futures Now” last week.

“We’re late cycle in the market. We’re late cycle in the economy, and you have an intensification in a tightening of monetary policy,” he said. Boockvar, a CNBC contributor, blamed the end of quantitative easing in the United States and Europe for increasing sell-off risks. “We’re a step closer to them wanting to take away negative interest rates. But there are still trillions of dollars of global bonds that have negative yielding rates,” he added. “So, it’s this rate environment that I think is becoming more of a headwind. That really is my main concern.” He doesn’t believe the situation will abate any time soon. Boockvar contended the 10-Year Treasury yield will push back toward 3 percent — preventing the S&P 500 from cracking above its Jan. 26 record high anytime soon.

The Fed generally tightens rates until something breaks. David Rosenberg points out that since 1950 there have been 13 Fed tightening cycles, and 10 of them ended in recession (while the others have often ended in emerging market blow-ups, like the 1994 Mexican peso crisis). Surging delinquency and charge-off rates for smaller banks suggest the breaking point for the economy may come sooner than the Fed and bulls expect.

What happens to stocks during the next recession? The Federal Reserve managed to short-circuit this derating process. In 2011, when quantitative easing, or QE, really kicked in, equity re-engaged with bond yields and P/Es expanded. Like an artificial stimulant, QE inflated all asset prices away from fundamental value and from where they would otherwise have gone. We haven’t seen the lows in bond yields. In the next recession, bond yields in the U.S. will go negative and converge with those in Germany and Japan. The forward U.S. P/E bottomed at about 10.5 times in March 2009 on trough earnings. That was lower than the previous recession.

In the next recession, I would expect the P/E to bottom at about seven times, a lower low with earnings about 30% lower because of the recession. That would put the S&P lower than the 666 low of the previous crash, versus 2671 Thursday afternoon. If a recession unfolds, easy monetary policy won’t stop the market from collapsing. It will play itself out.

When will the recession hit: The Conference Board’s leading indicators look OK for now. What’s different is that problems in the real economy aren’t being reflected in the stock and bond markets. What we may see is the reverse: The stock market and parts of the credit markets collapse and cause problems in the real economy. If confidence collapses because the equity market collapses, then a recession unfolds.

Will the US be hit harder than Japan and Europe in the next bear market? It should be. Traditionally, if the U.S. goes down 20%, the German Dax, though it is cheaper, would tend to go down a little more. Maybe this time it won’t. Japan is the one market we do like now on a long-term basis, and one of the reasons is the buildup of U.S. corporate debt during these past few years. The big bubble is U.S. corporate debt. In contrast, Japan’s corporate debt is collapsing. Over half of its companies have more cash than debt. When the Fed buys U.S. Treasuries, it pulls down all yields. There has been demand for yield, so investors look at corporate bonds as an alternative. Companies have been very keen to issue them, and they have used the money to buy back stock or as a way to enrich management. This is the way QE has washed through the system here.

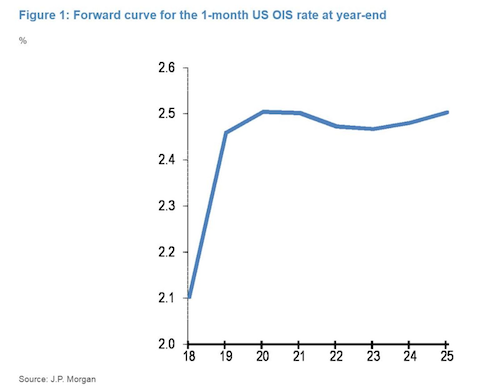

The forward curve of a closely watched proxy for the Federal Reserve’s policy rate has slightly inverted, signaling investors are either pricing in a mistake from central bankers or end-of-cycle dynamics, according to JPMorgan Chase. The inversion of the one-month U.S. overnight indexed swap rate implies some expectation of a lower Fed policy rate after the first quarter of 2020, the bank’s strategists including Nikolaos Panigirtzoglou, wrote in a note Friday. “An inversion at the front end of the U.S. curve is a significant market development, not least because it occurs rather rarely,” they said. “It is also generally perceived as a bad omen for risky markets.”

The negative market signal comes as investors grapple with higher short term borrowing costs, which have risen in the U.S. to levels unseen since the financial crisis. While the strategists admit it is difficult to discern which of the two explanations for the curve inversion carries more weight, flow data suggests it is more likely to be rising expectations of a Fed policy mistake.

A breakdown in the relationship between dollar weakness and Asian central bank intervention poses a risk to Treasuries, stocks and all risky assets, according to Deutsche Bank. Attempts by the Trump administration to clamp down on currency manipulation have limited the ability of central banks across the region to buy U.S. assets when the dollar weakens, and dampen the appreciation of their currencies, strategist Alan Ruskin write in a note Friday. These purchases have historically limited the greenback’s downside and acted as a “put” on Treasury market weakness, he wrote. Such central bank puts are usually associated with successive Federal Reserve chairs willing to support the wider market with loose monetary policy.

While such puts have been a continuous focus for investors, markets now risk overlooking other sources of central bank support that may be slipping as the U.S.’s “synergistic relationship with China,” comes to an end, according to Ruskin. “It is not a coincidence that in this recent period of dollar weakness, Treasury bonds were also soft,” he said. “Historically, foreign central banks of sizable current account surplus countries like China, Taiwan, Korea and Thailand would have been intervening.” According to the strategist, the “end of Chimerica” means American current account deficits are no longer financed to the same degree by Asian central bank reserve recycling of corresponding trade surpluses. That reduction in demand for Treasuries from foreign reserves is coming at a time when U.S. fiscal supply is set to increase dramatically, putting extra pressure on the country’s bond market.

