DPC Pere Marquette transfer boat 18 passing State Street bridge Chicago River 1901

On our way to $20 and beyond.

• Oil Falls 3% On Surplus Worries, As US Drops Toward $27 (Reuters)

Crude futures slumped again in Asian trade on Wednesday, with U.S. oil droppping more than 3% toward $27 a barrel and its lowest since 2003, on worries about global oversupply. That came after the International Energy Agency, which advises industrialized countries on energy policy, warned that oil markets could “drown in oversupply” in 2016. The crash hammered Asian stock markets with MSCI’s broadest index of Asia-Pacific equities outside Japan falling 2.8% to a four-year low. “Oil prices are at a level where OPEC countries are all struggling. They are selling oil for cashflow not for profit,” said Jonathan Barratt at Sydney’s Ayers Alliance. “U.S. producers are holding out, but I think they’re bleeding as well,” he said.

U.S. crude futures were trading down 97 cents at $27.49 a barrel, or 3.4%, at 0625 GMT, the lowest since September 2003. The contract settled down 96 cents, or 3.26%, the session before. The expiry of the February contract on Wednesday was “probably” adding further downward pressure on U.S. West Texas Intermediate oil as traders closed positions, said Michael McCarthy at Sydney’s CMC Markets. Brent futures dropped 61 cents to $28.15 a barrel, or 2.1%, not far from the 12-year low hit on Monday. It settled up 21 cents, or 0.7 per cent, in the previous session. McCarthy said the market had already taken into account the 500,000 barrels per day Iran has forecast it will add to global production. “(Iran) is really another strike in the same beating the market has taken,” McCarthy said.

Profit? You mean creative accounting.

• Shell Q4 Profit Plunges 50% as Oil’s Slump Deepens (BBG)

Royal Dutch Shell said fourth-quarter profit plunged as the rout in crude prices deepened. The company sees profit adjusted for one-time items and inventory changes of $1.6 billion to $1.9 billion, Shell said Wednesday in a preliminary earnings statement. That compares with the $1.8 billion average estimate of nine analysts surveyed by Bloomberg, and profit of $3.3 billion a year earlier. Shell, which is buying BG Group in the industry’s largest deal in a decade, has cut jobs and reduced spending as CEO Ben Van Beurden prepares for a prolonged downturn. Crude’s slump below $30 a barrel has driven down Shell’s market value to the lowest in almost seven years and prompted concern it may be overpaying for BG’s production and cash flow.

The average price of Brent crude, the international benchmark, fell 42% in the quarter from a year earlier to $44.69 a barrel, the lowest since 2009. Aberdeen Asset Management and Invesco Asset Management, two of Shell’s major shareholders, have said they will support the company’s plan to buy BG even with crude’s collapse. The acquisition allows Shell to accelerate the reshaping of its portfolio toward deepwater assets and natural gas and BG’s production is likely to grow strongly in the next three to five years, Invesco fund manager Martin Walker said. Standard Life Investments is the only Shell holder that has so far publicly said it will vote against the combination because the acquisition is “value destructive.”

Shell has justified the deal by saying it boosts its ability to maintain dividends, makes it the world’s biggest liquefied natural gas company and gives it oil and gas assets from Australia to Brazil. The company’s B shares, the class of stock used in the deal, have dropped 11% this year, extending last year’s 31% decline. Shell’s shareholders are scheduled to vote on the acquisition on Jan. 27 and BG’s the next day. Shell requires the backing of 50% of its holders. In BG’s case, votes in favor must represent at least 75% of the total value of the company’s shares. The merger will probably become effective Feb. 15, Shell said.

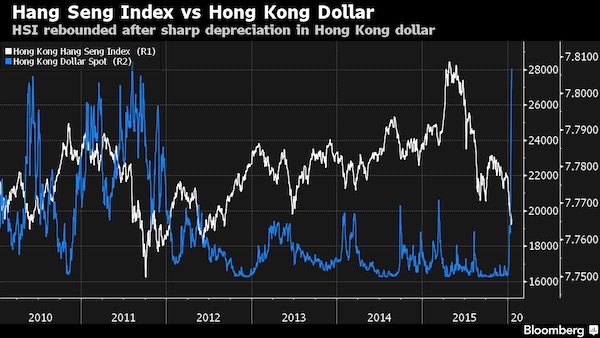

Hong Kong is fast becoming the eye of the storm.

• Chinese Stocks in Hong Kong Fall to Global Financial Crisis Lows (BBG)

Chinese stocks in Hong Kong tumbled to the lowest level since the depths of the global financial crisis as a slide in the city’s dollar spurred concerns over capital outflows. Oil producers and property developers led declines. The Hang Seng China Enterprises Index plunged as much as 5.5% before paring losses to trade 4% lower at 1:57 p.m. in Hong Kong. PetroChina fell to a 11-year low as oil extended its decline and Cnooc, China’s largest offshore oil company, said it will cut output for the first time in more than a decade. Hong Kong’s dollar traded near its weakest level since 2007 as concern about China’s slowing economy curbs demand for the city’s assets. The Shanghai Composite Index lost 0.8%.

