Vincent van Gogh A Restaurant at Asnieres 1887

This is going spectacularly wrong. Somone better stop it.

• The ‘Most Striking Development’ In 40 Years Of The US Economy (BI)

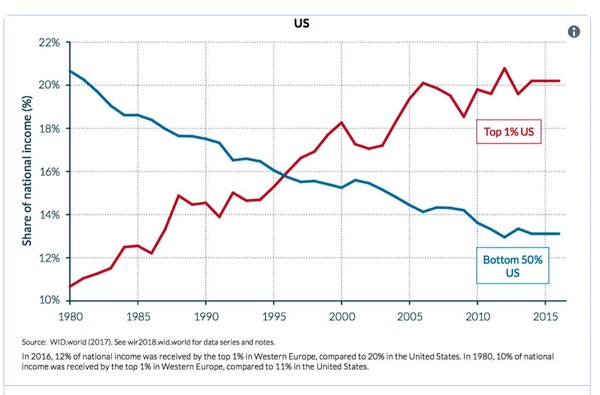

French economist Thomas Piketty is one of the world’s leading researchers of global income and wealth inequality, and became well-known in the United States when the English translation of his book “Capital in the 21st Century” became a surprise bestseller. For the past year, Piketty has been speaking about the 2018 World Inequality Report, published by the Paris School of Economics’ World Inequality Lab last December. Piketty coauthored the report alongside Facundo Alvaredo, Lucas Chancel, Emmanuel Saez, and Gabriel Zucman. In his talks in the US, Piketty has paid special attention to the following chart, which shows what he and his coauthors called “perhaps the most striking development in the United States economy over the last four decades.”

The authors write that “the incomes of the top 1% collectively made up 11% of national income in 1980, but now constitute above 20% of national income, while the 20% of US national income that was attributable to the bottom 50% in 1980 has fallen to just 12% today.” Further, “while average pre-tax income for the bottom 50% has stagnated at around $16,000 since 1980, the top 1% has experienced 300% growth in their incomes to approximately $1,340,000 in 2014. This has increased the average earnings differential between the top 1% and the bottom 50% from 27 times in 1980 to 81 times today.”

The Guardian/Observer, leading anti-Trump voice, has a piece ‘Unfit for President, but…” Look, just like the NYT, you no longer are a voice, because you’ve spent two years 24/7 denouncing the man with rumors and half-truths -like you did with Corbyn being anti-semite. You can’t now turn around and be a voice for democracy. You’re done.

• This Insider Betrayal Is A Sorry Precedent (Observer ed.)

[..] the president’s discomfort, and his detractors’ glee, should not obscure more serious issues raised by this affair and by similarly critical revelations contained in a new exposé by the celebrated Watergate reporter Bob Woodward. Whatever one’s opinion of Trump, it is a matter of concern that unelected, unnamed officials are apparently willing and able to act in ways contrary to an elected president’s stated wishes and calculated to thwart his policies. Trump’s worst instincts must undoubtedly be resisted, as Barack Obama, rejoining the fight last week, has declared. The best way to achieve that, as ever in a democracy, is through public scrutiny and open debate. Every leader needs candid advisers.

But who are these self-described “adults in the room” to clandestinely decide what is in the best interests of the country? Their motives may be sound, but their illicit actions, boasted of publicly, set a worrisome precedent. They have also gifted Trump a golden opportunity to peddle his favourite narrative of an establishment conspiring against him, aided and abetted by media organisations – which he terms “enemies of the people”. Speaking in Montana on Thursday, he seized his chance. “Unelected, deep state operatives who defy the voters to push their own secret agendas are truly a threat to democracy itself,” he declared.

The anonymous writer tried to provide reassurance that things in the White House are not as bad as they seem. Woodward’s new book, Fear, suggests the exact opposite: they are worse. It describes a “Crazytown” of tantrums, endless crises, serial lying, unhinged behaviour, and an administration in a recurring state of nervous breakdown.

It’s not so much dominoes falling one by one, it’s the USD that crashes down everything.

• Argentina, Turkey, Mexico … Fear Of Contagion Haunts Emerging Markets (G.)