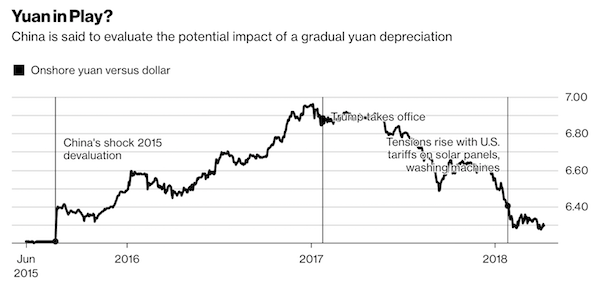

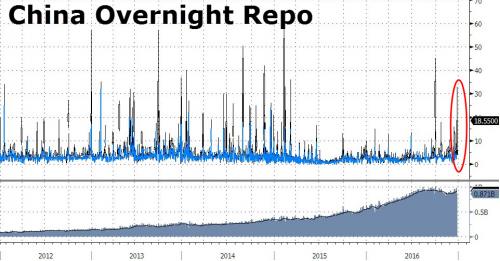

China is evaluating the potential impact of a gradual yuan depreciation, people familiar with the matter said, as the country’s leaders weigh their options in a trade spat with U.S. President Donald Trump that has roiled financial markets worldwide. Senior Chinese officials are studying a two-pronged analysis of the yuan that was prepared by the government, the people said. One part of the analysis looks at the effect of using the currency as a tool in trade negotiations with the U.S., while a second part examines what would happen if China depreciates the yuan to offset the impact of any trade deal that curbs exports. The analysis doesn’t mean officials will carry out a devaluation, which would require approval from top leaders, the people said.

The yuan erased early gains on Monday, weakening 0.1 percent to 6.3110 per dollar in onshore trading at 3:32 p.m. local time. While Trump regularly bashed China on the campaign trail for keeping its currency artificially weak, the yuan has gained about 9 percent against the greenback since he took office as China’s economic growth stabilized, the government clamped down on capital outflows and fears of a credit crisis receded. The Chinese currency touched the strongest level since August 2015 last month and has remained steady in recent weeks despite an escalation of trade tensions between the world’s two largest economies.

While a weaker yuan could help President Xi Jinping shore up China’s export industries in the event of widespread tariffs in the U.S., a devaluation comes with plenty of risks. It would make it easier for Trump to follow through on his threat to brand China a currency manipulator, make it more difficult for Chinese companies to service their mountain of offshore debt, and undermine recent efforts by the government to move toward a more market-oriented exchange rate system. It would also expose China to the risk of local financial-market volatility, something authorities have worked hard to subdue in recent years.

When China unexpectedly devalued the yuan by about 2 percent in August 2015, the move sent shock-waves through global markets. “Is it in their interest to devalue yuan? It’s probably unwise,” said Kevin Lai, chief economist for Asia ex-Japan at Daiwa Capital Markets Hong Kong Ltd. “Because if they use devaluation as a weapon, it could hurt China more than the U.S. The currency stability has helped to create a macro stability. If that’s gone, it could destabilize markets, and things would look like 2015 again.”

A coalition of 23 child advocacy, consumer and privacy groups have filed a complaint with the US Federal Trade Commission alleging that Google is violating child protection laws by collecting personal data of and advertising to those aged under 13. The group, which includes the Campaign for a Commercial-Free Childhood (CCFC), the Center for Digital Democracy and 21 other organisations, alleges that despite Google claiming that YouTube is only for those aged 13 and above, it knows that children under that age use the site. The group states that Google collects personal information on children under 13 such as location, device identifiers and phone numbers and tracks them across different websites and services without first gaining parental consent as required by the US Children’s Online Privacy Protection Act (Coppa).

The coalition urges the FTC to investigate and sanction Google for its alleged violations. “For years, Google has abdicated its responsibility to kids and families by disingenuously claiming YouTube — a site rife with popular cartoons, nursery rhymes, and toy ads — is not for children under 13,” said Josh Golin, executive director of the CCFC. “Google profits immensely by delivering ads to kids and must comply with Coppa. It’s time for the FTC to hold Google accountable for its illegal data collection and advertising practices.”

The group claims that YouTube is the most popular online platform for children in the US, used by about 80% of children aged six to 12 years old. Google has a dedicated app for children called YouTube Kids that was released in 2015 and is designed to show appropriate content and ads to children. It also recently took action to hire thousands of moderators to review content on the wider YouTube after widespread criticism that it allows violent and offensive content to flourish, including disturrbing children’s content and child abuse videos.

The number of buy-to-let investors in the UK rose to a record high of 2.5 million in the latest tax year, new research shows. The increase of 5% on the previous year comes despite the introduction of a host of extra taxes and regulations on the sector. In recent years, the government has brought in a 3% Stamp Duty levy, new stress tests for home loans, and ended mortgage interest tax relief. The number of landlords has increased 27% in the past five years, up from 1.97 million in 2011-12, research by London-focused estate agent Ludlow Thompson found.