“The local dollar’s slide is igniting concerns that capital outflows are accelerating as funds are selling equities en masse,” said Castor Pang at Core-Pacific Yamaichi Hong Kong. “Overall sentiment is very bad in Hong Kong.” The so-called H-shares gauge slid to 8,043.47, heading for the lowest level since March 2009. The index has slumped 17% this year, joining China’s Shanghai Composite as the world’s worst-performing major global benchmark measure out of the 93 tracked by Bloomberg. Similar to their mainland counterparts, Hong Kong policy makers are fighting to prevent a vicious cycle of capital outflows and a weakening currency with the resulting financial-market volatility heightening concern that China’s deepest economic slowdown since 1990 will worsen. PetroChina and China Petroleum & Chemical tumbled at least 6.2% in Hong Kong.

Oil extended its decline from the lowest close in more than 12 years, while Cnooc’s output cut increased speculation the nation’s producers are succumbing to the global price war. Cnooc’s acknowledgment that spending cuts are hurting production may be a prelude to further reductions by Chinese explorers, according to Nomura. The stock dropped 6%. Hong Kong’s Hang Seng Index tumbled 3.7% to a three-year low as trading volumes surged 77% above the 30-day average for this time of day. Property developers led declines, with Cheung Kong Property Holdings Ltd. sliding 6.1% to a record low. “To protect the Hong Kong dollar peg the government has to raise the interest rate,” said Louis Tse, a Hong Kong-based director at VC Brokerage Ltd. “The property companies are high-beta stocks because you have to borrow during the development phase,” with higher borrowing costs potentially weighing on home owners as well.

And Europe follows as we speak.

• Nikkei, Hang Seng Lead Slump In Asian Markets (CNBC)

Asian stocks tumbled Wednesday, with major indexes declining by more than 1% each, as global sentiment remained low on concerns over economic growth, China and low oil prices. “The frailty in the Chinese growth remain the core problem for investors and the spotlights are not moving away from it anytime soon,” Naeem Aslam, chief market analyst at AvaTrade, said in a note Wednesday. Overnight, the IMF cut its global growth forecast for 2016 to 3.4%, from 3.6%. The organization cited slower growth in emerging markets, especially in China, falling commodity prices, and rising interest rates in the U.S. as potential risks to global growth. Markets in China opened in negative territory, following a 3.5% gain in the previous session after Beijing released a slew of data including the full-year growth number for 2015.

The Shanghai composite was down 1.15% and the Shenzhen composite declined by 1.10%. The CSI300 was down 1.64%. Hong Kong’s Hang Seng index was down 3.77%. The Chinese economy grew by 6.9% in 2015, according to official data, down from 2014’s 7.3%, and the slowest pace of economic expansion since 1990. Some analysts believe further intervention and economic stimulus from Beijing are forthcoming as the country juggles a structural re-balancing act. Cynthia Kalasopatan from Mizuho Bank said in a morning note, “Soft growth momentum led to expectations that Chinese authorities will need to implement further policy easing to support the economy. “More policy and RRR cuts may be in the pipeline,” she added, “What’s more, targeted fiscal tools may be used as well to spur growth.”

The People’s Bank of China (PBOC) said late on Tuesday it would inject more than 600 billion yuan ($91.22 billion) into the financial system to help ease a liquidity squeeze expected before the Lunar New Year holiday in early February. [..] bank and property shares were sharply lower. Bank of China’s Hong Kong-listed shares dropped 1.97% and its Shanghai-listed ones fell 1.70%. Hong Kong-listed Shimao Property dropped 6.02%.

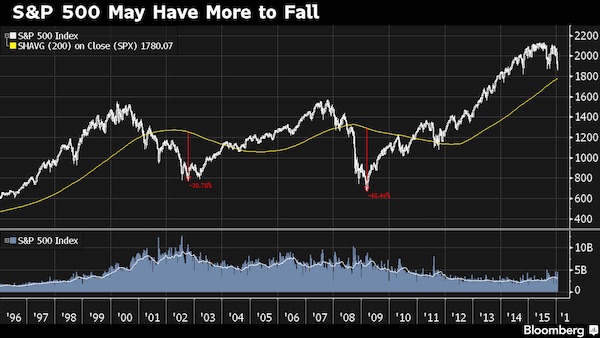

The shape of things to come.

• Recent S&P 500 Correction Appears Small in Context of History (BBG)

The recent 10% drop in U.S. stocks looks very small when considered in the context of the 220% rally from the 2009 nadir to the 2015 peak. The Standard & Poor’s 500 Index remains more than 5% above its 200-week moving average, and has not spent this long continuously above it since the 1990s dot-com era. When that bull run finished, the market fell to 38% below the 200-week moving average, while the 2009 crash bottomed out 48% below it.

“The European banking system may have to be recapitalized on a scale yet unimagined, and new “bail-in” rules mean that any deposit holder above the guarantee of €100,000 will have to help pay for it.”

• World Faces Wave Of Epic Debt Defaults: Central Bank Veteran (AEP)

The global financial system has become dangerously unstable and faces an avalanche of bankruptcies that will test social and political stability, a leading monetary theorist has warned. “The situation is worse than it was in 2007. Our macroeconomic ammunition to fight downturns is essentially all used up,” said William White, the Swiss-based chairman of the OECD’s review committee and former chief economist of the Bank for International Settlements (BIS). “Debts have continued to build up over the last eight years and they have reached such levels in every part of the world that they have become a potent cause for mischief,” he said. “It will become obvious in the next recession that many of these debts will never be serviced or repaid, and this will be uncomfortable for a lot of people who think they own assets that are worth something,” he said in Davos.