In the past six months, some of the world’s fastest-growing economies have found themselves flat on the floor, gasping for breath and, in one case, seeking help from the global financial rescue centre otherwise known as the IMF. Argentina’s $50bn bailout by the Washington-based lender of last resort is the most extreme event so far, but it sits alongside the dramatic collapse of the Turkish lira, a recession in South Africa and dire economic predictions for the Philippines, Indonesia and Mexico. Making matters worse, the US is poised to slap tariffs as high as 25% on as much as $200bn worth of Chinese goods. If the US goes ahead, Beijing has already threatened to retaliate, which would only incense President Donald Trump further.

This tit-for-tat might only end when tariffs are applied to the entire $500bn of Chinese goods imported by America each year. In response, the stock markets of many developing nations have slumped in value, leaving investors to ask themselves whether they are witnessing an emerging-markets meltdown akin to the Asian crisis of 1997: a panic that wrecked the finances of several hedge funds and proved to be an hors d’oeuvre before the dotcom crash of 1999 and the global financial crisis of 2008. Investors have run for safety to such an extent that the MSCI Emerging Markets index, which measures the value of shares in emerging economies, has tumbled by more than 20% since the beginning of the year.

That slump appeared to be over in July, when Turkey and Argentina were seen as being isolated, and more importantly ringfenced, economic trouble spots. But figures last week showing that the US economy is steaming along like a runaway train – underlining the likelihood of more US interest rate rises – have sent the currencies and stock markets of most emerging-market economies tumbling again. Lukman Otunuga, research analyst at currency dealer FXTM, says that a sense of doom is lingering in the financial markets as fears of contagion from the “brutal emerging-market sell-off” rattle investor confidence. “More pain seems to be ahead for emerging markets as the combination of global trade tensions, prospects of higher US interest rates and overall market uncertainty haunt investor attraction,” he says.

Now we’re talking.

• No-Deal Brexit Could Lead To “Military On The Streets” (Ind.)

A no-deal Brexit could lead to the “real possibility” of police calling upon the military to help with civil disorder, a leaked document claims. Contingency plans are being drawn up by police chiefs if there is chaos on the streets due to shortages of goods, food and medicine, The document prepared by the National Police Co-ordination Centre (NPoCC) warns of traffic queues at ports with “unprecedented and overwhelming” disruption to the road network. Concerns around medical supplies could “feed civil disorder”, while a rise in the price of goods could also lead to “widespread protest”, the document obtained by the Sunday Times said.

The potential for a restricted supply of goods raised concerns of “widespread protest which could then escalate into disorder”. It could also trigger a rise in non-Brexit-related acquisitive crime such as theft. The document, set to be considered by the National Police Chiefs’ Council (NPCC) later this month, also sets out concerns of increased data costs, loss of warrant cards and queues at ports and docks around the country. Shadow police minister Louise Haigh lashed out at the Government’s handling of the situation. “This is the nightmare scenario long feared; according to the UK’s most senior police officers a no-deal Brexit could leave Britain on the brink,” she said.

May keeps pushing the same button after it’s failed 1000 times. The EU won’t give.

• Brexit Talks At Risk Of Collapse (Ind.)

Brexit talks are at risk of collapse as a planned EU compromise on the critical question of the Irish border has been branded “unacceptable” by British cabinet ministers. The Independent has learnt that EU officials believe they have struck upon “the only way” to bring the two sides together on the Irish border in a bid to secure a withdrawal agreement later this year. But their proposal has already been outright rejected by at least two cabinet ministers, with one going further and branding the EU’s suggestion “bollocks”. The impasse over the Irish border threatens to bring the talks crashing down with Theresa May’s beleaguered Chequers proposal already lacking support both in Europe and among her own MPs in Westminster.

The Independent now understands that the EU will try to break the deadlock in negotiations by offering the UK a vague political declaration on the future UK-EU relationship in return for a deal on the Irish border. A well-placed Brussels source said: “This may well prove the only way to respect the EU’s red lines and allow Theresa May to win approval for a deal in the UK parliament. “The political declaration holds the key to reaching a deal.” Since the start of Brexit talks Brussels has insisted the UK sign up to a legally binding “backstop”, which would come into play if no arrangement to avoid a hard border in Northern Ireland is found before Brexit day. It would see Northern Ireland effectively remain in the EU’s customs union and single market, creating a customs border down the Irish sea – something both Ms May and her DUP partners say is unacceptable.

