Harris&Ewing Buying Army surplus food sold at fish market 1919

The referendum will be held against the backdrop of a warzone.

• Greek Banks Down To €500 Million In Cash Reserves As Economy Crashes (AEP)

Greece is sliding into a full-blown national crisis as the final cash reserves of the banking system evaporate by the hour and swathes of industry start to shut down, precipitating the near disintegration of the ruling coalition. Business leaders have been locked in talks with the Bank of Greece, pleading for the immediate release of emergency liquidity funds (ELA) to cover food imports and pharmaceutical goods before the tourist sector hits a brick wall. Officials say the central bank will release the funds as soon as Friday, but this is a stop-gap measure at best. “We are on a war footing in this country,” said Yanis Varoufakis, the Greek finance minister. The daily allowance of cash from many ATM machines has already dropped from €60 to €50, purportedly because €20 notes are running out.

Large numbers are empty. The financial contagion is spreading fast as petrol stations and small businesses stop accepting credit cards. Constantine Michalos, head of the Hellenic Chambers of Commerce, said lenders are simply running out of money. “We are reliably informed that the cash reserves of the banks are down to €500m. Anybody who thinks they are going to open again on Tuesday is day-dreaming. The cash would not last an hour,” he said. “We are in an extremely dangerous situation. Greek companies have been excluded from the electronic transfers of Europe’s Target2 system. The entire Greek business community is unable to import anything, and without raw materials they can’t produce anything,” he said.

Pavlos Deas, owner of an olive processing factory in Chalkidiki, told The Telegraph that he may have to shut down a plant employing 250 people within days. “We can’t send any money abroad to our suppliers. Three of our containers have been stopped at customs control because the banks can’t give a bill of landing. One is full of Spanish almonds, the others full of Chinese garlic,” he said. “We don’t know how we are going to execute and export an order of 60 containers for the US. We don’t even have enough gas. We asked for 10,000 litres but they are only letting us have 2,000. It’s being rationed by the day. Factories are closing around us in a domino effect and we’re all going to lose everything if this goes on,” he said.\

Read more …

Financial warfare.

• Cash Crunch Hits Everyday Life in Greece (WSJ)

At an automated teller machine underneath the Acropolis, Angeliki Andreaki clutched her debit card with both hands. She pays her bills in cash, and €330 in rent and €39 in telephone bills were due Wednesday. “Tsipras has turned this country into North Korea,” the 83-year-old Ms. Andreaki said Tuesday, shaking her head about Greece’s prime minister, Alexis Tsipras. “I can’t believe at this age I have to line up to get rationed cash.” She withdrew as much as she could—just €60 ($66)—and went straight to pay her phone bill. She said she would have to come back for five more days to get enough cash for the rent. This is everyday life in Greece since it shut down its banking system and imposed controls to prevent money from flooding out of the country.

Greece’s ruling party continued to say it was offering new compromises to its creditors and urged a “no” vote in Sunday’s referendum. European leaders dismissed the overtures as insufficient and said they would hold off on further negotiations until the vote. The first opinion surveys in Greece since Mr. Tsipras called for the referendum show conflicting results but suggest the outcome could be close. The freezing of Greece’s banking system is the most dramatic moment of the country’s five-year debt crisis—and perhaps its most pivotal. Since Monday, Greeks can get only €60 a day at cash machines and can’t transfer money abroad. How long the remaining cash lasts and how unsettled Greeks become will be big factors in Sunday’s referendum on creditors’ demands for more austerity in exchange for more bailout funds.

The tighter the squeeze, the more Greeks might vote “yes” to reconcile with creditors, analysts say. As of Wednesday, Greece’s banking system had about €1 billion in cash left, according to a person familiar with the situation. Even with the €60-a-day limit on ATM withdrawals from Greek’s closed banks, “it’s a matter of a few days” until the money runs out, this person said. By Wednesday, many ATMs in central Athens had constant lines of people waiting to withdraw their daily limit. The crunch has suffused the economy. Merchants report lower spending. Wholesalers can’t pay for supplies. Importers’ foreign counterparts won’t trade.

Read more …

“..expect biased vote counting in favor of a “YES” vote to stay in the euro..”

• Troika Maneuvering to Rig Greek Referendum (Martin Armstrong)

In a TV interview, Mr. Varoufakis said very clearly, “This is a very dark moment for Europe. They have closed our banks for the sole purpose of blackmailing what? Getting a ‘Yes’ vote on a non-sustainable solution that would be bad for Europe.” I must admit, most politicians do not come even close to the truth, but Varoufakis seems to be the ONLY finance minister who understands the demands of the Troika are not plausible for any nation. Merkel has tried to skirt any responsibility by saying this is a Troika decision. One must seriously ask, are those in the Troika just totally brain-dead? Their blackmail and economic war against Greece will be evidence to ensure that Britain leaves the EU. The ONLY thing that saved Britain was Maggie Thatcher’s effort to keep Britain out of the euro for she knew far too well where it would lead.