Landlords now own an average of 1.8 buy-to-let properties each – a figure that has risen for the fifth consecutive year. The data suggests that landlords continue to see residential property, especially in London, as a strong investment, despite signs that house price growth has stalled or even gone into reverse in some areas in the last year. Investors have seen annual returns of almost 10% since 2000, Ludlow Thompson said. Chairman Stephen Ludlow said the rising number of landlords shows the enduring appeal of investing in buy-to-let. “The long-term picture for the buy-to-let market remains strong,” he said.

Support is growing for a fresh referendum on the final Brexit deal, according to a new poll showing the public back the idea for the first time. The survey found that 44% of people want a vote on the exit terms secured by Theresa May, amid continued uncertainty over the withdrawal agreement. That is a clear eight points ahead of the 36% who reject a further referendum, the research conducted for the anti-Brexit Best for Britain group showed. The group pointed to evidence that “Brexit is sharpening the British public’s minds” and called for MPs to respond to the people’s growing desire for a “final say”.

The referendum would be held on the details of the deal the prime minister must strike by the autumn – on both the planned transition period and a “framework” for a permanent trade and security relationship. Eloise Todd, Best for Britain’s chief executive, said voters should be allowed to choose between the details of the future on offer outside the EU, or staying inside the bloc. “Now there is a decisive majority in favour of a final say for the people of our country on the terms of Brexit. This poll is a turning point moment,” she said. “The only democratic way to finish this process is to make sure the people of this country – not MPs across Europe – have the final say, giving them an informed choice on the two options available to them: the deal the government brings back and our current terms.

Renowned trends researcher Gerald Celente says the trade war President Trump is starting against China must be fought for America to survive. Celente explains, “We have lost 3.5 million jobs (to China). Some 70,000 manufacturing plants have closed. Why would anybody be fighting Trump to do a reversal of us being in a merchandise trade deficit of $365 billion? Tell me any two people that would do business with each other and one side takes a huge loss and keeps taking it. . . So, why would people argue and fight and bring down the markets because Trump wants to bring back jobs and readjust a trade deficit that, by any standard, is destroying the nation?” Who’s to blame for the lopsided trade deficits destroying the middle class of America?

Look no further than the politicians and corporations buying them off. Celente charges, “They sold us out. The European companies and the American companies sold us out, and the people fighting Trump are also the big retailers because they’ve got their slave labor making their stuff over there. They bring it back here and mark up the price, and they make more money. If they have to pay our people to do that work, they have to pay them a living wage and they can’t make enough profit. That’s who is fighting us. . You go back to our top trend in 2017, and it was China was going to be the leader in AI (artificial intelligence) now and beyond, and that is exactly what happened. All the corporations have sold us out. . . .The murderers and the thieves sold out America.”

Celente thinks the odds are there will not be a financial crash in 2018 “because they are repatriating all that dough from overseas at a very low tax rate and because of the tax cuts from 35% to 21%. These are the facts. In the first three months of this year, there have been more stock buybacks and mergers and acquisitions activity than ever before in this short period of time because of all that cheap money going back into the corporations. That’s what’s keeping the markets up.”

Oil giant Shell was aware of the consequences of climate change, and the role fossil fuels were playing in it, as far back as 1988, documents unearthed by a Dutch news organisation have revealed. They include a calculation that the oil company’s products alone were responsible for 4% of total global carbon emissions in 1984. They also predict that changes to sea levels and weather would be “larger than any that have occurred over the past 12,000 years”. As a result, the documents foresee impacts on living standards, food supplies and other major social, political and economic consequences.

In The Greenhouse Effect, a 1988 internal report by Shell scientists, the authors warned that “by the time the global warming becomes detectable it could be too late to take effective countermeasures to reduce the effects or even to stabilise the situation”. They also acknowledged that many experts predicted an increase in global temperature would be detectable by the end of the century. They went on to state that a “forward-looking approach by the energy industry is clearly desirable”, adding: “With the very long time scales involved, it would be tempting for society to wait until then before doing anything. “The potential implications for the world are, however, so large that policy options need to be considered much earlier. And the energy industry needs to consider how it should play its part.”

It is symptomatic of the colonial-settler prerogative that has sought to eliminate the offensive presence of the natives from any profitable territory. In 21st-century Australia, the “dispersal” that began with European invasion continues through the gentrification of city suburbs where Indigenous identities persist. In the colonial argot of the 19th century, dispersal euphemistically described a bloody practice of massacre and forced dispossession of First Nations peoples, often performed as punishment for perceived theft, or any other form of resistance to the colonisers more generally. In the early and mid-20th century, blackfullas were forcibly coerced into government reserves most commonly known as “missions”.

The overarching intent of these “protection” policies was to ensure the dissolution of First Nations culture and traditional governance structures, pushing mob to develop from “their former primitive state to the standards of the white man”, as the Aboriginal Protection Board said in 1935. When the missions began to be disbanded after the second world war, it forced significant Indigenous migration from the bush to towns and cities, where we repopulated places like Fitzroy, Brisbane’s West End and particularly Redfern in great numbers. This 1950s policy of “assimilation” was essentially a state-sanctioned experiment to force Indigenous people to give up their beliefs and traditions as they adapted to urban life.

[..] Yet the place of blackfullas in Australia’s cities is under threat. Faced with rapid gentrification and associated rental and ownership price hikes, urban Indigenous populations continue to relocate to the outer suburbs, where cheaper housing is usually located. The trend could be viewed as a contemporary iteration of the dispersals of the past – decidedly less bloody, though equally impelled by capitalistic imperatives.