[..] The strength of opposition indicates Ms May could face a further round of cabinet resignations if she were to consider agreeing to such a proposal, with Boris Johnson and David Davis having already quit earlier this year. A government spokesman said: “We don’t comment on speculation. The proposals we have put forward for our future relationship would allow both sides to meet our commitments to the people of Northern Ireland in full and we are working hard to get a deal on that basis. “But we are clear the EU backstop proposals are unacceptable.”

The Tories are thinking: we got rid of unions, didn’t we?

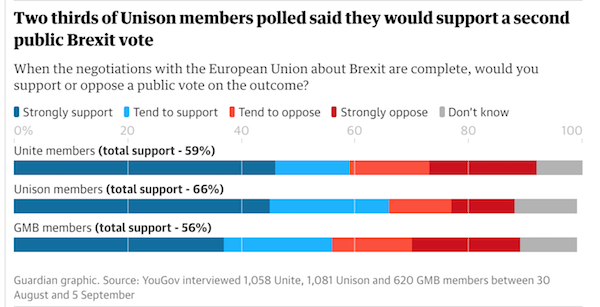

• Bombshell Poll Reveals Heavy Union Backing For Second Brexit Vote (G.)

Members of Britain’s three biggest trade unions now support a new referendum on Brexit by a margin of more than two to one, according to a bombshell poll that will cause political shockwaves on the eve of the party conference season. The survey of more than 2,700 members of Unite, Unison and the GMB by YouGov, for the People’s Vote campaign, also finds that a clear majority of members of the three unions now back staying in the EU, believing Brexit will be bad for jobs and living standards. The poll comes as union delegates gather in Manchester for the annual TUC conference, where Brexit will be debated on Monday, and two weeks before the Labour party conference in Liverpool, where delegates are expected to debate and vote on Brexit policy. They will also consider calls to keep open the option of a fresh referendum on any deal Theresa May may strike on the UK’s exit from the EU.

In an interview with the Observer before the poll findings were released, shadow chancellor John McDonnell said his preferred option was still for voters to be offered a say on the government’s handling of Brexit – and any deal brought back from Brussels by May – in a general election. But he said that if Labour was unable to force one in the coming months, he wanted to “keep all options open”, including supporting a new referendum. McDonnell said he was sure there would be a full debate, and votes, on Brexit at the Labour conference. And he went out of his way to praise the People’s Vote campaign, which he said had been very “constructive” and had made clear that its attempts to influence Labour policy should not be seen “as an attack on Jeremy Corbyn or positioning around the leadership. It should be a constructive debate and that is right.”

The poll found that members of Unite, the country’s biggest union, and Labour’s largest financial backer, now support a referendum on the final Brexit deal by 59% to 33% and support staying in the EU by 61% to 35%. GMB’s members support putting the issue back to the people by 56% to 33% and its members want the UK to stay in the EU by 55% to 37%. Unison members back another referendum by 66% to 22% and would opt to stay in the EU by 61% to 35%.

That second vote will come, or else…

• YouGov Poll Shows Support For A People’s Brexit Vote Is Solid (G.)