The view in Poland is also now anti-euro. Any Brit who now does not vote to get out of the EU and the grips of the Troika is ignorant of world events and the political power play going on. The EU leaders will not travel to Athens until after the referendum. Suddenly they realize that their powers are so off the wall that they dare not expose their own schemes. Hollande of France wants a resolution for he fears a Frexit is gaining momentum. Obama wants a resolution, fearing Greece will be forced into the arms of Russia, breaking down NATO. Yet through all of this, there is no hope because those in power are clueless. The Troika refuses to solve the euro crisis because they only see their own self-interest and assume they can force their will upon all the people.

The Troika is doing everything in their power to rig the Greek referendum to make it appear that the Greek people want Brussels. The Troika deliberately closed the banks to punish the people of Greece, and to show them what exiting the euro means. This appears to be their only way of diverting the crisis with orchestrating a fake “YES” vote to economic suicide. The Troika will attempt to rig the referendum as they did with the Scottish elections. So expect biased vote counting in favor of a “YES” vote to stay in the euro. As Stalin said, “Those who vote decide nothing. Those who count the vote decide everything.”

Read more …

Maybe teh Troika can move in on that as well.

• Greece’s Highest Court To Rule On Legality Of Referendum (Guardian)

Greece’s highest administrative court will rule on whether the country’s bailout referendum violates the constitution, amid growing concern that the hastily organised vote falls short of democratic standards. With less than 48 hours until polling day on Sunday, the yes and no sides will stage large rallies in Athens on Friday evening. The Greek prime minister, Alexis Tsipras, is expected to turn out at the no rally, having attacked his eurozone partners for trying to “blackmail” his country into accepting a bad deal. Greeks are being asked whether to support an EU bailout deal that would grant the debt-stricken country money in exchange for spending cuts and further reform. However, the bailout plan no longer exists, having lapsed on 30 June.

Eurozone leaders have lined up to say that voting no means saying goodbye to Greece’s eurozone membership, but Greece’s radical left Syriza-led government insists a no vote would simply boost its negotiating hand. Later on Friday, the Council of State will determine whether the vote violates Greece’s constitution, which bans referendums on fiscal policy. Europe’s top human rights body, the Council of Europe, has already said the vote falls short of international standards, because the poll was called at short notice and the questions asked are not clear. The Strasbourg-based organisation, which is not part of the European Union, recommends that voters should be sent “balanced campaign material” at least two weeks before a vote. Instead Greeks will have had just eight days to decide on a question couched in jargon-heavy “financialese”.

Read more …

And the Greeks didn’t murder anyone.

• When Greece Forgave Germany’s Debt (AP)

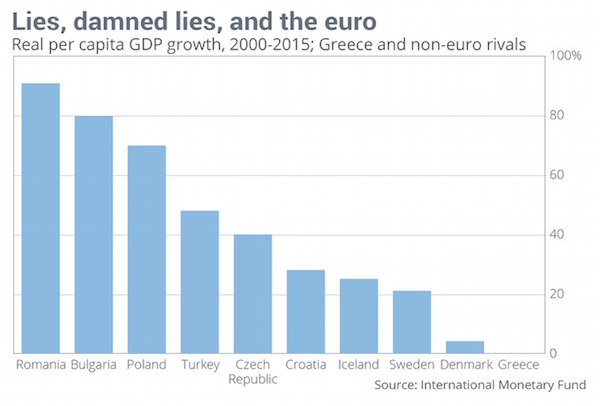

Forgiving debt, if done right, can get an economy back on its feet. The IMF certainly thinks so, according to a new report in which it argues Greece should get help. But Germany, another major creditor to Greece, is resisting, even though it should know better than most what debt relief can achieve. After the hell of World War II, the Federal Republic of Germany – commonly known as West Germany – got massive help with its debt from former foes. Among its creditors then? Greece. The 1953 agreement, in which Greece and about 20 other countries effectively wrote off a large chunk of Germany’s loans and restructured the rest, is a landmark case that shows how effective debt relief can be. It helped spark what became known as the German economic miracle.

So it’s perhaps ironic that Germany is now among the countries resisting Greece’s requests for debt relief. Greek Finance Minister Yanis Varoufakis claims debt relief is the key issue that held up a deal with creditors last week and says he’d rather cut off his arm than sign a deal that does not tackle the country’s borrowings. The IMF backed the call to make Greece’s debt manageable with a wide-ranging report on Thursday that also blames the Greek government for being slow with reforms. Despite years of budget cuts, Greece’s debt burden is higher than when its bailout began in 2010 – more than €300 billion, or 180% of annual GDP – because the economy has shrunk by a quarter. Here’s a look at when Germany got debt relief, and how such action might help Greece.

The 1953 London Agreement, hammered out over months, was generous to West Germany. It cut the amount it owed, extended the repayment schedule and granted low interest rates. And crucially, it linked West Germany’s debt repayment schedule to its ability to pay – tying repayments to the trade surplus it was running and expected to run. That created an incentive for trading partners to buy German goods. The deal effectively blocked claims for reparations for the destruction the Nazis inflicted on others. But it wasn’t a one-way street. “The London Agreement gave Germany sweeping debt forgiveness and protection from creditors, in exchange for pro-market reforms,” Professor Albrecht Ritschl, of the London School of Economics said.