“The only question is whether we are able to look reality in the eye and face what is coming in an orderly fashion, or whether it will be disorderly. Debt jubilees have been going on for 5,000 years, as far back as the Sumerians.” The next task awaiting the global authorities is how to manage debt write-offs – and therefore a massive reordering of winners and losers in society – without setting off a political storm. Mr White said Europe’s creditors are likely to face some of the biggest haircuts. European banks have already admitted to $1 trillion of non-performing loans: they are heavily exposed to emerging markets and are almost certainly rolling over further bad debts that have never been disclosed. The European banking system may have to be recapitalized on a scale yet unimagined, and new “bail-in” rules mean that any deposit holder above the guarantee of €100,000 will have to help pay for it.

The warnings have special resonance since Mr White was one of the very few voices in the central banking fraternity who stated loudly and clearly between 2005 and 2008 that Western finance was riding for a fall, and that the global economy was susceptible to a violent crisis. Mr White said stimulus from quantitative easing and zero rates by the big central banks after the Lehman crisis leaked out across east Asia and emerging markets, stoking credit bubbles and a surge in dollar borrowing that was hard to control in a world of free capital flows. The result is that these countries have now been drawn into the morass as well. Combined public and private debt has surged to all-time highs to 185pc of GDP in emerging markets and to 265pc of GDP in the OECD club, both up by 35 %age points since the top of the last credit cycle in 2007. “Emerging markets were part of the solution after the Lehman crisis. Now they are part of the problem too,” Mr White said.

[..] In retrospect, central banks should have let the benign deflation of this (temporary) phase of globalisation run its course. By stoking debt bubbles, they have instead incubated what may prove to be a more malign variant, a classic 1930s-style “Fisherite” debt-deflation. Mr White said the Fed is now in a horrible quandary as it tries to extract itself from QE and right the ship again. “It is a debt trap. Things are so bad that there is no right answer. If they raise rates it’ll be nasty. If they don’t raise rates, it just makes matters worse,” he said. There is no easy way out of this tangle. But Mr White said it would be a good start for governments to stop depending on central banks to do their dirty work. They should return to fiscal primacy – call it Keynesian, if you wish – and launch an investment blitz on infrastructure that pays for itself through higher growth.

Don’t think they’d do it in one go. But who knows, it might be the way to go.

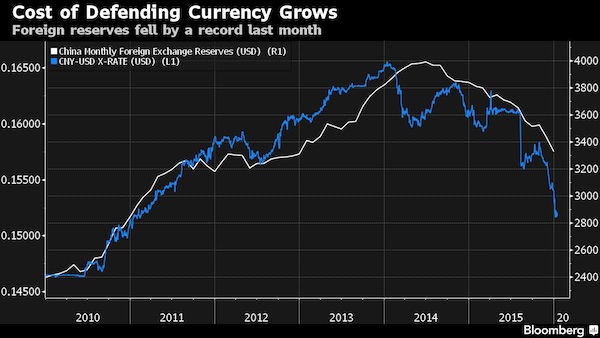

• Hedge Fund That Called Subprime Crisis Urges China To Devalue Yuan By 50% (BBG)

Mark Hart, the hedge fund manager whose bets against U.S. subprime mortgages and European sovereign debt proved prescient, said China should weaken its currency by more than 50% this year. A one-off devaluation would allow policy makers to “draw a line in the sand” at a more appropriate level for the yuan, easing pressure on China’s foreign-exchange reserves and removing an incentive for capital outflows, according to Hart, who’s been betting against the currency since at least 2011. China should devalue before its $3.3 trillion hoard of reserves shrinks much further, he said, because the country can still convince markets it’s acting from a position of strength. “There wouldn’t be anything underhanded about a sharp devaluation,” Hart said. “Why should China be forced to suffer deflationary effects of defending its currency when everyone else isn’t?”

Hart, whose prescription clashes with consensus forecasts for the yuan and recent comments from senior government officials, said China would be justified in weakening the currency after central banks in Europe and Japan fueled declines in their exchange rates to stoke economic growth in recent years. Such a move would likely come as a surprise to global investors, who were rattled by a drop of less than 3% in the yuan last August. China’s current approach to managing the currency’s decline has been costly. Foreign-exchange reserves dropped by a record $513 billion last year as the central bank intervened to ease the currency’s slide, while an estimated $843 billion of capital flowed out of China in the 11 months through November as some investors sought to get in front of further yuan weakness.

Aside from intervention, policy makers have moved to curb bearish bets against the yuan and tighten restrictions on the flow of money across the country’s borders. Those measures have fueled doubts among global investors about the ruling Communist Party’s commitment to give markets a central role in the world’s second-largest economy and make the yuan an international currency. “They’re trying to drive a car with one foot on the brake,” said Hart, who estimates the People’s Bank of China spent more than $100 billion supporting the yuan in onshore and offshore markets during the first 12 days of January. “If China were to devalue to a level that wasn’t actually a true equilibrium they will get run over pretty quickly, they will blow through FX reserves, and then they will lose face because they’ll be forced to devalue.”