The coral bleaching events that have devastated the Great Barrier Reef in recent years have also taken their toll on the region’s fish population, according to a new study. While rising temperatures on the reef killed nearly all the coral in some sections, the effects on the wider marine community have been less clear. Now, scientists have begun to establish the long-term effects of bleaching events on the Great Barrier Reef’s fish population. This work is essential for researchers trying to understand what will happen to coral reef ecosystems as global warming makes mass bleaching events more frequent. “The widespread impacts of heat stress on corals have been the subject of much discussion both within and outside the research community,” said PhD student Laura Richardson of the ARC Centre of Excellence for Coral Reef Studies.

“We are learning that some corals are more sensitive to heat stress than others, but reef fishes also vary in their response to these disturbances.” Ms Richardson and her collaborators studied reefs in the northern section of the Great Barrier Reef, where around two-thirds of corals were killed in the 2016 bleaching event that followed a global heatwave. The researchers found there were “winners” and “losers” among the fish species on the reef, but overall there was a significant decline in the variety of species following bleaching. Their results were published in the journal Global Change Biology. “Prior to the 2016 mass bleaching event, we observed significant variation in the number of fish species, total fish abundance and functional diversity among different fish communities,” said co-author Dr Andrew Hoey.

“Six months after the bleaching event, however, this variation was almost entirely lost.” Predictably, the scientists noted that fish with intimate associations with corals suffered severe losses. Butterflyfish, which feed on corals, faced the steepest declines. In response to the looming threat of coral bleaching, scientists have called for “radical interventions” to save the world’s reefs. Some have suggested that more than 90% of corals could die by 2050 at the current rate of global warming.

This really is the firefighter setting his own house on fire so he can play the hero. There’s often talk of central bankers taking away the punch bowl, but we need to take away the punch bowl from them. Urgently.

Central bankers, basking in a moment of synchronized growth and a global economy less dependent on easy-money policies, are thinking about what they will do when the next economic meltdown happens. ECB President Mario Draghi said Thursday that central banks might need to reuse some of the weapons employed to fight the last war, most notably negative interest rates. Federal Reserve and ECB officials, who are gathered in Washington for the fall meetings of the IMF and World Bank, are using a tranquil period to debate the type of monetary policies central banks might pursue. The world’s two most influential central banks signaled no shifts in strategy – in the Fed’s case, to raise rates gradually and shrink its bond portfolio, and in the ECB’s, to announce a slowdown of its bond-purchase program as soon as its next policy meeting on Oct. 26.

But while current policies are stepping away from the bond-purchase programs known as quantitative easing, central bankers are opening the door for a future that could include more negative interest rates and periods of higher inflation following recession. The discussions are still largely hypothetical. Ever since the global financial crisis of 2007-09, central bankers have wished for more moments when they could gather in calm and openly spitball monetary policy ideas without the risk of derailing recovery. That moment has finally arrived. Mr. Draghi said that negative interest rates, an untested policy for the ECB until 2014, had been a success, and that the decision to push the ECB’s target rate into negative territory hadn’t hurt bank profitability as critics suggested it would.

“We haven’t seen the distortions that people were foreseeing,” Mr. Draghi said at the Peterson Institute for International Economics in Washington. “We haven’t seen bank profitability going down; in fact, it is going up.” Mr. Draghi reiterated that the ECB would maintain its negative target rate “well past” the time it steps back from its bond-purchase program, underscoring growing comfort in the negative-rate strategy. And while Mr. Draghi endorsed negative rates, current and former Fed officials engaged in an unusually open discussion about changing the target for 2% inflation. That discussion was kicked off by former Federal Reserve Chairman Ben Bernanke, who presented a paper Thursday morning at the Peterson Institute arguing the Fed could overshoot its target for 2% inflation to make up for periods of recession in which inflation ran too low.

Bank of Japan Governor Haruhiko Kuroda said on Friday he did not see any signs of bubbles or excesses building up in U.S., European and Japanese markets as a result of heavy money printing by their central banks. Kuroda also dismissed some analysts’ criticism that the BOJ’s purchases of exchange-traded funds (ETF) were distorting financial markets or dominating Japan’s stock market. “I don’t think we have a very big share” of Japan’s total stock market capitalisation, he told reporters after attending the Group of 20 finance leaders’ gathering. The IMF painted a rosy picture of the global economy in its World Economic Outlook earlier this week, but warned that prolonged easy monetary policy could be sowing the seeds of excessive risk-taking.

Kuroda said that while policymakers should not be complacent about their economies, he did not see huge risks materializing as a result of their policies. Although major central banks deployed massive stimulus programmes to battle the global financial crisis, they have always scrutinized whether their policies were causing excessive risk-taking, he said. “I don’t think we’re seeing excesses building up and emerging as a big risk,” Kuroda said, adding that recent rises in global stock prices reflected strong corporate profits in Japan, the United States and Europe. He added that Japan’s economy was on track for a steady recovery that will likely gradually push up inflation and wages. “I don’t see any big risk for Japan’s economy. But there could be external risks, such as geopolitical ones, so we’re watching developments carefully,” he said.

Seccora Jaimes knows that she is not living in the land of opportunity. Her hometown has one of the highest unemployment rates in the nation, at 9.1%. Jaimes, 34, recently got laid off from the beauty school where she taught cosmetology, and hasn’t yet found another job. Her daughter, 17, wants the family to move to Los Angeles, so that she can attend one of the nation’s top police academies. Jaimes’s husband, who works in warehousing, would make much more money in Los Angeles, she told me. But one thing is stopping them: The cost of housing. “I don’t know if we could find a place out there that’s reasonable for us, that we could start any job and be okay,” she told me. Indeed, the average rent for a two-bedroom apartment in Merced, in California’s Central Valley, is $750. In Los Angeles, it’s $2,710.