West Germany was able to borrow on international markets again, and, free of onerous debt payments, saw its economy grow strongly. Development activists cite that case when arguing for easier terms for troubled countries today, including Greece. “The same opportunity should be given to Greece that was given to Germany in 1953,” said Eric LeCompte, executive director of the debt relief organisation Jubilee USA.

Read more …

“..there wouldn’t be any reason to fear default and pull deposits.”

• Greece Shows ECB’s Stress Tests Were Nonsense (FT)

The key challenge is figuring out whether a private bank is solvent in the heat of the moment. That, of course, was the whole point of the asset quality review and the comprehensive assessment. The methodology may not have been perfect but the ECB’s leaders can’t endorse the results without also agreeing that the banks that passed the tests will have unrestricted access to liquidity facilities from the central bank. It’s a trade-off: you get government support in a crisis in exchange for regulatory approval that your business is sound. That, in turn, ought to prevent the risk of runs. In Greece, the ECB doesn’t seem to be honoring this deal. Forget whether or not Greece would be better off leaving the euro.

The government has said it doesn’t want to leave and, strictly speaking, there is no reason it would have to leave even if it defaulted on certain outstanding sovereign debts. The only thing that would force an exit would be if the banks were in danger of failing and the government decided to restore monetary sovereignty in order to provide liquidity. (Default on only some debts wouldn’t have to hit the banks.) Even so, some Greek citizens have been converting their euro deposits into paper euros because they are worried about exit and devaluation. That could be self-fulfilling if it endangered the stability of the banks. However, it wouldn’t be much of an issue if Draghi’s 2012 promise that “the ECB is ready to do whatever it takes to preserve the euro” were genuine.

Greeks would know that the ECB would do its job — lend unconditionally to the Greek banks it had declared solvent back in October and print enough euro cash to ensure that the payments system would continue to operate smoothly — and there wouldn’t be any reason to fear default and pull deposits. (Yes, it’s possible that the ECB could end up lowering the initial costs of exit if central bank liquidity ended up replacing all domestic deposits but we’re still a long way off from that.) The ECB’s unwillingness to do its job as a lender of last resort is bad for Greece but it’s even worse as a precedent for other countries in the euro area. Plenty of other countries share Greece’s bad demographics, slow growth, and lots of public debt owed to foreigners, especially once QE proceeds further. Would they too be forced out of the single currency the next time growth ticks downward and the people elect a government unfavoured by elites?

Read more …

Following the logic. Must read from Yanis’ close friend and advisor. Yes vote will still break euro.

• Only the No Can Save the Euro (James K. Galbraith)

Greece is heading toward a referendum on Sunday on which the future of the country and its elected government will depend, and with the fate of the euro and the European Union also in the balance. At present writing, Greece has missed a payment to the IMF, negotiations have broken off, and the great and good are writing off the Greek government and calling for a “Yes” vote, accepting the creditors’ terms for “reform,” in order to “save the euro.” In all of these judgments, they are, not for the first time, mistaken. To understand the bitter fight, it helps first to realize that the leaders of today’s Europe are shallow, cloistered people, preoccupied with their local politics and unequipped, morally or intellectually, to cope with a continental problem.

This is true of Angela Merkel in Germany, of François Hollande in France, and it is true also of Christine Lagarde at the IMF. In particular North Europe’s leaders have not felt the crisis and do not know the economics, and in both respects they are the direct opposite of the Greeks. For the North Europeans, the professionals at the “institutions” set the terms, and there is only one possible outcome: to conform. The allowed negotiation was of one type only: more concessions by the Greek side. Any delay, any objection, could be seen only as posturing. Posturing is normal of course; politicians expect it. But to his fellow finance ministers the idea that the Greek Finance Minister Yanis Varoufakis was not posturing did not occur. When Varoufakis would not stop, their response was loathing and character assassination.

Contrary to some uninformed commentary, the Greek government knew from the beginning that it faced fierce hostility from Spain, Portugal and Ireland, deep suspicion from the mainstream left in France and Italy, implacable obstruction from Germany and the IMF, and destabilization from the European Central Bank. But for a long time, these points were not proved internally. There are influential persons close to Tsipras who did not believe it. There are others who felt that, in the end, Greece would have to take what it could get. So Tsipras adopted a policy of giving ground. He let the accommodation caucus negotiate. And as they came back with concession after concession, he winced and agreed.

Ultimately, the Greek government found that it had to bow to the creditors’ demands for a large and permanent primary surplus target. This was a hard blow; it meant accepting the austerity that the government had been elected to reject. But the Greeks did insist on the right to determine the form of austerity, and that form would be mainly to raise taxes on the wealthiest Greeks and on business profits. At least the proposal protected Greece’s poorest pensioners from further devastating cuts, and it did not surrender on fundamental labor rights. The creditors rejected even this. They insisted on austerity and also on dictating its precise shape. In this they made clear that they would not treat Greece as they have any other European country. The creditors tabled a take-it-or-leave-it offer that they knew Tsipras could not accept. Tsipras was on the line in any case. He decided to take his chances with a vote.