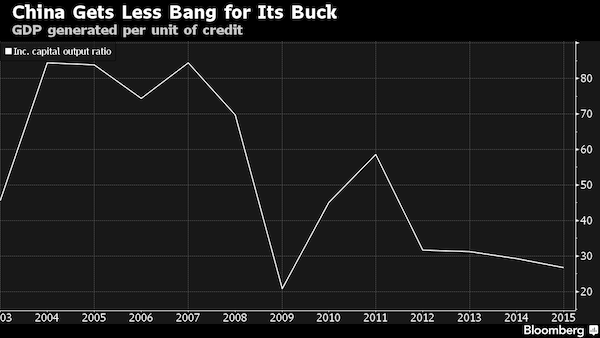

Omen.

• China Is Getting Less and Less Bang for Its Credit Buck (BBG)

Behind the numbers showing China’s continued slowdown at the end of last year lies a warning for Communist Party leaders who have been equally determined to embrace economic change and to ensure a rapid pace of growth. The flashing yellow light: there’s less and less power behind policy makers’ stimulus. For each $1 in credit expansion, China added the equivalent of 27 cents of GDP last year, the least since 2009, according to data compiled by Bloomberg from government figures released Tuesday. As recently as 2011, each $1 generated 59 cents.

The diminishing mileage for credit raises a conundrum for President Xi Jinping and his premier, Li Keqiang, of whether to let China slow further as they shut down surplus smokestack industrial capacity, or keep pumping liquidity. It also highlights the importance of financial-industry reforms – another ball the leadership is juggling. “This will require rolling back preferences that tilt, and trap, the flow of investment in inefficient state enterprises,” said David Loevinger, a former China specialist at the U.S. Treasury and now an analyst at fund manager TCW in Los Angeles. “This is always challenging because the companies that stand to lose are big and powerful and the companies that stand to win are small and may not even yet exist.”

Martin Wolf noticed the omen too: “..the “incremental capital output ratio” — the amount of capital needed to generate additional income — has roughly doubled since the early 2000s.”

• China Needs a Great Economic Shift Away From Debt Fueled ‘Growth’ (Wolf)

Chinese policymakers have a stellar reputation for the quality of economic management but the same was true of the Japanese three decades ago. For the Japanese, the difficulty of shifting from their high-savings, high-investment, catch-up economic model proved very large. Indeed, this has still not been completed. While the Chinese economy has far more room to grow than Japan a quarter of a century ago, its disequilibria are even bigger. Moreover, contrary to conventional wisdom, the transition to a new pattern of growth has not really begun. Already, the difficulty of handling this transition is damaging Chinese policymakers reputation. Mistakes in handling the implosion of the bubble economy of the 1980s did the damage in Japan. Now it is the Chinese authorities mishandling of the currency and the stock market.

Similarly, the financial crisis of 2007 and 2008 devastated the reputation of western financiers and policymakers. Everybody seems to be a genius when credit is surging. Understandably and rightly, observers are calling upon the Chinese authorities to be more transparent. Given their political system -‘the bureaucrat knows best’- that is going to be hard to do, but this is a second-order matter. The first-order one is that it is unclear how and whether the transition to a more balanced economy is to be made. Again, some people focus on the transition from manufacturing to services. This does seem to be going quite well: according to Chinese data, industry grew at an annual rate of just 6% in the first three quarters of 2015, while services grew 8.4%. However, a large part of this apparent success is due to growth of income from financial services.

Just as was the case in the west, before the crisis, this is as much a symptom of credit growth as of a transition to a more balanced ‘new normal’. The fundamental indicators of a change in the shape of the economy would be a fall in savings and investment and a rise in consumption. Such a shift is necessary not only because much of the investment is wasted, but because it is associated with an explosive rise in debt. China has today a far higher share of investment in GDP than other high-growth east Asian economies ever had. Furthermore, according to the McKinsey Global Institute, overall indebtedness is extremely high with a concentration in non-financial corporations. It is higher than in the US, for example.

In response to the 2008 financial crisis, China promoted a huge rise in debt-fuelled investment to offset the weakening in external demand. But underlying growth in the economy was slowing. As a result, the “incremental capital output ratio” — the amount of capital needed to generate additional income — has roughly doubled since the early 2000s. China’s overall capital-output ratio is also very high and rising. At the margin, much of this investment is likely to be lossmaking. If so, the debt associated with it will also be unsound. But, if wasteful investment were slashed, the economy would go into recession.

From debt to deflation, a natural course.

• China Data Indicate Heavy Deflationary Pressure (Nikkei)

Excess manufacturing capacity, rising real estate inventories and volatile financial markets weigh on China’s economy as the government tries to engineer a soft landing, with data for 2015 suggesting that deflation may loom. China’s real GDP growth slipped to 6.9% last year, the lowest in a quarter century. Real growth had not dropped below 7% since 1990, when international sanctions were imposed in response to the 1989 Tiananmen Square crackdown. Nominal growth, based on official GDP figures, totaled 6.4%, falling below real growth for the first time since 2009. Nominal growth that is slower than real growth indicates heavy deflationary pressure. Severe overcapacity in major manufacturing industries is one cause. China’s steel industry has 400 million tons of excess capacity.

Exports came to 100 million tons in 2015, on par with Japan’s annual output. With supply outstripping demand, wholesale prices sank 5.2% in 2015, 3.3%age points faster than in 2014. Companies are shouldering heavier real debt-repayment burdens despite repeated interest rate cuts by the People’s Bank of China. Production is depressed, with crude steel, cement and sheet glass output dropping in 2015. Electricity use, a more accurate gauge of economic conditions, slid 0.2%. Mounting real estate inventories are another drag on the economy. Inventories soared nearly 50% in two years to 718.53 million sq. meters at the end of 2015. Housing activity has been sluggish for some time in many outlying cities.