America used to be a place where moving one’s family and one’s life in search of greater opportunities was common. During the Gold Rush, the Depression, and the postwar expansion West millions of Americans left their hometowns for places where they could earn more and provide a better life for their children. But mobility has fallen in recent years. While 3.6% of the population moved to a different state between 1952 and 1953, that number had fallen to 2.7% between 1992 and 1993, and to 1.5% between 2015 and 2016. (The share of people who move at all, even within the same county, has fallen too, from 20% in 1947 to 11.2% today.) Of course, it wasn’t simply “moving” that mattered—it was that they moved to specific areas that were growing.

When farming jobs were plentiful in the Midwest, for example, people moved there—in 1900, states including Iowa and Missouri were more populous than California. Black men who moved from to the North from the South earned at least 100% more than those who stayed, according to work by Leah Platt Boustan, an economist at Princeton. Additionally, for most of the 20th century, both janitors and lawyers could earn a lot more living in the tri-state area of New York, New Jersey, and Connecticut than they could living in the Deep South, so many people moved, according to Peter Ganong, an economist at the University of Chicago. With less labor supply in the regions that they left, wages would then increase there, and fall in the regions they were moving to, as the supply of workers increased.

As a result, for more than 100 years, the average incomes of different regions were getting closer and closer together, something economists call regional income convergence. Wages in poorer cities were growing 1.4% faster than wages in richer cities for much of the 20th century, according to Elisa Giannnone, a post-doctoral fellow at Princeton. But over the past 30 years, that regional income convergence has slowed. Economists say that is happening because net migration—the tendency of large numbers of people to move to a specific place—is waning, meaning that the supply of workers isn’t increasing fast enough in the rich areas to bring wages down, and isn’t falling fast enough in the poor areas to bring wages up.

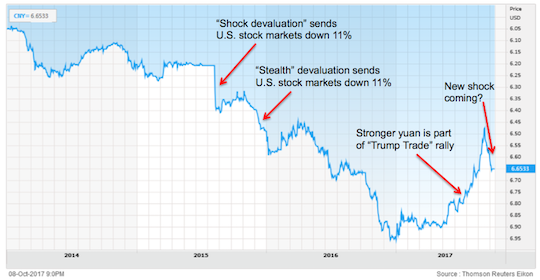

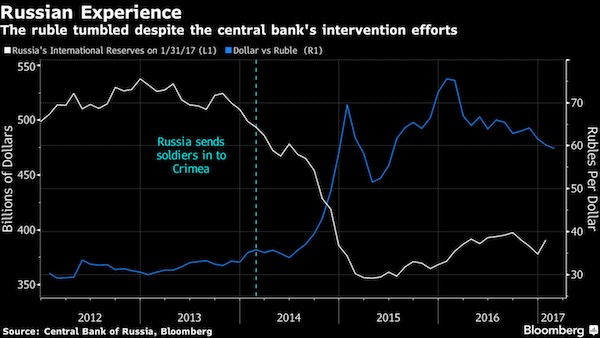

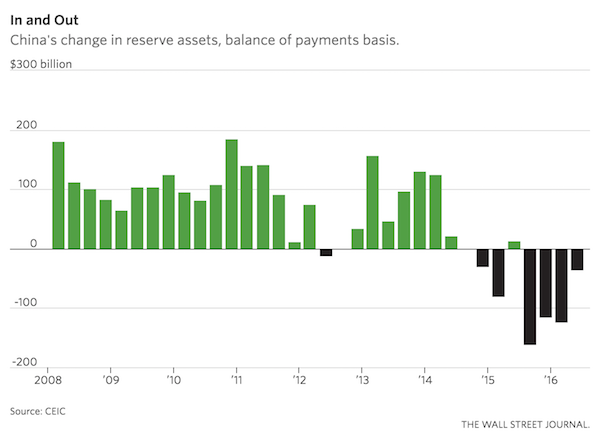

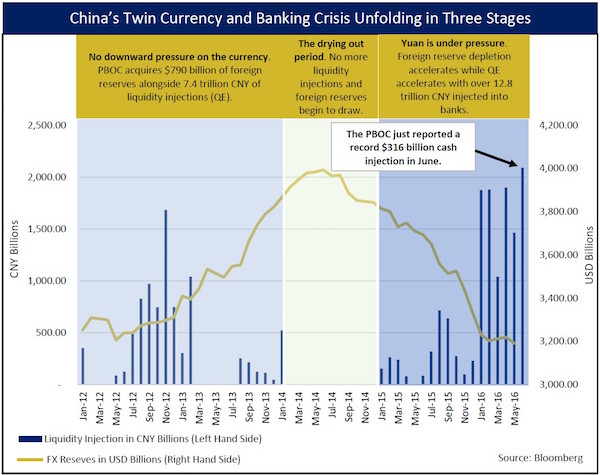

In August 2015, China engineered a sudden shock devaluation of the yuan. The dollar gained 3% against the yuan in two days as China devalued. The results were disastrous. U.S. stocks fell 11% in a few weeks. There was a real threat of global financial contagion and a full-blown liquidity crisis. A crisis was averted by Fed jawboning, and a decision to put off the “liftoff” in U.S. interest rates from September 2015 to the following December. China conducted another devaluation from November to December 2015. This time China did not execute a sneak attack, but did the devaluation in baby steps. This was stealth devaluation. The results were just as disastrous as the prior August. U.S. stocks fell 11% from January 1, 2016 to February 10. 2016. Again, a greater crisis was averted only by a Fed decision to delay planned U.S. interest rate hikes in March and June 2016. The impact these two prior devaluations had on the exchange rate is shown in the chart below.