Read more …

“So what do you do in a negotiation where (a) you have no choice but to negotiate and (b) your opponent won’t negotiate?”

• The Greek Vote (Steve Keen)

There is an adage in politics that you should never put anything to the vote unless you are sure of the outcome beforehand. On that front, the referendum Greeks will vote in this Sunday is a mistake, because the vote could go either way. If the majority votes No, as Syriza hopes, then it—hopefully—will strengthen its hand in future negotiations with the Troika. But if the majority votes Yes, then Syriza will have to capitulate to the Troika and accept its unbending policy of austerity. But I can also understand Tsipras’s decision to throw the issue over to a vote. Syriza’s expectation, when it won the election, was that its mandate from the Greek people would enable it to bargain with the Troika, and to therefore negotiate a less onerous economic program. Reality has proved otherwise.

Every time Syriza has compromised on one of its “red lines”, the Troika has demanded that it cross the red line behind it. So what do you do in a negotiation where (a) you have no choice but to negotiate and (b) your opponent won’t negotiate? You play whatever wildcard you have in your pack—and the only wildcard that Syriza has is that it was elected by its people, whereas the Troika’s officials were not. If the No vote wins, then it has a further right to insist that it is following the will of its people. We will return to almost daily Greek crises as each debt rollover or instalment payment arises, but Greece will have the power to legitimately threaten total default as a way of forcing the Troika to take a backwards step. But if the vote goes against Syriza, then the political balance in Greece will shift dramatically.

The Greeks will, in effect, have chosen to continue with austerity, even though just six months ago they elected a new government committed to ending it. Though Syriza will remain in power after Saturday, its spirit will have been irrevocably broken. Some political changes will flow immediately. Yanis Varoufakis has confirmed that he will resign—while also accepting the decision of the Greek people and assisting whoever replaces him to sign the terms of capitulation that the Troika wants. But that, as Yanis would vehemently agree, is small-scale, personal stuff. I have always found it amusing, in a perplexing way, that Schaeuble, the Troika’s chief hard man, has taken such umbrage to the left-wing Syriza and its metrosexual political leaders.

Clearly he prefers to negotiate with rightwing politicians like himself. But he seems unaware that, if the Greek tragedy rolls on, he may instead have to negotiate with rightwing politicians unlike himself—the neo-Nazi Golden Dawn. Golden Dawn is also an anti-austerity party, and before the sudden rise of Syriza, it was the premiere anti-austerity party in Greece. It came 3rd in the elections that brought Syriza to power—even though its leaders were in gaol pending a murder trial that began in May—and in the 2014 European Union elections, it scored just under 10% of the Greek vote.

Read more …

“The report is a “confession” of the bailout’s failure..”

• Greece Needs $40 Billion in Fresh Euro-Area Money, IMF Says (Bloomberg)

Greece needs at least another €36 billion over the next three years from euro-area states and easier terms on existing debt to keep the nation’s finances sustainable, according to an IMF analysis. Even if Greece delivers on reforms proposed by its international creditors, euro countries will have to come up with new financing and ease the nation’s debt load through steps such as doubling maturities on existing loans, according to a June 26 “preliminary draft” debt-sustainability analysis released Thursday. The Washington-based lender puts Greece’s total financing needs at €50 billion from October 2015 through the end of 2018. It also says state deposits in the Greek banking system had declined to less than €1 billion at the end of May, before the nation closed its banks and imposed capital controls.

Any weakening of the package proposed by the IMF and its creditor partners, the European Commission and ECB, means Europeans must accept a “haircut,” or writedown on the principal of the loans, according to the analysis. The document’s date is the day before Greek Prime Minister Alexis Tsipras called a surprise July 5 referendum on the creditors’ proposal. The analysis suggests any new deal is doomed to keep Greece wallowing in debt unless the Greek government and its European creditors can make further concessions. It also indicates the IMF, smarting from a $1.7 billion missed payment by Greece this week, may be reluctant to dispense new money without better prospects that the nation’s debt will be brought under control.

The timing of the analysis will prove controversial, since Tsipras is sure to use it to bolster his argument that Greeks should reject the creditors’ proposal in Sunday’s vote, said Jacob Funk Kirkegaard, a senior fellow at the Peterson Institute for International Economics in Washington. The IMF is suggesting that “Greece was essentially on track last November until Syriza blew up the political system and now the economy,” while hinting that it wouldn’t welcome working with the anti-austerity party in the future, he said. The IMF report justifies the Greek government’s position and its persistence in including debt restructuring in any deal with creditors, said Gabriel Sakellaridis, a government spokesman. The report is a “confession” of the bailout’s failure, he said in an e-mail.

Read more …

Curious: “Alexis Tsipras welcomed the IMF’s intervention saying in a TV interview that what the IMF said was never put to him during negotiations”.