Office building vacancy rates have reached about 40% in the inland cities of Chongqing and Chengdu, a developer said. With little new investment coming in, spending on property development edged up 1% in 2015 – just one-tenth the growth seen in 2014. Turmoil in financial markets compounds the country’s problem. The slide in Chinese stocks since the start of the year could dampen brisk consumer spending. Services accounted for half of GDP in 2015, with the finance industry contributing significantly amid a rise in stock trading. If retail investors flee the market, growth could drop accordingly.

“It doesn’t take a rocket scientist to figure out the growth in old China for the past year or so has been somewhere around zero — it’s nothing like 6.8%..”

• What Is China’s Actual GDP? (CNBC)

China announced Tuesday that its economy notched 6.9% growth in 2015 — down from the prior year, but perfectly matching expectations. And yet commentary from around the world suggests almost no outside investor or economist believes Beijing’s figures. Although there has never been definitive evidence that Chinese economic data is exaggerated, the widely-held theory says that China’s National Bureau of Statistics will overstate growth in a stability-minded effort to hide the truth about a slowing economy. So instead of relying on government reports, China-watchers analyze other metrics for a more complete picture of the country’s GDP. “Nobody knows for sure, but when we look at things that are harder numbers to fudge…our estimate is growth probably about 3.5% versus roughly 7,” said A. Gary Shilling.

“We watch (the official GDP announcement) as closely as we do in some sense out of a sense of obligation,” said Donald Straszheim, head of China Research at Evercore ISI. “I wasn’t expecting to learn a great deal last night when these numbers came out.” Not only does China’s NBS refuse to respond to inquiries, Straszheim said, but the statistics unit will announce only its total GDP growth figure — not the components of that number. “If you don’t have the components, how can you have a total? And if you have the components, which would add to the total, why are they not publicly available?” Straszheim asked. [..] For his part, Shilling said his firm models China’s possible GDP growth on measures of rail traffic, electricity consumption, coal consumption and debt.

Billionaire distressed asset investor Wilbur Ross, meanwhile, sees China’s actual growth at about 4% on a similar basket of metrics. The “reason is that if you look at physical indicators — rail car loadings, truck loadings, cement consumption, steel consumption, exports, natural gas consumption, electricity consumption — none of those are consistent with 6.8 or 6.9,” he explained. Straszheim said his group uses data from sources it regards as largely independent from government pressure, pointing to commodity consumption among other measures. But most of these indicators seek to measure the share of China’s economy based on exporting, manufacturing, and capital investment — and Beijing has made no secret that it sees the country shifting toward an increasingly service-oriented economy.

That could, in turn, potentially make it even harder for investors to know the truth about China’s GDP. “It doesn’t take a rocket scientist to figure out the growth in old China for the past year or so has been somewhere around zero — it’s nothing like 6.8%,” Straszheim said, explaining that the “new” China of services and consumer spending is tough to measure in the absence of robust data from the private sector. [..] Derek Scissors, a scholar for the American Enterprise Institute, pointed out that China’s own official numbers seem to contradict one another. For example, China’s Xinhua reported that November railways cargo fell 15.6% year on year, but the state statistics office said industrial production through the year was up 6.1%. “What? Did they just produce the goods and leave them on the factory floor and they never went anywhere?” Scissors asked.

Putting on the brave face mask.

• Mining Giant BHP Billiton Lowers Forecast, Investors Fear Dividend Cut (WSJ)

BHP Billiton said it is committed to protecting its balance sheet amid a sharp downturn in world commodity markets, as expectations build about the miner preparing to cut its dividend. The Anglo-Australian mining giant has faced growing speculation it may have to cut its payout by as much as half this year as it grapples with plunging resources prices and the fallout from one of its worst mining disasters, a deadly dam burst at a mine operated by Samarco Mineração SA, a 50-50 joint venture with Brazil’s Vale SA. Last week, BHP also announced its largest write-down ever, a roughly US$7.2 billion pretax charge against its U.S. onshore energy assets as oil prices slumped below US$30 a barrel for the first time in more than 10 years.

Only 18 months ago, the market was speculating about the possibility of a major share repurchase by the company to reward investors. Now, even maintaining its dividend, a US$6.6 billion annual burden on its balance sheet, appears a stretch. Cutting investor payouts is a measure big companies are loath to take, for fear of alienating important shareholders. It is particularly difficult when options for growth are limited. “We continue to cut costs and remain focused on safely improving our operational performance to enhance the resilience of our business,” Chief Executive Andrew Mackenzie said Wednesday. “In this environment, we are also committed to protecting our strong balance sheet so we have the financial flexibility to manage further volatility and take advantage of the expected recovery in copper and oil over the medium term,” he added.

In August, BHP recorded its worst annual earnings result since 2003. Slackening demand from China, as miners ramp up production from mines planned when prices were booming, has hit prices of nearly every commodity, including coal, iron ore, oil and copper, which are BHP’s core products. BHP’s share price has since slumped to its lowest level in more than a decade. That’s been exacerbated by uncertainty over the Samarco disaster. [..] the Nov. 5 incident killed at least 17 people and triggered a criminal investigation and roughly US$5 billion civil lawsuit by authorities. On Wednesday, it also led BHP to pare its projection for global iron-ore production in the year through June, to 237 million metric tons from an earlier forecast of 247 million. Investors have urged BHP to clear the air on its plans for future dividends. They say uncertainty over the outlook has been a key driver in sending the miner’s share price sharply lower.