Major moves in the dollar/yuan cross exchange rate (USD/CNY) have had powerful impacts on global markets. The August 2015 surprise yuan devaluation sent U.S. stocks reeling. Another slower devaluation did the same in early 2016. A stronger yuan in 2017 coincided with the Trump stock rally. A new devaluation is now underway and U.S. stocks may suffer again.

[..] China escaped the impossible trinity in 2015 by devaluing their currency. China escaped the impossible trinity again in 2017 using a hat trick of partially closing the capital account, raising interest rates, and allowing the yuan to appreciate against the dollar thereby breaking the exchange rate peg. The problem for China is that these solutions are all non-sustainable. China cannot keep the capital account closed without damaging badly needed capital inflows. Who will invest in China if you can’t get your money out? China also cannot maintain high interest rates because the interest costs will bankrupt insolvent state owned enterprises and lead to an increase in unemployment, which is socially destabilizing. China cannot maintain a strong yuan because that damages exports, hurts export-related jobs, and causes deflation to be imported through lower import prices. An artificially inflated currency also drains the foreign exchange reserves needed to maintain the peg.

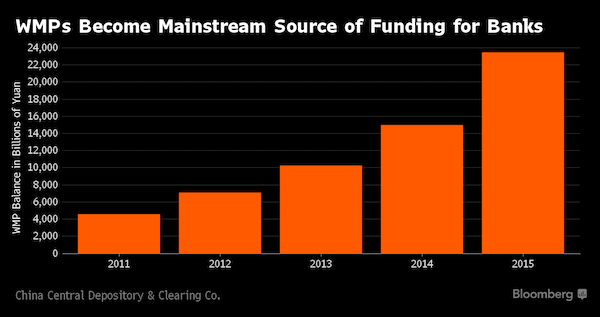

[..] Both Trump and Xi are readying a “gloves off” approach to a trade war and renewed currency war. A maxi-devaluation of the yuan is Xi’s most potent weapon. Finally, China’s internal contradictions are catching up with it. China has to confront an insolvent banking system, a real estate bubble, and a $1 trillion wealth management product Ponzi scheme that is starting to fall apart. A much weaker yuan would give China some policy space in terms of using its reserves to paper over some of these problems. Less dramatic devaluations of the yuan led to U.S. stock market crashes. What does a new maxi-devaluation portend for U.S. stocks?

Skepticism in global equity markets is getting expensive. From Japan to Brazil and the U.S. as well as places like Greece and Ukraine, an epic year in equities is defying naysayers and rewarding anyone who staked a claim on corporate ownership. Records are falling, with about a quarter of national equity benchmarks at or within 2% of an all-time high. “You’ve heard people being bearish for eight years. They were wrong,” said Jeffrey Saut, chief investment strategist at St. Petersburg, Florida-based Raymond James Financial Inc., which oversees $500 billion. “The proof is in the returns.” To put this year’s gains in perspective, the value of global equities is now 3 1/2 times that at the financial crisis bottom in March 2009.

Aided by an 8% drop in the U.S. currency, the dollar-denominated capitalization of worldwide shares appreciated in 2017 by an amount – $20 trillion – that is comparable to the total value of all equities nine years ago. And yet skeptics still abound, pointing to stretched valuations or policy uncertainty from Washington to Brussels. Those concerns are nothing new, but heeding to them is proving an especially costly mistake. Clinging to such concerns means discounting a harmonized recovery in the global economy that’s virtually without precedent — and set to pick up steam, according to the IMF. At the same time, inflation remains tepid, enabling major central banks to maintain accommodative stances. “When policy is easy and growth is strong, this is an environment more conducive for people paying up for valuations,” said Andrew Sheets, chief cross-asset strategist at Morgan Stanley.

“The markets are up in line with what the earnings have done, and stronger earnings helped drive a higher level of enthusiasm and a higher level of risk taking.” The numbers are impressive: more than 85% of the 95 benchmark indexes tracked by Bloomberg worldwide are up this year, on course for the broadest gain since the bull market started. Emerging markets have surged 31%, developed nations are up 16%. Big companies are becoming huge, from Apple to Alibaba. Technology megacaps occupy all top six spots in the ranks of the world’s largest companies by market capitalization for the first time ever. Up 39% this year, the $1 trillion those firms added in value equals the combined worth of the world’s six-biggest companies at the bear market bottom in 2009. Apple, priced at $810 billion, is good for the total value of the 400 smallest companies in the S&P 500.

If we use GDP as a broad measure of prosperity, we are 160% better off than we were in 1980 and 35% better off than we were in 2000. Other common metrics such as per capita (per person) income and total household wealth reflect similarly hefty gains. But are we really 35% better off than we were 17 years ago, or 160% better off than we were 37 years ago? Or do these statistics mask a pervasive erosion in our well-being? As I explained in my book Why Our Status Quo Failed and Is Beyond Reform, we optimize what we measure, meaning that once a metric and benchmark have been selected as meaningful, we strive to manage that metric to get the desired result. Optimizing what we measure has all sorts of perverse consequences. If we define “winning the war” by counting dead bodies, then the dead bodies pile up like cordwood.