• IMF Says Greece Needs Extra €60 Billion In Funds And Debt Relief

The IMF has electrified the referendum debate in Greece after it conceded that the crisis-ridden country needs up to €60bn of extra funds over the next three years and large-scale debt relief to create “a breathing space” and stabilise the economy. With days to go before Sunday’s knife-edge referendum that the country’s creditors have cast as a vote on whether it wants to keep the euro, the IMF revealed a deep split with Europe as it warned that Greece’s debts were “unsustainable”. Fund officials said they would not be prepared to put a proposal for a third Greek bailout to the Washington-based organisation’s board unless it included both a commitment to economic reform and debt relief. According to the IMF, Greece should have a 20-year grace period before making any debt repayments and final payments should not take place until 2055.

It would need €10bn to get through the next few months and a further €50bn after that. The Greek prime minister Alexis Tsipras welcomed the IMF’s intervention saying in a TV interview that what the IMF said was never put to him during negotiations. Urging a no vote on Sunday he said: “Voting no to a solution that isn’t viable doesn’t mean saying no to Europe. It means demanding a solution that’s realistic. “Either you give in to ultimatums or you opt for democracy. The Greek people can’t be bled dry any longer.” Tsipras is campaigning for a no vote in the referendum on Sunday, which is officially on whether to accept a tough earlier bailout offer, to impress on EU negotiators that spiralling poverty and a collapse in everyday business activity across Greece has meant further austerity should be ruled out of any new rescue package.

Greece’s finance minister, Yanis Varoufakis, pledged to resign if his country votes yes to the plan proposed by the EU, the ECB and what appears to be an increasingly reluctant IMF. Varoufakis, the academic-turned-politician who has riled his eurozone counterparts, said he would not remain finance minister on Monday if Greece voted yes. He said he would rather “cut off his arm” than accept another austerity bailout without any debt relief for Greece, adding that he was “quite confident” the Greek people would back the government’s call for a no vote. The Greek government’s defiant stance came as the head of the Hellenic Chambers of Commerce, Constantine Michalos, said he did not believe Greece’s banks would be able to reopen next Tuesday without further funding, telling the Daily Telegraph he had been told cash reserves were down to €500m.

Read more …

Bit late?!

• Why Not Donate To Something That Will Make A Real Difference To Greeks (PP)

The campaign to crowdfund €1.6 billion for Greece on indiegogo is a wonderful initiative to show solidarity, and indeed it has collected an astonishing amount of money in a short time. The only problem is that if the full amount is not collected, all donations will be returned. Although we’d like to hope that there’s a chance the campaign will reach its target, it is quite a long shot. So we’d like to present you with an alternative way to help Greece right now. The Greek media is corrupt. This might not come as a big shock, maybe there are corrupt media in your country too, but the truth of the situation here goes far beyond what you’d imagine. According to the NGO Reporters Without Borders, Greece ranks 93rd in the global index of press freedom (placing it last in Europe).

Private TV channels, newspapers and radio stations are majority owned by 5 key families, who use them to ensure their family of companies obtain government contracts. These private media outlets are members of large groups of companies who undertake construction projects, and shipowners who control the oil trade and imports. During the last few days, the mainstream media have declared war on citizens, taking a position on the referendum and violating any notion of journalistic ethics. Their reporting is designed to terrorize and create a culture of fear, without any trace of truth or balance, whilst presenting themselves as objective and responsible.

On Monday, the largest TV station was broadcasting misinformation all day about cash withdrawals being reduced from 60 to 20 euros -reports which had been denied three times officially by the government- trying to provoke a bankrun. Nobody can control them. The competent inspection body is at present too weak to impose any sanctions. At the same time the Greek state’s efforts to pursue €102 million in unpaid taxes from these media companies for the use of public frequencies (common practice in other EU countries) has brought zero results. But new technologies have created new communication channels.

Read more …

Big worry for US.

• China May Aid Greece Directly – Think Tank Expert (Sputnik)

China may help Greece through EU instruments or directly, a member of the Chinese Academy of Social Sciences, affiliated with China’s State Council, told Sputnik. China may help Greece directly through its new financial instruments, director of the Quantitative Finance Department at China’s Institute of Quantitative and Technical Economics told Sputnik China. Investment bank Goldman Sachs predicted in a report published on Wednesday that in a worst-case scenaria China’s exports would decline 2.2% as a result of Greece’s economic crisis. Other than exports to Greece itself, the crisis could also hurt the economies of nearby countries, where Chinese businessmen have also made considerable investments.

“The Greek crisis has an undoubtedly seriously influence on China’s trade with Greece and investment into the country. But I think that European countries together with China can help Greece overcome the problems that arose,” Fan Mingtao said. Fan added that the crisis is not likely to be an overbearing problem in the long term, although China will suffer losses in trade with Greece as a result. “I believe there are two ways to give Greece Chinese aid. First, within the framework of the international aid through EU countries. Second, China could aid Greece directly. Especially considering the Silk Road Economic Belt and the Asian Infrastructure Investment Bank. China has this ability,” Fan added. According to Fang, China has the financial ability to aid Greece if needed, because of its existing Silk Road Economic Belt project and the Asian Infrastructure Investment Bank.