Well, to be fair, this IS the crisis era.

• Fed’s $216 Billion Treasuries Rollover Recalls Crisis Era Buying (BBG)

If you were under the impression that the Federal Reserve was done buying Treasuries, think again. While the central bank won’t be expanding its balance sheet, about $216 billion of Treasuries in its portfolio mature in 2016, up from negligible amounts the past few years. Last week, New York Fed President William C. Dudley reiterated policy makers’ plan to keep reinvesting the proceeds for the time being, giving bondholders and Wall Street dealers reason to cheer. The Fed is the biggest holder of the government’s debt. Its $2.5 trillion hoard, amassed in a bid to support the economy after the financial crisis, is more of a focus for some investors than the trajectory of interest rates. From this month through 2019, about $1.1 trillion of Treasuries in the portfolio are set to mature.

For bond bulls, the Fed’s signals that it will roll over the obligations have been another reason to doubt the consensus forecast that yields will rise in 2016. If officials had chosen to stop funneling that money into new debt, the government would likely have to boost borrowing by roughly an equivalent amount this year, potentially pushing up Treasury yields. “The Fed tightening gave us little worry, but the unwind of the balance sheet gives us major worries,” said Mark MacQueen, co-founder of Sage Advisory Services. “The Fed is keenly aware that the balance sheet has a much greater impact on the overall yield levels in the markets going forward than raising rates.”

Officials anticipate keeping the holdings stable until the normalization of interest rates is “well under way,” though there’s no specific level for the Fed’s target at which reinvestment would end, Dudley said in prepared remarks of a speech Jan. 15. That ensures the legacy of the Fed’s quantitative-easing programs, which boosted its Treasuries holdings from less than $500 billion in 2009, will extend even further into the future. As officials roll maturing issues into new debt, that swells the amount coming due later in the decade.

As in: bring them out into the open. Problem is, that’s the death knell for many banks.

• ECB Plans To Order Banks To Tackle Bad Loans (Reuters)

The ECB plans to tell euro zone banks how to better manage bad loans, banking officials said on Tuesday, in an effort to resolve an issue that is curbing the region’s economic recovery. Bad loans have more than doubled across the euro zone since 2009 and stood at nearly a €1 trillion at the end of 2014, the IMF said last year. Those loans burden banks and make it harder for them to lend. The ECB has asked a number of banks across the euro zone, including Italy’s Monte dei Paschi di Siena and UniCredit, about their non-performing loans. They were selected to establish a representative sample, not necessarily because they are particularly affected, the sources said. Italian bank shares have tumbled in recent days on fears the ECB had singled out some banks because of their vulnerabilities.

But the banking sources said all types of banks across the continent were included in the sample. The request for information is the first step in a process that will see the ECB define best practices on how to deal with bad loans, encompassing banks with different business models in different jurisdictions. Those guidelines will eventually be used by the ECB’s supervisory teams when formulating recommendations for the banks on their watch. The recommendations might range from hiring more staff to deal with non-performing loans or changing internal practices, to making more provisions, reviewing the value of soured loans or even creating a bad bank. An ECB spokesman said the request for information was “standard supervisory practice”. A bad loan is typically one that is more than 90-days overdue.

“I carry a great responsibility,” he said. “I would do a lot of things differently.”

What really happened was Varoukais couldn’t guarantee Plan X would work, and Tsipras then said it would be too great a responsibility to implement it.

• Varoufakis Speaks About 2015 Greece Parallel Currency Plan (Kath.)

Yanis Varoufakis was instructed last year by Prime Minister Alexis Tsipras to put together a small team of people to draw up a plan for introducing a parallel currency if Greece was unable to reach an agreement with its lenders on a new bailout, the ex-finance minister said in a TV interview late Tuesday. Speaking on Skai TV’s “Istories” (Stories) program, Varoufakis outlined what was known as Plan X. He said that a small team of about six people examined the various parameters surrounding a potential standoff that would lead to Greece being unable to meet its obligations. Among the issues examined by Varoufakis and his advisers were how the country would continue to have access to medicines, fuel and food under such circumstances.

Varoufakis said that he advised Tsipras to put the plan, which would see Greece defaulting on 27 billion euros in Greek government bonds held by the European Central Bank, into action as soon as he called a referendum at the end of June. “I thought that if we did what we had decided as a negotiating team… and announced that we would restructure these bonds and implement the parallel payment system, then by the Monday, Tuesday or Wednesday before the referendum the discussion we expected between [ECB president Mario] Draghi and [German Chancellor Angela] Merkel would take place,” he said. Varoufakis said that Tsipras considered adopting Plan X but that he was advised against it by Deputy Prime Minister Yiannis Dragasakis.

“The prime minister thought about it very carefully,” said the ex-minister. “I saw him puzzle over what he should do and in the end he decided to follow Dragasakis’s recommendation and not mine.” Varoufakis added that he was against efforts to secure funding from Russia but that there had been an agreement with China regarding investment in Greece, including in Greek bonds. “This agreement was overturned, though, with a phone call from Berlin,” he claimed. The outspoken economist said that he became frustrated with Tsipras when the prime minister agreed to a primary surplus target of 3.5% of GDP for the coming years, saying that he thought this goal was “macroeconomically impossible.” Tsipras told him that he agreed in return for receiving debt relief. “It’s true I don’t have a lot of hair but when I heard this I started pulling out what little I have left,” he said. Varoufakis admitted that he “failed” during his time in office. “I carry a great responsibility,” he said. “I would do a lot of things differently.”