If we define “health” as low cholesterol levels, then we pass statins out like candy. If test scores define “a good education,” then we teach to the tests. We tend to measure what’s easily measured (and supports the status quo) and ignore what isn’t easily measured (and calls the status quo into question). So we measure GDP, household wealth, median incomes, longevity, the number of students graduating with college diplomas, and so on, because all of these metrics are straightforward. We don’t measure well-being, our sense of security, our faith in a better future (i.e. hope), experiential knowledge that’s relevant to adapting to fast-changing circumstances, the social cohesion of our communities and similar difficult-to-quantify relationships. Relationships, well-being and internal states of awareness are not units of measurement.

While GDP has soared since 1980, many people feel that life has become much worse, not much better: many people feel less financially secure, more pressured at work, more stressed by not-enough-time-in-the-day, less healthy and less wealthy, regardless of their dollar-denominated “wealth.” Many people recall that a single paycheck could support an entire household in 1980, something that is no longer true for all but the most highly paid workers who also live in locales with a modest cost of living.

The cheating crisis engulfing Kobe Steel just got bigger. Chief Executive Hiroya Kawasaki on Friday revealed that about 500 companies had received its falsely certified products, more than double its earlier count, confirming widespread wrongdoing at the steelmaker that has sent a chill along global supply chains. The scale of the misconduct at Japan’s third-largest steelmaker pummeled its shares as investors, worried about the financial impact and legal fallout, wiped about $1.8 billion off its market value this week. As the company revealed tampering of more products, the crisis has rippled through supply chains across the world in a body blow to Japan’s reputation as a high-quality manufacturing destination. A contrite Kawasaki told a briefing the firm plans to pay customers’ costs for any affected products.

“There has been no specific requests, but we are prepared to shoulder such costs after consultations,” he said, adding the products with tampered documentation account for about 4% of the sales in the affected businesses. Yoshihiko Katsukawa, a managing executive officer, told reporters that 500 companies were now known to be affected by the tampering. Kobe Steel initially said 200 firms were affected when it admitted at the weekend it had falsified data about the quality of aluminum and copper products used in cars, aircraft, space rockets and defense equipment. Asked if he plans to step down, Kawasaki said: “My biggest task right now is to help our customers make safety checks and to craft prevention measures.”

“The manufacturers can now exploit their monopoly positions, created by the patents, by marketing their drugs for conditions for which they never got regulatory approval.”

Once again, an out-of-control industry is threatening public health on a mammoth scale Over a 40-year career, Philadelphia attorney Daniel Berger has obtained millions in settlements for investors and consumers hurt by a rogues’ gallery of corporate wrongdoers, from Exxon to R.J. Reynolds Tobacco. But when it comes to what America’s prescription drug makers have done to drive one of the ghastliest addiction crises in the country’s history, he confesses amazement. “I used to think that there was nothing more reprehensible than what the tobacco industry did in suppressing what it knew about the adverse effects of an addictive and dangerous product,” says Berger. “But I was wrong. The drug makers are worse than Big Tobacco.”

The U.S. prescription drug industry has opened a new frontier in public havoc, manipulating markets and deceptively marketing opioid drugs that are known to addict and even kill. It’s a national emergency that claims 90 lives per day. Berger lays much of the blame at the feet of companies that have played every dirty trick imaginable to convince doctors to overprescribe medication that can transform fresh-faced teens and mild-mannered adults into zombified junkies. So how have they gotten away with it? The prescription drug industry is a strange beast, born of perverse thinking about markets and economics, explains Berger. In a normal market, you shop around to find the best price and quality on something you want or need—a toaster, a new car. Businesses then compete to supply what you’re looking for.

You’ve got choices: If the price is too high, you refuse to buy, or you wait until the market offers something better. It’s the supposed beauty of supply and demand. But the prescription drug “market” operates nothing like that. Drug makers game the patent and regulatory systems to create monopolies over every single one of their products. Berger explains that when drug makers get patent approval for brand-name pharmaceuticals, the patents create market exclusivity for those products—protecting them from competition from both generics and brand-name drugs that treat the same condition. The manufacturers can now exploit their monopoly positions, created by the patents, by marketing their drugs for conditions for which they never got regulatory approval. This dramatically increases sales. They can also charge very high prices because if you’re in pain or dying, you’ll pay virtually anything.

Luxury electric vehicle maker Tesla fired about 400 employees this week, including associates, team leaders and supervisors, a former employee told Reuters on Friday. The dismissals were a result of a company-wide annual review, Tesla said in an emailed statement, without confirming the number of employees leaving the company. “It’s about 400 people ranging from associates to team leaders to supervisors. We don’t know how high up it went,” said the former employee, who worked on the assembly line and did not want to be identified.

Though Tesla cited performance as the reason for the firings, the source told Reuters he was fired in spite of never having been given a bad review. The Palo Alto, California-based company said earlier in the month that “production bottlenecks” had left Tesla behind its planned ramp-up for the new Model 3 mass-market sedan. The company delivered 220 Model 3 sedans and produced 260 during the third quarter. In July, it began production of the Model 3, which starts at $35,000 – half the starting price of the Model S. Mercury News had earlier reported about the firing of hundreds of employees by Tesla in the past week.