Read more …

Schulz should be fired for such comments. Hoe doesn’t understand what democracy in a sovereign nation means.

• Schulz Says Tsipras Should Resign After ‘Yes’ Vote, Wants Technocrats (AFP)

European Parliament president Martin Schulz said his faith in the Greek government had reached “rock bottom,” and that he hopes it resigns after Sunday’s referendum. Prime Minister Alexis Tsipras has urged citizens to vote against EU and IMF bailout conditions in the plebiscite Sunday. Tsipras announced the balloting after talks with creditors broke down, leading Greece to default on a debt payment and stoking fears it could crash out of the euro. Schulz on Thursday told German Handelsblatt business daily that “new elections would be necessary if the Greek people vote for the reform programme and thus for remaining in the eurozone and Tsipras, as a logical consequence, resigns.”

The time between the departure of Tsipras’ hard-left Syriza party and new elections would have to “be bridged with a technocratic government, so that we can continue to negotiate,” Schulz was quoted as saying. “If this transitional government reaches a reasonable agreement with the creditors, then Syriza’s time would be over,” he said. “Then Greece has another chance.” Schulz charged that Tsipras was “unpredictable and manipulates the people of Greece, in a way which has almost demagogical traits.” “My faith in the willingness of the Greek government to negotiate has now reached rock bottom,” he said Greek Finance Minister Yanis Varoufakis said Thursday the government “may very well” quit if the public went against it in Sunday’s plebiscite by voting for more austerity in return for international bailout funds.

Read more …

When will the nonsense stop?

• US Part-Time Jobs Surge By 161,000; Full-Time Jobs Tumble By 349,000 (ZH)

While the kneejerk reaction algos were focusing on the +223K jobs number reported by the Establishment Survey, few if anyone notched that the Household survey reported a decline of 56,000 workers in June.

But what’s worse, is that according to this survey which according to some is far more reliable than its peer, the composition of the US labor force once again deteriorated rapidly with part-time jobs added in June surging by 161,000 while the number of full time jobs tumbled by 349,000.

Putting this number in context, while the total number of US workers has long since surpassed its previous crisis high, the number of full time US workers has yet to overtake its November 2007 lever of 121.9 million, and in June dropped to 121.1 million.

Why is this a problem: because while the US still has 800k full-time jobs to go to at least regain the prior peak, during the same time period the US civilian, non-institutional population has risen from 232.9 million to 250.7 million: an increase of 17.724 million!

Read more …

More proper IMF work. Will also be silenced, just like the Greek debt relief report.

• Causes and Consequences of Income Inequality: A Global Perspective (IMF)

Widening income inequality is the defining challenge of our time. In advanced economies, the gap between the rich and poor is at its highest level in decades. Inequality trends have been more mixed in emerging markets and developing countries (EMDCs), with some countries experiencing declining inequality, but pervasive inequities in access to education, health care, and finance remain. Not surprisingly then, the extent of inequality, its drivers, and what to do about it have become some of the most hotly debated issues by policymakers and researchers alike. Against this background, the objective of this paper is two-fold.

First, we show why policymakers need to focus on the poor and the middle class. Earlier IMF work has shown that income inequality matters for growth and its sustainability. Our analysis suggests that the income distribution itself matters for growth as well. Specifically, if the income share of the top 20% (the rich) increases, then GDP growth actually declines over the medium term, suggesting that the benefits do not trickle down. In contrast, an increase in the income share of the bottom 20% (the poor) is associated with higher GDP growth. The poor and the middle class matter the most for growth via a number of interrelated economic, social, and political channels.

Second, we investigate what explains the divergent trends in inequality developments across advanced economies and EMDCs, with a particular focus on the poor and the middle class. While most existing studies have focused on advanced countries and looked at the drivers of the Gini coefficient and the income of the rich, this study explores a more diverse group of countries and pays particular attention to the income shares of the poor and the middle class—the main engines of growth.

Read more …

it’s going downhill fast now.

• China’s Stocks Hit Critical Low Despite Government Lifelines (SCMP)

A series of lifelines from Beijing failed to stop the slide in the mainland’s stock market on Thursday, with the key Shanghai Composite Index closing below the critical 4,000 mark for the first time in almost three months. Analysts warned that the nation’s leadership would pay dearly if it failed to stabilise the market and prevent millions of small investors from losing their life savings. “The government’s response to the fall confirms that it will use all the resources at its disposal to influence the market when things do not go the way it wants and potentially puts its legitimacy at risk,” said Steve Tsang, chair of the School of Contemporary Chinese Studies at the University of Nottingham.

The China Securities Regulatory Commission said last night that the stock market had recorded a significant drop, and the commission would launch an investigation into suspected market manipulation. Those suspected of committing an offence would be handed over to public security agencies. The Shanghai Composite Index fell as much as 6.38% at one point in the afternoon session, before finishing down 3.48%, or 140.93 points, at 3,912.77, the lowest level since April 9. The Shenzhen Composite Index shed 5.55%, or 130.32 points, to close at 2,215.81 and ChiNext – the Nasdaq-style bourse for small-cap tech stocks – gave up 4%. Since falling off a seven-year peak of 5,166.35 on June 12, the Shanghai index has lost about a quarter of its value, with the mainland equity markets heading into bear territory after fears of a tightening of margin lending induced a sharp correction.