He should chide Brussels, not Ankara.

• Greek Immigration Minister Slams Turkish Failure To Curb Refugee Flow (Kath.)

Immigration Policy Minister Yiannis Mouzalas on Tuesday criticized Turkey for failing to take any serious measures to cut the flow of migrants into Europe as Brussels called on Greece to complete construction of five “hot spots” on its territory. In an interview with Deutsche Welle, Mouzalas said Ankara’s failure to clamp down on human traffickers put an excess burden on the country’s shoulders. “Smuggling networks are still in full operation… The deportation of migrants who have traveled from Turkey is also a big problem,” Mouzalas said. Greek authorities had carried out 130 deportations in the past 15 days, he said, while some 30,000 people had arrived from Turkey over the same period.

The International Organization for Migration (IOM) confirmed Tuesday that 31,244 migrants and refugees had arrived in Greece by sea since the beginning of 2016, compared with just 1,472 recorded arrivals in January last year. Meanwhile the Greek minister rebuffed criticism that his government had turned down EU help to deal with the crisis. He said that although Athens had officially requested 1,800 staff from EU border agency Frontex, only 900 were dispatched to Greece. Mouzalas did acknowledge delays in completing the five hot spots for registering and processing migrants and refugees on the islands of Lesvos, Samos, Leros, Kos and Chios. Speaking to German newspaper Sueddeutsche Zeitung, European Union Migration Commissioner Dimitris Avramopoulos said Greece – and Italy – must set up hot spots within the next four weeks.

Big turnaround, big relief for Greece. But big problems elsewhere.

• EU To Scrap ‘First Country’ Asylum Claim Rule (FT)

Brussels is to scrap rules that make the first country a refugee enters responsible for any asylum claim, revolutionising the bloc’s migration policy and shifting the burden from its southern flank to its wealthier northern members. The “first-country” requirement is the linchpin of the EU refugee system. But it has become politically toxic for EU leaders as Germany and other states criticise frontier countries such as Greece and Italy for failing to register and shelter the 1.1m people that have poured into Europe from the Middle East and North Africa. The policy essentially broke down last year, when Germany waived its right to send hundreds of thousands of asylum-seekers back to other EU member states, but exhorted its reluctant partners to shoulder more responsibility.

The European Commission has concluded the rule – which is part of the Dublin regulation – is “outdated” and “unfair”, and will be scrapped in a proposal to be unveiled in March, according to officials briefed on its contents. The move could oblige some EU members such as Britain to take in many more refugees, since it would become harder to send them back to neighbouring countries. It could also increase the pressure on EU members to back a formal quota system and common asylum rights and procedures to spread the burden across the union. European Council president Donald Tusk on Tuesday warned that the EU had “no more than two months to get things under control” or face “grave consequences”.

Changing the rules on who is responsible for refugees when they arrive would mark a victory for Italian prime minister Matteo Renzi, who has repeatedly argued that the law is unfair and that other member states should do more to help with the refugee crisis. Replacing the “first country of entry” principle is likely to prove technically and politically tricky. Countries in northern Europe such as the UK are net beneficiaries from the status quo, able to transfer asylum-seekers back to other EU states quickly. Although the UK has an opt-out on EU migration policy, it has opted into the Dublin rules for this reason. In practice, the current rules have broken down.

Last autumn, German chancellor Angela Merkel controversially waived the country’s right to return Syrian refugees to the first country of entry, generating both praise and opprobrium from her peers – before reversing course and triggering months of chaotic border openings and closures across Europe. Transfers to Greece have been effectively banned since 2011 after the European Court of Human Rights declared that the country’s asylum system was unfit for purpose even before the recent influx.

Don’t just talk, call that emergency assembly.

• Children On Syrian Refugee Route Could Freeze To Death: UN (Reuters)

Thousands of refugee children traveling along the migration route through Turkey and southeastern Europe are at risk from a sustained spell of freezing weather in the next two weeks, the United Nations and aid agencies said on Tuesday. The U.N. weather agency said it forecast below-normal temperatures and heavy snowfall in the next two weeks in the eastern Balkan peninsula, Turkey, the eastern Mediterranean and Syria, Lebanon, Israel and Jordan. “Many children on the move do not have adequate clothing or access to the right nutrition,” said Christophe Boulierac, spokesman for the U.N. children’s agency UNICEF. Asked if children could freeze to death, he told a news briefing: “The risk is clearly very, very high.”

Children were coming ashore on the Greek island of Lesbos wearing only T-shirts and soaking wet after traveling on unseaworthy rubber dinghies, the charity Save the Children said in a statement. “Aid workers at the border reception center in Presevo say there is six inches of snow on the ground and children are arriving with blue lips, distressed and shaking from the cold,” it said. It said temperatures were forecast to drop to -20 degrees Celsius (-4°F) in Presevo in Serbia and -13 degrees (9°F) on the Greek border with Macedonia. Last year children accounted for a quarter of the one million migrants and refugees arriving across the Mediterranean in Europe, Boulierac said. The UN refugee agency UNHCR said a daily average of 1,708 people had arrived in Greece so far in January, just under half the December daily average of 3,508.