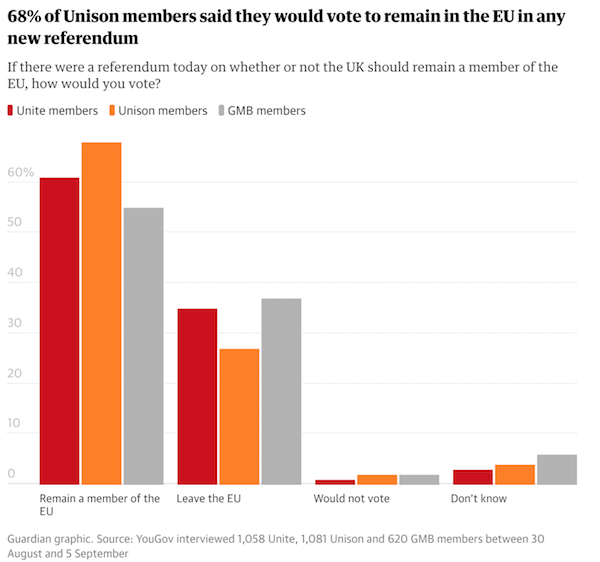

Thirty years ago this week, Jacques Delors came to Bournemouth to urge Britain’s trade unions to change their stance on Europe. The president of the European commission told TUC delegates that the EU was good for workers’ jobs, workers’ rights and workers’ living standards. It was a decisive moment in the union movement’s relationship with Brussels. This week could be equally decisive for the TUC – perhaps even more so – given the precarious balance of forces at Westminster. And the clear message from YouGov’s poll of more than 2,700 members of the TUC’s three biggest unions is that most trade union members think Brexit is bad for jobs; they want a fresh public vote and the chance to keep the UK in the EU.

Can we be sure that YouGov’s figures are right? Do the people it polled accurately reflect the views of all the members of the three big unions? I recall the same questions being asked when YouGov first showed Jeremy Corbyn well ahead in the race for the Labour leadership three years ago. Nonsense, said the critics. YouGov’s respondents, they claimed, were hopelessly biased towards leftwing activists. When it came to it, Corbyn won by almost precisely the majority reported in the final poll. And the methods YouGov used in the latest union survey are essentially the same as it used in Labour’s leadership election three years ago.

It’s not that trade union members are indulging in gesture politics or ideological breast-beating. They are worried about the impact of Brexit on jobs, taxes, living standards and the NHS. They fear a Brexit Britain would find it harder to sell products and services abroad. Their attitudes to immigration are especially significant. In the 2016 referendum, one of the arguments for Brexit was that immigrant workers were undercutting the pay of low-paid British workers. Brexit, so the argument ran, would allow Britain to stop this. As a result, there would be more, and better-paid, jobs for British workers.

Many Unite, Unison and GMB members earn below-average wages. They might be expected to support that part of the Brexit agenda. They don’t. Overwhelming majorities, ranging from 74% to 85%, want EU citizens either to have complete freedom of movement to come to the UK, or the freedom to settle here if they have a job or university place lined up.

Tsipras is trying to create the impression that he decides and is bold. He has no say at all.

• Fresh From End Of Bailout, Greek PM Announces Tax Breaks (R.)

Greek Prime Minister Alexis Tsipras on Saturday unveiled plans for tax cuts and pledged spending to heal years of painful austerity, less than a month after Greece emerged from a bailout program financed by its EU partners and the IMF. Tsipras, who faces elections in about a year’s time, used a keynote policy speech in the northern city of Thessaloniki to announce a spending spree that he said would help fix the ills of years of belt-tightening, and help boost growth. But he said Athens was also committed to sticking to the fiscal targets and reforms promised to its lenders. Greece has agreed to maintain an annual primary budget surplus – which excludes debt servicing costs – of 3.5 percent of GDP up to 2022.

So far, it has outperformed on fiscal goals and the economy has returned to growth. “We will not allow Greece to revert to the era of deficits and fiscal derailment,” he told an audience of officials, diplomats and businessmen. He said would beat its primary surplus target again this year and, following a debt relief deal in June, he could “safely plan its post-bailout future”. Government officials have put this year’s fiscal room at 800 million euros. Tsipras promised a phased reduction of corporate tax to 25 percent from 29 percent from next year, as well as an average 30 percent reduction in a deeply unpopular annual property tax on homeowners, rising to 50 percent for low earners.

Amnesty’s Aussie branch. Timing?!

• Protect Assange From US Extradition, Amnesty International Tells UK (RT)

Amnesty International has backed calls to not extradite WikiLeaks founder Julian Assange to the United States, arguing that this would put his human rights at serious risk of abuse. The statement, issued Friday by the group’s Australian branch, backed Assange’s lawyers and supporters’ claim that if he is sent to the US, “he would face a real risk of serious human rights violations due to his work with WikiLeaks.” Amnesty said that Assange could face several human rights violations in the event that he is extradited to the US, including: violation of his right to freedom of expression; right to liberty; right to life if the death penalty were sought; and being held in conditions that would violate his right to humane treatment.