Read more …

No kidding.

• China’s Boom Has World Bank Worried (Pesek)

The World Bank has a timely warning for Chinese President Xi Jinping: Don’t let all that money go to your head. The global lender didn’t refer directly to Shanghai’s stock boom or the Asian Infrastructure Investment Bank (Beijing’s attempt to develop a World Bank of its own). Nor did it have to. By urging Beijing to clamp down on wasteful investment, unsustainable debt, and a shadow banking industry run amok, it was delivering a clear enough warning that President Xi should stop fanning China’s giant asset bubble. The World Bank was also implying China should get its own economic house in order before trying to change the global economy. “China has reached a critical phase of its economic and social development path,” the lender said in a new report released Wednesday.

The economy “will need to be transformed to increase the efficiency of new investments and widen access to finance, enabling China to sustain solid growth and rebalance its economy.” The World Bank’s admonishment was amplified by a fascinating milestone the Chinese economy reached this week — one that presents Xi’s government with a complicated image problem. China’s 90 million mainland stock traders now outnumber its 87.8 million Communist Party members. This changing of the guard, if you will, is taking place the same week the party celebrated its 94th anniversary – hardly what Mao Zedong had in mind when he led the Communists to power in 1949. In truth, China’s fast-growing legions of stock traders are betting on a type of financial Communism.

Everyone knows the Chinese economy is slowing and deflation is approaching, but markets have generally stayed aloft amid perceptions Xi will use the full power of the state to protect investments. Along with weekend interest-rate cuts, authorities have just made it easier to take on even more leverage. Brokerages now have leeway to boost lending by about $300 billion. Yet recent stock market declines suggest those steps aren’t working their usual magic. Part of the problem is traders have realized nobody is shoring up the shaky pillars of the world’s second-biggest economy. As that awareness sinks in, the 24% decline in the Shanghai Composite Index from its June 12 peak (which wiped out more than the equivalent of Brazil’s annual output) will only intensify. So will the headwinds bearing down on the broader economy as plunging shares dent business and household confidence.

Read more …

It lost the entire German stock market value too. Though people put up their homes as collateral.

• Chinese Stocks Just Lost 10 Times Greece’s GDP

As Europeans hold their breath awaiting a referendum that will help determine Greece’s future in the euro zone, a stock market slump on the other side of the world is causing barely a ripple in global markets. A dizzying three-week plunge in Chinese equities has wiped out $2.36 trillion in market value — equivalent to about 10 times Greece’s gross domestic product last year. Still, the closed nature of China’s financial markets is allowing the rest of the world to watch in wonder without seeing spillovers into their markets…yet. “What happens in China will turn out to be far more consequential than any sting that Greece may deliver over the coming weeks or months,” said Frederic Neumann, co-head of Asian economic research at HSBC Holdings Plc in Hong Kong.

“As China’s equity markets lose their roar, the risk is that demand more broadly on the Mainland could take a hit. That would knock out an essential engine of world demand over the past decade. As dramatic as events in Greece currently appear, however, ultimately, it’s difficult to see these proving decisive for the world economy.” For now, even within China, economists find it tough to draw a link between its retail-driven stock market swings and the economy. A recent survey by Bloomberg shows analysts split on whether a rout would have any decisive effect on growth. One thing to note: With China opening its capital borders, roller-coaster rides on its stock market will have increasing repercussions for investors from London to New York and Tokyo. But that’s farther out in the future than the more immediate concerns in Greece.

Read more …

Betting on one horse. Or cow, rather.

• Top Economist Warns Of New Zealand Recession Risk (NZ Herald)

So much for the rock star economy. As dairy prices continue to slump and business confidence tapers off, a leading economist is warning that a “scenario where a recession becomes imminent” isn’t difficult to imagine. BNZ head of research Stephen Toplis said the biggest shock to New Zealand’s economy had been the ongoing demise of the dairy sector. The price of whole milk powder – which is responsible for about 75% of Fonterra’s farmgate milk price – plunged 10.8% to US$2054 a tonne at the latest GlobalDairyTrade auction this week. The overall index fell 5.9% to record its ninth consecutive decline, driving the New Zealand dollar to a fresh five-year low of US66.59c last night.

Economists are now picking the Reserve Bank to cut the official cash rate back to 2.5% (from 3.25% currently) in a complete reversal of a rate tightening cycle that began in early 2014. BNZ this week lowered its 2015/16 milk price forecast to $5.20kg from $5.70 previously. “In part, the demise of dairy will be having an impact on economy-wide confidence, such as reflected in the recently released ANZ [business confidence] survey,” Toplis said. “In turn these confidence readings are also useful in predicting future GDP [gross domestic product] growth. Unfortunately, the trend in confidence is down.” BNZ is forecasting annual average growth this year of 2.4%, falling to 2.1% over 2016 and 2017.