Well, obviously.

• Doctors Without Borders Says EU Worsens Refugee Crisis, Aids Smugglers (AP)

The aid group Doctors Without Borders said Tuesday attempts by various European Union nations to deter migrants have put thousands of people in danger and created more business for smugglers. In a report, it said border closures and tougher policing only encourage people seeking sanctuary or jobs to use other routes to get to Europe. MSF’s head of operations, Brice de le Vingne, said “policies of deterrence, along with their chaotic response to the humanitarian needs of those who flee, actively worsened the conditions of thousands of vulnerable men, women and children.” The group urged the EU to create more legal ways to come to Europe and allow asylum applications at the land border between Turkey and Greece.

More than 1 million migrants arrived in the EU last year, however they have not always been welcomed. Meanwhile, the EU’s top migration official says so-called “hotspots” should be up and running in Greece and Italy within a month in an effort to better control how migrants flow into the bloc and conduct early security checks on them. The hotspots are intended to register new arrivals, take fingerprints and other data, and perform background checks. Those with no chance of asylum would quickly be sent home, while others would be more evenly distributed among EU nations. Migration Commissioner Dimitris Avramopoulos was quoted by Germany’s Sueddeutsche Zeitung on Tuesday as saying he sees no immediate end to the flood of asylum seekers and that it’s critical to get hotspots running quickly.

And nobody’s preparing, all they talk about is fewer refugees, even zero.

• Rate Of Refugee Arrivals In Greece Dwarfs 2015 Pace (AFP)

Greece has seen 21 times more migrants arrive on its shores so far this month than in all of January 2015, the International Organization for Migration said Tuesday. Since the beginning of 2016, IOM said 31,244 migrants and refugees had arrived in Greece by sea, compared with just 1,472 recorded arrivals on the Greek islands in January last year. “This is a huge jump,” spokesman Itayi Viriri told reporters in Geneva, warning that it does not bode well for the rest of the year. “If the trend as it is now continues then certainly were looking at another record number,” he cautioned. In 2015, more than one million migrants and refugees made the perilous Mediterranean crossing to Europe – nearly half of them Syrians fleeing a civil war that has been raging for nearly five years.

Although the number of arrivals in Greece last year was initially small, by the end of the year the country alone saw well over 850,000 arrivals. The continued influx will likely add to the EUs dissatisfaction with Turkey, a hub for migrants seeking to reach Europe which has on occasion been criticised by its Western partners for not doing enough to limit the numbers crossing the Aegean Sea. Ankara and Brussels in November agreed a plan to stem the flow by providing Turkey with €3 billion of EU cash as well as political concessions for Turkish cooperation in tackling Europes worst refugee crisis since World War II. IOM said Tuesday that nearly 90% of those who have arrived in Greece so far this year are Syrians, Afghans and Iraqis. Most of them are not staying in Greece. IOM cited numbers from Greek police showing that nearly 31,000 migrants had crossed the border to Macedonia since the beginning of the month.

Time for us to leave.

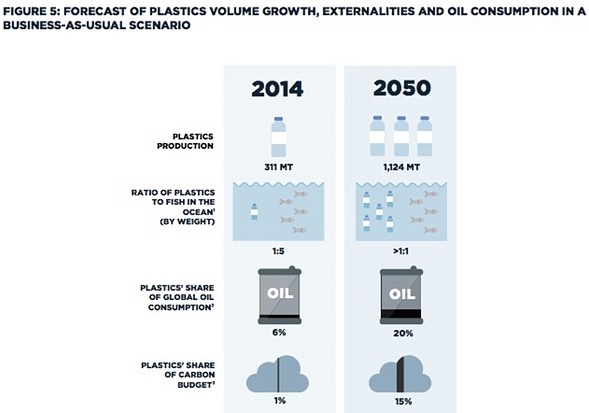

• More Plastic Than Fish In The Sea By 2050 (Guardian)

As a record-breaking sailor, Dame Ellen MacArthur has seen more of the world’s oceans than almost anyone else. Now she is warning that there will be more waste plastic in the sea than fish by 2050, unless the industry cleans up its act. According to a new Ellen MacArthur Foundation report launched at the World Economic Forum on Tuesday, new plastics will consume 20% of all oil production within 35 years, up from an estimated 5% today. Plastics production has increased twentyfold since 1964, reaching 311m tonnes in 2014, the report says. It is expected to double again in the next 20 years and almost quadruple by 2050. Despite the growing demand, just 5% of plastics are recycled effectively, while 40% end up in landfill and a third in fragile ecosystems such as the world’s oceans.

Much of the remainder is burned, generating energy, but causing more fossil fuels to be consumed in order to make new plastic bags, cups, tubs and consumer devices demanded by the economy. Decades of plastic production have already caused environmental problems. The report says that every year “at least 8m tonnes of plastics leak into the ocean – which is equivalent to dumping the contents of one garbage truck into the ocean every minute. If no action is taken, this is expected to increase to two per minute by 2030 and four per minute by 2050 “In a business-as-usual scenario, the ocean is expected to contain one tonne of plastic for every three tonnes of fish by 2025, and by 2050, more plastics than fish [by weight].”

Home › Forums › Debt Rattle January 20 2016