While Amnesty said it took “no position” on Ecuador’s decision to grant, and then withdraw, Assange’s diplomatic asylum, it did call on the UK government to recognize the “need for international protection vis-a-vis the USA” in relation to the whistleblower’s case. Amnesty has joined several other humanitarian organizations by backing Assange and denouncing any extradition attempt. These include the UN Human Rights office, Human Rights Watch, and the Inter-American Court of Human Rights.

How cheap money saved and doomed the world at the same time.

• The Latest Incarnation of Capitalism (Jacobin)

Financialization — “the increasing importance of financial markets, financial motives, financial institutions, and financial elites in the operation of the economy” — is a process that began in the 1980s with the removal of barriers to capital mobility. Global capital flows rose from about 5 percent of world GDP in the mid-1990s to about 20 percent in 2007. This is about three times faster than world trade flows. Increases in capital mobility helped facilitate the emergence of large imbalances between creditor countries with large current account surpluses and debtors with large current account deficits. According to textbook economic theory, these imbalances should be self-correcting.

When a country runs a deficit, currency is flowing out of the country. If this currency does not return in the form of capital inflows, the resulting increase in supply will exert downward pressure on the currency. A less valuable currency makes your exports cheaper to international consumers and should therefore increase demand for those exports. Played out over the scale of the global economy, this should lead to equilibrium. In the lead-up to the crisis, the fact that this equilibrium was not forthcoming puzzled some economists. Deficit countries should have been experiencing large currency depreciations, given the size of their current account deficits. These depreciations should, in turn, then have increased the competitiveness of their goods.

Ben Bernanke, then chairman of the Fed, accused a number of emerging economies of “hoarding” savings to protect themselves from future crises, preventing the global economy from reaching equilibrium. In fact, deficit countries were able to maintain strong currencies because, even though there was relatively little demand for their goods, there was strong demand for their assets — particularly financial assets. The main reason for the high demand for UK and US assets was the financial deregulation undertaken by neoliberal governments in these states in the 1980s, which facilitated a dramatic expansion in the provision of private credit to individuals, businesses, and financial institutions.

In the UK, consumer debt — primarily composed of mortgage lending — reached 148 percent of household disposable incomes in 2008, the highest it has ever been. While UK banks’ lending to the non-financial economy rose 50 percent between 2005-8, their lending to other financial institutions rose by 260 percent. Capital from the rest of the world flowed into banks in the UK and the US, which were generating significant returns from this lending.

Google shapes are thought and we have no idea.

• What’s The Biggest Influence On The Way We Think? (G.)

Google search is in a different league from earlier tools, and so the consequences of being dependent on it are more serious and far-reaching – for two inter-related reasons. The first is that it can influence what you think you know and shape the way you think because it knows more about you than you realise. And secondly, it’s not a passive tool that you own and control, but the property of a huge corporation that has acquired strange – and in some ways unprecedented – powers. Ten years ago, Nicholas Carr published a striking article – “Is Google Making Us Stupid?” – in the Atlantic. The title was misleading because the thrust of the piece was actually about how the internet might be messing with our brains, and in that sense Carr was using Google as a proxy for the technology in general.

Which is a pity because there are plenty of important questions to be asked about Google’s impact on the way we think. Its search results, for example, are heavily influenced by how many websites it finds that are supposedly relevant to a query. Sometimes, that’s fine. But sometimes it’s toxic – yet many people think it provides the “truth”. And because people’s search queries can sometimes be very revealing, the company knows more about people’s innermost secrets, fears and fantasies than even their friends or partners. We ask Google questions that we would not breathe to any living soul.

So Google, as philosopher Benjamin Curtis points out, is anything but a passive cognitive tool. Its current offerings, boosted by machine learning algorithms, are increasingly suggestive. Its Maps not only provide navigational help but give us “personalised location suggestions that it thinks will interest us”. Gmail makes helpful suggestions about what to type in a reply and Google News highlights stories that it believes we will find interesting. “All of this,” says Curtis, “removes the very need to think and make decisions for ourselves.” It “fills gaps in our cognitive processes, and so fills gaps in our minds”.

In two short decades, therefore, Google has gone from being a geeky delight to something that influences the way we think. All of which brings to mind something that John Culkin, a buddy of Marshall McLuhan, said many years ago: “We shape our tools and then our tools shape us.” Amen to that. And you can Google him to check the quote.