As things stand at the moment, eighteen months from now the UK will leave the EU without any agreement on trade regulation or tariffs, either with the EU or any of the other countries with which it currently has trade agreements. The arrangements which assure the smooth running of 60 percent of our goods trade will disappear. Once we are outside the regulatory framework, many products, particularly in highly regulated areas like agriculture and pharmaceuticals, will no longer be accredited for sale in Europe. Aeroplanes will be unable to fly to and from the EU to the UK. Those goods which can still legally be traded with the EU will face lengthy customs checks. Integrated supply chains and just-in-time manufacturing processes will be severely disrupted and, in some cases, damaged beyond repair. Unless politicians do something, that’s where we are heading.

International trade and commerce doesn’t just happen. It is facilitated by a framework of agreements on tariffs, quotas and regulations. Without these, trade is either very expensive or, in some cases, simply illegal. Therefore, if the UK were to leave the EU without concluding a trade deal, things wouldn’t simply stay the same. They would be very different and very damaging. Of course, it would be disruptive for the rest of the EU too, although it is much easier to find new suppliers and customers in a bloc of 27 countries than it is in a stand alone country with no trade deals. Even so, most of us have assumed that common sense will prevail at some point. No-one in their right mind would let such a thing happen so surely both sides will do what is necessary to between now and March 2019 to avoid it.

Incredibly, though, our government, egged on by ideologues on its own back benches, has been talking up the prospect of a no-deal Brexit, apparently as a negotiating ploy to make the EU realise that we are serious about walking away. Almost as soon as the no-deal idea was suggested, Phillip Hammond said that he was not willing to set aside any money to fund it. In any organisation, that’s a sure-fire sign of a project that’s going nowhere. If the finance director won’t even stump up the cash for the planning phase, you might as well forget the whole thing. Mr Hammond said that he would wait until “the very last moment” before committing any money to prepare for a no-deal scenario. Which means it’s not going to happen because the very last moment passed some time ago, most probably before we even had the referendum.

Britain must commit to paying what it owes to the European Union before talks can begin about a future relationship with the bloc after Brexit, European Commission President Jean-Claude Juncker said on Friday. “The British are discovering, as we are, day after day new problems. That’s the reason why this process will take longer than initially thought,” Juncker said in a speech to students in his native Luxembourg. “We cannot find for the time being a real compromise as far as the remaining financial commitments of the UK are concerned. As we are not able to do this we will not be able to say in the European Council in October that now we can move to the second phase of negotiations,” Juncker said. “They have to pay, they have to pay, not in an impossible way. I‘m not in a revenge mood. I‘m not hating the British.” The EU has told Britain that a summit next week will conclude that insufficient progress has been made in talks for Brussels to open negotiations on a future trade deal.

The president of the European commission has spoken of his regret at Spain’s failure to follow his advice and do more to head off the crisis in Catalonia, but claimed that any EU intervention on the issue now would only cause “a lot more chaos”. Speaking to students in Luxembourg on Friday, Jean-Claude Juncker said he had told the Spanish prime minister, Mariano Rajoy, that his government needed to act to stop the Catalan situation spinning out of control, but that the advice had gone unheeded. “For some time now I asked the Spanish prime minister to take initiatives so that Catalonia wouldn’t run amok,” he said. “A lot of things were not done.” Juncker said that while he wished to see Europe remain united, his hands were tied when it came to Catalan independence.

“People have to undertake their responsibility,” he said. “I would like to explain why the commission doesn’t get involved in that. A lot of people say: ‘Juncker should get involved in that.’ “We do not do it because if we do … it will create a lot more chaos in the EU. We cannot do anything. We cannot get involved in that.” Juncker said that while he often acted as a negotiator and facilitator between member states, the commission could not mediate if calls to do so came only from one side – in this case, the Catalan government. Rajoy has rejected calls for mediation, pointing out that the recent Catalan independence referendum was held in defiance of the Spanish constitution and the country’s constitutional court. “There is no possible mediation between democratic law and disobedience or illegality,” he said on Wednesday.

Despite his refusal to intervene, however, Juncker warned the international community that the political crisis in Spain could not be ignored. “OK, nobody is shooting anyone in Catalonia – not yet at least. But we shouldn’t understate that matter, though,” he added. he commission president also spoke more generally about the fragmentation of national identities within Europe, saying he feared that if Catalonia became independent, other regions would follow. “I am very concerned because the life in communities seems to be so difficult,” he said. “Everybody tries to find their own in their own way and they think that their identity cannot live in parallel to other people’s identity. “But if you allow – and it is not up to us of course – but if Catalonia is to become independent, other people will do the same. I don’t like that. I don’t like to have a euro in 15 years that will be 100 different states. It is difficult enough with 17 states. With many more states it will be impossible.”

“The people who deliver that way of life, and profit from it, are every bit as sincerely wishful about it as the underpaid and overfed schnooks moiling in the discount aisles. ”

The original Mad Max was little more than an extended car chase — though apparently all that people remember about it is the desolate desert landscape and Mel Gibson’s leather jumpsuit. As the series wore on, both the vehicles and the staged chases became more spectacularly grandiose, until, in the latest edition, the movie was solely about Charlize Theron driving a truck. I always wondered where Mel got new air filters and radiator hoses, not to mention where he gassed up. In a world that broken, of course, there would be no supply and manufacturing chains. So, of course, Blade Runner 2049 opens with a shot of the detective played by Ryan Gosling in his flying car, zooming over a landscape that looks more like a computer motherboard than actual earthly terrain.