“That said, the balance of risks around our forecast is becoming more skewed to the downside,” Toplis said. “Indeed, so much so that it is not hard to envisage a scenario where a recession becomes imminent.”

Read more …

At least someone tried to do something.

• Benjamin Lawsky’s Legacy (NY Times)

After four years on the job, Benjamin Lawsky, New York’s top financial regulator, stepped down in June. His legacy includes important protections against abusive debt collectors and usurious payday lenders, as well as aggressive enforcement actions against banks and financial firms for money laundering, currency manipulation, interest rate rigging, foreclosure abuses and insurance scams. He has also left Gov. Andrew Cuomo with a moment-of-truth decision. Will Mr. Cuomo appoint a replacement to build on Mr. Lawsky’s legacy or to tone it down? In 2011, Mr. Cuomo merged New York’s bank and insurance agencies into a single agency with expanded regulatory powers. The question at the time was whether the newly created Department of Financial Services would be a political tool — a way for Mr. Cuomo to impinge on the power of the state attorney general — or a true financial regulator.

The answer has been the latter, thanks largely to Mr. Cuomo’s choice of Mr. Lawsky, a onetime Democratic aide and former federal prosecutor, to run the department. But some of the names that are circulating as possible contenders for Mr. Lawsky’s job suggest that this time around, Mr. Cuomo is looking for a light regulatory touch. In addition to lawyers who have spent much of their careers representing and defending corporate clients, it also reportedly includes a former JPMorgan Chase executive. Mr. Lawsky’s tenure — and much of the regulatory history before and since the financial crisis — has disproved the notion that financial-industry professionals are uniquely qualified to regulate banks and financial firms. In fact, regulators from industry have been linked to rulemaking delays and regulatory capture, which occurs when a regulatory agency advances the interests of the industry it is charged with overseeing rather than the public interest.

To avoid those pitfalls, Mr. Cuomo should choose Mr. Lawsky’s successor from the nation’s ranks of prosecutors, legal and consumer advocates or federal or state officials who have shown an aggressive streak toward Wall Street. The choice comes at a crucial time. As memories of the financial crisis fade, banks have increasingly argued that regulation has become too heavy. They expect politicians to respond by easing up on regulatory efforts. That would be a mistake. Regulation today needs to be vigilant for continuation of behaviors from the crisis years and for developments that may portend the next crisis. Mr. Lawsky has left the Department of Financial Services in a position of strength. It is up to Mr. Cuomo to keep it strong.

Read more …

“..rates “simply can’t rise without causing deleveraging and a crash”.

• Arise Steve Keen, Forecaster Of The Year (SMH)

What was it Jesus said about a prophet being accepted everywhere but in his home town? Australian expatriate Steve Keen was by far the most successful of last year’s BusinessDay economic forecasters. He did it by being the most pessimistic of the 25, but hardly ever too pessimistic. None of the others thought our terms of trade would collapse by more than a few%. Keen picked 10%. We got 12.25%. The pay cut rocked the budget deficit, but not by as much as most predicted. Keen went for $40 billion. The budget papers say it’ll be $41.1 billion. Wage growth slipped to a new low of just 2.3%. Most of the panel couldn’t see it coming, many going for 3% or more. Only Keen and also University of Newcastle economist Bill Mitchell picked 2%.

Tom Skladzien, of the Australian Manufacturing Workers Union, deserves an honourable mention as well. With his ear to the ground he picked 2.5%. The Reserve Bank cut its cash rate twice in response to the slide in national income. None of the bank economists expected it. Only Keen and Mitchell went for a cut, to 2.25%. The lower rates spurred a sharemarket boom which pushed the S&P/ASX 200 to near 6000 in February before it fell back in May and June to close not too far from where it started at 5459. Keen picked 5500 – far closer than the much higher forecasts of the panellists who didn’t see the interest rate cuts coming. On the bond market the economists employed by banks embarrassed themselves.

Instead of climbing as they all expected, Australia’s 10-year bond rate slid to an all-time low before edging back up to 3.01. Keen picked 3.5%, the only forecast anywhere near reality. He says he takes private debt seriously unlike others who treat it as largely irrelevant to economic outcomes, a “consenting act between adults”. Given the historically unprecedented levels of private debt worldwide, rates “simply can’t rise without causing deleveraging and a crash”. Keen can rightly claim to have foreseen the events in the US which led to the global financial crisis and to have wrongly picked a collapse in Australian house prices in its wake, famously losing a bet and walking from Canberra to Mount Kosciuszko wearing a T-shirt that said: “I was hopelessly wrong about house prices, ask me how.”

Unwanted by the University of Western Sydney, he was snapped by Kingston University in London where he is gaining a reputation as one of Europe’s leading economic thinkers. He didn’t get it all right this year. Mitchell (another non-orthodox economist) was more accurate about economic growth, and almost everyone was more accurate about the US economy, expecting something closer to 3 per cent growth than the 1 per cent Keen forecasted. But Keen is doubling down and predicting 1 per cent again this year. There’s a chance he knows what he is doing. It’s the third time he has won the title of BusinessDay forecaster of the year.

Read more …